Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

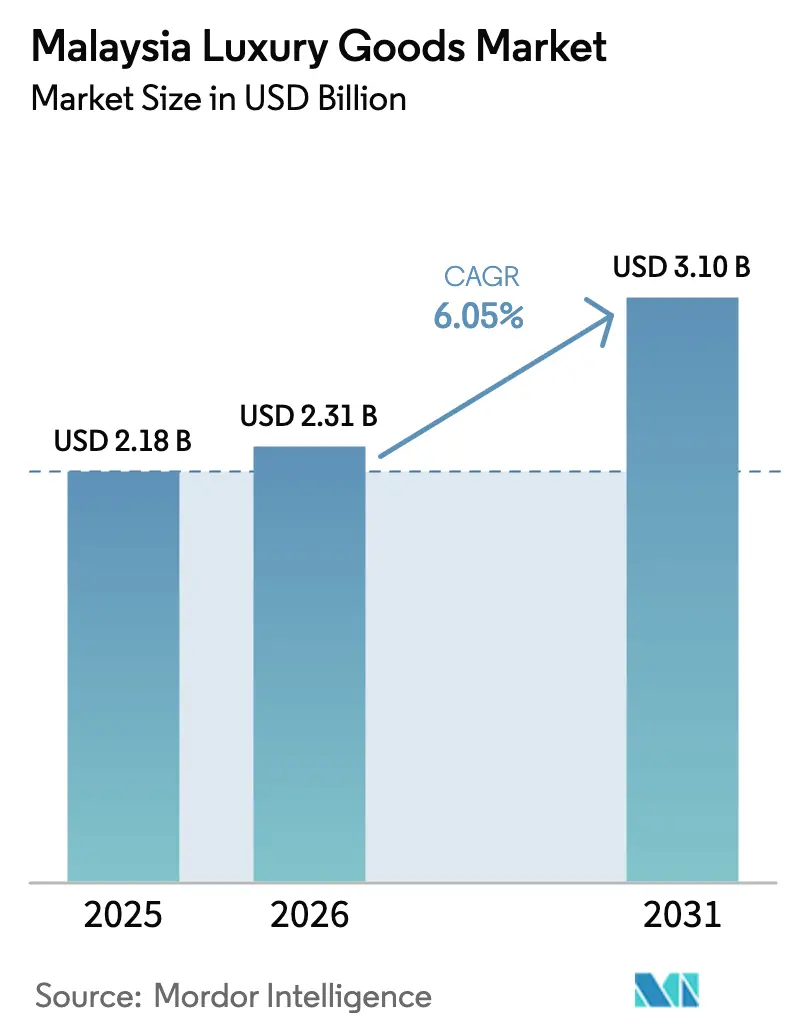

| Base Year Market Size (2025) | USD 2.18 Billion |

| Market Size (2026) | USD 2.31 Billion |

| Market Size (2031) | USD 3.1 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Malaysia Luxury Goods Market Analysis by Mordor Intelligence

The Malaysian luxury goods market size is expected to grow from USD 2.18 billion in 2025 to USD 2.31 billion in 2026 and is forecast to reach USD 3.1 billion by 2031 at 6.05% CAGR over 2026-2031. Steady tourism recovery, rising affluence, and a growing halal-conscious consumer base keep demand resilient. Duty-free destinations such as Langkawi and the Golden Triangle in Kuala Lumpur continue to draw regional shoppers, while the Visit Malaysia 2026 campaign targets higher-spending visitors from China and the GCC. However, currency weakness makes Malaysia more affordable for inbound tourists, even as it limits local purchasing power. Digital retail adoption accelerates on the back of 89.6% internet penetration, prompting brands to blend virtual services with in-store exclusivity. Moderate market fragmentation allows international Maisons and well-capitalised local groups to compete through experiential flagships, sustainability credentials, and halal certification.

Key Report Takeaways

- By product type, clothing and apparel led with 28.72% of the Malaysian luxury goods market share in 2025; jewelry is projected to expand at a 6.59% CAGR through 2031.

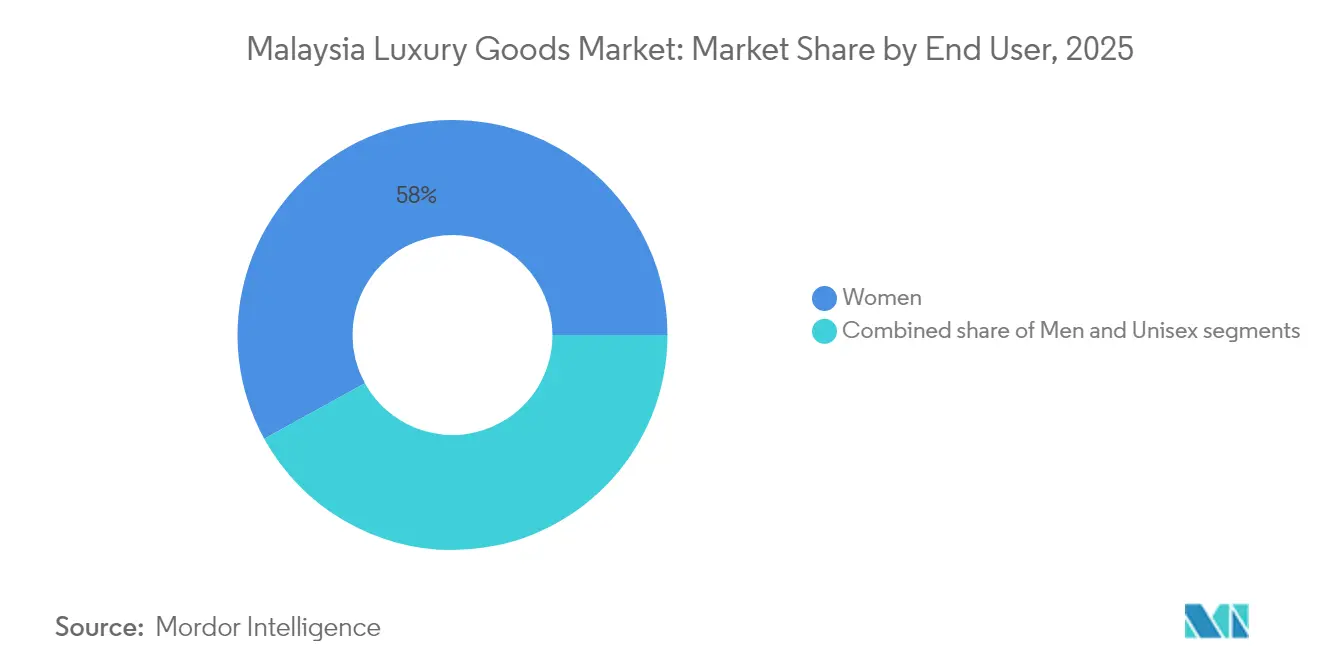

- By end user, women captured 58.01% of the Malaysian luxury goods market size in 2025, while men are forecast to grow at a 6.92% CAGR between 2026-2031.

- By distribution channel, offline stores held 82.15% of the Malaysian luxury goods market size in 2025; online stores are advancing at a 7.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Luxury Goods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer focus on sustainability across luxury categories | +1.2% | Urban Malaysia | Medium term (2-4 years) |

| Influence of social media and celebrity endorsement on Malaysian millennials | +0.8% | Kuala Lumpur, Penang, Johor Bahru | Short term (≤ 2 years) |

| High demand from inbound tourists, especially from China and GCC | +1.5% | Kuala Lumpur, Langkawi, Penang | Short term (≤ 2 years) |

| Product innovation in exotic-skins-free leather and design personalisation | +0.7% | National luxury hubs | Medium term (2-4 years) |

| Increasing e-commerce penetration | +0.9% | Urban Malaysia | Short term (≤ 2 years) |

| Rising affluent Muslim population seeking halal-certified luxury | +1.1% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer Emphasis on Sustainability Across Luxury Categories

Sustainability has become a key purchasing factor for Malaysian luxury consumers, especially among younger buyers. This significant change has prompted luxury brands to fundamentally transform their supply chains and product development approaches to meet evolving consumer preferences. In January 2025, Malaysian luxury footwear brand Lewre Bespoke partnered with Weng Meng Greentech to produce sustainable luxury footwear using palm oil trunks. This innovative initiative showcases how local luxury brands are adapting to meet growing consumer demands while addressing critical Malaysian environmental challenges. Brands that authentically weave environmental responsibility into their luxury offerings are reaping significant competitive advantages. This trend is driven by consumers' increasing focus on sustainability, as they actively seek eco-friendly products and practices. Companies that align their strategies with these values are not only meeting consumer expectations but also positioning themselves as leaders in the evolving luxury market.

Influence of Social-Media and Celebrity Endorsement on Malaysian Millennials

Social media and celebrity endorsements have transformed luxury purchasing patterns in Malaysia. Studies of urban Malaysian women show that social media influencers' visual appeal has a stronger impact on luxury cosmetics purchases than their perceived credibility. This shift in consumer behavior demonstrates a significant change in how luxury brands connect with their target audience. The trend is particularly evident in the beauty market, where influencer content has developed small communities of luxury consumers who prioritize peer recommendations over traditional marketing channels. These communities actively share product experiences, reviews, and recommendations, creating a powerful word-of-mouth network. Malaysian celebrities use their social media platforms to strengthen consumer relationships and advocacy, engaging with followers through personalized content and direct interactions. Research confirms that their social media engagement significantly increases luxury purchase intentions, with consumers more likely to trust and act on recommendations from their preferred social media personalities.

High Demand from Inbound Tourists, Especially from China and GCC

The resumption of Chinese tourist arrivals in Malaysia has increased revenue in the luxury retail segment across major shopping centers and retail districts. Chinese luxury consumers demonstrate high purchasing power through their demand for premium brands, authentic local Chinese cuisine, and high-end services. Their preference for Mandarin-speaking retail staff and personalized shopping experiences directly influences luxury goods consumption patterns. Tourism Malaysia data shows that in 2023, Malaysia received 1.47 million visitors from China, representing a 593.4% increase compared to 2022 [1]Source: Tourism Malaysia, "Malaysia Ushers in the Chinese New Year with Increased Flights from China to Malaysia", tourism.gov.my . While fewer Chinese tourists are engaging in general shopping activities overall, those who do are investing significantly more in luxury items across various categories, including fashion, accessories, and jewelry, demonstrating a clear shift toward quality-focused purchasing that benefits premium brands and high-end retailers.

Product Innovation in Exotic-skins-free Leather and Design Personalization

Luxury brands increasingly adopt exotic skin alternatives and personalization technologies to address evolving consumer preferences and regulatory pressures surrounding animal welfare. Malaysia's position as a manufacturing hub for leather goods creates opportunities for brands to develop sustainable alternatives using innovative materials like mushroom leather, lab-grown materials, and recycled synthetics. The personalization trend gains traction through digital technologies, enabling custom embossing, color selection, and design modifications at the point of sale. Malaysian consumers particularly value personalization services that incorporate Islamic calligraphy, local cultural motifs, and family crests, creating differentiation opportunities for brands willing to invest in localized customization capabilities. The convergence of sustainability and personalization appeals to Malaysia's affluent Muslim consumers who seek products reflecting both their values and individual identity. This innovation cycle positions Malaysia as a potential regional center for sustainable luxury manufacturing and customization services.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of counterfeit goods on grey market platforms | -0.8% | National, with concentration in urban areas and online platforms | Short term (≤ 2 years) |

| Lesser demand from price-sensitive middle-income consumers | -0.6% | National, affecting mass luxury segments | Medium term (2-4 years) |

| High import duties vs. Singapore and Thailand | -0.9% | National, with cross-border shopping impact | Long term (≥ 4 years) |

| MYR currency volatility compressing overseas buying power | -1.2% | National, affecting import-dependent luxury categories | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Availability of Counterfeit Goods on Grey Market Platforms

Counterfeiting in Malaysia has reached "alarming levels" according to OECD analysis, with counterfeit goods accounting for 2.5% of global trade valued at USD 461 billion, significantly affecting luxury brand integrity and consumer confidence. The proliferation of e-commerce platforms creates new distribution channels for counterfeit luxury goods, complicating enforcement efforts and diluting brand exclusivity. Low penalties and ineffective enforcement of existing regulations contribute to the problem's persistence, while the growth of cross-border e-commerce makes detection and prosecution increasingly difficult. Malaysia's government intensifies efforts to ensure genuine luxury products reach consumers, particularly in the gold and jewelry sectors, but the scale of counterfeiting continues to undermine legitimate luxury sales. The counterfeit issue particularly affects entry-level luxury segments where price sensitivity makes consumers more susceptible to fake alternatives, forcing brands to invest heavily in authentication technologies and consumer education programs.

Lesser Demand from Price-Sensitive Middle-Income Consumers

Economic pressures are influencing purchasing patterns in Malaysia's luxury market, as price sensitivity constrains market growth. Malaysia's inflation rate reached 3.4% in March 2023, according to the Department of Statistics Malaysia. Six states exceeded the national average, with Wilayah Persekutuan Putrajaya registering 4.5% and Selangor recording 4.0% [2]Souce: Department of Statistics Malaysia, "Consumer Price Index Malaysia", dosm.gov.my . The heightened inflationary environment has compelled consumers to minimize discretionary expenditure and modify their spending allocation. Additionally, Retailers from Singapore expanding into Malaysia must address this price sensitivity by balancing product quality with affordability while maintaining brand value. Luxury retailers are rolling out financing solutions, such as Buy Now, Pay Later (BNPL) services, to make their offerings more accessible to aspirational buyers. With these payment options, consumers can spread their luxury purchases over installments, reducing the immediate financial burden. This strategy not only broadens the retailer's customer base by appealing to a wider demographic but also helps them uphold their premium market stance, ensuring sustained growth and competitiveness in the luxury market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Jewelry Outshines Traditional Categories

The product landscape in Malaysia's luxury market reveals a strategic shift toward high-value, investment-oriented purchases. Clothing and apparel command the largest market share at 28.72% in 2025, benefiting from established brand presence and consistent demand for designer fashion. However, jewelry is emerging as the growth leader with a projected CAGR of 6.59% (2026-2031), outpacing all other segments. This acceleration reflects Malaysian consumers' increasing preference for tangible assets with enduring value, particularly in uncertain economic times. The jewelry segment's growth is further amplified by the expanding presence of international brands like Cartier and Bulgari, which are focusing on Malaysia as part of their Southeast Asian expansion strategy.

Moreover, luxury beauty and personal care products are gaining momentum as entry points to luxury consumption, particularly among younger consumers seeking accessible luxury experiences. Watches maintain a strong appeal among male consumers and collectors, with limited editions driving interest. Leather goods benefit from strong brand recognition but face increasing competition from emerging sustainable alternatives. Eyewear serves as an accessible entry point to luxury brands, though it represents a smaller portion of the market.

By Distribution Channel: Digital-Physical Integration Reshapes Retail

Malaysia's luxury retail landscape is characterized by the continued dominance of physical stores despite rapid digital acceleration. Offline stores command 82.15% of the market in 2025, reflecting Malaysian consumers' preference for immersive, tactile luxury shopping experiences. Established luxury malls like Pavilion KL and Suria KLCC remain the preferred destinations for both tourists and high-net-worth locals, maintaining their position despite new entrants like The Exchange TRX. The resilience of physical retail is particularly evident in the luxury segment, where the experiential aspect of shopping, including personalized service and immediate product access, continues to drive consumer preference for in-store purchases.

Online channels are growing faster at 7.38% CAGR (2026-2031), driven by improved digital experiences and changing consumer behaviors, particularly among younger luxury shoppers. However, the luxury market is increasingly characterized by omnichannel behavior rather than channel substitution. Research on luxury shopping behavior reveals that Malaysian consumers engage in "webrooming"—researching online before purchasing in-store, particularly for high-value items where tactile evaluation is important. This hybrid shopping pattern is prompting luxury retailers to invest in seamless integration between digital and physical touchpoints, enhancing the overall customer journey while maintaining the exclusivity associated with luxury brands.

By End User: Men's Segment Accelerates Despite Women's Dominance

The gender dynamics in Malaysia's luxury market are undergoing a notable shift despite women maintaining market dominance. Women account for 58.01% of the luxury goods market in 2025, driven by their traditionally stronger engagement with fashion, beauty, and jewelry categories. However, the men's segment is growing at a faster pace with a 6.92% CAGR (2026-2031), indicating evolving male consumer attitudes toward luxury consumption. This growth is partly attributed to expanding product ranges specifically designed for men across categories that were historically female-dominated, such as jewelry and beauty products. The men's luxury segment in Malaysia is particularly strong in watches, leather goods, and increasingly, fashion apparel, with brands like Louis Vuitton and Hermès expanding their men's collections to capitalize on this trend.

Cultural factors significantly influence gender-based purchasing patterns in Malaysia's luxury market, with research indicating that Malaysian men prioritize elitism in luxury consumption while women value refinement. The unisex segment represents a growing opportunity, particularly among younger consumers who increasingly reject traditional gender boundaries in fashion and accessories. Brands that effectively navigate these shifting gender norms while respecting Malaysian cultural sensitivities are positioned to capture growth across all end-user segments. The expansion of gender-fluid collections from major luxury houses suggests recognition of this emerging trend, though marketing approaches still largely maintain gender distinctions to align with prevailing consumer preferences in the Malaysian market, according to the American Marketing Association (2024).

Geography Analysis

Malaysia's luxury goods market exhibits distinct geographic patterns that reflect the country's economic development and tourism flows. Kuala Lumpur dominates the luxury landscape, hosting the highest concentration of premium retail spaces and international brand flagships. The capital's luxury ecosystem is anchored by established malls like Pavilion KL and Suria KLCC, which continue to outperform newer entrants like The Exchange TRX in attracting both tourist and local high-net-worth shoppers. This resilience is attributed to their iconic status and strategic locations near tourist attractions like the Petronas Twin Towers, which drive foot traffic.

Resort destinations like Langkawi are emerging as specialized luxury retail locations, focusing on duty-free shopping that appeals to both domestic and international tourists. This geographic diversification reflects a maturing luxury market that is expanding beyond traditional urban centers to capture regional spending power and tourist flows. The expansion is supported by improving retail infrastructure and increasing brand awareness in secondary cities, though challenges remain in matching the sophisticated luxury ecosystem established in the capital.

The geographic distribution of luxury consumption in Malaysia is increasingly influenced by digital connectivity, which is reducing the importance of physical location for brand discovery while maintaining its relevance for the purchase experience. Urban centers benefit from higher digital penetration and faster delivery options, enhancing the online luxury shopping experience. According to the International Trade Administration data from 2024, Malaysia demonstrates digitization rates, with internet penetration exceeding 97 percent and mobile phone penetration nearing 130 percent . However, the tactile nature of luxury goods ensures that physical retail locations in prime areas maintain their strategic importance, with brands focusing on creating destination stores that offer immersive brand experiences beyond mere transaction points. This dual approach allows luxury brands to maintain exclusivity through selective physical presence while expanding their reach through digital channels, creating a balanced geographic strategy that accommodates Malaysia's diverse luxury consumer base across urban and resort locations.

Competitive Landscape

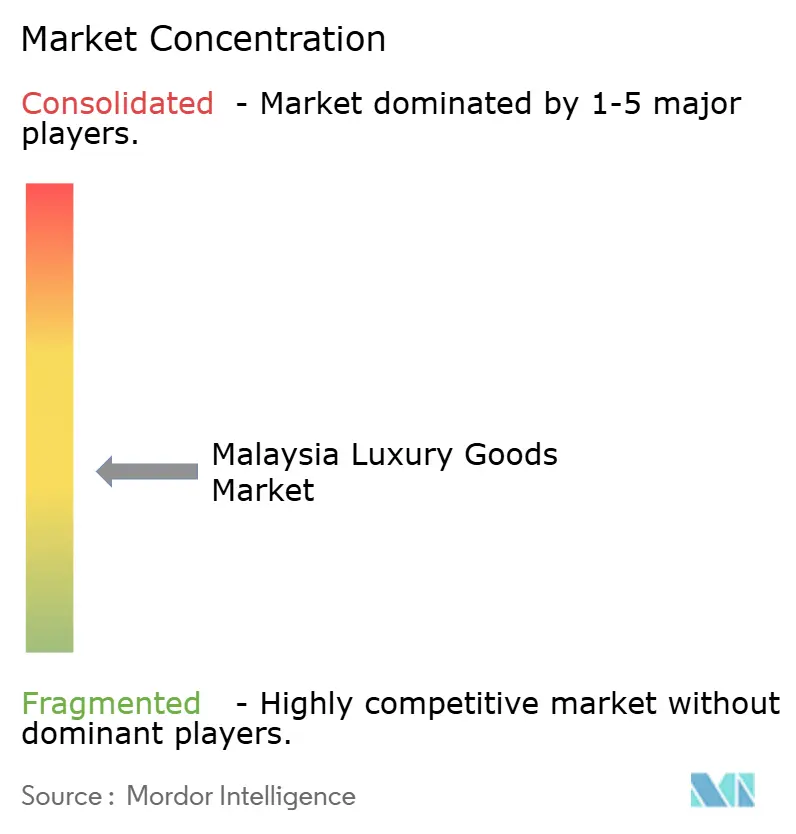

The Malaysian luxury goods market exhibits moderate fragmentation, creating a balanced competitive environment where established global houses maintain dominance while leaving room for niche players and local luxury brands. LVMH leads the market through its diverse portfolio spanning fashion, leather goods, watches, jewelry, and beauty, generating significant revenue from its flagship Louis Vuitton brand, which maintains strong appeal among Malaysian consumers despite global luxury market headwinds.

Competitive strategies increasingly focus on localization, with brands adapting their offerings to Malaysian cultural preferences and shopping behaviors while maintaining global brand positioning. This approach is particularly evident in product design, marketing campaigns, and retail experiences tailored to local sensibilities. White-space opportunities exist in several areas, including sustainable luxury, which resonates with environmentally conscious Malaysian consumers willing to pay premiums.

Digital innovation represents a competitive frontier, with brands leveraging technology to enhance customer experiences across online and offline channels. Emerging disruptors include digitally native luxury brands that bypass traditional retail models, and local Malaysian designers who combine international luxury standards with authentic cultural elements. The competitive landscape is further shaped by the integration of Total Quality Management practices by luxury conglomerates like LVMH, which enhances their market power through economies of scale and scope while maintaining the exclusivity and craftsmanship expected of luxury brands.

Malaysia Luxury Goods Industry Leaders

-

Prada S.p.A

-

LVMH Moët Hennessy Louis Vuitton

-

Kering SA

-

Chanel Ltd.

-

Hermès International S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Louis Vuitton strengthened its presence in Malaysia by establishing its largest flagship store at Pavilion Kuala Lumpur. The store provided the company's complete product range, including leather goods, ready-to-wear items, accessories, and exclusive products. This expansion demonstrated Louis Vuitton's commitment to the Malaysian luxury retail market and enhanced its distribution network in Southeast Asia.

- June 2024: French luxury jewelry and watch brand FRED (Fred Joaillier) established its first flagship store in Malaysia at Seibu The Exchange TRX, situated on the mall's ground floor. The flagship store featured FRED's complete collection of fine jewelry and timepieces, providing customers with access to the brand's entire product range in a premium retail location.

- May 2024: BurdaLuxury expanded its Malaysian operations by launching Lifestyle Asia Malaysia in Bahasa Malaysia. The expansion enabled the company to reach Malaysia's predominantly Malay-speaking population of over 32 million people while delivering region-specific content to Malaysian readers.

- December 2023: Louis Vuitton established a store at The Exchange TRX in Kuala Lumpur, Malaysia. The location offered the brand's complete product range, including men's and women's fashion, footwear, leather goods, travel bags, trunks, accessories, textiles, fragrances, watches, and jewelry.

Malaysia Luxury Goods Market Report Scope

Luxury goods are high-end products differentiated by superior quality, limited availability, and brand value. These products maintain premium price points and established market positioning. The category encompasses designer fashion, fine jewelry, and luxury watches, which consumers acquire based on product quality, market positioning, and discretionary spending patterns.

The Malaysian luxury goods market is segmented by type and distribution channel. By type, the market is segmented into clothing and apparel, footwear, bags, jewelry, watches, and other accessories. By distribution channel, the market is segmented into single-brand stores, multi-brand stores, online stores, and other distribution channels.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Clothing and Apparel |

| Footwear |

| Eyewear |

| Leather Goods |

| Jewelry |

| Watches |

| Beauty and Personal Care |

By End User

| Men |

| Women |

| Unisex |

By Distribution Channel

| Offline Stores |

| Online Stores |

| By Product Type | Clothing and Apparel |

| Footwear | |

| Eyewear | |

| Leather Goods | |

| Jewelry | |

| Watches | |

| Beauty and Personal Care | |

| By End User | Men |

| Women | |

| Unisex | |

| By Distribution Channel | Offline Stores |

| Online Stores |

Key Questions Answered in the Report

What is the current value of the Malaysia luxury goods market?

The market stands at USD 2.31 billion in 2026 and is projected to reach USD 3.1 billion by 2031.

Which product category holds the largest share?

Clothing and apparel leads with 28.72% of the Malaysia luxury goods market share in 2025.

How fast is online luxury retail growing in Malaysia?

Online channels are forecast to grow at a 7.38% CAGR between 2026-2031, supported by high internet penetration.

Why is halal certification important for luxury brands in Malaysia?

Halal credentials align luxury products with Islamic principles, unlocking demand from the majority Muslim population and regional markets.

Page last updated on: