Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

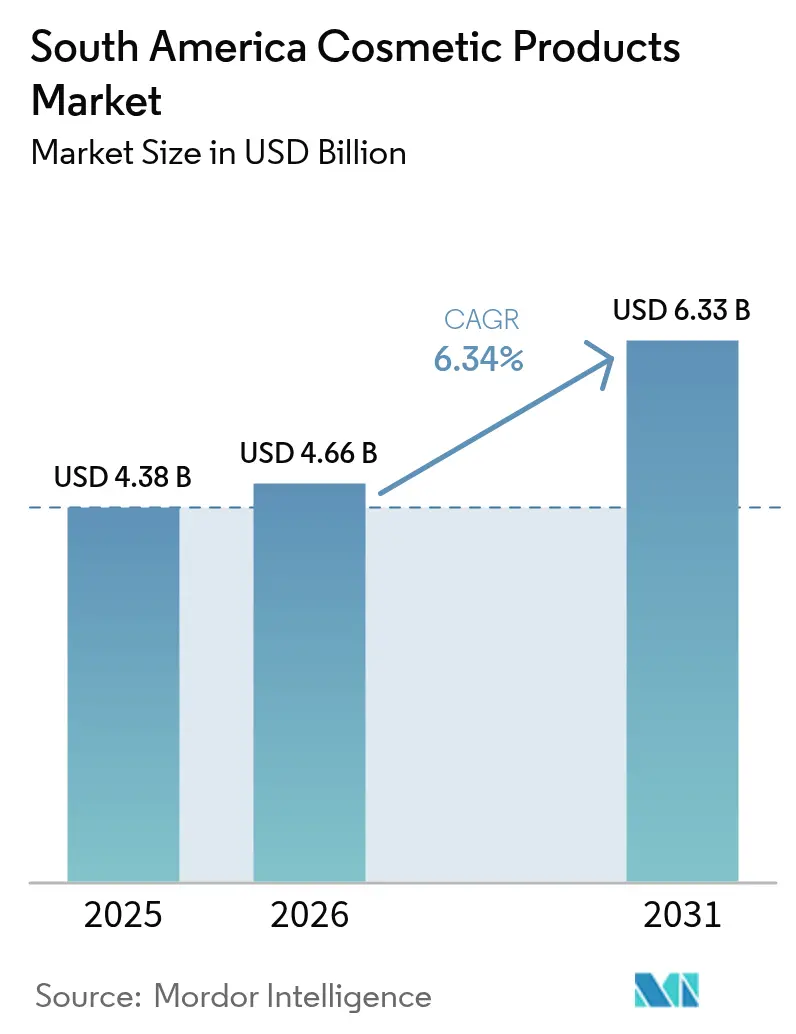

| Base Year Market Size (2025) | USD 4.38 Billion |

| Market Size (2026) | USD 4.66 Billion |

| Market Size (2031) | USD 6.33 Billion |

| Growth Rate (2026 - 2031) | 6.34% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Cosmetic Products Market Analysis by Mordor Intelligence

The South America cosmetic products market size in 2026 is estimated at USD 4.66 billion, growing from 2025 value of USD 4.38 billion with 2031 projections showing USD 6.33 billion, growing at 6.34% CAGR over 2026-2031. In South America, the cosmetic products market is experiencing a significant uptrend, driven by the widespread adoption of digital commerce, a growing emphasis on sustainability, and the introduction of premium product offerings. Brazil serves as the regional cornerstone, while Argentina contributes to the momentum. Both countries are benefiting from rising disposable incomes, the expansion of formal retail networks, and the rapid adoption of mobile-first shopping experiences. On the supply side, local industry leaders such as Natura and Co. are strategically leveraging biodiversity sourcing to minimize import-related risks. Meanwhile, multinational corporations like L’Oréal are investing heavily in research and development, particularly in AI-driven skin diagnostic technologies, to strengthen their market presence. As the South American cosmetic products market continues to enhance its omnichannel capabilities, the adoption of direct-to-consumer models and the implementation of micro-fulfillment pilots are optimizing inventory management, reducing working capital requirements, and accelerating product testing cycles.

Key Report Takeaways

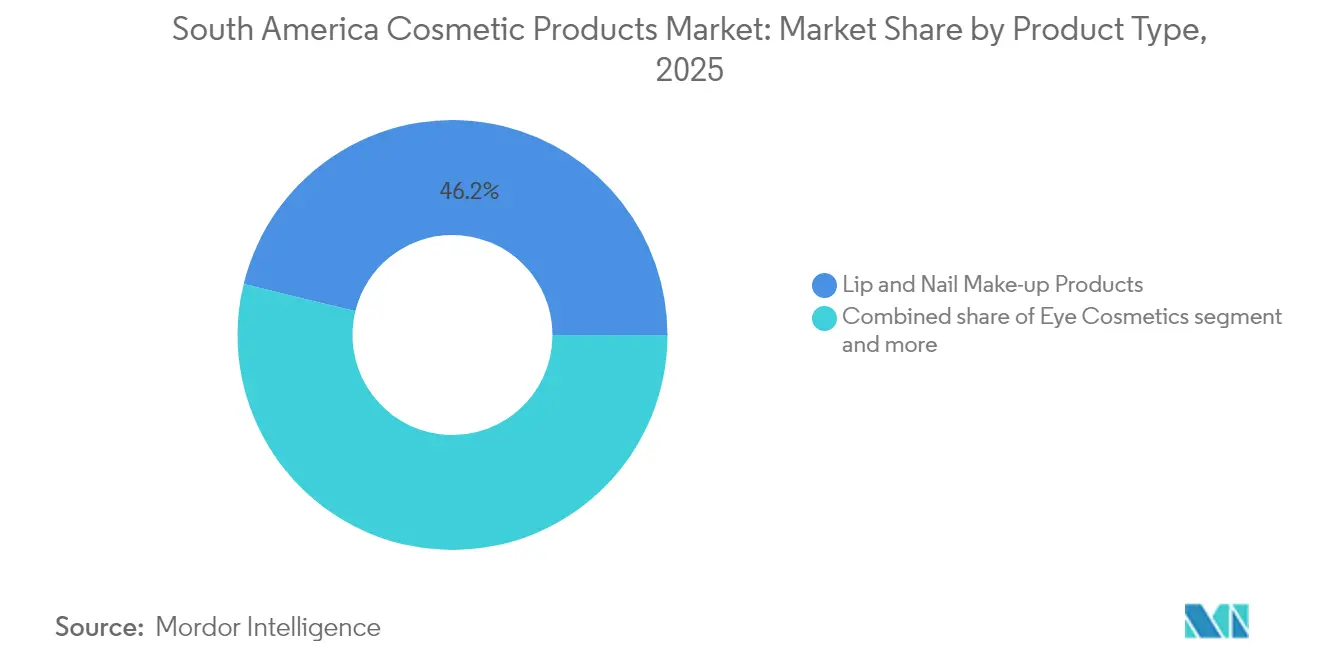

- By product type, lip and nail make-up led with 46.18% revenue share of the South American cosmetic products market in 2025, while eye cosmetics posted the fastest 6.72% CAGR forecast to 2031.

- By category, mass products held 90.98% of the South American cosmetic products market share in 2025; the premium tier is slated for a 7.05% CAGR to 2031.

- By ingredient type, conventional/synthetic lines captured 74.02% of the South American cosmetic products market size in 2025, and natural ingredients are expanding at a 7.44% CAGR through 2031.

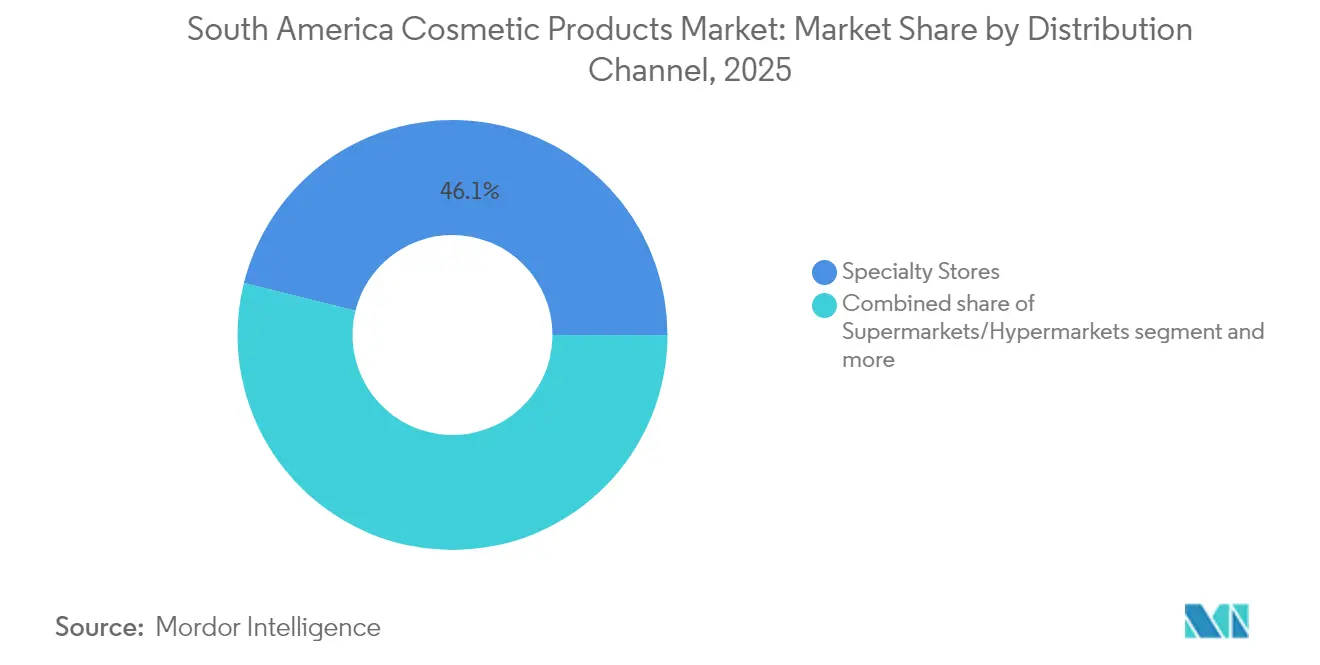

- By channel, specialty stores retained a 46.12% share of the South American cosmetic products market size in 2025, whereas online retail grew most quickly at 7.85% CAGR to 2031.

- By geography, Brazil commanded 60.88% of the South American cosmetic products market share in 2025; Argentina records the region’s highest 7.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South America Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Personalization-led product experience | +1.2% | Brazil, Chile | Long term (≥ 4 years) |

| Social-media and digital beauty trends | +1.0% | Brazil, Colombia | Short term (≤ 2 years) |

| Branding-centric marketing investments | +0.8% | Argentina, Chile | Medium term (2–4 years) |

| Rising disposable incomes and premium demand | +1.1% | Brazil, Peru | Long term (≥ 4 years) |

| E-commerce platform expansion | +1.3% | Brazil, Argentina | Medium term (2–4 years) |

| Sustainability and organic-cosmetics awareness | +0.9% | Chile, Uruguay | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing consumer focus on personalization and product experience

In South America, beauty personalization has evolved from shade matching to crafting entire rituals, blending products, digital services, and post-purchase interactions into an identity-affirming ecosystem. By analyzing detailed consumption patterns, brands streamline inventory, reducing SKU proliferation without sacrificing choice, thereby minimizing risk and freeing capital. Natura exemplifies this with its use of Amazonian botanicals, creating provenance narratives that resonate with regional pride and differentiate ingredient decks. Diagnostic tools, in-store or at-home, now craft tailored regimens, turning one-time shoppers into loyal subscribers. Brands target demographics like Gen Z and active-aging groups, enabling price variations without harming brand value. Consumers prioritize sensory elements texture, scent, packaging, alongside functionality, with premium textures, sustainable packaging, and appealing fragrances driving decisions. Inclusive products addressing diverse skin tones, hair types, and cultural preferences are in demand. Local and independent brands leverage this trend with hyper-targeted offerings celebrating Latin American heritage and diversity.

Influence of social media and digital beauty trends

Social platforms such as Instagram and TikTok have redefined the purchase funnel, shifting discovery and evaluation phases onto feeds that compress awareness and intent into a single scroll. Brazilian independent labels, for example, now routinely launch pilot runs below 10,000 units to test algorithmic traction before committing to full-scale manufacture. At the organisational level, digital intensity drives cross-functional hiring needs, content creators, data scientists, and supply chain analysts must coordinate under compressed timelines. The industry’s pivot toward influencer-led commerce also forces a re-think of intellectual property risk, as misalignment with contracted creators can inflict brand damage at a scale that traditional advertising seldom reached. In 2024, social media accounted for 81% of internet activities in Brazil, according to CETIC (Centre of Excellence in Information and Communication Technologies). This significant engagement is driving the influence of digital beauty trends in the region [1]Source: Centre of Excellence in Information and Communication Technologies, "ICT Households 2024", cetic.br.

Strong emphasis on branding and marketing activities

Brand storytelling in South America has shifted from purely aspirational imagery toward narratives of environmental and social accountability. Natura’s regenerative manifesto, which targets net-zero operational emissions by 2030, illustrates this transition; the company communicates not merely product benefits but their embedded social impact, thereby reframing purchase decisions as acts of collective participation. Brands optimize their campaigns by aligning them with regional cultures, languages, and beauty standards to enhance relevance and consumer engagement. Launching tailored campaigns during local festivals or incorporating regional dialects enables brands to establish stronger connections with their target audience. Highlighting local success stories and ensuring representation in advertisements fosters authenticity and inclusivity. By leveraging pop-up stores, in-store activations, and virtual reality tools, brands deliver impactful consumer experiences. These initiatives enable customers to engage with products before purchase, thereby increasing confidence and satisfaction. Additionally, interactive campaigns drive social sharing, expanding organic reach and brand visibility.

Rising disposable incomes drive demand for premium cosmetics

The rising middle class in South America is driving a significant shift toward premium cosmetic products, as consumers increasingly seek high-quality formulations that deliver superior performance and enhance social status. This premiumization trend is particularly pronounced in Brazil, Argentina, and Chile, where urban disposable incomes have grown faster than inflation, creating new consumer segments with a preference for prestige offerings. According to the Brazilian Institute of Geography and Statistics, Brazil's per capita household income reached BRL 2,069 in 2024 [2]Source: Brazilian Institute of Geography and Statistics, "Per capita household income 2024 for Brazil and federation units", igbe.gov.br. The premium beauty segment is expected to grow at a compound annual growth rate (CAGR) of 7.32% through 2030, significantly outpacing the overall market. This growth is driven by changing consumer perceptions, with cosmetic products increasingly viewed as investment items rather than disposable goods. Industry data indicates that first-time premium beauty buyers typically sustain their upgraded purchasing behavior even during economic downturns, ensuring consistent demand for higher-margin products. In response, mass-market players are introducing "masstige" products strategically positioned to bridge the gap between traditional and luxury segments, targeting consumers transitioning between these markets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory fragmentation across countries | - 0.8% | Brazil, Argentina | Long term (≥ 4 years) |

| Dependence on imported high-quality raw materials | - 0.6% | Chile, Peru | Medium term (2–4 years) |

| Limited access to advanced manufacturing technologies | - 0.5% | Colombia, Ecuador | Medium term (2–4 years) |

| Economic instability affecting purchasing power | - 1.2% | Argentina, Venezuela | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited regulatory harmonization across countries

South American countries, including Brazil, Argentina, Colombia, and Chile, enforce distinct regulatory frameworks for cosmetics, covering areas such as ingredient approvals, labeling requirements, testing protocols, and registration processes. For example, Brazil's Health Regulatory Agency (ANVISA) is increasing documentation requirements under its 2024-2025 agenda by revising e-labeling standards and safety certification pathways, favoring companies with larger compliance teams. Similarly, Argentina's ANMAT Resolution 155/98 maintains stringent registration protocols. The lack of harmonized standards creates a strategic advantage for companies that integrate compliance as a core capability, enabling them to turn regulatory fragmentation into a competitive barrier against resource-limited entrants. As a result, leading manufacturers are centralizing regulatory expertise within shared-service hubs that support multiple Latin American markets. This approach enhances operational efficiency and unlocks scale benefits often overlooked in cost-of-goods analyses.

Dependence on imports for high-quality raw materials

The region's reliance on imported active ingredients and specialty chemicals exposes it to significant operational risks, including currency fluctuations and supply chain disruptions. However, companies like Natura have addressed this challenge by sourcing bio-ingredients from Amazonian communities. This approach not only reduces foreign currency exposure but also integrates social enterprise principles into their supply chains. Additionally, it generates intellectual property through patented botanical extracts under benefit-sharing agreements, turning these patents into valuable licensing assets. This strategy demonstrates how vertical integration into raw material sourcing can shift bargaining power within the supplier ecosystem, enabling brands to enhance formulation differentiation and manage costs more effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lip and Nail Staples Out-earn; Eye Innovations Out-run

In 2025, lip and nail make-up products accounted for 46.18% of South America's cosmetic products market, driven by their low unit prices and rapid replenishment cycles. Impulse purchases at drugstores and the emergence of hybrid polish formulas, which promise week-long wear without the need for UV lamps, bolster this segment. While eye cosmetics hold a smaller market share, they are projected to grow at a 6.72% CAGR through 2031. This growth is fueled by post-mask consumers gravitating towards expressive brows, lightweight mascaras, and transfer-proof liners. Furthermore, digital try-on features in eye sub-segments have led to a threefold increase in click-to-cart ratios on brand apps.

Further analysis of secondary market effects reveals that the rising sales of long-wear eye pigments are directly influencing the demand for complementary cleansing SKUs. Retailers are capitalizing on this trend by bundling waterproof makeup removers with mascara promotions, thereby enhancing cross-selling opportunities. Moreover, the growing emphasis on eye-area microbiome care is enabling brands to position themselves strategically within the premium skincare segment. This approach is effectively dissolving traditional category boundaries, fostering a more integrated and dynamic competitive landscape within the South American cosmetic products market.

By Category: Mass Dominance with Premium Acceleration

In 2025, mass products dominate the South American cosmetic products market, accounting for a substantial 90.98% market share. This overwhelming dominance reflects the socioeconomic dynamics of the region and highlights the strategic prioritization of affordability by leading market players. In particular, Brazil exemplifies this trend, where prominent domestic companies such as Natura and Grupo Boticário have developed extensive and efficient distribution networks. These networks enable them to cater to consumers across diverse income groups, ensuring widespread accessibility to their products.

Meanwhile, the premium segment is emerging as a significant growth driver, with a projected CAGR of 7.05% through 2031. This robust growth trajectory indicates a notable shift in consumer preferences, fueled by increasing disposable incomes and a growing emphasis on beauty and personal care. The expansion of the premium segment is most evident in urban centers across Argentina, Chile, and Brazil. In these markets, international luxury brands are actively enhancing their presence by investing in both physical retail outlets and digital platforms. This strategic expansion aims to capture the attention and spending power of the region's rapidly growing affluent consumer base.

By Ingredient Type: Natural Formulas Break Out from Niche to Norm

Conventional/synthetic formats reached 74.02% of the South American cosmetic products market share in 2025, and natural and organic products pursued a 7.44% CAGR. This growth surpasses that of conventional synthetics, which continue to dominate in terms of volume. The expansion is driven by increasing consumer concerns over endocrine-disrupting chemicals and the region's emphasis on its biodiversity. Companies are leveraging ingredients such as Amazonian cupuaçu butter and Andean quinoa peptides, creating provenance-driven narratives that support a 15-20% price premium. Certification seals like Ecocert are enhancing conversion rates in Chilean specialty retail chains, highlighting the role of third-party verification in influencing consumer purchasing behavior.

The shift toward natural and organic products is also creating significant supply chain implications. Raw-material lead times are closely linked to harvest cycles, compelling businesses to integrate agronomy data into their demand planning strategies. Failure to secure a consistent supply of raw materials can result in back-order challenges, which may negatively impact e-commerce rankings and overall brand performance. To address these risks, companies are entering into multi-year offtake agreements with local cooperatives. These agreements not only ensure a stable supply of raw materials but also help mitigate environmental, social, and governance (ESG) risks. By adopting such proactive measures, businesses are strengthening their competitive positioning and establishing first-mover advantages within South America's cosmetic products market.

By Distribution Channel: Digital Acceleration Reshaping Retail Landscape

In 2025, specialty stores dominate the distribution channel, capturing a 46.12% market share. Their performance is driven by curated product assortments, tailored customer service, and the ability to deliver immersive brand experiences. These retailers excel in markets like Brazil and Colombia, where the beauty industry prioritizes product exploration and expert consultation. The channel's prominence is further supported by the sensory and emotional aspects of cosmetics purchases, as consumers place significant value on testing products before making a purchase.

Online retail stores are experiencing significant growth, with a projected CAGR of 7.85% through 2031. This growth is reshaping the competitive landscape, as consumers increasingly prefer e-commerce for its convenience, extensive product range, and transparent pricing. As of 2023, over 84.15% of Brazil's population accessed the internet, positioning the country as a major player in the global online market . This digital penetration strengthens Brazil's online retail channels. Key drivers of this trend include advancements in digital payment systems, innovative product visualization tools, and the growing influence of social media on purchasing behavior.

Geography Analysis

In 2025, Brazil holds a commanding 60.88% share of sales, driven by well-established manufacturing clusters and e-commerce penetration. Regulatory developments, such as Lei 15.022 introducing a chemicals inventory, enhance traceability standards and encourage the adoption of advanced enterprise resource planning systems. The market demonstrates technological maturity, with augmented-reality shade trials in São Paulo malls increasing sales by 18%, a metric now utilized in landlord lease negotiations to highlight traffic value.

Argentina, while contributing a smaller sales base, is projected to lead growth with a 7.56% CAGR through 2031, supported by affluent urban areas and a strong inclination toward beauty spending. Currency instability is shifting mid-range consumers toward value-focused mass-market products, but premium demand remains strong among affluent consumers, particularly in dermocosmetics. Companies developing hydrating products tailored to Buenos Aires’s humidity variations achieve faster inventory turnover, showcasing the impact of climate-specific research and development in the South American beauty market.

Chile, Colombia, and Peru complete the regional growth landscape. Natura’s mature franchise model in these markets reduces capital requirements while enhancing local adaptability, enabling rapid adjustments to product assortments based on regional skin-tone preferences. In Colombia, department-store kiosks report a significant increase in shopper engagement time due to the integration of AI skin scanners with loyalty programs, demonstrating the competitive advantage of data-driven solutions in physical retail.

Regulatory Landscape

South America cosmetics regulation is split across national rulebooks, with two main regional blocs covering MERCOSUR (including Brazil and Argentina) and the Andean Community (including Colombia, Ecuador, Peru, and Bolivia). In Brazil, ANVISA updated the operational rulebook with RDC 907/2024, which governs cosmetics classification, labeling, and technical procedures, and reinforced post-market safety controls via RDC 894/2024, which requires reporting serious adverse events through the Notivisa cosmetovigilance system. These changes raise documentation and surveillance expectations for mass and premium portfolios, particularly for multinational brands running multi-country SKU strategies.

Cross-border compliance is also influenced by ingredient-list convergence and the timing of country-by-country implementation. Argentina, through ANMAT, incorporated MERCOSUR GMC Resolutions 06/25 and 07/25 via Provisions 2599/2026 and 2601/2026 (published May 21, 2026), updating prohibited and restricted substance lists. For Andean markets, Decision 833 (2018) remains the harmonized basis, centered on mandatory sanitary notifications (NSO) with multi-year validity. Brazil also introduced a simplified pathway for small producers via Law 15.154 (published June 30, 2025), which provides simplified rules and registration exemptions for defined artisanal cosmetics, personal hygiene products, and perfumes.

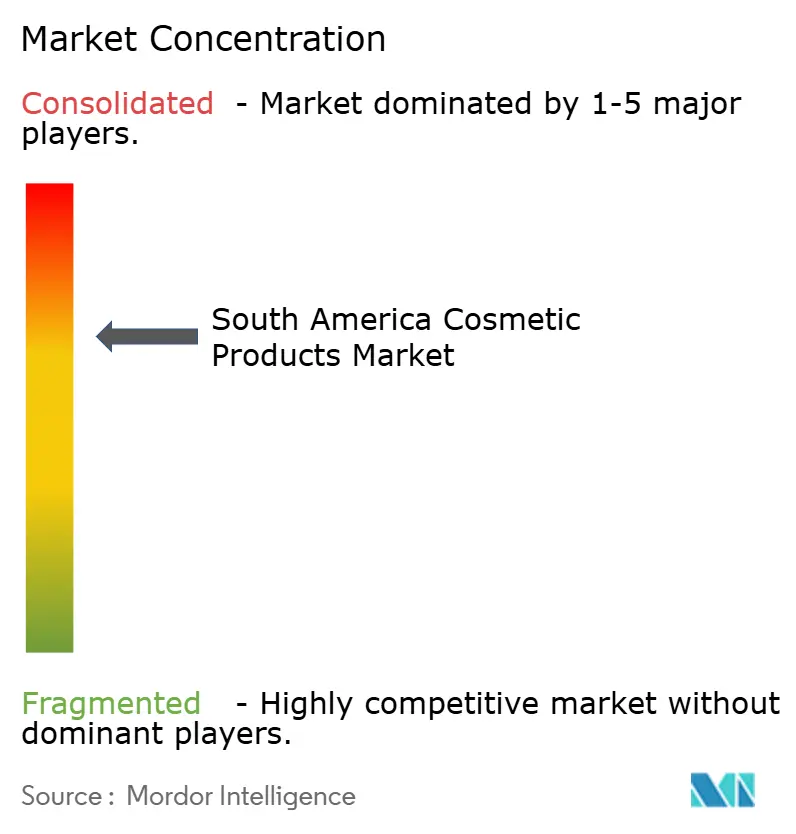

Competitive Landscape

The South American cosmetic products market is moderately consolidated. Key players in the market, including L'Oreal S.A., Shiseido Co. Ltd, Natura and Company, the Estée Lauder Companies Inc., and LVMH Moet Hennessy Louis Vuitton , maintain a strong market presence. These companies focus on product innovation as a primary strategy to differentiate themselves, attract new customers, and solidify their market position. In addition to innovation, they leverage mergers and acquisitions to enhance their competitive advantage. These initiatives enable firms to expand their customer base, increase geographic reach, enter new markets, and strengthen their presence in underserved regions.

Grupo Boticário is strategically expanding into the men’s grooming segment, as demonstrated by its acquisition of Dr. Jones, aimed at accelerating online revenue growth. L’Oréal is reinforcing its technological leadership by channeling significant resources through its Research and Innovation hub into biodegradable polymers and artificial intelligence. Unilever’s legal action against Boticário highlights the importance of packaging design as a defendable intellectual property asset, reflecting the increasing role of litigation in shaping competitive strategies.

Capital allocation trends indicate a shift from physical store expansions to investments in digital infrastructure. In April 2025, Natura allocated restructuring funds to scale its micro-fulfillment networks across metropolitan Brazil, targeting delivery times of under 24 hours. Meanwhile, Estée Lauder’s USD 1.6 billion turnaround plan prioritizes supply chain optimization, underscoring the growing importance of inventory precision alongside marketing efforts as key drivers of profitability.

South America Cosmetic Products Industry Leaders

-

Shiseido Company, Limited

-

The Estée Lauder Companies Inc.

-

Natura and Company

-

L'Oreal S.A

-

LVMH Moet Hennessy Louis Vuitton

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory-driven formulation upgrades and claim substantiation create room for compliant, region-scaled product platforms. Chile implemented Law 21.646 in January 2025, banning the import and sale of cosmetic products or ingredients tested on animals after that date, which increases demand for alternative safety assessment approaches and accelerates reformulation and supplier qualification across portfolios sold in Chile. At the same time, MERCOSUR-aligned ingredient restrictions are being refreshed through national instruments such as ANMAT Provisions 2599/2026 and 2601/2026 (May 2026) and ANVISA RDC 1,030/2026 (June 2026), favoring companies that can update restricted-substance screening, INCI-based labeling controls, and documentation quickly across Brazil-Argentina trade corridors.

Manufacturing localization and faster replenishment models provide tangible levers as brands expand omnichannel assortments and shorten launch-test cycles. In Brazil, capacity and footprint moves such as Flora acquiring a manufacturing facility in Cesario Lange (Sao Paulo) in March 2026, and Grupo Boticario announcing an investment of BRL 1.8 billion for a new factory in Pouso Alegre (MG) in December 2024 (designed for high-volume output), point to continued local supply build-out to reduce lead times and improve service levels. Upstream fragrance capacity additions in Latin America, including Givaudan beginning construction of a USD 110 million fragrance manufacturing facility in Pedro Escobedo, Mexico in June 2026, also support shorter regional sourcing cycles for fragrance-intensive categories, which aligns with South American launches emphasizing sensorial differentiation and premiumization.

Recent Industry Developments

- July 2026: Advent International finalized the build-up of an 8% economic position in Natura through share and derivative holdings. The transaction added an institutional backer as Natura refocuses on Latin America, strengthening access to capital and governance support during portfolio and operating-model changes.

- April 2026: L'Oreal confirmed a mandate for a share buyback program to be executed between April 2026 and June 2026, with a maximum value of EUR 500 million. The action reinforces capital-return capacity while maintaining strategic flexibility for brand investment and regional operating priorities in markets such as South America.

- August 2024: L'Oreal outlined plans to strengthen Colombia as a major makeup production hub for brands including Vogue, Maybelline, NYX, and L'Oreal Paris. Expanding regional manufacturing capability supports faster replenishment and localized assortment strategies for South American retail and e-commerce channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the value of cosmetics and grooming products sold in South America, counted at the point of sale into the market and expressed in USD. It includes products used to clean, improve, or change the appearance of skin, hair, nails, and related grooming use.

Scope exclusions: We exclude professional salon service revenues and beauty devices, and we also do not count illegal or untracked imports that are not captured in official trade signals.

Segmentation Overview

-

By Product Type

- Facial Cosmetics

- Eye Cosmetics

- Lip and Nail Make-up Products

-

By Category

- Premium Products

- Mass Products

-

By Ingredient Type

- Natural and Organic

- Conventional/Synthetic

-

By Distribution Channel

- Specialty Stores

- Supermarkets/Hypermarkets

- Online Retail Stores

- Other Distribution Channels

-

By Country

- Brazil

- Argentina

- Chile

- Colombia

- Peru

- Rest of South America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to anchor the model to repeatable public data series. We reviewed official statistics and reference points such as national statistics offices and central bank publications across key South American countries, along with UN Comtrade for import and export values tied to cosmetics related product codes.

To keep assumptions realistic, we also checked consumer price inflation series, household spending indicators, and retail trade signals published by public agencies, followed by industry bodies and regulatory portals that describe product definitions and labeling rules. Company filings, investor presentations, and trusted press coverage were then used to understand channel shifts, pricing direction, and category focus. Where public disclosure was thin, we used a paid subscription for company financials and a shipment-level trade database only to cross-check company exposure and country trade flows. These desk sources are illustrative, and we relied on other public references for data collection, validation, and clarification as well.

Primary Interviews and Surveys

Primary interviews and surveys were used to test what the desk signals could not fully explain, especially pricing ladders, channel mix changes, and the pace of premiumization versus mass demand. We spoke with a mix of brand-side managers, distribution and retail channel leaders, and participants from the ingredient and packaging ecosystem, plus local market specialists across South America, so that country differences did not get averaged out too early.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 46% |

| Mid tier: 50% | Functional/Unit leaders: 41% | EMEA: 33% |

| Smaller Players: 14% | Managers: 45% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where country-level consumption is reconstructed using a demand-pool lens, then split across cosmetics categories and channels using observed mix patterns. To keep the totals honest, the result is corroborated with selective bottom-up approximations, such as sampled price points across mass and premium ranges, channel checks on online versus store-led sales, and sanity checks using supplier and distributor revenue exposure.

Inputs that shaped the model (illustrative, not exhaustive) included cosmetics import values and unit price direction, consumer price inflation for beauty and personal care baskets, retail and e-commerce growth signals, premium versus mass mix shifts, and country-level currency movement timing for USD conversion. Forecasts were produced using scenario analysis supported by interview feedback, with trading-down risk, premium growth, and channel expansion as the key variables that were stressed. When gaps appeared in country or category splits, we used conservative proxy weights from the closest comparable markets, then re-tested them in follow-up calls before locking assumptions.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including trade flows, price movement, and retail growth direction, and then reviewed for unusual jumps by country, category, or channel. If a variance cannot be explained by an input change, we re-check the underlying series, revisit conversion timing, and re-contact sources to confirm whether a real market shift occurred.

Before sign-off, the work goes through a multi-step analyst review so that scope boundaries, math, and assumptions are consistent across the dataset. The report is refreshed annually, and interim updates are made when a material event changes pricing, trade access, or demand behavior. Right before delivery, a fresh pass is done so clients receive the most current view available at that time.

Mordor Intelligence's South America Cosmetics Products Market Market Estimate Compared With Other Published Estimates

Published market sizes for South America cosmetics products do not always align, because each publisher applies its own product boundaries, year coverage, and currency handling. Differences also show up when some studies lean more on brand revenue roll-ups, while others rely more on trade and consumption signals.

By tracking import-value direction, consumer price inflation, and currency-conversion timing, Mordor Intelligence keeps the 2025 total tied to a consistent South America-only demand pool, which reduces the chance of counting broader personal care baskets or double counting cross-border flows.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.38 B (2025) | |

| Regional Consultancy A | USD 8.21 B (2023) | The scope appears to use a broader beauty and personal care basket in parts of the sizing, and the earlier base year can lock in a different price level and exchange-rate window than a 2025 USD conversion. |

| Industry Publisher B | USD 26.46 B (2026) | This estimate is built for Latin America, not South America, so it brings in additional geographies and demand pools that inflate the regional total when compared on a like-for-like basis. |

The spread mainly comes from geography boundaries and what gets counted as cosmetics versus a wider personal care set, followed by year selection and currency timing. With clear scope rules and repeatable checks tied to trade, pricing, and channel signals, the final number stays easier to trace and explain when decisions need a stable reference.

Key Questions Answered in the Report

What is the South America cosmetic products market worth in 2026?

The South America cosmetic products market is valued at USD 4.66 billion in 2026.

How fast will the South America cosmetic products market grow through 2031?

It is forecast to expand at a 6.34% CAGR, reaching USD 6.33 billion by 2031.

Which country dominates the South America cosmetic products market?

Brazil leads with 60.88% revenue share in 2025 thanks to extensive domestic production and high digital engagement.

Why are natural formulations important to regional growth?

Natural/organic lines grow faster than synthetics at a 7.44% CAGR, because consumers prioritize sustainable sourcing and clean-label transparency.

Page last updated on: