Music Production and Recording Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

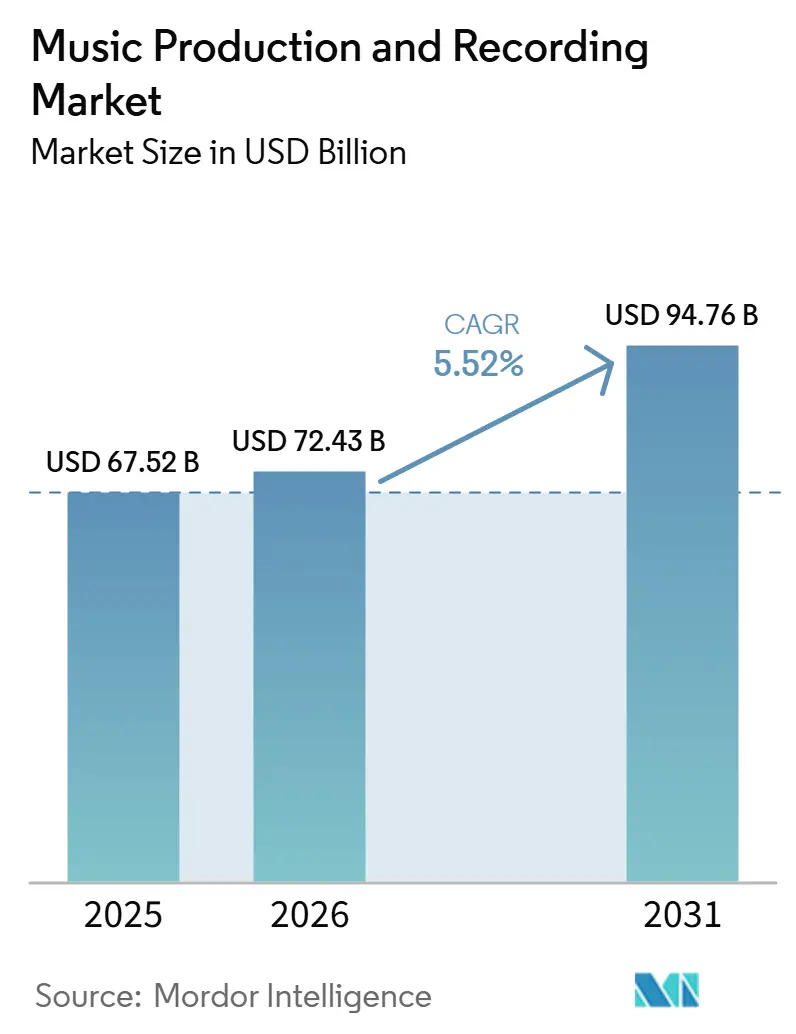

| Market Size (2026) | USD 72.43 Billion |

| Market Size (2031) | USD 94.76 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Music Production and Recording Market Analysis by Mordor Intelligence

The Music Production and Recording market size is projected to expand from USD 67.52 billion in 2025 and USD 72.43 billion in 2026 to USD 94.76 billion by 2031, registering a CAGR of 5.52% between 2026 to 2031. The music production and recording market is being shaped by the fast expansion of the creator economy, the wider use of AI-assisted production tools, and the steady move toward subscription access across software workflows. Demand is also shifting from fixed studio setups toward cloud-linked and modular production environments, which is changing how vendors package tools and how users adopt them. Competition now reflects a mix of established workstation providers, hardware ecosystems, and newer platforms that combine production, distribution, mastering, and collaboration in one offer. The music production and recording market also faces clear pressure from copyright uncertainty around AI training, piracy in high-growth regions, and workflow friction created by fragmented tool stacks. Even so, broader access to affordable tools and rising monetization opportunities for independent creators continue to support the market’s expansion over the forecast period.

Key Report Takeaways

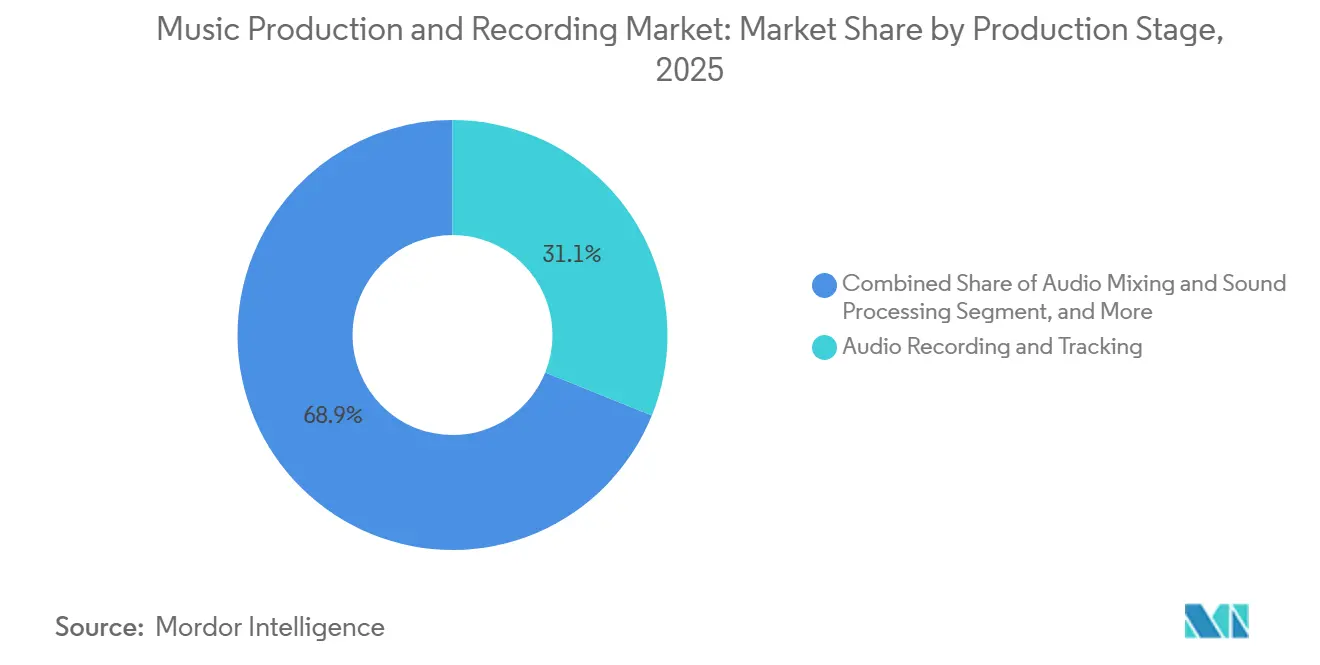

- By Production Stage, Audio Recording and Tracking held 31.11% of the music production and recording market share in 2025, while Audio Mixing and Sound Processing is projected to expand at an 11.32% CAGR through 2031.

- By Application, Commercial Music Production accounted for 51.73% of the music production and recording market size in 2025, while Gaming Audio Content is projected to grow at an 11.63% CAGR through 2031.

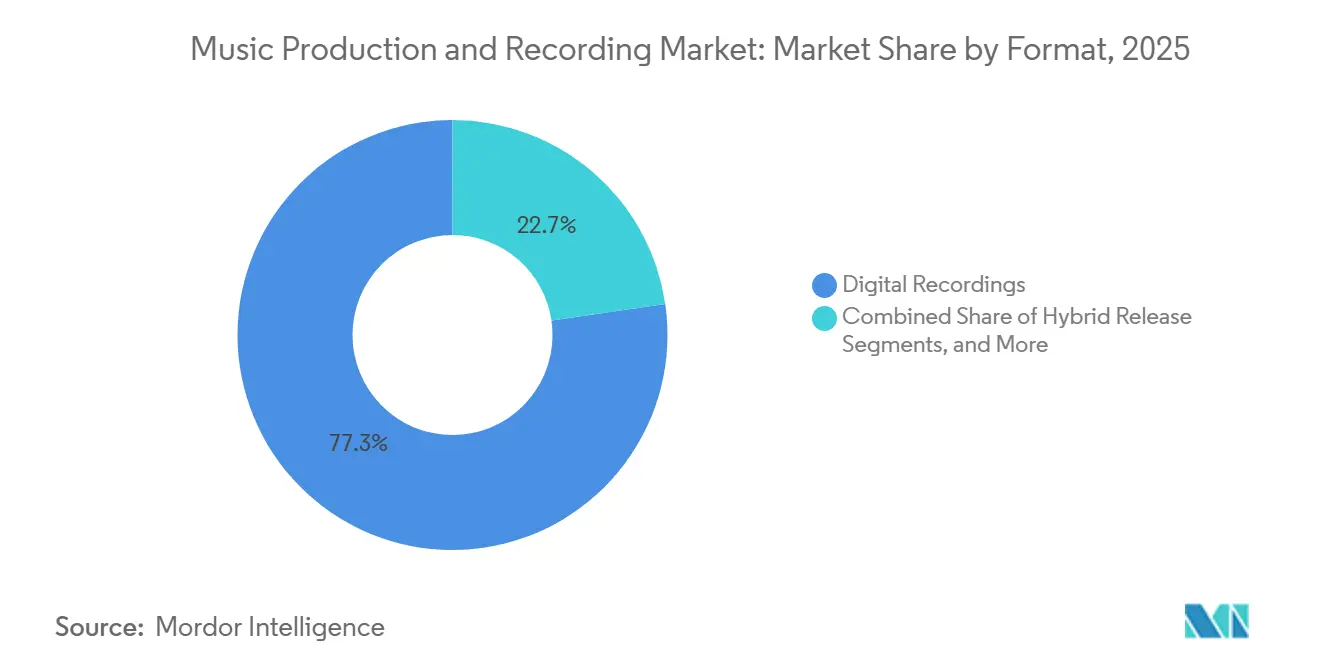

- By Formats, Digital Recordings led with a 77.31% share in 2025, while Hybrid Releases are projected to expand at a 13.48% CAGR through 2031.

- By End User, Enterprises and Professional users held 52.61% share in 2025, while Individual Consumers are projected to advance at a 12.46% CAGR through 2031.

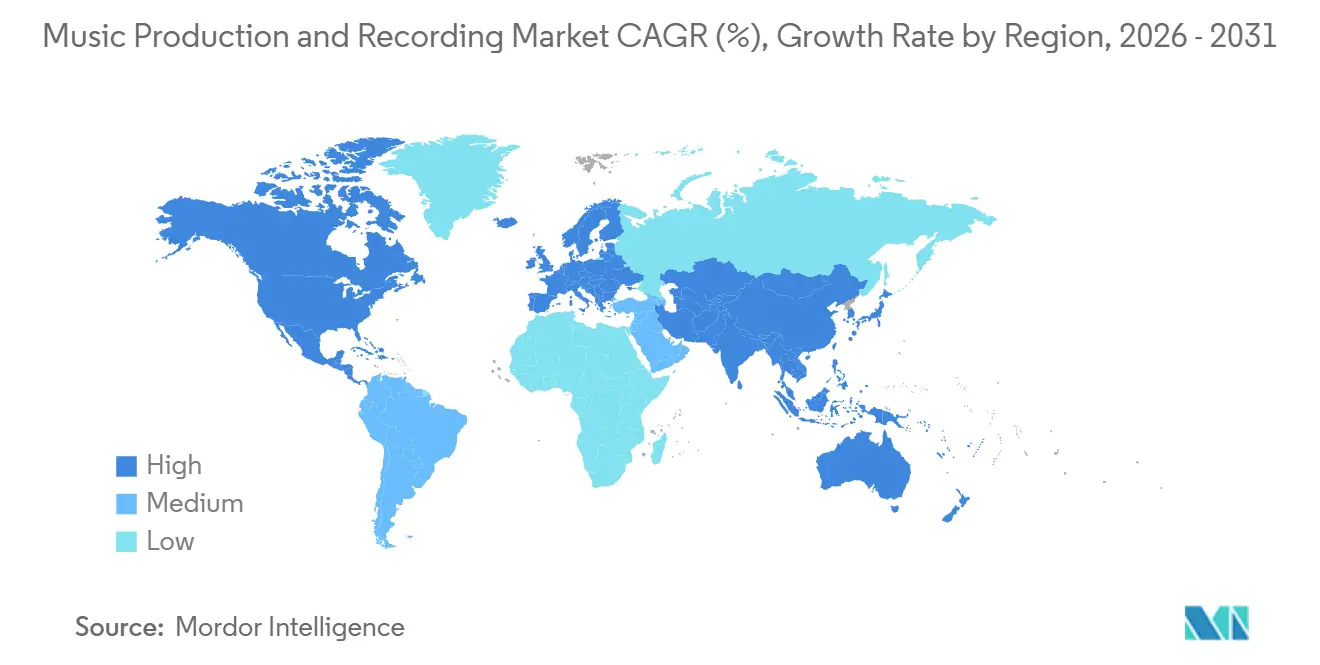

- By Geography, North America held 35.64% share in 2025, while Asia-Pacific is projected to grow at a 10.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Music Production and Recording Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Assisted Composition, Editing, and Mixing | +1.2% | Global, with early intensity in North America and Western Europe | Short term (≤ 2 years) |

| Rising Independent Creator Economy and DIY Artist Expansion | +1.0% | Global, with strongest pull in North America, South America, and Asia-Pacific | Medium term (2-4 years) |

| Subscription-Based Music Creation Tools | +0.7% | North America and Europe core, APAC spillover accelerating | Medium term (2-4 years) |

| Remote Collaboration Across Distributed Production Teams | +0.5% | Global, strongest in Europe and North America | Medium term (2-4 years) |

| Spatial Audio and Immersive Music Delivery | +0.4% | North America, South Korea, Japan, Western Europe | Long term (≥ 4 years) |

| Creator Monetization Through Short-Form Content Platforms | +0.3% | Global, with high intensity in North America, India, and South America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Assisted Composition, Editing, and Mixing is Reshaping Core Production Workflows

AI tools are now influencing composition, editing, mixing, and final delivery across the music production and recording market. This shift matters because it reduces manual effort in tasks that once required deeper technical experience and more studio time. Avid reflected this direction in May 2026 when Pro Tools 2026.4 added native MPEG-H support and Dolby Atmos Headphone Personalization in partnership with Fraunhofer IIS, which shows that advanced workflow features are moving into mainstream professional tools.[1]Avid Technology, “Avid Launches Pro Tools 2026.4,” Avid Press Room, avid.com Apple followed the same path when it launched Logic Pro 12 inside Apple Creator Studio in January 2026 with AI-powered Chord ID and the Synth Player Session tool, which widened access for entry and mid-tier creators without removing professional depth.[2]Apple Inc., “Introducing Apple Creator Studio, an Inspiring Collection of Creative Apps,” Apple Newsroom, apple.com The music production and recording market is, therefore, seeing AI move from an optional enhancement to a built-in layer of the production stack.

Rising Independent Creator Economy is Expanding Demand Across The Full Tool Chain

The rise of self-releasing artists is broadening demand across the music production and recording market, especially for affordable tools that still deliver professional output. Spotify stated in its Loud and Clear 2026 report that it paid the music industry more than USD 11 billion in 2025, and more than 13,800 artists each earned at least USD 100,000 annually from Spotify alone, which shows that independent careers are gaining real economic scale.[3]Spotify, “Loud and Clear 2026,” Spotify Newsroom, spotify.com That income pattern supports stronger spending on software, interfaces, monitors, and collaboration tools rather than only low-cost entry products. It also narrows the line between hobbyist creation and sustained commercial activity, which lifts demand across multiple workflow stages. The music production and recording market benefits because a larger share of users now sees production spending as part of an income-generating path rather than a one-time personal expense.

Subscription-Based Music Creation Tools are Lowering The Professional Access Barrier

Recurring access models are changing how users enter and stay in the music production and recording market. Apple Creator Studio launched in January 2026 at USD 12.99 per month or USD 129 per year, bundling Logic Pro for Mac and iPad with other creative tools and making a professional-grade environment easier to access for smaller creators and students. This model shifts competition away from one-time software purchases and toward retention, feature depth, and the ability to move users across adjacent services. It also supports a smoother upgrade path, because creators can adopt advanced tools earlier without a large initial payment. The music production and recording market is therefore seeing subscription design become part of product strategy, customer acquisition, and long-term monetization.

Remote Collaboration Across Distributed Production Teams is Creating Lasting Infrastructure Demand

Distributed work has become a stable feature of the music production and recording market rather than a temporary adjustment. Teams now often span composers, performers, engineers, and editors across several countries, which increases the value of cloud session management, low-latency transfer, and version control. IEEE research on 5G-enabled Internet of Musical Things architectures described technical foundations for remote immersive musical practices, which points to a longer-term shift toward richer real-time collaboration workflows. This matters because collaboration is no longer limited to exchanging files after recording, and is moving closer to synchronized production and monitoring. The music production and recording market gains from this shift because collaboration tools are becoming part of the core workflow infrastructure that users expect from higher-value platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI Content Rights Uncertainty | -0.8% | Global, Europe most acute due to DSM Directive and GEMA v OpenAI precedent | Short term (≤ 2 years) |

| Piracy and Unlicensed Software Use in Emerging Markets | -0.6% | APAC, Middle East and Africa, South America | Medium term (2-4 years) |

| Professional Studio Capital Expenditure Remains High | -0.5% | Global, most acute in Africa and South America | Long term (≥ 4 years) |

| Fragmented Toolchains Raise Switching Costs and Workflow Friction | -0.4% | Global, concentrated in enterprise and post-production segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

AI Content Rights Uncertainty is Slowing Enterprise Adoption

Copyright uncertainty around AI-generated and AI-trained music tools is acting as a clear brake on the music production and recording market. The US Copyright Office stated in its 2025 Part 3 report on generative AI training that licensing markets should be allowed to develop, while also noting that voluntary licensing is not always feasible, which leaves commercial users with limited clarity on how to proceed.[4]United States Copyright Office, “Copyright and Artificial Intelligence, Part 3: Generative AI Training,” United States Copyright Office, copyright.gov That uncertainty affects broadcasters, licensors, agencies, and larger studios more than casual users because enterprise buyers face heavier legal and reputational exposure. As a result, some high-value customers are likely to move more carefully on procurement even when the productivity upside is clear. The music production and recording market therefore faces a near-term limit on AI adoption speed in the part of the user base that usually supports higher average revenue per account.

Piracy and Unlicensed Software Use Continue to Limit Revenue Capture

Piracy remains a meaningful restraint on the music production and recording market in several fast-growth regions. IFPI documented continued digital piracy patterns in its Global Music Report 2025, and that matters because these same regions are also expected to add creator volume and new users over time. Unlicensed DAWs and cracked plugins weaken the link between creator growth and legitimate software revenue, especially where incomes are lower and enforcement is uneven. Free and low-cost cloud tools can reduce some of this pressure, but they do not fully replace demand for higher-capability professional software. The music production and recording market thus faces a persistent gap between potential usage growth and actual monetized demand in parts of Asia-Pacific, South America, the Middle East, and Africa.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Stage: Mixing Tools Gain Speed as Workflows Become More Software Led

Audio recording and tracking held 31.11% share in 2025, which kept it as the largest production stage in the music production and recording market because every downstream process still depends on capture quality and stable DAW session foundations. This stage continues to benefit from demand for microphones, interfaces, preamps, and core recording software, even as more creators shift away from large commercial studios. Pre-production and creative development remain smaller in revenue terms, but they are gaining importance because early-stage idea creation is becoming faster and more iterative. That shift supports tools that help users sketch arrangements, test harmonies, and move quickly from idea to session without extending studio setup time.

Audio mixing and sound processing is projected to grow at an 11.32% CAGR through 2031, giving it the fastest expansion within the production stage view of the music production and recording market. Avid strengthened this part of the workflow in May 2026 with Pro Tools 2026.4 and native MPEG-H integration developed with Fraunhofer IIS, which improved support for immersive and object-based delivery. The faster growth rate reflects how mixing is now where automation, immersive delivery, and software-driven enhancement are converging most directly. The music production and recording industry is also seeing this stage pull in a wider user base, because AI-assisted tools reduce the time and skill once needed for tasks such as leveling, spatial placement, and corrective processing.

By Application: Commercial Production Holds The Lead While Gaming Audio Adds New Demand

Commercial music production accounted for 51.73% of the music production and recording market size in 2025, which shows that the largest demand pool still comes from users producing for direct music release, catalog development, and recurring commercial output. This segment continues to absorb spending on full-featured software, plugin suites, monitoring systems, and interface upgrades because reliability and delivery quality remain essential. Film and television soundtracks and advertising and brand audio also support demand, since both rely on controlled workflows, revision capacity, and consistent post-production standards. Other applications add useful volume to the broader base, including podcasting, sports audio, and live-related production tasks that increasingly overlap with music workflows.

Gaming audio content is projected to grow at an 11.63% CAGR through 2031, making it the fastest-growing application in the music production and recording market. That rise reflects stronger demand for immersive sound design, adaptive audio, and higher production budgets in interactive media. Apple reinforced cross-workflow relevance when Logic Pro updates in 2025 expanded production capabilities that support more flexible beat making and editing use cases across modern content formats. The music production and recording industry is therefore seeing game-related workflows become a more important pull factor for advanced editing, mixing, and delivery features. This creates room for vendors that can serve both traditional music release work and interactive audio creation inside one environment.

By Formats: Digital Output Dominates While Hybrid Releases Support Premium Positioning

Digital recordings held 77.31% share in 2025, which made them the leading format in the music production and recording market, as streaming-ready delivery remained the standard commercial output across both major and independent creators. This dominance reflects the practical need for fast distribution, easy metadata handling, and compatibility with platform-led discovery models. Physical recordings still retain relevance, especially where collector demand and format loyalty remain strong in established music economies. The Recording Industry Association of Japan reported that Japan’s physical music software market generated JPY 228.8 billion in 2025, which, when converted to approximately USD 1.53 billion, confirms that physical output still carries economic weight in selected markets.

Hybrid releases are projected to advance at a 13.48% CAGR through 2031, giving them the fastest format growth in the music production and recording market. This pattern reflects demand for releases that combine digital convenience with premium physical or interactive elements that can support higher spending by committed audiences. It also changes production requirements because creators and labels need tools that can manage high-resolution masters, alternate delivery formats, and packaging-ready assets inside one workflow. The music production and recording market share of purely digital distribution remains dominant, but hybrid growth shows that premium positioning is increasingly tied to how creators package content rather than only how they distribute it.

By End User: Professional Demand Leads While Prosumer Upgrading Gains Momentum

Enterprises and professional users held 52.61% share in 2025, which kept them as the largest end-user group in the music production and recording market because studios, agencies, broadcasters, and post-production facilities continue to purchase high-value hardware, software, and support packages. Their spending supports premium workstation tiers, larger control surfaces, advanced routing systems, and more formal service contracts. This user group also tends to stay inside established ecosystems for longer periods because switching costs remain high once teams, archives, and training paths are built around specific platforms. That gives incumbent vendors durable revenue support even as new creators enter through lower-cost tools.

Individual consumers are projected to grow at a 12.46% CAGR through 2031, which makes them the fastest-rising end-user group in the music production and recording market. Spotify stated in 2026 that more than a third of artists earning at least USD 10,000 in annual Spotify royalties in 2025 were DIY or started that way, which shows that independent creation is converting into sustained income more often than before. Yamaha also targeted this migration path in January 2026 with the URX Series audio interfaces and the CC1 USB DAW controller, aimed at musicians, streamers, and content creators moving toward more advanced setups. The result is a shorter path from casual experimentation to serious production investment, which broadens the spending base of the music production and recording market without removing the importance of enterprise accounts.

Geography Analysis

North America held 35.64% share in 2025, which made it the largest regional block in the music production and recording market. The region benefits from a dense mix of major labels, software developers, post-production facilities, and premium studio hardware ecosystems. It also remains important because many global workflow standards are set by companies with a strong North American presence, including Apple, Avid, and Universal Audio. The region is likely to keep its leadership position through the forecast period as AI-led upgrades, subscription-based access, and creator monetization continue to reinforce demand across professional and prosumer users.

Europe remained a core region within the music production and recording market in 2025 because it combines a mature infrastructure base with strong specialized demand in electronic music, broadcast production, and studio software. The region benefits from established production centers in the United Kingdom, Germany, and the Nordic countries, where software and hardware adoption has stayed structurally strong. Europe also matters because product development and standards-focused workflow innovation continue to have a visible presence there. The US Copyright Office discussion on licensing feasibility in the AI training debate shows why regulatory clarity remains important for vendors serving commercial users across advanced markets, including Europe. As a result, Europe supports stable demand, but it also places more weight on compliance, rights management, and platform transparency than some emerging regions do.

Asia-Pacific is projected to grow at a 10.41% CAGR through 2031, making it the fastest-growing region in the music production and recording market. This growth is supported by K-pop’s scaled production model, a wider independent artist base in India and Southeast Asia, and the continued coexistence of physical and digital demand in Japan. The Recording Industry Association of Japan reported that Japan’s full-year record market reached JPY 398.8 billion in 2025, which the input converted to approximately USD 2.66 billion, while streaming subscriptions rose to JPY 137.7 billion, which the input converted to approximately USD 919 million. That combination shows why the region remains commercially varied rather than dependent on one release model. South America and the Middle East and Africa add a different layer to the music production and recording market because creator adoption is rising faster than infrastructure depth, which increases demand for affordable tools, lighter cloud workflows, and better monetization pathways.

Competitive Landscape

The music production and recording market remains moderately fragmented, with competition spread across enterprise systems, mid-market software, creator platforms, and hardware-led ecosystems. Avid, Apple, and Ableton have continued to hold strong positions at the professional end because they benefit from embedded workflows, training familiarity, and large installed user bases. At the same time, newer and more flexible platforms are trying to pull users through lower entry costs, cloud access, and faster onboarding. This means the music production and recording market is not dominated by one single vendor model, and success now depends on how well companies connect creation, editing, delivery, and monetization.

Strategic moves in 2026 showed that platform bundling and workflow expansion are central competitive tools in the music production and recording market. Apple launched Creator Studio in January 2026 and bundled Logic Pro into a broader subscription offer, which strengthened its position with users who work across music, video, and visual content. LANDR also acquired Reason Studios in January 2026, combining AI-powered production and mastering capabilities with one of the more established modular DAW brands. Avid then reinforced the professional tier in May 2026 through Pro Tools 2026.4, using immersive and broadcast-grade workflow support to keep enterprise and advanced studio users inside its ecosystem. These moves show that vendors are competing not only on tool quality, but also on how much of the full production path they can cover inside one commercial relationship.

Hardware-linked ecosystem expansion also remains important in the music production and recording market. Yamaha’s January 2026 launch of the MGX Digital Mixer Series, URX Series interfaces, and the CC1 USB DAW controller showed how hardware makers are positioning themselves around creators, streamers, and hybrid users rather than only traditional musicians. Samsung’s relevance in this space remains tied to Harman’s professional audio portfolio, which extends its reach into studio and broadcast equipment rather than software-led creation alone. Fender remains more peripheral, but its connected instrument and modeling software position still gives it a defensible link to recording workflows. The competitive picture therefore supports a market where ecosystem breadth, workflow continuity, and user retention matter as much as individual product features.

Music Production and Recording Industry Leaders

Avid Technology, Inc.

Adobe Inc.

Apple Inc.

Steinberg Media Technologies GmbH

Ableton AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Yamaha launched the refreshed ARIUS Series 88-key weighted digital pianos (models YDP-146, YDP-166, YDP-S36, YDP-S56), priced from USD 1,199 to USD 1,699, featuring a newly developed keyboard and speaker system designed for home studio and educational recording environments.

- May 2026: Avid released Pro Tools 2026.4 with native MPEG-H immersive broadcast standard support developed in partnership with Fraunhofer IIS, Dolby Headphone Personalization for Atmos mixing, and enhanced AI Speech-to-Text workflows. The update positions Pro Tools as the first major commercial DAW to support both MPEG-H and Dolby Atmos natively.

- January 2026: Apple launched Logic Pro 12 as part of Apple Creator Studio on January 28, 2026, introducing AI-powered Chord ID, the Synth Player Session tool, MIDI 2.0 display, and a new Sound Library with royalty-free loops and samples. The Creator Studio subscription is priced at USD 12.99 per month or USD 129 per year.

- January 2026: LANDR Audio acquired Stockholm-based Reason Studios, makers of the Reason DAW and Reason Rack, for an undisclosed sum, bringing together AI-powered production, distribution, and mastering tools with one of the industry’s most recognized modular DAW architectures.

Global Music Production and Recording Market Report Scope

The Music Production and Recording Report is Segmented by Production Stage (Pre-Production and Creative Development, Audio Recording and Tracking, Audio Mixing and Sound Processing, Audio Mastering and Editing, and Post-Production Support), Application (Commercial Music Production, Film & Television Soundtracks, Advertising & Brand Audio, Gaming Audio Content, and Other Applications), Formats (Digital Recordings, Physical Recordings, Special Edition & Collector Formats, and Other Formats), End User (Individual Consumers, Enterprises and Professional Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). Forecasts in Value (USD).

| Pre-Production and Creative Development |

| Audio Recording and Tracking |

| Audio Mixing and Sound Processing |

| Audio Mastering and Editing |

| Post-Production Support |

| Commercial Music Production |

| Film and Television Soundtracks |

| Advertising and Brand Audio |

| Gaming Audio Content |

| Other Applications |

| Digital Recordings |

| Physical Recordings |

| Hybrid Releases |

| Special Edition and Collector Formats |

| Other Formats |

| Individual Consumers |

| Enterprises and Professional Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Production Stage | Pre-Production and Creative Development | |

| Audio Recording and Tracking | ||

| Audio Mixing and Sound Processing | ||

| Audio Mastering and Editing | ||

| Post-Production Support | ||

| By Application | Commercial Music Production | |

| Film and Television Soundtracks | ||

| Advertising and Brand Audio | ||

| Gaming Audio Content | ||

| Other Applications | ||

| By Formats | Digital Recordings | |

| Physical Recordings | ||

| Hybrid Releases | ||

| Special Edition and Collector Formats | ||

| Other Formats | ||

| By End User | Individual Consumers | |

| Enterprises and Professional Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the music production and recording market?

The music production and recording market stood at USD 72.43 billion in 2026 and is forecast to reach USD 94.76 billion by 2031 at a 5.52% CAGR.

Which application area leads revenue generation?

Commercial music production led with 51.73% share in 2025, which shows that direct music release workflows still account for the largest spending base.

Which format is growing the fastest through 2031?

Hybrid releases are projected to grow at a 13.48% CAGR through 2031, even though digital recordings remained dominant with 77.31% share in 2025.

Why is Asia-Pacific important for future expansion?

Asia-Pacific is projected to grow at a 10.41% CAGR through 2031, supported by K-pop scale, a wider independent artist base, and Japans strong physical and digital mix.

Page last updated on: