Music Streaming Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

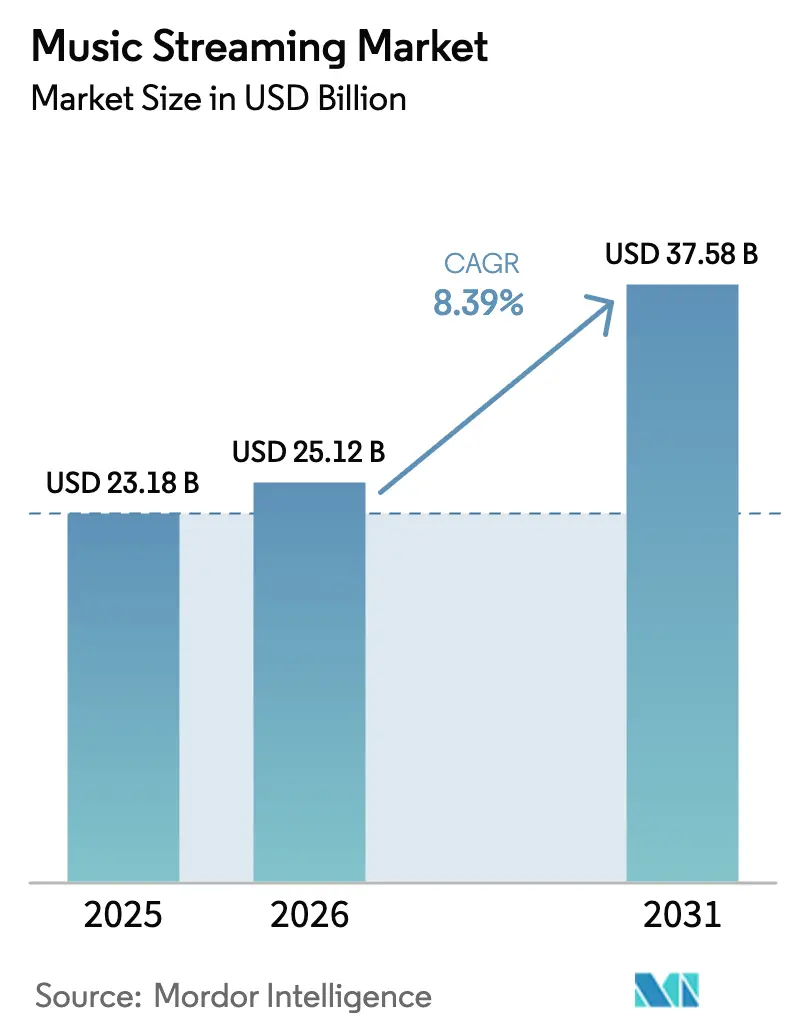

| Market Size (2026) | USD 25.12 Billion |

| Market Size (2031) | USD 37.58 Billion |

| Growth Rate (2026 - 2031) | 8.39% CAGR |

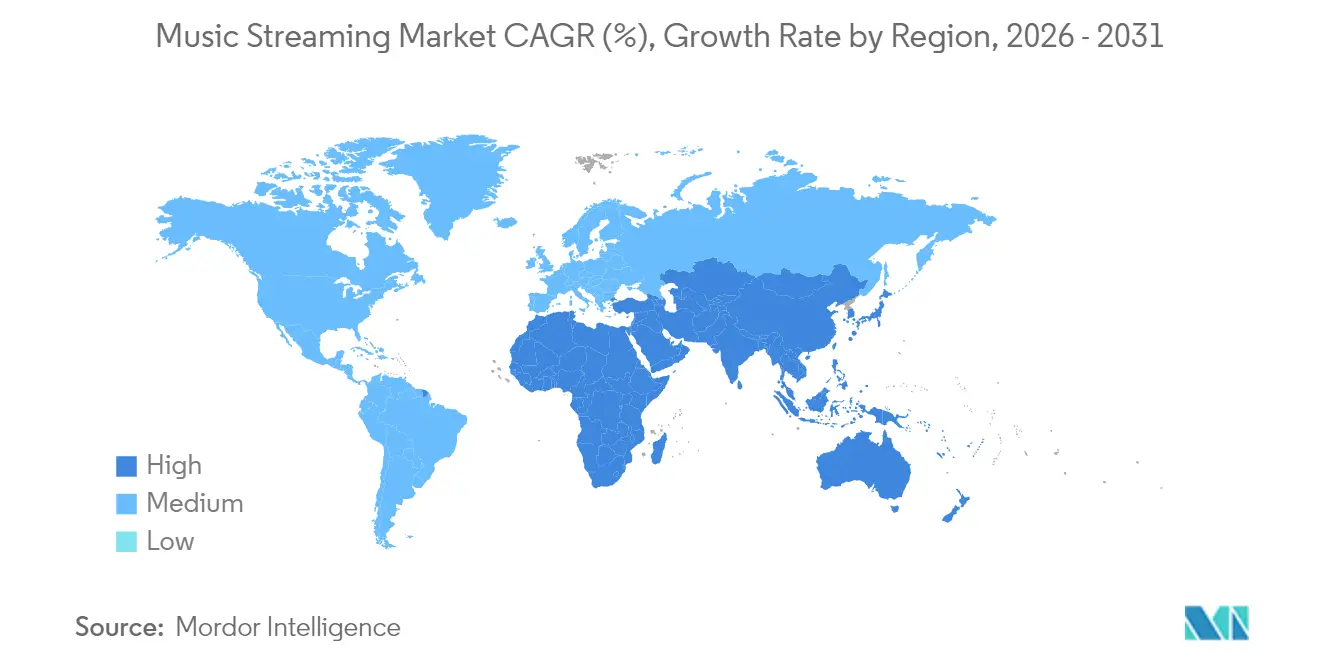

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Music Streaming Market Analysis by Mordor Intelligence

The music streaming market size is expected to grow from USD 23.18 billion in 2025 to USD 25.12 billion in 2026 and is forecast to reach USD 37.58 billion by 2031 at 8.39% CAGR over 2026-2031. Subscriber totals passed 752 million in 2024, and streaming already delivers 69% of all recorded-music revenue, underscoring the channel’s central role in the global music economy [2]Mark Sutherland, “Streaming Subscriptions Soar to 752 Million,” Music Week, musicweek.com . Competitive intensity is rising as AI-curated discovery, premium lossless audio, and telco bundles redefine user expectations and shrink switching costs. Growth patterns are diverging: North America retains the largest regional slice, yet emerging territories such as the Middle East and Africa are expanding at double-digit rates thanks to mobile-first access and lower-priced plans. At the same time, rising licensing fees and mounting artist pressure for fan-centric royalty models are squeezing margins and forcing platforms to explore new revenue levers.

Key Report Takeaways

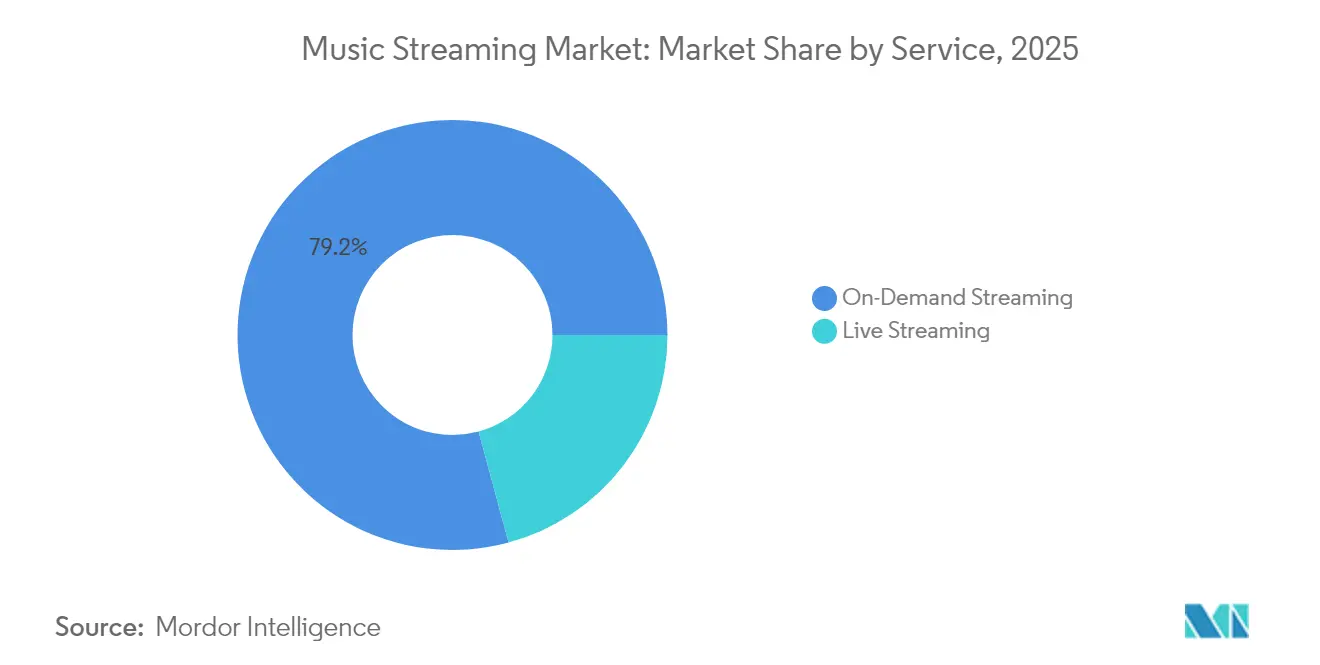

- By service, On-Demand streaming led with 79.20% of the music streaming market share in 2025, while Live Streaming is advancing at a 15.12% CAGR through 2031.

- By revenue model, the Subscription tier held 64.20% of the music streaming market size in 2025; Ad-Supported options are projected to expand at a 8.72% CAGR over 2026-2031.

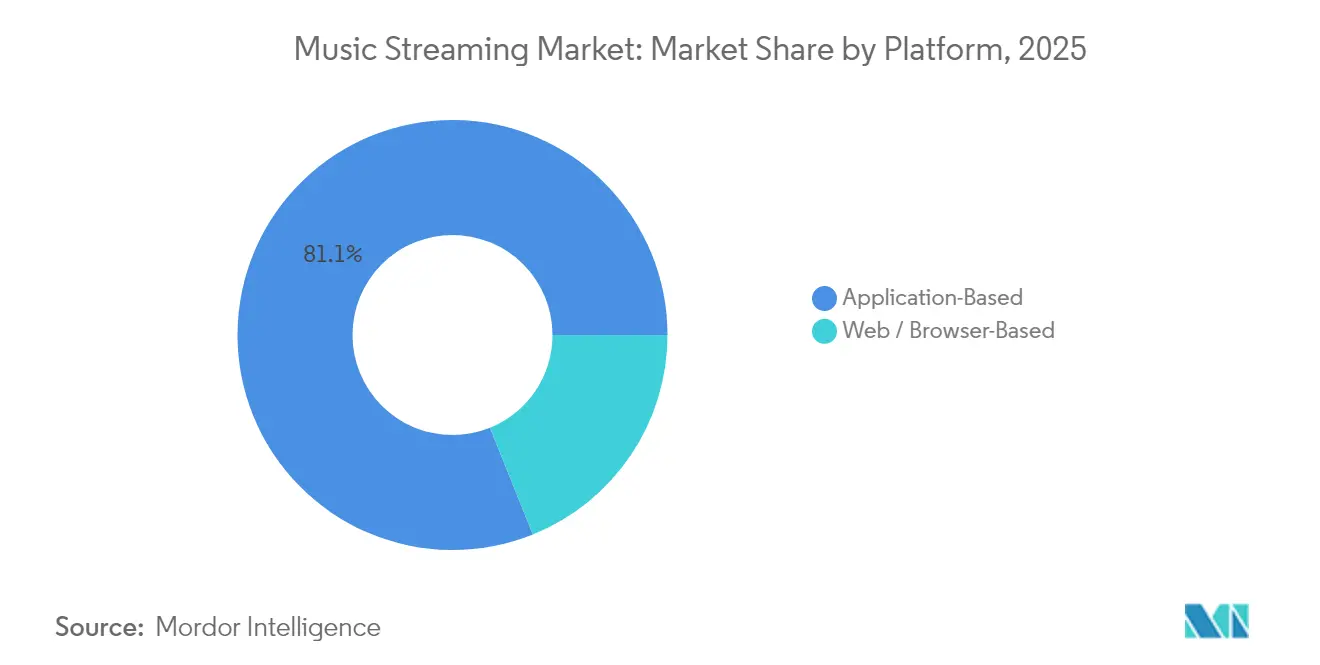

- By platform, Application-based listening accounted for 81.10% share of the music streaming market size in 2025, whereas Browser-based access is forecast to grow at a 9.94% CAGR.

- By content type, Audio dominated with 74.20% share of the music streaming market in 2025, while Video usage is set to climb at a 11.52% CAGR.

- By end user, Individual listeners commanded 62.10% share in 2025; the Commercial segment is pacing fastest at a 13.56% CAGR to 2031.

- By geography, North America captured 33.40% of the music streaming market share in 2025, but the Middle East & Africa region is on track for a 16.90% CAGR.

- Spotify, Apple Music, Amazon Music, Tencent Music Entertainment and YouTube Music collectively held 72% of global revenue in 2024, with Spotify alone at 32.2% share musicweek.com.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Music Streaming Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Paid subscriptions boom in emerging markets | +2.5% | Southeast Asia, MENA, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Podcast and spoken-word integration | +1.2% | North America, Europe | Short term (≤ 2 years) |

| Telco-bundled streaming plans | +1.8% | Africa, Middle East, South Asia | Medium term (2-4 years) |

| 5G-enabled lossless and spatial audio | +0.9% | Europe, North America, East Asia | Long term (≥ 4 years) |

| AI-Curated Personalization | +1.1% | Global | Short term (≤ 2 years) |

| Connected Car Integrations | +0.6% | North America, Europe, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of Paid Subscriptions in Emerging Markets

Subscriber additions in Southeast Asia, MENA and Sub-Saharan Africa are reshaping the music streaming market as 78.4% of 2024’s new users originated from these regions. Rising smartphone ownership, inexpensive data plans and culturally localised catalogs are speeding formal adoption where physical formats never scaled. Chinese platforms counted 190 million paying listeners, India’s paid cohort still sits below 2% of population yet is expanding above 22% annually, and MENA derives 99.5% of recorded-music revenue from streaming. Multilingual interface upgrades, offline caching, daily micro-pricing, and prepaid gift codes continue to lower entry barriers. Consequently, leading services report double-digit growth even with modest average revenue per user (ARPU), positioning emerging territories to deliver the bulk of absolute subscriber gains through 2030.

Podcast & Non-Music Audio Integration Driving Average Time Spent

Platforms that distribute podcasts alongside songs are realising session-length uplifts of 41%, a metric closely tied to both ad inventory and churn reduction [3]Frontiers Editorial Board, “User Retention in Hybrid Audio Streams,” Frontiers in Artificial Intelligence, frontiersin.org . In the United States, content diversification has become a hedge against slowing subscription upgrades as revenue growth cooled to 3.6% in 2024. Spoken-word catalogs also cut royalties owed to major labels, rebalancing negotiating leverage. Independent creators gain brand-safe exposure, and dynamic ad-insertion engines monetise high-engagement niches such as true crime and wellness with CPMs that often exceed music’s. Cross-promotion between playlists, live shows and podcast episodes deepens ecosystem stickiness, further reinforcing premium conversion funnels.

Telco-Bundled Streaming Plans Expanding Addressable Base

Partnerships with carriers are unlocking new paid cohorts where credit-card penetration is low. Airtel’s 2025 Apple Music bundle for Indian Wi-Fi and post-paid customers immediately widened access to millions who previously streamed via ad-supported tiers [4]Airtel Communications, “Airtel Brings Apple Music to Wi-Fi & Post-Paid Customers,” Airtel, airtel.com. In Africa, MTN’s music passes priced at less than USD 1 per month scaled rapidly by leveraging airtime billing and zero-rating data usage telecomlead.com. For platforms, bundled billing slashes acquisition costs and back-end churn. For carriers, services raise average revenue per user and reduce subscriber turnover, creating virtuous network effects in markets where prepaid SIM cycles dominate.

5G & Edge Computing Enabling Lossless & Spatial Audio Adoption

Increased bandwidth and lower latency permit FLAC and Dolby Atmos streams to load instantly, stimulating a premium tier within the music streaming market ieee.org. European operators already pilot network slicing dedicated to audio, guaranteeing uninterrupted delivery during peak hours. Enhanced fidelity satisfies audiophile segments and empowers artists to showcase immersive mixes. Because higher-bit-rate catalogs trigger tier upgrades, labels and platforms capture incremental revenue while raising perceived differentiation versus video-first social apps that emphasise short previews over full songs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising content licensing costs | -1.5% | Global | Short term (≤ 2 years) |

| Fragmented regional copyright regimes | -0.8% | Global | Medium term (2-4 years) |

| Low Subscription Willingness-to-Pay | -1.4% | Latin America, Africa, parts of Asia | Short term (≤ 2 years) |

| Intensifying Artist Royalty Disputes | -0.9% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Content Licensing Costs Compressing Margins

Royalty outlays remain near 70% of platform revenue; Spotify alone transferred more than USD 10 billion to rights holders in 2024. Mid-tier providers lack comparable scale and diversified income, prompting exits or consolidation. As major labels lobby for “Streaming 2.0” frameworks that segment user plans and uptick per-stream rates, cost curves threaten profitability even for leaders. To defend margins, services accelerate direct-to-artist programs, original podcasts, and dynamic pricing models, yet these pivots require heavy upfront investment.

Intensifying Artist Royalty Disputes Over Fan-Centric Models

Streaming’s pro-rata payout delivers less than USD 0.0032 per Spotify stream, a figure many musicians label unsustainable. Universal Music and Deezer introduced a user-centric approach in 2024, promising stronger alignment between subscription dollars and individual listening. While established artists stand to benefit, independents fear reduced pool size. The negotiation uncertainty slows catalog windows in some territories and could raise licensing fees if large rights owners succeed in reshaping economics to their favor.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Live Streaming Captures Momentum

Live Streaming generated the fastest CAGR at 15.12% between 2026-2031, even though On-Demand models held 79.20% of total revenue in 2025. The music streaming market size for Live events is scaling as 5G eradicates latency, allowing real-time fan reactions, tipping, and exclusive merch drops. Platforms host digital festivals that reach geographies where physical tours remain rare. In contrast, On-Demand growth in North America slowed to 3.6% as libraries hit saturation and customer acquisition costs rose. Providers now bundle exclusive singles or backstage passes to reinvigorate on-demand catalogs and cross-sell toward live formats, blurring usage boundaries.

Live adoption also correlates with creator economics: ticketed streams often net artists higher take-home percentages than standard royalty splits, motivating performers to schedule recurrent digital shows. For listeners, interactive emoji reactions and real-time polls enrich communal experiences that on-demand playback cannot replicate. Consequently, hybrid releases combining a pre-recorded studio album with a launch-week live performance are becoming normative, weaving both service modes into a single campaign arc. These synergies reinforce user loyalty and diversify monetisation for rights holders in the music streaming market.

By Revenue Model: Ad-Supported Tier Gains Traction

Subscription plans delivered 64.20% of 2025 turnover, yet ad-supported listening is forecast to post a 8.72% CAGR and will command a growing slice of the music streaming market size by 2031. Economic headwinds and regional ARPU gaps fuel consumer migration to cost-free options. At the same time, programmatic audio ads fetch rising CPMs as brands target segments based on mood, activity, and location cues. Spotify’s Q4 2024 advertising revenue climbed 7% on the back of a 12% expansion in ad-supported monthly active users.

Free tiers also function as onboarding funnels: roughly 45% of Spotify’s 2024 premium sign-ups originated from the ad-supported cohort. Meanwhile, subscription models diversify into duo, family, student, and high-fidelity plans, each addressing discrete willingness-to-pay clusters. Limited-time upsells, such as audiobooks or concert presales, encourage users to shift upward across tiers. As economic conditions vary by region, dual-track monetisation delivers flexibility for platforms to harvest maximum lifetime value across the global music streaming market.

By Platform: Browser-Based Access Surges

Native apps captured 81.10% of listening hours in 2025, yet browser sessions are rising at a 9.94% CAGR, the fastest of any platform slice. Developers exploit progressive web applications to bypass 15-30% app-store commissions, freeing margin for artist royalties or discounted pricing. In storage-constrained emerging markets, users appreciate avoiding 200 MB downloads, and lighter footprints reduce churn driven by “app fatigue.”

Still, native software maintains an edge in offline playback and deep OS integrations such as widgets and voice assistants. Hence, leading brands pursue an omnichannel approach, ensuring UI parity and synchronized libraries whichever entry point users choose. Browser progress may ultimately temper gatekeeper leverage exerted by dominant mobile ecosystems, shifting bargaining power toward streaming services in the wider music streaming market.

By Content Type: Video Drives Engagement Growth

Audio streams retained 74.20% revenue share in 2025, but video consumption is advancing at 11.52% CAGR, bolstered by short-form clips on TikTok and YouTube as feeders into full tracks. Labels exploit behind-the-scenes reels and vertical videos to spike release-day visibility, then redirect traffic into paid audio subscriptions. The integration of synced lyrics, real-time commenting and fan “duet” functions elevates stickiness.

Podcasts and other spoken-word assets keep expanding as platforms invest in exclusive talent, further lowering dependency on label licenses. Dynamic ad-insertion within episodic content commands premium rates, while host-read promotions nurture intimate brand trust. Experimentation with multi-modal formats—such as interactive choose-your-own-story music videos—illustrates converging boundaries between audio, video and gaming inside the music streaming market.

Geography Analysis

North America retained 33.40% of 2025 revenue, yet growth moderated to 3.6% on signs of penetration. The United States celebrated the 100-million paid-subscriber milestone in March 2025, pushing platforms to extract higher ARPU through hi-fi tiers, audiobooks and podcast bundles. Canada shows parallel trends, with regulators reviewing merger proposals to safeguard catalog diversity.

The Middle East & Africa is the fastest-growing territory, charting a 16.90% CAGR outlook to 2031. Saudi Arabia’s Vision 2030 investments and United Arab Emirates’ streaming-friendly copyright reforms encourage both local production and foreign catalog licensing. MENA generated a 22.8% revenue jump in 2024, over 99% of which stemmed from streaming. Regional champion Anghami grew premium accounts 18% year-over-year by integrating Arabic podcast networks and telecom bundles.

Europe posted 8.3% revenue growth in 2024, aided by widespread 5G coverage that propels lossless adoption. The UK commands nearly half of domestic listener share for Spotify at 47.1%, yet YouTube Music delivered the quickest expansion Germany, France and the Nordics show robust appetite for spatial audio and vinyl-bundle hybrids. In contrast, Asia-Pacific reveals a patchwork: Japan inches forward amid a resilient CD culture, China boasts 190 million payers across Tencent Music, NetEase Cloud and Alibaba, while India’s penetration remains low but rising quickly due to vernacular catalogs and telco pricing innovations. Latin America delivers 22.5% growth as Brazil, Mexico and Colombia embrace pay-per-day micro-plans and social-media-led discovery. Collectively, these regional currents sustain the long-range expansion of the music streaming market.

Competitive Landscape

The music streaming market is moderately concentrated, with the top five platforms holding roughly 72% of revenue. Spotify leads at 32.2% worldwide, but Apple Music’s 30.7% North-American share narrows the global gap. Amazon Music benefits from ecosystem bundling, while Google’s YouTube Music capitalizes on video heritage to escalate conversion. Tencent Music dominates China’s walled market; NetEase Cloud captures fandom via social commenting threads.

The relationship with rights owners defines competitive tactics. Major labels Universal, Sony and Warner collectively command close to 70% of recorded-music income, granting them steep leverage in licensing rounds. To counterbalance, services diversify into podcasts, audiobooks and direct-fan tools that bypass label control. Spotify’s AI-driven “DJ” voice assistant personalises playlists, boosting session times, while Apple Music integrates spatial audio as a hardware differentiator. Deezer partners with UMG on artist-centric royalties, positioning itself as a purer music advocate amid big-tech rivals.

White-space opportunities persist in regional niches. Boomplay in Africa and Anghami in MENA underscore how culturally attuned catalogs, offline caching and telco billing can fend off global giants. Separately, TikTok’s music distribution ambitions threaten to shift discovery upstream, forcing incumbents to embed short-form clips and social-sharing workflows. As margins compress, analysts anticipate selective mergers or asset swaps podcast studios, rights marketplaces, data-analytics startups that enhance scale efficiencies or elevate bargaining positions within the evolving music streaming market.

Music Streaming Industry Leaders

Spotify Technology S.A.

Apple Inc. (Apple Music)

Amazon.com Inc. (Amazon Music)

Tencent Music Entertainment

Alphabet Inc. (YouTube Music)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Deezer revealed that 18% of all new music uploaded to streaming platforms is fully AI-generated, spotlighting artificial intelligence’s growing content role deezer.com.

- April 2025: Universal Music Group reported strong Q1 2025 performance but noted levelling growth in mature regions variety.com.

- March 2025: IFPI announced global recorded-music revenue reached USD 29.6 billion in 2024, with streaming exceeding USD 20 billion for the first time ifpi.org.

- February 2025: Airtel partnered exclusively with Apple to bundle Apple Music for Wi-Fi and post-paid subscribers in India airtel.com.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global music streaming market as all revenue accruing to digital services that transmit licensed audio content in real time or near-real time to consumer devices, whether through paid subscriptions or advertising-supported access. The definition captures on-demand and live streams delivered via dedicated apps or web players, but excludes physical sales, terrestrial radio, video-only streaming, and rights management fees not tied to end-user listening.

(Scope exclusion) Revenues from podcast hosting, video music clips, and artist merchandise are outside the present scope.

Segmentation Overview

- By Service

- On-Demand Streaming

- Live Streaming

- By Revenue Model

- Subscription (Premium, Family, Student)

- Ad-Supported (Free Tier, Sponsored Events)

- By Platform

- Application-Based

- Web / Browser-Based

- By Content Type

- Audio

- Video

- Podcast and Other Spoken-Word

- By End-User

- Individual (Consumers)

- Commercial (Fitness, Retail, Hospitality, Others)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed executives from DSPs, indie label aggregators, advertising networks, and mobile operators across North America, Europe, Asia-Pacific, and Latin America. Conversations clarified bundled pricing strategies, regional royalty norms, and emerging freemium uptake, allowing us to reconcile desk findings and close data gaps.

Desk Research

We gathered foundational figures from publicly available tier-1 sources such as IFPI's Global Music Report, Luminate's annual consumption dashboards, national telecom regulators, and international trade bodies like the OECD for broadband indicators. Company 10-Ks, investor decks, and association portals (RIAA, ERA) provided pricing, subscriber counts, and advertising yield patterns. Subscription churn ratios and user-time metrics were extracted from datasets in D&B Hoovers and Dow Jones Factiva, while Questel patent trends signaled platform innovation intensity. The sources listed illustrate our approach and are not exhaustive.

Market-Sizing & Forecasting

A top-down construct starts with paid and ad-supported listener pools reconstructed from telecom penetration and household income tiers, which are then multiplied by region-specific average revenue per user and ad-impression yields. Select bottom-up checks, streaming hours multiplied by royalty per stream, and sampled platform revenues refine totals. Key variables tracked include smartphone install base growth, broadband speed adoption, subscription pricing ladders, advertising CPMs on free tiers, and label revenue-share ratios. A multivariate regression blended with ARIMA captures how these drivers steer revenue through 2030. Scenario stress tests guided by primary-research consensus bound the forecast range.

Data Validation & Update Cycle

Every iteration undergoes variance scans against external indicators, senior analyst peer review, and anomaly callbacks to interviewees. Reports refresh yearly, with interim recalculations triggered by material events such as major royalty-rate resets or policy shifts.

Why Mordor's Music Streaming Baseline Earns Industry Trust

Published estimates often diverge because firms apply different content scopes, revenue inclusions, and refresh cadences. Understanding these levers helps buyers interpret the spread of numbers in the public domain.

Key gap drivers include whether podcasts and video clips are folded into totals, the handling of advertising versus subscription revenue, currency year alignment, and how aggressively future ARPU expansion is assumed before volume growth is validated.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 23.18 B (2025) | Mordor Intelligence | - |

| USD 46.66 B (2024) | Global Consultancy A | Includes podcasts and music videos, limited primary validation |

| USD 48.60 B (2024) | Industry Analytics B | Adds platform ad spend and uses single top-down feed |

The comparison shows that when scope is tightened to pure audio streams and estimates are cross-tested with bottom-up probes, totals align closer to the realities disclosed by leading DSPs. This disciplined, transparent pathway is how Mordor Intelligence delivers a dependable baseline for strategic decision-making.

Key Questions Answered in the Report

What is the current Music Streaming Market size?

In 2026, the Music Streaming Market size is expected to reach USD 25.12 billion.

Who are the key players in Music Streaming Market?

Spotify Inc., Apple Inc., Amazon Inc., Pandora Inc. and YouTube Inc. are the major companies operating in the Music Streaming Market.

Which is the fastest growing region in Music Streaming Market?

Middle East & Africa is estimated to grow at the highest CAGR over the forecast period (2026-2031) at 16.90%.

Which region has the biggest share in Music Streaming Market?

In 2025, the North America accounts for the largest market share in Music Streaming Market.

What years does this Music Streaming Market cover, and what was the market size in 2025?

In 2025, the Music Streaming Market size was estimated at USD 25.12 billion. The report covers the Music Streaming Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Music Streaming Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: