Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

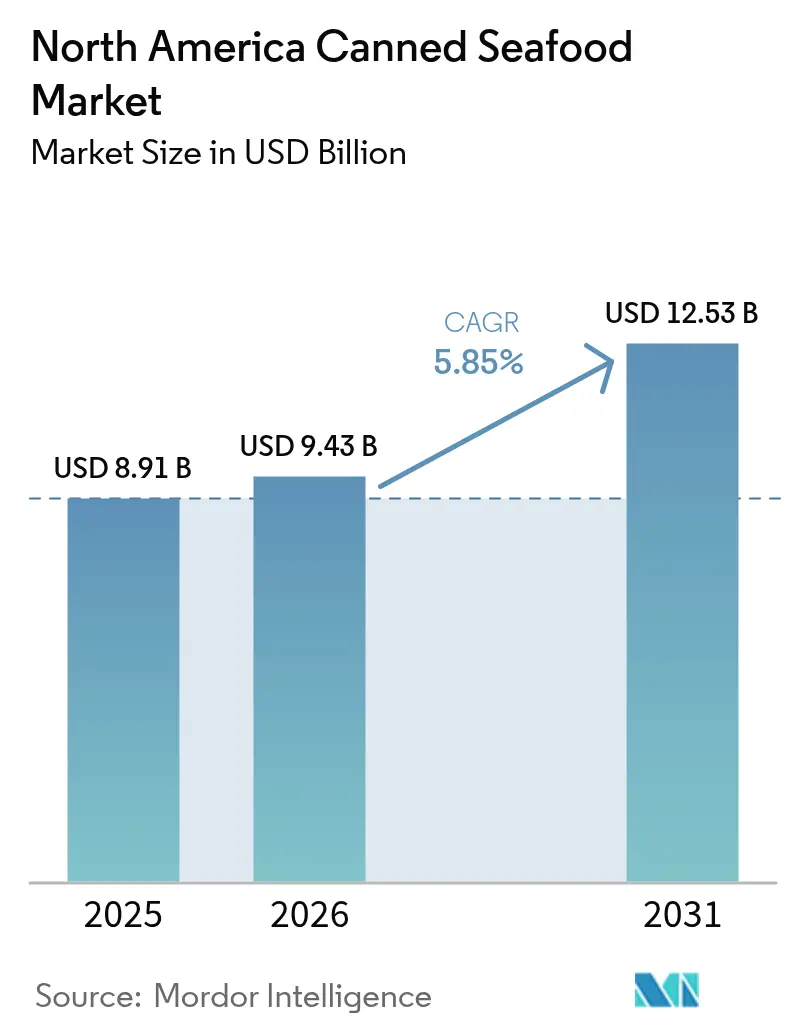

| Base Year Market Size (2025) | USD 8.91 Billion |

| Market Size (2026) | USD 9.43 Billion |

| Market Size (2031) | USD 12.53 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Canned Seafood Market Analysis by Mordor Intelligence

North America canned seafood market size in 2026 is estimated at USD 9.43 billion, growing from 2025 value of USD 8.91 billion with 2031 projections showing USD 12.53 billion, growing at 5.85% CAGR over 2026-2031. This growth trajectory is primarily driven by the increasing consumer preference for shelf-stable protein options, the implementation of new regulatory requirements concerning food-contact chemicals, and the expanding prevalence of urban lifestyles. Sustainability certifications have emerged as a significant factor, enabling companies to command premium pricing. Additionally, the FDA's 2025 decision on PFAS has accelerated deadlines for packaging innovations, compelling canneries to adjust their capital allocation strategies accordingly. While digital commerce is gaining traction, traditional brick-and-mortar retail channels continue to dominate the market due to entrenched consumer shopping habits, particularly for center-store product categories. The competitive landscape is characterized by moderate intensity. Multinational corporations maintain an edge through scale advantages; however, they face increasing margin pressures caused by raw material price volatility and rising compliance costs. These challenges are prompting companies to optimize their operations through rightsizing initiatives and strategic portfolio rationalization.

Key Report Takeaways

- By species, canned fish led with 68.20% revenue share in 2025; canned shrimp is forecast to expand at a 6.62% CAGR to 2031.

- By packaging material, steel cans held 62.80% of the 2025 North American canned seafood market share, while retort pouches are advancing at a 7.05% CAGR through 2031.

- By product form, chunks/pieces captured a 57.60% share of the North American canned seafood market size in 2025, and whole fish formats are projected to grow at an 8.15% CAGR to 2031.

- By distribution channel, the off-trade segment accounted for 62.70% of the North American canned seafood market size in 2025; on-trade is progressing at a 6.65% CAGR between 2026 and 2031.

- By geography, the United States dominated with 78.10% of North American canned seafood market share in 2025, whereas Mexico recorded the fastest CAGR at 7.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Canned Seafood Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enhanced convenience features and preservation benefits | +1.2% | North America | Medium term (2-4 years) |

| Increasing urban population and modern lifestyle changes driving market growth | +0.9% | North America core, spillover to urban Mexico | Long term (≥ 4 years) |

| Growing demand for premium portable seafood snacks | +0.8% | United States and Canada | Short term (≤ 2 years) |

| Expanding consumer preference for protein-rich seafood convenience foods in the united states | +0.7% | United States | Medium term (2-4 years) |

| Room temperature storage advantages in regions with underdeveloped cold chain networks | +0.5% | Mexico and Rest of North America | Long term (≥ 4 years) |

| Sustainability certifications and product origin transparency influencing consumer purchasing behavior | +0.4% | North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Enhanced Convenience Features and Preservation Benefits

Market expansion is being significantly influenced by the increasing consumer demand for ready-to-eat protein sources that require minimal preparation. The Food Industry Association's Power of Seafood 2024 report indicates that 59% of seafood consumption now occurs at home, compared to 41% at restaurants[1]Source: Food Industry Association, “Power of Seafood 2024,” fmi.org. This shift highlights a growing preference for cost-effective meal solutions, driven by inflationary pressures and changing consumer behavior. Technological advancements in preservation methods have further supported this trend by enabling seafood to maintain an extended shelf life without refrigeration. These innovations have addressed critical supply chain vulnerabilities that were exposed during recent disruptions, ensuring greater product availability and reliability. Manufacturers are strategically utilizing these advancements to diversify their market reach, targeting not only traditional meal occasions but also emerging segments such as emergency preparedness and outdoor recreation. In densely populated urban markets, where time constraints heavily influence purchasing decisions, the demand for shelf-stable protein alternatives has become increasingly prominent, further driving market growth.

Increasing Urban Population and Modern Lifestyle Changes Driving Market Growth

The urbanization trend in North America continues to grow, concentrating purchasing power within densely populated trade areas. In these urban settings, smaller household sizes often result in limited freezer space, influencing consumer purchasing behavior. Additionally, the prevalence of dual-income families and extended commuting hours has significantly reduced the time available for meal preparation, driving a stronger preference for convenient protein options. To address concerns about food waste and align with sustainability objectives, manufacturers are increasingly offering packaging designed for single or two-person servings. Among young professionals, canned seafood has gained popularity as a convenient and nutritious choice for lunchboxes and post-work snacks, reflecting a growing connection between health and convenience. Urban-focused retailers are responding to these shifts by enhancing in-store merchandising strategies, including the use of recipe cards and cross-aisle promotions that feature complementary products such as pasta, rice, and salad kits. These evolving consumer preferences and retail strategies provide a strong and sustainable foundation for the North American canned seafood market.

Growing Demand for Premium Portable Seafood Snacks

Following the pandemic, there has been a significant shift in consumer behavior, with Americans increasingly prioritizing health and wellness. According to the Norwegian Seafood Council's 2024 trends report, 70% of Americans now identify as more health-conscious. In response to this growing demand, brands are innovating by offering artisanal flavors and sustainably sourced tuna belly packaged in convenient single-serve pull-tab tins specifically designed to complement charcuterie boards. Additionally, online specialty stores and subscription boxes have simplified access to exclusive, limited-edition product varieties, catering to niche consumer preferences. This strategic premium positioning not only enhances average selling prices but also mitigates the impact of fluctuations in commodity costs. Furthermore, Millennials and Gen Z consumers are particularly drawn to narratives centered around ethical harvesting practices, which strengthen brand loyalty and drive social media-driven word-of-mouth marketing. These factors collectively contribute to the expansion of the North American canned seafood market.

Expanding Consumer Preference for Protein-rich Seafood Convenience Foods in the United States

Canned tuna continues to rank among the top three most consumed seafood products in the United States, reflecting a strong consumer preference for convenient, shelf-stable protein options. Product labels now emphasize key nutritional benefits, such as omega-3 fatty acid content, high lean protein levels, and minimal processing, positioning canned tuna as a healthier alternative to many snack bars. The fitness community has increasingly adopted tuna pouches as a go-to post-workout snack, driving their availability in sporting goods retail outlets. Additionally, the growing popularity of flexitarian diets, which prioritize seafood over red meat, has contributed to consistent household purchases of canned tuna. To further strengthen their nutritional claims, manufacturers are actively collaborating with registered dietitians to validate and communicate these benefits effectively at the point of sale. These combined factors are significantly contributing to the expansion of the canned seafood market across North America.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material price volatility affects market growth | -1.1% | North America | Short term (≤ 2 years) |

| Regulatory compliance costs for BPA and PFAS packaging standards | -0.8% | North America | Medium term (2-4 years) |

| Consumer health concerns regarding sodium and preservative content | -0.6% | United States and Canada | Long term (≥ 4 years) |

| Consumer preference for fresh seafood limits market growth | -0.5% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw Material Price Volatility affects Market Growth

Commodity price fluctuations continue to exert significant margin pressure on the seafood industry, driven by factors such as seasonal variations, climate-related disruptions, and geopolitical events that impact global fishing operations. NOAA Fisheries reported that the Alaska seafood industry incurred a substantial loss of USD 1.8 billion in 2023, accompanied by a sharp 50% decline in profitability[2]Source: NOAA Fisheries, “Economic Status of Alaska Fisheries 2024,” fisheries.noaa.gov. This highlights the sector's pronounced vulnerability to price volatility. Additionally, North American processors, particularly those with considerable reliance on imported seafood, face compounded challenges due to currency fluctuations when sourcing from international suppliers. The unpredictability of prices further complicates long-term contract negotiations with retail partners, who prioritize stable and predictable cost structures for private label programs. Beyond raw seafood inputs, the effects of price volatility extend to packaging materials, with fluctuations in aluminum and steel prices significantly influencing overall production costs.

Regulatory Compliance Costs for BPA and PFAS Packaging Standards

In March 2025, the FDA invalidated 35 food-contact notifications associated with PFAS, necessitating immediate and significant adjustments in packaging processes. Concurrently, the European Union's ban on BPA, which takes effect in January 2025, introduces additional challenges for exporters navigating regulatory compliance across multiple regions. Packaging converters are required to invest in pilot production lines, conduct qualification trials, and obtain customer approvals, all within highly constrained timelines. The need to maintain dual inventories of both legacy materials and their replacements further exacerbates working capital requirements. Mid-sized companies are redirecting their research and development budgets toward meeting compliance obligations, which, in turn, delays the introduction of new products to the market. These escalating costs are placing considerable pressure on profitability within the North American canned seafood market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species/Type: Canned Fish Dominance Faces Premium Shrimp Challenge

In 2025, canned fish accounted for a significant 68.20% share of the North American canned seafood market, driven by the widespread consumer preference for tuna, salmon, and sardine varieties. This substantial share establishes canned fish as the largest single contributor to the market, underscoring the operational efficiencies achieved in procurement and production processes. The market is witnessing a notable shift toward canned shrimp, which is projected to grow at a robust CAGR of 6.62% through 2031. This growth reflects an increasing consumer inclination toward premium products that offer superior texture and a sense of indulgence.

Canned shrimp products are leveraging global flavor combinations and incorporating resealable plastic lids to enhance convenience and cater to snacking occasions. Additionally, a smaller segment focusing on prawns is exploring gourmet positioning by integrating Caribbean and South Asian spice profiles to appeal to niche markets. Manufacturers are also innovating by introducing mixed-species medleys, such as blends of tuna and octopus, to create unique offerings while optimizing the use of existing canning infrastructure. This strategic diversification of species not only opens new revenue streams but also ensures the core offerings of the North America canned seafood market remain unaffected.

By Packaging Material: Steel Cans Resilience Amid Retort Pouch Innovation

In 2025, steel cans constituted 62.80% of the market volume, supported by an established recycling infrastructure and widespread consumer familiarity. Despite ongoing efforts within the industry to achieve lightweighting objectives, steel cans have retained their characteristic rigidity, making them a preferred choice for packaging. Concurrently, the North American canned seafood market is experiencing a significant shift towards retort pouches, which are anticipated to grow at a compound annual growth rate (CAGR) of 7.05%. Retailers are increasingly adopting these pouches due to their reduced logistics costs, while consumers value their convenience, particularly the easy-open tear notches.

Aluminum cans present a balanced solution by combining high recyclability with effective barrier properties. Companies such as B and G Foods, which has pledged to achieve full recyclability by 2027, are leveraging can-to-can closed-loop recycling narratives to emphasize their commitment to sustainability and circular economy principles. Furthermore, innovative packaging formats, including transparent glass jars designed for premium fillets, are gaining traction. These formats cater to gifting occasions and are also being utilized in pilot programs for reusable packaging solutions. The ongoing evolution in packaging formats is largely driven by regulatory mandates to phase out harmful substances such as PFAS and BPA, prompting increased capital investments across the North American canned seafood sector.

By Product Form: Chunks/Pieces Convenience Versus Whole Fish Premium Appeal

Chunks and pieces captured a 57.60% share in 2025, aligning with salad kits, pasta toppers, and sandwich styles. his format's suitability for ready-mix solutions appeals to meal preparation audiences, further driving the penetration of private-label offerings. The consistent demand for chunk light tuna multipacks among urban households highlights the growing emphasis on convenience and efficiency in modern lifestyles.

Whole fish formats, riding the wave of authenticity narratives, are set to grow at an 8.15% CAGR through 2031. Transparent packaging, prominently displaying intact sardines or mackerel, boosts perceived quality. Culinary aficionados value visual cues that enhance plating aesthetics. Producers are innovating with portion-controlled whole fish, bones intact for flavor richness, yet tailored for single servings. Flavor-infused broths, like olive oil with chili, amplify gastronomic allure. This premiumization trend is expanding margins for players in North America's canned seafood market.

By Distribution Channel: Off-Trade Dominance Challenged by Online Retail Growth

Off-trade outlets delivered 62.70% of 2025 revenues, supported by weekly grocery trips and in-store price promotions. Supermarkets and hypermarkets, known for their extensive stock-keeping unit (SKU) variety, strategically utilize end-cap displays to attract consumer attention, particularly during high-demand periods such as Lent and the back-to-school season. Additionally, convenience stores play a significant role in capturing incremental purchases, catering to commuters seeking quick and convenient lunch options.

HoReCa industry players are not only offering unique and convenient flavors but also presenting dishes that patrons may find challenging to replicate at home. With their expertise in cooking techniques and flavor enhancement, restaurants frequently surpass home cooks, particularly in seafood preparation. As a result, the On-Trade sector, projected to grow at a 6.65% CAGR, is witnessing a surge. In online retail, subscription services encourage repeat purchases, and direct-to-consumer startups stand out with unique storytelling and tailored bundles. Supermarkets' e-commerce platforms promote store pickup choices, enhancing the synergy between off-trade and online sales. Yet, despite the digital boom, many consumers still value the tactile experience of inspecting can integrity, underscoring the enduring importance of physical stores in North America's canned seafood landscape.

Geography Analysis

In 2025, the United States holds a commanding 78.10% share of the market, driven by well-established consumption patterns, an expansive retail infrastructure, and high levels of disposable income that encourage the adoption of premium seafood products. The U.S. seafood trade deficit, which reached USD 20.3 billion in 2023, underscores the country's significant reliance on international suppliers. This dependency presents a substantial opportunity for domestic canned seafood processors to capture market share. Retailers leverage the strong consumer trust in long-standing tuna brands, while niche players are gaining traction by introducing MSC-certified albacore product lines that cater to environmentally conscious consumers. Furthermore, government procurement for nutrition assistance programs ensures a consistent baseline demand, contributing to market stability and growth.

Canada ranks as the second-largest market, benefiting from its geographic proximity to both Atlantic and Pacific harvesting regions and a strong cultural preference for seafood. Urban centers such as Toronto and Vancouver exhibit a notable preference for premium pole-and-line seafood selections, reflecting a shift towards sustainable and high-quality options. In Quebec, retailers address local consumer preferences by offering bilingual packaging that complies with regulatory requirements and resonates with the province's cultural nuances. Additionally, nationwide wellness campaigns emphasizing the health benefits of omega-3 fatty acids have bolstered seafood consumption across various demographic groups, enhancing the overall performance of the North American canned seafood market.

Mexico is the fastest-growing market in the region, with a projected CAGR of 7.25% (2026-2031). The rise in middle-class incomes, coupled with the expansion of supermarket chains into tier-two cities, has significantly improved access to canned seafood products. Shelf-stable formats are particularly well-suited to Mexico's warmer climate, where inconsistent electricity supply continues to challenge cold-chain logistics. The integration of canned tuna into traditional dishes such as tacos and salads has further reduced barriers to adoption. Domestic processors are increasingly investing in advanced retort processing lines to meet both domestic demand and export requirements along the North American trade corridor. Additionally, coastal tourism hubs are driving incremental demand through the hospitality sector's sourcing needs. Collectively, these factors are fueling the sustained growth and expansion of the North American canned seafood market.

Competitive Landscape

In the North American canned seafood market, a handful of major players dominate, holding a substantial market share. These key players are increasingly prioritizing sustainable seafood production to attract a broader consumer base. Notable players in the market include Dongwon Enterprise Co., Ltd., Thai Union Group PCL, The Jim Pattison Group, Blue Harbor Fish Co., and Crown Prince, Inc., among others.

Mid-tier players are grappling with intensified challenges. These firms are also forming co-packing alliances, enhancing both plant utilization and negotiating leverage. Their innovation efforts are centered on themes like sustainability, digital traceability, and unique flavors.

Many processors are adopting blockchain verification and QR packaging, allowing consumers to access data directly linked to the vessels. Some are even exploring alternative proteins, combining them with kelp or pulses as a strategy to navigate seafood quota restrictions. As large consumer-goods conglomerates set their sights on these portable protein adjacencies, interest in mergers and acquisitions is on the rise. Such strategic moves ensure the North American canned seafood market remains both dynamic and stable, making it an attractive arena for long-term capital investments.

North America Canned Seafood Industry Leaders

Dongwon Enterprise Co., Ltd.

Thai Union Group PCL

The Jim Pattison Group

Blue Harbor Fish Co.

Crown Prince, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: Island Creek Oysters has inaugurated its first-ever tinned seafood cannery in the U.S. Spanning 10,000 square feet; the facility specializes in crafting European-style, ready-to-go tinned seafood products.

- July 2023: Wild Planet Foods introduced five new sustainably sourced seafood products at Whole Foods Market stores. The company remains committed to sourcing responsibly harvested seafood for its canned product line

- March 2023: Natural Grocers, the largest family-owned organic and natural grocery retailer in the United States, has expanded its premium "Natural Grocers Brand Products" line by introducing five new canned seafood varieties.

North America Canned Seafood Market Report Scope

North America canned seafood market is segmented by type into canned fish, canned prawns, canned shrimp, and other canned seafood. Canned fish is further segmented into tuna, salmon, and other canned fish. By distribution channel the scope includes supermarkets/ hypermarkets, convenience stores, online retail stores, and other distribution channels. By geography the scope includes United States, Canada, Mexico, and Rest of North America.

By Species/Type

| Canned Fish | Tuna |

| Salmon | |

| Sardines | |

| Mackerel | |

| Other Canned Fish | |

| Canned Shrimp | |

| Canned Prawns | |

| Other Types |

By Packaging Material

| Steel Cans |

| Aluminum Cans |

| Retort Pouches |

| Others |

By Product Form

| Whole |

| Chunks/Pieces |

By Distribution Channel

| Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail | |

| Specialty Stores | |

| Other Distribution Channels | |

| On-Trade (HoReCa) |

By Geography

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Species/Type | Canned Fish | Tuna |

| Salmon | ||

| Sardines | ||

| Mackerel | ||

| Other Canned Fish | ||

| Canned Shrimp | ||

| Canned Prawns | ||

| Other Types | ||

| By Packaging Material | Steel Cans | |

| Aluminum Cans | ||

| Retort Pouches | ||

| Others | ||

| By Product Form | Whole | |

| Chunks/Pieces | ||

| By Distribution Channel | Off-Trade | Supermarkets/Hypermarkets |

| Convenience Stores | ||

| Online Retail | ||

| Specialty Stores | ||

| Other Distribution Channels | ||

| On-Trade (HoReCa) | ||

| By Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Key Questions Answered in the Report

What is the current value of the North America canned seafood market?

The North America canned seafood market size stands at USD 9.43 billion in 2026 and is on track to reach USD 12.53 billion by 2031.

Which species segment leads the market?

Canned fish dominates with 68.20% share in 2025, driven mainly by tuna, salmon, and sardines.

Which geography is expanding the quickest?

Mexico is forecast to record a 7.25% CAGR through 2031 thanks to rising incomes and broader supermarket coverage.

Why are retort pouches gaining popularity?

Retort pouches support lighter shipping weights, quick opening, and compliance with PFAS-free mandates, which fuels a 7.05% CAGR outlook.

Page last updated on: