Market Overview

| Study Period | 2022 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

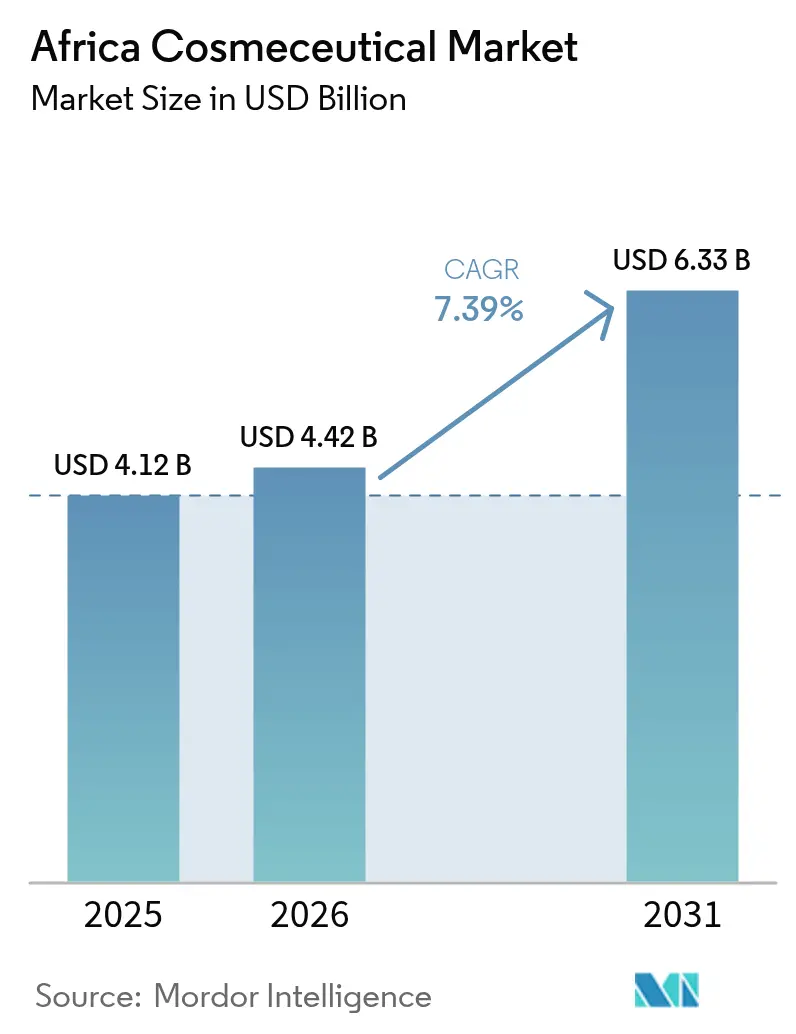

| Base Year Market Size (2025) | USD 4.12 Billion |

| Market Size (2026) | USD 4.42 Billion |

| Market Size (2031) | USD 6.33 Billion |

| Growth Rate (2026 - 2031) | 7.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Cosmeceutical Market Analysis by Mordor Intelligence

The Africa cosmeceuticals market size is expected to grow from USD 4.12 billion in 2025 to USD 4.42 billion in 2026 and is forecast to reach USD 6.33 billion by 2031 at 7.39% CAGR over 2026-2031. This robust trajectory stems from the region’s unique blend of validated indigenous botanicals and modern dermatological science. Zero-tariff trade agreements under the African Continental Free Trade Area (AfCFTA) are cutting raw-material costs, while rising urban pollution is steering consumers toward sophisticated barrier-repair formulations. A sharp uptick in mobile commerce—now 69% of web traffic—has redrawn the path to purchase, empowering direct-to-consumer strategies even in traditionally underserved locales. Competitive intensity remains moderate as multinationals leverage scale and local challengers capitalize on botanical authenticity, enabling price–quality stratification across income tiers.

Key Report Takeaways

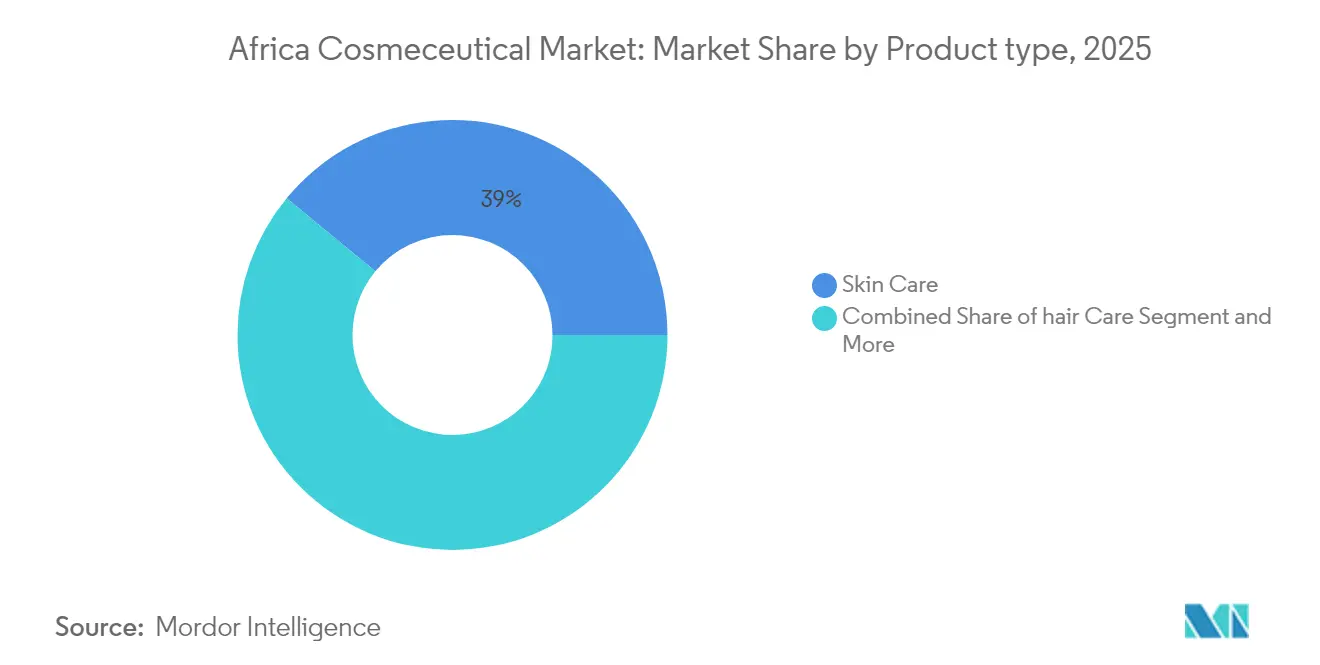

- By product type, skin care led with 39.02% of Africa cosmeceuticals market share in 2025, whereas hair care is forecast to expand at a 9.06% CAGR to 2031.

- By category, conventional products accounted for 55.60% share of the Africa cosmeceuticals market size in 2025, while natural/organic offerings are set to grow at an 11.19% CAGR through 2031.

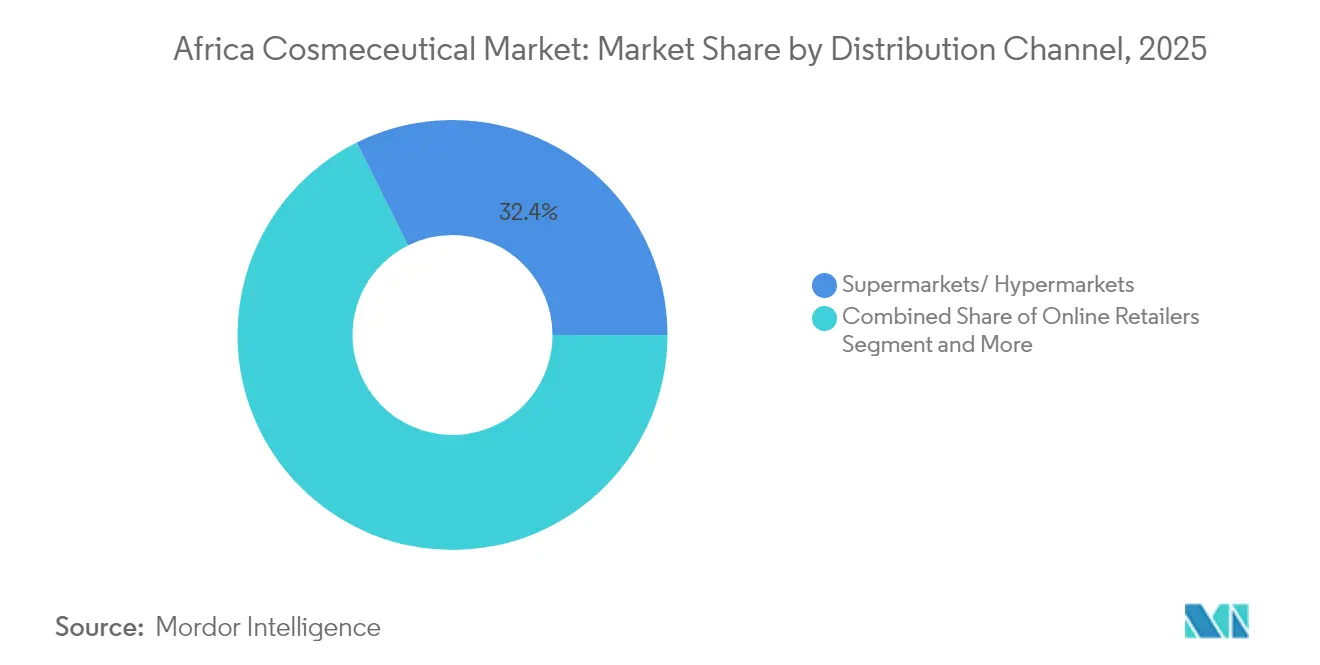

- By distribution channel, supermarkets/hypermarkets captured 32.35% revenue in 2025, whereas online retail is advancing at a 10.70% CAGR to 2031.

- By geography, South Africa held 27.98% share in 2025; Nigeria is anticipated to record the fastest 9.41% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Cosmeceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Zero-tariff trade pacts accelerating raw-material flows | +1.8% | Global; early gains in SADC and EAC | Medium term (2-4 years) |

| Urban pollution-driven demand for advanced skin care | +2.1% | Nigeria, South Africa, Kenya urban centers | Short term (≤ 2 years) |

| Expansion of organised retail & e-commerce | +1.5% | South Africa, Nigeria, Kenya; spillover to Morocco | Medium term (2-4 years) |

| Influence of social media platforms and beauty bloggers | +1.2% | Global; strongest in Nigeria and South Africa | Short term (≤ 2 years) |

| Validation of indigenous botanicals in dermatology | +0.9% | Continental; led by South African institutions | Long term (≥ 4 years) |

| Surge in male-grooming adoption | +0.7% | Urban Nigeria, South Africa, Kenya | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Zero-tariff trade pacts accelerating raw-material flows

AfCFTA eliminates import duties on biodiversity-based inputs, letting formulators source marula, baobab, and rooibos across borders without cost penalties[1]United Nations Conference on Trade and Development, “Implications of the African Continental Free Trade Area for Trade and Biodiversity,” unctad.org. Procurement cycles tighten as customs paperwork shrinks, and ingredient diversity rises, supporting quick-turn product launches. Regional economic communities such as SADC have begun harmonizing cosmetic standards, reducing compliance duplication. As a result, brands can scale pilot batches continent-wide, anchoring the African cosmeceuticals market in lean, cross-border supply chains. Cost savings cushion R&D investment in new activities, which in turn widens premium price corridors without eroding margins.

Urban pollution–driven demand for advanced skin care

Particulate levels in Lagos and Johannesburg routinely exceed WHO guidelines, heightening oxidative stress on skin[2]World Health Organization, “African Vaccine Regulatory Forum – Regulators,” who.int. Consumers are pivoting from basic moisturizers to serums fortified with antioxidants and barrier-repair peptides. Dermatologists cite a 32% rise in clinic visits for pollution-linked dermatitis between 2023 and 2024, nudging retailers to spotlight “anti-pollution” shelves. Formulators are blending indigenous compounds, such as Ximenia americana seed oil, with niacinamide, creating products that claim both natural origin and clinical efficacy. Premium positioning is justified as urban professionals view barrier defense as a wellness essential rather than a discretionary luxury, propelling the Africa cosmeceuticals market toward higher average selling prices.

Expansion of organised retail & e-commerce

Africa’s digital commerce value is on track to hit USD 72 billion by 2026, with beauty as a headline category[3]EBANX, “Africa’s Digital Commerce Projected to Reach USD 72 Billion by 2026,” ebanx.com. Smartphone penetration enables video consultations and virtual try-ons via ModiFace on Jumia, closing the experiential gap of online shopping. Logistics upgrades, including motorcycle last-mile fleets in Nairobi, have reduced delivery windows from five days to forty-eight hours. Supermarkets upgrade shelf analytics with RFID to cut stockouts, but online channels outpace brick-and-mortar in customer-data granularity, allowing hyper-targeted promotions. Consequently, omnichannel players enjoy basket sizes 22% larger than single-channel counterparts, cementing the Africa cosmeceuticals market’s digital pivot.

Influence of social media platforms and beauty bloggers

TikTok hashtag views for “#NaijaSkinCare” jumped 240% year-over-year, making influencer-led tutorials a primary education vehicle for actives such as retinol and azelaic acid. Male content creators normalize grooming rituals, expanding the addressable base. Brands partnering with micro-influencers see click-through rates three times higher than celebrity endorsements, demonstrating trust currency in peer-level voices. Live-stream shopping events convert at 12% during product drops, dwarfing conventional banner ads. This digital word-of-mouth accelerates trial, shortening the purchase cycle and boosting the Africa cosmeceuticals market penetration in younger demographics.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented & inconsistent regulatory regimes | -1.4% | Continental, varying by country regulatory capacity | Long term (≥ 4 years) |

| Counterfeit / grey-market products eroding brand trust | -1.1% | Nigeria, Kenya, Ghana with cross-border implications | Medium term (2-4 years) |

| Cultural backlash against controversial skin-lightening actives | -0.8% | Global, strongest in South Africa and Kenya | Short term (≤ 2 years) |

| Dependence on imported active ingredients exposes firms to FX volatility & shipping disruptions | -0.9% | Import-dependent markets: Nigeria, Kenya, Morocco | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented & inconsistent regulatory regimes

Country-specific agencies—SAHPRA, NAFDAC, Ghana FDA—maintain divergent dossier requirements, forcing brands to duplicate stability trials and labeling translations. Mutual recognition under the AU Model Law progresses slowly; only eight states enacted harmonization statutes by mid-2025. The resulting compliance drag inflates launch timelines by an average of nine months. Smaller firms without multi-country regulatory teams defer expansion, narrowing their assortment in secondary markets. Consequently, supply remains sub-optimal relative to latent demand, constraining the Africa cosmeceuticals market despite underlying growth drivers.

Counterfeit / grey-market products eroding brand trust

Lab tests in Ilorin uncovered hydroquinone levels above legal thresholds in 46% of sampled skin-lightening creams, many bearing fraudulent NAFDAC numbers. Counterfeits retail at one-third the authentic price, undercutting legitimate SKUs and diluting brand equity. Incidents of contact dermatitis spark social-media backlash, causing shoppers to question safety claims. Brands invest in QR-code verification and tamper-proof seals, raising the cost of goods. For conservative consumers, the risk of fakes deters initial trial, capping premium-segment conversion rates and dampening the Africa cosmeceuticals market uplift.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pollution-Shielded Skin Care Maintains Lead While Hair Care Accelerates

Skin care retained a 39.02% share in 2025, equivalent to USD 1.61 billion within the Africa cosmeceuticals market size. Uptake stems from antioxidant-rich serums featuring marula and baobab oils, which scientific panels ranked highly for transepidermal water-loss reduction. Barrier-repair moisturizers command double-digit price premiums as urban dwellers prioritize pollution defense. Hyperpigmentation products leverage Cassipourea flanaganii’s IC50 of 1.5 µg/mL against tyrosinase, appealing to consumers tackling post-inflammatory marks. The segment’s innovation cadence is bolstered by local R&D partnerships, shortening formulation cycles to under twelve months.

Hair care, although smaller, posts the fastest 9.06% CAGR, reaching an estimated USD 1.12 billion by 2031. Male grooming accounts for 22% of incremental sales as cultural norms shift. Shampoos infused with peppermint oil address scalp sebum balance, while growth serums packed with caffeine and kigelia extract target androgenic alopecia. Digital tutorials on protective styling, fuel conditioner, and leave-in treatment usage among natural-hair communities. Category cross-pollination—such as skin-grade actives in scalp products—broadens premiumization angles, reinforcing value density across the Africa cosmeceuticals market.

By Category: Conventional Formulations Hold Ground as Natural Options Surge

Conventional SKUs captured 55.60% revenue in 2025, translating to USD 2.29 billion of Africa cosmeceuticals market share. Multinationals dominate with retinol creams and chemical exfoliants, backed by decades of clinical validation. Stable emulsions and long shelf-life suit hot climates with intermittent cold-chain breaks. Price segmentation enables mass reach, although rising scrutiny over synthetic preservatives prompts gradual reformulation toward low-irritant systems.

Natural/organic products log an 11.19% CAGR, forecast to touch USD 2.06 billion by 2031 within the Africa cosmeceuticals market size. Shea butter’s triterpene esters demonstrate collagen-stimulation, granting clean-beauty brands efficacy parity with lab-synthesized actives. Transparent supply chains, often backed by fair-trade cooperatives, resonate with ethically minded consumers. As regulatory agencies formalize guidelines for “natural” claims, credibility strengthens, propelling crossover from niche boutiques to mainstream aisles.

By Distribution Channel: Store Presence Dominates Spending Yet Digital Grows Fastest

Supermarkets/hypermarkets generated 32.35% of 2025 sales, equal to USD 1.33 billion within the Africa cosmeceuticals market. Their advantage lies in tactile product trial and promo-endcaps that spur impulse buying. Chains expand beauty corners with trained advisors who upsell regimens rather than single units. Nevertheless, SKU turnover faces physical-space ceilings, and rural penetration lags.

Online retail, advancing at a 10.70% CAGR, will surpass USD 1.27 billion by 2031. Live chat consultations substitute for in-store sampling. Cart-level promotions powered by AI lift average order values 18%. Integration of mobile wallets circumvents card-adoption hurdles, elevating checkout conversion. Pure-play platforms also provide export windows for indie labels, allowing pan-African reach without distributor mark-ups, further democratizing the Africa cosmeceuticals market.

Geography Analysis

In 2025, South Africa commands a significant 27.98% revenue share, a testament to its leadership. This dominance is bolstered by SAHPRA's transparent regulatory pathways and the nation's modern retail corridors. Clinical trials validating marula oil's efficacy bolster consumer trust. Johannesburg's vibrant mall culture champions experiential retail, while loyalty apps, with their tiered rewards, drive repeat purchases. Although currency fluctuations elevate import costs, local contract manufacturing offers a buffer. Domestic challenger brands, harnessing indigenous extracts, now hold a 14% market share, intensifying competition on store shelves. Nigeria, with a robust 9.41% CAGR, stands as Africa's growth powerhouse. A young median age of 17 fuels a social-media-driven appetite for trendy active ingredients. While NAFDAC's digital portal streamlines product registration for SMEs, the battle against counterfeits remains inconsistent. E-commerce hubs in Lagos promise nationwide deliveries within 48 hours, significantly reducing lead times. Furthermore, global giants like Maybelline have set up innovation labs in Lagos, tailoring shade assortments to local preferences, underscoring their long-term commitment.

Egypt, Kenya, and Morocco present distinct opportunities. Egyptian cosmetics factories cater to Arab markets, enabling cost-effective roll-outs. With 90% mobile-money penetration, Kenya simplifies micro-transaction sampling. Morocco's export routes to the EU draw interest in contract manufacturing, especially for argan-infused products. Meanwhile, the diverse Rest-of-Africa region benefits from unified pan-African media campaigns, which standardize aspirational imagery across different languages, steadily expanding the continent's footprint in the cosmeceuticals market.

Competitive Landscape

Moderate fragmentation yields a concentration score of 5. L’Oréal, Unilever, and Johnson & Johnson harness scale efficiencies, while local specialists exploit botanical IP niches. Technology adoption is a pivot: L’Oréal’s ModiFace AR-try-on records dwell times triple that of static images on Jumia, driving conversion. Shiseido’s OBP2A discovery exemplifies high-barrier IP that underpins premium pricing tiers. Start-ups like Zuri, funded by Launch Africa Ventures, utilize D2C channels to test formulations rapidly and crowdsource feedback.

M&A appetite rises as multinationals scout indigenous ingredient pipelines. Unilever’s 2024 volume-led growth validates bet sizes on African wellness segments. Beiersdorf’s double-digit Africa/Asia uptick shows incumbents can still accelerate through targeted SKU rationalization. Strategic white spaces include melanin-compatible sunscreens—a gap Colgate-Palmolive’s EltaMD Deep Tint aims to fill—and male-focused cosmeceuticals targeting beard care and scalp health.

Africa Cosmeceutical Industry Leaders

L'Oréal SA

Unilever PLC

Johnson & Johnson Inc.

Beiersdorf AG

Procter & Gamble Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Prelude Growth invested USD 20 million in OneSkin, demonstrating continued investor confidence in innovative cosmeceutical companies and supporting research into longevity-focused skincare solutions.

- August 2025: Colgate-Palmolive's EltaMD launched Deep Tint Sunscreen specifically designed for darker skin tones, addressing a significant market gap in sun protection products for African consumers

- April 2024: Pan-African beauty startup Zuri secured investment from Launch Africa Ventures, highlighting investor interest in locally-focused cosmeceutical innovation

Africa Cosmeceutical Market Report Scope

The African cosmeceuticals market offers a wide range of products broadly categorized under skincare, hair care, lip care, and oral care. Also, the market covers the products available across distribution channels Supermarket/Hypermarkets, Convenience stores, online Retail, specialist stores, others. Moreover, the study provides an analysis of the cosmeceuticals market in the emerging and established markets across the region, including South Africa, Nigeria, and Egypt.

By Product Type

| Skin Care | Anti-ageing |

| Hyper-pigmentation / Skin-lightening | |

| Anti-acne & Blemish Control | |

| Sun Protection | |

| Moisturisers & Emollients | |

| Other Skin-care Types | |

| Hair Care | Shampoos and Conditioners |

| Hair-regrowth Tonics and Serums | |

| Colourants and Dyes | |

| Other Hair-care Types | |

| Oral Care | |

| Lip Care | |

| Others |

By Category

| Conventional |

| Natural/ Organic |

By Distribution Channel

| Supermarkets / Hypermarkets |

| Convenience Stores |

| Online Retailers |

| Specialist Beauty Retailers and Pharmacies |

| Others |

By Country

| South Africa |

| Nigeria |

| Egypt |

| Kenya |

| Morocco |

| Rest of Africa |

| By Product Type | Skin Care | Anti-ageing |

| Hyper-pigmentation / Skin-lightening | ||

| Anti-acne & Blemish Control | ||

| Sun Protection | ||

| Moisturisers & Emollients | ||

| Other Skin-care Types | ||

| Hair Care | Shampoos and Conditioners | |

| Hair-regrowth Tonics and Serums | ||

| Colourants and Dyes | ||

| Other Hair-care Types | ||

| Oral Care | ||

| Lip Care | ||

| Others | ||

| By Category | Conventional | |

| Natural/ Organic | ||

| By Distribution Channel | Supermarkets / Hypermarkets | |

| Convenience Stores | ||

| Online Retailers | ||

| Specialist Beauty Retailers and Pharmacies | ||

| Others | ||

| By Country | South Africa | |

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Morocco | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the Africa cosmeceuticals market in 2026?

It is valued at USD 4.42 billion, with expansion to USD 6.33 billion expected by 2031.

Which product type leads spending across African beauty consumers?

Skin care remains the largest segment, accounting for 39.02% of 2025 revenue.

What CAGR is forecast for Nigeria’s cosmeceuticals demand?

Nigeria is projected to grow at 9.41% CAGR through 2031, the fastest in the region.

Which sales channel is expanding most rapidly?

Online retail is advancing at 10.70% CAGR, fueled by mobile commerce adoption.

Page last updated on: