Audio Streaming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

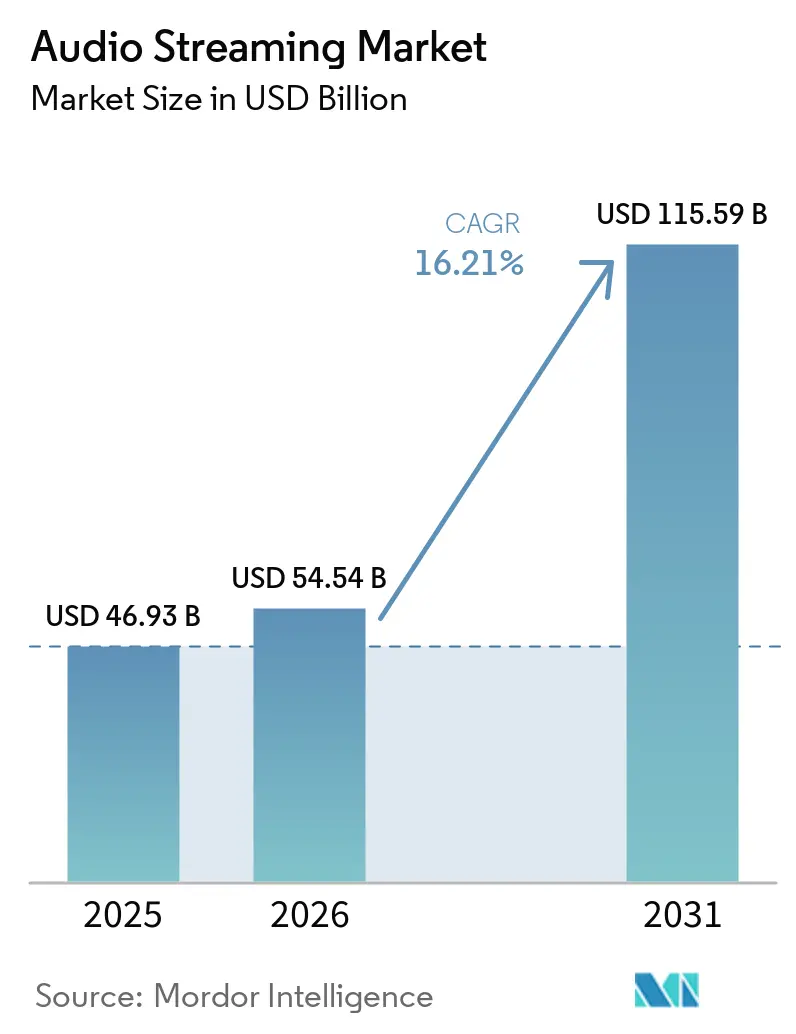

| Market Size (2026) | USD 54.54 Billion |

| Market Size (2031) | USD 115.59 Billion |

| Growth Rate (2026 - 2031) | 16.21% CAGR |

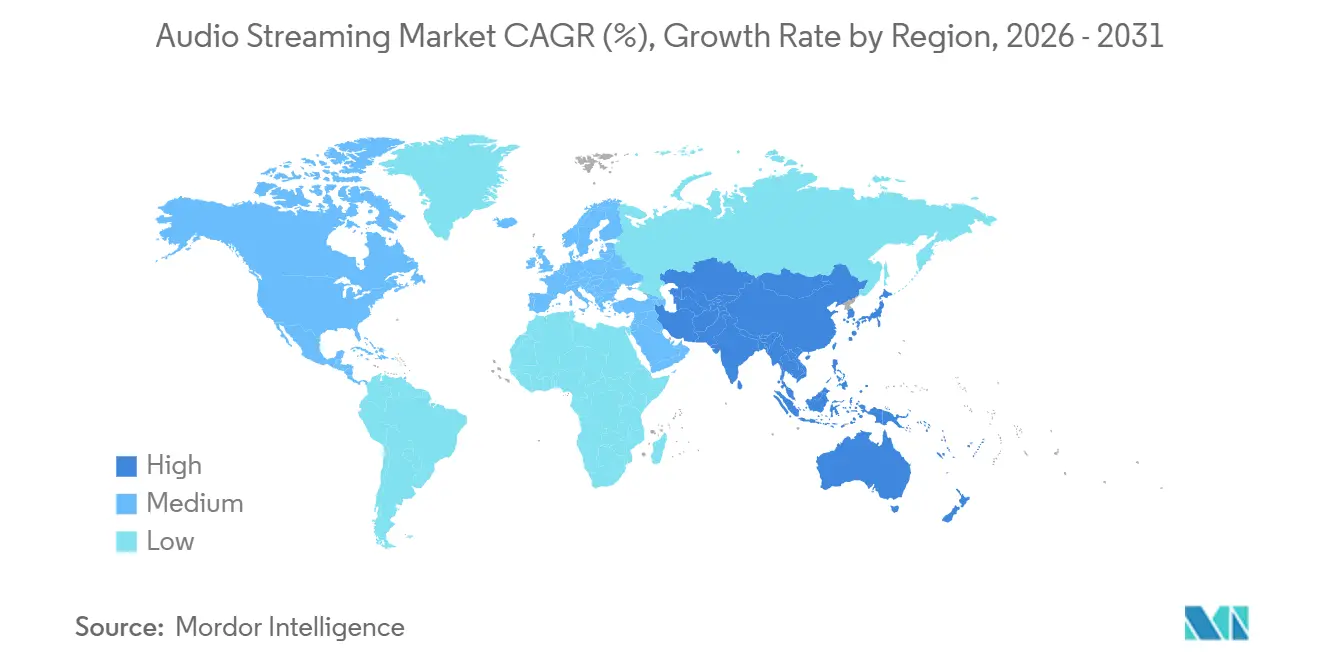

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Audio Streaming Market Analysis by Mordor Intelligence

The audio streaming market size is expected to grow from USD 46.93 billion in 2025 to USD 54.54 billion in 2026 and is forecast to reach USD 115.59 billion by 2031 at 16.21% CAGR over 2026-2031. The audio streaming market is being lifted by smartphone-led access, stronger personalization tools, and a larger push to monetize listening time that was historically underpriced in advertising. Paid demand is still proving resilient even after repeated price increases, which shows that high-engagement users continue to see subscription audio as a regular digital entertainment expense. The audio streaming market is also widening beyond the app economy as carmakers make native streaming part of the vehicle interface, which can tie platform usage to multi-year ownership cycles. At the same time, the audio streaming market is becoming more selective in how value is created, because higher royalty obligations are putting pressure on gross margins and rewarding platforms that balance scale, pricing, advertising yield, and rights costs more effectively. This leaves room for global leaders to consolidate premium demand while regional specialists continue to compete through local language content, distribution partnerships, and market-specific pricing.

Key Report Takeaways

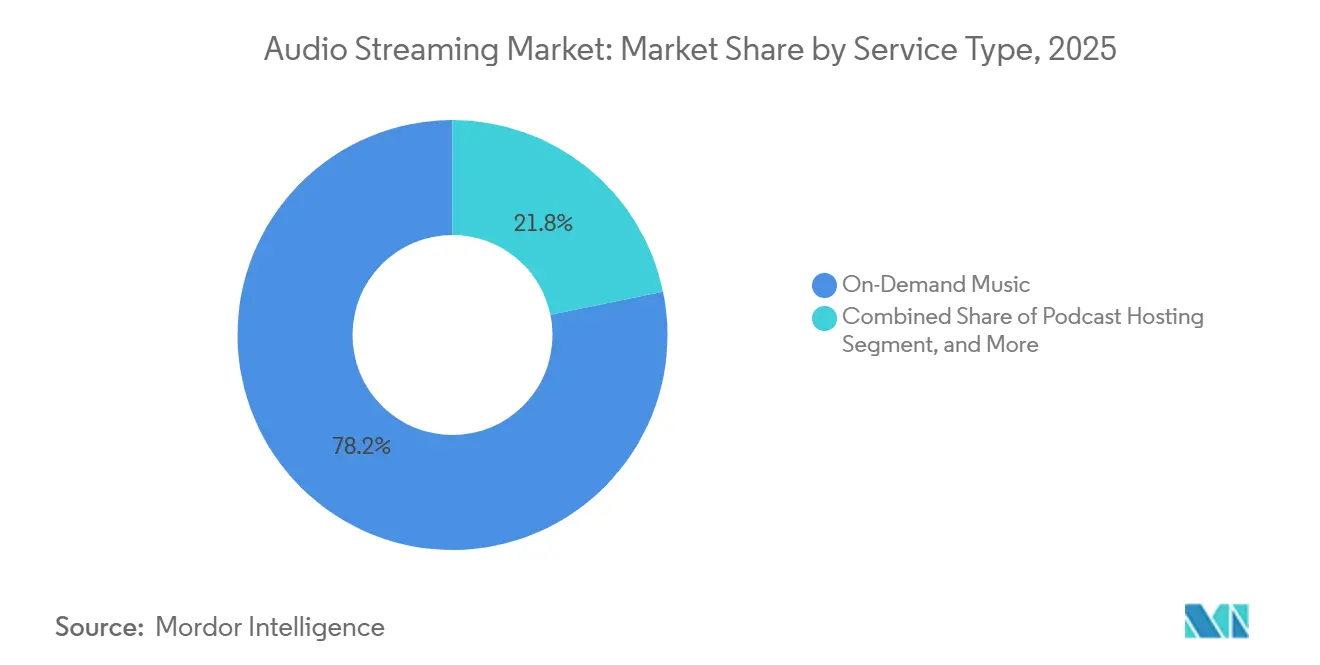

- By service type, on-demand music streaming led with 78.23% revenue share of the audio streaming market in 2025, while podcast hosting and distribution is forecast to expand at a 19.62% CAGR through 2031.

- By monetization, subscription-based monetization held 63.11% revenue share of the audio streaming market in 2025, while the advertising-supported model recorded the highest projected CAGR at 17.82% through 2031.

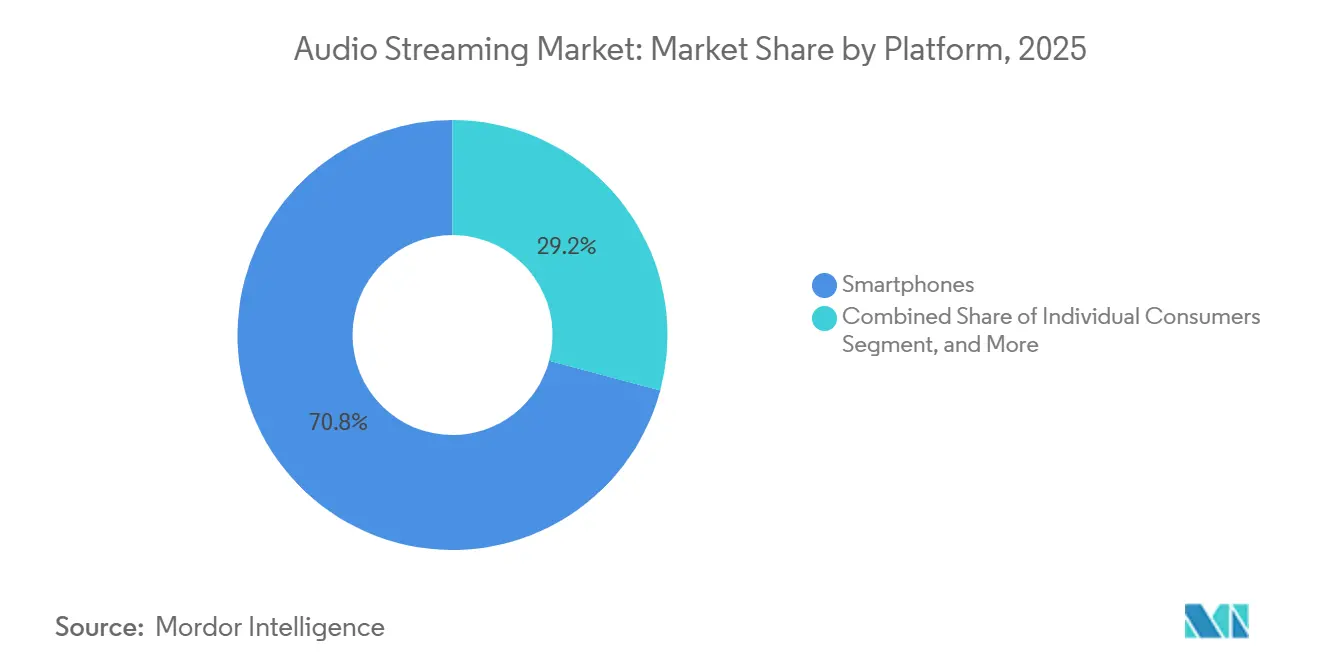

- By platform, smartphones and tablets accounted for 70.84% share of the audio streaming market in 2025, while connected cars are advancing at an 18.21% CAGR through 2031.

- By content type, music held a 60.22% share of the audio streaming market in 2025, while podcasts represent the fastest-growing format at a 20.43% CAGR through 2031.

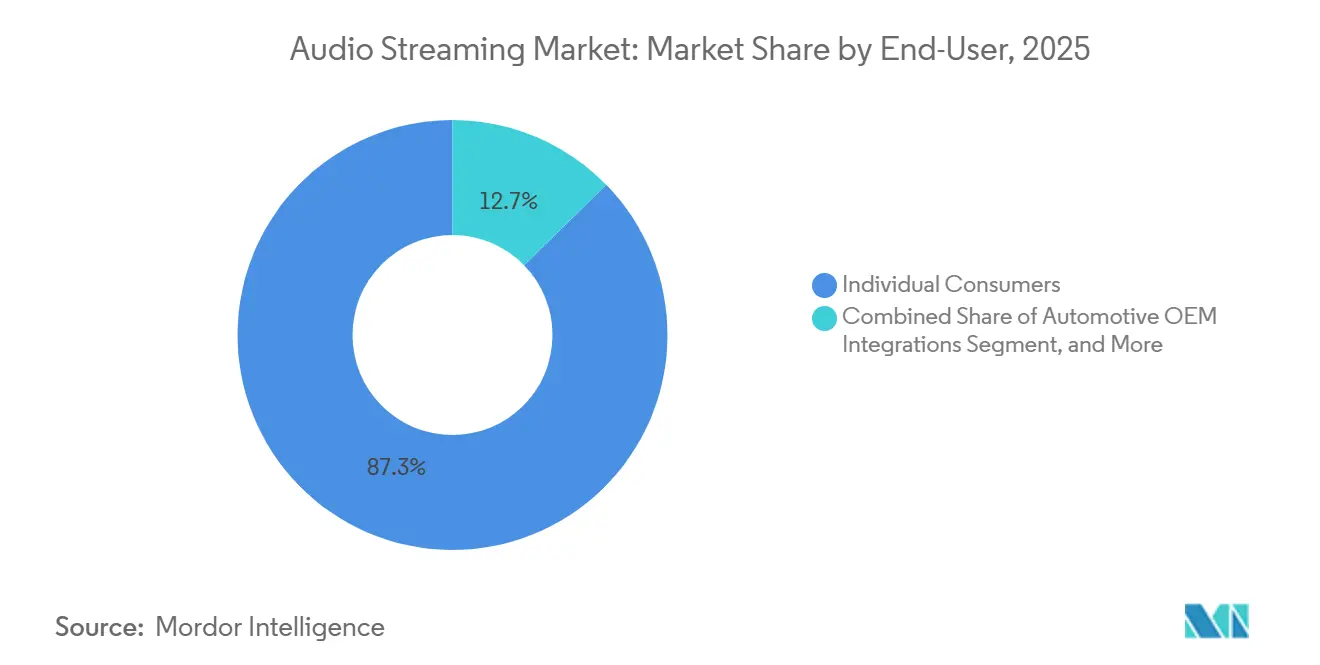

- By end-user, individual consumers commanded 87.31% share in 2025, while automotive OEM channels are projected to grow at a 17.24% CAGR through 2031.

- By geography, North America held 39.64% share of the audio streaming market in 2025, while Asia-Pacific recorded the highest projected CAGR at 17.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Audio Streaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subscription Price Rationalization In Emerging Economies | +3.5% | Asia-Pacific, Middle East and Africa, South America | Short term (≤ 2 years) |

| Telco-OTT Bundling Pushes Paid Uptake | +3.0% | Asia-Pacific core, spill-over to Middle East and Africa | Short term (≤ 2 years) |

| Rapid Smart Speaker Install Base Expansion | +2.0% | North America and Europe, to Asia-Pacific | Medium term (2-4 years) |

| OEM-Level In-Car Streaming Integrations | +1.5% | North America, Europe, China | Medium term (2-4 years) |

| AI Voice DJ And Generative Playlists Extend Daily Listening Time | +1.5% | Global, early gains in North America and Europe | Medium term (2-4 years) |

| Blockchain-Based Royalty Settlement Attracts Independent Catalogs | +0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Subscription Price Rationalization In Emerging Economies

Subscription price changes in lower-income markets are improving revenue mix without fully stopping user additions, which makes them more than a simple volume tactic in the audio streaming market. Spotify raised Premium pricing in India by 17-28% in August 2025, yet subscriber growth continued, which suggests that the most engaged listener groups were less price sensitive than many consumer models assumed. The same pattern matters even more in regions where streaming already dominates the listening economy. IFPI reported that recorded music revenue in the Middle East and North Africa grew 22.8% year over year in 2024, with streaming accounting for 99.5% of total revenue, which means pricing decisions directly shape category monetization in that region IFPI.ORG.[1]International Federation of the Phonographic Industry, “IFPI Global Music Report 2025,” IFPI, ifpi.orgIFPI also stated that Sub-Saharan Africa was the fastest-growing music market in 2025 and crossed USD 100 million in revenue for the first time, which supports the view that localized pricing is opening new revenue pools instead of just shifting existing spending. For the audio streaming market, this driver stays durable as long as platforms keep regional tiers aligned with mobile broadband expansion and keep cross-border arbitrage from weakening local price structures.

Telco-OTT Bundling Pushes Paid Uptake

Telco bundling is reducing the friction of subscription adoption by placing streaming inside monthly connectivity plans instead of treating it as a separate purchase in the audio streaming market. The Digital Media Association reported more than 500 OTT-operator partnerships across Asia-Pacific by the end of 2025, which shows that bundling had become a standard commercial route rather than a trial model.[2]Digital Media Association, “DIMA Annual Report 2025,” DIMA, dima.org Airtel added Apple Music to its postpaid and home Wi-Fi plans in February 2025, which extended the platform’s reach through an operator channel in one of the most price-sensitive large consumer bases. Anghami disclosed partnerships with 45 telecom operators across 16 Middle East and North Africa countries, showing that local specialists are also using bundling to defend their position against larger global services. This matters because bundled users usually face a more deliberate cancellation step than app-based sign-ups, and that tends to improve retention and lower voluntary churn over time in the audio streaming market.

Rapid Smart Speaker Install Base Expansion

Smart speakers are expanding listening into rooms and routines where screens compete poorly for attention, which gives the audio streaming market more ambient usage time. Amazon’s Alexa Plus launch introduced generative AI features and context memory, moving voice interaction from command-based requests toward more natural conversations. Amazon said users engaging with AI-assisted recommendations on Amazon Music explored 3 times more music and listened 70% more than users relying on standard interface interactions.[3]Amazon.com Inc., “Amazon Music Alexa Plus Features and Usage Data,” Amazon News, aboutamazon.com That deeper engagement can lift ad impressions at the free tier and can also create more frequent moments where users discover enough value to consider upgrading. For the audio streaming market, the next leg of this driver comes from adoption spreading beyond North America and Europe into younger urban households in Asia-Pacific, where home audio accessories are becoming a more regular part of connected living.

OEM-Level In-Car Streaming Integrations

Vehicle-level integrations are turning the dashboard into a durable access point for the audio streaming market and moving listener acquisition beyond app stores. Toyota launched the 2026 RAV4 with AT&T 5G connectivity and native Spotify integration, and Lexus followed in May 2026 with native Spotify in the 2026 ES, which shows that embedded streaming is moving across brand tiers rather than staying confined to pilot programs.[4]Lexus USA, “2026 ES with AT&T 5G and Native Spotify Integration,” Lexus Newsroom, newsroom.lexus.com Volvo also launched the EX60 in January 2026 with native Apple Music and Dolby Atmos through a 28-speaker Bowers and Wilkins audio system, tying premium audio quality more directly to the vehicle purchase decision. General Motors completed native Apple Music deployment across 1.2 million Cadillac, Chevrolet, Buick, and GMC vehicles by March 2026, which confirmed that in-car streaming had reached production scale. Because these integrations can stay active across ownership cycles of 5-10 years, they may create a form of platform familiarity and habit that is more durable than short-cycle consumer marketing in the audio streaming market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Royalty-Rate Inflation Exceeding ARPU Growth | -1.5% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Content-License Windowing By Major Labels | -0.8% | Global, particularly North America and Europe | Medium term (2-4 years) |

| Data-Privacy Regulations Limiting Ad-Targeting | -0.7% | Europe and North America | Short term (≤ 2 years) |

| Algorithmic Discovery Bias Marginalizing Long-Tail Creators | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Royalty-Rate Inflation Exceeding ARPU Growth

Royalty inflation is one of the clearest structural limits on profit expansion in the audio streaming market. The Copyright Royalty Board’s Web VI determination raised the per-performance mechanical rate from USD 0.0021 under Web V to USD 0.0028 in 2026 and set a path to USD 0.0032 by 2030. The Digital Media Association stated that platforms already remit around 70% of revenue to rights holders under existing frameworks, which means there is limited room to absorb higher rates without price action or margin pressure. The problem is sharper in emerging markets, where localized pricing can expand the addressable base but often cannot raise ARPU fast enough to match the speed of royalty increases. IMPALA also warned in June 2025 that streaming reform proposals could steer more royalty flows toward catalog-heavy rights owners, which may deepen cost pressure for platforms that rely on long-tail content to differentiate.

Content-License Windowing By Major Labels

Content windowing weakens the basic promise of instant access, which is central to the audio streaming market. When labels delay or restrict availability on lower-priced tiers, the impact can be larger than a catalog count suggests because new releases still shape habit formation, search behavior, and early subscription satisfaction. Windowing is especially sensitive during the first year of a subscriber relationship, when users are still deciding whether one service is materially better than another. The tension between shorter artist-preferred licensing terms and longer label-preferred terms also creates recurring points of renegotiation where temporary gaps can appear in the catalog. For platforms in the audio streaming market, those gaps can drive search abandonment and churn at a time when customer acquisition costs remain high, and differentiation on catalog depth is still important.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Podcast Hosting Challenges On-Demand Music’s Structural Lead

On-demand music streaming held 78.20% of the audio streaming market share in 2025, which kept it as the core revenue engine for the category. That lead came from catalog depth, recommendation systems, and repeat listening habits that support monthly recurring revenue across large subscriber bases. The service also benefits from long-established licensing relationships, playlist ecosystems, and social sharing features that make switching less effortless than it appears at first glance. Those features matter because the audio streaming market still depends heavily on predictable, repeat use cases, and on-demand music remains the format most closely tied to everyday listening. At the same time, the segment is no longer the only driver of engagement growth because adjacent spoken-audio categories are adding new listening occasions and ad inventory.

Podcast hosting and distribution is projected to grow at a 19.60% CAGR through 2031, helped by advertising demand and the lower marginal cost of hosting creator-led content versus licensed music. Global monthly podcast listenership reached 619 million in 2026, and the United States podcast advertising market expanded 31% year over year in the same period, showing why podcast distribution is gaining strategic weight inside the audio streaming market. Spotify said audiobook listeners rose 36% year over year in the service’s second year in that category, with a catalog that exceeded 500,000 titles across 14 markets, which supports the view that audiobooks are becoming an added engagement layer inside broader subscriptions rather than a separate purchase decision. Live internet radio, ASMR, and meditation audio still retain dedicated audiences whose sessions are often longer and more ambient than standard on-demand use. That means the audio streaming industry is gradually supporting more listening modes, even though on-demand music still sets the commercial baseline for service type economics.

By Monetization Model: Programmatic Audio Narrows The Value Gap

Subscription-based monetization held 63.10% share of the audio streaming market size in 2025, which shows that recurring paid access remained the main cash foundation across leading platforms. This structure is still supported by large premium bases, including Spotify’s 293 million premium subscribers, and by ecosystem advantages that help services like Apple Music stay closely tied to device usage and account identity. Subscription revenue also remains easier to forecast than advertising income, which is why platforms continue testing periodic price increases even in mature markets. The model has resilience because highly engaged users treat ad-free listening, offline access, and broader content libraries as part of the core value proposition. In the audio streaming market, this keeps paid tiers central even as the next phase of growth is coming from improved ad monetization rather than only new subscriptions.

The advertising-supported model is forecast to grow at a 17.80% CAGR through 2031, making it the fastest-growing monetization path in the audio streaming market. IAB and PwC reported that digital audio advertising grew 10.2% to USD 8.4 billion in 2025, which shows that monetization is still rising against a very large base of listening time. Programmatic tools are helping platforms make that inventory more usable through audience targeting, dynamic creative, and better cross-device measurement, which narrows the long-standing gap between time spent and ad spend capture. Hybrid freemium tiers still matter because they reduce entry barriers in lower-income markets and create a funnel into paid plans over time. Pay-per-listen models remain smaller, but they preserve a place for occasional users who want access without a monthly commitment, which keeps pricing architecture broad in the audio streaming industry.

By Platform: Connected Cars Become A Durable Access Layer

Smartphones and tablets held 70.84% share of the audio streaming market size in 2025, which confirms that mobile devices remain the default access point across nearly every geography and income tier. Their position is reinforced by near-universal app availability, portable listening, mobile data access, and the fact that subscriptions are often activated and managed through the phone. This gives the audio streaming market a very broad delivery base, but it also means competition for attention stays high because music, podcasts, video, gaming, and messaging all sit on the same screen. Even so, the phone remains the center of account identity and the most direct route to discovery, saving, and sharing behavior. That is why mobile-led engagement still anchors the platform mix even as other devices are becoming more valuable for longer or more context-specific sessions.

Connected cars are projected to expand at an 18.21% CAGR through 2031, making them the fastest-growing device category in the audio streaming market. General Motors rolled out native Apple Music to 1.2 million vehicles by March 2026, while Hyundai’s Pleos Connect system integrated Spotify and YouTube with an LLM-powered voice assistant, showing that automotive streaming has moved into large-scale deployment. Smart speakers and home hubs support a second access layer by creating ambient listening in domestic settings rather than replacing mobile usage outright. Wearables are also emerging through fitness-linked use cases, and Spotify’s April 2026 Peloton partnership shows how exercise can extend daily listening time into additional routines. Desktop and laptop listening is declining as a share of use, but it still matters in work, study, and background environments where long sessions are common. Together, these shifts show that the audio streaming market is no longer just mobile-first, but increasingly context-specific across cars, homes, and activity-linked devices.

By Content Type: Podcasts And Audiobooks Expand Beyond Music-Led Habits

Music held 60.20% share in 2025, which kept it as the largest content segment and the central engagement engine in the audio streaming market. The category benefits from broad daily relevance, deep catalogs, and personalization loops that improve with every interaction. Tencent Music reported music services revenue of CNY 6.51 billion (USD 0.95 billion), in Q1 2026, up 12.2% year over year, and highlighted premium live audio events, including a digital album from Jay Chou that generated RMB 100 million (USD 14.8 million) or more in the quarter. That shows music content can still support monetization beyond standard subscription and ad formats when fandom, exclusivity, and event-style releases are present. In the audio streaming market, music remains the universal anchor because it serves both active and passive listening better than any other content format.

Podcasts are forecast to grow at a 20.40% CAGR through 2031, which makes them the fastest-expanding content format in the audio streaming market. SiriusXM stated that YouTube accounted for 32% of all United States podcast listening time in Q4 2025, which shows that podcast competition now spans audio-first and video-led distribution channels. Audiobooks are also widening their appeal, and Spotify cited UK Publishers Association data showing that United Kingdom audiobook revenue reached a record GBP 268 million (USD 341 million), in 2024, up 31% year over year. Live radio streams continue to hold loyal audiences in sports, talk, and cultural programming, which regional specialists can use to defend audience positions that pure on-demand models do not fully replace. As a result, the audio streaming market is broadening from a music-led service into a multi-format consumption layer where spoken audio carries increasing strategic value.

By End-User: OEM Channels Add A B2B2C Layer To A Consumer-Led Model

Individual consumers held 87.31% of the audio streaming market share in 2025, which reflects how strongly the category still depends on direct platform-to-person relationships. The Digital Media Association reported that 94% of United States music streamers loved or liked their primary service, and 92% of paid subscribers rated it as strong value, which helps explain why personalization and catalog depth remain priority investment areas. This segment continues to define the commercial center of the audio streaming market because users make repeat decisions on subscription renewal, listening time, and ad receptivity. It also provides the largest base for upselling podcasts, audiobooks, family plans, student offers, and higher-priced premium tiers. Even as the ecosystem becomes more complex, individual demand still determines what content gets surfaced, monetized, and scaled across platforms.

Automotive OEM channels are projected to grow at a 17.24% CAGR through 2031, which adds a more structured B2B2C layer to the audio streaming market. Hyundai said it is targeting 20 million connected vehicles with integrated streaming by 2030, while General Motors bundled 8 years of complimentary connectivity with its Apple Music rollout, showing how subscription access can now be tied to vehicle delivery rather than app store discovery. Commercial venues remain underdeveloped but important, and Deezer relaunched Deezer for Business in March 2026 after a successful 300-customer pilot in 2025, which suggests venue licensing is becoming a more deliberate growth path. Media and entertainment enterprises form another end-user group by using APIs, streaming data, and catalog analytics for audience intelligence and performance monitoring. These layers do not displace the consumer base, but they do make the audio streaming market more diverse in how subscriber value is acquired and monetized.

Geography Analysis

North America held 39.64% share of the audio streaming market in 2025, which made it the largest regional contributor. The United States wholesale recorded music market reached USD 11.535 billion in 2025, and paid streaming subscriptions rose to 106.5 million, the strongest net annual intake since 2022, showing that growth continued even in a mature environment. The region also has the deepest programmatic audio advertising base, which gives leading platforms a stronger ability to monetize free listening and podcasts alongside paid subscriptions. Canada supports premium uptake through high broadband penetration, while Mexico is benefiting from middle-class expansion and bundle-led conversion from free to paid listening. In parallel, the SiriusXM and YouTube audio advertising arrangement announced in April 2026 points to a market where podcast and radio inventory is being drawn more tightly into large-scale ad sales infrastructure. Royalty regulation also matters more here than in many other regions because the United States rate decisions can influence broader licensing and pricing behavior across the audio streaming market.

Asia-Pacific is the fastest-growing region in the audio streaming market, with a projected CAGR of 17.66% through 2031. Tencent Music reported revenue of CNY 7.90 billion (USD 1.15 billion), in Q1 2026, up 7.3% year over year, showing that local platform investment and content localization are still supporting strong expansion. India’s mobile broadband base exceeded 812 million subscriptions, which leaves a large addressable audience for paid audio as pricing and bundling continue to adapt to income realities. Japan, South Korea, and Australia remain premium markets, but each has distinct content preferences that require localized editorial decisions and recommendation models. South America is growing as well, though unevenly, with Brazil supported by 84.3% internet penetration and operator-led distribution models such as Claro Música still important where discretionary spending is tighter.

Europe held a significant share in 2025, but its growth profile is split between highly penetrated Western markets and faster-expanding emerging parts of the region. Germany’s household digital music spending rose 18.7% year over year in 2024, and the United Kingdom audiobook segment reached GBP 268 million (USD 341 million), which shows that willingness to pay is widening across audio formats rather than staying limited to music. Privacy rules are reshaping monetization in Europe because tighter targeting standards are pushing platforms toward contextual advertising methods for ad-supported audio. Middle East and Africa is becoming a more strategic growth pocket in the audio streaming market, with Saudi Arabia allocating SAR 4.8 billion (USD 1.28 billion), toward entertainment development in 2024, Anghami reporting FY2025 revenue of USD 99.3 million with 27% year-over-year growth, and Boomplay’s 145-million-track catalog helping position West Africa as a content origination hub. This combination of regulation, local content depth, and rising entertainment investment means regional specialists still have room to hold meaningful ground even as global platforms expand.

Competitive Landscape

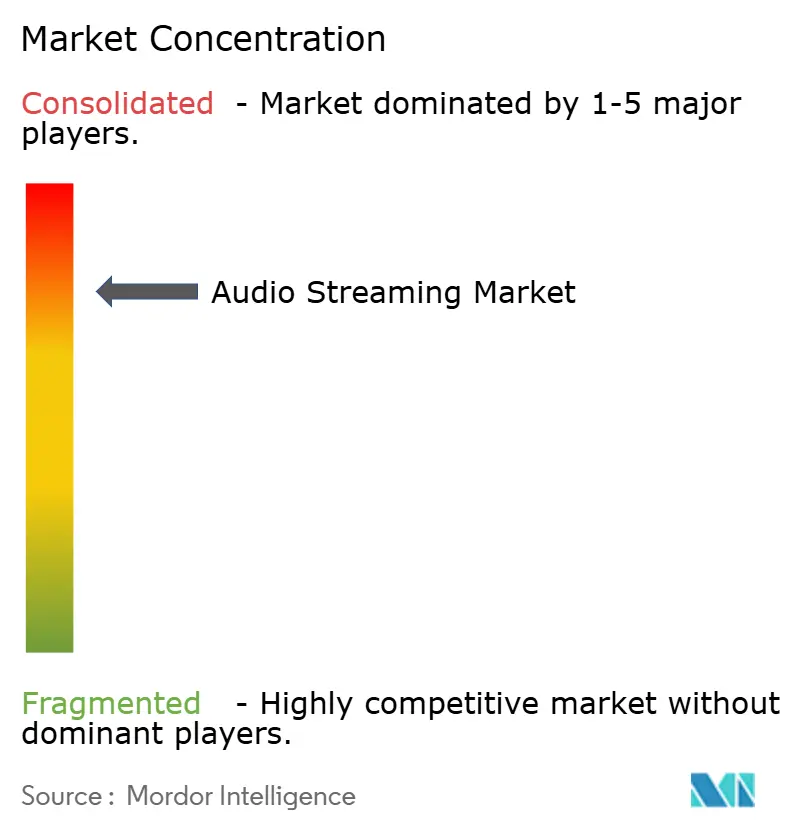

The audio streaming market combines heavy concentration in developed paid subscription markets with visible regional fragmentation elsewhere. In the United States, five platforms collectively command close to 99% of paid subscriptions, which shows how consolidated the premium tier has become in a mature market. Spotify remains the reference point for scale, with Q1 2026 revenue of EUR 4.5 billion (USD 5.09 billion), a 33% gross margin, and EUR 715 million (USD 808 million), in operating income, indicating a clearer shift from growth-at-any-cost toward margin discipline. Deezer’s first annual profit, EUR 8.5 million (USD 9.62 million), in FY2025 showed that mid-tier platforms can still build viable positions by focusing on selective geographies and differentiated offerings instead of pursuing uniform global expansion. For the audio streaming market, this means competition is no longer only about subscriber volume, but increasingly about how efficiently each platform turns listening into profit.

Strategic moves are clustering around personalization, monetization infrastructure, and ecosystem embedding in the audio streaming market. Spotify expanded Prompted Playlists and kept building its AI-assisted discovery layer, while Deezer advanced features such as Flow Tuner to make listening sessions more responsive to user intent. On the monetization side, Spotify’s programmatic partnership with Amazon DSP and the SiriusXM and YouTube advertising arrangement show that control over audio ad distribution is becoming a stronger differentiator. On the access side, General Motors’ Apple Music rollout and Hyundai’s Pleos Connect launch show that platform presence inside the vehicle is now a strategic channel rather than a side feature. The underserved white space remains commercial venue licensing, where compliance and rights complexity have kept many consumer-led services from scaling a strong position.

Disruption is also coming from adjacent technology models that may change how the audio streaming market sources content and manages rights. AI-native audio tools are lowering production barriers in podcasts and spoken-word formats, while PodcastOneAI and Deezer’s AI detection licensing show that generative audio is already entering operating workflows and platform services. Blockchain-based royalty settlement is still early, but the model is attracting independent rights holders by promising faster and more transparent disbursement, which could create a supply-side edge for platforms willing to support nontraditional rights infrastructure. Compliance now adds another layer of competitive cost because data security, AI transparency, and platform governance expectations are easier for larger services to manage than for smaller entrants. Napster and Yandex Music are less representative of the active competitive field discussed here because Napster has shifted toward blockchain and web3 ownership infrastructure and Yandex Music is geographically constrained after corporate restructuring. By contrast, Melon in South Korea and Audiomack in Africa-facing listening corridors are more relevant examples of regional competitive pressure where local content fit and usage habits still matter.

Audio Streaming Industry Leaders

Spotify Technology S.A.

Apple Inc.

Amazon.com Inc.

Alphabet Inc.

Tencent Music Entertainment Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Hyundai Motor Group unveiled the Pleos Connect in-car infotainment system on April 30, 2026, featuring native Spotify and YouTube integration alongside the Gleo AI large language model voice assistant, the system targets Hyundai's broader connected vehicle ecosystem and positions audio streaming as a core vehicle interface layer.

- April 2026: PodcastOne launched PodcastOneAI on April 30, 2026, a suite of AI-assisted podcast production tools for its network of creators, targeting production cost reduction and episode turnaround speed as competitive pressures on podcast economics intensify.

- April 2026: Spotify launched a fitness streaming hub in partnership with Peloton on April 27, 2026, enabling subscribers to access workout playlists synchronized with Peloton instructor sessions, extending the platform's addressable daily listening time into the exercise occasion category.

- April 2026: SiriusXM and YouTube entered an exclusive audio advertising sales arrangement announced on April 22, 2026, under which SiriusXM will represent YouTube's podcast audio inventory in the United States, effective fall 2026, the deal combines SiriusXM's programmatic audio sales infrastructure with YouTube's dominant podcast listening share of 32% of all US podcast time.

Global Audio Streaming Market Report Scope

The Audio Streaming Market refers to the global industry centered on platforms and services that deliver music, podcasts, audiobooks, and other audio content directly to consumers via the internet, often through subscription-based or ad-supported models. This market encompasses streaming providers, technology enablers, and content creators, offering on-demand access to vast libraries of audio content across devices such as smartphones, smart speakers, and computers.

The Audio Streaming Market Report is Segmented by Service Type (On-Demand Music Streaming, Live Internet Radio, Podcast Hosting and Distribution, Audiobook Streaming, and Other Niche Audio (ASMR, Meditation)), Monetization (Subscription-Based, Advertising-Supported, Hybrid Freemium, and Pay-Per-Listen), Platform/Device (Smartphones and Tablets, Desktop/Laptop, Smart Speakers and Home Hubs, Connected Cars, and Wearables and Other IoT), Content (Music, Podcasts, Audiobooks, and Live Radio Streams), End-User (Individual Consumers, Commercial Venues (Retail and Hospitality), Automotive OEM Integrations, and Media and Entertainment Enterprises), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| On-Demand Music Streaming |

| Live Internet Radio |

| Podcast Hosting and Distribution |

| Audiobook Streaming |

| Other Niche Audio (ASMR, Meditation) |

| Subscription-Based |

| Advertising-Supported |

| Hybrid Freemium |

| Pay-Per-Listen |

| Smartphones and Tablets |

| Desktop/Laptop |

| Smart Speakers and Home Hubs |

| Connected Cars |

| Wearables and Other IoT |

| Music |

| Podcasts |

| Audiobooks |

| Live Radio Streams |

| Individual Consumers |

| Commercial Venues (Retail, Hospitality) |

| Automotive OEM Integrations |

| Media and Entertainment Enterprises |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | On-Demand Music Streaming | ||

| Live Internet Radio | |||

| Podcast Hosting and Distribution | |||

| Audiobook Streaming | |||

| Other Niche Audio (ASMR, Meditation) | |||

| By Monetization Model | Subscription-Based | ||

| Advertising-Supported | |||

| Hybrid Freemium | |||

| Pay-Per-Listen | |||

| By Platform/Device | Smartphones and Tablets | ||

| Desktop/Laptop | |||

| Smart Speakers and Home Hubs | |||

| Connected Cars | |||

| Wearables and Other IoT | |||

| By Content Type | Music | ||

| Podcasts | |||

| Audiobooks | |||

| Live Radio Streams | |||

| By End-User | Individual Consumers | ||

| Commercial Venues (Retail, Hospitality) | |||

| Automotive OEM Integrations | |||

| Media and Entertainment Enterprises | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current and forecast value of audio streaming?

The audio streaming market was valued at USD 46.93 billion in 2025, stands at USD 54.54 billion in 2026, and is projected to reach USD 115.59 billion by 2031 at a 16.21% CAGR.

What is driving growth in audio platforms through 2031?

Growth is being driven by smartphone-led access, AI-based personalization, stronger ad monetization, telco bundles, and native in-car integrations that make listening more habitual across daily routines.

Which service category leads revenue today?

On-demand music streaming led service type revenue with a 78.23% share in 2025, supported by catalog scale, repeat sessions, and steady subscription economics.

Which monetization model is growing the fastest?

Ad-supported streaming is the fastest-growing monetization model, with a projected 17.82% CAGR through 2031 as digital audio ad tools and inventory monetization continue to improve.

Why are connected cars becoming important for streaming platforms?

Connected cars are projected to grow at an 18.21% CAGR through 2031 because native integrations from automakers such as General Motors, Hyundai, Toyota, Lexus, and Volvo are turning vehicles into long-term listening environments.

Which region is expanding the fastest?

Asia-Pacific is the fastest-growing regional segment with a projected 17.66% CAGR through 2031, supported by mobile-first users, telco-OTT bundles, and rising digital entertainment spending in India and Southeast Asia.

Page last updated on: