Liquid Soap Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

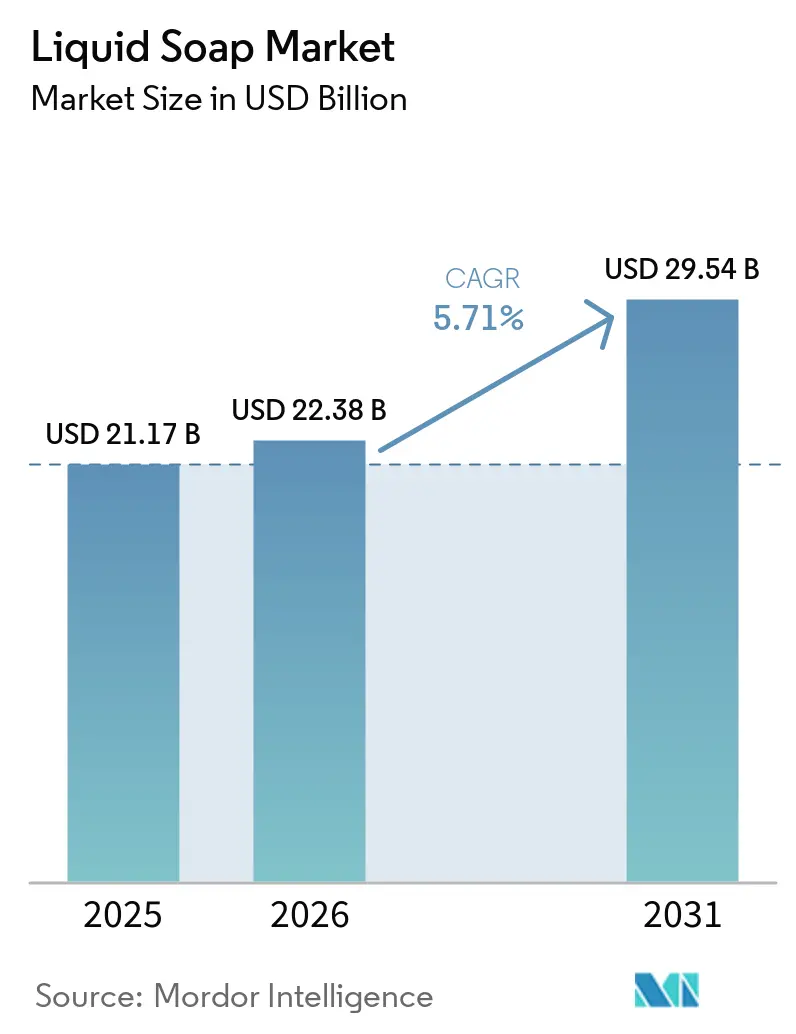

| Market Size (2026) | USD 22.38 Billion |

| Market Size (2031) | USD 29.54 Billion |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

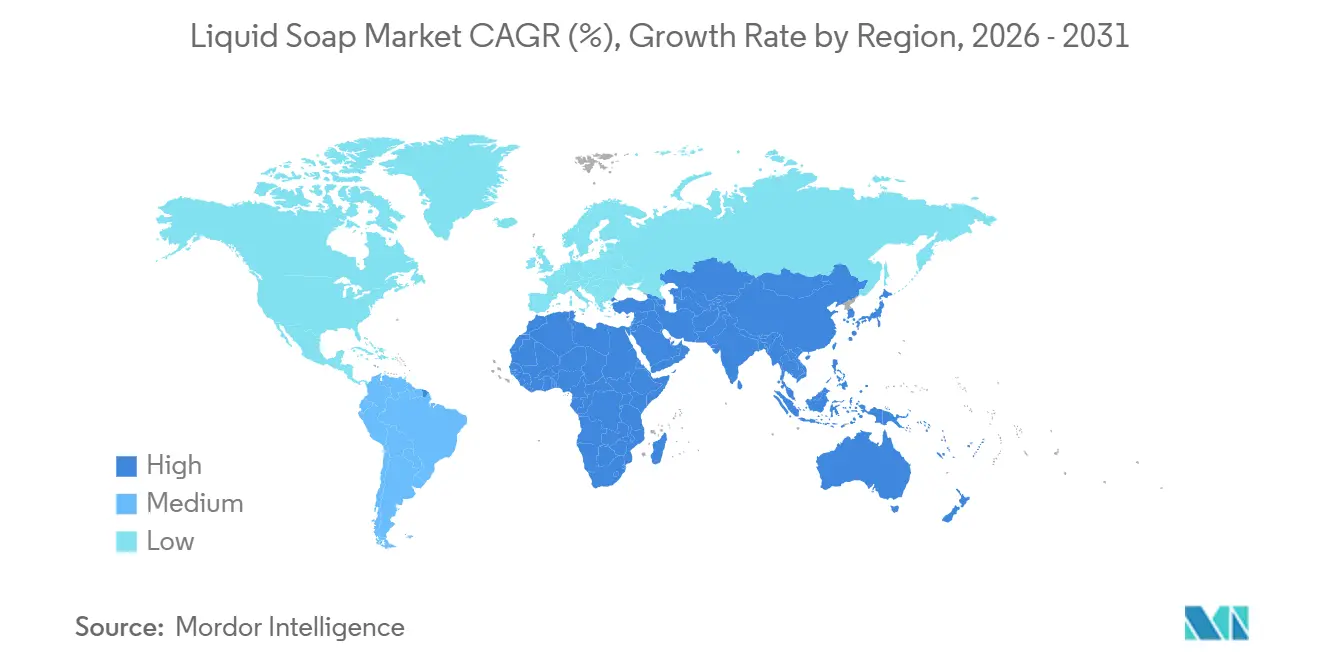

| Fastest Growing Market | North America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Liquid Soap Market Analysis by Mordor Intelligence

The liquid soap market size is expected to increase from USD 21.2 billion in 2025 to USD 22.4 billion in 2026 and reach USD 29.5 billion by 2031, growing at a CAGR of 4.9% over 2026-2031. As consumers increasingly favor pumps and dispensers over traditional bars for their cleaner, more convenient use, the liquid soap market is witnessing notable growth. This surge is further fueled by brands emphasizing skincare benefits in their hand and body washes, focusing on moisture support and skin comfort rather than just cleansing. A 2025 Barrows survey, highlighted by Method, revealed that 83% of participants prioritize skincare and wellness benefits in their hand soap choices. This trend bolsters the industry's shift towards premium formulas and dermatologist endorsements. Additionally, the market's growth is buoyed by the rising adoption of refills, online product discovery, and heightened institutional demand. However, fluctuations in resin and surfactant costs are exerting pressure on profit margins across various value tiers. While the competitive landscape remains moderately fragmented, allowing major consumer goods companies to leverage scale advantages, there's still ample opportunity for regional specialists and premium brands to carve out their niche through innovative formulations, packaging, and strategic channel execution.

Key Report Takeaways

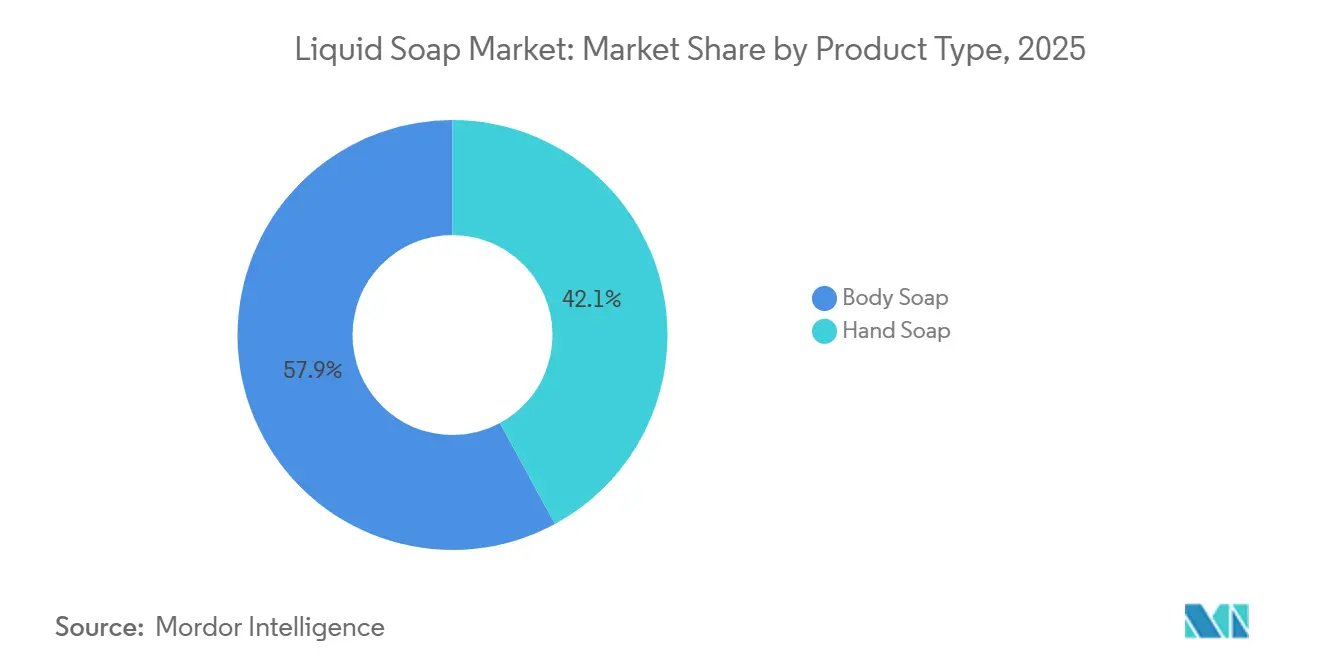

- By product type, hand soap held 42.1% of the liquid soap market share in 2025, while body soap is projected to grow at a 6.8% CAGR through 2031.

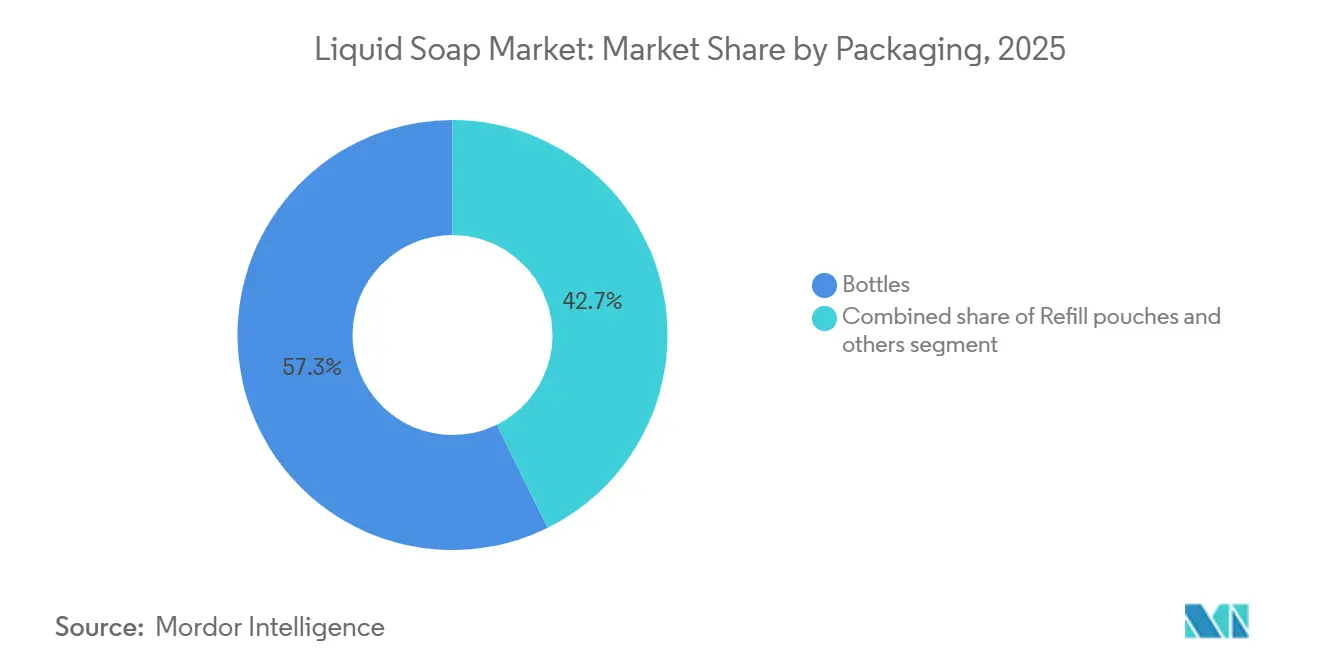

- By packaging, bottles accounted for 57.3% of the global liquid soap market size in 2025, while refill pouches are forecast to expand at a 6.9% CAGR through 2031.

- By ingredient, conventional formulations represented 71.1% share in 2025, while the free-from segment is set to advance at a 5.2% CAGR through 2031.

- By consumer group, adults made up 87% share in 2025, while kids and children are expected to record a 6.6% CAGR through 2031.

- By distribution channel, supermarkets and hypermarkets held 39% share in 2025, while online retail is projected to grow at a 6.3% CAGR through 2031.

- By geography, Asia-Pacific held 34.3% share of the liquid soap market size in 2025, while North America is forecast to grow at a 6.8% CAGR through.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liquid Soap Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hygiene shift toward pump and dispenser formats | +1.3% | Global | Medium term (2-4 years) |

| Skin-friendly and natural formula premiumization | +0.9% | North America, Europe, APAC core | Long term (≥ 4 years) |

| E-commerce discovery and refill access | +0.6% | Global, led by North America and East Asia | Medium term (2-4 years) |

| Refill economics in hospitality and commercial washrooms | +0.5% | Global, with spillover to Middle East and Africa and South America | Medium term (2-4 years) |

| High-frequency handwashing demand for mild cleansers | +0.7% | Global, particularly South and Southeast Asia | Long term (≥ 4 years) |

| Innovation in packaging and dispensing systems | +0.4% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hygiene-led shift from bar soap to pump and dispenser formats

As hygiene control and user convenience take precedence, the liquid soap market is witnessing a sustained shift away from traditional bar soaps. Pump and dispenser systems not only minimize direct product contact but also enhance portion control, seamlessly aligning with both household and institutional washing habits. Data from the Japan Soap and Detergent Association reveals that in 2024, liquid hand soap volumes reached 116,272 metric tons, indicating that the demand for liquid formats has remained robust, even post-pandemic[1]Source: Japan Securities Dealers Association, "Sales trends of body cleansing products (1990-2024)", jsda.org. Commercial entities are echoing this trend; for instance, GOJO highlighted that its PURELL CX10 system is designed to use 20% less plastic than its predecessors, and each 2-liter refill can save up to 10 gallons of water when compared to conventional foam soap systems. This blend of heightened hygiene control, efficient dispensing, and reduced material consumption solidifies liquid soap's dominance over solid formats, both in retail settings and away-from-home scenarios.

Natural and skin-friendly formulation premiumization

Shifting focus from mere fragrance-led premiumization, the liquid soap market is now emphasizing mildness, skin comfort, and ingredient transparency. As consumers begin to view hand and body washes akin to personal care products, there's a heightened emphasis on features like barrier support, microbiome-safe surfactants, and dermatologist endorsements. A 2025 Barrows survey, highlighted by Method, revealed that 83% of participants prioritize skincare and wellness benefits when selecting hand soaps. This insight underscores the trend of benefit-driven reformulations in the industry. In response to the demand for gentler cleansing systems, ingredient suppliers are making notable moves. For instance, Clariant launched 'Hostapon CT solid' in April 2026, introducing a salt-free taurate surfactant boasting 80% renewable carbon content and RSPO Mass Balance certification. Similarly, Kensing rolled out fully upcycled biosurfactants in April 2026, emphasizing that their platform results in over four times lower CO2 emissions compared to traditional biosurfactant feedstocks. Such innovations are steering the liquid soap market towards premium formulas, bolstering pricing power and fostering brand loyalty.

High-frequency handwashing demand for barrier-safe mild cleansers

Repeated washing occasions are reshaping the liquid soap market, especially in sectors like healthcare, food service, and childcare. In these high-use environments, harsh cleansers can compromise skin comfort, leading to diminished brand loyalty. In response, brands are prioritizing mildness, elevating it from a mere claim to a core performance feature, particularly in their premium hand and body wash lines. Reckitt's Dettol Activ Botany, which secured a notable 44% market share on TikTok in China in 2025, is now making its debut in the UK and ASEAN markets. This expansion underscores the global appeal of gentle hygiene products. Method's hand wash, launched in March 2026, spotlighted ingredients like hydrolyzed jojoba esters and glycerin, further cementing the notion that skin barrier support is becoming a commercial standard in the liquid soap arena. With consumers increasingly washing their hands both at home and work, brands that emphasize mild cleansing alongside credible skin-support claims are poised for success.

E-commerce-led premium SKU discovery and refill access

Online channels are driving growth in the liquid soap market, as premium and refill products are more easily explained, compared, and reordered digitally than on crowded retail shelves. This is significant because higher-value products often require more space for ingredient stories, refill logic, and routine-based positioning—space that physical retail typically doesn't provide. In February 2026, Bath & Body Works underscored this trend by launching its inaugural authorized storefront on Amazon in the U.S., enhancing the accessibility of its hand soaps and body washes through a search and convenience-driven platform. Similarly, packaging innovations are aligning with this trend. For instance, Amcor's AmPrima 2-Liter Refill Pouch, introduced in July 2025, was specifically designed for e-commerce fulfillment. It not only secured the ISTA 6A certification but also achieved recyclability certification across multiple European markets. As a result, the liquid soap market is witnessing a synergistic relationship between digital distribution and sustainable packaging, bolstering repeat purchases, encouraging larger pack sizes, and enhancing the economics for niche premium lines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw material and packaging resin cost volatility | -0.7% | Global | Short term (≤ 2 years) |

| Private-label pressure and low switching costs | -0.5% | Europe and North America | Medium term (2-4 years) |

| Epr, recyclability, and microplastics compliance burden | -0.4% | Europe, expanding to North America and APAC | Medium term (2-4 years) |

| Risk of skin irritation and chemical sensitivity | -0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Raw material and packaging resin cost volatility

Volatile costs of surfactants and resins continue to squeeze margins in the liquid soap market. This is particularly challenging for private-label and mid-tier players, who struggle more than their larger counterparts to absorb rising input costs without compromising their value positioning. As feedstock costs climb, brands face tough choices: raise prices, tweak formulas, or cut back on promotions. However, each of these decisions risks diminishing their competitive edge by either alienating price-sensitive consumers, reducing product quality, or limiting market visibility. Furthermore, the economics of packaging encompassing pumps, bottles, and refills are intricately tied to the unpredictable patterns of plastic costs, which are influenced by factors such as crude oil price fluctuations and supply chain disruptions. For brands without the flexibility in supply or the leverage of premium pricing, this cost sensitivity stands out as a significant short-term challenge in the liquid soap arena.

EPR, recyclability, and microplastics compliance burden

Stricter packaging compliance requirements in developed regions are putting pressure on the liquid soap market. Brands that rely on pumps, mixed-material packs, and certain refill structures face heightened costs and complexities, as these elements are often harder to certify or recover at scale. This challenge is significant: while sustainability claims increasingly sway shopper choices, they must also withstand more stringent recycling and producer-responsibility standards. Amcor's launch of a certified refill pouch underscores the swift moves by some suppliers to bridge this gap. However, not all brands enjoy the same level of packaging readiness or financial backing, which creates disparities in their ability to adapt. Smaller or emerging brands, in particular, may struggle to meet these compliance demands due to limited resources or access to advanced packaging solutions. As a result, compliance has evolved from a peripheral concern to a pivotal competitive factor in the liquid soap market, influencing format choices, margin structures, and market entry speeds. This shift highlights the growing importance of aligning packaging strategies with regulatory and consumer expectations to maintain competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Hand Soap Leads While Body Soap Expands Faster

In 2025, hand soap dominated the liquid soap market, capturing a 42.05% share. This prominence is driven by consistent demand across various sectors, including homes, offices, food services, healthcare, and public facilities, all of which prioritize frequent hand cleansing. The segment benefits from its widespread use in both personal and institutional settings, where hygiene is a critical concern. Additionally, the segment's established dispenser infrastructure ensures more predictable repeat purchases compared to other cleansing categories. This infrastructure not only supports convenience but also encourages bulk purchasing, particularly in institutional environments. Hand soap remains the cornerstone of the liquid soap market, seamlessly blending everyday utility with a strong institutional demand, making it an indispensable product in maintaining hygiene standards.

Body soap, on the other hand, is set to chart a different course, with projections indicating a 6.8% CAGR growth rate through 2031, making it the liquid soap market's fastest-growing segment. This surge is attributed to a notable shift in consumer preferences, moving from basic cleansing to more sophisticated body wash routines emphasizing hydration, comfort, and sensory appeal. Consumers are increasingly seeking products that not only cleanse but also provide skincare benefits, reflecting a broader trend toward wellness and self-care. Highlighting this trend, Method unveiled its Body Wash Tonics and Hydrating Serum Hand Washes in March 2026, underscoring the industry's pivot towards integrating skincare claims into liquid cleansing formats for enhanced value. These innovations cater to a growing demand for premium products that combine functionality with indulgence. As consumers increasingly associate premium body washes with self-care, this segment is poised to close the value gap with hand soap in the coming years.

By Ingredient: Conventional Formulas Hold Scale While Free-From Gains Momentum

In 2025, conventional formulations commanded a dominant 71.05% share, solidifying their status as the leading ingredient segment in the liquid soap market. Their dominance stems from cost-effectiveness, reliable performance, and widespread adoption in both mass-market and private-label products. These conventional systems cater to price-sensitive consumers and major retail channels, underscoring the importance of unit economics. Additionally, their compatibility with existing manufacturing processes and supply chains further reinforces their position. Consequently, even as premium claims gain traction, the liquid soap market remains anchored in conventional chemistry for its foundational volume, ensuring accessibility and affordability for a broad consumer base.

Forecasted to grow at a 5.2% CAGR through 2031, the free-from segment is poised to outpace the broader liquid soap market. This surge is driven by consumers increasingly favoring sulfate-free, paraben-free, and fragrance-free options, particularly those with sensitive skin. Under COSMOS and Ecocert standards, rinse-off personal-care products are mandated to have a minimum of 10% organic content by weight[2]Source: COSMOS Standard, "COSMOS v4.0 Cosmetic Organic Standard,"cosmos-standard.org. In parallel, the U.S. Department of Agriculture's organic certification requires that 95% of plant-derived ingredients comply with organic farming protocols[3]Source: United States Department of Agriculture, "National Organic Program Handbook," usda.gov. The segment's allure is further heightened by a growing awareness of ingredient transparency and the environmental ramifications of personal care products. Clariant's 2026 launch of Hostapon CT solid exemplifies this industry pivot, with ingredient suppliers collaborating with brands to formulate milder liquid cleansers, boasting both enhanced renewable content and certification credentials. Concurrently, Kensing's upcycled biosurfactant platform provides brands a route to harmonize gentle performance with eco-friendlier sourcing, amplifying the appeal of the free-from stance within the liquid soap domain. These advancements underscore the industry's commitment to aligning with the rising consumer demand for safer, sustainable products.

By Packaging: Bottles Stay Dominant While Refill Pouches Reshape Format Economics

In 2025, bottles commanded a dominant 57.25% share, solidifying their status as the leading packaging choice in the liquid soap market. Bottles have become the go-to format: consumers are familiar with their use, retailers adeptly merchandise them, and both homes and institutions have dispensers designed for bottles. Furthermore, bottles accommodate a broad spectrum of products, from budget-friendly hand washes to luxury body washes, all without necessitating a shift in consumer behavior. This adaptability ensures bottles maintain their significance, even as the liquid soap market leans towards more eco-friendly packaging solutions. Their widespread acceptance and compatibility with existing infrastructure make them a resilient choice in the evolving market landscape.

Refill pouches are on track to expand at a robust 6.9% CAGR through 2031, positioning them as the quickest-evolving packaging choice in the liquid soap arena. Their rise can be attributed to reduced plastic consumption, enhanced transport efficiency, and a compelling value for repeat customers with existing dispensers. Amcor's July 2025 AmPrima 2-Liter Refill Pouch boasts an 80% reduction in plastic use and a 64% smaller carbon footprint compared to two 1-liter PET bottles. Moreover, it adheres to recyclability and e-commerce standards across various European markets. L’Occitane’s refill initiative underscores that even premium brands can embrace refills without diluting their brand prestige, emphasizing significant material savings and heightened biodegradability in select formats. The growing adoption of refill pouches highlights the industry's shift towards sustainability while addressing consumer demand for cost-effective and environmentally friendly solutions.

By Consumer Group: Adults Provide the Base While Children’s Products Grow More Quickly

In 2025, adults commanded a dominant 87.02% share of the liquid soap market, underscoring their status as the primary consumer group. This prevalence is attributed to the widespread household use of liquid soap, heightened washing frequency, and a diverse array of hand and body cleansing products tailored for adults, spanning all price ranges. Demand among adults is diversifying; some consumers are opting for premium products with skin-enhancing benefits, while others prioritize value and convenience. Consequently, the liquid soap market continues to generate the bulk of its revenue from adult consumers, even as new demands surface within this expansive demographic. The consistent innovation in adult-focused products ensures that this segment remains a cornerstone of the market's growth trajectory.

Forecasts indicate that the segment catering to kids and children will expand at a 6.6% CAGR through 2031, outpacing the overall liquid soap market. This growth is fueled by a rising demand for gentle cleansers, reflecting parental priorities on sensitive skin care, mild surfactants, and formulas that minimize irritation. Furthermore, the attributes prized for children's products, particularly their mildness, are gaining traction among adults, especially those with frequent washing needs. Thus, what was once viewed as a niche focus on children's care is now evolving into a standard that significantly influences product offerings for adults in the liquid soap industry. This shift highlights the growing importance of cross-segment innovation in shaping the future of the market.

By Distribution Channel: Supermarkets Hold Scale While Online Retail Builds Faster

In 2025, supermarkets and hypermarkets dominated the liquid soap market, capturing a 39.02% share. Their dominance stems from routine household shopping, heightened promotional visibility, and the ability to encourage trials through prominent shelf exposure. These outlets boast a wide assortment, enabling both mass and premium brands to connect with a diverse shopper base. Consequently, the liquid soap market continues to rely on physical retail for volume and consistent replenishment, as these channels remain integral to consumer purchasing habits.

Online retail is projected to expand at a 6.3% CAGR through 2031, positioning it as the fastest-growing channel in the liquid soap market. Digital platforms shine for premium, niche, and refill products, offering ample space for product details, ingredient education, and subscription options. Bath & Body Works’ February 2026 debut on Amazon underscores that even established premium brands now see digital marketplaces as pivotal growth drivers for hand soaps and body washes. Additionally, the convenience and accessibility of online retail continue to attract a growing number of consumers, further solidifying its role in the market's evolution.

Geography Analysis

In 2025, Asia-Pacific commanded a dominant 34.27% share of the liquid soap market, solidifying its status as the leading regional player. The region's robust urban populations, increasing investments in hygiene, and a diverse demand spectrum from mass to premium anchor its global volume. Highlighting the region's strength, Japan's industry association reported a solid demand in 2024, with liquid hand soap volumes hitting 116,272 metric tons, underscoring the vitality of one of Asia-Pacific's most established markets. Furthermore, Asia-Pacific's adeptness at product adaptation across various income tiers fuels the liquid soap market's expansion, balancing both affordability and premiumization.

North America is set to lead with a projected 6.8% CAGR growth rate through 2031, marking it as the fastest-growing region in the liquid soap market. This growth trajectory is bolstered by the introduction of premium formulas, enhanced online visibility, and intensified institutional procurement. In a strategic move, The Clorox Company finalized its acquisition of GOJO Industries in April 2026, paving the way for a more extensive platform in both consumer and institutional hygiene products, thereby amplifying its presence in hand soap and dispensing systems. Concurrently, Bath & Body Works bolstered its U.S. market strategy by expanding its authorized presence on Amazon in early 2026, facilitating quicker access to its premium soap and body wash lines.

While Europe has traditionally been a mature player in the liquid soap arena, it's witnessing a gradual evolution, marked by formulation enhancements and a shift towards refill-centric packaging. Major regional brands are pivoting towards plant-based ingredients, milder surfactants, and packaging that's not only easier to certify but also recyclable. Unilever's 2025 acquisition of Wild underscores the significance of refillable and digitally-driven personal care models, indicating a strategic pivot at the highest corporate echelons. Similarly, Amcor's rollout of certified refill pouches in Italy, Germany, and Austria highlights the growing synergy between packaging compliance and refill convenience in the region's evolving packaging landscape. Meanwhile, South America, the Middle East, and Africa, though smaller markets, are witnessing growth closely tied to urbanization, hospitality trends, and increasing personal care expenditures, rather than a focus on premium skincare positioning.

Competitive Landscape

The liquid soap market remains moderately fragmented, with a group of large consumer goods companies holding scale advantages but not closing the door on regional or premium challengers. Global players such as Unilever, Reckitt, Procter & Gamble, and Colgate-Palmolive compete from a position of brand reach, retailer access, and formulation depth. At the same time, the liquid soap market still leaves enough room for regional specialists to defend local channels and for premium brands to grow through claims-led positioning. This balance keeps pricing, shelf competition, and innovation pressure active across most major regions.

Large companies are increasingly using acquisitions, refill platforms, and ingredient partnerships to sharpen their position in the liquid soap market. Unilever’s acquisition of Wild in April 2025 showed a direct move toward refillable and plant-based personal care formats that fit digital and premium growth spaces. Clorox’s completion of the GOJO deal in April 2026 created a stronger bridge between retail hygiene products and institutional dispensing systems, which can improve cross-channel scale and customer access. Ingredient suppliers are also becoming more relevant to competition, as Clariant and Kensing both launched new mild or lower-impact surfactant platforms in 2026 that help brands improve claims without fully reworking product performance expectations. These moves show that competition in the liquid soap market is no longer centered only on fragrance and price.

The next phase of competition is likely to be shaped by barrier-safe formulas, refill models that work at scale, and stronger links between online discovery and repeat purchase. Premium brands are already adjusting, as Bath & Body Works paired its Amazon expansion with broader emphasis on ingredient transparency and dermatologist-approved positioning for body wash and hand soap. Regional players in Asia-Pacific remain important because they understand local wash habits, pricing thresholds, and retail structures better than many global rivals. As a result, the liquid soap market should remain competitive across both volume and premium tiers rather than consolidate around a single dominant operating model.

Liquid Soap Industry Leaders

-

Reckitt Benckiser Group plc

-

Procter & Gamble Company

-

Unilever PLC

-

Colgate-Palmolive Company

-

Henkel AG & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Dove Canada has unveiled its premium Dove Serum+ Oil Body Wash, an innovative oil-to-foam line infusing serum-inspired hydration into daily body care. This collection, co-created with dermatologists, boasts two variants: Radiance and Soothing. Each variant is enriched with a 50% glycerin serum, ensuring instant, non-greasy hydration and a radiant glow after just one shower.

- November 2025: Bend Soap Company has debuted its Foaming Goat Milk Liquid Soap. This all-natural, non-toxic hand soap harnesses the goodness of fresh, raw goat milk and nutrient-rich oils. Tailored for sensitive and eczema-prone skin, it promises gentle cleansing, deep hydration, and a creamy foam, all while being free from sulfates, parabens, synthetic fragrances, and fillers.

- June 2025: Native, the clean personal care brand under P&G, has rolled out its much-anticipated Native Liquid Hand Soap. Responding to demands from 82% of its users, this new offering brings Native’s signature nourishing experience from the shower to the sink. Crafted with naturally derived, vegan, and cruelty-free ingredients, the soap is devoid of sulfates, parabens, and dyes.

- June 2025: Caprica Soapery has launched its inaugural liquid hand soap, marking a new chapter in its handcrafted bath and body range. With a focus on convenience, the brand introduces a pump format. Caprica expresses enthusiasm for the new formulation, treating this launch as a trial run: a positive customer reception could solidify liquid hand soap as a staple in their collection.

Global Liquid Soap Market Report Scope

Liquid soap, a water-based product, uses surfactants to cleanse the skin, effectively removing dirt, oils, and microbes upon rinsing. Tailored for hand and body hygiene, it often includes moisturizing agents and preservatives, ensuring skin integrity. Additionally, its dispenser-based application offers a more hygienic alternative to traditional bar soap.

The scope of the market includes product types such as hand soap and body soap. By ingredient type, the market is segmented into free-from and conventional. By packaging type, the market is segmented into bottles, tubes, refill pouches, and others. Based on the consumer group, the market is segmented into adults and kids/children. By distribution channel, the market is segmented into supermarkets/hypermarkets, health and beauty stores, and other distribution channels. Also, the report offers detailed analysis on major economies across North America, Europe, Asia-Pacific, South America and Middle East and Africa.

| Hand Soap |

| Body Soap |

| Free-From |

| Conventional |

| Bottles |

| Tubes |

| Refill Pouches |

| Others |

| Adults |

| Kids/Children |

| Supermarkets/Hypermarkets |

| Health & Beauty Stores |

| Online Retail Stores |

| Other Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Hand Soap | |

| Body Soap | ||

| By Ingredient | Free-From | |

| Conventional | ||

| By Packaging | Bottles | |

| Tubes | ||

| Refill Pouches | ||

| Others | ||

| By Consumer Group | Adults | |

| Kids/Children | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health & Beauty Stores | ||

| Online Retail Stores | ||

| Other Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is driving liquid soap demand worldwide?

Demand is being lifted by the shift from bar soap to pump formats, premium skin-friendly formulations, refill adoption, and online discovery. The liquid soap market is projected to grow from USD 22.4 billion in 2026 to USD 29.5 billion by 2031 at a 4.9% CAGR.

Which product category is leading liquid soap sales?

Hand soap leads with 42.1% share in 2025 because it is used widely across households and institutional settings. Body soap is growing faster at a 6.8% CAGR through 2031.

Which region leads global liquid soap consumption?

Asia-Pacific held the largest share at 34.3% in 2025 due to its large urban population base, rising hygiene spending, and broad demand across value and premium products.

Which region is growing the fastest for liquid soap?

North America is forecast to grow at a 6.8% CAGR through 2031, supported by premium launches, stronger e-commerce discovery, and deeper institutional purchasing.

Page last updated on: