Portugal Heat Pump Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

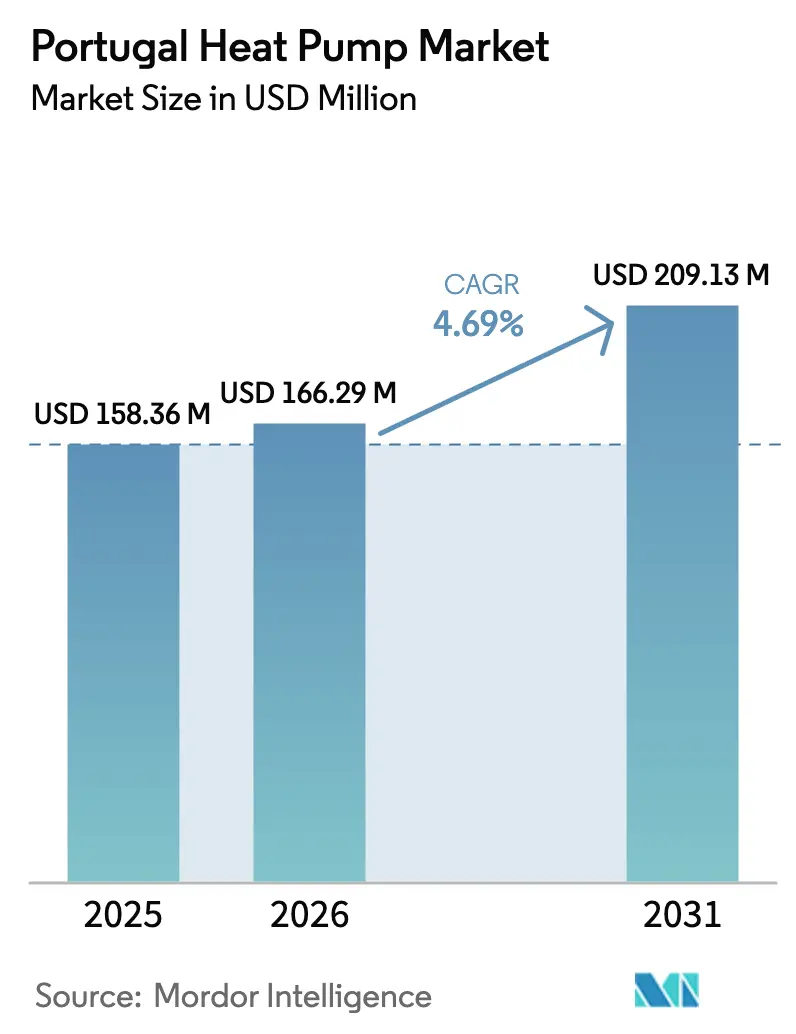

| Base Year Market Size (2025) | USD 158.36 Million |

| Market Size (2026) | USD 166.29 Million |

| Market Size (2031) | USD 209.13 Million |

| Growth Rate (2026 - 2031) | 4.69% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Portugal Heat Pump Market Analysis by Mordor Intelligence

The Portugal heat pump market size is projected to expand from USD 158.36 million in 2025 and USD 166.29 million in 2026 to USD 209.13 million by 2031, registering a 4.69% CAGR between 2026 to 2031. Surging renewable-electricity penetration, the EU-driven phase-out of fossil boilers, and the ability of heat pumps to shift loads toward low-price solar hours are reshaping demand profiles. The expiration of Portugal’s 6% value-added-tax concession in mid-2025 briefly raised system costs, yet installations remained resilient as building owners relied on forward carbon-pricing signals and grid-decarbonization targets to justify electrification. Commercial and industrial buyers now outpace households, with food, beverage, and hospitality operators seeking long-run operating-cost certainty ahead of the 2027 extension of the EU Emissions Trading System. Equipment vendors have responded with propane-based models, inverter-driven compressors, and modular architectures that shorten lead times and simplify staging, while policy makers emphasize green-loan programs to close residual capital gaps.

Key Report Takeaways

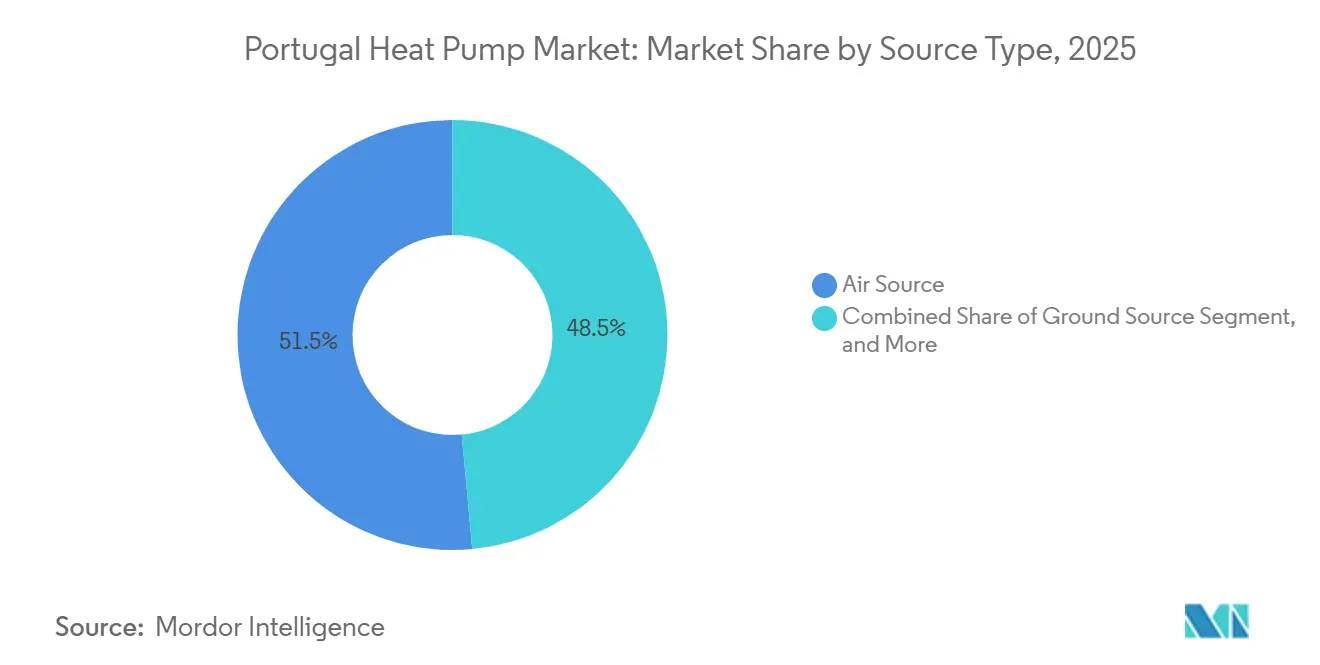

- By source Type, air-source systems captured 51.46% of 2025 revenue, while hybrid configurations are forecast to expand at a 5.61% CAGR through 2031.

- By technology, air-to-water technology accounted for 60.71% of 2025 sales and ground-to-water designs are projected to grow at 5.38% through 2031.

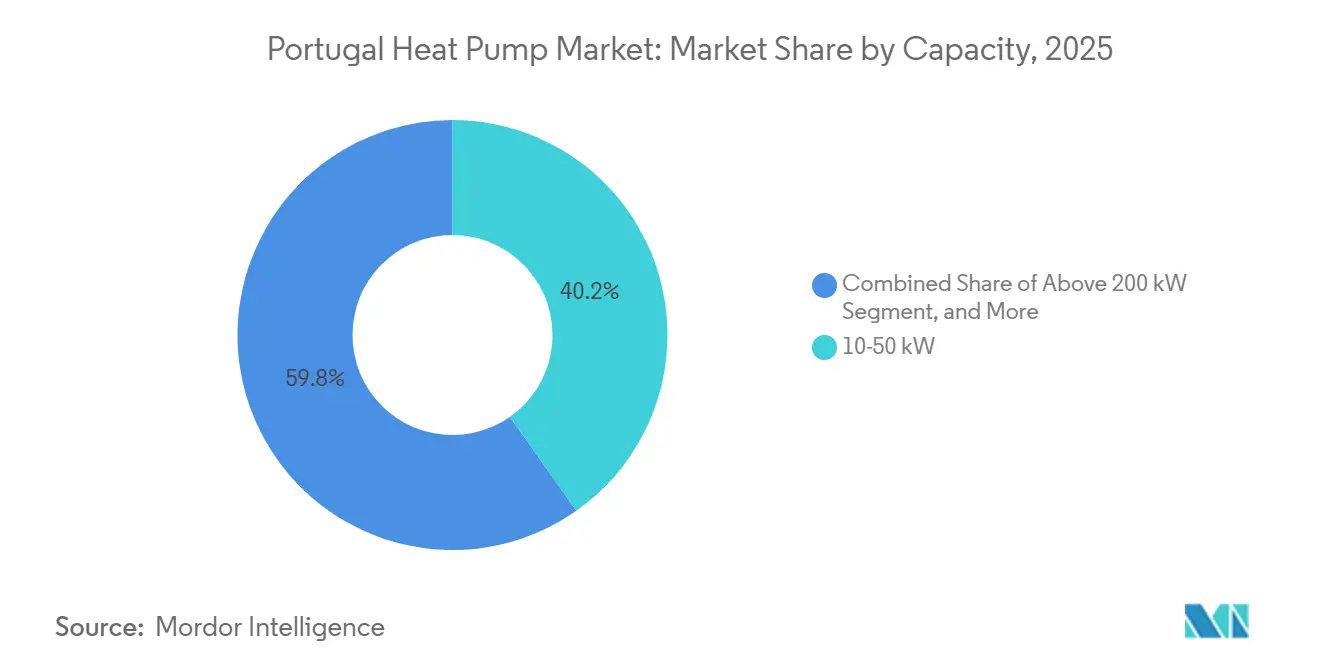

- By capacity, the 10-50 kW band held 40.23% of 2025 installations, whereas the 50-200 kW segment shows the fastest 5.14% CAGR to 2031.

- By application, domestic hot water led with 42.32% of 2025 revenue and industrial process heating is expected to rise at a 5.07% CAGR.

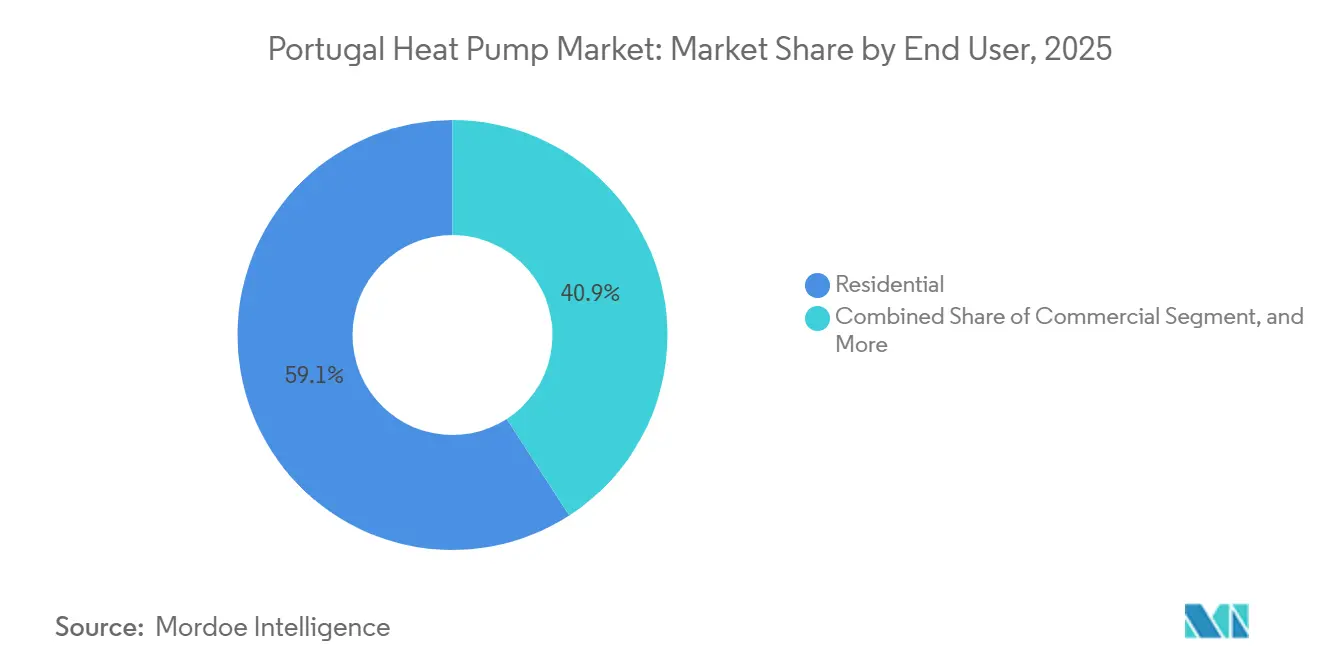

- By end-user, residential customers represented 59.14% of 2025 turnover, but industrial buyers are expanding at a 4.86% CAGR toward 2031.

- By installation type, retrofit work commanded 53.47% of 2025 spending and new-build installations are advancing at a 4.92% CAGR as developers pre-wire projects for heat pumps.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Portugal Heat Pump Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Extension of 0% VAT on Heat Pumps Through 2027 | +1.2% | National, stronger price elasticity in Lisbon, Porto, Braga | Short term (≤ 2 years) |

| EU-level Ban on Stand-Alone Fossil-Fuel Boilers from 2029 | +0.9% | National, aligned with EPBD deadlines | Medium term (2-4 years) |

| Surge in Cooling-Degree Days Driving Reversible Models | +0.7% | Algarve, Lisbon, Setúbal coastal zones; interior Alentejo spillover | Medium term (2-4 years) |

| Net-Metering Reforms Encouraging Solar-Heat Pump Hybrids | +0.6% | National, early uptake in Guimarães, Loulé, Évora | Long term (≥ 4 years) |

| Rapid Roll-Out of “Mais Sustentável Edifício” Green-Loan Program | +0.8% | National, Lisbon 22.3% of applications, Porto 11.7% | Short term (≤ 2 years) |

| Industrial Process Electrification in Food Sector | +0.5% | Norte, Centro, Alentejo food-processing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extension of 0% VAT On Heat Pumps Through 2027

Parliamentary debate over reinstating a reduced VAT rate has left the standard 23% in place, widening price gaps with Spain and France and nudging cross-border purchasers toward foreign installers. Trade bodies warn the differential siphons service jobs and slows technician certification, exacerbating Portugal’s 5,000-worker HVAC shortfall. Without relief, residential unit sales could fall 8-12% and drag the Portugal heat pump market by roughly 1.2 percentage points of CAGR. A return to 6% VAT would trim air-to-water payback to four-six years in oil-heated rural homes and accelerate LPG boiler replacements. EU rules already permit lower VAT on efficiency goods, so the fiscal lever remains entirely domestic.[1]Assembleia da República, “Debate on VAT Reinstatement for Heat Pumps,” Parlamento Português, parlamento.pt

EU-Level Ban On Stand-Alone Fossil-Fuel Boilers From 2029

The December 2025 Ecodesign draft raised minimum seasonal‐efficiency thresholds instead of imposing an outright marketing ban, allowing hybrid systems to remain compliant as long as renewable output exceeds half of annual heat. Portugal’s national transposition keeps a 2040 phase-out target but lacks binding interim milestones, enabling landlords to defer capital outlays until end-of-life events. Subsidies for fossil-only boilers ended in 2025, however, and the forthcoming carbon price on natural gas under the EU ETS extension will lift the levelized cost of gas-fired space heat by EUR 15-25 per MWh by 2030, strengthening the Portugal heat pump market case for both buildings and industry.

Surge In Cooling-Degree Days Driving Reversible Models

Record 46.6 °C temperatures in 2025 and rising tropical-night frequency push summer peaks higher than winter loads. Reversible air-to-water and air-to-air units now displace separate chillers, letting offices cool perimeter zones while heating interior cores from a shared two-pipe loop. Field surveys reveal that 30-40% of households already rely on reversible splits as their main winter heater, meaning official statistics understate the installed base. Dual-season comfort also addresses energy-poverty metrics that show 38.3% of Portuguese homes struggle with summer overheating.[2]Instituto Português do Mar e da Atmosfera, “Heatwave Report 2025,” IPMA, ipma.pt

Net-Metering Reforms Encouraging Solar-Heat Pump Hybrids

Portugal surpassed 6.3 GW of self-consumption PV by late 2025. A 2026 grid-access charge now discourages exporting surplus and instead rewards on-site use, prompting owners to schedule domestic hot-water production during solar hours. Smart controllers lift self-consumption above 70% and curb evening peak costs, a profile that meshes neatly with the Portugal heat pump market strategy for both households and hotels. Ground-source designs that incorporate photovoltaic-thermal panels further lower borehole depth and raise seasonal COP to 6.22 in prototype projects.[3]Directorate-General for Energy and Geology, “Self-Consumption Photovoltaic Statistics 2025,” DGEG, dgeg.gov.pt

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Front-Loaded CapEx versus Gas Boiler Replacement | -0.9% | National, acute in rural Centro and interior Norte | Short term (≤ 2 years) |

| Volatile Day-Ahead Power Prices and Peak Tariffs | -0.6% | National, highest stress in Lisbon and Porto evening peaks | Medium term (2-4 years) |

| Bottleneck in F-Gas Certified Installers | -0.7% | National, installer scarcity outside metropolitan areas | Short term (≤ 2 years) |

| Distribution-Grid Hosting-Capacity Saturation | -0.4% | Lisbon metro, spillover to Cascais, Oeiras, Sintra | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Front-Loaded CapEx Versus Gas Boiler Replacement

Installed air-to-water systems cost EUR 4,000-9,000 versus EUR 1,500-2,500 for condensing gas units, widening payback periods when electricity-to-gas price ratios creep above 3:1. The June 2025 VAT reset added EUR 680-1,360 per system, stretching household payback to 6-10 years without PV self-consumption. Green-loan facilities launched in 2026 aim to bridge the gap, yet uptake remains nascent, keeping cost sensitivity a near-term drag on the Portugal heat pump market.[4]Entidade Reguladora dos Serviços Energéticos, “2026 Tariff Methodology,” ERSE, erse.pt

Volatile Day-Ahead Power Prices and Peak Tariffs

Drought-driven gas dispatch pushed intraday power swings to EUR 50-150 per MWh in 2025, with winter evenings peaking at EUR 200 per MWh. Time-of-use tariffs unveiled in 2026 penalize 18:00-22:00 consumption, inflating heat-pump operating cost by 15-25% for users lacking thermal or battery storage. Grid-modernization surcharges add another EUR 8-12 per MWh, dulling savings versus modern condensing boilers and tempering growth for the Portugal heat pump market.[5]Operador del Mercado Ibérico de Energía, “Iberian Day-Ahead Prices 2025-2026,” OMIE, omie.es

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Hybrid Configurations Hedge Price Risk

Hybrid systems that pair electric compressors with gas back-up are expanding faster than the broader Portugal heat pump market, growing 5.61% annually as facility managers cap peak kW charges without sacrificing renewable-heat mandates. Air-source designs still hold the largest 51.46% 2025 share, but ground-source options improve when photovoltaic-thermal panels pre-warm shallow loops, delivering seasonal COP above six. Manufacturers now embed real-time tariff algorithms that switch between fuels, supporting resilience when Portugal’s power prices spike.[6]Robur S.p.A., “Hybrid Heat Pump Systems,” robur.com

Air-to-air models dominate the Algarve and Madeira cooling belt, yet regulators increasingly credit their winter performance, unlocking subsidies that lift residential uptake. Water-source units remain niche because abstraction permits are slow, but treatment-plant waste-water pilots demonstrate high-grade heat recovery potential for district energy schemes. As F-gas quotas tighten, R290 and CO₂ refrigerants move to center stage, reinforcing the Portugal heat pump market pivot toward natural-refrigerant platforms.

By Technology: Ground-To-Water Gains From PV-Thermal Synergy

Air-to-water designs held 60.71% of 2025 sales, underscoring their dominant Portugal heat pump market share in domestic heating upgrades. Ground-to-water systems, however, are growing 5.38% a year because PV-thermal collectors trim loop installation depth and raise seasonal COP above six, widening the addressable retrofit base in tight urban lots.

Air-to-air reversible splits remain the go-to choice in Algarve and Madeira where cooling days already outnumber heating days, yet national statistics undercount their winter use. Water-to-water units mainly serve district energy and industrial sites that can tap stable source temperatures from rivers or wastewater. As EU rules lift the minimum seasonal efficiency to 115%, inverter-driven compressors and natural-refrigerant circuits are becoming standard across every technology track.

By Capacity: 50-200 kW Band Leads Commercial Adoption

Systems rated 50-200 kW are advancing at a 5.14% CAGR through 2031, the fastest band within the Portugal heat pump market size, because modular arrays let hotels, hospitals, and factories scale up to 640 kW without custom engineering. The 10-50 kW class still led with 40.23% of 2025 installations, primarily in multifamily housing and small commercial blocks.

Below-10 kW machines are losing share as tighter building envelopes cut design loads, allowing smaller homes to downsize equipment. Very large plants above 200 kW remain confined to district networks and process industries, yet even here suppliers favor cascades of 40 kW modules that shorten lead times and disperse compressor risk. Integrated BACnet and Modbus gateways now ship as standard, enabling builders to monetize flexibility in emerging demand-response programs.

By Application: Industrial Process Heating Accelerates

Domestic hot-water heaters accounted for 42.32% of 2025 revenue, reflecting Portugal’s limited gas grid and widespread use of electric boilers that are easy to replace. Industrial process-heat projects, though a smaller base, are climbing at a 5.07% CAGR as dairies, beverage bottlers, and olive mills capture refrigeration waste heat to shave gas demand ahead of the 2027 carbon-price rollout.

Space-heating growth is moderating because new-build standards cut envelope loads, but reversible units revive interest by delivering cooling through the same hydronic loop. High-temperature CO₂ machines now reach 90 °C water, enabling pasteurization and sanitation without steam, which helps industrial buyers lock in sub-EUR 50 (USD 55) per MWh thermal costs. The dual-season proposition also addresses energy-poverty stress, offering single-asset comfort for both cold snaps and summer peaks.

By End User: Industry Narrows the Gap With Households

Residential buyers still produced 59.14% of 2025 turnover, yet their growth is slowing after the VAT hike stretched payback periods. Industrial customers are advancing at a 4.86% CAGR, closing in on households as EU Emissions Trading System charges make gas-fired heat pricier.

Commercial properties, especially hotels and offices, favor modular 50-200 kW cascades that can grow with occupancy. Subscription models that shift capital and maintenance risk to third-party owners are expected to widen access for cash-constrained public buildings. Together, these trends diversify demand away from single-family retrofits and broaden the end-user base of the Portugal heat pump market

By Installation: New-Builds Gain as Developers Pre-Wire

Retrofits captured 53.47% of 2025 spending, but new-build activity is expanding at a 4.92% CAGR because specifying heat pumps from the outset avoids EUR 800-2,500 (USD 910-2880) in labor premiums linked to post-occupancy upgrades.

Developers now reserve rooftop space, size electrical panels for peak compressor draw, and pre-install hydronic loops, trimming overall installed cost by up to 25%. Retrofit momentum persists in oil- and LPG-heated rural homes, yet installer shortages and longer paybacks temper immediate conversion rates. Financing instruments that wrap the residual out-of-pocket outlay into green mortgages will determine how swiftly the installation mix tilts toward fresh construction.

Geography Analysis

Lisbon and Porto account for one-third of subsidy applications, mirroring installer density and marketing reach rather than superior economics. Lisbon’s aging feeders near saturation, triggering a USD 1.81 billion upgrade plan that may delay approvals for large commercial heat pumps until 2027. Porto’s industrial fringe exploits modular 50-200 kW units for cheese, beverage, and chemical plants, leveraging waste-heat recovery to reach 1.7-year payback, strengthening the Portugal heat pump market foothold in the Norte region.[7]E-Redes, “2026-2030 Distribution-Grid Investment Plan,” e-redes.pt

Algarve municipalities confront cooling-load dominance as record 46.6 °C days multiply; reversible air-to-water and air-to-air systems thus replace split chiller-boiler pairs in hotels and luxury residences. The Nine in Vilamoura installed 48 R290 rooftop units serving individual apartments, illustrating decentralized architectures that sidestep central-plant space constraints. PV self-consumption exceeds 70% here, smoothing evening tariff spikes and underlining solar-heat-pump synergies in the Portugal heat pump market.[8]Energie EST, “Vilamoura Luxury Multifamily Rooftop Heat-Pump Project,” energie.pt

Interior Centro and Norte host the sharpest energy-poverty indicators, with 20.8% of households unable to heat adequately in winter. Yet installer scarcity hampers rollout, as only 6,536 F-gas-certified personnel serve the entire country. Targeted vocational programs and mobile training centers form policy priorities if the Portugal heat pump market is to meet decarbonization targets outside major metros.[9]Associação Portuguesa da Indústria de Refrigeração e Ar Condicionado, “F-Gas Technician Registry 2025,” apirac.pt

Competitive Landscape

Bosch, Viessmann, Vaillant, Daikin, and NIBE collectively command roughly 60-70% of the Portugal heat pump market by combining local assembly, multi-refrigerant portfolios, and 3,400-plus certified partner installers across Iberia. Bosch’s USD 113 million Aveiro expansion adds 150,000 propane units yearly and a 14-chamber R&D lab, trimming delivery lead time to two-three days for Iberian dealers. Asian challengers, Midea, LG, Panasonic, undercut pricing by up to 25% in air-to-air splits but struggle in hydronic segments due to sparse service coverage and limited installer familiarity.

Strategic focus is shifting to vertical integration of after-sales support. Daikin maintains 116 European training centers, while Ariston’s Wolf Campus certifies technicians on high-temperature hybrids, mitigating the installer bottleneck that constrains the Portugal heat pump market. Refrigerant strategies converge on R290, R454C, and CO₂ as EU 2024/573 accelerates hydrofluorocarbon phase-down; Vaillant already made R290 standard in 2025 and extended warranties to five years to underscore reliability.

Modular cascade systems redefine the 50-200 kW niche. Mitsubishi’s 40 kW R454C ecodan Pro CAHV stacks to 640 kW, and Modutherm’s AW290 reaches 1,600 kW, cutting engineering cycles from 16 to six weeks and distributing compressor risk. Indigenous player Ecoforest pushes shallow-loop geothermal for Portuguese retrofits, contending that local geology favors horizontal trenches over expensive boreholes, a proposition that could enlarge domestic share in the Portugal heat pump market.[10]Ecoforest, “Geothermal Solutions for the Iberian Peninsula,” ecoforest.com

Portugal Heat Pump Industry Leaders

Bosch Thermotechnology (Robert Bosch GmbH)

Daikin Industries Ltd.

Viessmann Werke GmbH & Co. KG

Mitsubishi Electric Corporation

LG Electronics Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Panasonic installed two 300 kW ECOi-W reversible heat pumps with R32 refrigerant in a Lisbon office building, enabling simultaneous zone-level heating and cooling.

- March 2026: Mitsubishi Electric Trane introduced the ecodan Pro CAHV 40 kW R454C heat pump, scalable to 640 kW for hotel and hospital hot-water retrofits.

- February 2026: The European Commission launched the HP4INDUSTRY LIFE project to standardize industrial heat-pump solutions for pulp, paper, food, beverage, and chemical plants.

- January 2026: Bosch Thermotechnology began production of Compress 5800i AW and 6800i AW propane models at its expanded Aveiro facility, adding 300 local jobs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

We size Portugal's heat pump market as the annual revenues generated from newly manufactured air-source, water-source, and ground-source units up to 1 MW that are installed for space heating, cooling, or domestic hot water in residential, commercial, industrial, and institutional premises.

Scope exclusion: portable ACs, solar-assisted hybrids sold as solar kits, and second-hand equipment are outside this study.

Segmentation Overview

- By Source Type

- Air Source

- Water Source

- Ground Source

- Hybrid

- By Technology

- Air-to-Air

- Air-to-Water

- Water-to-Water

- Ground-to-Water

- By Capacity

- Below 10 kW

- 10-50 kW

- 50-200 kW

- Above 200 kW

- By Application

- Space Heating

- Space Cooling

- Domestic and Sanitary Hot Water

- Industrial and Process Heating

- Other Applications

- By End User

- Residential

- Commercial

- Industrial

- By Installation

- New Installation

- Retrofit

Detailed Research Methodology and Data Validation

Desk Research

Our analysts first collect publicly available fundamentals from tier-1 sources such as Eurostat building-stock data, the European Heat Pump Association country fiche, APIRAC statistics, customs shipment tables, and patent filings before layering in price and competitor cues from Portugal's Diario da Republica tender notices. Paid repositories, D&B Hoovers for company financials, Dow Jones Factiva for deal flow, and Questel for refrigerant patent trends, add depth where open data thin out. The team supplements these with corporate 10-Ks, investor decks, and reputable press articles tracking OEM capacity additions (e.g. Bosch's Aveiro R290 line). This list illustrates, not exhausts, the desk sources referenced.

Primary Research

Conversations with installers across Lisbon, Porto, and the Algarve, facility managers in tourism, housing co-op presidents, and regional energy agency officers help us verify average selling prices, real-world COPs, subsidy uptake, and retrofit share. Follow-up surveys clarify seasonality swings and lead-time bottlenecks, ensuring assumptions reflect on-ground reality.

Market-Sizing & Forecasting

A top-down demand pool is built from dwelling counts, HVAC renovation rates, and heat pump penetration, which are then costed with median ASPs gathered above; selective supplier roll-ups and channel checks validate totals. Key drivers tracked include electricity-to-gas price ratios, renovation grant value, summer cooling degree days, installer headcount, grid carbon factor, and R290 unit share. A multivariate regression links these variables to historical sales and feeds an ARIMA scenario that projects through 2030; gaps in installer-reported volumes are bridged using import data and capacity utilization heuristics.

Data Validation & Update Cycle

Outputs pass three-step peer review, variance checks against trade and subsidy disbursement records, and a final analyst walkthrough before release. Mordor refreshes the model annually and reopens interviews when incentives or energy prices shift materially.

Why Mordor's Portugal Heat Pump Baseline earns trust

Published estimates often diverge because firms choose different scopes, currencies, and refresh timetables.

Key gap drivers here stem from whether services, installation labor, and O&M are folded into 'market value,' from the cutoff size class, and from how fast fiscal incentives are assumed to taper.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 151.2 m (2024) | Mordor Intelligence | - |

| USD 125 m (2024) | Regional Consultancy A | Excludes installation and service revenue; counts only 'heat pumps other than air-conditioning machines' (Prodcom code). |

| EUR 1.7 bn (2022) | Industry Association B | Bundles equipment manufacturing, installation, and ongoing O&M turnover; uses turnover not point-of-sale value. |

The comparison shows that Mordor's disciplined scope, finished units sold at end-user prices, updated every twelve months, offers a balanced, transparent baseline that clients can retrace to clear variables and repeatable steps.

Key Questions Answered in the Report

How large will Portugal's heat-pump sector become by 2031?

It is forecast to reach USD 209.13 million by 2031, expanding at a 4.69% CAGR from 2026.

Which source configuration is growing fastest?

Hybrid systems that combine an electric compressor with a gas-boiler backup are rising at a 5.61% CAGR through 2031.

What capacity band now leads commercial retrofits?

Units rated 50-200 kW show the strongest 5.14% annual growth, favored by hotels, hospitals, and light-industrial facilities.

Where do reversible heat pumps hold the greatest upside?

Algarve, Lisbon, and Setúbal areas, where rising cooling-degree days drive demand for systems that can both heat and cool.

How does VAT policy affect residential adoption?

Retaining the 23% VAT adds roughly one to two years to system payback, while reinstating a 6% rate would shorten payback to four-six years.

What is the main hurdle beyond equipment cost?

A shortage of roughly 5,000 certified HVAC technicians is slowing installation timelines, especially in interior regions.

Page last updated on: