Musical Instrument Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

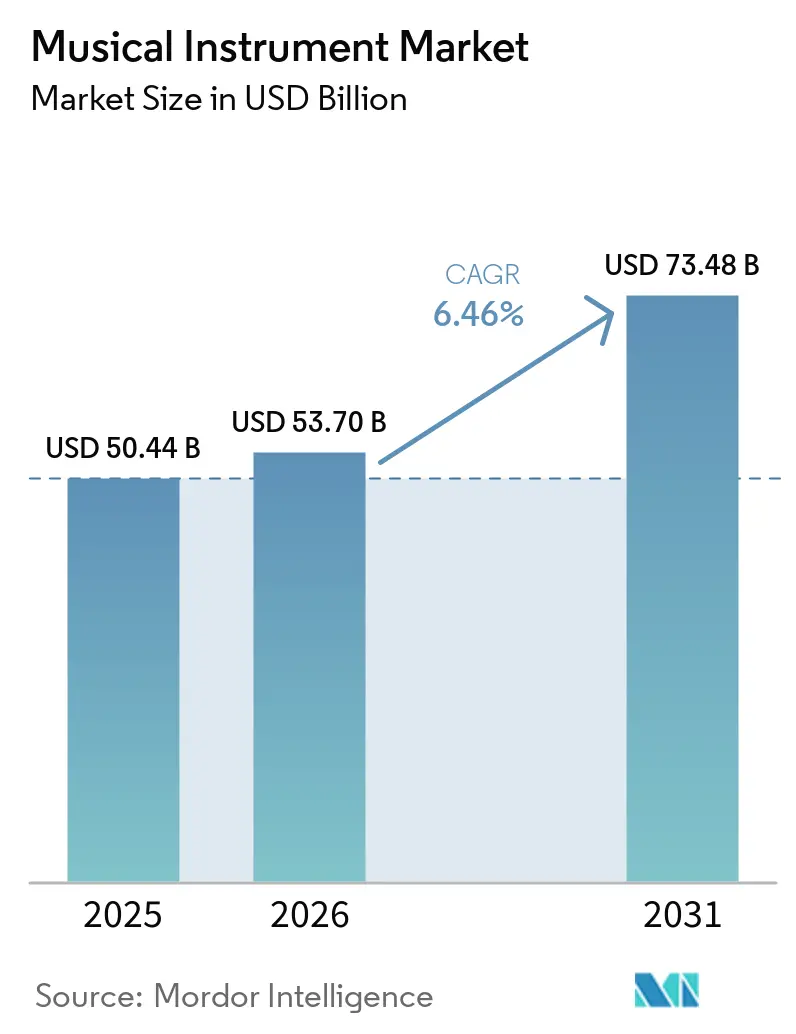

| Market Size (2026) | USD 53.70 Billion |

| Market Size (2031) | USD 73.48 Billion |

| Growth Rate (2026 - 2031) | 6.46% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Musical Instrument Market Analysis by Mordor Intelligence

The Musical Instrument Market size was valued at USD 50.44 billion in 2025 and estimated to grow from USD 53.7 billion in 2026 to reach USD 73.48 billion by 2031, at a CAGR of 6.46% during the forecast period (2026-2031). Rising demand stems from subscription-driven remote learning, IoT-enabled smart instruments, and steady government funding for music education, all of which cushion the sector against macro-economic swings. Technology is sharpening competitive edges as manufacturers embed sensors, cloud connectivity, and AI capabilities into traditional product lines, creating new recurring-revenue models. At the same time, stringent CITES regulations on tonewoods, growing consumer interest in eco-friendly materials, and a noticeable shift toward software-only production tools are reshaping product-development priorities. Regional performance diverges: Asia remains the volume anchor, the Middle East now leads growth, and North America holds firm in premium niches.

Key Report Takeaways

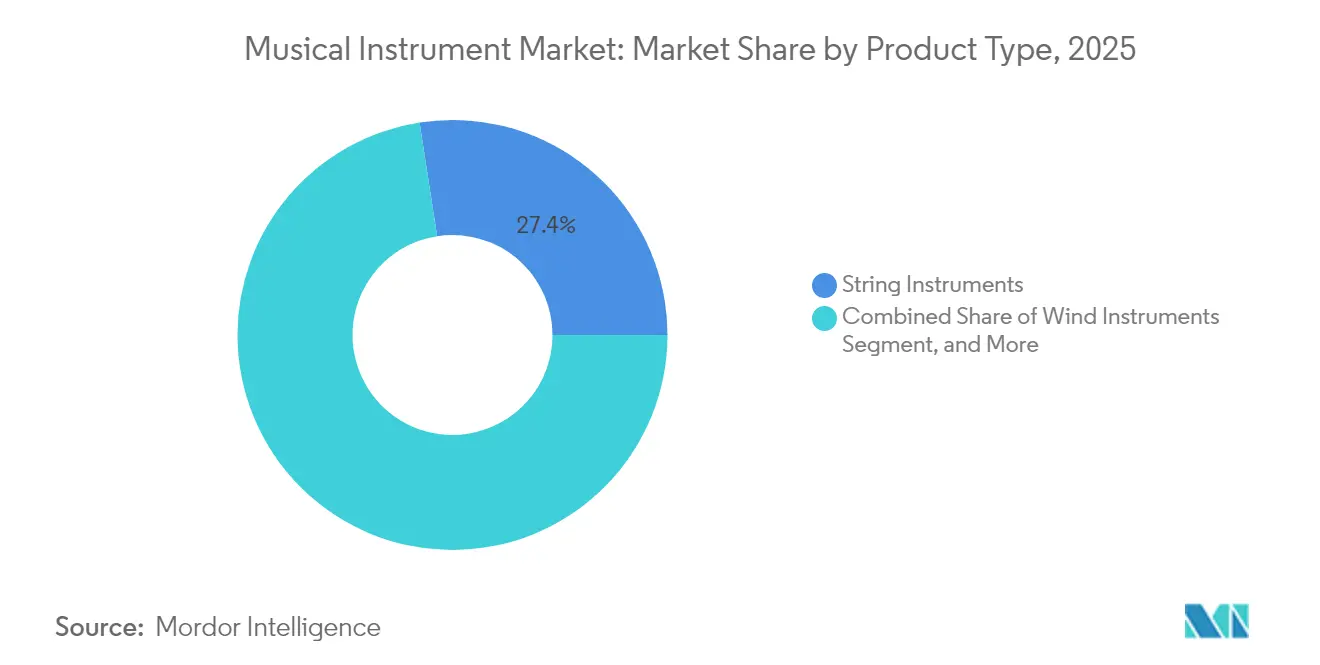

- By product type, string instruments accounted for 27.45% of musical instrument market share in 2025, while electronic instruments are projected to grow at an 8.78% CAGR through 2031.

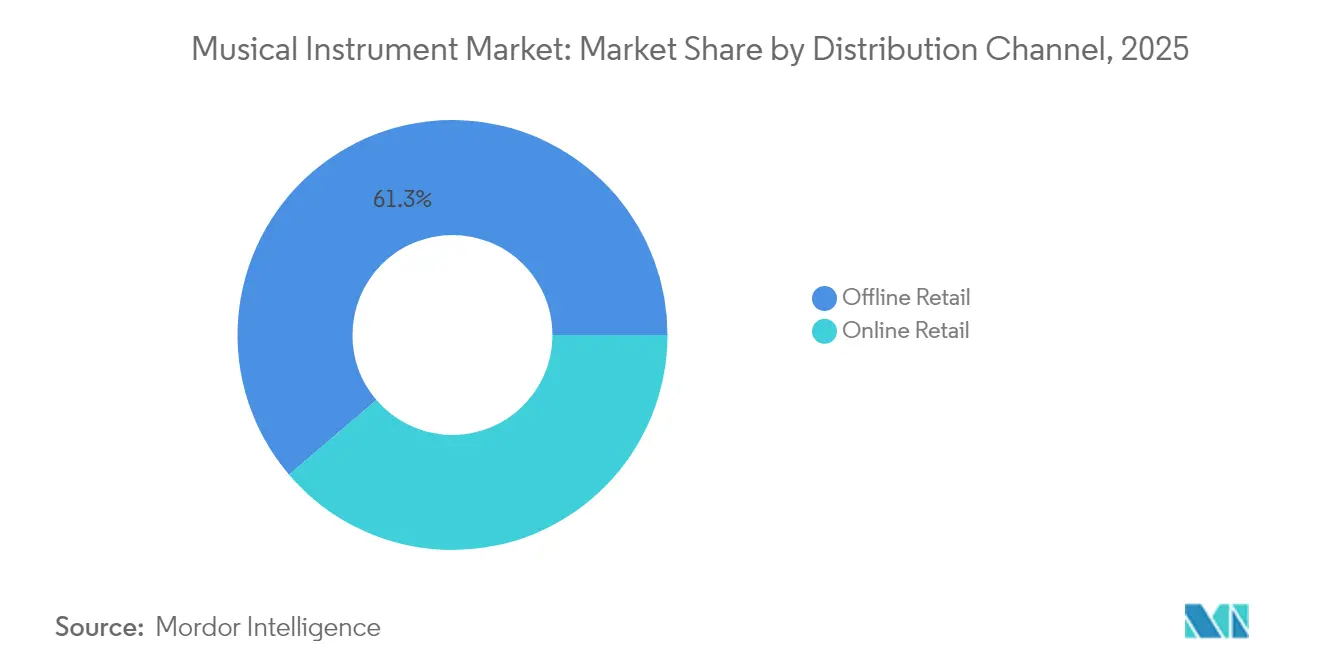

- By distribution channel, offline retail held 61.25% of the musical instrument market size in 2025, whereas online retail is forecast to expand at a 10.18% CAGR to 2031.

- By technology, acoustic instruments captured 54.55% of musical instrument market share in 2025; hybrid/smart instruments are expected to post the fastest 12.12% CAGR between 2026-2031.

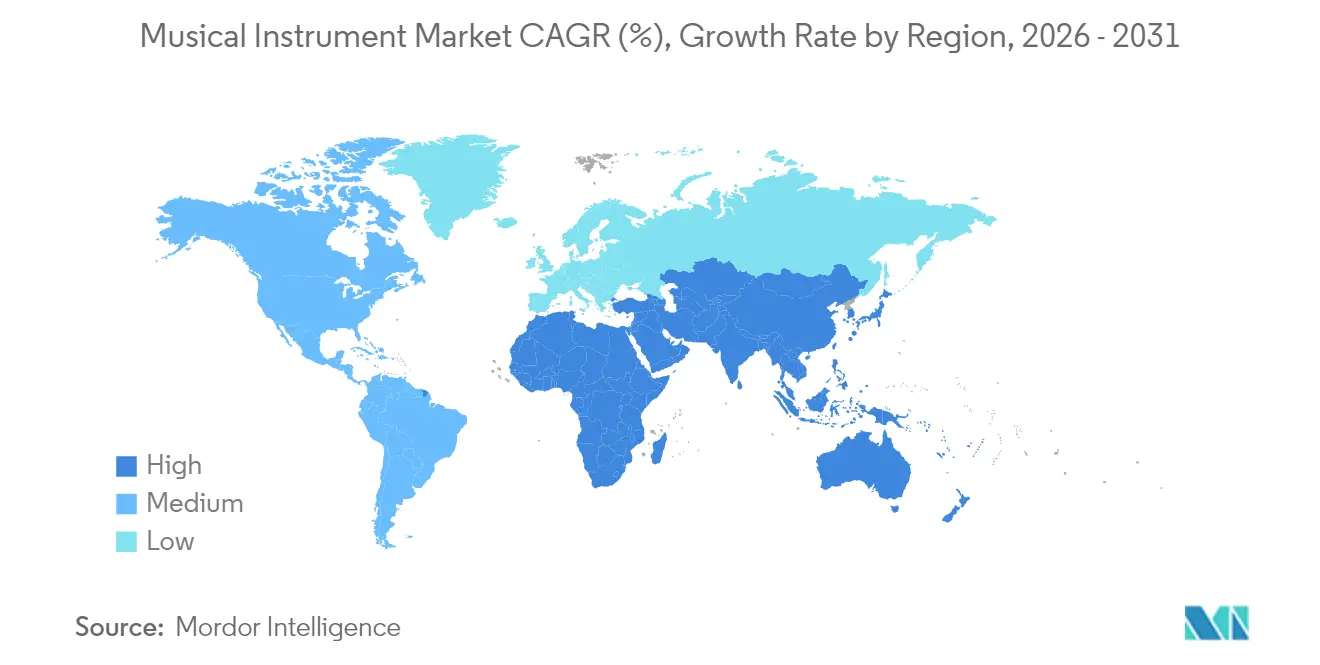

- By geography, Asia commanded 33.45% revenue share in 2025, but the Middle East is set to register the strongest 7.72% CAGR to 2031.

- Yamaha maintained about 50% share of digital pianos and portable keyboards in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Musical Instrument Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Subscription-Based Remote Music Learning Platforms | +1.20% | North America and Europe | Medium term (2-4 years) |

| Chinese Middle-Class Income Growth Accelerating Acoustic Piano Sales | +0.80% | Asia-Pacific (China focus) | Short term (≤2 years) |

| Social-Media-Driven “Bedroom Producer” Culture Boosting MIDI Controller Demand | +0.90% | Global, youth demographics | Short term (≤2 years) |

| Government-Backed Music-Education Mandates in Nordics and South Korea | +0.70% | Europe and Asia-Pacific | Long term (≥4 years) |

| Eco-Friendly Tonewoods and Circular-Luthier Programs Differentiating Premium Guitars | +0.40% | Global, premium segments | Long term (≥4 years) |

| IoT-Enabled Smart Instruments Creating Recurring Revenue Streams | +1.10% | Global, tech-forward markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Subscription-Based Remote Music Learning Platforms

Subscription-centric learning portals have dismantled geographical and economic barriers, heightening first-time purchases of entry-level keyboards and guitars across North America and Europe. Yamaha’s School Project alone has connected with more than 3 million children, expanding its funnel for digital and acoustic starter models. [1]Yamaha Corporation, “Ⅳ. Strategies by Business and Function,” yamaha.com Recurring fees motivate platform owners to continuously refresh curricula, keeping learners engaged and nudging periodic instrument upgrades. The alignment between structured lessons and instrument replacement cycles accelerates revenue stability for manufacturers. Moreover, data exhaust from these platforms furnishes granular insights into play patterns, narrowing feedback loops on product design. Together, these dynamics fuel sustained tailwinds for the musical instrument market.

Government-Backed Music-Education Mandates in Nordics and South Korea

Nordic governments and South Korea now embed multi-year funding for music into school budgets, anchoring predictable procurement of durable, education-grade instruments. England’s Music Opportunities Pilot allocates GBP 5.8 million (USD 7.89 million) to supply lessons, instruments, and examinations for disadvantaged students. [2]Department for Education, “Music pilot launched to help break down barriers to opportunity,” gov.uk In the United States, California’s Proposition 28 dedicates 1% of K-12 Proposition 98 monies to arts, reserving at least 80% for certified staff. [3]California Department of Education, “Proposition 28—Arts and Music in Schools Funding,” cde.ca.gov Such mandates smooth order visibility for producers, yet skew specifications toward ruggedness and cost-efficiency over premium sound. Manufacturers thus balance feature sets to meet institutional price points while preserving margins.

Social-Media-Driven “Bedroom Producer” Culture Boosting MIDI Controller Demand

TikTok, YouTube Shorts, and Twitch streams showcase compact workstations lit by RGB pads, spurring demand for MIDI controllers that fit small desks and photograph well on camera. Young creators often bypass formal training, valuing production flexibility over performance finesse. Collaborations between AI labs and artists like Jordan Rudess demonstrate real-time human-machine co-creation, widening appeal for MIDI gear integrated with intelligent software and digital audio workstation tools. [4]MIT Generative AI, “Developing Symbiotic Virtuosity: AI-Augmented Musical Instruments and Their Use in Live Music Performances,” mit-genai.pubpub.org Aesthetics, portability, and plug-and-play connectivity thus outweigh traditional build materials, shifting R&D budgets toward industrial design and firmware updates.

IoT-Enabled Smart Instruments Creating Recurring Revenue Streams

Embedding sensors and wireless modules transforms one-off product sales into service ecosystems. Adaptive pipa prototypes now maintain pitch accuracy within ±0.1 Hz regardless of humidity shifts, transmitting performance data with 98% integrity. Subscription dashboards offer analytics, firmware upgrades, and personalized practice regimens, monetizing usage long after checkout. For schools, automatic diagnostics reduce maintenance downtime; for gigging artists, predictive alerts prevent mid-show failures. This linkage of hardware, software, and cloud services is expanding average revenue per user, underscoring why the musical instrument market continues to tilt toward hybrid-smart formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scarcity of CITES-Regulated Tonewoods Disrupting High-End Guitar Supply | -0.90% | Global, premium segments | Long term (≥4 years) |

| Import Tariffs on Finished Instruments in Brazil and Argentina | -0.30% | South America | Medium term (2-4 years) |

| Shift to Software-Only Virtual Instruments Reducing Entry-Level Keyboard Demand | -1.10% | Global, entry-level segments | Short term (≤2 years) |

| Fragmented After-Sales Networks in Africa Constraining Electronic Drum Adoption | -0.20% | Africa, electronic segments | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Scarcity of CITES-Regulated Tonewoods Disrupting High-End Guitar Supply

Despite the 2024 easing for certain rosewood items under 10 kg, Brazilian Dalbergia remains tightly controlled, squeezing supplies for boutique luthiers and mass-market brands alike. Gibson and Martin now source FSC-certified alternatives, yet buyers often equate heritage timbers with tonal authenticity, limiting substitution elasticity. Resulting cost inflation narrows margins or pushes retail prices higher, dampening demand among aspirational amateurs. The premium guitar corridor therefore faces lingering volatility that tempers the otherwise upbeat musical instrument market trajectory.

Shift to Software-Only Virtual Instruments Reducing Entry-Level Keyboard Demand

Streaming synth plug-ins and realistic sample libraries give bedroom producers a near-infinite palette for under USD 200, undercutting sub-USD 500 hardware keyboards. Space-constrained urban dwellers often prefer virtual setups, citing easier updates and zero maintenance. Manufacturers counter with weighted keybeds, onboard speakers, and premium all-in-one workstations, effectively reallocating R&D toward mid- and high-tier SKUs. The practical effect is a contraction in low-margin volume streams, slowing overall unit growth even as value growth remains positive for the musical instrument market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Electronic Instruments Drive Innovation

String instruments delivered 27.45% of musical instrument market share in 2025, underscoring their foundational place across genres. In contrast, the electronic cohort led segment expansion with an 8.78% CAGR tailwind, propelled by rising demand for MIDI controllers, digital pianos, and electronic drums. Hybrid guitars that blend piezo pickups with modeled amplifiers have blurred acoustic-electric borders, appealing to live performers who need tonal versatility without pedalboard clutter. CITES-related tonewood scarcities prompted wider adoption of 3D-printed bridges and responsibly harvested pau ferro, keeping production lines fluid despite regulatory friction. Meanwhile, violin, viola, and cello categories benefit from conservatory programs, though growth remains modest relative to electronics.

Electronic innovation is also reshaping percussion. Apartment dwellers and content creators gravitate toward mesh-head kits with Bluetooth, satisfying both noise restrictions and mobile creativity. The infusion of sample libraries into hardware modules allows drummers to blend acoustic strikes with EDM layers on the fly. Above all, demand interplay between heritage craftsmanship and digital enhancement supports balanced portfolio strategies, illustrating why both traditional and electronic lines remain central pillars of the musical instrument market.

By Distribution Channel: Digital Transformation Accelerates

Offline showrooms still contributed 61.25% of 2025 revenue, signaling that play-before-pay remains critical. Hands-on trials help consumers judge resonance, key action, and ergonomics—elements hard to gauge through screens. Independent retailers leverage repair services, personalized setups, and community events to defend footfall. Yet online storefronts booked a 10.18% CAGR, buoyed by friction-less checkout, richer product videos, and improved logistics. Direct-to-consumer flagship sites from brands such as Yamaha knit physical and virtual paths, offering AI-guided tone matching and appointment-based in-store pickups.

Marketplace growth also reshapes accessories. Strings, reeds, and cases migrate easily to e-commerce baskets, often bundled as subscription replenishments. Counterfeit risks persist: U.S. customs officers seized 3,000 fake Gibson guitars in 2024. To reassure shoppers, brands are deploying NFC tags for instant authenticity checks. Over time, these safeguards could lift digital trust, gradually nudging higher-value segments online and extending the reach of the musical instrument market.

By Technology: Smart Instruments Reshape Traditional Categories

Acoustic formats comprised 54.55% of 2025 sales, affirming their irreplaceable timbre and tactile charm. Smart hybrids, however, are forecast to sprint at 12.12% CAGR, illustrating the appeal of embedded metronomes, auto-tuning, and companion apps. Roland’s new Future Design Lab concentrates resources on melding acoustic feel with cloud connectivity, underlining how R&D is gravitating toward cross-disciplinary engineering.

Digital pianos bridge usability gaps for learners lacking space or budget for grands, while advanced sample modeling narrows sonic gaps. For orchestral musicians, pickup-equipped violins stream latency-free signals to digital audio workstations, expanding tonal palettes without forsaking wood resonance. Collectively, these innovations keep legacy segments relevant while unlocking fresh monetization layers, underpinning robust value growth for the musical instrument market.

Geography Analysis

Asia generated 33.45% of 2025 revenue, sustained by Japan’s innovation leadership and a dense supplier ecosystem. Yet Chinese piano makers Pearl River and Hailun posted respective 31.47% and 21.99% revenue declines in 2023, reflecting softening middle-class sentiment and shifting parental priorities away from costly piano lessons. South Korea and Singapore counterbalance with government support, anchoring steady classroom demand. India’s rising disposable income and widespread smartphone adoption offer fertile ground for app-linked guitars and keyboards, though import duties still constrain price competitiveness.

North America remains a premium outpost. Gibson, Fender, and Taylor command loyalty among hobbyists and touring artists, while classical education keeps orchestral instrument turnover steady. Yet acoustic piano shipments fell to fewer than 18,000 units in 2024, eclipsed by 188,000 digital pianos that cater to apartment dwellers. California’s Proposition 28 secures ongoing school budgets, stabilizing low-to-mid price tiers.

The Middle East leads growth at 7.72% CAGR on the back of national cultural initiatives and expanding youth populations. Concert halls in Dubai, Riyadh, and Doha now specify smart stage pianos and modular PA rigs, fostering spill-over demand for practice instruments. Europe shows moderate but steady momentum. Germany’s orchestral heritage sustains wind-instrument factories, while the Nordics channel public funds into school music kits that emphasize sustainability and digital integration. South America’s potential remains tempered by Brazil’s and Argentina’s import tariffs, nudging local assembly operations but keeping prices elevated.

Mordor Intelligence provides coverage of the musical instrument market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

Market structure is moderately consolidated. Yamaha’s multi-category breadth, plus roughly 50% share in digital pianos and portable keyboards, positions it as the reference player. Its USD 50 million Silicon Valley CVC underscores a strategic push to harness start-ups in AI composition, haptic feedback, and immersive audio. Gibson leans on brand legacy and artist endorsements while exploring augmented-reality practice tools. Roland focuses on sensor fusion and cloud analytics, exemplified by its Future Design Lab.

M&A reshaped the landscape in 2024-2025. Marshall Group sold a majority stake to HongShan Capital for EUR 1.1 billion (USD 1.29 billion), unlocking funds for e-commerce and supply-chain optimizations. Hal Leonard merged with Muse Group, combining sheet-music catalogs with platforms such as MuseScore and Ultimate Guitar, creating pervasive reach among educators and DIY producers. Warner Music’s acquisition of Tempo Music Investments added marquee song rights, intensifying competition around intellectual-property portfolios.

Competitive priorities now center on hybrid product pipelines, direct digital engagement, and ESG-oriented sourcing. Firms that blend acoustic craftsmanship with embedded tech, validated supply chains, and persuasive community content are best placed to capitalize on forthcoming expansion in the musical instrument market.

Musical Instrument Industry Leaders

Yamaha Corporation

Fender Musical Instruments Corporation

Gibson Brands, Inc.

Roland Corporation

Steinway & Sons

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Hal Leonard completed its combination with Muse Group, creating a unified global digital publishing powerhouse that reaches 300 million annual visitors.

- March 2025: Hal Leonard joined forces with Muse Group through Francisco Partners investment to expand digital capabilities.

- February 2025: Warner Music Group acquired a controlling stake in Tempo Music Investments, securing rights to catalogs from Bruno Mars and Adele.

- January 2025: Marshall Group AB sold a majority stake to HongShan Capital Group for EUR 1.1 billion.

Global Musical Instrument Market Report Scope

The musical instrument market encompasses the production, distribution, and sale of instruments used to create music across various genres and skill levels. It includes traditional instruments like pianos, guitars, and violins, as well as modern electronic instruments such as synthesizers and digital keyboards. The market is driven by factors such as increasing interest in music education, advancements in technology, and the growing popularity of live performances and home music production.

The Musical Instrument Market is Segmented by product type (string instruments, wind instruments, percussion instruments, keyboard instruments, electronic instruments, accessories, other product types), distribution channel (online retail, offline retail), technology (digital instruments, acoustic instruments, hybrid instruments), and geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| String Instruments | Guitars |

| Violins, Violas, Cellos | |

| Harps and Others | |

| Wind Instruments | Brass |

| Woodwind | |

| Percussion Instruments | Acoustic Drums |

| Electronic Drums and Pads | |

| Keyboard Instruments | Acoustic Pianos |

| Digital Pianos and Stage Pianos | |

| MIDI Controllers and Synthesizers | |

| Electronic Instruments | DJ Controllers and Turntables |

| Samplers and Workstations | |

| Accessories | Pedals and Effects |

| Strings, Reeds and Sticks | |

| Cases and Bags | |

| Other Product Types |

| Offline Retail | Independent Music Stores |

| Specialty Chains | |

| Online Retail | Direct-to-Consumer Brand Stores |

| E-commerce Marketplaces |

| Acoustic Instruments |

| Digital Instruments |

| Hybrid/Smart Instruments |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | String Instruments | Guitars |

| Violins, Violas, Cellos | ||

| Harps and Others | ||

| Wind Instruments | Brass | |

| Woodwind | ||

| Percussion Instruments | Acoustic Drums | |

| Electronic Drums and Pads | ||

| Keyboard Instruments | Acoustic Pianos | |

| Digital Pianos and Stage Pianos | ||

| MIDI Controllers and Synthesizers | ||

| Electronic Instruments | DJ Controllers and Turntables | |

| Samplers and Workstations | ||

| Accessories | Pedals and Effects | |

| Strings, Reeds and Sticks | ||

| Cases and Bags | ||

| Other Product Types | ||

| By Distribution Channel | Offline Retail | Independent Music Stores |

| Specialty Chains | ||

| Online Retail | Direct-to-Consumer Brand Stores | |

| E-commerce Marketplaces | ||

| By Technology | Acoustic Instruments | |

| Digital Instruments | ||

| Hybrid/Smart Instruments | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the musical instrument market?

The musical instrument market size was USD 53.7 billion in 2026 and is forecast to rise to USD 73.48 billion by 2031.

Which region is growing the fastest?

The Middle East shows the highest growth momentum, projected at a 7.72% CAGR through 2031.

How are smart instruments influencing demand?

IoT-enabled smart instruments convert one-time sales into subscription platforms, boosting recurring revenue and driving a 12.12% CAGR for the hybrid/smart segment.

What share do online channels hold?

Although online channels are expanding at 10.18% CAGR, offline retail still represents 61.25% of 2025 sales due to the tactile nature of instrument buying.

Which company leads in digital pianos?

Yamaha commands roughly 50% of global digital-piano and portable-keyboard shipments.

How are CITES regulations affecting guitar makers?

Tight controls on Brazilian rosewood restrict availability, raise material costs, and push brands toward certified alternatives, tempering premium-guitar growth.

Page last updated on: