Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

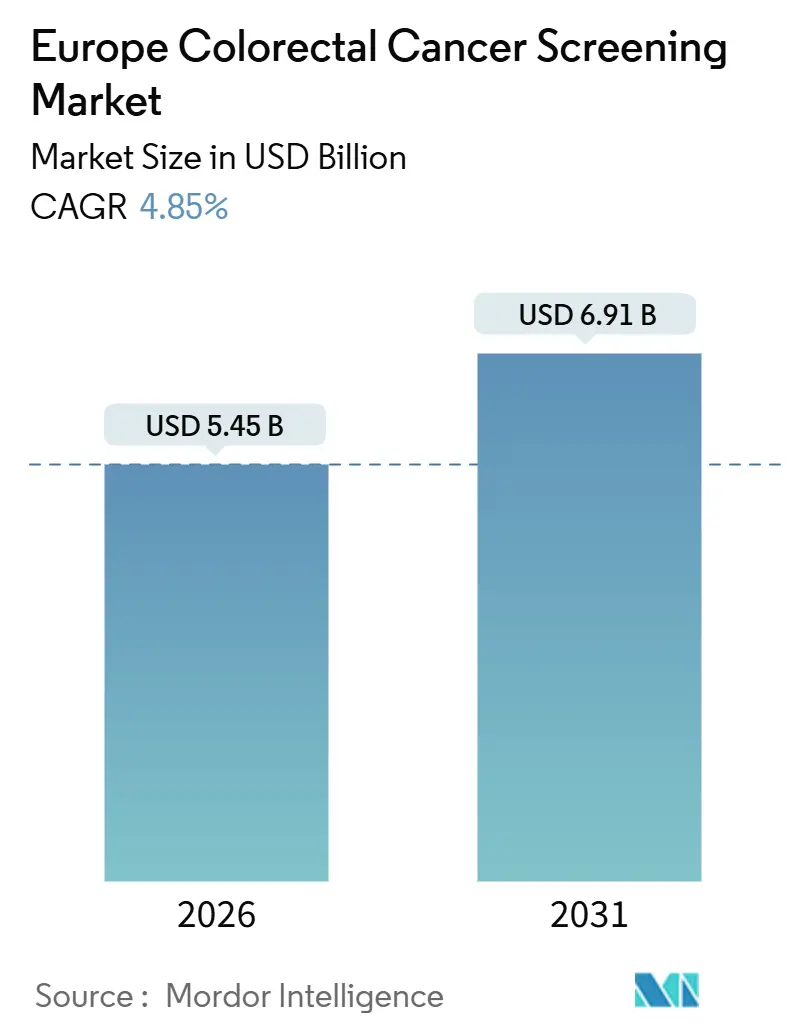

| Market Size (2026) | USD 5.45 Billion |

| Market Size (2031) | USD 6.91 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Colorectal Cancer Screening Market Analysis by Mordor Intelligence

The Europe Colorectal Cancer Screening Market size is estimated at USD 5.45 billion in 2026, and is expected to reach USD 6.91 billion by 2031, at a CAGR of 4.85% during the forecast period (2026-2031).

The measured expansion reflects well-established programs in Western Europe and rapid scale-up in Central and Eastern member states. Quantitative fecal immunochemical tests (FIT) are displacing guaiac-based methods, artificial-intelligence-guided endoscopy is lifting adenoma-detection rates, and blood-based assays are entering pilot pathways. EU Beating Cancer Plan funding, procedural reimbursement aligned to quality metrics, and patient preference for non-invasive methods underpin demand, while workforce shortages and uneven reimbursement for advanced tests temper growth. Competitive dynamics center on FIT analyzer upgrades, CADe-enabled colonoscopy systems, and early-stage blood-biomarker developers seeking European conformity assessment.

Key Report Takeaways

- By screening test type, imaging-based procedures captured 52.55% of Europe colorectal cancer screening market share in 2025, while blood-based and other emerging tests are forecast to grow at a 10.25% CAGR through 2031.

- By end user, hospitals and university medical centers held 45.53% of the Europe colorectal cancer screening market size in 2025, whereas home-based and direct-to-consumer channels expand at a 12.85% CAGR to 2031.

- By country, Germany led with 24.63% revenue share of the Europe colorectal cancer screening market size in 2025; Spain records the fastest growth at a 10.87% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Colorectal Cancer Screening Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift from gFOBT to quantitative FIT | +0.8% | Western Europe, expanding eastward | Medium term (2-4 years) |

| Rapid adoption of AI-assisted endoscopy | +1.2% | Germany, UK, France, Benelux | Short term (≤ 2 years) |

| Uptake of blood-based MCED assays | +0.9% | Germany, UK, France, Spain | Long term (≥ 4 years) |

| EU Beating Cancer Plan funding | +0.7% | Central & Eastern Europe, Southern Europe | Medium term (2-4 years) |

| Incidence plateau pivoting demand to surveillance colonoscopy | +0.6% | Western Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Shift From gFOBT to Quantitative FIT in Organized EU Programmes

Quantitative FIT has become the reference test in organized screening because it eliminates dietary restrictions, achieves pooled 87% sensitivity for colorectal cancer, and fits high-throughput laboratory workflows. National guidelines lowered hemoglobin thresholds to 10 µg/g in symptomatic triage, boosting negative predictive value above 99.6% and safely deferring colonoscopy for low-risk patients[1]Health Service Executive, “Faecal Immunochemical Testing in Acute Hospital GI Endoscopy Services: Position paper,” hse.ie. Direct-mail FIT distribution in France and Ireland raised participation, yet overall uptake remains below the EU 90% target, indicating further headroom for reminder systems and digital invitations. Lower thresholds exponentially raise positivity, stressing colonoscopy capacity, so programs must balance sensitivity with workforce constraints. Analyzer suppliers benefit from reagent pull-through, but they must support data connectivity for real-time quality monitoring mandated by EU Beating Cancer Plan grants.

Rapid Adoption of AI-Assisted Endoscopy Improving Adenoma-Detection Rates

Computer-aided detection embedded in colonoscopes lifts quality metrics that tie directly to interval cancer prevention. Olympus OLYSENSE gained CE mark in 2024 and demonstrated a 7.4-percentage-point adenoma-detection increase, including a 2.3-fold rise in sessile-serrated lesion capture, the subtype responsible for up to 30% of missed cancers. Danish and Swedish trials of Medtronic’s GI Genius showed consistent gains, reinforcing payer willingness to reimburse CADe-enabled systems. Early adoption concentrates in university centers with capital budgets and research incentives, while community units face return-on-investment questions. FUJIFILM’s ELUXEO 8000 launch paired advanced chromoendoscopy with an AI-driven pathology venture, signaling convergence of imaging, analytics, and digital pathology. Over the forecast horizon, reimbursement frameworks linking payment to adenoma-detection benchmarks are expected to accelerate penetration.

Uptake of Blood-Based Multi-Cancer Early-Detection Assays in High-Risk Cohorts

Guardant Health’s Shield received FDA approval in 2024 with 83.1% cancer sensitivity but detected only 13.2% advanced adenomas, limiting average-risk application. European pilot use therefore targets high-risk cohorts where the cost per cancer detected becomes favorable. The EU-funded DIOPTRA project and liquid-biopsy surveillance studies are expanding evidence generation, but reimbursement will depend on demonstrating that higher test costs are offset by earlier-stage detection. Patient surveys show strong preference for blood draws over stool collection, suggesting latent demand once performance improves. Manufacturers are expected to position future versions as adjuncts that raise participation without cannibalizing FIT volumes.

EU Beating Cancer Plan Funding for Population Screening Expansion

The EUR 4 billion policy package supports infrastructure, IT platforms, and workforce training to push screening coverage to 90% by 2025. Grants accelerate FIT capacity build-out in Poland, Romania, and Bulgaria, while Spain leverages funds to close regional gaps. Procurement criteria favor analyzers with quality-control modules and open connectivity. Endoscopy suppliers aligning to ESGE accreditation guidelines gain an edge because compliance is tied to reimbursement eligibility. Progressive roll-out of IVDR from February 2025 adds cost but offers regulatory clarity that benefits well-capitalized vendors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneven reimbursement for advanced non-invasive tests | -0.5% | EU-wide | Medium term (2-4 years) |

| Shortage of endoscopy workforce | -0.8% | UK, Ireland, Germany, France | Short term (≤ 2 years) |

| Price premium of stool-DNA / ctDNA tests | -0.4% | Public health systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Uneven Reimbursement for Advanced Non-Invasive Tests Across Member States

Coverage decisions vary widely across the EU, with cost-constrained systems favoring USD 30 FIT over USD 600 stool-DNA or blood assays. CMS’s 2024 denial of Epi proColon is influencing European assessments given similar sensitivity shortfalls. Germany reimburses FIT and colonoscopy but would require new cost-effectiveness dossiers for multitarget DNA tests. France distributes FIT free of charge, further squeezing the value proposition of higher-priced alternatives. Manufacturers must therefore conduct real-world studies that link higher upfront test costs to stage-shift savings.

Shortage of Endoscopy Workforce Limiting Capacity Growth

Endoscopy demand is rising 5-10% yearly, yet accredited gastroenterologists and nurse endoscopists remain in deficit, especially in rural regions. UK accreditation standards introduced in 2024 improve quality but restrict provider numbers. FIT triage partially mitigates pressure by deferring low-risk symptomatic cases, though long waitlists persist. CT colonography guidelines offer an alternative imaging pathway but adoption is slow due to funding and training gaps. Workforce expansion programs and AI-based quality support tools are expected to ease but not fully resolve capacity constraints before 2030.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Screening Test Type: AI and Blood Biomarkers Reshape Detection Paradigm

Imaging-based procedures retained 52.55% of Europe colorectal cancer screening market share in 2025, anchored by colonoscopy’s diagnostic-therapeutic dual role. The Europe colorectal cancer screening market size for imaging modalities is poised to expand steadily as CADe features become mainstream and CT colonography fills capacity gaps. Olympus OLYSENSE’s EAGLE trial data underscore the competitive advantage of AI, while FUJIFILM’s ELUXEO 8000 links advanced chromoendoscopy with digital pathology to streamline workflows. Yet staffing shortages cap throughput, nudging policymakers to reinforce FIT as the gatekeeper test.

Stool-based platforms enjoy high throughput and low cost, with quantitative FIT replacing guaiac tests across organized programs. Multitarget DNA assays promise superior cancer sensitivity but their premium prices challenge reimbursement. Blood-based tests are forecast to post a 10.25% CAGR, the highest among modalities, yet their Europe colorectal cancer screening market share will remain modest until adenoma sensitivity improves. Digital pathology, protein-augmented FIT, and AI-enhanced CT colonography represent medium-term disruptors converging toward integrated diagnostic pathways.

By End User: Home-Based Channels Capture Convenience Premium

Hospitals and university centers controlled 45.53% of the Europe colorectal cancer screening market size in 2025 as colonoscopy remains an inpatient or ambulatory procedure requiring sedation, reprocessing, and skilled staff. Academic facilities also host early AI deployments and clinical trials. Independent laboratories handle the bulk of FIT processing under stringent quality schemes. Cancer research institutes add marginal volume through biomarker studies but amplify innovation.

Home-based and direct-to-consumer channels, expanding at 12.85% CAGR, benefit from mailed FIT kits and rising tele-health adoption. Ireland’s BowelScreen and Luxembourg’s program demonstrate that removing clinic visits lifts participation, a finding likely to inform other national schemes. Blood-based sampling at pharmacies or mobile vans could further accelerate uptake once assays gain CE-IVDR certification. Vendors must optimize packaging, sample stability, and logistics to serve this segment effectively.

Geography Analysis

The Europe colorectal cancer screening market in Germany stood at 24.63% share in 2025, supported by concurrent FIT and colonoscopy options. The United Kingdom maintains high FIT coverage but faces workforce bottlenecks that elongate follow-up times. France’s 34% participation lags EU targets, leaving a sizable screening gap.

Spain records the highest forecast CAGR at 10.87% as regional governments harmonize invitation systems and invest EU funds to standardize FIT logistics. Italy displays north-south divergence, while the Basque Country’s 68.6% participation showcases best-practice potential. Central and Eastern Europe collectively accelerate as EU Beating Cancer Plan grants finance analyzer procurement, IT platforms, and training. Closing adherence gaps to ESGE surveillance guidelines remains a region-wide priority.

Regulatory Landscape

Colorectal cancer screening in Europe is shaped by EU-wide public health policy and device regulation. The Council Recommendation on cancer screening adopted in December 2022 (replacing the 2003 recommendation) sets out organized programs for ages 50-74 and identifies quantitative fecal immunochemical testing (FIT) as the preferred primary/triage approach, with endoscopy positioned as a primary or combined strategy option. The policy target to offer screening to 90% of the eligible population by 2025, along with the requirement for Member States to report implementation progress to the European Commission within around three years of adoption (late 2025/early 2026), supports the push for standardized quality assurance and program reporting.

For product approval, screening-related devices and assays marketed across the EU must comply with Regulation (EU) 2017/745 (MDR) for medical devices and Regulation (EU) 2017/746 (IVDR) for in vitro diagnostics, with interpretation supported by Medical Device Coordination Group (MDCG) guidance. The staged IVDR rollout from February 2025 places more emphasis on clinical performance evidence, post-market surveillance, and documentation quality for FIT systems and emerging biomarkers. At the same time, it clarifies conformity assessment expectations for well-capitalized suppliers operating within EU quality frameworks, including Commission and Joint Research Centre resources.

Competitive Landscape

Market concentration is moderate. Major players, Abbott, Roche, and other, dominate stool-based testing with OC-Sensor and HM-JACKarc FIT analyzers referenced in NICE guidance[2]National Institute for Health and Care Excellence, “Screening tests | Background information | Bowel screening | CKS,” cks.nice.org.uk . Endoscopy giants Olympus, FUJIFILM, and Medtronic differentiate via CADe algorithms that lift adenoma detection. Olympus OLYSENSE’s CE-marked launch in 2025 produced a 7.4-percentage-point ADR gain in the multi-center EAGLE trial, a performance lever for premium pricing. FUJIFILM’s ELUXEO 8000 integrates advanced imaging with IBEX AI pathology to form an end-to-end diagnostic chain.

Smaller disruptors exploit niche segments. Mainz Biomed’s ColoAlert posted 33% revenue growth in 2024 and gained UK MHRA registration in September 2025, signaling early traction in private and employer markets. Geneoscopy’s ColoSense, FDA-cleared in 2024, awaits CE-IVDR submission. Owkin’s MSIntuit CRC v2 illustrates the rise of software-as-a-medical-device solutions that augment histopathology. Strategic patterns highlight equipment-software tie-ups, EU public-private infrastructure partnerships, and vertical integration into lab services. Upcoming IVDR compliance costs may consolidate the field, disadvantaging smaller firms lacking regulatory muscle.

White-space opportunities revolve around blood-based tests combining higher participation with cost-effective performance, AI decision-support tools that optimize surveillance intervals, and reagent-agnostic analyzers compatible with next-generation biomarkers. However, reimbursement fragmentation and workforce shortages pose persistent barriers. Vendors demonstrating outcome-based value will capture share as procurement shifts to quality-linked contracts across the Europe colorectal cancer screening market.

Europe Colorectal Cancer Screening Industry Leaders

Abbott Laboratories

Exact Sciences Corporation

F. Hoffmann-La Roche AG

Novigenix SA

Epigenomics AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

EU policy and quality frameworks create specific room for organized screening expansion and modernization. The EU-supported Cancer Screening Scheme under Europe’s Beating Cancer Plan aims to broaden access toward the 90% offer target for eligible populations, prompting investment in FIT throughput, invitation logistics, and interoperable reporting tools that support ongoing program monitoring. This setting favors quantitative FIT platforms with scalable analyzer capacity, quality-control modules, and connectivity that helps programs meet audit and quality assurance requirements referenced in EU guidance and related Joint Research Centre resources.

Opportunity also sits in evidence generation and workflow productivity, rather than modality replacement. Horizon Europe projects support risk-based screening and AI validation in endoscopy, including ONCOSCREEN (risk stratification methodologies) and OperA (a population-based randomized trial evaluating AI-assisted colonoscopy for prevention). In parallel, blood-based biomarkers remain an unmet-need route to higher participation among people who avoid stool tests; AMADIX reported ongoing European prospective validation activity (March 2025) for its PreveCol signature. Vendors with non-invasive sampling alongside IVDR-ready clinical performance packages, and positioning that aligns with FIT gatekeeping and colonoscopy capacity constraints, can pursue adoption through pilots and program procurement cycles.

Recent Industry Developments

- May 2026: The American Cancer Society updated colorectal cancer screening guidelines and reaffirmed Cologuard and Cologuard Plus as preferred noninvasive options, which Abbott highlighted following its expansion in cancer diagnostics. Guideline reinforcement supports the evidence narrative for stool-based molecular screening and backs commercial investment in evidence generation and payer discussions beyond FIT-only pathways.

- March 2026: Abbott completed its acquisition of Exact Sciences, bringing Cologuard and Oncotype DX into Abbott’s diagnostics portfolio. The deal consolidates a major noninvasive colorectal screening franchise under a large IVD player, increasing resources for international regulatory workstreams and broader commercialization that can shape competitive intensity in Europe under IVDR.

- September 2025: Mainz Biomed announced MHRA registration of ColoAlert, authorizing marketing across the United Kingdom. UK registration expands a stool-DNA offering into a major European screening geography and adds competitive pressure in private and employer-led channels while national programs continue to scale quantitative FIT.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Europe colorectal cancer screening market is defined as the revenues generated from tests and procedures used to screen for colorectal cancer across European healthcare settings, including stool-based tests, imaging and endoscopy-based screening, and selected emerging assay formats.

Scope exclusions: Treatment, surgery, chemotherapy drugs, and follow-up therapeutics are excluded, and diagnostic workups done purely for symptomatic patients are not counted as routine screening.

Segmentation Overview

- By Screening Test Type

- Stool-Based Tests

- Fecal Immunochemical Test (FIT)

- Guaiac-based FOBT

- Multitarget Stool-DNA

- Imaging-Based Tests

- Colonoscopy

- CT Colonography (Virtual)

- Flexible Sigmoidoscopy

- Blood-Based & Other Emerging Tests

- Methylated DNA / ctDNA Assays

- Breath & Volatile Organic-compound Tests

- Stool-Based Tests

- By End User

- Hospitals & University Medical Centres

- Independent Diagnostic Laboratories

- Cancer Research Institutes

- Home-Based / Direct-to-Consumer Channels

- By Country

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by building a fact base on screening eligibility, program coverage, and test pathways across Europe, then mapping how patients move from an invitation to a completed screening test. We relied on non-paywalled sources such as WHO Europe publications, OECD Health Statistics, Eurostat, and European Cancer Information System (ECIS) indicators to anchor population, age bands, and disease burden signals used in the demand pool.

To connect demand signals to spend, we reviewed public reimbursement schedules and national screening program pages (where available), and we cross-checked peer-reviewed clinical guidance from European gastroenterology and oncology journals for standard intervals and follow-up approaches after test positivity. We also reviewed company filings, investor presentations, and reputable press releases to understand product-mix shifts and pricing direction. For company-level financial inputs, we used a paid subscription, and we used a patent database to cross-check technology activity and commercialization timing. These examples are not exhaustive, and we also reviewed other public sources for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to sanity-check the desk model and tighten assumptions that typically vary by country, such as screening uptake, FIT versus colonoscopy pathway share, and the portion of testing routed through hospitals versus independent labs. We spoke with clinicians, lab and program stakeholders, and commercial roles across major European countries and the rest of Europe, so the final totals better reflect real-world workflow and reimbursement conditions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 17% | |

| Mid tier: 58% | Functional/Unit leaders: 41% | |

| Smaller Players: 17% | Managers: 42% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool reconstruction, where the age-eligible population and organized program coverage are translated into completed screening volumes, and then priced using typical test and procedure reimbursement levels. Country totals are modeled first for key markets (Germany, the United Kingdom, France, Italy, and Spain) and then extended to the rest of Europe using comparable program maturity and access indicators.

To keep the model grounded, we use a small set of practical inputs such as screening participation rates, FIT and gFOBT kit utilization, positivity rates that drive follow-up colonoscopy volume, capacity and waiting-time constraints for endoscopy, and the pace of adoption for stool-DNA and emerging blood-based assays. After the top-down build, selective bottom-up checks are applied using sampled price points, channel feedback on kit shipments, and supplier revenue context to adjust any totals that look out of line. For forecasting, scenario analysis is used around program expansion, uptake changes, and pricing movement, and the annual path is smoothed using trend-based extrapolation aligned with expert consensus on realistic implementation timelines.

Data Validation & Update Cycle

Validation is done in steps, starting with internal consistency checks so that volumes, prices, and implied per capita spend do not contradict each other across countries. Outliers are flagged and reviewed against independent signals such as public screening participation reports, published colonoscopy capacity commentary, and reimbursement updates, then assumptions are revised when the mismatch is material.

Before sign-off, the model and narrative go through multiple analyst reviews, and call-backs are triggered when a key input shifts or a country-level logic needs reconfirmation. Reports are refreshed annually, and interim updates are made when there are major guideline changes, reimbursement moves, or program expansions. Right before delivery, a fresh data pass is completed so clients receive the most current view.

Mordor Intelligence's Europe Colorectal Cancer Screening Market Market Size Measured Against Other Published Estimates

Published market sizes for Europe colorectal cancer screening often differ, even when the topic name looks the same, because the counted activities and pricing logic can change from one publisher to another. Differences also come from the chosen base year, which countries are included, and whether the estimate is built around organized screening programs or a broader set of diagnostic testing.

Program participation statistics, reimbursement schedules, and procedure follow-through rates are the evidence checks that tie Mordor Intelligence's estimate to screening activity that is actually delivered in Europe, which reduces the risk of over-counting from adjacent diagnostic testing or broader gastrointestinal procedure baskets.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.45 B (2026) | |

| Industry Databook A | USD 8.78 B (2025) | This figure is presented as a broader colon screening revenue pool, which can fold in a wider set of screening-related products and procedures and may apply different country coverage and pricing assumptions than a CRC-only screening workflow model. |

| Specialist Publisher B | USD 1.60 B (2030) | This estimate is shown as a single-year projection and appears to focus on a narrower subset of screening activity, which can exclude higher-cost procedure components or omit emerging test formats, leading to a lower total. |

The spread is mainly created by scope boundaries and what gets priced, rather than by math differences alone. When the model is anchored to clear screening volumes, follow-up pathways, and country-specific reimbursement, the final market size becomes easier to explain, re-check, and update each year.

Key Questions Answered in the Report

How large is the Europe colorectal cancer screening market in 2026?

The market is valued at USD 5.45 billion in 2026.

What CAGR is forecast for colorectal cancer screening across Europe to 2031?

A 4.85% CAGR is projected for 2026-2031.

Which screening modality is growing the fastest?

Blood-based and other emerging tests are expected to rise at a 10.25% CAGR.

Why does Spain present the highest growth prospect?

Regional programs are standardizing FIT logistics and leveraging EU funding, supporting a 10.87% CAGR.

How are AI tools impacting colonoscopy quality?

CADe systems such as Olympus OLYSENSE raise adenoma detection by more than seven percentage points, improving interval cancer prevention.

What is the main barrier to adopting premium DNA or blood tests?

Their price premium over FIT and uneven reimbursement across public health systems limit uptake.

Page last updated on: