Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

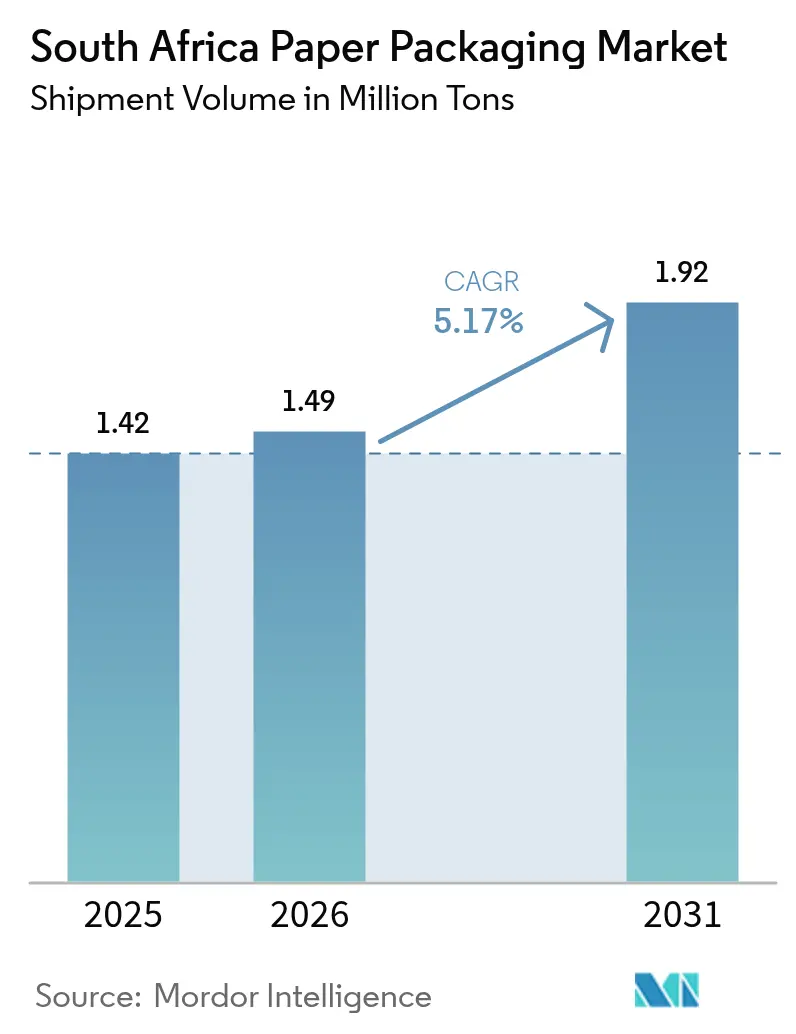

| Base Year Market Size (2025) | 1.42 Million tons |

| Market Volume (2026) | 1.49 Million tons |

| Market Volume (2031) | 1.92 Million tons |

| Growth Rate (2026 - 2031) | 5.17% CAGR |

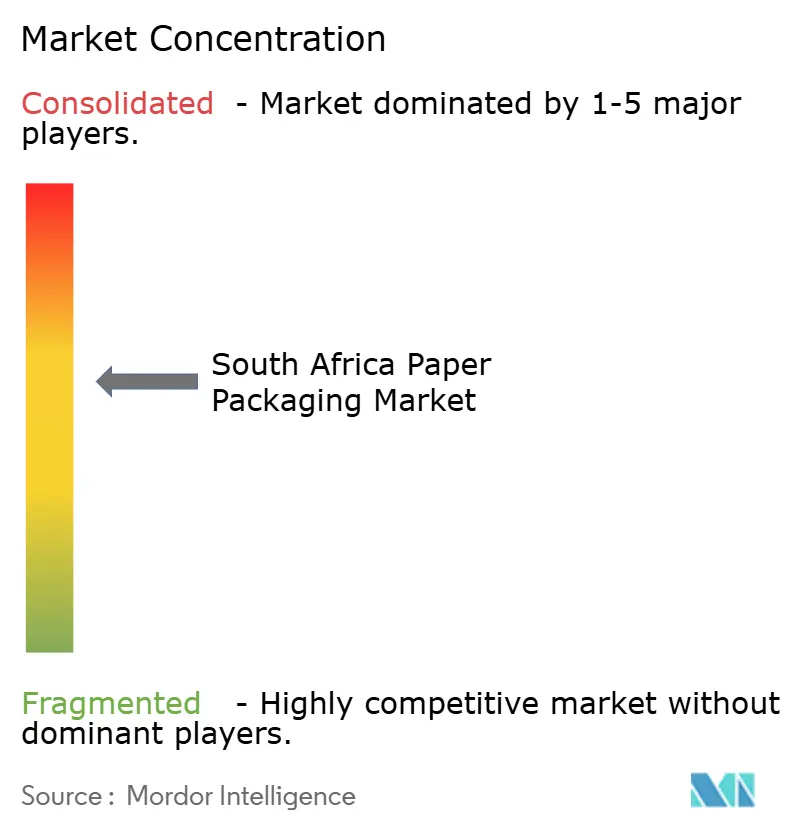

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Africa Paper Packaging Market Analysis by Mordor Intelligence

The South Africa paper packaging market size is expected to grow from 1.42 million tons in 2025 to 1.49 million tons in 2026 and is forecast to reach 1.92 million tons by 2031 at 5.17% CAGR over 2026-2031. Regulators continue to escalate the national carbon-tax rate and tighten plastic restrictions, boosting demand for fiber-based formats that carry a lower life-cycle footprint than most polymer alternatives. Load-shedding disruptions are prompting mills to invest in captive solar and wheeled wind power, improving operational resilience while lowering Scope 2 emissions. Brand owners in fast-moving consumer goods and agriculture are adopting connected and traceable packs that communicate provenance, nutrition, and responsible-sourcing credentials. At the same time, high-graphic flexo and digital printing systems enable cost-effective short runs, encouraging design refreshes that keep pace with e-commerce sales cycles.

Key Report Takeaways

- By material type, corrugated board accounted for 44.58% of market share in 2025. while kraft paper is forecast to post the fastest expansion, advancing at a 6.56% CAGR to 2031.

- By product type, rigid paper packaging captured 54.12% revenue share in 2025, while flexible paper packaging is projected to rise at a 6.08% CAGR through 2031.

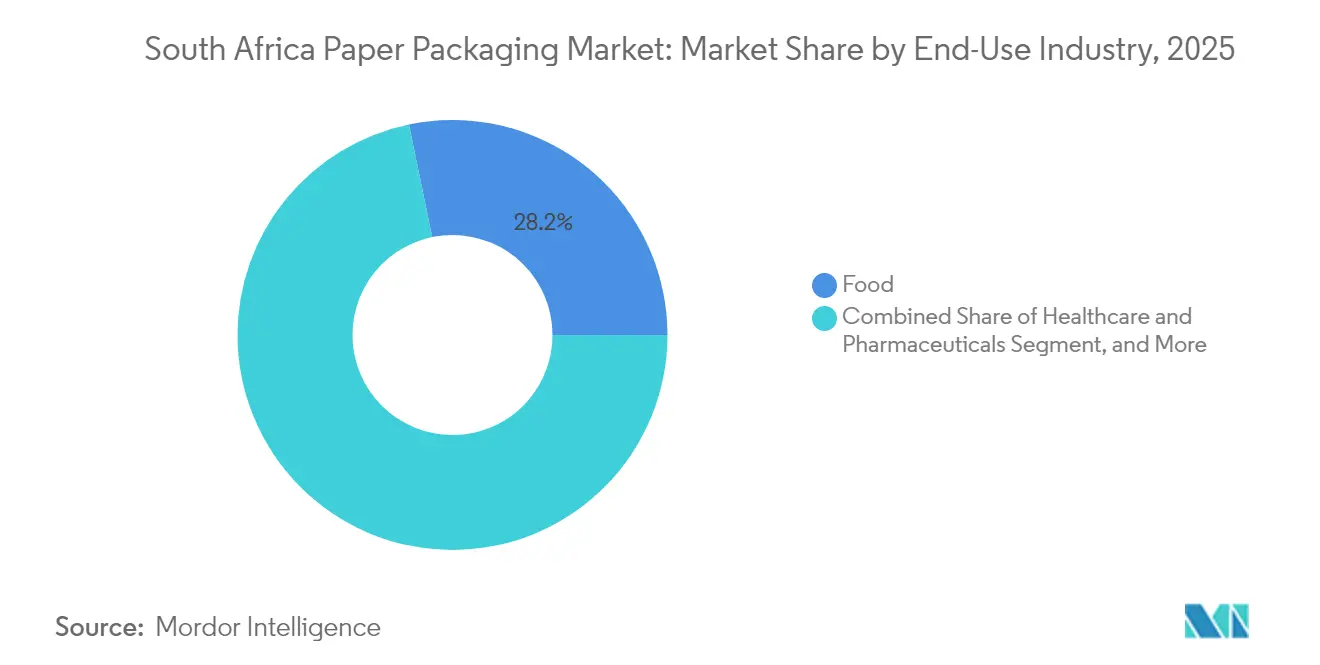

- By end-use industry, food sector commanded 28.25% of the 2025 demand, but healthcare and pharmaceuticals are expected to register the highest growth at a 6.65% CAGR to 2031.

- By distribution channel, direct sales channels held 56.18% of the 2025 volume, whereas indirect sales are anticipated to expand at a 6.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

South Africa Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fand B sector packaging boom | +1.2% | National, concentrated in Western Cape, Gauteng | Medium term (2-4 years) |

| E-commerce fulfillment demand | +0.8% | Urban centers: Cape Town, Johannesburg, Durban | Short term (≤ 2 years) |

| Plastic-ban legislation | +1.0% | National, with provincial variations | Long term (≥ 4 years) |

| Export-fruit carton innovations | +0.6% | Western Cape, Eastern Cape citrus regions | Medium term (2-4 years) |

| Child-resistant cannabis cartons | +0.3% | National, emerging regulatory framework | Long term (≥ 4 years) |

| Carbon-tax driven lightweighting | +0.7% | National, affecting energy-intensive manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fand B Sector Packaging Boom

Food and beverage processors are redesigning packs to lengthen shelf life, cut waste, and showcase provenance credentials. PepsiCo’s post-acquisition investment program added more than 40 production sites that consume diversified corrugated, cartonboard, and barrier-paper formats. Shelf-stable dairy producer Woodlands Dairy recorded a 30% sales uplift after deploying interactive QR-enabled cartons, underscoring the commercial power of connected packaging. Mpact’s Freshpact range supplies single-flute kraft crates that are fully recyclable and compostable, helping grocery retailers hit mandatory recovery targets. These initiatives drive sustained tonnage growth for the South Africa paper packaging market.

E-commerce Fulfillment Demand

Parcel volumes linked to online retail rose in 2024 as omnichannel merchants pushed stock through last-mile networks. Shippers require sturdy yet lightweight boxes engineered for diverse fulfillment centers, spurring orders for multi-depth corrugated SKUs and custom-fit void fillers. DHL reports retail modernization is shifting buyer preference toward home delivery and click-and-collect, elevating demand for brandable, frustration-free packs. Urban consumers also voice stronger sustainability expectations, favoring recyclable board over single-use plastic mailers. Together, these trends reinforce a resilient growth pipeline for the South Africa paper packaging market.

Plastic-Ban Legislation

Successive ministerial notices restrict non-recyclable or difficult-to-collect plastic items and set escalating recovery targets. Although enforcement gaps persist, policy direction clearly favors biodegradable and recyclable substrates. The Department of Forestry, Fisheries, and the Environment targets diverting more than 58% of packaging waste from landfill within five years, a goal that aligns directly with mature recycling infrastructure already servicing paper grades. Fiber converters thus benefit from a regulatory tailwind that nudges brand owners toward paper-based formats, bolstering long-term demand.

Export-Fruit Carton Innovations

South Africa’s citrus exporters require temperature-resistant cartons that comply with EU and Chinese cold-treatment rules. Lightweight flute profiles, stronger edge-crush ratings, and RFID-enabled labels are now commonplace in lemon and orange shipments. Produce Report forecasts a 12% lift in lemon and lime exports for the 2023/24 season, sustaining orders for specialty board optimized for chilled logistics. Manufacturers that supply FSC-certified, condensation-resistant boxes enjoy preferred-supplier status with export pack-houses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile pulp and recovered-paper prices | -1.4% | National, affecting all manufacturers | Short term (≤ 2 years) |

| Forest stewardship/deforestation limits | -0.6% | KwaZulu-Natal, Mpumalanga forestry regions | Long term (≥ 4 years) |

| Load-shedding energy disruptions | -1.8% | National, concentrated in industrial areas | Medium term (2-4 years) |

| Limited barrier-paper recycling | -0.4% | Urban recycling centers, Cape Town focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Pulp and Recovered-Paper Prices

Fluctuations in global kraft pulp and local recovered-paper prices compress gross margins and complicate budgeting cycles. Mondi’s interim results for 2024 revealed higher pulp costs despite favorable currency hedges, illustrating bottom-line sensitivity to fiber volatility. Smaller sheet-feed converters lack integration and therefore face sharper cost swings, which can slow capital spending on new packaging lines, weighing on near-term growth for the South Africa paper packaging market.

Load-Shedding Energy Disruptions

Recurring power outages force mills to halt paper machines or absorb steep diesel-generator bills. Investec estimates rolling blackouts clipped 2.1% off GDP in a recent quarter, reflecting the macro-level drag on heavy industry. Although equipment upgrades and on-site renewables improve resilience, many small converters cannot finance the transition quickly. Production delays and cost inflation temper the otherwise robust expansion trajectory of the South Africa paper packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type – Corrugated Board Holds Critical Mass

Corrugated Board generated the largest tonnage in 2024, supplying agriculture, e-commerce, and fast-moving consumer goods. Mpact’s network of nine corrugated plants provides short lead times and customized die-cutting that align with brand marketing calendars. The South Africa paper packaging market size allocated to Corrugated Board is forecast to climb steadily as online retailers and produce exporters favor high-stacking-strength boxes. Kraft Paper, although smaller in absolute terms, is scaling fastest. Coated and uncoated kraft grades integrate water-based barrier coatings that unlock frozen food and dry goods applications previously dominated by laminates, creating a fresh opportunity lane within the South Africa paper packaging market.

Beyond those top performers, Paperboard retains a resilient niche in folding carton for confectionery, pharma, and beauty segments. Sappi’s shift from graphic paper toward packaging grades signals long-run optimism for cartonboard demand. Specialty grades, including grease-resistant wraps and pharmaceutical inserts, round out the material portfolio, catering to compliance-heavy end markets that demand traceability and hygienic performance.

By Product Type – Rigid Formats Still Command Majority Share

Rigid Paper Packaging dominated shipments thanks to extensive use of corrugated boxes, solid bleached sulfate cartons, and industrial sleeves. Customers value the crush resistance and shelf-display versatility these formats provide. The South Africa paper packaging market share for Rigid formats is expected to moderate slightly as Flexible Paper Packaging accelerates. Recent launches such as Sappi’s Changemaker concept pair printable cartonboard with advanced barrier paper to offer resealable and heat-sealable pouches that replace multi-layer films.

Flexible solutions also benefit from quick-turn gravure and digital presses that accommodate micro-runs for promotional campaigns. Consumer brands targeting urban millennials prefer stand-up kraft pouches and twist-wraps that underscore environmental credentials while preserving food safety. This shift drives incremental volume for converters that master water-based barrier coatings and precision slitting.

By End-Use Industry – Healthcare and Pharmaceuticals Expand Rapidly

While Food retained the highest 2024 volume, pharmaceutical and medical device players are fueling outsized gains. Updated South African Health Products Regulatory Authority rules require tamper-evident and child-resistant cartons for regulated therapeutics, elevating demand for board grades with precise caliper control. Cannabis-derived product restrictions implemented in March 2025 further complicate sourcing, favoring converters with deep regulatory expertise.the

Beverage brands leverage luxury cartons for premium wine exports, while personal-care companies adopt high-gloss folding cartons that convey brand story at point of sale. Industrial and electronics sectors continue to rely on heavy-duty corrugated bins and corner-protection sets for intra-factory movement of metal and plastic components.

By Distribution Channel – Direct Sales Retain Primacy, Indirect Gains Momentum

Large buyers still source directly from integrated mills to secure predictable volumes and co-develop custom specifications, keeping Direct Sales in the majority. Integrated suppliers bundle technical services, linerboard supply, and recovery programs, strengthening buyer stickiness. However, Indirect Sales via specialist distributors are scaling fast. Smaller e-tailers and craft-food producers value online portals that offer low minimum order quantities and rapid design templates. Digitalization lowers transaction costs, enabling distributors to reach underserved rural businesses that struggle to meet direct minimums. The expanding distributor footprint diversifies access routes to the South Africa paper packaging market, increasing competitive pressure on mill sales teams.

Geography Analysis

The Western Cape anchors export-oriented demand tied to citrus, table grapes, and wine. High humidity and cold-chain requirements push converters to supply wax-free, water-resistant corrugated grades that survive multi-week sea voyages. Gauteng, as the economic heartland, absorbs the highest FMCG cartonboard tonnage. Its proximity to retail headquarters accelerates design-approval cycles and just-in-time deliveries.

KwaZulu-Natal benefits from the Port of Durban, South Africa’s busiest container hub, although congestion has nudged some exporters toward Maputo. Converters in Durban leverage that shift by offering cross-border warehousing services. The Eastern Cape’s automotive corridor drives demand for returnable corrugated dunnage and expendable export packs that protect catalytic converters, seat frames, and electronic harnesses.

Inland provinces such as Mpumalanga supply forestry feedstock and host biomass-rich plantations certified under FSC and SAFAS schemes, underpinning sustainable raw-material sourcing. These forests also employ community smallholders, supporting inclusive economic development. Across all provinces, mills are progressively installing rooftop solar and wheeled wind contracts to mitigate load-shedding, ensuring the South Africa paper packaging market remains operationally resilient.

Competitive Landscape

MPACT operates three paper mills totaling more than 400,000 tons of annual capacity and runs the nation’s largest collection network for recyclable packaging, giving it cost-effective access to recovered fiber. Sappi differentiates through high-brightness paperboard and has locked in a 175 GWh/year power-purchase agreement that will trim Scope 2 emissions and buffer energy costs.[2]Bizcommunity, “Guala Closures to acquire Coleus Packaging,” bizcommunity.com Mondi boasts global integration, and this scale deepened after its USD 6.3 billion purchase of DS Smith, which extends its containerboard footprint and South African corrugated capacity.

Competitive strategies increasingly emphasize cradle-to-cradle design, lightweighting, and carbon-neutrality pledges. Double-A CDP ratings for forestry stewardship and water security highlight Mondi’s leadership in environmental disclosure.[3]Mondi Group, “Double A CDP scores,” mondigroup.com Smaller regional converters attempt to carve niches in quick-turn flexographic printing or specialty barrier coatings but face capital constraints when matching the R&D budgets of integrated giants. Ongoing consolidation, such as Guala Closures’ acquisition of Coleus Packaging, signals further rationalization among ancillary suppliers

South Africa Paper Packaging Industry Leaders

Sappi Limited

Mondi plc

Nampak Limited

Mpact Limited

Corruseal Holdings (Pty) Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Sappi completed a USD 500 million upgrade of Paper Machine 2 at Somerset Mill, doubling SBS capacity to 470,000 tons annually and supplying converters with brighter, stiffer board grades.

- May 2025: Kapag and Sappi introduced Changemaker fully recyclable barrier-paper packs for food, cosmetics, and pet food.

- March 2025: The health ministry banned foodstuffs containing Cannabis sativa derivatives, driving carton redesign and supply-chain adjustments.

- March 2024: Mondi agreed to absorb DS Smith for R119 billion (USD 6.3 billion), cementing its position as a global packaging leader.

South Africa Paper Packaging Market Report Scope

Paper packaging is a cost-efficient and versatile method to protect, preserve, and transport a broad range of products. Additionally, it can be customized to meet customers' needs or product-specific requirements. Attributes like biodegradability, lightweight, and recyclability of paper packaging make it an essential component for packaging. This type of packaging is currently used for designing new and beautiful models and adding branding functions.

The South Africa paper packaging market is segmented by product type (folding cartons, corrugated boxes, and other product types [flexible paper, liquid cartons, and others]) and end-user industry (food, beverage, healthcare, personal care, household care, electrical products).

The market sizes and forecasts are provided in volume (metric tons) for all the above segments.

By Material Type

| Kraft Paper |

| Paperboard |

| Corrugated Board |

| Other Material Types |

By Product Type

| Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | |

| Other Flexible Paper Packaging | |

| Rigid Paper Packaging | Folding Carton |

| Corrugated Boxes | |

| Other Rigid Paper Packaging |

By End-Use Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial and Electronic |

| Other End-Use Industries |

By Distribution Channel

| Direct Sales |

| Indirect Sales |

| By Material Type | Kraft Paper | |

| Paperboard | ||

| Corrugated Board | ||

| Other Material Types | ||

| By Product Type | Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | ||

| Other Flexible Paper Packaging | ||

| Rigid Paper Packaging | Folding Carton | |

| Corrugated Boxes | ||

| Other Rigid Paper Packaging | ||

| By End-Use Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial and Electronic | ||

| Other End-Use Industries | ||

| By Distribution Channel | Direct Sales | |

| Indirect Sales | ||

Key Questions Answered in the Report

What is the forecast volume for South Africa paper packaging by 2031?

The market is projected to reach 1.92 million tons by 2031, up from 1.49 million tons in 2026.

Which segment shows the fastest growth within South Africa paper packaging?

Kraft Paper leads with a projected 6.56% CAGR through 2031.

How is load-shedding influencing packaging manufacturers?

Producers are adding on-site renewables and backup generators to maintain paper-machine uptime and manage energy costs.

Why are citrus exporters demanding specialized cartons?

Temperature-resistant, condensation-proof cartons comply with cold-treatment rules for EU and Chinese markets, protecting fruit quality during long sea voyages.

How concentrated is the competitive landscape?

The top five suppliers hold about 60% of output, reflecting a moderately consolidated market with some space for regional converters.

Page last updated on: