Lumpectomy Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

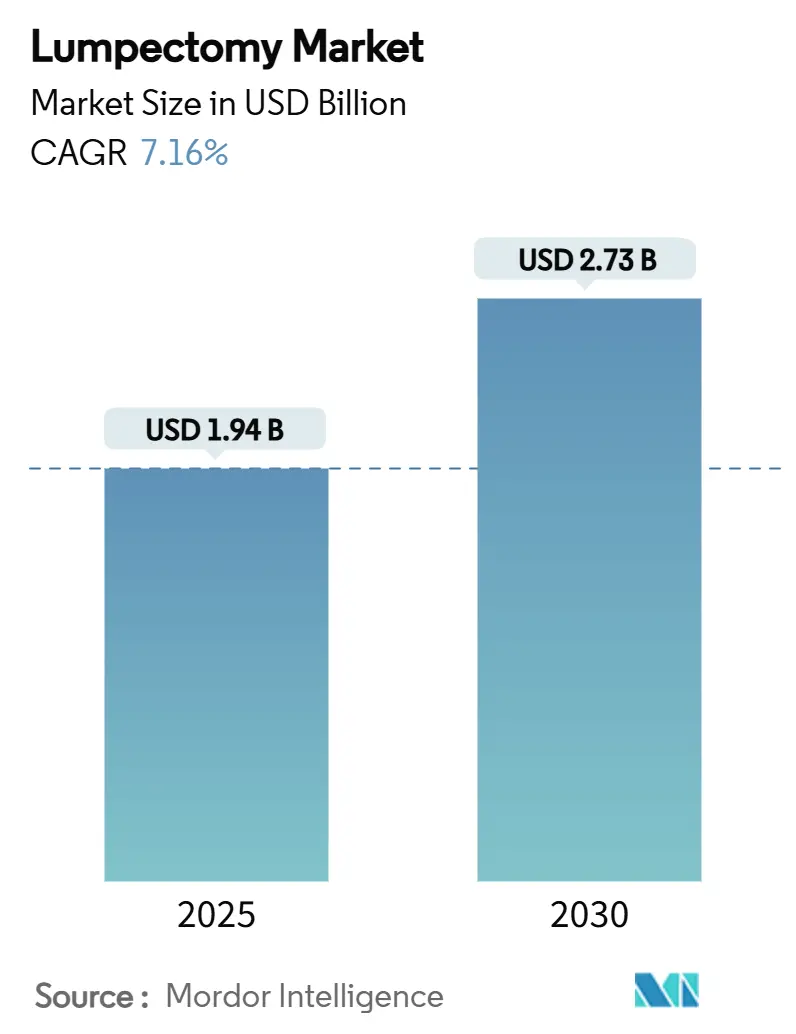

| Market Size (2025) | USD 1.94 Billion |

| Market Size (2030) | USD 2.73 Billion |

| Growth Rate (2025 - 2030) | 7.16% CAGR |

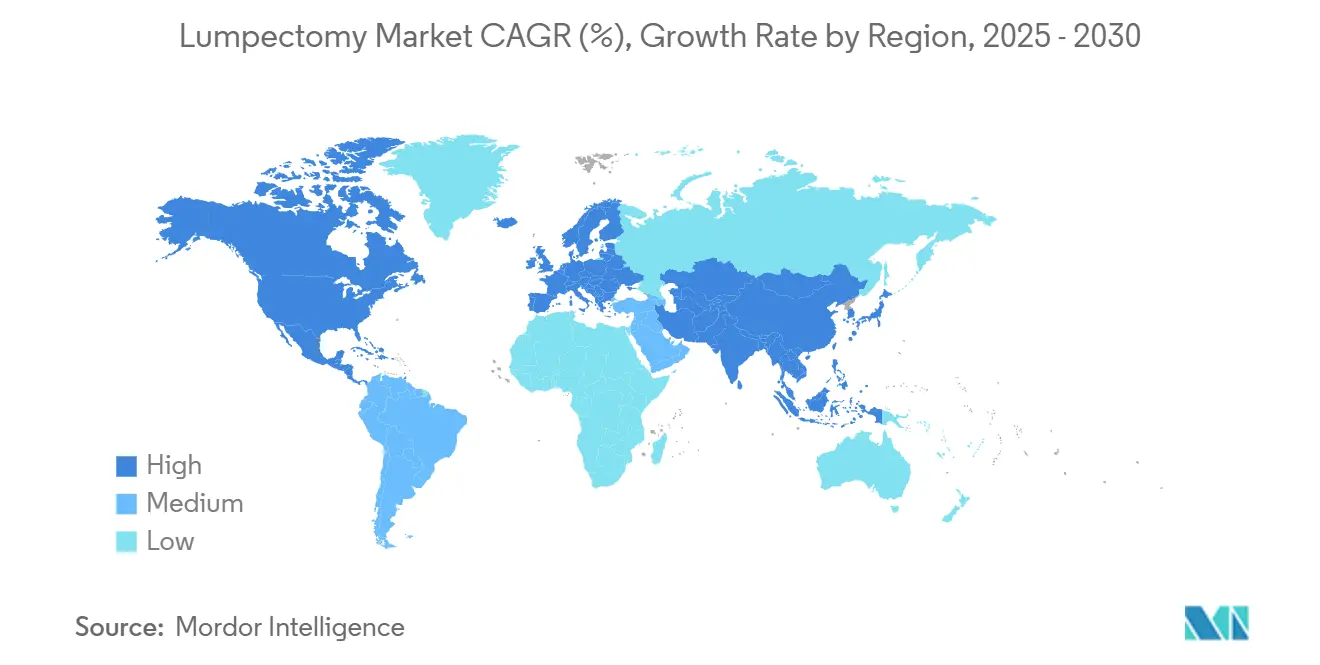

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lumpectomy Market Analysis by Mordor Intelligence

The lumpectomy market size stands at USD 1.94 billion in 2025 and is forecast to reach USD 2.73 billion by 2030, reflecting a 7.16% CAGR over the period. This trajectory is supported by accelerating adoption of real-time intraoperative imaging, a steady shift in oncology guidelines toward breast-conserving surgery, and widening reimbursement for advanced localization devices. Consistent gains in early-stage cancer detection, particularly among women aged 40–54, enlarge the surgical candidate pool and sustain procedural growth. Hospital networks are updating care pathways to integrate wireless localization, while ambulatory surgical centers (ASCs) capture growing case volumes by offering cost-effective outpatient lumpectomy procedures. Technology suppliers are consolidating expertise across imaging and magnetic seed platforms to deliver end-to-end solutions, and their supply chains are gradually diversifying away from single-source sterilization assets to mitigate shortages.

Key Report Takeaways

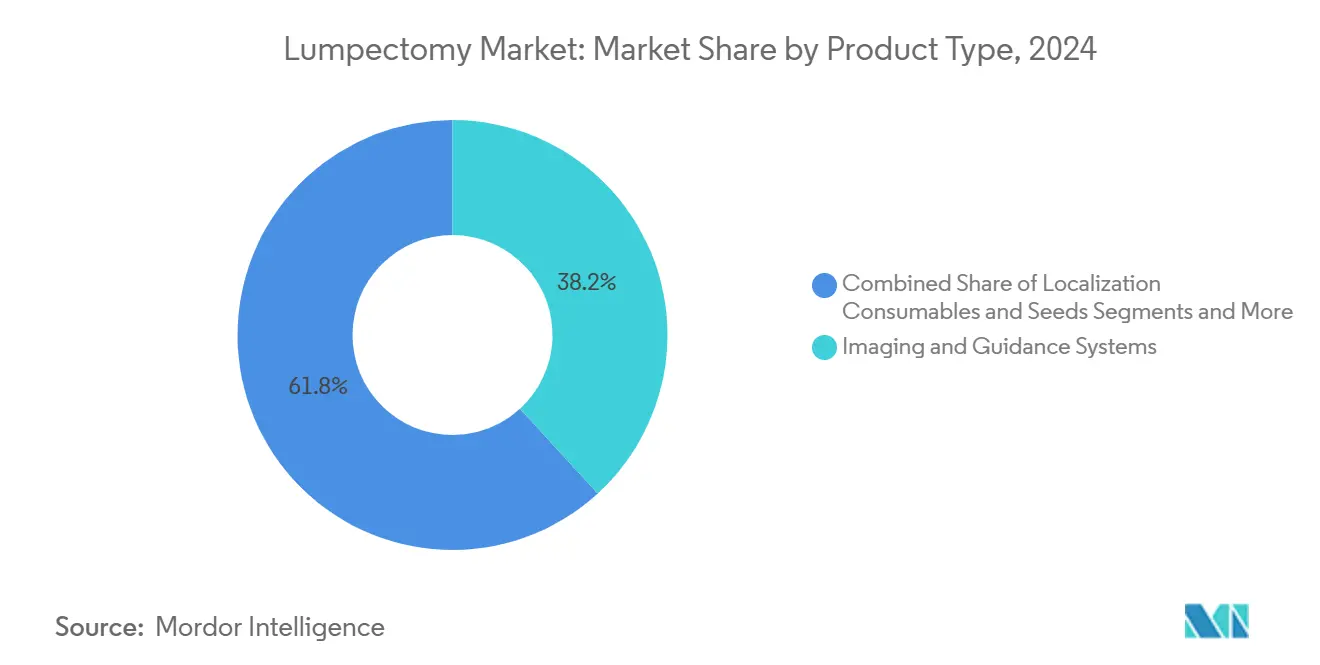

- By product type, Imaging & Guidance Systems led with 38.2% of lumpectomy market share in 2024.

- By localization technology, wire-guided systems accounted for 46.7% share of the lumpectomy market size in 2024, while magnetic seed solutions are advancing at an 8.1% CAGR through 2030.

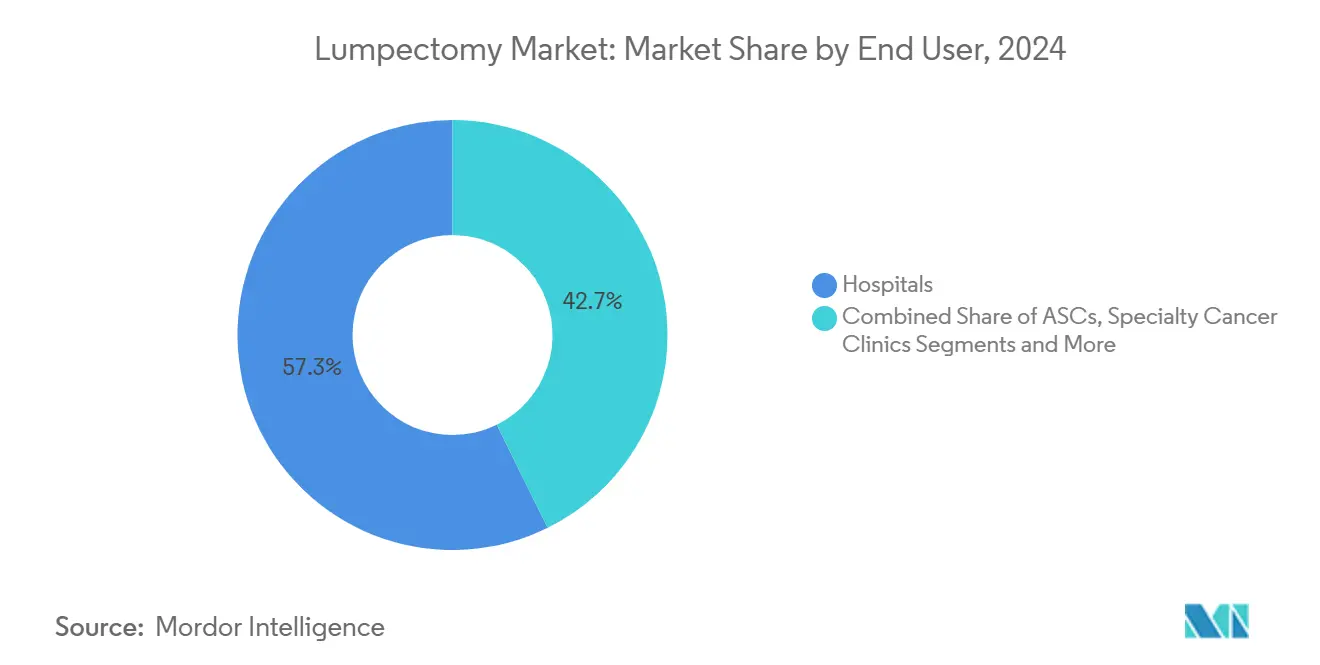

- By end user, hospitals held 57.3% share of the lumpectomy market in 2024; ASCs represent the fastest-growing venue at a 6.4% CAGR to 2030.

- By procedure type, standard lumpectomy captured 63.5% of lumpectomy market share in 2024, whereas oncoplastic techniques are projected to expand at 7.9% CAGR between 2025-2030.

- Geographically, North America led geographically with 42.8% of the lumpectomy market in 2024; Asia Pacific is forecast to grow at 8.5% CAGR over the same period.

Global Lumpectomy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Early-stage breast cancer detected via screening | +1.80% | Global (North America, Europe highest) | Medium term (2–4 years) |

| Shift toward breast-conserving surgery in oncology guidelines | +1.50% | Global (APAC accelerated) | Long term (≥ 4 years) |

| Adoption of real-time margin-assessment systems | +1.20% | North America, EU, expanding APAC | Short term (≤ 2 years) |

| Reimbursement expansion for localization & margin devices | +0.9% | North America, Europe; selective APAC | Medium term (2–4 years) |

| Miniaturization of radar/magnetic seed tools | +0.80% | Developed markets global | Short term (≤ 2 years) |

| AI-driven intraoperative imaging workflows | +0.70% | North America, EU, gradual APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Incidence of Early-Stage Breast Cancer Detected Via Screening

High-resolution digital mammography and tomosynthesis programs are identifying tumors under 2 cm, boosting eligibility for breast-conserving surgery and directly strengthening the lumpectomy market.[1]American Cancer Society, “Cancer Facts & Figures 2025,” cancer.org Updated guidance advocating annual screening from age 40 enlarges the candidate base, and localized disease now posts a five-year survival above 99%. Expanding national screening in Saudi Arabia and other emerging economies drives procedure growth despite workforce constraints. Cost savings also accrue because early detection avoids more invasive therapy.

Shift Toward Breast-Conserving Surgery in Oncology Guidelines

International consensus now regards breast-conserving surgery plus radiotherapy as equivalent—if not superior—to mastectomy on survival metrics, placing sustained demand on the lumpectomy market. Oncoplastic approaches that blend wide excision with cosmetic reconstruction extend tissue-sparing options to larger tumors, prompting healthcare systems to invest in multidisciplinary training. The realignment of clinical protocols in Central-Eastern Europe further normalizes oncoplastic procedures.

Adoption of Real-Time Margin-Assessment Systems Reduces Re-Excisions

Optical coherence tomography and fluorescence-guided platforms such as the FDA-cleared LumiSystem provide intraoperative margin visualization with 84% diagnostic accuracy, cutting historical re-excision rates of 20-40%.[2]Food and Drug Administration, “P230014 SSED,” fda.gov Perimeter Medical’s B-Series OCT achieved statistical superiority over standard care, reinforcing economic arguments for technology adoption. Reduced re-excision lowers patient anxiety and shortens radiation therapy in close to half of eligible cases.

Reimbursement Expansion for Localization & Margin-Assessment Devices

Transitional pass-through payments and permanent HCPCS codes for intraoperative imaging ease hospital budgeting and drive volume migration toward AI-guided solutions. Private insurers are mirroring Medicare policy, while European payers maintain supportive pathways. Variability in coverage across emerging economies remains a hurdle, slowing the uptake of premium devices despite demonstrated value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Steep learning curve for oncoplastic techniques | -1.10% | Global (APAC, emerging markets acute) | Long term (≥ 4 years) |

| Supply-chain bottlenecks for single-use localization consumables | -0.80% | Global (APAC hubs) | Medium term (2–4 years) |

| Inconsistent reimbursement in emerging economies | -0.60% | APAC, MEA, South America | Long term (≥ 4 years) |

| Litigation risk around positive-margin recurrence cases | -0.40% | North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Steep Learning Curve for Oncoplastic Lumpectomy Techniques

Limited fellowship positions and multidisciplinary coordination hurdles restrict surgeon throughput and delay procedural diffusion, particularly across the Asia Pacific, where only 10.7% of eligible Chinese patients receive reconstruction despite service availability. Resource-intensive training centers in Brazil illustrate the capital and time needed to scale competency.[3]Angelo G. Z. Matthes et al., “Development of an Oncoplastic Training Center,” sciencedirect.com

Supply-Chain Bottlenecks for Single-Use Localization Consumables

Sterilization capacity constraints for ethylene oxide and gamma radiation slow device release, and 80% of providers anticipate worsening shortages. Shift toward vaporized hydrogen peroxide requires revalidation and investment, while geopolitical disruptions expose reliance on Asia Pacific manufacturing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Imaging Systems Drive Innovation

Imaging & Guidance Systems commanded 38.2% lumpectomy market share in 2024 on the strength of fluorescence imaging and OCT integration that enhance real-time decision making. The symbiosis of optical platforms with AI modules funnels surgeon demand toward premium consoles, translating into steady capital-equipment cycles. Margin-assessment devices, led by LumiSystem and Perimeter B-Series OCT, are projected to register a 7.8% CAGR through 2030, underpinning incremental revenue via disposable probe sales. Surgical excision instruments remain baseline spend, while localization consumables grow with wireless migration. Adjunctive therapy devices, including intraoperative radiotherapy systems, emerge as add-on revenue streams, signaling convergence between surgical and radiation oncology businesses.

Rapid software-hardware convergence defines next-generation portfolios. FDA-cleared TumorSight Viz converts standard MRI into 3D-guidance maps inside a sterile cockpit, reducing set-up time and shortening OR minutes per case. Vendors are bundling visualization software with magnetic seed kits to capture end-to-end workflows, thereby deepening account penetration and creating lock-in for the lumpectomy market.

By Localization Technology: Wireless Revolution Accelerates

Wire-guided localization held a 46.7% share of the lumpectomy market in 2024 due to entrenched clinical familiarity and broad reimbursement. Yet scheduling complexity, patient discomfort, and radiation exposure have catalyzed investment in wire-free options. Magnetic seed systems are projected to outpace all competitors at an 8.1% CAGR, aided by Stryker’s acquisition of MOLLI Surgical and its ultra-small markers. Radar-reflector technologies such as SAVI SCOUT demonstrate successful deployment in challenging dense-breast cases, while radio-frequency tags carve a niche in multi-lesion guidance.

Workflow efficiency is the overriding purchasing criterion. Same-day localization and surgery streamline radiology and OR calendars, freeing capacity and improving patient experience. As wireless adoption widens, suppliers are building hybrid platforms able to support seeds, radar, and RF tags through interchangeable detectors, preserving hospital capital while future-proofing inventory.

By End User: Hospitals Dominate Amid ASC Growth

Hospitals controlled 57.3% of the lumpectomy market in 2024 thanks to integrated oncology units, reconstructive capability, and access to advanced imaging. Comprehensive cancer centers anchor complex oncoplastic procedures, benefit from in-house pathology, and attract research funding that keeps them at the forefront of clinical innovation. ASCs are forecast to expand at 6.4% CAGR to 2030, leveraging 25-50% cost savings compared with hospital outpatient departments and offering patients quicker turnaround. Specialty cancer clinics maintain focused expertise where case density supports dedicated breast teams, while office-based suites accommodate niche populations seeking concierge services.

Payer alignment speeds venue shift. Medicare added more lumpectomy-related CPT codes to its ASC-covered list in 2023 and boosted facility fees 15.4% in 2024, enhancing financial viability. Device vendors respond by tailoring wireless localization kits for ASC sterilization cycles and stocking patterns, ensuring that the lumpectomy market continues to diversify across care settings.

By Procedure Type: Oncoplastic Techniques Gain Momentum

Standard lumpectomy held 63.5% lumpectomy market share in 2024, grounded in decades of data validating oncologic safety when margins are clear. Incremental improvements in intraoperative imaging have reduced positive margins, but cosmetic outcomes remain variable, prompting growth in oncoplastic variants that integrate tissue rearrangement or reduction mammoplasty at the time of excision. Oncoplastic procedures are projected at a 7.9% CAGR, buoyed by evidence showing positive-margin rates as low as 2% and superior patient-reported quality of life.

Re-excision lumpectomy volume is expected to decline as real-time margin assessment permeates operating rooms, while accelerated partial-breast irradiation (APBI) assisted lumpectomy continues to attract interest for its condensed radiation schedule. Training deficits remain the primary inhibitor, yet virtual reality simulators and telementoring platforms are beginning to shorten the learning curve, helping healthcare systems broaden their procedural mix within the lumpectomy market.

Geography Analysis

North America captured 42.8% of the lumpectomy market in 2024, reflecting deep penetration of AI-enhanced imaging consoles, broad insurance coverage, and active clinical trial networks. Medicare reimbursement rates, however, have lagged general inflation, spurring health systems to rationalize capital budgets and prioritize devices offering measurable reductions in re-excision. Canada’s single fellowship slot underscores ongoing workforce constraints, motivating cross-border fellowships and virtual learning consortia.

Asia Pacific is forecast to post an 8.5% CAGR, the fastest among all regions. Expanding screening programs in China, India, and Saudi Arabia are uncovering larger pools of early-stage cases compatible with breast-conserving surgery. Yet, breast-conserving adoption sits at only 22% in China as cultural preferences and limited oncoplastic expertise hold back growth. Governments are funding cancer hospitals and buying wireless localization kits to modernize surgical pathways, while venture funding for medtech startups softens amid macroeconomic uncertainty. Supply-chain dependence on Asia Pacific sterilization hubs exposes devices to export delays, pushing local manufacturers to invest in alternate sterilants and in-country production.

Europe constitutes a mature but steadily innovating arena. Training curricula in Germany and the United Kingdom have normalized oncoplastic rotations, and national health services reimburse wireless localization to curb re-excisions. Budget scrutiny requires vendors to present robust health-economic dossiers demonstrating cost offsets from fewer repeat surgeries. Middle East & Africa and South America remain underpenetrated yet promising. Brazil’s 21-module oncoplastic training center and Gulf-state vision plans for women’s health centers illustrate nascent momentum, but inconsistent reimbursement and surgeon shortages restrict immediate volume. Long-term infrastructure and capacity investments will determine their eventual contribution to the global lumpectomy market.

Competitive Landscape

The lumpectomy market displays moderate fragmentation, with the top five players controlling a significant market share of global revenue. Hologic’s USD 310 million purchase of Endomagnetics marries diagnostic imaging with magnetic seed technology, positioning the group as an integrated guidance powerhouse. Stryker’s takeover of MOLLI Surgical adds ultra-small markers to its fluorescence portfolio, extending cross-selling potential across orthopedics and oncology.

Competitive advantage hinges on proprietary AI algorithms, multi-modal imaging integration, and disposable revenue from localization consumables. Perimeter Medical, backed by strong pivotal-trial data, is viewed as a potential acquisition target for larger strategics seeking OCT capability. SimBioSys differentiates with digital-twin surgical planning, aiming to license software to console manufacturers.

Emerging-market entrants emphasize price-sensitive wireless localization kits with reusable detectors to capitalize on cost constraints in Asia Pacific and Latin America. Meanwhile, supply-chain resilience has become a marketing lever, with BD investing USD 2.5 billion in domestic plants and touting shorter delivery cycles. Patent walls and multi-year FDA pathways remain high entry barriers, steering newcomers toward software, analytics, and service models linked to the lumpectomy market.

Lumpectomy Industry Leaders

Hologic, Inc

Stryker Corporation

Becton, Dickinson and Company

Medtronic plc

Merit Medical Systems, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: BD committed USD 2.5 billion to U.S. manufacturing upgrades, addressing recurring device shortages that have impacted seed localization supply.

- March 2025: Perimeter Medical filed a PMA for its next-generation B-Series OCT with ImgAssist AI 2.0 after pivotal trials confirmed residual-cancer reduction.

- January 2025: Hologic closed a USD 350 million acquisition of Gynesonics, extending its women’s health procedural portfolio.

Global Lumpectomy Market Report Scope

| Surgical Excision Instruments |

| Imaging & Guidance Systems |

| Margin-Assessment Devices |

| Localisation Consumables & Seeds |

| Adjunctive Therapies & Accessories |

| Wire-Guided Localisation (WGL) |

| Radio-frequency Tag Localisation |

| Magnetic Seed Localisation |

| Radar-Reflector Localisation |

| Radio-isotope Localisation (RSL) |

| Hospitals |

| Ambulatory Surgical Centres (ASCs) |

| Specialty Cancer Clinics |

| Others |

| Standard Lumpectomy |

| Oncoplastic Lumpectomy |

| Re-Excision Lumpectomy |

| APBI-Assisted Lumpectomy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Surgical Excision Instruments | |

| Imaging & Guidance Systems | ||

| Margin-Assessment Devices | ||

| Localisation Consumables & Seeds | ||

| Adjunctive Therapies & Accessories | ||

| By Localisation Technology | Wire-Guided Localisation (WGL) | |

| Radio-frequency Tag Localisation | ||

| Magnetic Seed Localisation | ||

| Radar-Reflector Localisation | ||

| Radio-isotope Localisation (RSL) | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centres (ASCs) | ||

| Specialty Cancer Clinics | ||

| Others | ||

| By Procedure Type | Standard Lumpectomy | |

| Oncoplastic Lumpectomy | ||

| Re-Excision Lumpectomy | ||

| APBI-Assisted Lumpectomy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the lumpectomy market in 2025?

The lumpectomy market size is USD 1.94 billion in 2025 and is projected to reach USD 2.73 billion by 2030 at a 7.16% CAGR.

Which product category dominates sales?

Imaging & Guidance Systems lead with a 38.2% share, driven by real-time fluorescence and OCT platforms.

Which localization technology is growing fastest?

Magnetic seed localization is advancing at 8.1% CAGR, supported by 99.9% placement success and improved patient comfort.

Why are ambulatory surgical centers gaining share?

ASCs offer 25-50% cost savings and shorter wait times, leading to a 6.4% CAGR in lumpectomy volumes through 2030.

What is the top regional growth opportunity?

Asia Pacific is forecast to expand at 8.5% CAGR, fueled by expanding screening programs and rising investments in surgical infrastructure.

How is AI impacting lumpectomy procedures?

AI-driven imaging and planning systems provide 3D visualization and margin assessment, reducing re-excisions and streamlining surgery.

Page last updated on: