Clean Beauty Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 179.65 Billion |

| Market Size (2031) | USD 288.99 Billion |

| Growth Rate (2026 - 2031) | 9.98% CAGR |

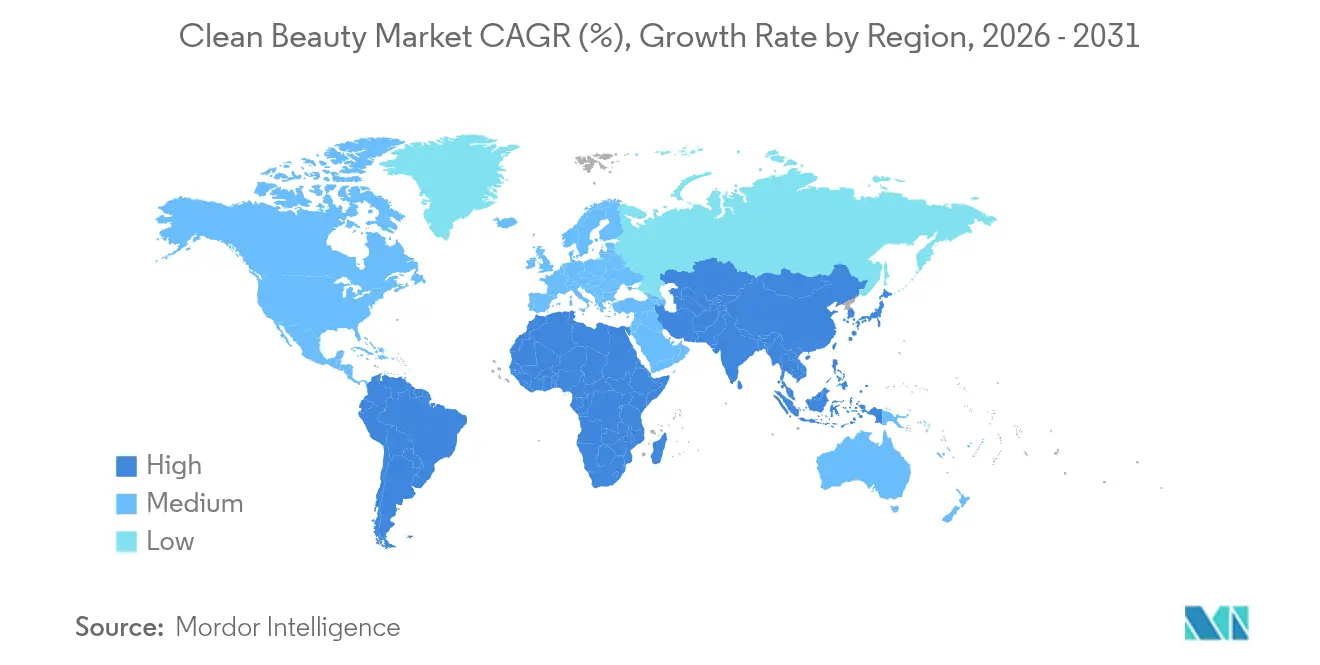

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

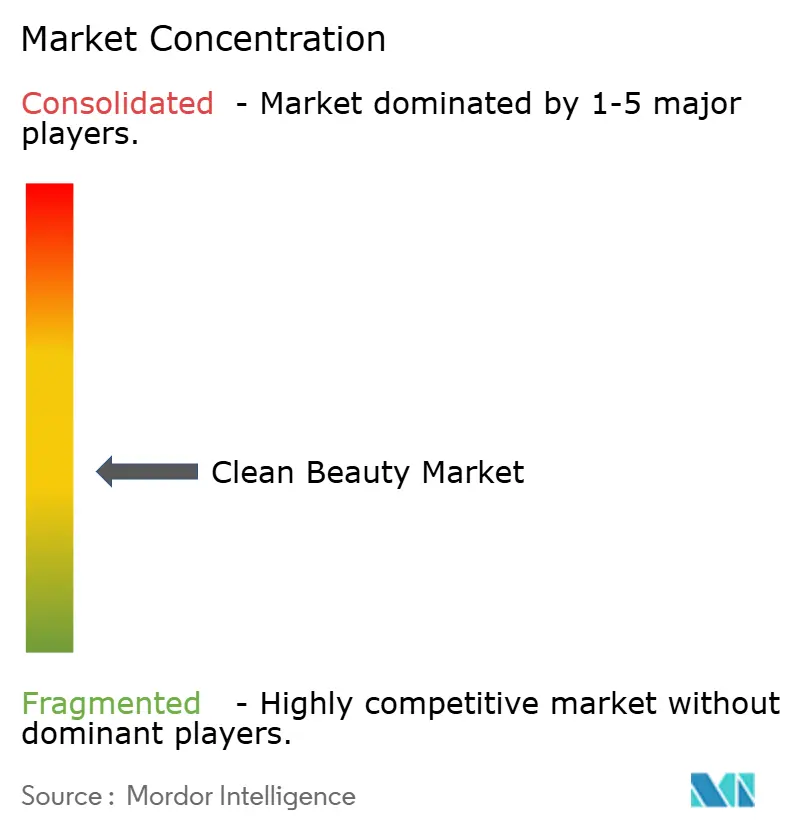

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Clean Beauty Market Analysis by Mordor Intelligence

The clean beauty market size was valued at USD 163.35 billion in 2025 and estimated to grow from USD 179.65 billion in 2026 to reach USD 288.99 billion by 2031, at a CAGR of 9.98% during the forecast period (2026-2031). The clean beauty market is transforming, driven by consumer demand for transparency, ingredient safety, and sustainability. Stricter global regulations, like the FDA’s MoCRA, favor brands with strong compliance. Asia-Pacific leads growth, with rising demand in India and premiumization in China, while the market's moderate concentration allows room for new players. Skincare dominates, but color cosmetics are growing rapidly due to biotech innovations and social media influence, especially among Gen Z. Digital-first purchasing is reshaping beauty commerce, with platforms like TikTok Shop and Amazon gaining prominence. Despite inflation and rising compliance costs, brands are absorbing expenses to stay accessible, focusing on biotech, ethical sourcing, and consumer trust in clean formulations for long-term clean beauty market growth.

Key Report Takeaways

- By product type, skincare captured 34.02% of the clean beauty market share in 2025, while make-up and colour cosmetics are projected to grow at a 12.19% CAGR through 2031.

- By price tier, the mass segment held 61.55% of revenue in 2025, whereas the premium segment is forecast to expand at a 11.74% CAGR to 2031.

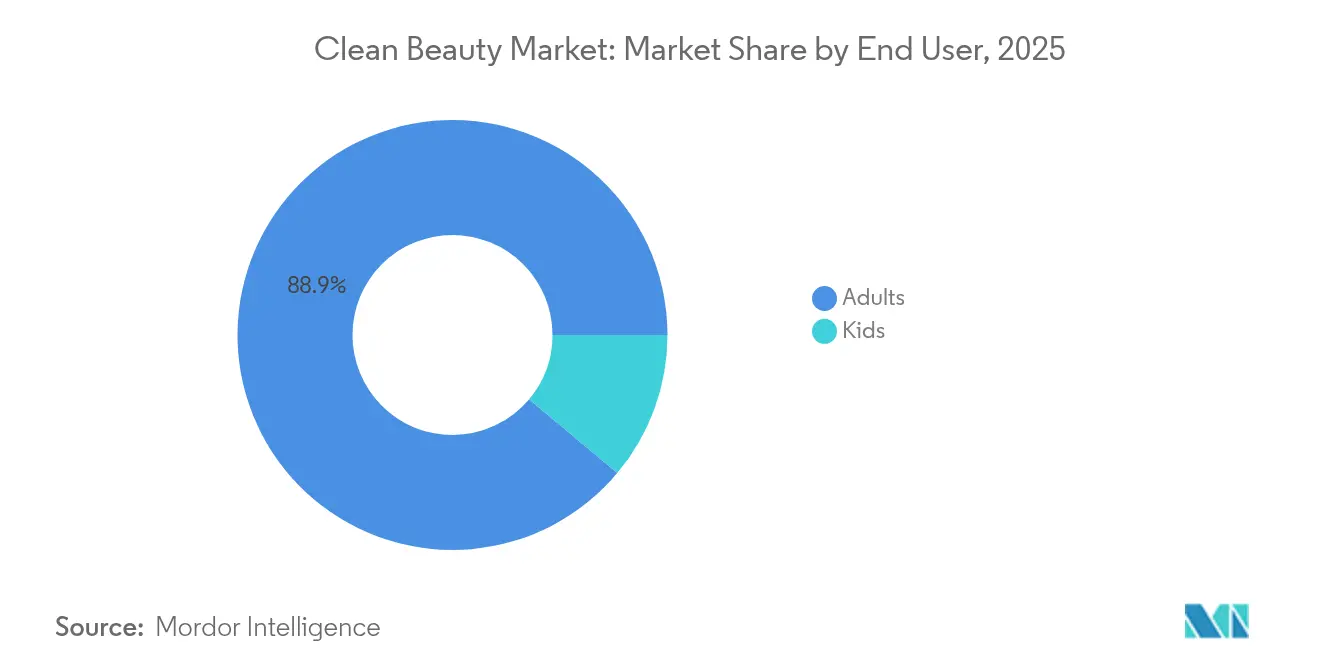

- By end user, adults accounted for 88.90% of the clean beauty market size in 2025; the kids category is advancing at a 13.12% CAGR through 2031.

- By distribution channel, health and beauty stores led with 35.72% share in 2025, while online retail stores are set to grow at a 12.06% CAGR to 2031.

- By geography, Asia-Pacific commanded 31.00% of the clean beauty market share in 2025 and is poised to record a 12.11% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Clean Beauty Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and Safety Concerns | +2.8% | Global, with higher impact in North America and EU | Long term (≥ 4 years) |

| Environmental Sustainability | +2.1% | Global, led by EU regulations, expanding to Asia-Pacific | Medium term (2-4 years) |

| Ingredient Transparency | +1.9% | North America and EU core, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Ethical Sourcing and Cruelty-Free Practices | +1.4% | Global, with premium segments in developed markets | Long term (≥ 4 years) |

| Biotech-fermented actives enabling high-performance clean labels | +1.2% | Asia-Pacific innovation hubs, scaling to global markets | Short term (≤ 2 years) |

| Influence of Social Media and Digital Platforms | +1.6% | Global, with Gen Z concentration in urban markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Health and Safety Concerns

Consumers are increasingly demanding rigorous ingredient safety substantiation, creating a competitive edge for brands with strong clinical validation. The FDA's MoCRA implementation requires cosmetic manufacturers to report serious adverse events within 15 days, favoring companies with established pharmacovigilance systems. With a major portion of consumers viewing toxic chemicals as a major threat, demand for third-party certifications and transparent sourcing is rising. Regulatory pressures and consumer awareness are driving brands to invest in safety infrastructure for sustainable advantages. Post-COVID, consumers are linking topical product safety to overall wellness. State-level regulations, like California and Colorado's PFAS bans, create compliance challenges that benefit larger players with advanced regulatory capabilities.

Environmental Sustainability

Sustainability has shifted from greenwashing concerns to an operational priority, with the EU's Green Claims Directive requiring scientific proof for environmental claims by 2026 [1]Source: European Union, "Directive (EU) 2024/825 of the European Parliament and of the Council of 28 February 2024 amending Directives 2005/29/EC and 2011/83/EU as regards empowering consumers for the green transition through better protection against unfair practices and through better information (Text with EEA relevance)", eur-lex.europa.eu. L'Oréal missed its 2025 packaging targets, achieving only 49% recyclable, reusable, or compostable packaging, highlighting the challenges of sustainability transitions. These challenges, however, create opportunities for agile brands delivering genuine outcomes. Unilever's refill solutions and its pledge to cut virgin plastic use by 50% by 2025 show how sustainability drives cost savings and consumer loyalty. The circular economy is advancing through innovations like Evonik's biosurfactants facility in Slovakia, which uses renewable feedstocks for glycolipid surfactants. Rising consumer willingness to pay premiums for sustainable products, reflected in the growing clean beauty market share of sustainability-marketed items, validates the business case for environmental investments.

Ingredient Transparency

MoCRA's mandate for detailed ingredient listings and safety substantiation shifts transparency from voluntary to regulatory, favoring brands with clean formulations. The EU's requirement to label 56 fragrance allergens by 2026-2028 adds compliance challenges, better managed by established players with strong regulatory frameworks. Social media-driven consumer education has led to informed purchasing. A 2024 NSF survey shows 74% of Americans prioritize organic ingredients, and 65% seek transparent ingredient lists [2]Source: National Sanitation Foundation (NSF), "74% of Consumers Consider Organic Ingredients Important in Personal Care Products", nsf.org. This focus on ingredient awareness benefits brands by simplifying complex formulation science. The "skincare as makeup" trend drives demand for multifunctional products with concise ingredient lists, boosting biotech-derived actives. Blockchain adoption for supply chain transparency offers a competitive edge by verifying sourcing credentials and building trust.

Biotech-fermented actives enabling high-performance clean labels

Biotechnology is bridging the gap between clean ingredients and product efficacy. Fermentation-derived actives deliver superior performance while meeting clean beauty standards. L'Oréal's partnership with Debut Biotech aims to replace traditional ingredients with biotech alternatives, ensuring product performance. Dermegen's DermaCare NP, a fermentation-based phenoxyethanol alternative, addresses preservative challenges with broad antimicrobial protection. The precision fermentation market is growing rapidly, with Brenntag and Cambrium launching NovaColl vegan collagen in European markets, highlighting biotech's commercial viability. This technology enables clean labels without compromising efficacy, addressing consumer concerns. Fermentation also strengthens supply chains by reducing reliance on climate-sensitive agricultural inputs.

Restraints Impact Analysis of Clean Beauty Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Product Costs | -1.8% | Global, with higher impact in price-sensitive emerging markets | Medium term (2-4 years) |

| Lack of harmonised global "clean" definition causing confusion | -1.2% | Global, with regulatory fragmentation across regions | Long term (≥ 4 years) |

| Ingredient Sourcing and Supply Chain Complexity | -1.5% | Global, with acute impact in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Retailer clamp-down on greenwashing and delisting risk | -0.9% | North America and EU core, expanding to global retail chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Product Costs

Rising costs from premium ingredient sourcing and stricter regulations are increasing entry barriers in the clean beauty market, especially for budget-conscious consumers. The U.S. Bureau of Labor Statistics reported a 0.5% rise in personal care prices in May 2025, reflecting ongoing inflation in this sector [3]Source: Bureau of Labor Statistics, "Consumer Price Index– May 2025", bls.gov. While seemingly minor, these increases affect affordability and buying habits over time. Brands are adopting “upflation” strategies, positioning products as premium to justify higher prices. Supply chain disruptions and elevated raw material costs are pressuring margins, leaving smaller clean beauty brands vulnerable. Although many consumers are willing to pay more for sustainable formulations, persistent cost inflation limits broader market access and adoption.

Lack of harmonised global "clean" definition causing confusion

Regulatory fragmentation across markets complicates compliance and confuses consumers. Varying definitions of "clean" undermine brand positioning and inflate costs. Without standardized clean beauty criteria, greenwashing thrives, penalizing brands with rigorous standards. Canada's updated cosmetic regulations and the EU's Green Claims Directive create compliance pathways favoring multinationals over emerging brands. This forces brands to develop multiple formulations, increasing costs and delays. Ambiguity around clean beauty definitions leads to inefficiencies, where marketing claims outweigh formulation quality. Initiatives like COSMOS certification and the EcoBeautyScore Consortium aim for unified standards, but adoption remains voluntary and fragmented.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Clean Beauty Market Segment Analysis

By Product Type:

Skincare Dominance Drives InnovationIn 2025, skincare commands a dominant 34.02% of the clean beauty market, evolving from basic cleansing to advanced treatments with biotech actives and personalized formulations. This leadership is driven by consumers prioritizing skin health over mere cosmetic enhancement. Major companies, like L’Oréal, report a 16.4% growth in their dermatological beauty divisions in the first half of 2024. While make-up and color cosmetics hold a smaller clean beauty market share, they're set to grow at a 12.19% CAGR through 2031, spurred by social media and hybrid products merging color with skincare benefits. The fragrance segment is seeing a push towards premiumization, and categories like bath, shower, and haircare are embracing clean principles, focusing on wellness, scalp solutions, and sustainable sourcing.

The lines between skincare and color cosmetics are blurring, highlighted by the "skincare as makeup" trend that favors non-toxic, skin-friendly ingredients over mere aesthetics. Innovations in clean beauty are driven by advancements in green chemistry and fermentation, allowing brands to swap synthetic ingredients for bio-based ones without losing effectiveness. Even categories like deodorants and oral care are embracing clean beauty, with new brands emphasizing natural actives and clear labeling. This fragmentation across product types offers niche specialists a chance to excel in specific segments, while larger players anchor their growth in skincare and color cosmetics.

By Price Tier:

Premium Growth Outpaces Mass MarketIn 2025, mass market products held 61.55% of the clean beauty market, reflecting strong demand for affordable formulations. However, the premium segment, growing at a 11.74% CAGR, highlights consumers' willingness to invest in clean products with proven efficacy and sustainable ingredients. This "premiumization" trend shows consumers trading up for higher-quality formulations, even in mass retail. The line between mass and prestige is blurring as mass brands introduce elevated, cleaner product lines.

Premium segment consumers prioritize ingredient transparency, safety, and brand authenticity over luxury branding, creating opportunities for emerging brands to highlight efficacy and sustainability. The mass segment remains resilient by offering clean alternatives at accessible prices without compromising performance. Private equity investments in brands like Beautycounter and bareMinerals reflect confidence in premium segment growth. The convergence of pricing strategies between mass and premium players signals a shift toward value-based pricing, where consumers focus on formulation quality and ethical sourcing over brand tiering.

By End User:

Kids Segment Accelerates Despite Adult DominanceIn 2025, adults hold an 88.90% clean beauty market share, highlighting their purchasing power and complex beauty routines. The kids' segment, however, is growing rapidly at a 13.12% CAGR, driven by parental concerns over ingredient safety and the rise of clean, age-appropriate formulations. This growth reflects shifting consumer priorities, with parents applying adult-level scrutiny to children's products. The kids' segment aligns with health-conscious trends, as parents seek safe yet effective options for sensitive skin. In contrast, the adult segment shows a shift toward clean formulations, with consumers replacing conventional products rather than increasing usage.

The kids' segment's growth creates opportunities for brands that can meet regulatory requirements while delivering safe, appealing formulations. Brands like Honest Company, known for clean kids' products, demonstrate this potential, though expansion requires balancing safety with performance. The adult segment's move toward clean beauty is driven by Millennials and Gen Z, who prioritize transparency and sustainability over traditional benefits. This generational shift suggests clean beauty will become the norm rather than a premium option, with kids' segment growth signaling broader market transformation.

By Distribution Channel:

Digital Transformation AcceleratesIn 2025, health and beauty stores hold a 35.72% clean beauty market share, leveraging product education and personalized recommendations. Online retail stores are growing fastest at a 12.06% CAGR, driven by social media commerce and direct-to-consumer strategies. This reflects consumer preference for digital convenience, with TikTok Shop selling beauty products every second and Amazon leading as Europe's largest e-commerce beauty merchant. Traditional retailers are adopting experiential offerings, though with mixed results as consumer behavior shifts to digital-first patterns. Supermarkets and hypermarkets are adding clean beauty sections to meet mainstream demand, while direct-to-consumer platforms gain traction through personalized marketing and subscription models.

Digital transformation benefits clean beauty brands that effectively communicate ingredient benefits and sustainability through content marketing and influencer partnerships. Online channels allow emerging brands to bypass traditional retail barriers, though success requires strong digital marketing and supply chain management. Fragmented distribution channels create opportunities for omnichannel strategies, blending digital discovery with physical experiences. Brands using online education to drive in-store sales exemplify this approach. Traditional beauty retailers are enhancing digital capabilities and forming exclusive partnerships, while new formats like subscription services and refill stations cater to evolving consumer preferences.

Geography Analysis

APAC Clean Beauty Market

In 2025, Asia-Pacific commands a 31.00% share of the global clean beauty market and stands out as the region with the fastest growth rate, anticipated to surge at a 12.11% CAGR through 2031. Diverse factors drive this leadership position: In India, a youthful demographic coupled with a heightened focus on ingredient safety propels market growth. Meanwhile, in the more established markets of Japan and South Korea, there's a pronounced emphasis on premium clean formulations and cutting-edge delivery systems. Furthermore, regulatory harmonization efforts, notably the 2024-2 updates to the ASEAN Cosmetic Directive, are streamlining market access. By standardizing ingredient restrictions, these regulations bolster the expansion of clean brands throughout Southeast Asia.

North America Clean Beauty Market

North America is witnessing a pivotal regulatory transformation, spurred by the Modernization of Cosmetics Regulation Act (MoCRA) and escalating state-level restrictions on PFAS in cosmetics. These developments are tightening compliance standards, benefitting clean beauty brands that champion transparency and stringent safety measures. Even amidst economic headwinds and supply chain disruptions, consumers remain steadfast in their commitment to health, sustainability, and ethical sourcing, propelling innovation in the clean beauty arena.

EMEA and South America Clean Beauty Market

Europe continues to set the regulatory benchmark. Here, heightened consumer awareness, combined with the EU Green Claims Directive, which demands scientific validation for environmental assertions, are propelling the clean beauty movement. This regulatory transparency not only bolsters the competitive stance of European brands but also shapes global benchmarks. Meanwhile, emerging markets in South America, the Middle East, and Africa are witnessing a surge in demand for safer, ethically-produced beauty products, driven by a burgeoning middle class. However, to navigate the distinct regional landscapes, brands must adopt tailored formulation and distribution strategies.

Competitive Landscape

The clean beauty market exhibits moderate fragmentation, creating substantial white-space opportunities for emerging brands that can navigate regulatory complexity while delivering authentic clean formulations. With clean beauty making its way into the mainstream, major beauty conglomerates are swiftly acquiring clean brands, hastening their entry into this burgeoning arena. Concurrently, independent brands are harnessing the power of digital platforms and social media, forging direct consumer relationships and carving out unique identities through purpose-driven branding.

Competition is being shaped by two primary strategies: global giants like Unilever, via its Prestige division, are expanding their portfolios through acquisitions, while companies such as L’Oréal are pursuing organic growth, channeling investments into biotech partnerships and cutting-edge formulation technologies. This strategic pivot underscores a wider industry trend: a move towards science-backed clean beauty, where the pillars of efficacy and safety are gaining parity with sustainability and transparency.

Technology stands out as a pivotal competitive tool, with AI-driven personalization and biotech ingredients not only boosting product performance but also upholding the core tenets of clean beauty. A case in point is L’Oréal’s partnership with IBM, crafting an AI model tailored for sustainable cosmetics, underscoring the blend of innovation with environmental stewardship. On another front, brands like Merit, rooted in digital platforms, are witnessing meteoric growth through direct-to-consumer strategies and a focused, minimalist product lineup, raking in revenues between USD 100 –USD 125 million. As smaller players consolidate, a vacuum emerges, allowing specialized brands to stake their claim in niche categories or specific demographic segments, thanks to their genuine positioning and nimble distribution tactics.

Clean Beauty Industry Leaders

-

L’Oréal SA

-

Unilever PLC

-

Coty Inc.

-

The Estee Lauder Companies Inc.

-

The Procter & Gamble Company

- *Disclaimer: Major Players sorted in no particular order

Clean Beauty Market Companies Covered in this Report

- L'Oreal S.A.

- Unilever PLC

- The Estee Lauder Companies Inc.

- The Procter & Gamble Company

- Coty Inc.

- L'Occitane International SA

- Shiseido Company, Limited

- Natura & co Holding SA.

- Beiersdorf AG

- Honest Company Inc.

- Kose Corporation

- Aramara Beauty LLC

- Beautycounter

- Amorepacific Corporation

- Weleda Group

- Honasa Consumer Ltd.

- Famille C Participations

- Pacifica Beauty LLC

- Herbivore Botanicals, LLC.

- Dr. Hauschka Skin Care Inc.

Recent Industry Developments in Clean Beauty Market

- May 2025: Juicy Chemistry’s new Juicy Actives line blends biotech with organic ingredients, offering clinical-grade efficacy in clean beauty. The launch marks a strategic shift to meet growing demand for science-backed natural skincare.

- January 2025: L'Oréal partnered with IBM to develop the first AI model for sustainable cosmetics, aimed at enhancing formulation processes and optimizing production while using renewable ingredients as part of L'Oréal's Digital Transformation Program.

- January 2025: Credo Beauty has entered the body care space with its first in-house line, Credo Body Care, a three-step system focused on hydration. Powered by fermentation, the range features ethically sourced sugar kelp extract, mineral-rich seawater, and a marine ferment blend, marking the retailer’s clean, science-driven approach to body care.

- December 2024: Estée Lauder Companies announced the establishment of a new biotech hub in Belgium to enhance capabilities in developing clean beauty products through innovative biotechnology solutions.

Global Clean Beauty Market Report Scope

Segmentation Overview

| Skincare |

| Haircare |

| Make-up and Colour Cosmetics |

| Fragrances |

| Bath and Shower |

| Other Products Types |

| Mass |

| Premium |

| Kids |

| Adults |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Skincare | |

| Haircare | ||

| Make-up and Colour Cosmetics | ||

| Fragrances | ||

| Bath and Shower | ||

| Other Products Types | ||

| By Price Tier | Mass | |

| Premium | ||

| By End User | Kids | |

| Adults | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the clean beauty market?

The clean beauty market is valued at USD 179.65 billion in 2026 and is forecast to reach USD 288.99 billion by 2031.

How does MoCRA impact the clean beauty industry?

MoCRA mandates facility registration, adverse-event reporting, and detailed ingredient listings, benefitting brands with robust compliance infrastructures.

Which region is growing fastest in the clean beauty market?

Asia-Pacific leads growth with a 12.11% CAGR, driven by India’s 15% annual expansion and rising premium demand in China, Japan, and South Korea.

Why are biotech-fermented actives important?

They deliver high performance while meeting clean standards, enable supply-chain resilience, and often lower the environmental footprint compared with agricultural extraction.

Are consumers willing to pay more for clean beauty?

Yes. The premium tier, though smaller, is growing at 11.74% CAGR, indicating shoppers will pay higher prices when efficacy and ethical sourcing align.

Page last updated on: