Live Music Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

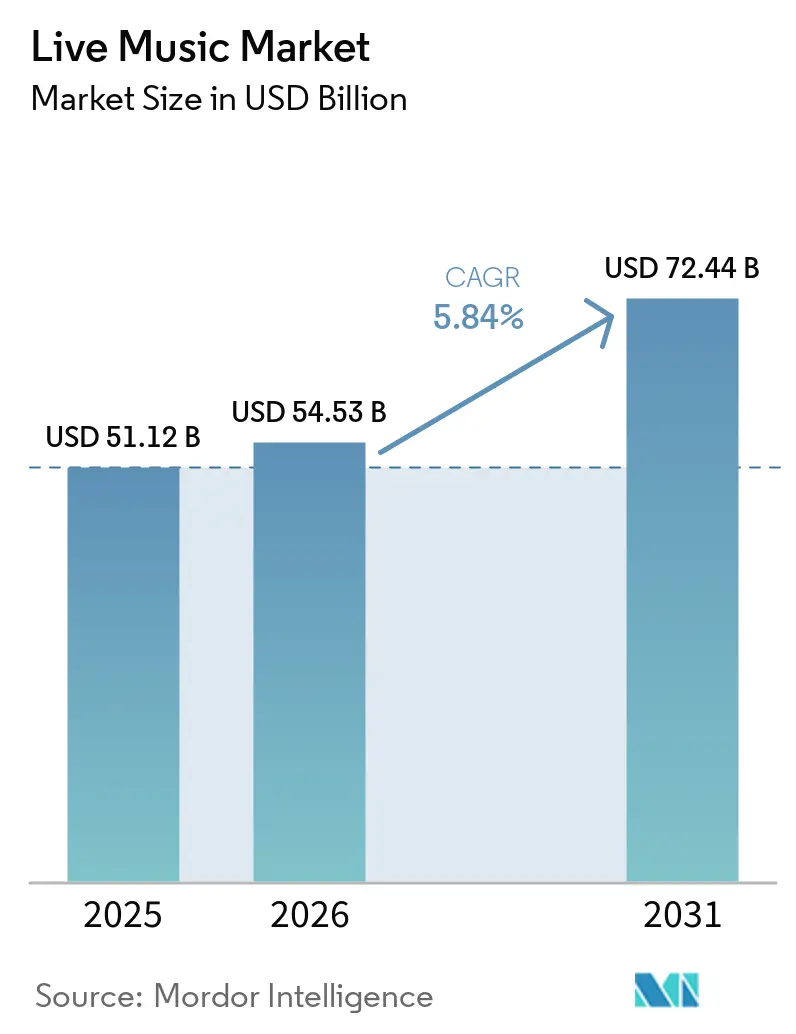

| Market Size (2026) | USD 54.53 Billion |

| Market Size (2031) | USD 72.44 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Live Music Market Analysis by Mordor Intelligence

The Live Music market size is expected to increase from USD 51.1 billion in 2025 to USD 54.5 billion in 2026 and reach USD 72.4 billion by 2031, growing at a CAGR of 5.8% over 2026-2031. The live music market is moving on a broader base than simple recovery, because large tours, repeat attendance, and stronger demand outside the United States are now supporting growth across more countries. The live music market is also benefiting from the closer link between streaming reach and ticket demand, which is helping artists fill more dates across more cities with less delay between digital discovery and ticket conversion. Premium ticketing, sponsorship, and venue expansion are improving revenue per fan, which gives large operators more room to invest across promotion, venues, and data systems. At the same time, the live music market faces real pressure from higher production costs, rising artist fees, and tighter regulatory attention on ticketing practices. This keeps the outlook positive, but it also means that execution, scale, and access to integrated infrastructure matter more than before.

Key Report Takeaways

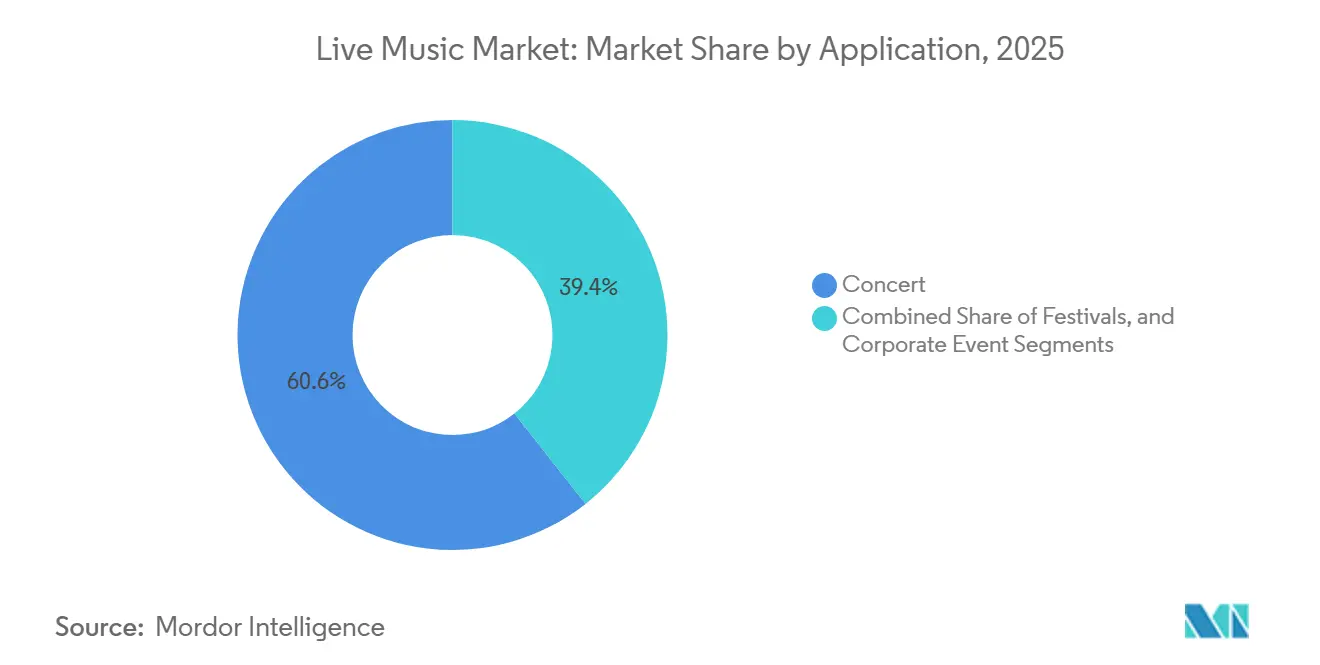

- By application, concerts held 60.62% of the market in 2025, while festivals are forecast to expand at a 6.5% CAGR through 2031.

- By revenue stream, ticket sales accounted for 69.12% share of the live music market size in 2025, while sponsorship is projected to grow at a 6.4% CAGR through 2031.

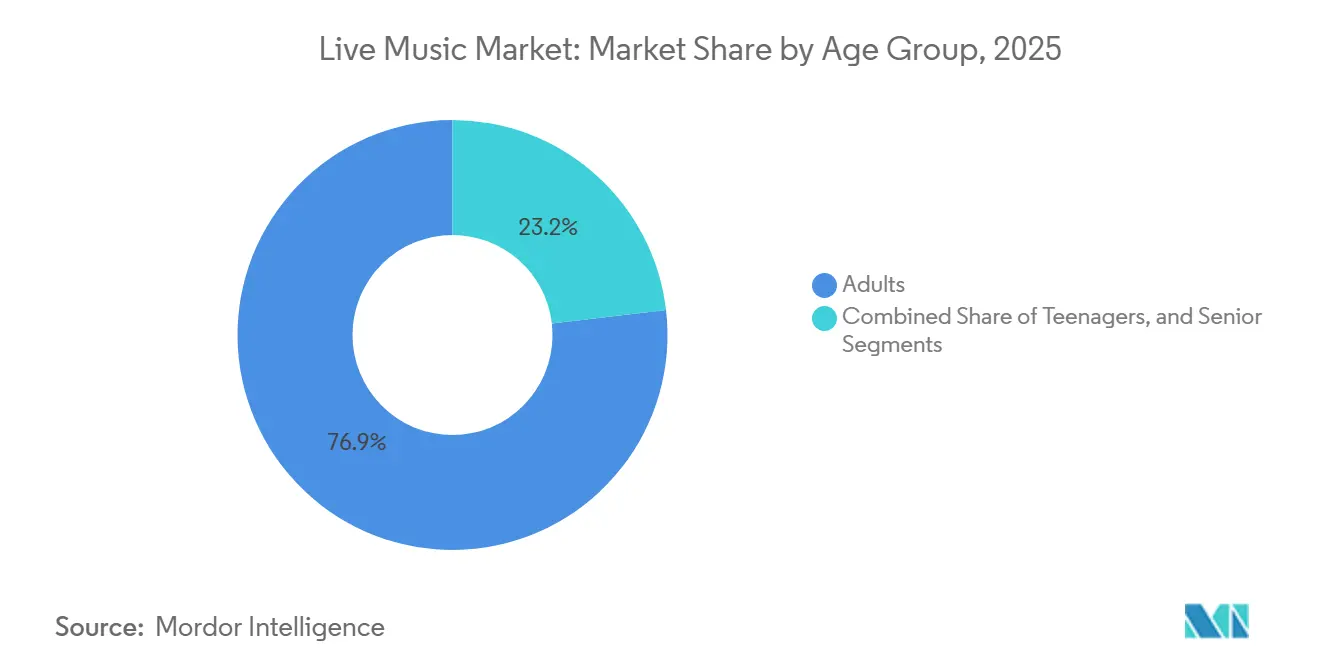

- By age group, adults held 76.85% of the market in 2025, while teenagers are expected to record the highest CAGR at 6.4% through 2031.

- By venue size, large venues captured 54.27% of the market in 2025, while medium venues are projected to advance at a 6.3% CAGR through 2031.

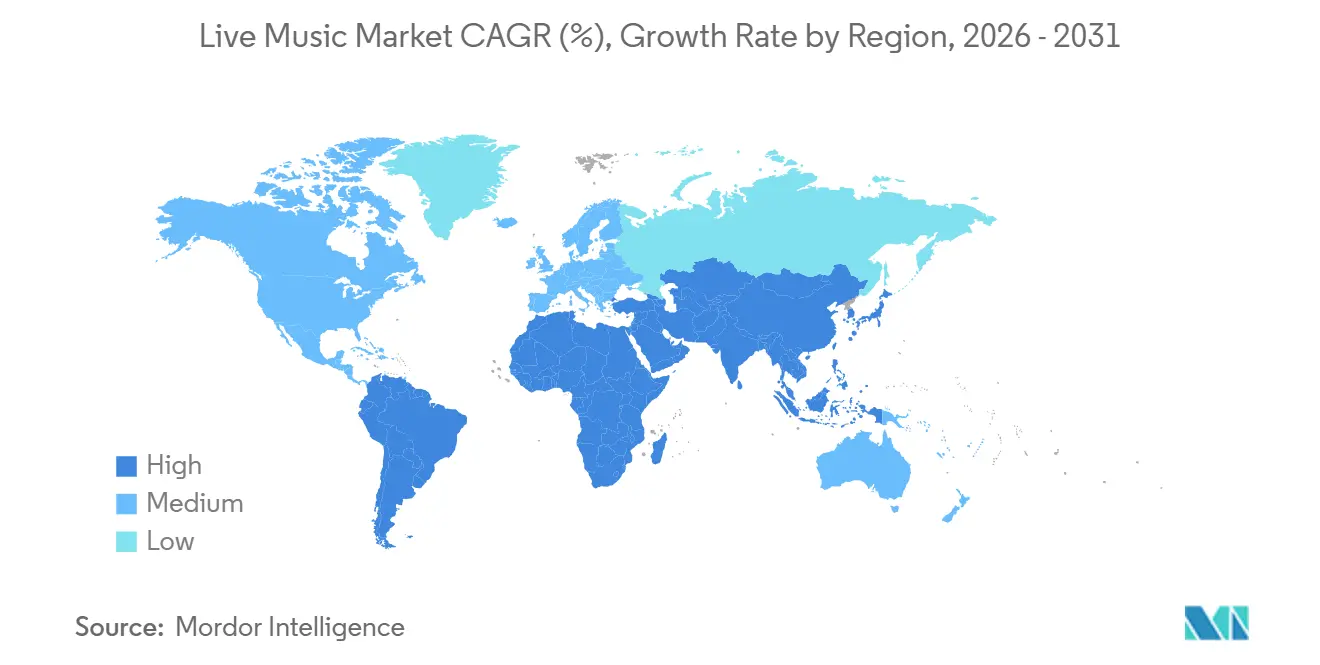

- By geography, North America held 49.67% of the live music market share in 2025, while Asia-Pacific is set to expand at a 6.3% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Live Music Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Premium Ticketing and VIP Monetization | +1.4% | Global, North America and Western Europe lead adoption | Short term (≤ 2 years) |

| Expansion of Brand Sponsorship and Experiential Marketing Budgets | +1.0% | Global, North America and Europe lead, Asia-Pacific scaling rapidly | Medium term (2-4 years) |

| Surge in Hybrid and Data-Driven Fan Engagement Models | +0.8% | Global, strongest in digitally connected markets | Medium term (2-4 years) |

| Growth Of Multi-City Touring and Festival Ecosystems | +0.7% | Global, Asia-Pacific and South America emerging as key expansion corridors | Medium term (2-4 years) |

| Rising Demand for Immersive, Shareable Live Experiences | +0.6% | Global, urban markets in North America, Europe, and East Asia | Long term (≥ 4 years) |

| Expansion of Secondary Spend across Merchandising and Hospitality | +0.5% | Global, highest revenue impact in North America and Western Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Premium Ticketing and VIP Monetization

Premium tiers are lifting revenue without requiring a similar rise in attendance, which is one of the clearest supports for the live music market. Live Nation stated that 75% of its United States tickets stayed below USD 100 in 2025, which shows that broad access and premium upsell are now working side by side rather than as opposites.[1]Live Nation Entertainment, “Full Year and Fourth Quarter 2025 Results,” Live Nation Newsroom, newsroom.livenation.com Spotify expanded this model in June 2026 when it launched Reserved in the United States for eligible Premium users in partnership with Live Nation and Ticketmaster.[2]Spotify, “How Reserved by Spotify Works A Step-by-Step Guide,” Spotify Newsroom, newsroom.spotify.com That kind of access model helps the live music market separate casual buyers from high-intent fans in a more organized way. It also gives promoters more control over yield, while keeping the base offer visible enough to protect attendance.

Expansion of Brand Sponsorship and Experiential Marketing Budgets

Sponsorship has become a more important growth lever because brands now expect measurable engagement instead of simple logo placement, and that shift is helping the live music market diversify beyond ticket sales. Live Nation reported that sponsorship adjusted operating income reached USD 845 million in 2025, up 11%, and it said 85% of full-year 2026 sponsorship commitments were already booked by the end of April. That booking pattern looks more like a scaled media business than an occasional event budget. The live music market also benefits because sponsorship income can offset volatility in ticket prices and production costs. Operators with strong festival properties, premium venues, and direct fan data are in the best position to turn that demand into recurring contracts.

Surge in Hybrid and Data-Driven Fan Engagement Models

Fan discovery, ticketing, and purchase timing are becoming more connected, which improves conversion efficiency across the live music market. SeatGeek said in February 2026 that its Spotify integration placed primary ticket inventory inside Spotify's event discovery experience for 751 million monthly active users. Live Nation reported event-related deferred revenue of USD 6.6 billion at the end of Q1 2026, up 22%, which points to a stronger forward revenue pipeline built on earlier fan commitment. Fever also strengthened this model when it acquired DICE in June 2025, creating a broader discovery-to-ticketing platform with more than 10 million monthly active users. As a result, the live music market is moving toward systems where streaming behavior, purchase history, and location signals shape routing, presales, and venue planning.

Growth of Multi-City Touring and Festival Ecosystems

Multi-city networks are improving scale economics, and that is helping the live music market expand across more geographies with lower per-event friction. AEG Presents widened its European footprint through the We Love Green acquisition in 2025 and the launch of Roundhay Festival for 2026. Live Nation also increased its venue base in 2026 through acquisitions in Chile, Italy, and Thailand, adding around 4 million in annual fan capacity. These moves matter because the live music market is increasingly shaped by operators that can combine routing, venue access, sponsorship sales, and data across multiple stops. The same scale advantages also raise the pressure on independent promoters that do not control a wider calendar or estate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Artist, Venue, and Production Costs | -1.8% | Global, Germany, the UK, and North America show the highest documented cost pressure | Short term (≤ 2 years) |

| Ticket Price Sensitivity and Demand Pushback | -1.2% | Global, North America and Western Europe most exposed at current price points | Short term (≤ 2 years) |

| Weather Volatility and Outdoor Event Disruption Risk | -0.5% | Global, outdoor festival-heavy markets in the UK, Germany, and the United States | Medium term (2-4 years) |

| Rising Compliance Burden across Safety, Noise, and Crowd Control | -0.3% | Europe and Asia-Pacific most affected by tightening venue and event regulations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Artist, Venue, and Production Costs

Cost inflation is the sharpest near-term constraint on the live music market, especially below the top tier of global operators. BDKV said that production costs in Germany rose 50% since the pandemic, while ticket prices increased 30%, and artist fees tripled in some cases.[3]Bundesverband der Konzert- und Veranstaltungswirtschaft, “Festivalbranche Verzeichnet Hohe Nachfrage Trotz Wirtschaftlicher Belastungen,” CIM Fachmagazin der Eventbranche, cimunity.com Live Nation disclosed that it invested nearly USD 15 billion in artists and shows in 2025, which shows how much capital scale now matters in this business. That gap is widening the distance between integrated leaders and smaller independent operators across the live music market. It also makes sponsorship, owned venues, and onsite spend more important because they provide other ways to absorb rising show costs.

Ticket Price Sensitivity and Demand Pushback

Pricing pressure remains a real demand risk for the live music market, even when headline attendance is still healthy. Live Nation kept 75% of its United States tickets below USD 100 in 2025, which suggests that broad attendance still depends on affordable entry tiers. BDKV also reported growing price sensitivity in Germany, even though regular concert attendance remained above pre-pandemic levels.[4]Bundesverband der Konzert- und Veranstaltungswirtschaft, “Festivals Bleiben Priorität,” BDKV, bdkv.de This means the live music market cannot rely only on higher face values to grow revenue. Operators that explain pricing clearly and separate premium inventory from standard access are more likely to protect both trust and conversion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Concerts Anchor Revenue, Festivals Accelerate Growth

Concerts accounted for 60.62% of live music market share in 2025, which kept them as the main commercial format for the largest tours. The segment remains central to the live music market because stadium and arena shows offer the highest revenue potential per night when ticketing, sponsorship, and hospitality work together. Live Nation's Concert segment generated USD 20.9 billion in 2025, equal to 83% of its total revenue, and fan attendance rose 5% during the year. That scale shows why concerts remain the base layer of the live music market even as other formats grow.

Festivals are projected to grow at a 6.5% CAGR through 2031, making them the fastest-growing application in the live music market. Their format supports longer audience dwell time, multiple stages, and stronger brand integration, which gives sponsors and organizers more revenue touchpoints than a single-show event. BDKV estimated that Germany had around 1,800 music festivals in 2025, which points to both depth of demand and a crowded operating field. Corporate events remain the smaller third segment, but they add diversification for venue operators and production companies. Their demand base is less tied to household spending, which gives the live music market one steadier pocket of B2B revenue during softer consumer cycles.

By Revenue Stream: Ticket Sales Lead as Sponsorship Scales Fast

Ticket sales represented 69.12% share of the live music market size in 2025, so the core economics of the live music market still start with paid admission. Live Nation said Ticketmaster's fee-bearing concert gross transaction value reached USD 26 billion in 2025 across 346 million fee-bearing tickets. That volume confirms how central ticketing remains to funding tours, venues, and promotion. It also shows why regulators, artists, and consumers continue to focus on fee structures and transparency.

Sponsorship is forecast to expand at a 6.4% CAGR through 2031, making it the fastest-growing revenue stream in the live music market. Live Nation reported that 85% of its full-year 2026 sponsorship commitments were booked by the end of April, which indicates deeper planning cycles and stronger advertiser confidence. Merchandising remains smaller, but it is gaining support from faster onsite payments and stronger upsell design inside premium venues. The revenue mix in the live music market is therefore becoming more balanced, especially for operators with direct fan data and repeat access to high-traffic properties.

By Age Group: Adults Dominate, Teenagers Drive Fastest Expansion

Adults held 76.85% of the market in 2025, which reflects their larger spending power and stronger willingness to buy premium seats, hospitality, and higher-value packages. This keeps adults at the center of the live music market because they convert music interest into dependable spend across ticketing and secondary purchases. The segment also supports premium inventory strategies better than other age groups because it has a broader range of budgets and stronger repeat attendance patterns. That makes adult demand especially important for the live music market in North America and Europe, where higher-priced touring formats are most established.

Teenagers are set to grow at a 6.4% CAGR through 2031, making them the fastest-rising age cohort in the live music market. In South Korea, ticket sales for overseas artist concerts rose sharply in 2025, which points to stronger youth participation in live events and international touring demand. Platforms built around discovery, mobile purchase, and social sharing are well aligned with how this group decides what to attend. That gives the live music market a longer-term pipeline of future high-frequency attendees. Seniors remain a smaller segment, but they can still support better per-fan revenue where venues offer comfort, accessibility, and premium service features.

By Venue Size: Large Venues Lead, Mid-Size Gains Momentum

Large venues captured 54.27% of the market in 2025, which shows that the highest-value activity in the live music market still sits with stadiums and major arenas. Live Nation expanded this position in 2026 through acquisitions of Movistar Arena Santiago, Unipol Forum in Milan, and IMPACT Arena Bangkok, adding around 4 million in annual fan capacity. Large venues remain critical because they combine scale, premium inventory, and strong food, beverage, and sponsorship economics in one asset. That keeps them at the top of the live music market when global artists route major tours.

Medium venues are projected to grow at a 6.3% CAGR through 2031, which makes them the fastest-growing venue segment in the live music market. CTS Eventim highlighted the opening of the Unipol Dome in Milan as part of its broader expansion, showing how operators are positioning mid-to-large assets as multi-use anchors. This segment fits artists who are moving beyond club tours but do not yet need full arena production. It also gives the live music market more flexibility across city tiers and event types. Small venues remain important as talent pipelines, but they face the heaviest margin pressure because fixed costs are rising faster than their pricing power.

Geography Analysis

North America held 49.67% of the live music market share in 2025, which kept it as the largest regional base for the live music market. Live Nation said concert ticket gross transaction value in January 2026 rose more than 50% year over year, led by North American on-sales. The region benefits from deep venue infrastructure, strong consumer spending on premium experiences, and dense touring calendars. It also remains the key testing ground for pricing, ticketing technology, and regulatory changes.

Asia-Pacific is forecast to grow at a 6.3% CAGR through 2031, which makes it the fastest-growing region in the live music market. South Korea recorded KRW 1.7326 trillion in ticket sales in 2025, equal to USD 1.24 billion, and that total rose 18.8% from the prior year. The region combines several different growth models, including K-pop driven demand in Korea, international act expansion in India, and strong domestic artist dependence in Japan. India's organized live events sector was valued at INR 12,000 crore, equal to USD 1.43 billion, and it is expected to exceed INR 20,000 crore, equal to USD 2.38 billion, by 2027. Japan also remains strategically important because local repertoire still dominates listening, which makes partnership-led entry more effective than direct expansion for international operators.

Europe remained commercially important to the live music market in 2025, supported by strong ticket revenue and dense touring circuits. Spain reported EUR 807.2 million in live music ticket revenue in 2025, equal to USD 888 million, marking a fourth consecutive annual record. Germany's GEMA reported EUR 530 million in live and background music royalties in 2025, equal to USD 583 million, across 870,000 events. South America is expanding as larger operators add venues and sponsorship programs, while the Middle East is gaining relevance through state-backed entertainment infrastructure. Africa remains earlier in formal development, but its young demographics and mobile-first audience give the live music market longer-term demand potential.

Competitive Landscape

The live music market is led by a small group of scaled operators, but it still leaves room for regional promoters, venue owners, and specialist ticketing platforms. Live Nation reported 159 million fans across 55,000 events in 2025, while CTS Eventim said it handled more than 300 million ticket transactions annually across more than 25 countries. That scale gives both companies strong leverage in venue access, promoter relationships, and consumer reach across the live music market. It also raises the barrier for smaller firms that lack owned infrastructure or high-volume ticketing networks.

Strategic expansion in 2025 and 2026 shows how the live music market is being shaped by portfolio building rather than isolated event growth. Live Nation added major venues in Chile, Italy, and Thailand in 2026, which increased international capacity and widened its control over premium touring routes. CTS Eventim crossed EUR 3 billion in revenue in 2025, equal to USD 3.39 billion, and it continued to position ticketing, data, and venue assets as linked growth engines. AEG Presents widened its summer festival network through We Love Green and Roundhay Festival, which strengthened its position in European outdoor events. These moves show that the live music market increasingly rewards operators that can connect promotion, venues, ticketing, and sponsorship inside one system.

Technology is the main competitive lever below the top promoter tier in the live music market. SeatGeek used its Spotify integration in 2026 to push ticket inventory closer to the moment of discovery, while Fever strengthened its live events stack through the DICE acquisition in 2025. This keeps competitive pressure high in areas such as mobile conversion, presale targeting, and fan analytics. The live music market also has clear whitespace in underbuilt regions where audience demand is outpacing venue capacity and formal event infrastructure.

Live Music Industry Leaders

Live Nation Entertainment

Ticketmaster

CTS Eventim

AEG Presents

SeatGeek

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Spotify launched its Reserved feature in the United States for eligible Spotify Premium subscribers, in partnership with Live Nation and powered by Ticketmaster. The feature reserves up to 2 concert tickets per tour for an artist's most dedicated fans ahead of the general sale, creating a loyalty-linked distribution channel that extends streaming's monetization reach directly into live event revenue.

- May 2026: CTS Eventim AG and Co. KGaA reported Q1 2026 consolidated revenue of EUR 613.5 million (approximately USD 675 million), a 23% increase over the prior-year period. The Live Entertainment segment grew 38.3% to EUR 403.6 million (approximately USD 444 million), driven by strong US tour activity and high-demand events in Germany.

- March 2026: Live Nation completed acquisitions of Movistar Arena Santiago (Chile), Unipol Forum in Milan (Italy), and IMPACT Arena Bangkok (Thailand) as part of its Venue Nation expansion, adding approximately 4 million in annual fan capacity. Over half of the new capacity is located outside the United States, reflecting a deliberate strategic shift toward international venue ownership.

- February 2026: SeatGeek launched an integration with Spotify that brings its primary ticket inventory directly into Spotify's event discovery experience, extending SeatGeek's reach to 751 million monthly active users and enabling direct purchase pathways at the moment of musical discovery.

- September 2025: AEG Presents announced the launch of Roundhay Festival in Leeds, UK, for summer 2026, with Lewis Capaldi confirmed as the inaugural headliner. The festival, presented by American Express at the 700-acre Roundhay Park, extends AEG's European summer festival circuit alongside BST Hyde Park and All Points East.

Global Live Music Market Report Scope

The Global Live Music Market Report is Segmented by Application (Concerts, Festivals, and Corporate Events), Revenue Stream (Tickets, Sponsorship, and Merchandising), Age Group (Teenagers, Adults, and Seniors), Venue Size (Small, Medium, and Large), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The market forecasts are provided in terms of value, USD.

| Concerts |

| Festivals |

| Corporate Events |

| Tickets |

| Sponsorship |

| Merchandising |

| Teenagers |

| Adults |

| Seniors |

| Small |

| Medium |

| Large |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Application | Concerts | |

| Festivals | ||

| Corporate Events | ||

| By Revenue Stream | Tickets | |

| Sponsorship | ||

| Merchandising | ||

| By Age Group | Teenagers | |

| Adults | ||

| Seniors | ||

| By Venue Size | Small | |

| Medium | ||

| Large | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the global live music sector?

The live music market size stands at USD 54.5 billion in 2026 and is expected to reach USD 72.4 billion by 2031, growing at a 5.8% CAGR over 2026-2031.

Which application generates the most revenue in live music?

Concerts led with 60.62% of total revenue in 2025, supported by strong arena and stadium touring economics.

Which revenue stream is growing the fastest in this space?

Sponsorship is projected to grow the fastest at a 6.4% CAGR through 2031, helped by stronger brand activation and better use of first-party fan data.

Which region is expanding the fastest for live events?

Asia-Pacific is the fastest-growing region, with a projected 6.3% CAGR through 2031, supported by growth in Korea, India, and Japan.

Why are large operators gaining an advantage over smaller promoters?

Large operators can spread rising production costs across venues, sponsorship, ticketing, and data platforms, while smaller independents rely more heavily on gate revenue alone.

What is the main risk to growth over the next few years?

The biggest near-term risk is cost pressure from higher artist fees, venue costs, and production expenses, along with stronger consumer sensitivity to ticket pricing.

Page last updated on: