Cloud Music Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

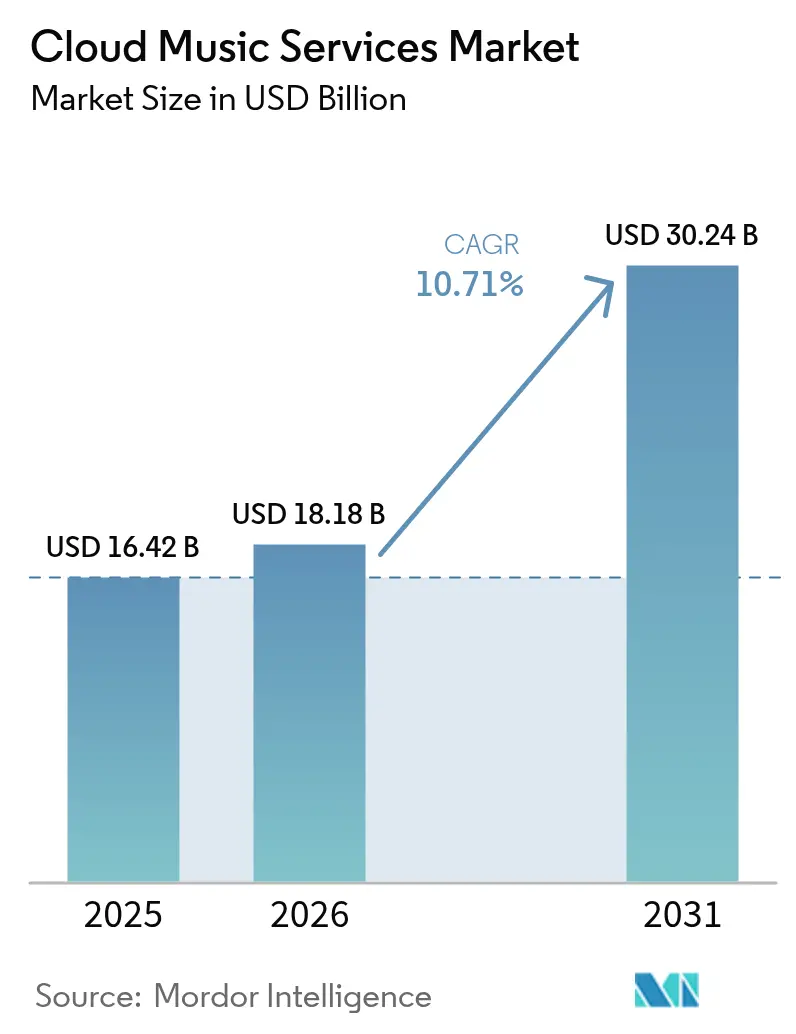

| Market Size (2026) | USD 18.18 Billion |

| Market Size (2031) | USD 30.24 Billion |

| Growth Rate (2026 - 2031) | 10.71% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Music Services Market Analysis by Mordor Intelligence

The cloud music services market size is expected to grow from USD 16.42 billion in 2025 to USD 18.18 billion in 2026 and is forecast to reach USD 30.24 billion by 2031 at 10.71% CAGR over 2026-2031. Continuous smartphone adoption, lower data tariffs, and artificial-intelligence personalization keep listening sessions longer, reduce churn, and draw new users into premium tiers. Superfan monetization and telco bundles are widening the revenue base beyond advertising and basic subscriptions, while live event streaming and podcast expansion diversify engagement touchpoints. In parallel, regulatory mandates in North America and Europe increase compliance costs that favor scale leaders; yet, the same rules also amplify catalog transparency, which benefits artists. Profitability remains squeezed because rights holders capture about 70% of platform revenue, forcing operators to pursue price increases, margin-rich premium tiers, and B2B licensing for commercial locations.

Key Report Takeaways

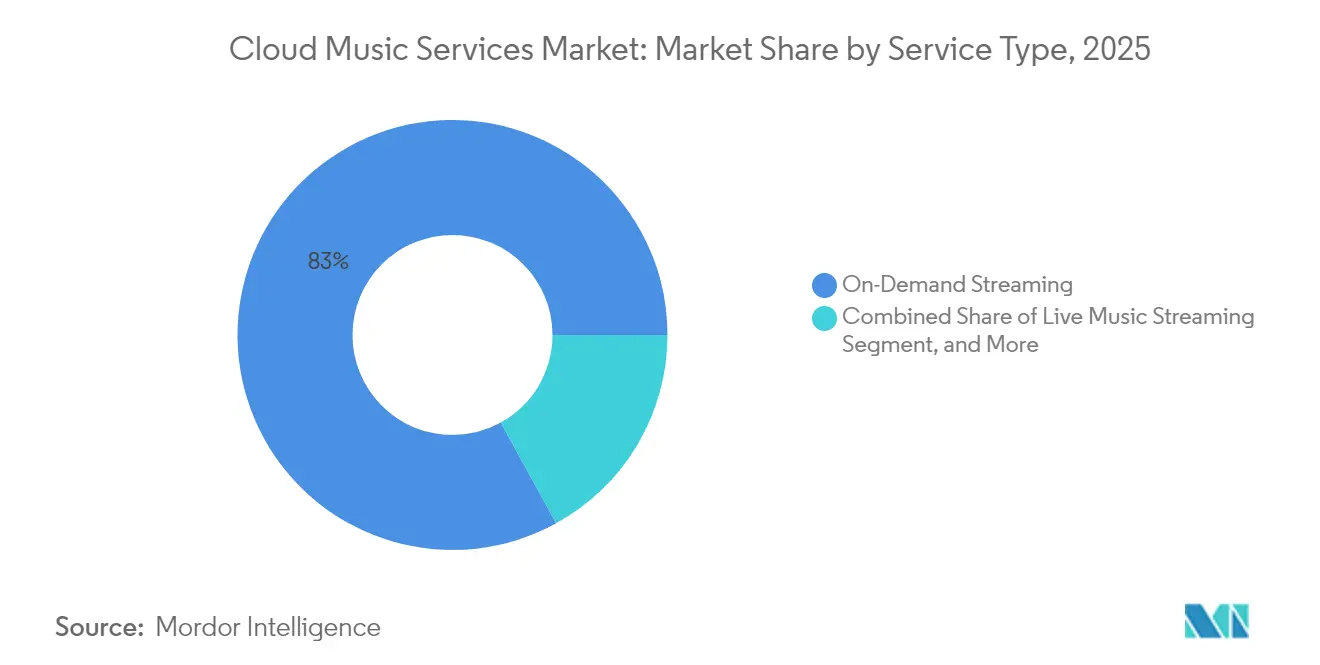

- By service type, on-demand streaming led with 83.01% revenue share in 2025, while live streaming is forecast to expand at a 12.96% CAGR through 2031.

- By revenue model, subscription tiers held 78.05% share in 2025, whereas freemium models are projected to grow at a 12.21% CAGR to 2031.

- By platform, smartphones accounted for 68.82% of 2025 revenue; however, automotive infotainment systems are projected to post the fastest growth rate of 14.62% CAGR through 2031.

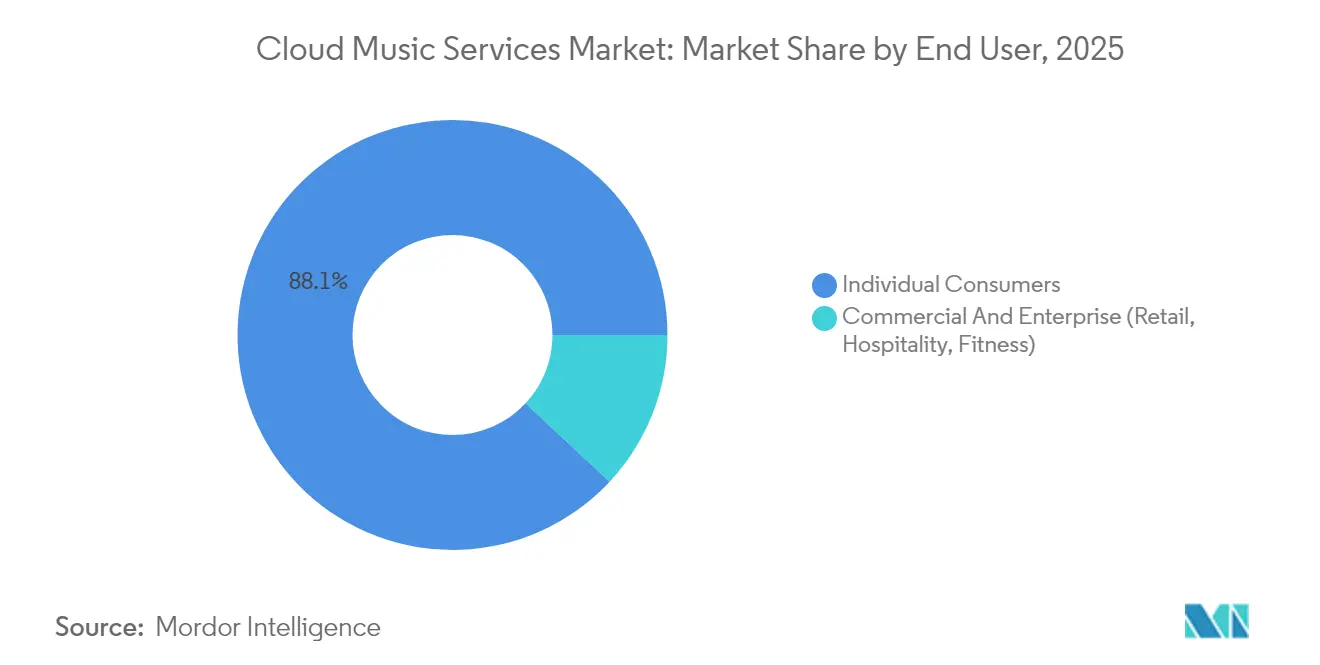

- By end user, individual accounts captured an 88.05% share in 2025, while commercial premises are expected to advance at an 11.54% CAGR.

- By content type, audio-only music accounted for a 61.75% share in 2025, and podcasts are projected to grow at a 16.78% CAGR through 2031.

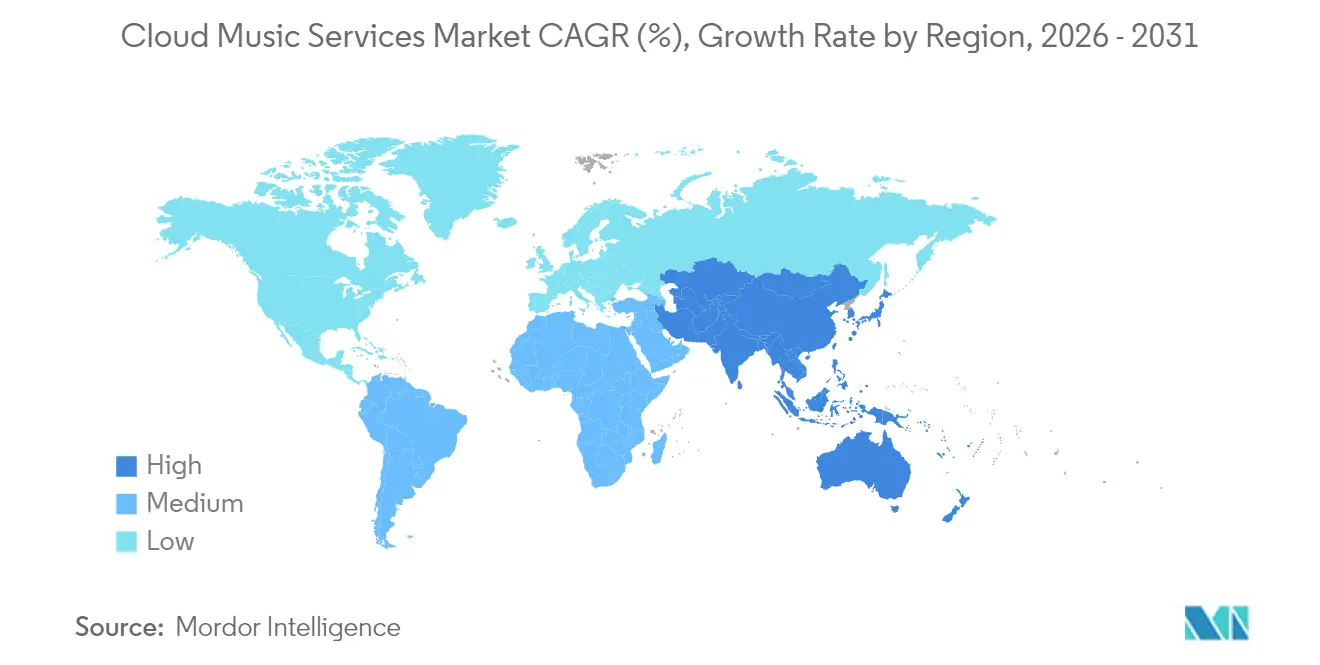

- By geography, North America held a 41.92% share in 2025, and the Asia Pacific is anticipated to grow at an 11.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Music Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising smartphone penetration and affordable data | +2.8% | Asia Pacific, Middle East and Africa, Latin America | Medium term (2-4 years) |

| Paid streaming price increases are boosting ARPU | +1.9% | North America and Europe | Short term (≤ 2 years) |

| Emergence of superfan monetization tiers | +1.5% | North America and Europe | Medium term (2-4 years) |

| AI-driven personalization enhances engagement | +2.2% | Global with early lead in North America, Europe, Asia Pacific | Long term (≥ 4 years) |

| Cloud-native creator tools expanding supply | +1.4% | Global | Long term (≥ 4 years) |

| Regional telco-bundle partnerships | +2.1% | Asia Pacific, Latin America, the Middle East, and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Smartphone Penetration and Affordable Data

India added approximately 50 million smartphone users in 2024, and sub-Saharan Africa recorded double-digit growth in mobile broadband lines. Meanwhile, data tariffs fell by 15% to 20% in India, Indonesia, and Nigeria.[1]Goldman Sachs Research, “Music in the Air Stairway to the Metaverse,” goldmansachs.com Ubiquitous connectivity has shifted millions from radio or sideloaded files to cloud catalogs, accelerating the adoption of the cloud music services market. Telcos, from Reliance Jio to Claro, embed streaming into prepaid bundles and reduce acquisition costs for platforms. Lower data pricing creates a virtuous circle where streaming usage justifies further network upgrades, which in turn support richer audio and video formats. Platforms that secure carrier partnerships win shelf space on devices, simplify billing, and unlock the next billion listeners.

Paid Streaming Price Increases Boosting ARPU

Spotify increased its US individual plan from USD 9.99 to USD 10.99 in 2024, and Apple Music followed a similar move across Europe.[2]Reuters Staff, “Spotify Raises Prices Again as Streaming Wars Intensify,” reuters.com A one-dollar rise across Spotify’s 226 million premium base equates to roughly USD 2.7 billion in extra annual revenue. Early churn only ticked up one to two points because playlists, social features, and device integration create switching costs. Nonetheless, consumer surveys flag resistance at monthly prices above USD 15, so platforms are layering premium “superfan” tiers rather than pushing the headline rate too quickly. The price-led ARPU lift shores margins in the cloud music services market, even as royalty costs climb.

Emergence of Superfan Monetization Tiers

Universal Music Group sized the superfan opportunity at USD 4.5 billion, covering early ticket access, merchandise drops, and virtual meet-and-greets.[3]Financial Times Reporters, “Superfan Economy How Music Platforms Are Monetizing Engagement,” ft.com Spotify introduced Supremium in 2024, priced roughly 40% above standard plans, and Apple Music Artist Edition followed in 2025 at USD 16.99. Data shows that the most engaged 10% of users can drive up to 40% of total artist revenue when merch and events are bundled. Premium tiers expand margin without alienating price-sensitive listeners who stay on free or basic plans. Careful tier design is vital, since too many options can confuse customers and erode brand clarity in the cloud music services market.

AI-Driven Personalization Enhancing Engagement

Spotify’s AI DJ, launched globally in 2024, narrates track transitions and adapts in real time to user feedback. Deezer’s text-to-playlist tool lets subscribers request mood-based mixes via natural language. A Journal of Marketing Research study found that personalized recommendations increase engagement by 25% to 30% compared to generic playlists.[4]AMA Journal Editors, “The Impact of Personalized Recommendations on User Engagement in Music Streaming,” journals.ama.org Longer sessions increase ad inventory for freemium users and reinforce retention for paying members, directly supporting revenue growth in the cloud music services market. Yet algorithmic echo chambers can narrow discovery, so platforms now balance machine suggestions with editorial curation to widen genre exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Royalty cost pressure on profitability | -1.8% | Global with higher weight in mature markets | Short term (≤ 2 years) |

| Intense competition and subscription churn | -1.3% | North America and Europe | Medium term (2-4 years) |

| Piracy and stream-ripping services | -0.9% | Emerging markets | Long term (≥ 4 years) |

| Streaming fraud and fake-stream manipulation | -0.7% | Markets with weak enforcement | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Royalty Cost Pressure on Platform Profitability

Music licenses absorb 65% to 75% of streaming revenue. Spotify’s 2024 filings showed royalties accounting for nearly 70% of revenue, resulting in single-digit operating margins. Mid-tier players such as Deezer remain loss-making despite surpassing 10 million subscribers. Since labels can withdraw catalogs, platforms have little leverage to lower rates, pushing them to diversify into owned podcasts or direct artist deals. High payout ratios limit capital for product innovation and slow profitability improvement in the cloud music services market.

Intense Competition and Subscription Churn

Monthly churn rates typically range from 3% to 5%, necessitating ongoing user acquisition to maintain momentum. Apple, Amazon, and Google can subsidize music through hardware or commerce profits, putting volume pressure on independent platforms. Amazon bundles Music Unlimited into Prime, and Google pairs YouTube Music with ad-free video, eroding the differentiation between the two services. Without cross-subsidy economics, challengers focus on niche content or a regional scale; yet, even those gains are vulnerable to larger rivals entering with aggressive pricing. Sustained head-to-head rivalry caps pricing power and compresses margins across the cloud music services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type - Live Streaming Bridges Digital and Physical Experiences

On-demand streaming accounted for 83.01% of revenue in 2025, underscoring its dominance in the cloud music services market. Live music streaming is forecast to grow at a 12.96% CAGR as concert broadcasts, backstage Q&As, and virtual festivals become staples on major platforms. Amazon Music Live taps prime-time audiences during Thursday Night Football, while Apple Music streams intimate shows that spark social buzz.

Live content introduces scarcity and appointment viewing, deepening fan loyalty and driving incremental monetization such as virtual tickets. Locker-style cloud storage remains relevant in bandwidth-constrained areas and among audiophiles storing lossless files, but falling storage costs and the advent of 5G are reducing its mass appeal. The segment mix reflects a broader shift in the cloud music services market, where experiential features complement catalog access to sustain engagement and raise switching costs.

By Revenue Model - Freemium Funnels Drive Conversion at Scale

Subscription plans accounted for 78.05% of 2025 revenue, solidifying their role as the economic engine of the cloud music services market. Freemium tiers are projected to expand at a rate of 12.21% as platforms fine-tune ad loads, skip limits, and trial offers to transition free listeners into paid tiers. Spotify’s free base of 348 million monthly users feeds a steady upgrade pipeline.

Ad-supported users deliver USD 5 to USD 7 per year, compared with about USD 120 for premium subscribers, yet they lower acquisition costs and widen global reach. Conversion efficiency relies on predictive analytics that identify high-propensity cohorts for discounted trials. Pure ad-only models struggle as on-demand access becomes a table-stakes requirement. Blended revenue streams, therefore, remain central to sustaining growth in the cloud music services market.

By Platform - Automotive Integration Redefines In-Car Listening

Smartphones contributed 68.82% of 2025 revenue thanks to ubiquitous ownership and seamless device handoff. Automotive infotainment systems are poised for a 14.62% CAGR as General Motors phases out CarPlay in favor of embedded Android Automotive, featuring native Spotify and YouTube Music clients.

In-car streaming gives automakers revenue participation and data control, but fragmentation complicates developer support. Smart speakers and wearables are expanding listening contexts in homes and gyms, while PCs are declining as mobile sessions become increasingly dominant. Platform diversification enhances stickiness for the cloud music services market, as users value uninterrupted access across all screens and scenarios.

By End User - Commercial Premises Unlock B2B Revenue Streams

Individual accounts captured 88.05% of 2025 revenue; however, commercial locations, such as retail stores, hotels, and gyms, are forecast to expand at a 11.54% CAGR. Soundtrack Your Brand’s deal with Accor covers 5,700 hotels, replacing static playlists with dynamic mood-based curation.

Commercial subscriptions cost USD 30 to USD 50 per location per month, reflecting legal certainty and business-grade features. Higher unit pricing and low churn give platforms diversification beyond consumer cycles, supporting overall revenue resilience in the cloud music services industry.

By Content Type - Podcasts and Video Broaden Engagement Horizons

Audio-only music retained a 61.75% share in 2025; however, podcasts are projected to rise by 16.78% annually, leading to longer listening sessions and lower content costs. Spotify reported a 39% jump in video podcast hours in 2024, challenging YouTube’s dominance in long-form audio-visual content.

Podcasts carry direct or owned rights, easing royalty burden and attracting advertisers targeting niche audiences. Video layers visual storytelling and incremental ad slots. The growing mix of spoken word and video enriches the cloud music services market, moving platforms beyond pure music toward holistic audio entertainment hubs.

Geography Analysis

North America controlled 41.92% of 2025 revenue, reflecting high ARPU and near-saturation subscription levels in the cloud music services market. Growth now hinges on selective price increases, account sharing crackdowns, and the uptake of superfan tiers. The region also serves as a test bed for new features, including AI DJs and high-resolution audio, before they are rolled out globally. State privacy laws and pending federal algorithm transparency proposals increase compliance costs that smaller challengers struggle to absorb, thereby reinforcing the incumbent's advantage.

Asia Pacific is projected to grow at 11.52% through 2031, driven by subscriber gains in China, India, and Southeast Asia. Tencent Music reached 119.8 million paying users in Q3 2024 and generated revenue of CNY 7.02 billion (USD 0.99 billion). NetEase Cloud Music achieved 49 million payers and CNY 2.5 billion (USD 0.35 billion) revenue in the same period. Local ecosystem integration and telco bundles underpin rapid expansion. In India, JioSaavn leverages Reliance Jio distribution to exceed 100 million users, demonstrating the power of bundled data plans.

Europe, South America, the Middle East, and Africa collectively account for approximately 45.98% of global revenue. Europe exhibits high penetration, but faces heavier regulation under the Digital Services Act and Copyright Directive, resulting in increased operating overheads. South America benefits from falling handset costs yet faces currency volatility that complicates pricing. The Middle East and Africa showcase regional platforms like Anghami and Boomplay, which thrive through localized catalogs and handset pre-installation. Diverse regional dynamics make localization and flexible payment options decisive for success in the cloud music services market.

Competitive Landscape

The top five platforms, Spotify, Apple Music, Amazon Music, YouTube Music, and Tencent Music, account for a significant share of global subscriptions, resulting in a moderately concentrated profile for the cloud music services market. Each leader leverages ecosystem advantages: Apple bundles services with hardware, Amazon ties music to Prime and Alexa, YouTube wields video discovery, and Tencent integrates social features. Exclusive podcasts, live-stream deals, and merchandise shops enhance differentiation and raise the barriers to switching.

White-space opportunities lie in B2B music for commercial venues, superfan monetization, and emerging markets where payment infrastructure remains underdeveloped. Soundtrack Your Brand, Anghami, and Boomplay illustrate the value of region-specific content and telco distribution. Generative AI radio and blockchain royalty platforms represent nascent threats but face scalability and compliance challenges.

Sustaining edge demands continual investment in personalization, creator tools, and adjacent content formats such as video podcasts and live events. Margins will favor platforms that balance scale with diversified revenue streams, as royalty payments remain indexed to usage and limit operating leverage in the cloud music services industry.

Cloud Music Services Industry Leaders

Spotify AB

Apple Inc.

Amazon.com Inc.

Google Llc

Youtube Llc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Spotify launched global AI playlist generation that creates mixes from natural-language prompts.

- September 2025: Tencent Music announced 128.5 million payers and CNY 7.8 billion (USD 1.1 billion) revenue for Q3 2025.

- August 2025: Amazon Music partnered with Ford to embed Amazon Music Unlimited in SYNC 4 vehicles for a six-month trial.

- July 2024: Apple Music introduced the Artist Edition superfan tier at USD 16.99 per month.

Global Cloud Music Services Market Report Scope

The Cloud Music Services Market Report is Segmented by Service Type (On-Demand Streaming, Cloud Music Storage and Locker, Live Music Streaming), Revenue Model (Subscription, Ad-Supported, Hybrid or Freemium), Platform (Smartphones, Smart Speakers and Wearables, PCs and Laptops, Automotive Infotainment), End User (Individual Consumers, Commercial and Enterprise), Content Type (Audio-Only Music, Podcasts and Audio Shows, Video Music Content), and Geography (North America, South America, Europe, Asia Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Demand Streaming |

| Cloud Music Storage And Locker |

| Live Music Streaming |

| Subscription |

| Ad-Supported |

| Hybrid / Freemium |

| Smartphones |

| Smart Speakers And Wearables |

| Pcs And Laptops |

| Automotive Infotainment |

| Individual Consumers |

| Commercial And Enterprise (Retail, Hospitality, Fitness) |

| Audio-Only Music |

| Podcasts And Audio Shows |

| Video Music Content |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By Service Type | On-Demand Streaming | |

| Cloud Music Storage And Locker | ||

| Live Music Streaming | ||

| By Revenue Model | Subscription | |

| Ad-Supported | ||

| Hybrid / Freemium | ||

| By Platform | Smartphones | |

| Smart Speakers And Wearables | ||

| Pcs And Laptops | ||

| Automotive Infotainment | ||

| By End User | Individual Consumers | |

| Commercial And Enterprise (Retail, Hospitality, Fitness) | ||

| By Content Type | Audio-Only Music | |

| Podcasts And Audio Shows | ||

| Video Music Content | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the projected revenue value of cloud music services in 2031?

The sector is forecast to reach USD 30.24 billion by 2031, growing at a 10.71% CAGR.

Which region is expected to grow the fastest through 2031?

Asia Pacific is anticipated to post an 11.52% CAGR as China, India, and Southeast Asia add millions of paying users.

Why are superfan tiers crucial for future monetization?

They capture a higher willingness to pay from the most engaged 10% of listeners, expanding the margin without raising basic plan prices.

How do royalty costs impact platform profitability?

Royalties consume 65% to 75% of revenue, leaving single-digit operating margins and driving the need for price hikes and new revenue streams.

What role will automotive integration play in driving user growth?

Embedded infotainment apps are expected to grow at a 14.62% CAGR, giving platforms a direct channel to drivers and reducing reliance on smartphones.

Page last updated on: