Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

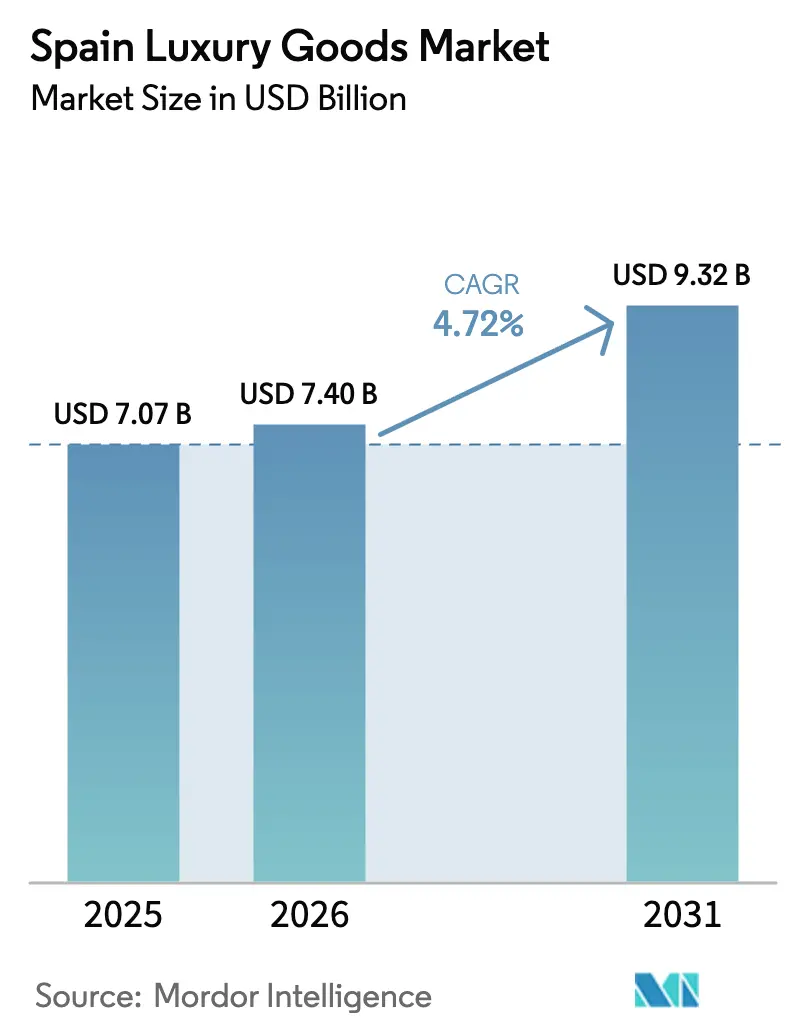

| Base Year Market Size (2025) | USD 7.07 Billion |

| Market Size (2026) | USD 7.4 Billion |

| Market Size (2031) | USD 9.32 Billion |

| Growth Rate (2026 - 2031) | 4.72% CAGR |

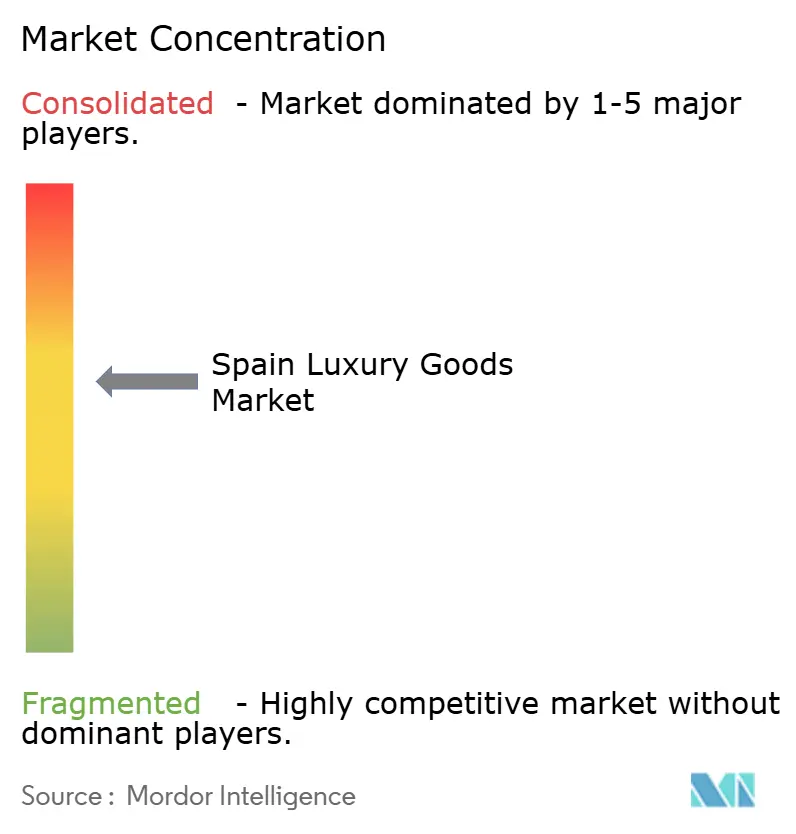

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Luxury Goods Market Analysis by Mordor Intelligence

Spain luxury goods market size in 2026 is estimated at USD 7.4 billion, growing from 2025 value of USD 7.07 billion with 2031 projections showing USD 9.32 billion, growing at 4.72% CAGR over 2026-2031. Resilient domestic demand and strong tourism inflows, especially from affluent travelers drawn to Spain's fashion heritage and luxury retail hubs like Madrid and Barcelona, are key drivers of this growth. Iconic Spanish brands, supported by the presence of international luxury houses, play a significant role in solidifying the market's stature and appeal. With rising disposable incomes, consumers are increasingly able to invest in high-end products, while the rapid expansion of e-commerce platforms provides greater accessibility to luxury offerings. Consumer preferences are evolving, with a growing demand for personalized, sustainable, and innovative luxury products that cater to unique tastes and values. Furthermore, increased investments in luxury retail infrastructure and the introduction of premium experiential offerings, such as exclusive in-store events and tailored services, enhance Spain's reputation as Europe's premier luxury shopping destination.

Key Report Takeaways

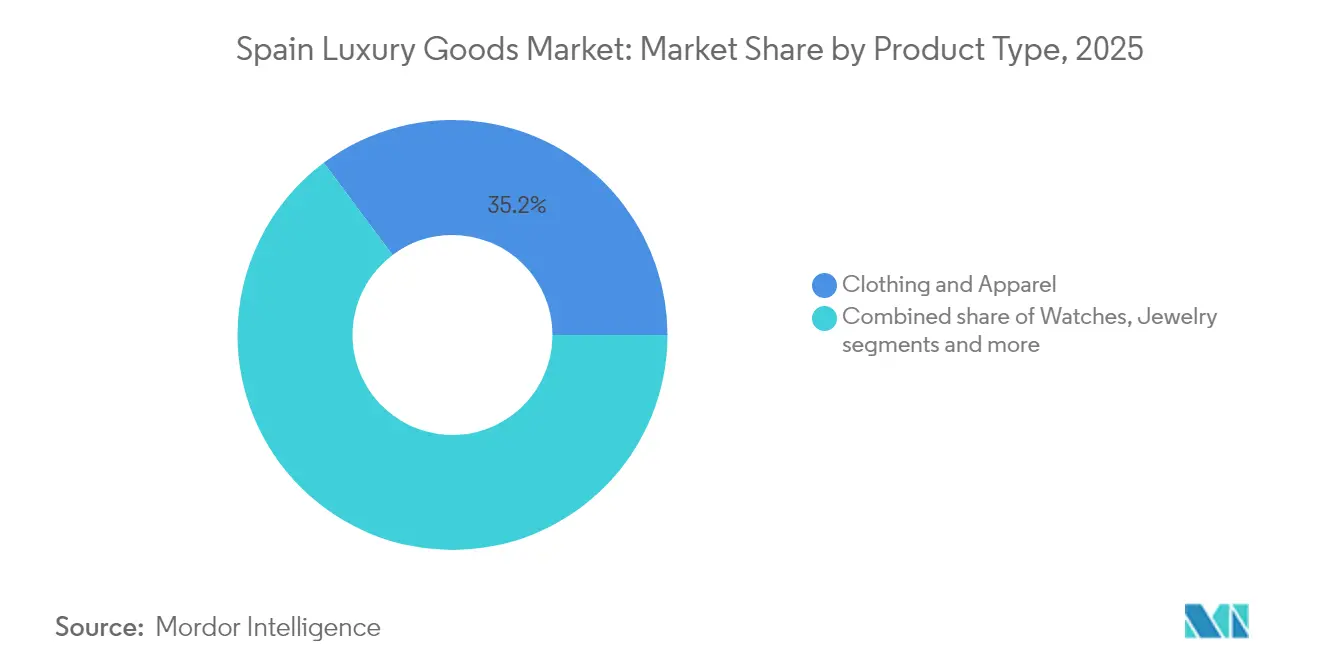

- By product type, Clothing and apparel led with 35.22% of the Spain luxury goods market share in 2025, while Watches posted the fastest 5.12% CAGR to 2031.

- By end user, Women held 55.88% of the Spain luxury goods market in 2025; Men’s spending is forecast to expand at a 4.98% CAGR through 2031.

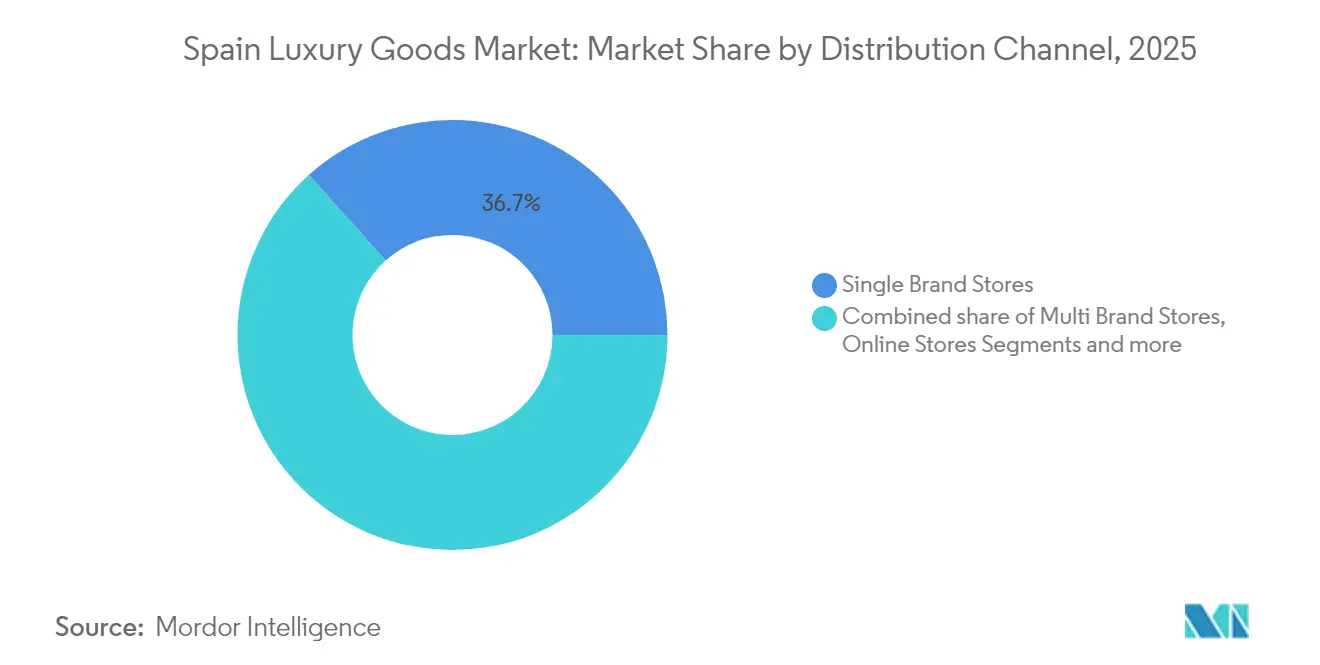

- By distribution channel, Single-brand stores captured 36.65% of 2025 sales, whereas online stores are projected to advance at a 6.84% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing affluent and high-net-worth individual base | +0.9% | National, concentrated in Madrid, Barcelona, Valencia, Marbella | Medium term (2-4 years) |

| Increasing brand consciousness and prestige demand | +0.8% | National, with spillover to Balearic and Canary Islands resort markets | Short term (≤ 2 years) |

| Personalization and premiumization in fashion, jewelry, cosmetics | +0.7% | National, early adoption in Barcelona and Madrid luxury districts | Medium term (2-4 years) |

| Influence of social media and celebrity endorsements | +0.6% | National, strongest among Gen Z and Millennials in urban centers | Short term (≤ 2 years) |

| Demand for experiential and immersive luxury offerings | +0.5% | Madrid, Barcelona, with expansion to Palma de Mallorca, Ibiza | Medium term (2-4 years) |

| Trends toward sustainability and ethical luxury products | +0.4% | National, driven by EU regulations and consumer preferences | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing affluent and high-net-worth individual base

Growing numbers of affluent and high‑net‑worth individuals in Spain are a fundamental demand driver for the country’s luxury goods market. As private wealth rises, this segment allocates a larger share of spending to discretionary categories such as designer fashion, leather goods, fine jewelry, and premium watches. Wealth concentration in Spain’s top 1% increased from 22.1% of total household net worth in 2020 to 24.3% in 2024, expanding the addressable base for ultra‑premium niches like haute joaillerie, bespoke tailoring, and made‑to‑measure accessories [1]Source: Bancode Espana Eurosistema, "Spanish Survey of Household Finances", app.bde.es . This concentrated purchasing power is especially visible in hubs such as Madrid and Barcelona, where it supports a dense network of flagships and high‑service boutiques. High‑net‑worth clientele are relatively insulated from short‑term macroeconomic volatility, providing a resilient revenue stream when mass‑market demand softens. They also seek exclusivity, limited editions, and personalized experiences, encouraging brands to invest in VIP lounges, private events, and concierge‑style services.

Increasing brand consciousness and prestige demand

Increasing brand consciousness and prestige demand are key forces propelling Spain’s luxury goods market, as consumers place greater value on labels that signal status, taste, and social distinction. Exposure to global fashion trends through social media, influencers, and international travel has heightened awareness of leading maisons and sharpened preferences for recognizable logos and signature designs. Younger affluent shoppers, in particular, view luxury purchases as expressions of identity and lifestyle, driving interest in statement handbags, sneakers, and accessories. At the same time, more mature clients continue to prioritize craftsmanship, heritage, and timeless pieces, reinforcing the appeal of established European and Spanish brands. This rising prestige orientation is evident in the willingness to pay premiums for limited editions, collaborations, and exclusive in-store experiences.

Personalization and premiumization in fashion, jewelry, cosmetics

Personalization and premiumization across fashion, jewelry, and cosmetics are powerful growth levers for Spain’s luxury goods market, as consumers increasingly seek products and experiences that feel unique to them rather than mass-produced. Clients are gravitating toward monogrammed leather goods, made-to-measure tailoring, and customizable fine jewelry that allow them to co-create designs and express individual identity. In beauty, demand is rising for personalized shade matching, engraved packaging, and bespoke fragrance blending that elevate cosmetics from routine purchases to collectible objects. Hermès illustrates this monetization of customization in Spain: in 2024, 34% of its Spanish sales involved some form of personalization, from hand-painted Birkin bags to made-to-measure silk scarves, with average transaction values 2.3 times higher than standard ready-to-wear purchases [2]Source: Hermès International S.A. "Hermes: Annual Report-2024", hermes.com. Such high-touch services deepen emotional attachment, justify premium pricing, and drive higher spend per client visit.

Influence of social media and celebrity endorsements

Influence of social media and celebrity endorsements is a critical demand driver for Spain’s luxury goods market, as digital platforms shape brand awareness, aspiration, and purchase intent among local and international consumers. Constant exposure to luxury lifestyles on Instagram, TikTok, and YouTube encourages younger, image-conscious shoppers to emulate the styles of celebrities, athletes, and influencers. Collaborations between global maisons and Spanish or Latin talent amplify relevance, linking products to aspirational narratives around success, creativity, and exclusivity. Branded content, livestreams, and “get ready with me” formats allow audiences to see how luxury items fit into everyday life, lowering psychological barriers to first-time purchases. User-generated content and influencer reviews also serve as powerful social proof, reinforcing perceptions of quality and desirability. According to Ministry of Industry and Tourism, more 82.8 million international travellers have visited Spain in the first ten months of 2024, 10.8% more than the same period last year [3]Source: Ministry of Industry and Tourism, "News of the ministry 2024", mintur.gob.es. For tourists visiting Madrid, Barcelona, Ibiza, and Marbella, seeing the same brands and ambassadors online and in flagship locations strengthens the urge to buy while traveling.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prevalence of counterfeit products | -0.6% | National, concentrated in Madrid, Barcelona, Valencia street markets | Short term (≤ 2 years) |

| Intense competition from established and emerging brands | -0.5% | National, most acute in Clothing and Apparel and Footwear segments | Medium term (2-4 years) |

| Luxury taxes and import duties/VAT regulations | -0.4% | National, with higher impact on cross-border e-commerce | Medium term (2-4 years) |

| Economic volatility and downturn risks | -0.3% | National, with regional variation tied to tourism flows | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Prevalence of counterfeit products

The prevalence of counterfeit luxury goods in Spain significantly restrains the luxury market by undermining brand authenticity and consumer confidence. Counterfeit products, sold at a fraction of the genuine price, are widely available and cater to consumers seeking to express social status affordably, which dilutes the exclusivity traditionally associated with luxury brands. This broad accessibility challenges the controlled distribution strategies of luxury brands, making it difficult for them to maintain their premium positioning. The presence of counterfeit items also negatively impacts brand perception, as consumers associate these fake products with lower quality, which can harm the reputation of genuine luxury labels. Furthermore, counterfeiting disrupts the market by fostering unfair competition, reducing the market share of authentic goods, and leading to financial losses for luxury brands.

Intense competition from established and emerging brands

The luxury goods market in Spain experiences intense competition from both established multinational conglomerates and emerging niche brands. Major players like LVMH, Kering, Prada, and Hermès dominate the market, leveraging strong brand images, extensive distribution networks, and ongoing mergers or acquisitions to maintain and expand their market shares. Meanwhile, emerging brands focus on differentiation through unique product offerings, personalized experiences, and regional craftsmanship, adding diversity and vibrancy to the market. This competitive landscape drives continuous innovation, compelling all players to prioritize digital transformation, including luxury e-commerce, which is growing rapidly and appealing especially to younger consumers. The competition also intensifies through aggressive marketing and product development strategies aimed at capturing Spain’s increasing affluent consumer base and tourist-driven demand. The resulting market dynamics pressure brands on pricing, exclusivity, and consumer engagement, influencing luxury goods' positioning and growth prospects.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Watches Outpace Apparel on Scarcity and Collectibility

Clothing and apparel represented the largest segment of Spain’s luxury goods market in 2025, accounting for 35.22% of the total market share. The category maintained its dominance due to the strong presence of well-established European fashion houses and the continued appeal of high-end designer labels among affluent consumers. Premium clothing in Spain also benefits from high tourist spending and brand-conscious local consumers seeking exclusivity and craftsmanship. Luxury apparel collections, including seasonal and limited-edition designs, continue to drive repeat purchases and enhance brand equity. The rise of online luxury retail platforms and flagship store experiences has further broadened consumer access to global fashion trends.

Watches, while a smaller segment by value, is recording the fastest expansion among luxury product categories, with a compound annual growth rate of 5.12% expected through 2031. This growth reflects the transformation of mechanical watches from everyday timepieces into collectible, investment-grade assets. Rising consumer appreciation for craftsmanship, mechanical innovation, and brand heritage has made luxury watches increasingly desirable as symbols of status and financial value. Limited editions and vintage models have gained traction among collectors and investors seeking both prestige and long-term appreciation potential. The pre-owned and boutique watch markets are also contributing to growth, offering consumers access to exclusive pieces.

By End User: Men's Segment Gains Share Through Category Expansion

Women accounted for the largest share of Spain’s luxury goods market in 2025, commanding 55.88% of total market value. This dominance reflects the strong influence of female consumers in driving demand for high-end fashion, accessories, beauty products, and handbags. Established luxury brands continue to focus heavily on women’s collections, leveraging brand heritage, design innovation, and exclusivity to attract and retain loyal clientele. Increased participation of women in the workforce and rising disposable incomes have also strengthened their purchasing power, further boosting market growth. The trend toward self-expression and individuality has led to greater spending on statement pieces and personalized luxury items.

Men’s luxury goods, while representing a smaller share of the market, are expanding at a robust compound annual growth rate of 4.98% between 2025 and 2031, marking the fastest growth across gender segments. The rise of modern masculinity and shifting attitudes toward style and grooming have driven greater interest in premium apparel, watches, fragrances, and accessories among male consumers. Luxury brands are increasingly investing in men’s lines, offering tailored designs and exclusive collections that emphasize sophistication and individuality. The influence of social media and celebrity-driven fashion trends has further accelerated awareness and aspiration in this segment. Younger male consumers, in particular, are expressing a growing preference for high-end craftsmanship and understated luxury.

By Distribution Channel: Online Stores Surge on Omnichannel Integration

Single-brand stores accounted for the largest share of Spain’s luxury goods market in 2025, representing 36.65% of total revenue. These stores have remained central to luxury retail by offering immersive brand experiences, personalized services, and exclusive product lines. The physical presence of luxury boutiques in prime shopping districts such as Madrid and Barcelona continues to attract both domestic and international shoppers. Consumers value the opportunity to interact directly with brand heritage, craftsmanship, and in-store exclusivity, which reinforces brand loyalty and perceived value. Additionally, luxury houses leverage flagship stores as key touchpoints for curated marketing events, limited-edition launches, and high-end client engagement. As a result, single-brand stores maintain their position as the foundation of Spain’s luxury retail landscape, blending tradition with experience-driven retailing.

Online stores, although currently smaller in market share, are expected to record the fastest expansion in the luxury market, growing at a compound annual rate of 6.84% through 2031. The acceleration of digital transformation and the integration of virtual shopping platforms have reshaped how Spanish consumers access and purchase luxury products. E-commerce offers convenience, accessibility, and a wider product range, attracting younger, digitally savvy shoppers who value both authenticity and personalization. Leading brands have enhanced their online presence through virtual try-ons, live consultations, and exclusive digital collections that mirror the in-store luxury experience. The growing popularity of luxury resale platforms and cross-border online purchases has also fueled this momentum.

Geography Analysis

Madrid serves as Spain's unrivaled epicenter for luxury goods, drawing affluent residents and global tourists to its prestigious Salamanca district. The Golden Mile along Calle Serrano features an unparalleled concentration of flagship boutiques, offering immersive brand experiences and personalized services. High disposable incomes among locals foster consistent demand for premium fashion and accessories, while international visitors from emerging markets enhance vibrancy. Cultural events and exclusive launches in these stores cultivate deep brand loyalty and prestige. Madrid's sophisticated infrastructure and central location solidify its role as the benchmark for luxury retail excellence. This dominance reflects a blend of economic strength and aspirational consumer culture.

Barcelona thrives as a vibrant secondary hub, propelled by its cosmopolitan allure and surging high-end tourism. Passeig de Gràcia hosts expanding luxury retail with innovative experiential formats that appeal to diverse demographics. Local wealth complements influxes of international shoppers seeking unique Mediterranean-inspired luxury. The city's post-pandemic recovery has amplified brand investments in prime locations, emphasizing digital integration and sustainability. Barcelona's fusion of culture, lifestyle, and accessibility positions it as a growth magnet for emerging luxury trends. Its retail evolution underscores adaptability to global consumer shifts.

Southern coastal areas like Marbella and Costa del Sol gain traction through luxury resorts and seasonal affluent tourism, focusing on experiential purchases. Northern and island regions contribute via boutique hospitality and niche high-end offerings tied to leisure lifestyles. Urban centers beyond the capitals show steady potential from rising middle-class aspirations and digital access. Geographic disparities highlight tourism's pivotal influence alongside localized wealth concentrations. Brand strategies increasingly target these peripheries for diversification and market penetration. This distribution reveals Spain's luxury market as urban-centric yet ripe for balanced regional expansion.

Competitive Landscape

Spain's luxury goods market exhibits moderate fragmentation, characterized by the coexistence of global conglomerates and niche regional players vying for consumer attention. International giants such as LVMH Moët Hennessy Louis Vuitton, Kering Group, Prada Holding S.P.A., Hermès International S.A., and Chanel SA dominate through extensive portfolios spanning fashion, leather goods, and accessories, yet no single entity commands outright control. Local Spanish brands like Loewe and Puig add layers of competition by leveraging national heritage in craftsmanship and design innovation. This diverse structure fosters intense rivalry across product categories, with brands differentiating via exclusivity, storytelling, and experiential retail.

Major players pursue aggressive expansion through mergers, acquisitions, partnerships, and product diversification to capture market share in this fragmented environment. For instance, Puig's investment in Charlotte Tilbury exemplifies how strategic alliances bolster portfolios and reach new demographics. Global brands emphasize flagship stores in Madrid and Barcelona to cultivate prestige, while smaller entities focus on niche sustainability and personalization appeals. Competition intensifies around high-demand segments like apparel and leather goods, where innovation in materials and digital integration sets leaders apart. Regional players counter with authentic Spanish motifs, appealing to tourists and locals seeking cultural resonance.

Fragmentation presents opportunities for both established leaders and agile newcomers, particularly as younger consumers prioritize experiential luxury and ethical practices. While conglomerates hold sway through brand equity and distribution networks, niche brands gain ground via e-commerce and resale channels that democratize access. Ongoing tourism recovery and rising affluence further fragment demand across demographics, compelling all players to innovate in omnichannel strategies. Challenges like counterfeits and economic volatility heighten the need for authenticity and resilience.

Spain Luxury Goods Industry Leaders

-

Hermès International S.A.

-

Chanel SA

-

LVMH Moët Hennessy Louis Vuitton

-

Kering SA

-

Richemont SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Louis Vuitton formalized a multi-year partnership with Real Madrid, becoming the club's Official Luggage and Lifestyle Partner, with co-branded products sold exclusively at the Santiago Bernabéu Stadium and projected to contribute EUR 18 million (USD 19.6 million) in incremental revenue by 2026, targeting the club's 450 million global fans

- September 2024: Louis Vuitton reinforced its retail footprint in Barcelona for the Louis Vuitton 37th America’s Cup by opening two temporary points of sale a kiosk within the official race village and a dedicated pop-up store designed to capitalize on elevated tourist traffic and event-driven brand visibility.

- August 2024: Loewe has expanded its Spanish retail footprint by opening a permanent boutique at the Marbella Club resort, reinforcing its presence in high-end leisure destinations and deepening access to affluent international clientele frequenting the Costa del Sol.

Spain Luxury Goods Market Report Scope

Luxury goods refer to premium or elite quality products which are expensive as compared to conventional accessories. The Spain luxury goods market is segmented by type and distribution channel. By type, the market is categorized into clothing and apparel, footwear, bags, jewelry, watches, and other luxury goods. By distribution channel, the market is segmented into single-brand stores, multi-brand stores, online stores, and other distribution channels. The report offers market size and forecasts in terms of value (USD million ) for all the above segments.

By Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Jewelry |

| Leather Goods |

| Watches |

| Other Types |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Single Brand Stores |

| Multi Brand Stores |

| Online Stores |

| Other Distribution Channels |

| By Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Jewelry | |

| Leather Goods | |

| Watches | |

| Other Types | |

| By End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Single Brand Stores |

| Multi Brand Stores | |

| Online Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

How large is the Spain luxury goods market in 2026?

The market totaled USD 7.4 billion in 2026 and is forecast to reach USD 9.32 billion by 2031 at a 4.72% CAGR.

Which product category is growing fastest in Spain’s luxury segment?

Watches lead growth with a projected 5.12% CAGR through 2031 as mechanical timepieces evolve into collectible investment assets.

Why are online channels gaining share in the Spanish luxury space?

Digital natives demand seamless omni-channel journeys, pushing online luxury sales to grow 6.84% annually, four times faster than the broader market.

Which cities dominate luxury sales in Spain?

Madrid and Barcelona jointly capture 69% of national luxury receipts thanks to dense HNWI populations, international tourism, and flagship-store corridors.

Page last updated on: