Cancer Biopsy Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

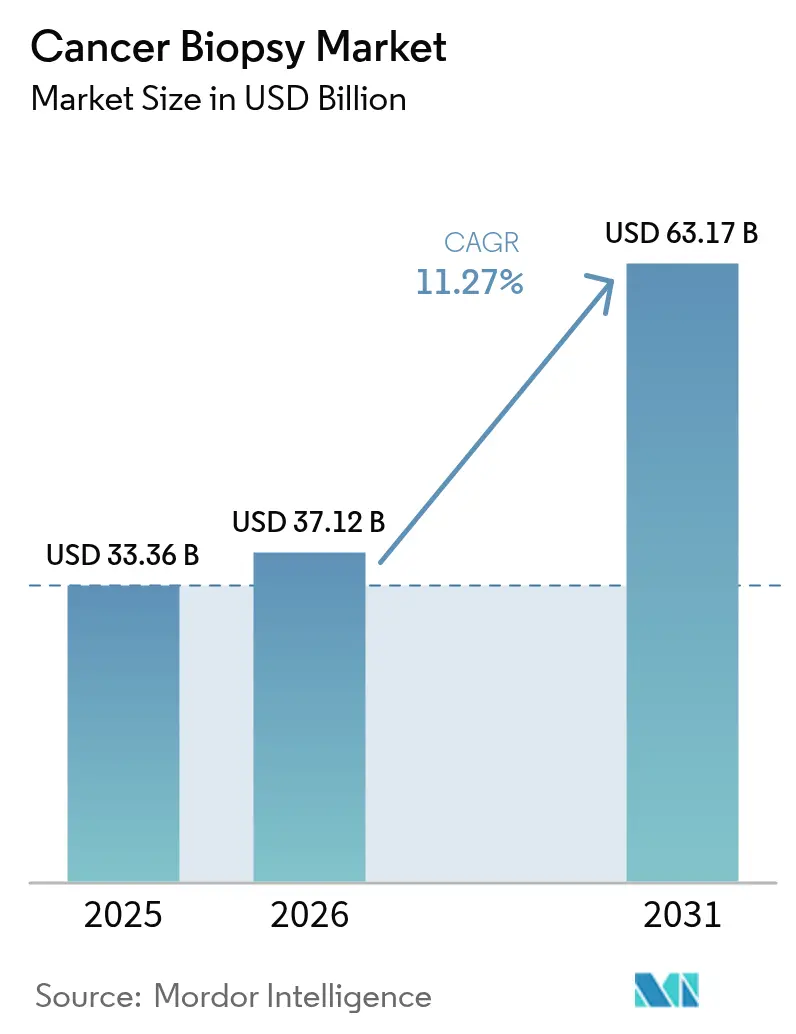

| Market Size (2026) | USD 37.12 Billion |

| Market Size (2031) | USD 63.17 Billion |

| Growth Rate (2026 - 2031) | 11.27% CAGR |

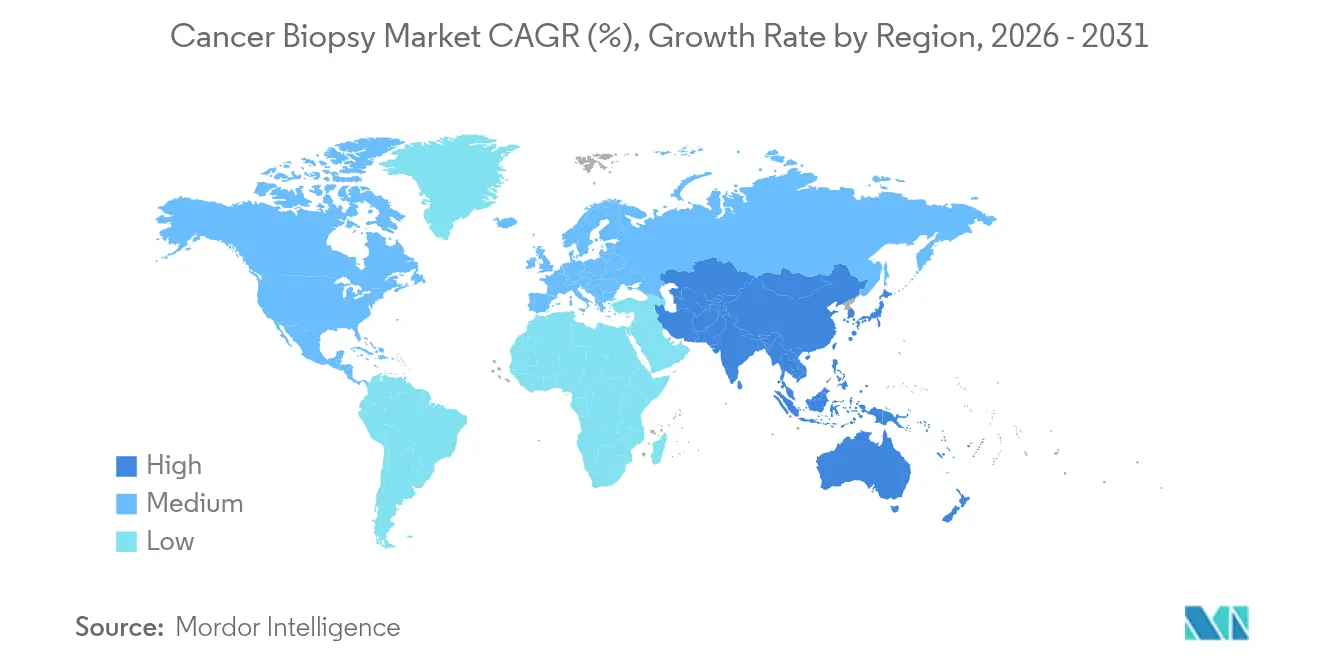

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cancer Biopsy Market Analysis by Mordor Intelligence

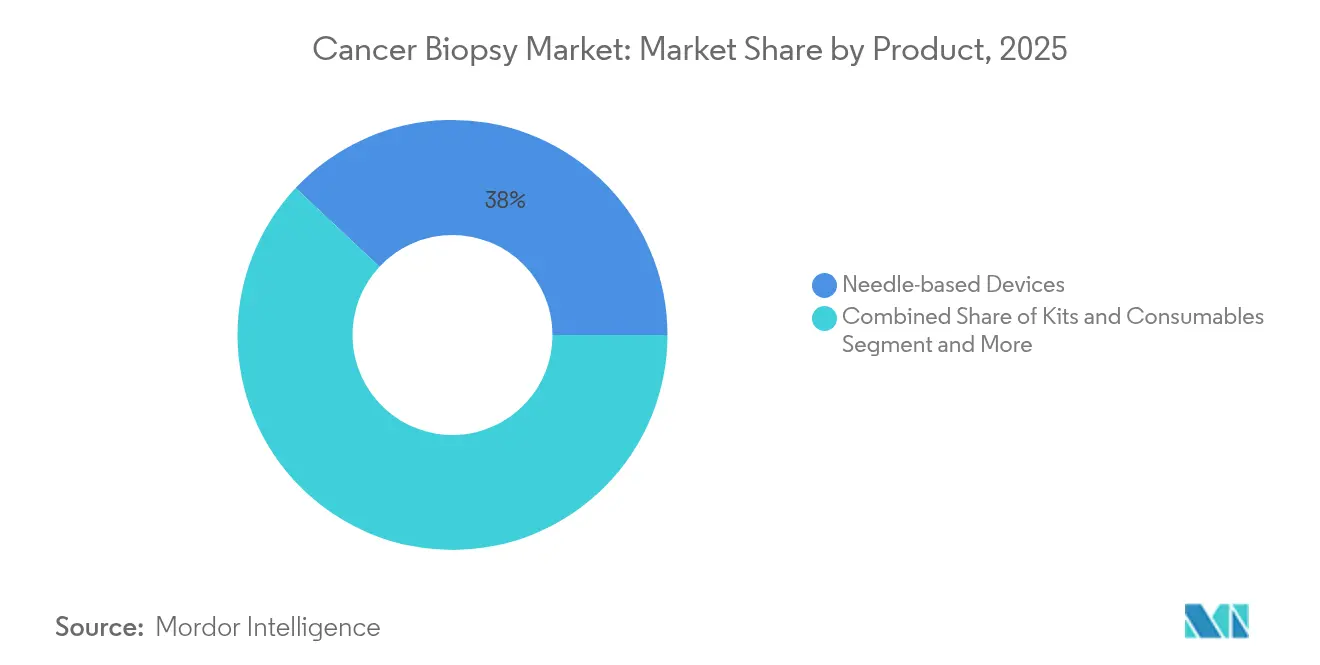

The cancer biopsy market size was valued at USD 33.36 billion in 2025 and estimated to grow from USD 37.12 billion in 2026 to reach USD 63.17 billion by 2031, at a CAGR of 11.27% during the forecast period (2026-2031). Demand growth stems from rapid uptake of liquid biopsy technologies, supportive reimbursement policies and an aging population that is expanding the global oncology patient pool. The July 2024 FDA approval of Guardant Health’s Shield blood test, the first blood-based primary cancer screen reimbursed by Medicare, illustrates how regulatory momentum is moving diagnostics from tissue-dependent to predictive blood-based testing. Although tissue procedures still account for 65.53% of 2024 revenues, liquid biopsy volumes are climbing fastest at a 14.15% CAGR as clinicians embrace minimally-invasive workflows. Regionally, North America held 38.72% of 2024 revenue, yet Asia-Pacific is accelerating at a 14.22% CAGR on the back of China’s national lung-cancer screening protocol and India’s AI-powered hospital roll-outs. Product preferences are also shifting: needle-based devices led with 38.55% share in 2024, but single-use kits and consumables are expanding 12.25% per year as laboratories favor standardized, automated runs. End-user patterns mirror broader care decentralization. Hospitals retained 45.72% share in 2024, yet ambulatory surgical centers are growing 13.22% annually as payors push lower-cost outpatient pathways.

Key Report Takeaways

- By product category, needle-based devices led with 38.02% revenue share in 2025; kits and consumables are projected to grow at a 12.05% CAGR to 2031.

- By procedure, tissue biopsies retained 65.12% of the cancer biopsy market share in 2025, whereas liquid biopsy volumes are poised to expand at a 13.92% CAGR through 2031.

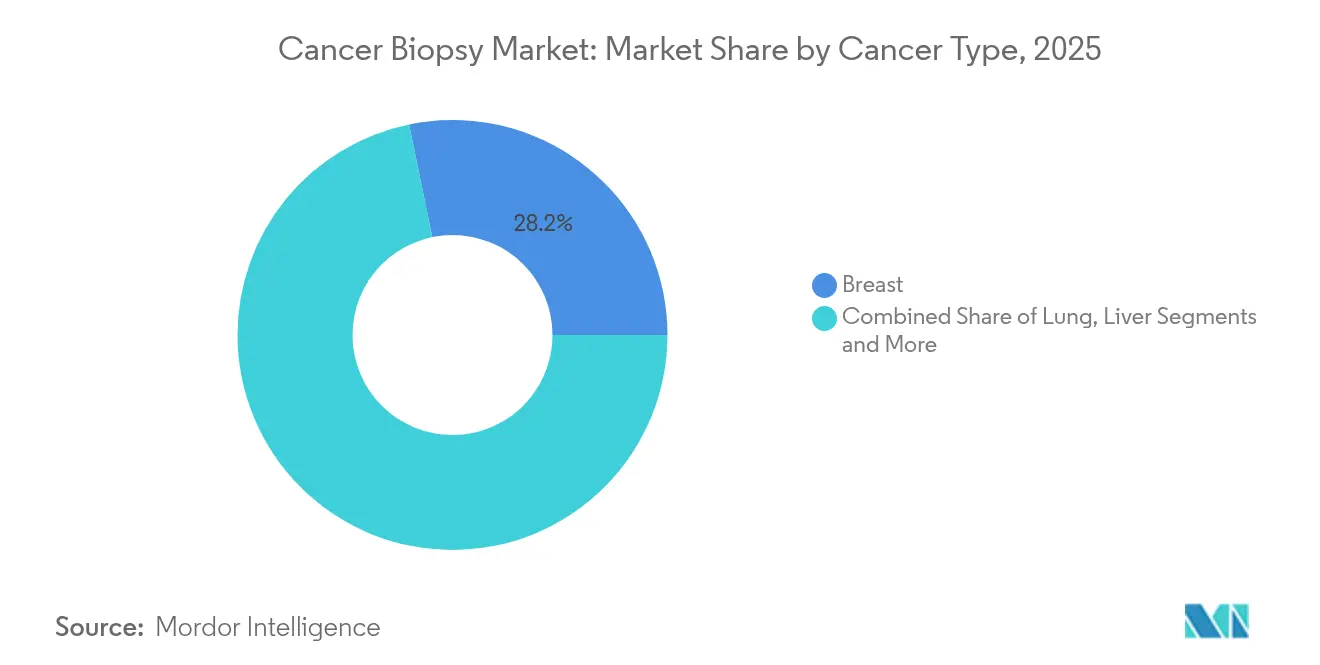

- By cancer type, breast cancer accounted for a 28.24% share of the cancer biopsy market size in 2025, while pancreatic cancer diagnostics are advancing at a 12.96% CAGR to 2031.

- By end-user, hospitals commanded 45.05% of 2025 revenue; ambulatory surgical centers exhibit the highest projected CAGR at 13.04% to 2031.

- By geography, North America held 38.35% of 2025 revenue, with Asia-Pacific expected to post a 14.03% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cancer Biopsy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Oncology Burden & Ageing Population | +2.8% | Global, with concentrated impact in North America & Europe | Long term (≥ 4 years) |

| Technological Advances In NGS-Enabled Liquid Biopsy | +3.2% | Global, early adoption in North America, rapid expansion in APAC | Medium term (2-4 years) |

| Patient Demand For Minimally-Invasive Diagnostics | +1.9% | Global, strongest in developed markets | Short term (≤ 2 years) |

| Reimbursement Wins & Regulatory Green-Lights For Ctdna Tests | +2.1% | North America & EU primary, spillover to APAC | Medium term (2-4 years) |

| Real-Time Nanopore Sequencing & AI-Augmented Analytics | +1.4% | Global, concentrated in research-intensive markets | Long term (≥ 4 years) |

| Point-Of-Care Biopsy Kits For Low-Resource Settings | +0.8% | APAC, MEA, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Oncology Burden & Ageing Population

Cancer incidence is expected to rise 47% by 2040, a shift that is enlarging the long-run addressable base for diagnostic providers. In markets such as China, a national lung-cancer protocol built on three-dimensional CT reconstruction has already improved early-stage detection rates and driven screening volumes higher[1]Weimin Li, “China Protocol for Early Screening, Precise Diagnosis, and Individualized Treatment of Lung Cancer,” Nature, nature.com. The combination of older patient cohorts living longer with cancer and expanding chronic-disease infrastructure in emerging economies keeps the demand curve steep for both tissue and liquid tests. Growing survivor populations also sustain repeated molecular residual-disease monitoring, bolstering test utilisation after initial diagnosis. As population-scale screening becomes standard, payors are increasingly viewing early detection as a cost-containment strategy rather than an incremental expense.

Technological Advances in NGS-Enabled Liquid Biopsy

The convergence of next-generation sequencing with blood-based assays now allows comprehensive genomic profiling from a single tube of plasma. FDA endorsement of FoundationOne Liquid CDx for non-small-cell lung cancer companion uses in November 2024 underscored the platform’s clinical validity. Oxford Nanopore’s real-time sequencing can detect structural variants and methylation signatures in under two hours, narrowing the feedback loop between sampling and treatment decisions. Academic demonstrators such as the MRD-EDGE workflow have pushed analytic sensitivity to parts-per-million ranges, enabling earlier relapse detection. These innovations are repositioning the cancer biopsy market from a confirmatory tool into a longitudinal disease-management platform.

Patient Demand for Minimally-Invasive Diagnostics

Patients increasingly opt for procedures that involve little or no discomfort. Nanoneedle skin patches under development at King’s College London promise painless cellular sampling that could obviate traditional punch biopsies. Completion rates for blood-based assays run near 90%, significantly outpacing colonoscopy adherence, and thus strengthen screening program yield. Salivary Raman spectroscopy kits further extend minimally-invasive options to oral and breast cancers, a critical consideration for low-resource settings. As consumers weigh convenience alongside clinical benefit, demand gravitates toward workflows that minimise travel time, recovery, and anxiety.

Reimbursement Wins & Regulatory Green-Lights for ctDNA Tests

Consistent reimbursement is translating technical breakthroughs into predictable cashflows. Medicare now covers both Shield screening and Guardant Reveal surveillance, anchoring revenue forecasts for laboratories and hospitals[2]Guardant Health, “Guardant Health Receives Medicare Coverage for Guardant Reveal™,” guardanthealth.com. Fifteen US states have enacted biomarker mandates compelling private insurers to fund precision tests when clinically indicated, smoothing the reimbursement landscape. FDA guidance issued in November 2024 clarified the evidentiary bar for ctDNA use in drug development, catalysing pharma-diagnostics alliances. Similar clarity is emerging in Europe and Japan, accelerating multi-regional trial designs that rely on liquid biopsy endpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Test Costs & Patchy Reimbursement Coverage | -1.8% | Global, most pronounced in emerging markets | Short term (≤ 2 years) |

| Procedural & Sampling-Error Risks (False Negatives) | -1.2% | Global, clinical validation concerns | Medium term (2-4 years) |

| Genomic-Data Privacy / Ownership Concerns | -0.9% | North America & EU primary, expanding globally | Medium term (2-4 years) |

| Liquid-Biopsy Sensitivity Gaps In Early-Stage Solid Tumours | -1.5% | Global, concentrated in developed markets with advanced screening | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Test Costs & Patchy Reimbursement Coverage

Comprehensive liquid biopsy panels often exceed USD 3,000 per sample, a price still out of reach for many payors outside North America and Western Europe. In emerging economies where out-of-pocket spending remains common, limited insurance penetration suppresses test utilisation despite high disease burden. Even in the United States, commercial insurers frequently trail Medicare by up to two years before granting coverage, creating revenue gaps for laboratories. Laboratories also face heavy upfront capital expenditures for automated extraction and sequencing instruments, costs that discourage market entry by smaller regional players. Until supply-chain scale and competition compress kit pricing, economic barriers will slow uniform adoption.

Procedural & Sampling-Error Risks (False Negatives)

Liquid biopsy still struggles to detect early-stage tumours with very low circulating DNA levels. For instance, Shield’s sensitivity for Stage I colorectal lesions is 54.5%, a limitation that leads conservative oncologists to continue requesting tissue confirmation. Pre-analytical variables such as sample handling or delayed processing can degrade cfDNA, compounding false-negative risk. Inadequate tissue cores remain a parallel problem in solid biopsies, with up to 15% of samples failing molecular testing due to insufficient tumour content. Laboratories must therefore invest in robust standard operating procedures and quality controls, adding complexity and cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Automation Expands Consumable Uptake

Needle-based devices captured 38.02% of 2025 revenue, reflecting their entrenched role in hospital-based tissue collection. The cancer biopsy market size for kits and consumables, however, is projected to grow at a 12.05% CAGR between 2026 and 2031 as laboratories pivot toward automated, cartridge-driven protocols that reduce human error and turn fixed costs into variable costs. QIAGEN’s QIAsymphony Connect, announced for 2026 launch, can run 192 samples in a single shift, driving per-test reagent demand and anchoring a recurring revenue model.

Instruments remain essential but face price compression as buyers allocate budgets toward high-margin consumable streams. Software and bioinformatics suites such as Ingenuity Pathway Analysis, now expanded with an AI engine, improve variant annotation turnaround and reinforce vendor lock-in. Guidance systems and vacuum-assisted devices occupy niche procedure types where tactile feedback or tissue volume is critical; growth here is steady but not spectacular. Over the forecast window, consumable line-extensions—from cfDNA collection tubes to sequencing cartridges—will account for a rising share of overall cancer biopsy market revenue as providers favor predictable cost-per-test economics.

By Procedure: Liquid Workflows Challenge Tissue Dominance

Tissue biopsies still accounted for 65.12% of cancer biopsy market share in 2025, yet liquid procedures will capture a growing slice of spending as technology matures. Core needle extraction remains preferred for many solid tumours because it balances diagnostic yield against patient discomfort. Fine-needle aspiration supports anatomically challenging sites but delivers limited material for multi-omic profiling.

Surgical excisions continue for complex lesions but are declining in frequency as blood-based assays gain confidence among multidisciplinary tumour boards. On the liquid side, blood tests dominate given the ease of serial sampling and recent regulatory wins. Urine-based workflows are scaling in urological cancers, and research into saliva and cerebrospinal fluid profiling extends test menus to other hard-to-biopsy indications. Throughout the next five years, hybrid pathways—initial non-invasive screen followed by tissue confirmation—will become common, gradually reducing the volume of first-line surgical biopsies and redirecting capital budgets to high-throughput plasma labs.

By Cancer Type: Early Pancreatic Detection Leads Growth Curve

Breast cancer retained a 28.24% revenue share in 2025 thanks to decades-old mammography programs and strong patient awareness. Nonetheless, the cancer biopsy market size linked to pancreatic testing is forecast to rise fastest, at a 12.96% CAGR, as liquid biopsy finally offers a practical surveillance method for high-risk cohorts. Breakthrough platforms combining KRAS mutational panels with methylation signatures are showing promising sensitivity below 1% tumour fraction, a performance unattainable with prior biomarkers.

In breast cancer, Bio-Rad’s ddPLEX ESR1 assay allows laboratories to detect endocrine-resistance mutations at parts-per-billion levels, supporting therapy adjustment decisions. Lung cancer remains a large addressable volume due to population-scale CT screening, but reimbursement for broad gene panels is still being negotiated in many countries. Colorectal cancer liquid tests have gained commercial traction following Shield’s approval; yet specificity debates continue, highlighting the ongoing need for balanced cost-effectiveness evidence.

By End User: Outpatient Shift Accelerates

Hospitals held 45.05% of 2025 revenue, yet ambulatory surgical centers are registering a 13.04% CAGR as payors encourage lower-acuity sites for routine diagnostics. The cancer biopsy market is thus fragmenting across a wider network of collection points. Large reference laboratories such as Labcorp and Quest Diagnostics are investing in liquid-biopsy automation lines to centralize molecular testing volumes; Labcorp’s April 2025 launch of two plasma-based MRD assays underscores this push. Cancer research institutes influence protocol adoption through clinical trials but represent a small slice of ordered tests.

Meanwhile, primary-care networks are piloting blood-draw stations that feed central labs nightly, shortening turnaround times and improving patient retention. As outpatient volumes climb, hospitals are integrating rapid-on-site evaluation rooms to hold more complex oncology procedures that still require surgical skill and multidisciplinary support.

Geography Analysis

North America generated 38.35% of global revenue in 2025, buoyed by Medicare coverage, biomarker mandates in 15 states and a constant stream of FDA device approvals. Canada benefits from unified reimbursement across provinces and a growing roster of precision-medicine pilot projects, while Mexico’s medical-device export corridor supplies disposable biopsy kits at competitive prices. Asia-Pacific is the fastest-expanding theatre, logging a 14.03% CAGR through 2031. China’s three-dimensional CT reconstruction pathway for lung-cancer screening and AI-assisted nodule triage has already scaled to provincial centres, lifting test volumes and creating bulk-procurement tenders. India’s AIIMS-led deployment of deep-learning diagnostics into district hospitals showcases leap-frog adoption in resource-limited settings, while Japan’s approval of Guardant360 CDx as a companion assay aligns domestic oncology care with global standards.

Europe advances at a steadier pace, aided by cross-border research programs and harmonised CE-IVD regulation. Uptake of AI-enabled histopathology, along with national genomics initiatives in the United Kingdom and France, supports broader adoption of molecular biopsy approaches. Nevertheless, reimbursement disparities among member states mean private laboratories often face multi-year approval cycles before liquid tests are fully funded. The Middle East and Africa region is experiencing moderate expansion, driven by GCC investments in comprehensive cancer centres and targeted tourism from neighbouring countries. South Africa leads sub-Saharan diagnostics capacity, whereas many other African markets lack sequencing infrastructure, extending the time to widespread liquid biopsy availability.

South America’s outlook is positive yet volatile. Brazil is directing public funds toward national cancer-control plans that include molecular screening components, and Argentina’s biomedical cluster is piloting local reagent manufacturing to lower costs. Currency fluctuations and regulatory heterogeneity, however, can stall cross-border expansion for multinational vendors.

Collectively, geographic trends signal a gradual rebalancing of the cancer biopsy market toward emerging economies, although North American and European payor systems will continue to anchor premium test revenue through 2030.

Competitive Landscape

The cancer biopsy market is moderately concentrated, with technological differentiation outweighing price wars. Illumina, having divested GRAIL in June 2024, is doubling down on core sequencing chemistry and expanding its TruSight Oncology panel series to feed downstream diagnostic partners[3]Illumina Inc., “Illumina Completes the Divestiture of GRAIL,” illumina.com. QIAGEN is scaling its Digital Insights unit, embedding AI functions that auto-interpret variant significance and ease bottlenecks for hospital pathologists. Guardant Health, Exact Sciences and Foundation Medicine maintain first-mover advantages in US reimbursement, yet emerging entrants such as Oxford Nanopore and Grail’s former competitors are targeting point-of-care and ultra-rapid readouts.

Horizontal consolidation is accelerating. Labcorp announced acquisitions of regional pathology assets in May and March 2025 to secure specimen flow and enhance oncology assay menus. Quest Diagnostics is investing in cloud-based bioinformatics to shorten diagnostic-report delivery for community oncologists. Device manufacturers are also shedding non-core units: BD’s strategic review could see its in-vitro diagnostics division spun out by 2026, potentially reshaping supply-chain alliances.

Competitive intensity is tilting toward integrated service offerings. Vendors combining collection devices, reagents, and interpretation software lock in laboratories and secure recurring consumables revenues. At the same time, AI-driven skin-patch or saliva-based screening prototypes from academic spin-outs threaten to decentralise sampling further, creating white-space niches. Pharma-diagnostic co-development agreements remain a lucrative channel: Agilent’s January 2024 agreement with Incyte to co-develop haematology companion tests exemplifies how assay developers can tie revenue streams to drug-label expansion.

Cancer Biopsy Industry Leaders

Illumina, Inc.

Becton, Dickinson and Company

Myriad Genetics

Thermo Fisher Scientific

QIAGEN NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Labcorp launches two precision-oncology solutions—Plasma Detect for molecular residual disease assessment and PGDx elio plasma focus Dx, the first FDA-authorized kitted liquid biopsy for pan-solid tumours.

- January 2025: Guardant Health secures Medicare coverage for Guardant Reveal surveillance in colorectal-cancer patients, expanding blood-based MRD access.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global cancer biopsy market as all dedicated instruments, needles, vacuum or image-guided systems, kits, reagents, software, and outsourced laboratory services used to collect or interrogate solid-tissue or liquid samples for histopathologic or molecular confirmation of malignancy across every organ system and care setting.

Scope exclusion: general imaging scanners and broad laboratory automation platforms not expressly marketed for biopsy workflows remain outside this scope.

Segmentation Overview

- By Product

- Instruments

- Kits & Consumables

- Software & Bioinformatics

- Needle-based Devices

- Vacuum-assisted Devices

- Guidance Systems

- By Procedure

- Tissue Biopsy

- Core Needle

- Fine-Needle Aspiration

- Surgical Excisional

- Liquid Biopsy

- Blood

- Urine

- Saliva

- Cerebrospinal Fluid

- Tissue Biopsy

- By Cancer Type

- Breast

- Lung

- Colorectal

- Prostate

- Cervical

- Pancreatic

- Melanoma

- Others

- By End User

- Hospitals

- Diagnostic Laboratories

- Ambulatory Surgical Centres

- Cancer Research Institutes

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed pathologists, interventional radiologists, oncology lab managers, and lab-supply distributors in North America, Europe, China, India, and Brazil. These conversations clarified biopsy penetration rates, liquid-biopsy adoption curves, replacement cycles, and regional price corridors, helping us reconcile desk findings and stress-test early model outputs.

Desk Research

We began with incidence and procedure files from WHO-IARC, GLOBOCAN, SEER, Eurostat, and OECD Health Data, then layered in tariff and shipment tallies from UN Comtrade and U.S. ITC to size cross-border kit flows. White papers from the College of American Pathologists, European Society of Medical Oncology, and China Medical Device Association informed consumable usage norms, while 10-Ks accessed through D&B Hoovers and news pulls on Dow Jones Factiva supplied brand-level revenue splits. The listed sources are illustrative; many additional public datasets were reviewed to verify signals and close gaps.

Market-Sizing & Forecasting

A top-down engine converts new-cancer incidence into biopsy volumes using region-specific penetration, re-biopsy, and screen-positive factors, which are then multiplied by blended average selling prices to compute revenue. Bottom-up rollups sampled shipment logs for needle devices, channel checks at five reference labs, and disclosed tender awards calibrate totals. Key variables modeled forward include screening-program coverage, liquid-biopsy share shift, kit re-use restrictions, and ASP erosion; multivariate regression on these drivers anchors the forecast period view.

Data Validation & Update Cycle

Outputs flow through variance screens, peer review, and senior analyst sign-off. We refresh annually and re-open the model whenever material regulatory, reimbursement, or M&A events occur, ensuring buyers get the latest read.

Why Mordor's Cancer Biopsy Baseline Commands Trust Worldwide

Published market values often diverge because firms favor different biopsy types, pricing assumptions, and refresh cadences.

According to Mordor Intelligence, the market stood at USD 33.36 billion in 2025. Global Consultancy A places the same year at USD 34.84 billion, while another public forecast cites USD 36.55 billion.

Key gap drivers include: (1) some publishers fold liquid-biopsy test revenue into broader companion-diagnostics figures, (2) others inflate ASPs by indexing to list rather than transacted prices, and (3) several carry forward pre-pandemic incidence baselines without reconciling post-COVID screening rebounds.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 33.36 B (2025) | Mordor Intelligence | - |

| USD 34.84 B (2025) | Global Consultancy A | Liquid + tissue scopes blended; incidence base year 2021 |

| USD 36.55 B (2025) | Industry Association B | Uses list ASPs and single growth scenario |

The comparison shows how Mordor's disciplined variable selection, yearly refresh, and dual-path validation deliver a balanced, transparent baseline decision-makers can rely on.

Key Questions Answered in the Report

What is the current size of the cancer biopsy market?

The global market is valued at USD 37.12 billion in 2026, with an 11.27% CAGR forecast to 2031.

Which biopsy procedure is growing fastest?

Liquid biopsy is expanding at a 13.92% CAGR through 2031 as clinicians adopt blood-based and other minimally-invasive sampling methods.

Why is Asia-Pacific growing faster than other regions?

Government-backed screening programs in China and AI-powered hospital initiatives in India are accelerating technology adoption, driving a 14.03% regional CAGR.

Which cancer type offers the highest growth opportunity?

Pancreatic cancer diagnostics are forecast to grow at a 12.96% CAGR because liquid biopsy finally enables practical early detection for this historically hard-to-screen disease.

How are reimbursement changes affecting market growth?

Medicare coverage and state biomarker mandates in the United States, alongside evolving EU and Japanese policies, are reducing payment uncertainty and boosting test volumes.

Page last updated on: