Oculoplastic Surgery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 11.61 Billion |

| Market Size (2031) | USD 16.07 Billion |

| Growth Rate (2026 - 2031) | 6.72% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oculoplastic Surgery Market Analysis by Mordor Intelligence

The Oculoplastic Surgery Market size is expected to grow from USD 10.88 billion in 2025 to USD 11.61 billion in 2026 and is forecast to reach USD 16.07 billion by 2031 at 6.72% CAGR over 2026-2031.

Consistent demand from aging populations, the rapid roll-out of AI-assisted surgical planning, and continuing patient preference for procedures that improve both function and appearance underpin this expansion. Technology lowers recovery times while improving accuracy, which broadens patient acceptance and strengthens reimbursement arguments. Consolidation among device makers and specialty providers allows the largest firms to bundle implants, imaging, and practice-management tools, thereby locking in surgeons and capturing recurring revenue. Finally, social-media-driven cosmetic consciousness, especially in younger cohorts, turns elective interventions into lifestyle purchases that propel global procedure volumes.

Key Report Takeaways

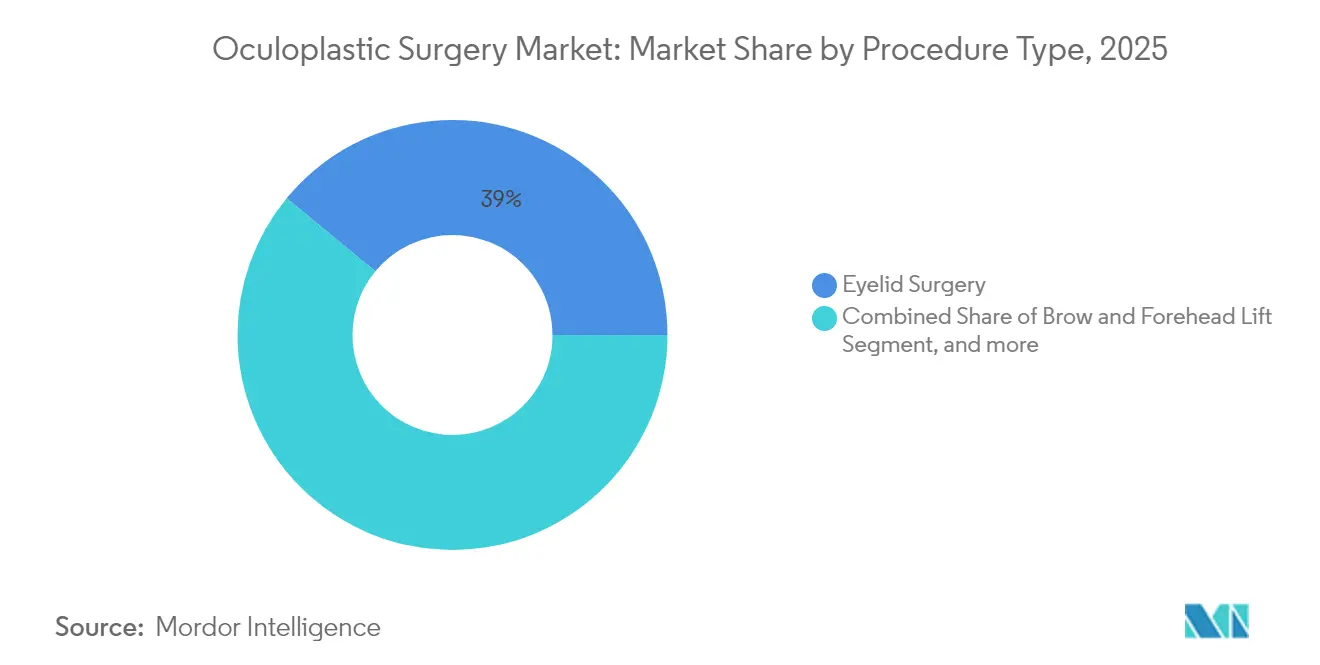

- By procedure type, eyelid surgery led with 39.02% of oculoplastic surgery market share in 2025, while brow & forehead lift recorded the fastest CAGR at 8.64% through 2031.

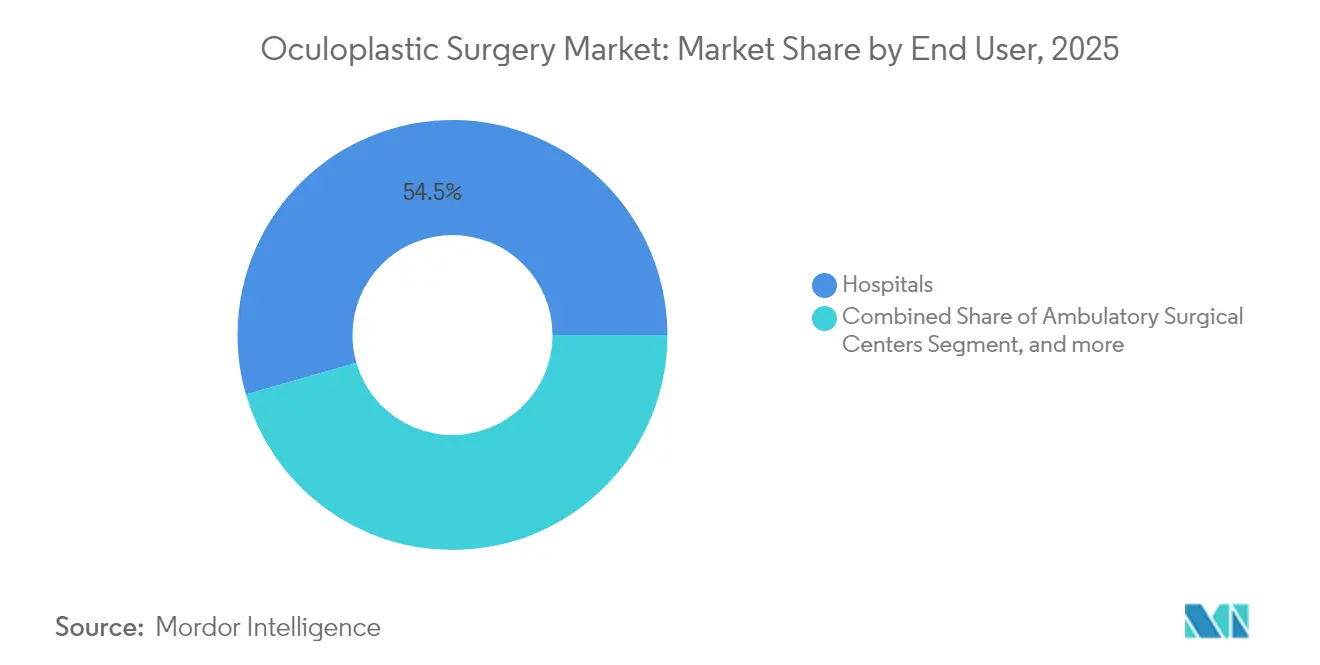

- By end user, hospitals held 54.47% share of the oculoplastic surgery market size in 2025, whereas ambulatory surgical centers are projected to expand at 9.11% CAGR to 2031.

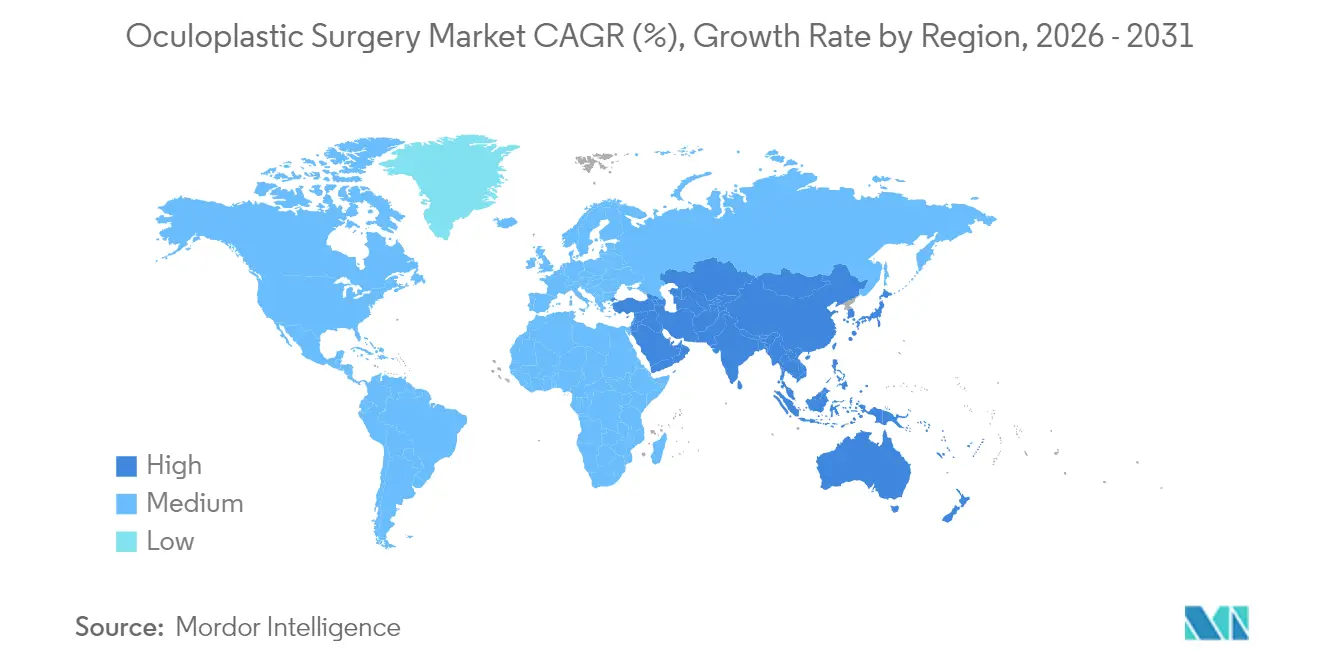

- By geography, North America dominated with 36.25% share of the oculoplastic surgery market in 2025, but Asia Pacific is advancing at a 7.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Oculoplastic Surgery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising geriatric population with eyelid needs | +1.8% | North America and Europe dominant | Long term (≥ 4 years) |

| Growing incidence of thyroid eye disease | +1.2% | Higher prevalence in developed markets | Medium term (2-4 years) |

| Uptake of minimally invasive blepharoplasty | +1.5% | North America and Europe lead, Asia Pacific follows | Short term (≤ 2 years) |

| AI-assisted pre-operative planning | +0.9% | Early use in North America and Europe, global diffusion | Medium term (2-4 years) |

| Human amniotic graft adoption | +0.7% | Primarily North America and Europe | Medium term (2-4 years) |

| Social-media-driven cosmetic demand | +1.4% | Asia Pacific, Latin America, Middle East | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Population with Functional & Aesthetic Eye-Lid Concerns

The surge in individuals aged 65 and above adds millions of potential candidates for functional eyelid repair and cosmetic enhancement. In the United States alone, this population will grow from 56.1 million in 2020 to 73.1 million by 2030, expanding the core patient base that seeks blepharoplasty to restore superior visual fields and facial harmony. Techniques such as the minimally invasive eyelid lift preserve orbital fat and minimize bruising, aligning clinical outcomes with the recovery expectations of older adults. Because Medicare reimburses functional blepharoplasty when documented visual field loss is improved, surgeons can justify intervention despite fee-schedule pressure. Longer life expectancy further extends the window during which patients expect clear vision and a refreshed appearance, generating repeat business for touch-up procedures and adjunct treatments. Practices that integrate pre-surgical ocular surface optimization and post-operative dry-eye management are best placed to capture this demographic tailwind.[1]American Academy of Ophthalmology, “Minimally Invasive Eyelid Lift Technique Shows Faster Recovery,” aao.org

Growing Incidence of Thyroid Eye Disease & Orbital Tumors

Thyroid eye disease now benefits from targeted biologics that calm inflammation, allowing surgery to be timed when tissue is less friable and results are more predictable. Post-biologic decompressions remove 3.5–7.6 mm of proptosis with lower diplopia rates, reinforcing surgeon confidence and raising patient satisfaction. TED often requires staged lid, strabismus, and orbital work, which lifts revenue per case while creating barriers to entry for non-specialists. Orbital tumors, although less common, demand high-resolution imaging and navigation systems that large device firms bundle into integrated platforms. Centers that can provide same-day endocrine and oculoplastic consultation capture referrals from community endocrinologists and primary-care physicians. Regional variations in iodine sufficiency shape disease clustering and create opportunities for branded centers of excellence in Europe, East Asia, and parts of the Gulf states.[2]Ophthalmic Plastic & Reconstructive Surgery, “Endoscopic Orbital Decompression Outcomes,” journals.lww.com

Rapid Uptake of Minimally Invasive Blepharoplasty & Brow-Pexy Techniques

Barbed PDO sutures, 2–3 mm access ports, and transconjunctival fat repositioning allow surgeons to treat functional dermatochalasis and cosmetic concerns without lengthy incisions. Recovery now averages 7 days instead of 14, which eliminates the career downtime that once deterred younger professionals. Training courses offered by device makers create revenue, but more importantly build surgeon loyalty to specific platforms. Most minimally invasive cases shift from hospital operating rooms to accredited office suites, lifting surgeon control of scheduling and ancillary income. High satisfaction rates translate into positive online reviews that lower marketing spend per lead and compound local demand. The diffusion curve mirrors LASIK adoption two decades earlier, suggesting that the oculoplastic surgery market will continue redistributing volume toward lower-acuity sites in urban and suburban settings

AI-Assisted Pre-Operative Planning Improving Surgical Outcomes

Machine learning models now map periorbital distances, simulate outcomes at multiple incision points, and forecast lid height to within 0.5 mm. These predictive tools shorten chair-time consultations and support informed consent with photographic renders that set realistic expectations. Artificial intelligence also flags CPT combinations, reducing under-billing and payor denials that erode practice margins. Large practices refine proprietary algorithms with each case, creating data moats that discourage commoditization. Regulators have begun issuing guidance on algorithm change control, so early compliance will protect first-mover advantage. Younger patients actively request AI visualization during consultations, framing the technology as a standard of care rather than a novelty.[3]Plastic and Reconstructive Surgery – Global Open, “AI-Based Coding Automation in Oculoplastic Practice,” journals.lww.com/prsgo

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost and limited reimbursement | -1.4% | Acute in emerging markets | Short term (≤ 2 years) |

| Shortage of trained oculoplastic surgeons | -0.8% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Peri-operative infection risk costs | -0.6% | Higher impact in developing health systems | Medium term (2-4 years) |

| Competition from nonsurgical alternatives | -1.1% | North America and Europe, rising in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost & Limited Reimbursement

The 5.4% cut to the 2024 Medicare conversion factor forces U.S. oculoplastic practices to chase volume or pivot toward cash-pay cosmetic work. Similar dynamics occur in Europe where diagnosis-related-group payments lag inflation. Hospitals respond by moving lower-risk cases into ambulatory centers, thus retaining surgeons while shedding inpatient overhead. In Asia Pacific and Latin America, partial insurance coverage leaves many patients self-funding, which suppresses uptake of multi-step reconstructions. Price disparities have fueled a medical-tourism circuit that routes cost-sensitive patients to centers in Turkey, Thailand, and Colombia. Digital platforms that quote all-inclusive surgical packages are altering competitive boundaries by shifting demand across borders.

Shortage of Fellowship-Trained Oculoplastic Surgeons in Low-Income Regions

Global ophthalmology faces a projected 30% clinician deficit by 2035, with the shortfall felt most acutely in rural provinces and low-income countries. Fellowship seats remain limited, and matching rates hover below 55%, constraining graduate output. The vacuum invites task-shifting to general ophthalmologists, although complex orbit cases remain beyond their scope. Tele-mentoring and AI-driven diagnostics extend specialist reach, yet legal liability and bandwidth gaps slow adoption. International non-governmental organizations fund regional training hubs, but retention is difficult when graduates migrate to urban private practice. Scalable solutions may hinge on modular fellowships that blend virtual reality simulators with brief on-site intensives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Eyelid Dominance and Brow Acceleration

Eyelid Surgery accounted for 39.02% of oculoplastic surgery market size in 2025, confirming longstanding dominance that blends functional necessity with cosmetic demand. Upper-lid blepharoplasty remains covered by many payors when visual-field testing proves obstruction, which preserves a reliable reimbursement stream. Surgeons have refined incision placement beneath natural folds, while fat-preservation philosophies limit hollowing that once compromised aesthetics. Concurrently, rising uptake of laser skin tightening enhances results without added incisions.

The brow & forehead lift category is expanding at 8.64% CAGR toward 2031, making it the fastest segment inside the oculoplastic surgery market. Endoscopic platforms now permit 1 cm hairline incisions that anchor the brow on absorbable screws, cutting convalescence to under 10 days. Younger patients seek subtle brow elevation paired with toxin maintenance, building a pipeline for eventual surgical conversion. Cross-selling opportunities emerge when surgeons coordinate upper-lid and brow work in a single sitting, optimizing theatre time and improving per-case revenue. These dynamics maintain eyelid dominance yet position brow procedures to capture an outsized growth share.

By End User: Hospital Stronghold Meets ASC Momentum

Hospitals held 54.47% of oculoplastic surgery market size in 2025 because they manage high-acuity cases such as orbital decompression that need intensive monitoring. Integrated imaging, pathology, and intensive-care resources remain persuasive for complex cases, even as cost scrutiny mounts. Academic centers also sustain demand by running fellowship programs that funnel trainees through operating lists, guaranteeing procedure flow and device utilization.

Ambulatory Surgical Centers will grow 9.11% CAGR to 2031 and are reshaping the oculoplastic surgery market with nimble scheduling and lower overhead. Procedural migration accelerates as insurers approve site-of-service differentials that share savings with patients. Surgeons gain autonomy over staff selection and postoperative protocols, while bundled implant pricing further lifts margins. Specialty eye clinics and office-based suites bridge hospital capability and ASC efficiency, offering advanced anesthesia and sterile environments without the bureaucracy of large systems. The competitive map will hinge on which setting can validate safety equivalence while maintaining price advantage.

Geography Analysis

North America commands 36.25% of the oculoplastic surgery market share in 2025 and continues to benefit from strong fellowship pipelines, high awareness, and sophisticated payor networks. Conversion-factor cuts in 2024 encourage practices to add cash-pay cosmetic lids and brow lifts, smoothing revenue volatility. Office-based surgery suites, representing 2.2% of procedures in Q1 2023, provide surgeons with facility fees once captured by hospitals, reinforcing regional leadership. Consolidators backed by private equity expand multi-state networks that negotiate supply contracts at scale and invest in AI imaging to lure referrals.

Asia Pacific registers the fastest regional CAGR at 7.55% through 2031 as expanding middle classes prioritize appearance in professional and social contexts. Government-supported universal health schemes in South Korea and Japan reimburse functional blepharoplasty, while private payment covers cosmetic add-ons. Device leaders such as Alcon dedicate USD 828 million in 2023 R&D toward lens and imaging products tuned to Asian anatomy, signaling a long-term commitment. Meanwhile, China’s National Medical Products Administration tightens device approval timelines, ensuring quality but lengthening market-entry planning cycles.

Europe maintains moderate growth based on universal coverage and strong clinical governance. Aging demographics push functional lids and brow lifts upward, yet austerity measures cap reimbursement growth. Innovative techniques like anterior ptosis repair remain favored by 66% of surgeons surveyed in the United Kingdom. The Middle East & Africa and South America trail in share yet display pockets of rapid adoption. Brazilian surgeons pioneer microscope-integrated optical coherence tomography that improves macular visualization and demonstrates the region’s capacity to leapfrog with advanced tools.

Competitive Landscape

The oculoplastic surgery market features moderate fragmentation with global device multinationals, specialty pharmaceutical firms, and nimble startups all vying for surgeon loyalty. Alcon, Johnson & Johnson Vision, and Carl Zeiss Meditec use broad portfolios and global sales teams to influence procedure technique and product choice. Alcon’s USD 430 million LENSAR acquisition and majority stake in Aurion Biotech illustrate a strategy to wrap femtosecond lasers and regenerative cell therapy into one ecosystem, raising switching costs for surgeons.

Technology leadership remains the central battleground. Carl Zeiss Meditec lifted first-half fiscal-year revenue 10.9% to EUR 1,050.5 million after acquiring Dutch Ophthalmic Research Center, which broadened the refractive and retina line-up. KARL STORZ’s purchase of Asensus Surgical adds the LUNA system with intra-operative augmented intelligence, signaling a push into robotics that promises tremor-free dissection and sub-millimeter precision. Startups focusing on AI-driven pre-operative planning or bioresorbable implants attract venture funding but often partner with larger players for distribution muscle.

Regulatory compliance is a potent differentiator. An FDA warning letter to Integra LifeSciences over quality-system lapses halted implant shipments and opened doors for competitors that could certify uninterrupted supply. Providers increasingly demand post-market surveillance data, pressuring vendors to finance long-term registries. In emerging economies, the first vendor to navigate local approval frameworks and organize surgeon training often captures entrenched share. Intense merger activity is likely to continue as strategic buyers fill product gaps and startups monetize innovations.

Oculoplastic Surgery Industry Leaders

TEKNO-MEDICAL Optik-Chirurgie GmbH

B. Braun Melsungen AG

Katena (Blink Medical Ltd.)

Karl Storz SE & Co. KG

Integra LifeSciences Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Alcon announced its agreement to acquire LENSAR, Inc. for approximately USD 356 million, enhancing its cataract surgery technology portfolio with the ALLY Robotic Cataract Laser Treatment System and proprietary Streamline software. The acquisition targets improved efficiency and precision in cataract procedures, addressing the high prevalence of visually significant astigmatism and expanding femtosecond laser technology adoption.

- March 2025: Alcon acquired a majority interest in Aurion Biotech, which develops AURN001, a clinical-stage allogeneic cell therapy for corneal edema due to corneal endothelial disease. The therapy combines human corneal endothelial cells with a rho kinase inhibitor, with U.S. phase 3 trials planned for late 2025 to address global corneal tissue shortages.

- February 2025: Lumenis launched OptiLIFT, a noninvasive device utilizing Dynamic Muscle Stimulation technology to treat lower lid laxity and impaired blinking. Clinical studies demonstrated 75% reduction in lid laxity and 70% improvement in blinking quality, targeting the significant gap in non-surgical treatment options for conditions affecting over 60% of dry eye patients.

- January 2025: Cencora completed the acquisition of an 85% stake in Retina Consultants of America from Webster Equity Partners for USD 4.6 billion, highlighting significant investment in ophthalmology services and demonstrating the sector's attractiveness for large-scale healthcare consolidation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the global oculoplastic surgery market as the total yearly revenue generated by functional and aesthetic surgical procedures on the eyelids, orbit, tear ducts, and adjoining facial structures, performed in hospitals, ambulatory surgery centers, and licensed specialty clinics. The scope includes related instruments, implants, and equipment sales that are billed as part of the procedure package.

Scope exclusion: stand-alone non-surgical injectables such as botulinum toxin and dermal fillers are not tallied here.

Segmentation Overview

- By Procedure Type

- Eyelid Surgery

- Brow & Forehead Lift

- Facelift Adjacent Oculoplastic

- Lacrimal & Orbital Decompression

- Pediatric Oculoplastic

- Others Procedure Type

- By End User

- Hospitals

- Ambulatory Surgical Centers

- Specialty Eye Clinics

- Cosmetic Surgery Centers

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews and structured surveys with oculoplastic surgeons, theater nurses, ASC managers, and distributor executives across North America, Europe, and Asia gave us real-time insights on case mix shifts, typical consumable loads, and regional price ladders, allowing us to challenge desktop assumptions and fine-tune conversion factors.

Desk Research

Our analysts reviewed public sources such as the American Society of Plastic Surgeons, WHO demographic tables, FDA device approvals, United Nations Comtrade shipment data, and national health expenditure dashboards, which together outline procedure volumes, aging population trends, reimbursement rules, and trade flows of surgical kits. Company 10-Ks, investor decks, and clinical trial registries then helped us track average selling prices of orbital implants and emerging laser platforms.

We layered in select paid datasets, D&B Hoovers for company revenue splits, Dow Jones Factiva for procedure pricing news, and Questel for patent momentum, to test market saturation signals. The sources listed illustrate our approach and are not exhaustive.

Market-Sizing & Forecasting

We start with a top-down reconstruction that multiplies annual eyelid, brow, orbital, and lacrimal surgery counts (gleaned from procedure registries and insurer billing codes) by validated regional average procedure values, then adjust for hospital-owned ASC leakage and cash-pay cosmetic volumes. A selective bottom-up check, supplier roll-ups of implants and disposable packs, anchors the totals before reconciliation. Key variables feeding our multivariate regression forecast include 65+ population growth, thyroid eye disease prevalence, elective surgery wait times, technology-driven ASP uplift, and ASC penetration. Gaps in raw counts are bridged with weighted regional proxies or three-year rolling means.

Data Validation & Update Cycle

Outputs pass a two-step analyst review, variance thresholds trigger re-contact of sources, and every model is refreshed annually, with mid-cycle updates if regulatory or reimbursement shocks alter baseline assumptions.

Why Mordor's Oculoplastic Surgery Baseline Commands Reliability

Published market figures often diverge because firms choose different procedure baskets, price benchmarks, and refresh cadences. We acknowledge these variables upfront and specify them inside every workbook so clients can reproduce the math.

Key gap drivers versus other studies include our exclusion of non-surgical injectables, our weighting of ASC cash-pay volumes, and our yearly refresh cadence, whereas others may mix cosmetic fillers into totals or freeze demographic baselines for several years.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 10.88 B (2025) | Mordor Intelligence | - |

| USD 9.86 B (2024) | Global Consultancy A | averages hospital charge data without ASC adjustment |

| USD 11.35 B (2024) | Research Publisher B | applies uniform ASP across regions and includes some injectable revenue |

The comparison shows that, by clearly isolating surgical revenue and by updating inputs yearly, Mordor Intelligence delivers a balanced, transparent baseline that managers can track and replicate with confidence.

Key Questions Answered in the Report

What is the projected value of the oculoplastic surgery market by 2031?

The oculoplastic surgery market size is expected to reach USD 16.07 billion by 2031, underpinned by a 6.72% CAGR.

Which procedure currently dominates the market?

Eyelid Surgery leads, accounting for 39.02% of oculoplastic surgery market share in 2025.

Why are ambulatory surgical centers growing faster than hospitals?

ASCs deliver lower costs, shorter scheduling delays, and physician control, and they are forecast to expand at 9.11% CAGR through 2031.

Which geographic region is growing the fastest?

Asia Pacific is forecast to grow at 7.55% CAGR due to rising middle-class spending and social-media-driven aesthetic demand.

How is artificial intelligence changing oculoplastic practice?

AI now simulates surgical outcomes, optimizes incision planning, and automates billing, all of which cut revision rates and boost practice margins.

What are the main restraints on market growth?

High procedure costs with limited reimbursement and a shortage of fellowship-trained surgeons in low-income regions slow overall expansion.

Page last updated on: