Music App Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.28 Billion |

| Market Size (2031) | USD 37.62 Billion |

| Growth Rate (2026 - 2031) | 4.44% CAGR |

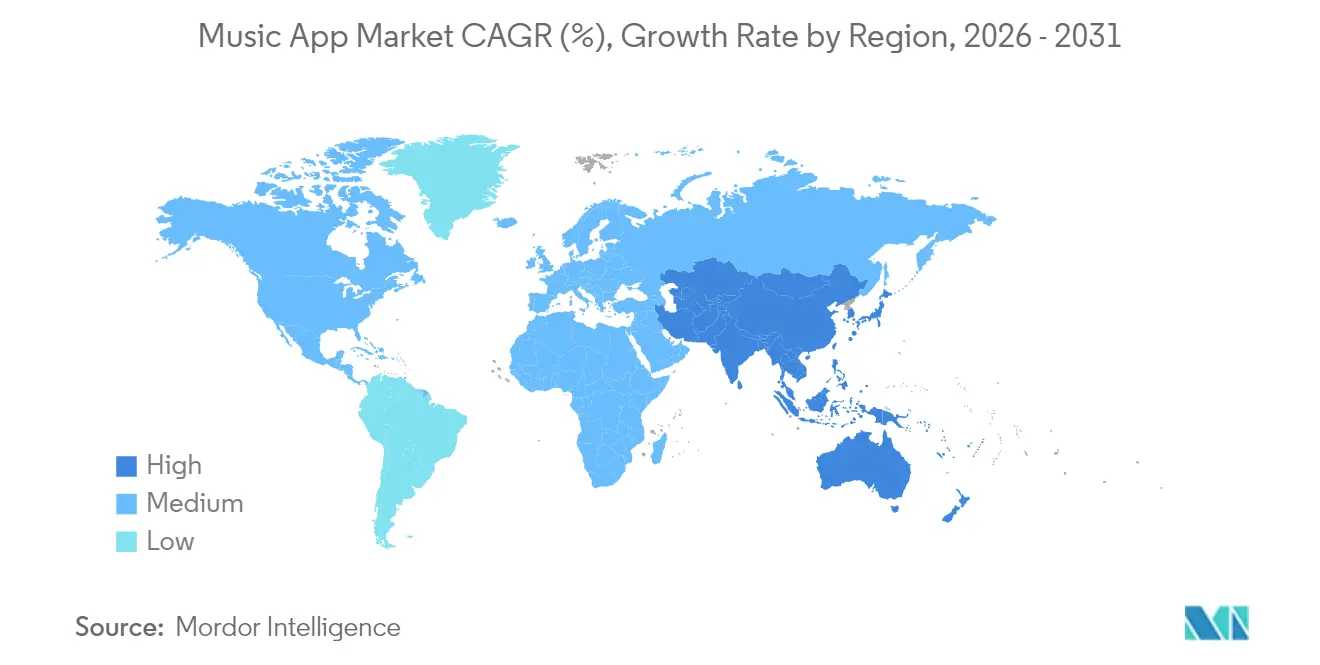

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Music App Market Analysis by Mordor Intelligence

The music app market size in 2026 is estimated at USD 30.28 billion, growing from 2025 value of USD 28.99 billion with 2031 projections showing USD 37.62 billion, growing at 4.44% CAGR over 2026-2031. This expansion reflects a maturing yet opportunity-rich landscape in which subscription models still dominate but are increasingly reinforced by hybrid freemium tiers, bundled offerings, and connected-device channels that lengthen engagement cycles. Growing smartphone penetration, affordable mobile data, and AI-powered recommendation engines continue to widen the addressable base, while rising carrier-billing adoption in emerging regions removes historical payment frictions. In parallel, partnerships with automotive OEMs and smart-home brands are extending listening beyond phones, creating incremental touchpoints that strengthen platform stickiness. Competitive pressure remains intense as licensing costs climb and margin protection requires simultaneous investment in catalog depth, geotargeted content, and personalized user experiences, prompting platforms to diversify revenue and rationalize pricing strategies.

Key Report Takeaways

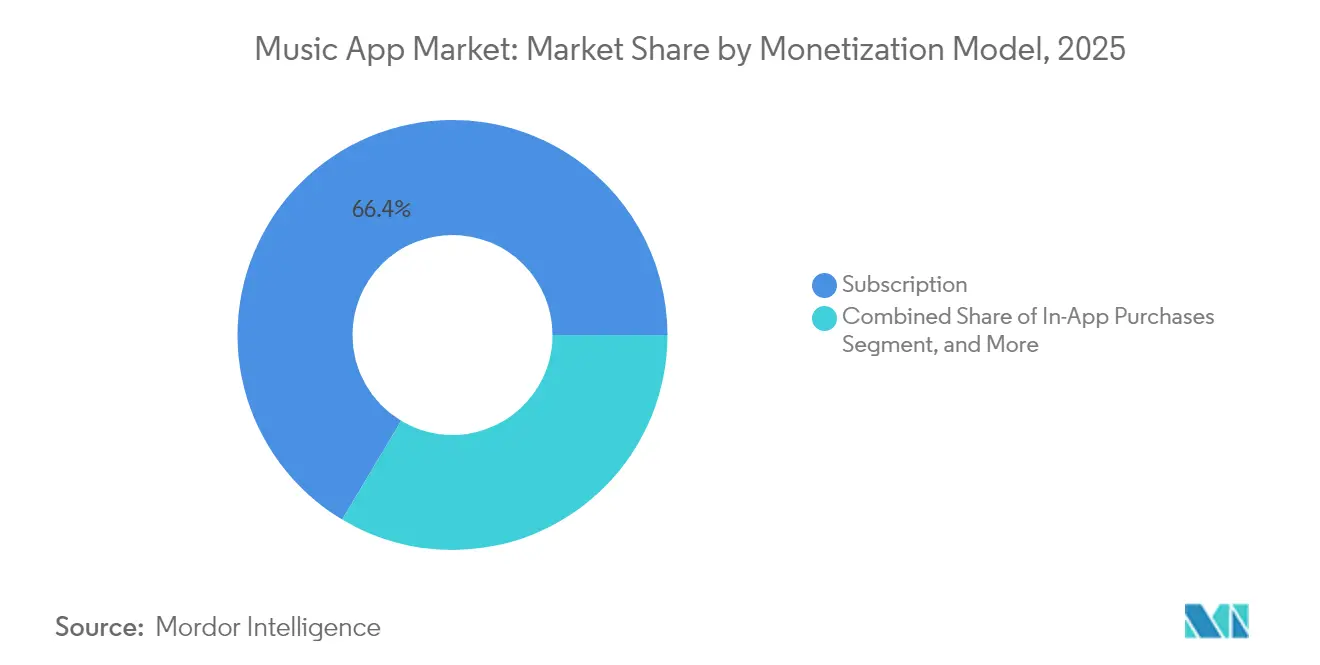

- By monetization model, subscription streaming held 66.42% of the music app market share in 2025, while hybrid freemium is forecast to accelerate at a 13.58% CAGR through 2031.

- By platform, Android accounted for 71.05% of the music app market size in 2025; smart speakers and connected devices are projected to grow at an 17.25% CAGR between 2026 and 2031.

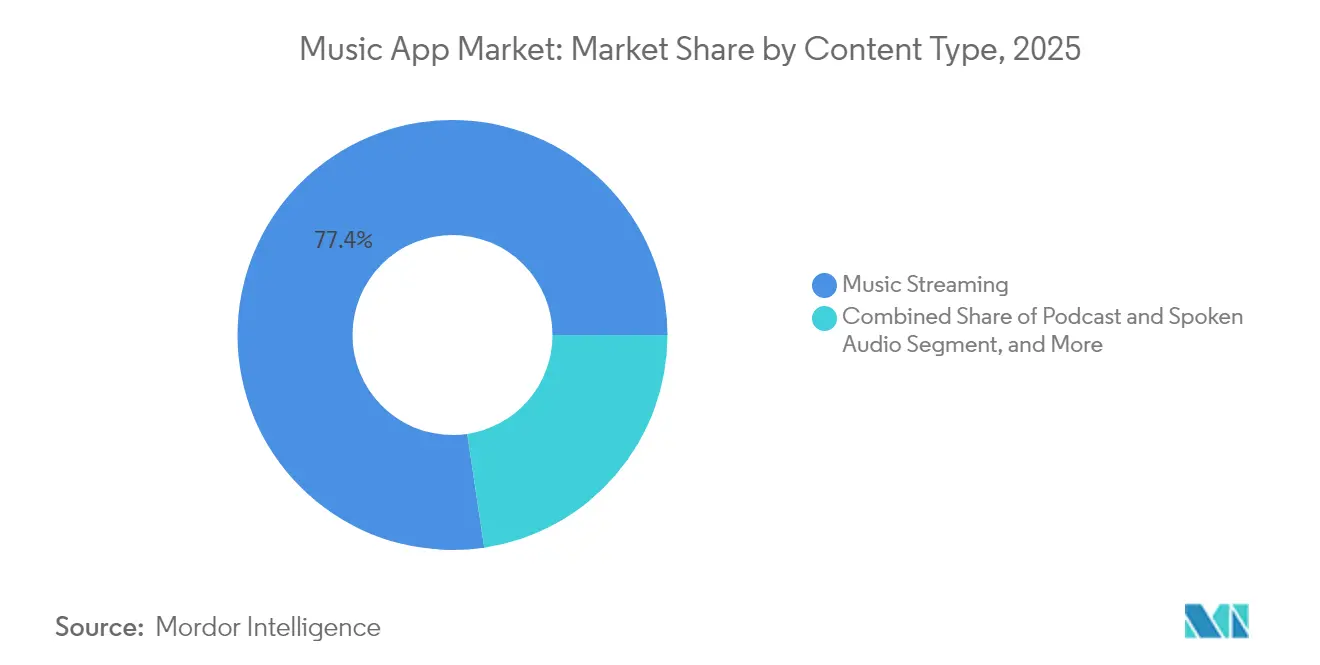

- By content type, podcast and spoken audio segments are advancing at a 20.85% CAGR through 2031, whereas music streaming retained 77.36% share of the music app market size in 2025.

- By age group, users aged 13-24 years captured 36.12% of the music app market share in 2025 and are expanding at a 10.53% CAGR to 2031.

- By geography, North America held a 46.58% share of the market in 2025, while Asia-Pacific is projected to grow with a 24.70% share.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Music App Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of paid music-streaming subscriptions | +1.8 | Global, strongest in Asia-Pacific and Latin America | Medium term (2–4 years) |

| Growing smartphone penetration and mobile-data affordability | +1.2 | India, Southeast Asia, Sub-Saharan Africa | Short term (≤ 2 years) |

| Integration with smart speakers and connected cars | +0.9 | North America and Europe first, Asia-Pacific next | Long term (≥ 4 years) |

| Expansion of global licensing agreements and catalog depth | +0.7 | Global | Medium term (2–4 years) |

| AI-driven hyper-personalization boosting retention | +0.5 | Mature markets then emerging | Short term (≤ 2 years) |

| Carrier-billing uptake in emerging regions | +0.4 | Asia-Pacific, Latin America, Middle East and Africa | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Paid Music-Streaming Subscriptions

Subscription conversion momentum continues to climb as platforms refine value propositions through exclusive content bundles and dynamic pricing. Universal Music Group reported EUR 1.61 billion (USD 1.77 billion) in subscription and streaming revenue for Q1 2025, up 7.2% year over year, reflecting robust paid-user growth. Tencent Music Entertainment added 13.4% more paying users in China, reaching 121 million and lifting monthly ARPPU to RMB 11.1 (USD 1.6), underscoring price elasticity even in cost-sensitive markets. Platforms also leverage diversified content—podcasts, audiobooks, and artist exclusives to reinforce perceived value and justify incremental price steps.

Growing Smartphone Penetration and Mobile-Data Affordability

Low-cost Android devices and competitive data plans have unlocked vast rural and youth cohorts. In India, streaming constituted 88% of recorded-music revenue in 2024, with listeners averaging 26.7 hours per week 30% above the global mean. Carrier-billing rails such as Airtel Mobile Money now plug more than 31.5 million Kenyans directly into app stores, removing credit-card dependence and expanding the music app market.

Integration with Smart Speakers and Connected Cars

Voice-enabled speakers and native in-car apps are redefining distribution. Mercedes-Benz’s FYI RAiDiO, built with Google Cloud and Azure OpenAI, personalizes audio for eligible 2024+ models, demonstrating OEM appetite for embedded services. TuneIn’s alliance with Visteon embeds 100,000 radio stations and millions of podcasts in dashboards aimed first at India and Asia-Pacific buyers. These integrations lengthen daily listening windows, boosting retention metrics and ARPU.

Expansion of Global Licensing Agreements and Catalog Depth

Cross-border licensing expands discovery and raises switching costs. Universal Music Group’s multiyear pact with Amazon Music covers exclusive releases and “Streaming 2.0” features, signaling the strategic weight of differentiated catalogs. IFPI data show that one-third of artists earning over USD 1,000 receive more than 75% of their income from outside their home market, highlighting the commercial upside of global availability.[3]International Federation of the Phonographic Industry, “Industry Data,” ifpi.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating content-licensing costs compressing margins | -1.1 | Global, greatest in mature markets | Short term (≤ 2 years) |

| High churn amid intense platform competition | -0.8 | Mature markets then emerging | Medium term (2–4 years) |

| Regulatory scrutiny on royalties and antitrust issues | -0.4 | North America and Europe | Long term (≥ 4 years) |

| Sustainability concerns over streaming energy use | -0.2 | Europe and North America first | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Content-Licensing Costs Compressing Margins

Mechanical royalty rates effective January 2025 rose to 12.7 cents per song plus 2.45 cents per minute, lifting cost bases for every major platform. [2]Royalty Exchange, “Music Royalties Tax Changes 2025,” royaltyexchange.comSpotify’s rule that tracks must hit 1,000 streams within 12 months before earning royalties reflects attempts to triage payouts and protect gross margin. High fees hit hardest in low-ARPU emerging markets, challenging scalability and potentially driving price tier differentiation.

High Churn Amid Intense Platform Competition

Average subscription life cycles hover around seven months as promotions reset user expectations and feature parity narrows. Rapid imitation, illustrated by NetEase Cloud Music and QQ Music’s public clash over player customization, erodes novelty advantages and fuels user switching. Bundling strategies that cut per-seat revenue yet raise retention complexity further pressure profitability benchmarks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Model: Subscription Dominance Drives Premium Shift

Subscription services commandeered 66.42% music app market share in 2025, translating into predictable recurring revenue that underpins most platform valuations. Hybrid freemium tiers, however, are projected to grow 13.58% annually as platforms accommodate variable purchasing power. Spotify’s USD 11.99 Premium and lower-priced Basic options illustrate layered monetization that widens the funnel while preserving yield. Tencent Music Entertainment diversified revenue to RMB 21.74 billion (USD 3.04 billion) in 2024, combining subscriptions, virtual albums, and live events. Carrier billing proliferation is expected to add tens of millions of first-time payers, broadening the music app market size for lower-priced introductory plans. Advertising-supported models remain essential in markets where average disposable income constrains subscription uptake, but rising ad loads risk dampening user satisfaction and could speed the pivot to micro-payment or creator-tip mechanisms.

The music app market is evolving toward blended income streams that fuse subscriptions, micro-transactions, and contextual advertising. As catalog costs climb, platforms favor higher-margin verticals such as podcast ads and live-event ticketing. Analysts expect subscription ARPU to stabilize as bundles replace single-format offerings, reducing churn and smoothing revenue for rights-holders. Competitive advantage will rest on data-driven segmentation that aligns tier pricing with regional income bands and content preferences, ensuring the music app market size expands without sacrificing profitability.

By Platform: Android Leadership Faces Smart Device Disruption

Android commanded 71.05% of global installations in 2025, anchored by its ubiquity in emerging economies. Despite this dominance, smart speakers and connected devices are surging at an 17.25% CAGR, signaling the next frontier for the music app market. Voice-first usage simplifies discovery, while in-car integration captures captive commuting time. iOS, although smaller in user count, delivers higher per-capita revenue, reinforced by Apple’s ecosystem stickiness. Desktop platforms play a complementary role for playlist management and creator tools, especially in professional and prosumer circles.

Connected cars are becoming significant demand drivers; KUKE Music now reaches 100 million Chinese in-vehicle users through partnerships covering 90% of local OEMs. BMW streams classical performances direct to dashboards, illustrating niche-content differentiation strategies. These developments suggest that future music app market share gains will hinge on seamless cross-device continuity rather than mobile-only dominance. Platforms investing early in automotive SDKs and smart-home APIs are poised to secure outsized influence as screenless listening accelerates.

By Content Type: Music Streaming Dominance Amid Podcast Acceleration

Music streaming still accounts for 77.36% of the music app market size in 2025, functioning as the gateway product for most users. Podcast and spoken-audio content, however, is expanding at a 20.85% CAGR as exclusive shows and serialized storytelling increase session length. Podcast advertising surpassed USD 2.4 billion in 2024, offering CPMs well above music equivalents and giving platforms a margin lever. Live audio, though nascent, enables artist-fan monetization pathways that bypass traditional label splits. High-resolution formats serve audiophile niches but act as premium-tier differentiators that justify price premiums and lock in high-value customers.

The diversification into spoken-word strengthens platform economics by optimizing ad inventory and boosting dwell time, sharpening retention cohorts. Exclusive shows from major studios and cross-sport collaborations exemplify content strategies aimed at capturing non-music listening moments, reinforcing the music app market growth narrative. Future expansion will likely mix short-form interactive audio and AI-generated soundscapes tailored to wellness, education, and productivity contexts.

By Age Group: Youth Demographics Drive Innovation Cycles

Users aged 13-24 years controlled 36.12% music app market share in 2025 and are growing at 10.53% annually, making them the primary engine of product innovation. Their appetite for social listening, short-form discovery, and creator interaction shapes platform roadmaps. The 25-34 cohort, though smaller, delivers the highest subscription conversion and premium-tier uptake. Older segments require frictionless interfaces and curated discovery rather than social-first engagement, prompting UI bifurcation strategies.

Integrations like TikTok-to-Spotify playlist saving exemplify how platforms harness youth-centric viral loops to acquire and retain users. Collaborative playlists, gaming tie-ins, and AR filters are becoming table stakes in courting Gen Z listeners. Balancing this youth focus with universal usability is pivotal as the music app market matures; family plans and cross-generational curation tools will help platforms extend lifetime value across age brackets.

Geography Analysis

North America retained 46.58% music app market share in 2025, driven by high-value subscribers willing to pay USD-level premiums for lossless audio and bundled services. Apple’s Services segment generated USD 26.3 billion in Q1 FY25, highlighting the region’s monetization depth. However, saturation is slowing net additions, shifting strategic emphasis to ARPU optimization via multi-format bundles and connected-device upsells. Regulatory headwinds around royalty transparency and antitrust scrutiny are intensifying, influencing content-licensing negotiations and platform fee structures.

Asia-Pacific delivered the fastest growth at 24.70% CAGR through 2031, propelled by India’s mobile-first adoption and China’s scale. Tencent Music Entertainment reported RMB 28.40 billion (USD 3.98 billion) in 2024 revenue, with premium service upselling offsetting a user-base contraction. India’s users average 26.7 hours of weekly listening, yet subscription penetration remains low, presenting a sizable conversion opportunity. Carrier billing and localized pricing models are essential for unlocking this latent demand.

Europe posted steady 8.05% growth in 2025 as supportive digital-single-market regulations and affluent audiences sustain healthy paid uptake. Latin America advanced 21.9%, with Mexico entering the global top-10 recorded-music markets, demonstrating Spanish-language catalog power. Middle East and North Africa grew 22.1%, with Anghami emphasizing Arabic content and culturally aligned UX. Sub-Saharan Africa’s 24.0% growth potential hinges on continued investment in network infrastructure and micro-payment solutions that align with lower income levels.

Competitive Landscape

The competitive arena exhibits moderate concentration. Spotify retained roughly 32% global share after adding 28 million subscribers in 2024. Apple Music, Amazon Music, and Tencent Music follow, collectively bringing the top four to approximately 70% of the paid universe. Competitive differentiation increasingly revolves around ecosystem breadth, AI-powered personalization, and exclusive content rather than core catalog, which is largely commoditized. Rapid feature replication shortens innovation cycles, as visible in Chinese platforms’ swift copying of social and UI enhancements.

White-space competition is heating up in the automotive and smart-home verticals. Mercedes-Benz’s FYI RAiDiO illustrates OEM efforts to internalize entertainment layers, potentially disintermediating smartphone-centric apps. Creator economy dynamics also add complexity: Spotify’s Partner Program allows video podcasters to earn ad revenue, while Tencent Music offers virtual concert tickets. These initiatives alter revenue splits and require delicate balancing between labels, creators, and platform margins.

Sustainability considerations, such as data-center energy intensity, are emerging as brand-equity factors, especially in Europe where consumers show growing eco-sensitivity. Platforms investing in green cloud architectures may gain reputational advantage as regulators examine streaming’s carbon footp

Music App Industry Leaders

Spotify AB

Apple Inc.

Amazon.com, Inc.

Alphabet Inc. (YouTube Music)

Tencent Music Entertainment Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TuneIn partnered with Visteon to embed 100,000 radio stations and millions of podcasts into the AllGo automotive platform, initially targeting India and Asia-Pacific vehicles .

- March 2025: KUKE Music and China Media Group IoV Digital Media launched “Master Symphony Theater” and “Classical Music Radio” for connected cockpits, reaching 100 million users across 90% of Chinese automakers

- March 2025: Mercedes-Benz debuted FYI RAiDiO, an AI-powered in-car audio app developed with will.i.am, Google Cloud, and Microsoft Azure, initially rolling out to 2024+ E-Class models in the United States.

- March 2025: Universal Music Group posted EUR 1.61 billion (USD 1.77 billion) in Q1 2025 subscription and streaming revenue, exceeding analyst forecasts.

Global Music App Market Report Scope

Applications in the music segment allow users to listen to various audio files and music. The most popular apps are music streaming services Spotify and Pandora. Their cutting-edge recommender systems let users identify new artists based on their current tastes and make creative music playlists. This category also includes apps that enable music creation, performance, and/or recording.

The Music App Market is segmented by Type (In-app Purchases, Advertisement), Platform (Android and iPhone), and Geography (North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| In-App Purchases |

| Subscriptions |

| Advertising-Supported |

| Hybrid and Other Models |

| Android |

| iOS |

| Web/Desktop |

| Smart Speakers and Connected Devices |

| Music Streaming |

| Podcast and Spoken Audio |

| Live Audio and Events |

| High-Resolution and Lossless Streaming |

| 13-24 Years |

| 25-34 Years |

| 35-44 Years |

| 45 Years and Above |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia Pacfic | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Monetization Model | In-App Purchases | ||

| Subscriptions | |||

| Advertising-Supported | |||

| Hybrid and Other Models | |||

| By Platform | Android | ||

| iOS | |||

| Web/Desktop | |||

| Smart Speakers and Connected Devices | |||

| By Content Type | Music Streaming | ||

| Podcast and Spoken Audio | |||

| Live Audio and Events | |||

| High-Resolution and Lossless Streaming | |||

| By Age Group | 13-24 Years | ||

| 25-34 Years | |||

| 35-44 Years | |||

| 45 Years and Above | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia Pacfic | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the music app market in 2026, and what growth is expected by 2031?

The music app market size is USD 30.28 billion in 2026 and is forecast to reach USD 37.62 billion by 2031, expanding at a 4.44% CAGR.

Which monetization model generates the most revenue for music apps today?

Subscription streaming remains dominant, holding 66.42% music app market share in 2025, with hybrid freemium tiers growing fastest at 13.58% CAGR through 2031.

Which region will contribute the most new users over the next five years?

Asia-Pacific is projected to grow at a 24.70% CAGR through 2031, accounting for the majority of new subscriber additions as smartphone adoption and carrier billing proliferate.

What technology trends are shaping future music app experiences?

AI-driven personalization, integrated smart-speaker and automotive apps, and expanded podcast catalogues are redefining how users discover and consume audio content.

How are rising royalty rates affecting platform strategies?

Higher U.S. mechanical royalties effective 2025 increase cost pressure, prompting platforms to refine pricing tiers and impose minimum-stream thresholds to protect margins.

Which age segment is growing fastest among music-app users?

The 13-24 age bracket is expanding at 10.53% CAGR, driving demand for social-centric features, collaborative playlists, and short-form discovery tools.

Page last updated on: