Makeup Remover Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

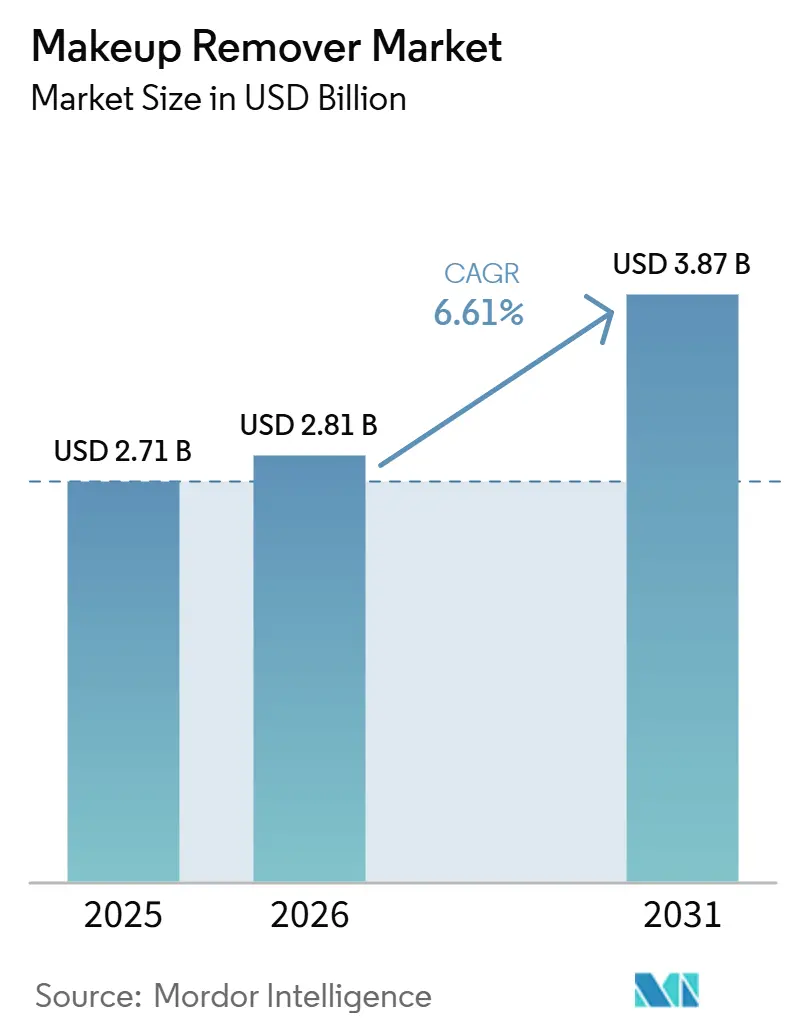

| Market Size (2026) | USD 2.81 Billion |

| Market Size (2031) | USD 3.87 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Makeup Remover Market Analysis by Mordor Intelligence

The makeup remover market size is projected to grow from USD 2.71 billion in 2025 and USD 2.81 billion in 2026 to USD 3.87 billion by 2031, registering a CAGR of 6.61% between 2026 and 2031. Urban consumers increasingly view cleansing as a self-care practice, with dermatological advice on barrier preservation popularizing double-cleansing routines globally. Social media platforms have further amplified Korean and Japanese skincare practices, turning niche techniques into widespread habits. On the supply side, innovations in water-free fibers, micro-emulsions, and upcycled packaging are driving laboratory advancements into retail adoption. Simultaneously, regulatory changes in the United States and European Union are reshaping the market by pushing out marginal brands and raising quality standards. For example, the implementation of the Modernization of Cosmetics Regulation Act of 2022 (MoCRA) has significantly impacted the competitive landscape. This regulation requires cosmetic manufacturers to register facilities and list products with the FDA, creating barriers for counterfeit producers while strengthening the position of established brands [1]Source: U.S Food & Drug Administration, "Cosmetics & U.S Law", fda.gov.

Key Report Takeaways

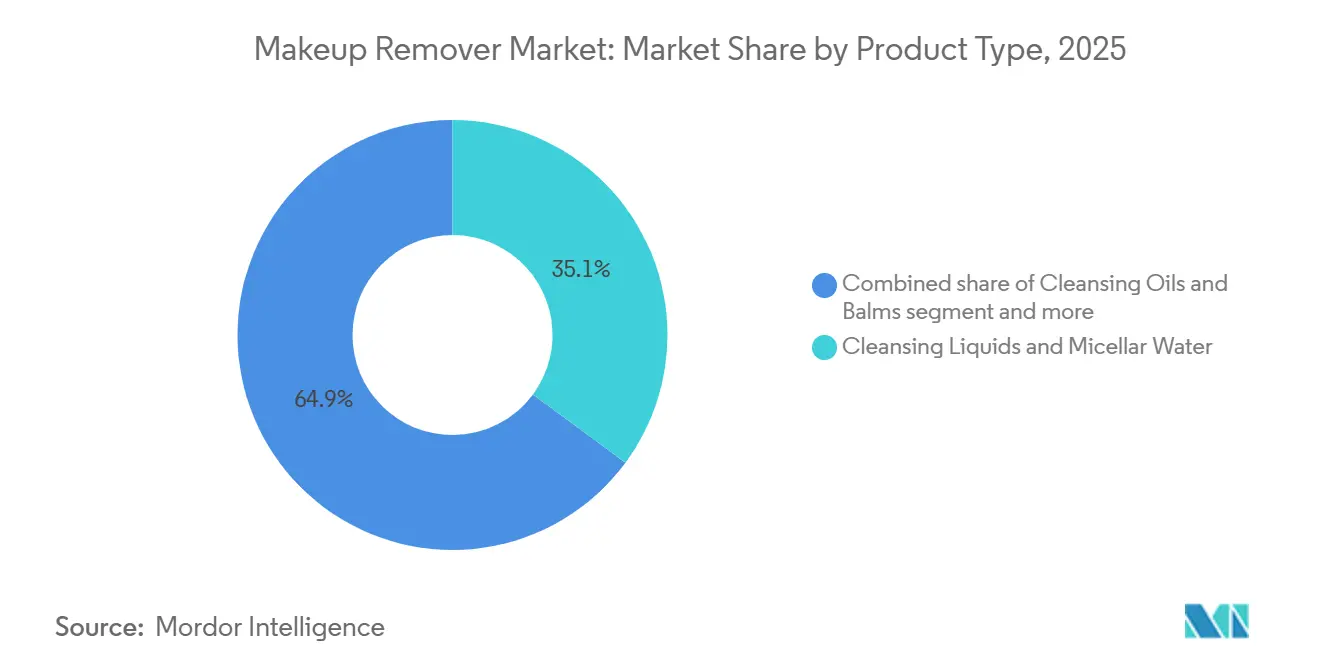

- By product type, cleansing liquids and micellar water led with 35.13% of makeup remover market share in 2025, while cleansing oils and balms are forecast to advance at a 7.18% CAGR through 2031.

- By category, conventional products held 83.19% share of the makeup remover market size in 2025 and organic variants are projected to grow at an 8.08% CAGR to 2031.

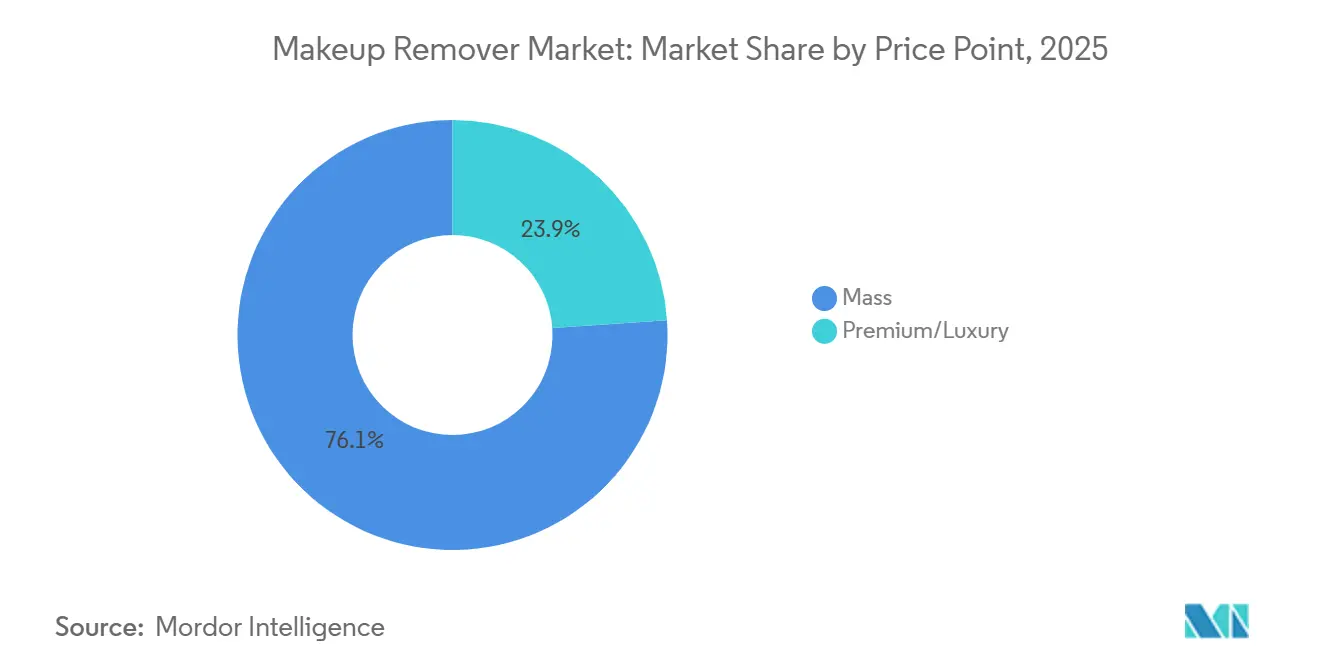

- By price point, mass offerings commanded 76.10% revenue share in 2025, yet premium/luxury lines are poised for a 7.85% CAGR over 2026-2031.

- By distribution channel, health and beauty stores captured 44.76% share in 2025, while online retail is expected to post an 8.17% CAGR to 2031.

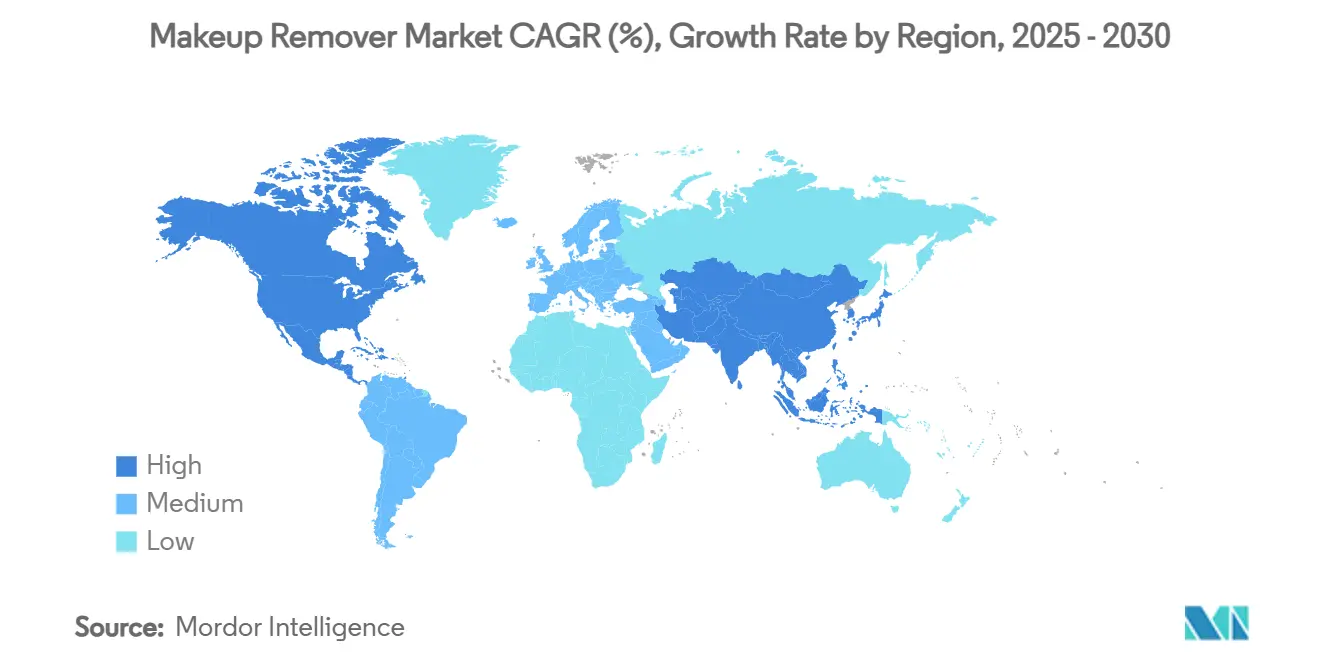

- By geography, Asia-Pacific accounted for 35.40% of the makeup remover market in 2025 and is projected to grow at a 7.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Makeup Remover Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing prevalence of daily makeup use | +1.8% | Global, with concentration in Asia-Pacific and North America | Long term (≥ 4 years) |

| Growth in awareness of skin health and hygiene | +1.5% | Global, particularly strong in developed markets | Medium term (2-4 years) |

| Innovation in product formulations | +1.2% | Global, led by North America and Europe research and devlopment centers | Medium term (2-4 years) |

| Trend toward natural and organic ingredients | +0.9% | North America and European Union, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Expansion of product availability and retail channels | +0.7% | Asia-Pacific core, spill-over to Middle East and Africa and South America | Short term (≤ 2 years) |

| Influence of social media and beauty influencers | +0.6% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing prevalence of daily makeup use

The increasing prevalence of daily makeup use is driving the growth of the makeup remover market by elevating the frequency and necessity of product application for effective skin cleansing. As consumers increasingly use makeup to address skin concerns and explore multifunctional products, the demand for reliable makeup removers has risen. This growing demand has also contributed to higher imports of cosmetics in various countries. According to UN Comtrade, Argentina imported USD 147.77 million worth of makeup, beauty, and skincare products in 2023. The habitual use of makeup, particularly among women over 55 and millennials, has led to frequent application of products such as foundation, lipstick, and waterproof formulas. This results in greater accumulation of cosmetic residues on the skin, necessitating thorough removal to maintain skin health and prevent irritation. Consequently, there is a consistent demand for specialized removers designed for various formulations (e.g., long-wear and hybrid cosmetics) and different skin types. Additionally, the growth of the beauty industry and the increasing adoption of skincare-focused makeup further amplify this demand, as consumers prioritize products that deliver both performance and skin care benefits. Therefore, the rise in daily makeup usage serves as a key driver for the growth of the makeup remover market, linking consumer habits to the essential need for effective cleansing solutions.

Growth in awareness of skin health and hygiene

Dermatologist-led discussions emphasize the connection between incomplete makeup removal and issues such as acne, dryness, and premature aging. Consumers increasingly examine ingredient labels, seeking non-comedogenic oils, balanced pH surfactants, and soothing botanicals. Growing awareness of dermatological concerns, such as sensitivity, acne, and the effects of residual makeup on the skin, has driven demand for high-quality makeup removers that effectively and gently remove cosmetics, dirt, and pollutants. Dermatologists frequently recommend gentle, fragrance-free makeup removers, particularly for sensitive skin. Examples include micellar waters like Bioderma Sensibio H2O and Garnier Micellar Cleansing Water, cleansing balms such as Clinique Take The Day Off Cleansing Balm and Farmacy Green Clean Makeup Meltaway Cleansing Balm, and oil-based cleansers like DHC Deep Cleansing Oil. Retailers have introduced “derm-tested” shelving cues, while many brands highlight clinical study results on their packaging. Regulatory focus on ingredient transparency and product safety further supports these consumer preferences, encouraging brands to develop innovative formulations, including micellar waters and oil-based cleansers, known for their effectiveness and skin-soothing benefits. This trend drives premium purchases, as consumers associate higher price points with safer, skin-friendly products. As a result, value growth surpasses volume growth, contributing to the expansion of the makeup remover market across various channels.

Trend toward natural and organic ingredients

The increasing preference for natural and organic ingredients is a significant driver of growth in the makeup remover market, as more consumers seek products free from synthetic chemicals and harsh additives. This trend is driven by growing awareness of the potential skin and health risks associated with conventional removers, such as irritation, allergies, and hormone disruption. Consequently, there is a rising demand for plant-based and eco-friendly alternatives. According to a 2024 survey by NSF, 74% of consumers prioritize organic ingredients in personal care products, while 65% look for transparent ingredient lists to identify potentially harmful components [2]Source: NSF, "TGM Research to survey 1,000 Americans in 2024", nsf.org. Organic and natural makeup removers, formulated with ingredients such as oils, botanical extracts, and micellar waters, are perceived as safer and gentler, particularly appealing to health-conscious consumers and those with sensitive skin. Retailers in North America and Europe are dedicating more shelf space to products certified by organizations like Ecocert, USDA Organic, and COSMOS. Ingredients such as coconut, moringa, and camellia seed oils are increasingly replacing mineral oil as primary solubilizers, while sugar-derived surfactants provide milder foaming action and are environmentally friendly due to their quick biodegradability. As a result, the organic makeup remover segment is experiencing strong growth, surpassing the conventional category. This highlights how the demand for clean, natural, and organic formulations is reshaping the makeup remover market.

Influence of social media and beauty influencers

Social media and beauty influencers play a significant role in driving demand within the makeup remover market by increasing consumer awareness, shaping preferences, and influencing purchasing decisions. Through tutorials, reviews, and product showcases, influencers educate audiences on the importance of effective makeup removal and promote specific products that align with evolving beauty standards. This has led to greater consumer interest in not only using makeup but also investing in high-quality removers, particularly those featuring natural and gentle ingredients. Platforms such as Instagram, TikTok, and YouTube enable influencers to reach large and targeted demographics, especially younger generations who are highly responsive to beauty trends and skincare routines promoted online. According to the World Population Review, Instagram users in 2024 included 392.5 million in India, 172.6 million in the United States, and 141.4 million in Brazil, among others [3]Source: World Population Review, "Instagram Users by Country 2025", worldpopulationreview.com. The growth of social media has also increased demand for clean, organic, and eco-friendly formulations, as influencers increasingly advocate for products that align with health, wellness, and sustainability values. Consequently, makeup remover brands are strategically collaborating with influencers and utilizing e-commerce platforms to expand their reach, boost sales, and remain competitive in a market increasingly shaped by digital engagement and evolving consumer expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of counterfeit and imitation products | -0.9% | Global, especially Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Consumer skepticism for over-hyped claims | -0.6% | Developed markets in North America and Western Europe | Medium term (2-4 years) |

| Concerns over harsh chemicals and allergens | -0.8% | North America and European Union | Long term (≥ 4 years) |

| Time constraints in multi-step routines | -0.5% | Global urban consumer segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of counterfeit and imitation products

The prevalence of counterfeit and imitation (lookalike) products poses significant challenges to the growth of the makeup remover market. These products result in considerable revenue losses for legitimate brands, weaken consumer trust, and pose risks to public health. Counterfeit items, often sold at lower prices and manufactured with unsafe or inferior ingredients, divert sales from authentic brands and may cause adverse effects such as skin irritation, allergic reactions, or severe health issues. Such incidents damage the reputation of genuine brands and can discourage consumers from purchasing not only the affected product but also other products within the category. The widespread availability of counterfeits, particularly on online platforms, further undermines consumer confidence, leading to hesitation and reduced demand for authentic makeup remover products. Moreover, when legitimate brands are associated with safety concerns—even if caused by counterfeit products, it exacerbates reputational harm, invites increased regulatory scrutiny, and limits the ability of authentic brands to achieve growth and innovation in the market.

Time constraints in multi-step routines

Time constraints associated with multi-step skincare routines present a notable challenge to the growth of the makeup remover market. As multi-step regimens, often including five or more steps such as cleansers, exfoliators, serums, creams, and masks, become increasingly common, consumers are required to allocate significant time, particularly in the evening, to complete each step and allow for product absorption. Even skincare enthusiasts, who recognize the advantages of layered routines, frequently report spending over 20 minutes on these processes. The inclusion of double cleansing, which involves using a makeup remover followed by a separate cleanser, further adds to the time and complexity. For many consumers, the perceived inconvenience of such extended routines discourages the use of dedicated makeup removers. Instead, they often prefer multi-functional products, such as all-in-one cleansers or micellar waters, which offer greater convenience and efficiency. This preference for streamlined solutions limits the adoption of standalone makeup removers, particularly among time-conscious or minimalist users who prioritize simplicity over elaborate skincare rituals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Liquids Lead, Oils Accelerate

Cleansing liquids and micellar water represented 35.13% of the makeup remover market share in 2025, driven by their lightweight texture and no-rinse convenience. These products are particularly favored by Gen Z consumers, who prioritize quick and efficient nighttime skincare routines. The market size for these liquids is anticipated to grow steadily as brands incorporate ingredients such as ceramides and antioxidants. In contrast, cleansing oils and balms are preferred by users of long-wear foundations due to their ability to provide deeper emulsification. While this category is currently smaller, its projected CAGR of 7.18% indicates consistent growth, supported by the increasing popularity of K-beauty rituals and the demand for gentle, tug-free makeup removal. Additionally, beauty brands' training videos demonstrating double-cleansing techniques are encouraging more consumers to include oils and balms in their routines.

Innovation in makeup removers is primarily driven by texture and sensory appeal. Gel-to-milk cleansers attract consumers seeking unique, transformative experiences, while stick formats provide spill-proof convenience, appealing to frequent travelers. Sampling stations at prestige beauty counters allow customers to test aromatic oils that melt upon contact with the skin, encouraging premium purchases. Meanwhile, price-sensitive consumers continue to prefer value-pack liquids, particularly in pharmacy chains where loyalty programs and coupons help reduce costs. The combination of high-volume liquids and the growing demand for oils creates a balanced product portfolio, enabling manufacturers to mitigate risks within the category.

By Category: Conventional Dominates, Organic Captures Share

Conventional solutions accounted for 83.19% of the makeup remover market in 2025, supported by cost-efficient synthetic surfactants and well-established supply chains. Mass-market players utilize economies of scale to secure favorable raw material contracts, enabling them to maintain low unit prices even during periods of inflation. While the market size for conventional offerings remains significant, its growth trajectory is leveling off due to increasing concerns about ingredient transparency. In contrast, organic formulas are growing at a compound annual growth rate (CAGR) of 8.08%, driven by consumer trust in eco-label certifications and positive user reviews highlighting irritation-free experiences. The demand for natural and safe ingredients is rising as consumers increasingly seek products free from harsh chemicals and suitable for sensitive skin. Additionally, the growing emphasis on eco-friendly packaging and sustainability has boosted the popularity of organic makeup removers, particularly those featuring biodegradable or recyclable materials.

Conventional makeup removers maintain a dominant position over organic alternatives primarily due to their affordability and extensive product range. These products are typically priced lower, making them accessible to a broader consumer base that values cost-effectiveness in their beauty routines. Furthermore, conventional makeup removers offer a wide variety of options tailored to different skin types and preferences, providing convenience and versatility that appeal to mass-market consumers. Although awareness of the potential drawbacks of synthetic ingredients has contributed to the growth of the organic segment, the higher price point and, in some cases, limited availability or familiarity with organic alternatives have allowed conventional products to retain their leading market share.

By Price Point: Mass Holds Volume, Premium Drives Value

Mass-market SKUs represented 76.10% of units in 2025, driven by the importance of price accessibility in emerging economies. Bundle promotions, which pair wipes with liquids, contribute to inflated unit counts. However, premium and luxury product lines demonstrated a stronger CAGR of 7.85%, contributing to the growth of the makeup remover market in revenue terms. Consumers justify higher spending on these products due to added skincare benefits, such as niacinamide for barrier repair. At prestige counters, consultants perform half-face demonstrations to showcase residue removal and the hydration glow post-cleanse, encouraging customers to trade up. Luxury balms are often packaged in recyclable glass jars with tactile spatulas, enhancing the premium experience.

Mass-market makeup remover products continue to dominate over premium options due to their affordability, accessibility, and alignment with consumer priorities for effective yet cost-efficient skincare solutions. Most consumers prioritize products that deliver reliable results without the higher price associated with premium offerings, especially during periods of economic uncertainty when budget-friendly options are more appealing. Mass-market brands frequently innovate with advanced yet gentle formulations and user-friendly packaging, further strengthening their appeal. This dominance reflects consumers’ preference for affordable, accessible, and effective solutions, positioning mass-market products as the leading choice in a competitive market, despite the increasing presence of premium alternatives.

By Distribution Channel: Stores Retain Clout, Online Surges

Health and beauty stores accounted for 44.76% of the makeup remover market in 2025. Consumers rely on in-store testers and beauty advisors to evaluate product texture, scent, and potential for irritation. Chain retailers have expanded dermatology sections, placing non-comedogenic removers near acne treatments to encourage cross-selling. Loyalty programs play a key role by offering personalized coupons, encouraging shoppers to return approximately every six weeks, aligning with typical product replenishment cycles. However, e-commerce is growing rapidly, with a projected CAGR of 8.17%. Online platforms leverage features such as instructional videos, ingredient glossaries, and auto-replenishment subscriptions to attract and retain customers.

Cross-border online platforms have introduced consumers to Korean and Japanese cleansing oils, which are often unavailable in physical stores, thereby expanding brand options. Logistics providers now offer two-day delivery for liquid products, supported by improved hazardous material handling procedures. In response, brick-and-mortar retailers have adopted omnichannel strategies, including buy-online-pick-up-in-store services. The makeup remover market benefits from this hybrid approach, as consumers often conduct online research before confirming purchases in-store. Retail landlords are allocating smaller boutique spaces for digitally native brands, while larger chains are testing micro-fulfillment hubs in back rooms to facilitate same-day delivery.

Geography Analysis

Asia-Pacific dominates both value and volume metrics, holding a 35.40% share of the makeup remover market in 2025. This reflects the region's large urban population and increasing disposable incomes. The rapid diffusion of trends through social media, particularly short-form videos, has popularized practices like double cleansing within a short time frame. Government investments in e-commerce logistics have improved rural access and enabled niche brands to reach new areas. Additionally, domestic companies collaborate with local dermatologists to create culturally relevant products. The makeup remover market in Asia-Pacific is projected to grow at a 7.41% CAGR through 2031, surpassing all other regions.

In North America, the demand for makeup removers is driven by high consumer awareness of skincare, advanced formulation technologies, and a well-established culture of daily makeup use. Consumers show a strong preference for premium and organic products, influenced by social media, evolving beauty trends, and robust distribution networks across physical and online platforms. These factors collectively sustain the region's significant market position. The European market benefits from a strong focus on sustainability, natural ingredients, and high regulatory standards, which foster consumer trust and drive product innovation. European consumers are particularly attracted to eco-friendly, dermatologically tested, and cruelty-free products. This demand encourages leading brands to develop gentle and effective makeup removers that prioritize both skin health and ethical considerations.

In the Middle East and Africa (MEA) and South America, increasing beauty and personal care trends are key drivers of the makeup remover market. Rising disposable incomes and growing awareness of skincare routines contribute to this growth. The adoption of Western beauty standards and the rising importance of personal grooming have led to more frequent makeup use, boosting the demand for effective removers. Enhanced accessibility through international and local brands, along with greater product availability in supermarkets and e-commerce platforms, is making makeup removers more widely available. As consumers in these regions continue to prioritize skin health and explore new beauty habits, the demand for makeup removers is expected to grow steadily.

Competitive Landscape

The makeup remover market exhibits a moderate level of fragmentation. This indicates a competitive landscape where multinational corporations such as L'Oréal, Estée Lauder, Unilever, and Procter & Gamble operate alongside regional players like Kao, Amorepacific, and Beiersdorf, as well as digitally native brands such as Glossier and Tatcha. These established companies leverage their strong brand equity and extensive distribution networks to offer a wide range of products, including wipes, micellar waters, oils, and balms, catering to diverse consumer preferences. They consistently invest in research and development to introduce gentler and more effective formulations, addressing consumer demand for multifunctional products that meet both functional and sensorial needs.

Product innovation focusing on sustainability, dermatological safety, and ingredient transparency is a critical strategy driving competition in the market. Companies differentiate themselves by launching eco-friendly and biodegradable products, adopting clean-label claims, and incorporating microbiome-friendly or natural surfactants to align with growing consumer expectations for sustainability and health-conscious choices. For example, in March 2025, Natracare, an environmentally conscious, women-led company, introduced its COSMOS Organic Cleansing Makeup Removal Wipes. These wipes, made from GOTS 100% certified organic cotton cloth, are particularly suitable for sensitive skin as they exclude harmful chemicals and are enriched with vitamin E and soothing aloe vera. Frequent product updates, reformulations to eliminate controversial ingredients, and investments in premium and luxury product lines, such as those from LVMH and Shiseido, further segment the market and cater to a broad spectrum of consumer priorities, ranging from affordability to exclusivity.

The expansion of digital presence and direct-to-consumer strategies is another significant trend shaping the competitive environment. Companies are increasingly utilizing online retail platforms, social media marketing, and influencer partnerships to enhance consumer engagement, build brand communities, and respond swiftly to evolving trends. Personalized skincare solutions are gaining popularity, with brands offering tailored cleansing regimens to address specific skin concerns. As regulatory scrutiny on ingredient safety intensifies, companies are adopting greater transparency and agility, enabling them to adapt quickly to policy changes and consumer feedback. This ensures their continued relevance in a dynamic and rapidly evolving marketplace.

Makeup Remover Industry Leaders

-

L'Oreal S.A

-

The Esee Lauder Inc

-

Revlon Consumer Products LLC

-

Unilever Plc

-

Chanel Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AyuSkin, a skincare brand developed by the creators of Ayu Cosmetics, launched with a 4-in-1 makeup remover balm aimed at cleansing, nourishing, and protecting the skin in a single step. Suitable for all skin types, the formula effectively removed makeup, deeply cleansed pores, and provided nourishment with each application. The balm transformed upon contact, featuring a dense, creamy texture that removed impurities while preserving the skin's moisture.

- February 2025: Garnier collaborated with Ilana Glazer to introduce its new skincare product, Garnier Micellar Water with Salicylic Acid. This product is formulated for sensitive, oily, and acne-prone skin. The new Micellar Water effectively removes makeup, mattifies, and cleanses impurities in a single step. Its lightweight, non-stripping formula provides all-day mattification while keeping the skin fresh and balanced.

- January 2025: Qosmedix introduced its branded Micellar Cleansing Water in a 32-ounce refill size. This product offered the convenience of a cleanser without requiring rinsing or harsh scrubbing, leaving the skin soft and nourished. The Micellar Cleansing Water featured a gentle, fragrance-free formula suitable for all skin types.

- January 2025: Conserving Beauty, an Australian skincare brand, introduced dissolvable makeup remover wipes and face masks with environmentally friendly packaging. The dissolvable makeup remover wipes were developed using vegetable oils and vitamins, providing gentle and effective cleansing suitable for sensitive skin. As part of its sustainability efforts, Conserving Beauty adopted Econic compostable packaging, supplied by Convex.

Global Makeup Remover Market Report Scope

| Cleansing Liquids and Micellar Water |

| Creams and Lotions |

| Wipes and Face Towels |

| Cleansing Oils and Balms |

| Foaming Cleansers and Face Wash |

| Others |

| Organic |

| Conventional |

| Mass |

| Premium/Luxury |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channel |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

| By Product Type | Cleansing Liquids and Micellar Water | |

| Creams and Lotions | ||

| Wipes and Face Towels | ||

| Cleansing Oils and Balms | ||

| Foaming Cleansers and Face Wash | ||

| Others | ||

| By Category | Organic | |

| Conventional | ||

| By Price Point | Mass | |

| Premium/Luxury | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the makeup remover market expected to grow through 2031?

It is forecast to post a 6.61% CAGR between 2026 and 2031, rising from USD 2.81 billion in 2026 to USD 3.87 billion by the end of the period.

Which region will contribute most incremental value?

Asia-Pacific, driven by China, South Korea, and India, will add the largest absolute dollars on a 7.41% CAGR pathway.

What product format is growing fastest?

Cleansing oils and balms are projected to expand at 7.18% CAGR, outpacing micellar liquids and wipes.

Why are organic makeup removers gaining traction?

Certification schemes such as COSMOS and consumer demand for low-toxicity, eco-designed goods are supporting an 8.08% CAGR for organic products.

Page last updated on: