Breast Reconstruction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

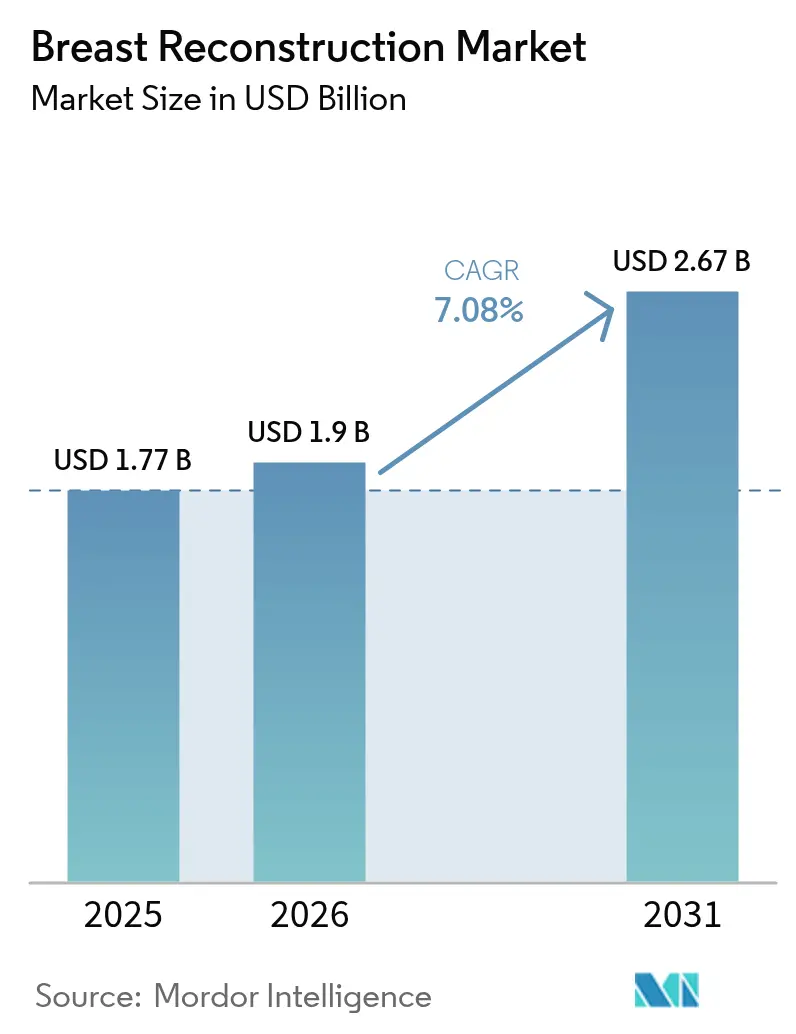

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.67 Billion |

| Growth Rate (2026 - 2031) | 7.08% CAGR |

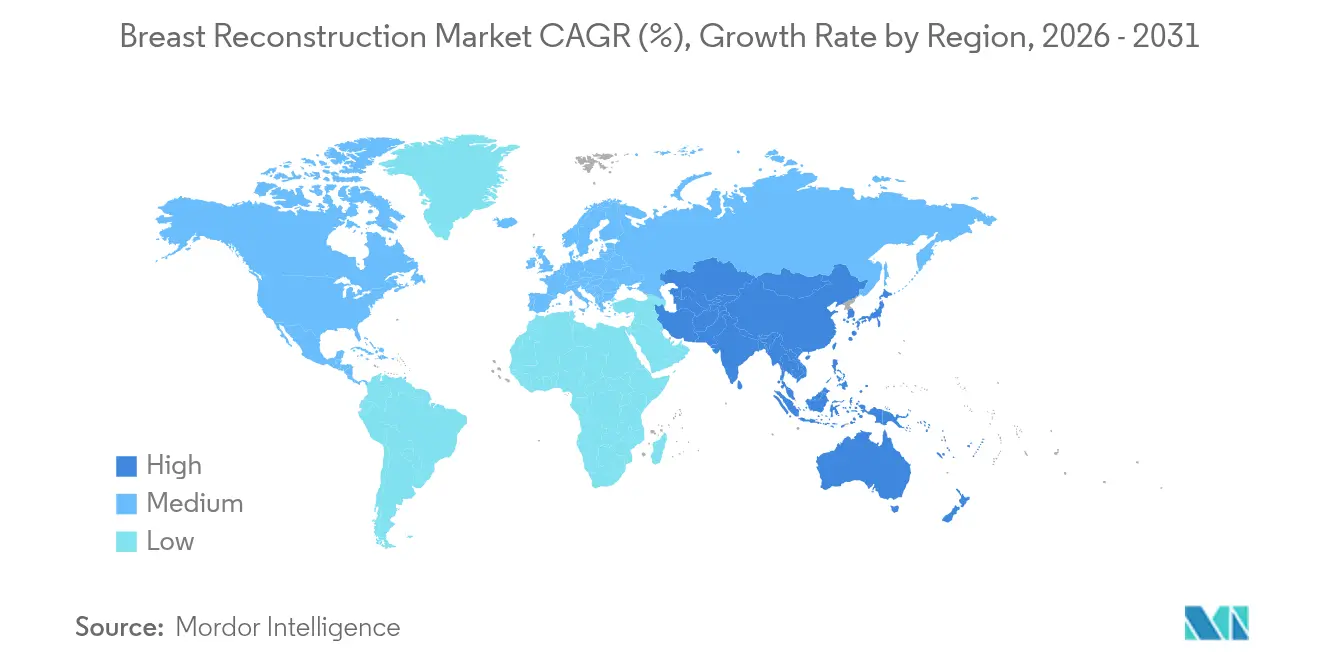

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Breast Reconstruction Market Analysis by Mordor Intelligence

The breast reconstruction market size is expected to grow from USD 1.77 billion in 2025 to USD 1.9 billion in 2026 and is forecast to reach USD 2.67 billion by 2031 at 7.08% CAGR over 2026-2031. This growth links directly to rising breast-cancer incidence, expanding reimbursement mandates, and innovations such as artificial-intelligence (AI) imaging and 3-D bioprinted scaffolds[1]American Cancer Society, “Cancer Facts & Figures 2025,” cancer.org. A 91% five-year survival rate in major oncology regions enlarges the eligible patient pool, while emerging tissue-engineering platforms reduce revision surgeries and improve long-term outcomes. Market leadership currently rests with implants, yet rapid gains in regenerative products and biologic meshes are shifting surgeon preference toward hybrid procedures that blend form stability with natural tissue integration. Geographically, North America holds a 37.72% breast reconstruction market share in 2024, and Asia-Pacific is advancing at 9.22% CAGR, supported by the World Health Organization’s forecast of a 38% global breast-cancer case rise by 2050.

Key Report Takeaways

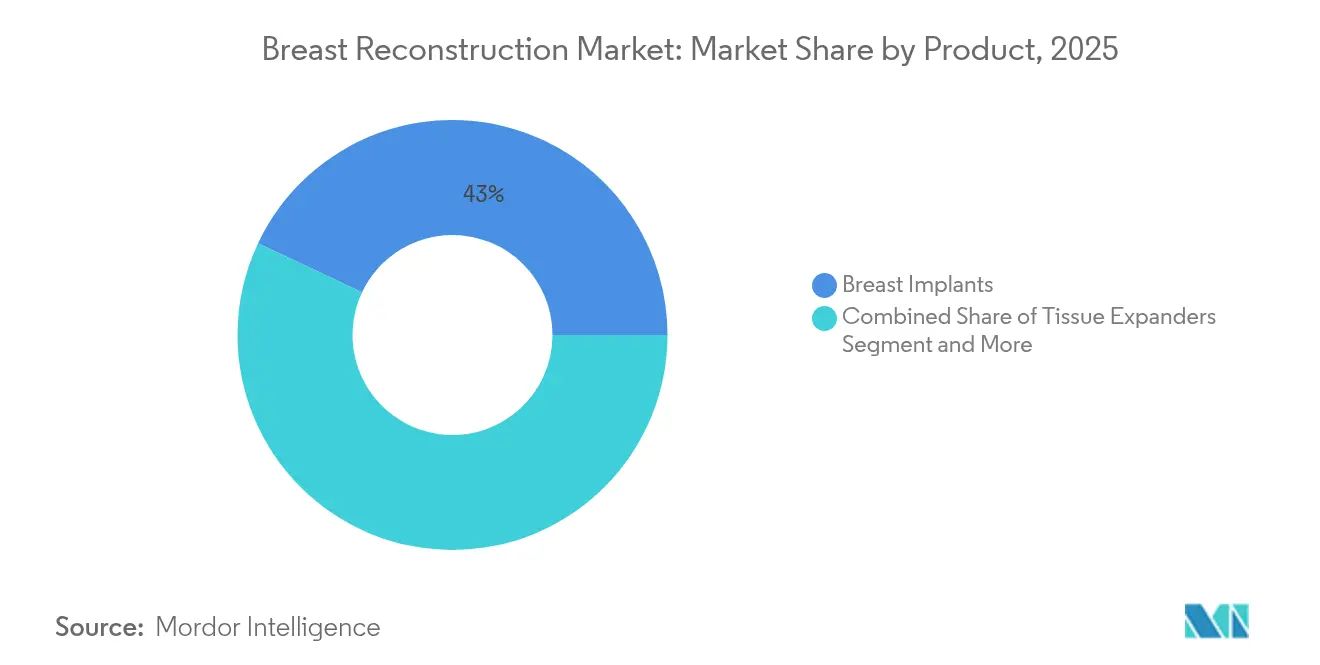

- By product, breast implants led with 42.98% revenue share in 2025; 3-D bioprinted scaffolds are projected to expand at a 14.64% CAGR through 2031.

- By material, silicone captured 45.05% of the breast reconstruction market size in 2025, while biologic mesh is growing fastest at 8.74% CAGR.

- By reconstruction technique, implant-based methods commanded 63.85% of the breast reconstruction market size in 2025; hybrid approaches show the highest projected CAGR at 7.86% to 2031.

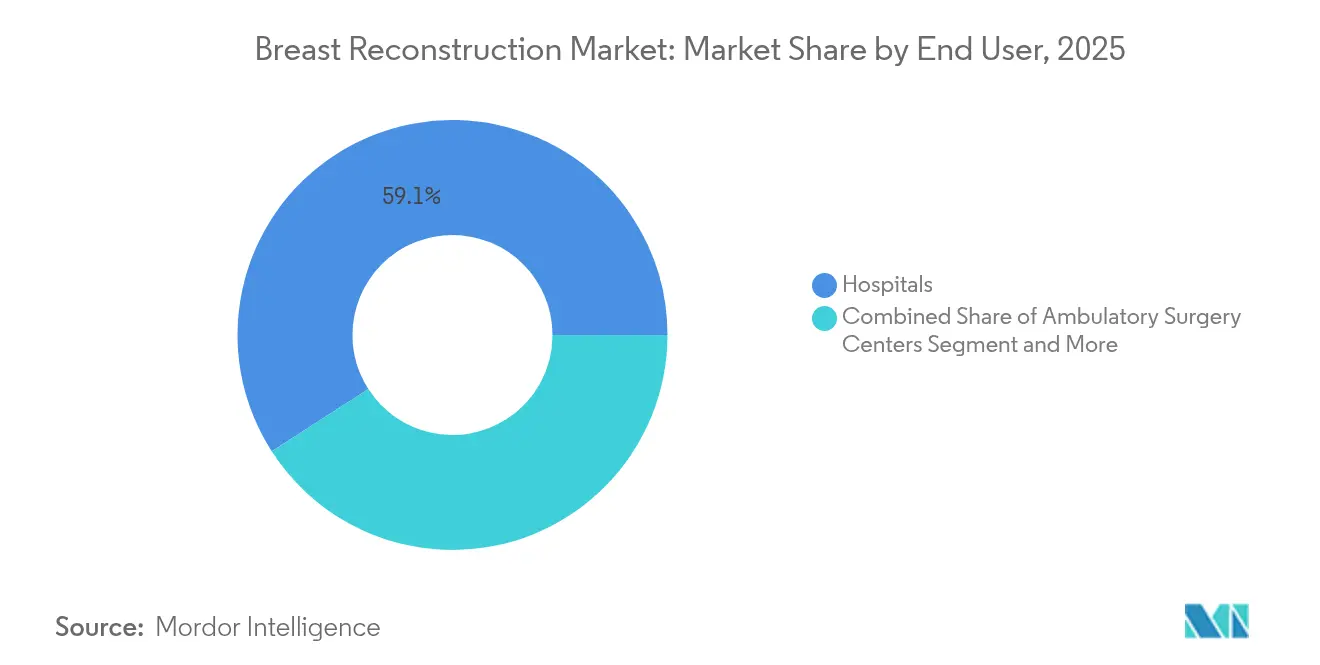

- By end user, hospitals held 59.10% market share in 2025; ambulatory surgery centers are forecast to grow at 8.25% CAGR.

- By application, post-mastectomy cancer reconstruction accounted for 68.12% of the breast reconstruction market size in 2025, whereas prophylactic procedures are advancing at 9.07% CAGR.

- By geography, North America led with 37.25% market share in 2025; Asia-Pacific records the fastest growth at 8.85% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Breast Reconstruction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidence of breast cancer | +1.8% | Global; most pronounced in Asia-Pacific and North America | Long term (≥ 4 years) |

| Growing reimbursement mandates & awareness | +1.2% | North America, EU; scaling to Asia-Pacific | Medium term (2–4 years) |

| Advancements in cohesive-gel “gummy-bear” implants | +0.9% | North America and Europe | Short term (≤ 2 years) |

| Surge in nipple-sparing & pre-pectoral mastectomies | +0.7% | North America, EU; early urban Asia-Pacific adoption | Medium term (2–4 years) |

| 3-D bioprinted regenerative implants in clinical trials | +0.6% | North America, EU; spillover to Asia-Pacific | Long term (≥ 4 years) |

| AI-guided imaging & sizing platforms | +0.5% | Developed markets worldwide | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence Of Breast Cancer

The World Health Organization projects 3.2 million new breast-cancer diagnoses per year by 2050, up 38% from current levels[2]UN News, “Breast cancer cases projected to rise by nearly 40 per cent by 2050, WHO warns,” un.org. Asia accounted for 985,400 new cases in 2022, a number expected to cross 1.4 million by 2050. Younger women under 50 and Asian American/Pacific Islander populations have shown the steepest incidence upticks, leading to longer survivorship and higher reconstruction uptake. In China and India, value-driven hospital systems are opening new operating-room slots for implant-based and hybrid procedures, creating white-space growth pockets for device makers able to offer cost-effective solutions at scale. The demographic expansion is therefore not merely numerical; it also shifts product-mix demand toward durable, low-complication implants that minimize lifetime revision risk.

Growing Reimbursement Mandates & Awareness

The Women’s Health and Cancer Rights Act guarantees comprehensive reconstruction benefits across US group health plans, and February 2025 billing-code preservation for DIEP and GAP flaps underscores regulator commitment to advanced autologous techniques. State-level actions, such as California’s July 2024 Medi-Cal policy update, broaden access to implant procedures for lower-income patients. Major private payers have redefined reconstruction as medically necessary, covering symmetry surgeries and complication management. As ambulatory centers embrace value-based payment models, surgeons gain financial incentives to adopt technologies that reduce operative time and downstream revisions, accelerating demand for AI-guided sizing software paired with cohesive-gel implants.

Advancements In Cohesive-Gel & Gummy-Bear Implants

Johnson & Johnson’s December 2024 FDA approval of MemoryGel Enhance implants, available in volumes up to 1,445 cc, addresses unmet needs among patients with larger chest walls while retaining shape-holding cohesive gel properties. Histologic analysis of 493 patients demonstrates that gel cohesiveness directly lowers leakage rates, making newer formulations safer over multi-year horizons. The FDA’s September 2024 clearance for Motiva SmoothSilk implants adds surface-texture innovations that reduce inflammatory responses[3]U.S. Food and Drug Administration, “Premarket Approval (PMA),” fda.gov. Together, these approvals validate manufacturer focus on both form stability and biocompatibility, guiding hospitals toward next-generation devices that can be inserted pre-pectorally without sacrificing durability.

Surge In Nipple-Sparing & Pre-Pectoral Mastectomies

Pre-pectoral placement above the muscle lowers post-operative pain and animation deformity, and a prospective study has shown superior nipple position maintenance versus sub-pectoral approaches. Combining nipple-sparing mastectomy with acellular dermal matrix wrapping yields strong cosmetic results in large, ptotic breasts that were once challenging to reconstruct. Stanford University’s clinical trial on decellularized nipple-areolar complex grafts may eliminate multi-stage reconstruction, signaling a future where aesthetic completeness is achieved in a single setting. Higher satisfaction rates encourage more patients to choose immediate reconstruction, bolstering demand for biologic meshes and smart implant systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure & device costs in emerging markets | −1.1% | Asia-Pacific emerging, Latin America, MEA | Long term (≥ 4 years) |

| Implant-safety concerns (BIA-ALCL, capsular contracture) | −0.8% | Global; highest in developed markets | Medium term (2–4 years) |

| Shortage of microsurgical expertise for autologous flaps | −0.6% | Global; acute in rural and emerging areas | Long term (≥ 4 years) |

| ESG-driven silicone & ADM supply-chain disruptions | −0.4% | Global; production-hub concentration risks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure & Device Costs In Emerging Markets

Average out-of-pocket costs for implant reconstruction in Southeast Asia exceed 45% of median annual income, limiting uptake outside major urban centers. Local payers seldom reimburse advanced biomaterials, forcing surgeons to rely on saline implants that carry higher revision risk. Multinational device firms must localize manufacturing or offer tiered price structures to penetrate these cost-sensitive regions. Government pilot programs in India and Thailand to subsidize reconstruction for low-income patients have shown positive early results but remain limited in scope.

Implant-Safety Concerns (BIA-ALCL, Capsular Contracture)

As of 2025, 1,290 global cases of breast implant-associated anaplastic large-cell lymphoma have been recorded, primarily linked to textured devices. Capsular contracture affects 2.3%–4.1% of implants and is the leading cause of revision surgery. Heightened surveillance requirements increase post-market study costs and may deter smaller entrants. Patient advocacy groups continue to demand transparent safety data, pressuring manufacturers to publish long-term trials and accelerate innovation in smooth-surface or biointegrative materials.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Bioprinting Disrupts Traditional Implant Dominance

Breast implants retained 42.98% share of the breast reconstruction market in 2025, driven by broad surgeon familiarity and predictable outcomes. Yet 3-D bioprinted scaffolds and regenerative implants are growing at a 14.64% CAGR, signaling a pivot to tissue-engineering platforms that minimize foreign-body responses and enable personalized shapes. Traditional tissue expanders still bridge staged reconstructions, but their role is narrowing as pre-pectoral, single-stage procedures gain popularity.

The breast reconstruction industry increasingly values devices that reduce revision rates. AI-guided sizing software pairs with cohesive-gel implants to deliver custom profiles, while poly-4-hydroxybutyrate scaffolds support natural tissue ingrowth. BD’s STANCE trial on GalaFLEX LITE highlights bioabsorbable meshes that address the 54% capsular-contracture recurrence in revision surgeries. Such innovations are reshaping hospital procurement criteria toward long-term cost savings and patient-reported outcomes.

By Material Type: Biologic Mesh Gains Ground Against Silicone

Silicone held 45.05% of breast reconstruction market share in 2025, backed by decades of refinement and recent FDA clearances for larger-volume options. Biologic mesh, however, leads growth at 8.74% CAGR as surgeons seek materials that promote vascularized tissue integration and reduce chronic inflammation. Saline implants remain relevant for patients with specific safety concerns but are gradually losing ground.

In parallel, synthetic meshes face heightened scrutiny over permanence and infection risk, spurring demand for biodegradable alternatives. Research into environmental footprints of implant supply chains also favors biologic and biodegradable materials with lower carbon impacts, aligning procurement policies with hospital ESG targets.

By Reconstruction Technique: Hybrid Approaches Bridge Traditional Methods

Implant-based reconstruction commanded 63.85% share of the breast reconstruction market size in 2025 due to its speed and lower technical complexity. Hybrid techniques that combine implant volume with autologous fat grafting are expanding at 7.86% CAGR, offering a middle ground between form stability and natural feel. Autologous tissue flaps remain the gold standard for patients undergoing radiation but are limited by microsurgical workforce constraints.

Pre-pectoral placement paired with acellular dermal matrices delivers improved aesthetic outcomes and shorter recovery times, encouraging surgeons to adopt hybrid workflows. Fat grafting further enhances contour and symmetry, making hybrid methods a flexible option adaptable to diverse patient anatomies.

By End User: Ambulatory Centers Capture Market Share

Hospitals accounted for 59.10% of procedures in 2025, yet ambulatory surgery centers are growing at 8.25% CAGR as payers emphasize cost containment. The Centers for Medicare & Medicaid Services increased ASC conversion factors for 2025, making outpatient reconstruction financially attractive. Specialty aesthetic clinics handle complex revisions and augmentations, offering tailored care but commanding premium pricing.

The breast reconstruction market is therefore decentralizing, with ASCs leveraging shorter stay times and bundled-payment models to win cases traditionally performed in full-service hospitals. Device makers now target training programs and turnkey equipment packages specifically for ASC environments.

By Application: Prophylactic Procedures Drive Growth

Post-mastectomy cancer reconstruction made up 68.12% of the breast reconstruction market size in 2025, but prophylactic mastectomy cases are accelerating at 9.07% CAGR, influenced by wider genetic testing and heightened risk awareness. Trauma-related and congenital reconstructions remain smaller segments yet often draw on the most advanced hybrid techniques due to unique anatomical challenges.

Insurance coverage for BRCA-positive prophylactic surgery under the Women’s Health and Cancer Rights Act broadens eligibility, and younger patients typically opt for cohesive-gel or bioprinted implants that promise fewer lifetime revisions. This shift propels demand for premium device lines and long-term follow-up services.

Geography Analysis

North America led the breast reconstruction market with 37.25% share in 2025, underpinned by federal coverage mandates and a dense network of board-certified plastic surgeons. The region also hosts many pivotal trials, allowing earlier access to next-generation implants and biologic meshes. Market expansion is expected to remain steady as AI-guided planning tools penetrate large hospital systems and ambulatory surgery centers.

Asia-Pacific is the fastest-growing region, forecast at 8.85% CAGR through 2031. Rising breast-cancer prevalence, expanding middle-class incomes, and cultural normalization of reconstruction fuel procedure volumes, while Japan’s immediate-reconstruction rate of 11.2% illustrates latent upside. Government initiatives to subsidize mastectomy care in China and India are slowly being extended to reconstruction, opening a path for cost-optimized implants and locally manufactured meshes.

Europe sustains moderate growth under universal healthcare frameworks that ensure baseline access, though procedure uptake varies by country. Latin America and the Middle East/Africa remain nascent markets, with growth contingent on surgical-infrastructure build-out and clinician-training partnerships. Multinational firms that localize production and align product portfolios with regional reimbursement tiers will capture early mover advantages.

Competitive Landscape

The breast reconstruction market shows moderate concentration. AbbVie-Allergan and Johnson & Johnson-Mentor command large installed bases through broad implant portfolios and strong distribution. Motiva’s surface-textured SmoothSilk implants and Establishment Labs’ smart-sensor prototypes illustrate insurgent pressure on incumbents. Sientra’s April 2024 asset sale after bankruptcy highlights mid-tier vulnerability to litigation and supply-chain shocks.

Strategic responses include portfolio diversification and selective acquisitions. BD’s investment in bioabsorbable scaffolds via the GalaFLEX LITE trial positions it in the high-growth mesh sub-segment, while larger players are exploring AI partnerships to bundle imaging platforms with premium implants. Meanwhile, regional manufacturers in Asia-Pacific gain share by offering price-tiered silicone devices that meet local regulatory standards.

Industry barriers remain high due to FDA and EU MDR approval costs, yet technological differentiation presents viable entry paths. Firms capable of integrating data analytics, sustainable materials, and surgeon-training support will outperform in a market shifting from commodity implants to holistic reconstruction solutions.

Breast Reconstruction Industry Leaders

GC Aesthetics plc

AbbVie (ALLERGAN)

Johnson & Johnson

Establishment Labs SA

Sientra Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BD enrolled the first patient in the STANCE study evaluating GalaFLEX LITE bioabsorbable scaffolds for capsular-contracture reduction in breast-implant revision.

- December 2024: Johnson & Johnson secured FDA approval for MENTOR MemoryGel Enhance implants sized 930 cc to 1,445 cc, targeting larger-volume reconstruction needs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the breast reconstruction market as the value generated by surgical products and ancillary solutions used to restore breast form after mastectomy or prophylactic breast removal, including implants, tissue expanders, acellular dermal matrices, and autologous-flap consumables. Procedures for purely cosmetic augmentation, gynecomastia correction, or congenital deformity repair fall outside this scope.

Scope Exclusion: Revision surgeries performed ten-plus years after the original reconstruction are not counted because they respond to device aging rather than the index cancer event.

Segmentation Overview

- By Product

- Breast Implants

- Tissue Expanders

- Acellular Dermal Matrices (Biologic, Synthetic)

- 3-D Bioprinted Scaffolds & Regenerative Implants

- Other Adjunct Products (NAC prosthetics, fixation devices)

- By Material Type

- Silicone

- Saline

- Autologous Tissue

- Biologic Mesh

- Synthetic Mesh

- By Reconstruction Technique

- Implant-based

- Autologous Tissue

- Hybrid

- By End User

- Hospitals

- Ambulatory Surgery Centers

- Specialty Aesthetic Clinics

- By Application

- Post-mastectomy Cancer Reconstruction

- Prophylactic Mastectomy

- Trauma & Congenital Deformity

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with oncologic surgeons, reconstructive specialists, hospital supply managers, and regional payers across North America, Europe, and Asia-Pacific allowed us to validate mastectomy-to-reconstruction conversion rates, typical device pricing bands, and upcoming policy changes. Follow-up surveys captured patient pathway nuances that are absent in public statistics, letting us fine-tune timing assumptions.

Desk Research

We began with oncology and procedure statistics from GLOBOCAN, WHO Cancer Observatory, the American Society of Plastic Surgeons, and Eurostat, which anchor national surgical volumes.

Device approval and recall files from the US FDA PMA database, EMA CE Mark registry, and Health Canada interim orders informed product availability timelines.

Cost and reimbursement inputs drew on Medicare Physician/Supplier data, NHS tariff sheets, and Japan's MHLW fee schedule.

Financial signals pulled through D&B Hoovers and Dow Jones Factiva helped us trace revenue swings among leading implant suppliers, while PubMed articles in Plastic and Reconstructive Surgery clarified emerging techniques that shift mix toward pre-pectoral and hybrid reconstructions.

The sources above are illustrative; many additional open and proprietary references were reviewed for completeness.

Market-Sizing & Forecasting

A top-down model starts with country-level female breast-cancer incidence, applies surgery uptake ratios, and then layers procedure-specific reconstruction rates to build an addressable case pool. Bottom-up checks, supplier revenue roll-ups, and sampled average selling price x unit estimates calibrate totals. Key levers include implant ASP progression, flap procedure prevalence, insurer coverage breadth, day-case surgery shift, and emerging 3-D scaffold adoption. A multivariate ARIMA model projects each lever, and scenario bands agreed with interviewed surgeons bound the forecast through 2030. Data gaps, such as unreported outpatient volumes, are bridged by regional proxies that are later stress tested with new primary calls.

Data Validation & Update Cycle

Outputs pass a three-tier review: automated anomaly flags, analyst peer checks, and senior sign-off. Variances exceeding +/-5% versus historical trend or external benchmarks trigger re-contact of experts. Reports refresh each year, with interim revisions if device withdrawals, coding reforms, or major reimbursement moves materially shift the baseline.

Why Mordor's Breast Reconstruction Baseline Earns Trust

Published numbers differ because firms choose distinct product mixes, geographic breadth, and update cadences. We disclose our device-inclusive yet procedure-specific scope and refresh annually, which stabilizes comparisons.

Key gap drivers include competitors counting cosmetic augmentations, using list rather than transacted ASPs, or rolling forward 2021 volumes without new cancer incidence data.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.77 B | Mordor Intelligence | - |

| USD 2.10 B (2024) | Global Consultancy A | Includes cosmetic implants and rounds to manufacturer list prices |

| USD 1.57 B (2023) | Industry Association B | Excludes ADM and flap consumables; limited to five regions |

The comparison shows that our clearly framed scope, dual-sourced variables, and yearly reviews provide a balanced, reproducible baseline clients can rely on for strategic planning.

Key Questions Answered in the Report

What is the current value of the breast reconstruction market?

The market is valued at USD 1.9 billion in 2026 and is projected to reach USD 2.67 billion by 2031.

Which region is growing fastest in breast reconstruction procedures?

Asia-Pacific shows the highest growth, forecast at 8.85% CAGR through 2031 due to rising cancer incidence and expanding reimbursement.

Why are 3-D bioprinted implants considered disruptive?

They enable personalized shapes and encourage natural tissue ingrowth, reducing revision surgeries and driving a 14.64% CAGR for the segment.

How are reimbursement policies influencing market growth?

Expanded mandates like the Women’s Health and Cancer Rights Act cover reconstruction and symmetry procedures, boosting patient access and procedure volumes.

What safety concerns are affecting implant choice?

Issues such as BIA-ALCL and capsular contracture drive surgeons toward smooth-surface and biologic products with better long-term safety profiles.

Are ambulatory surgery centers important to future market expansion?

Yes, ASCs are growing at 8.25% CAGR as payers favor cost-efficient outpatient settings, increasing demand for quick-recovery implants and AI planning tools.

Page last updated on: