North America Liquid Hand Soap Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

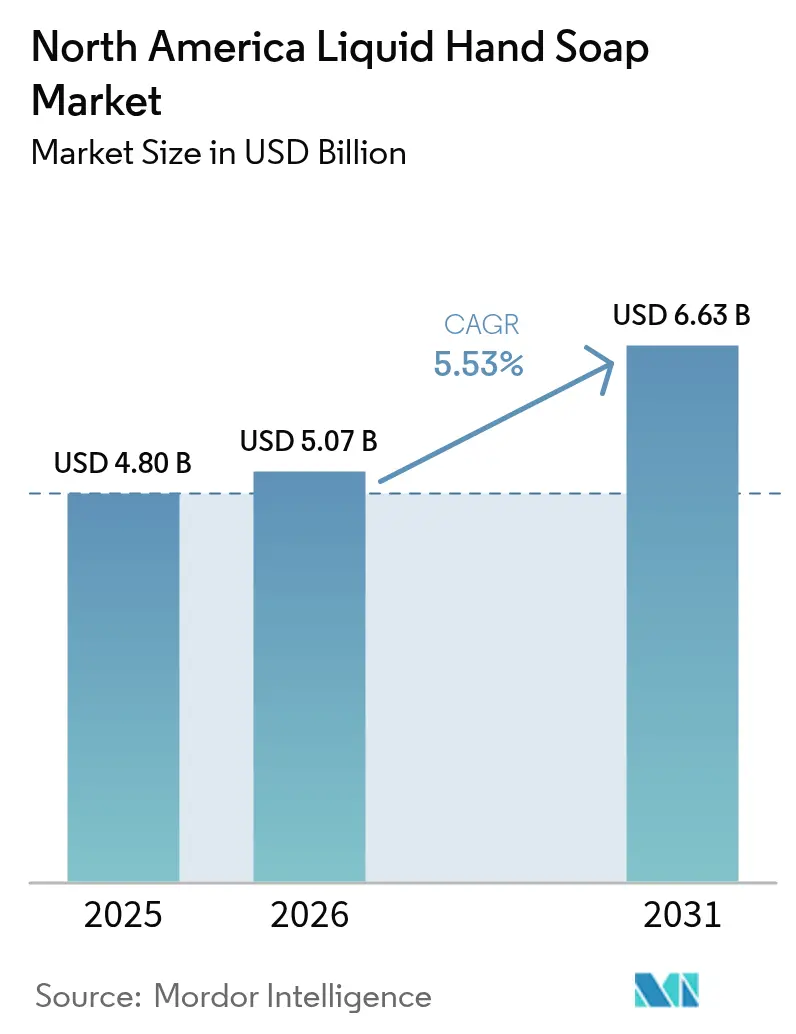

| Base Year Market Size (2025) | USD 4.8 Billion |

| Market Size (2026) | USD 5.07 Billion |

| Market Size (2031) | USD 6.63 Billion |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

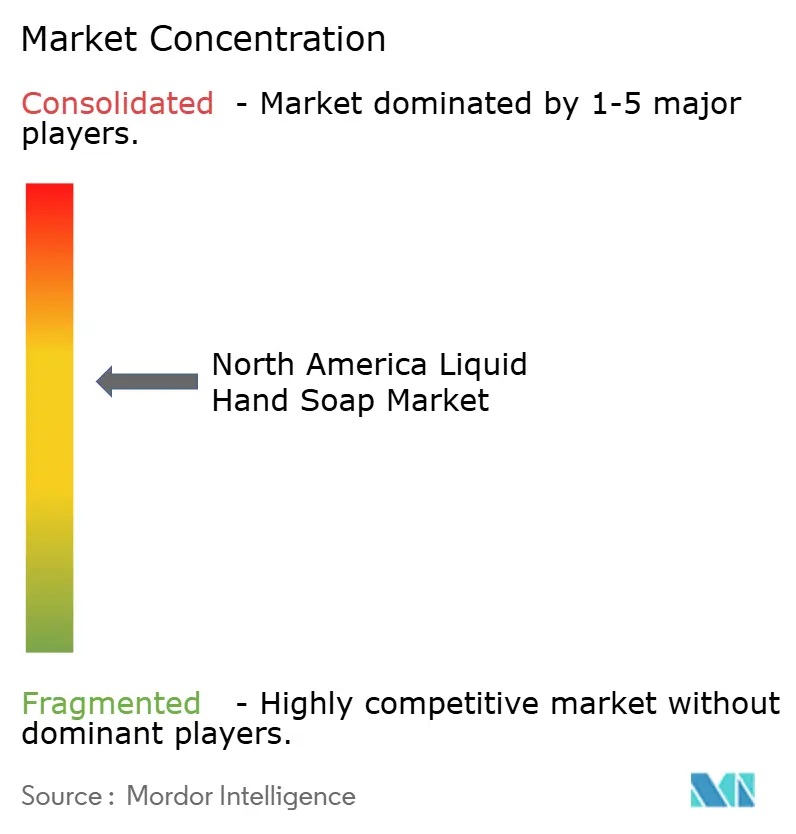

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Liquid Hand Soap Market Analysis by Mordor Intelligence

The North America liquid hand soap market size is expected to grow from USD 4.8 billion in 2025 to USD 5.07 billion in 2026 and is forecast to reach USD 6.63 billion by 2031 at 5.53% CAGR over 2026-2031. This growth is propelled by premium formulation launches, federal “Buy-American” purchasing rules, and brand investments in refillable packs that lower plastic use. Demand is also supported by touchless dispensing technology adopted in hospitals and foodservice operations, while shrinkflation scrutiny pressures brand pricing strategies[1]The White House, “Biden-Harris Administration Finalizes Rule to Maximize Federal Purchases of American-Made Sustainable Products,” whitehouse.gov. Rising biosurfactant adoption, combined with hypoallergenic positioning, further broadens consumer reach across income tiers. Together, these dynamics reinforce the long-term resilience of the North America liquid hand soap market.

Key Report Takeaways

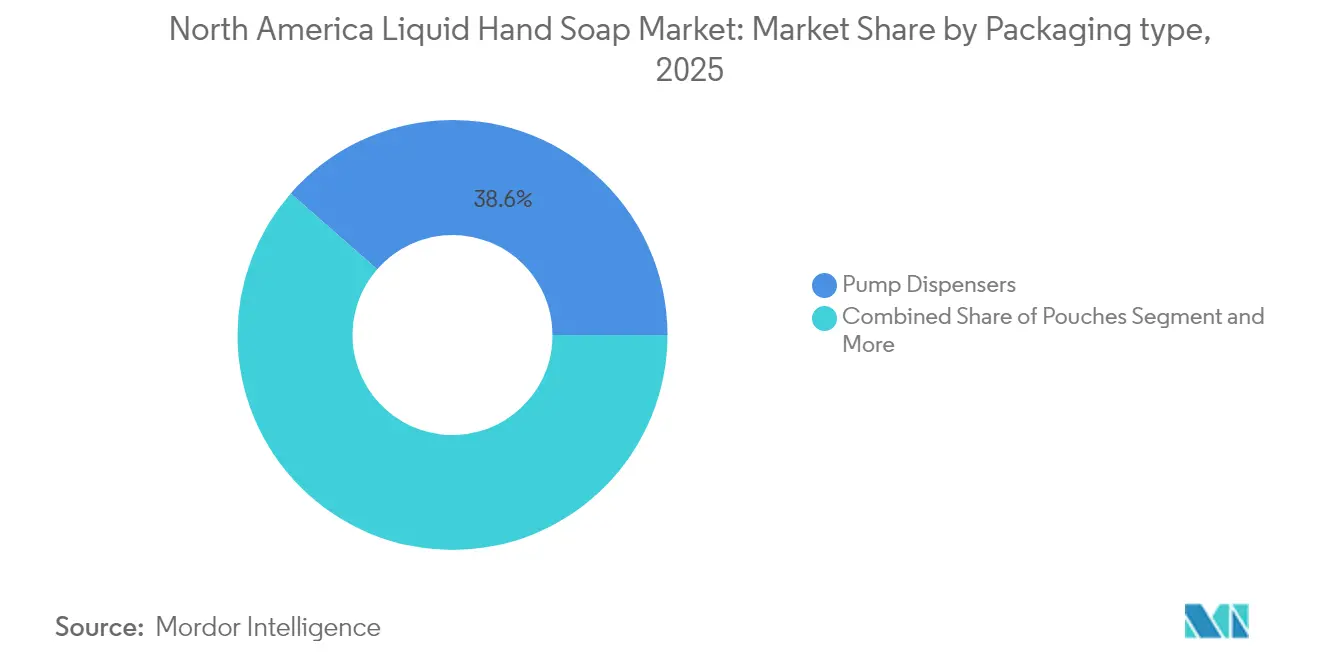

By packaging type, pump dispensers captured 39.27% of the North America liquid hand soap market share in 2024, while pouches are expanding at a 5.23% CAGR through 2030.

By end-user, residential consumption accounted for 53.64% of the North America liquid hand soap market size in 2024; commercial usage is advancing at a 5.92% CAGR to 2030.

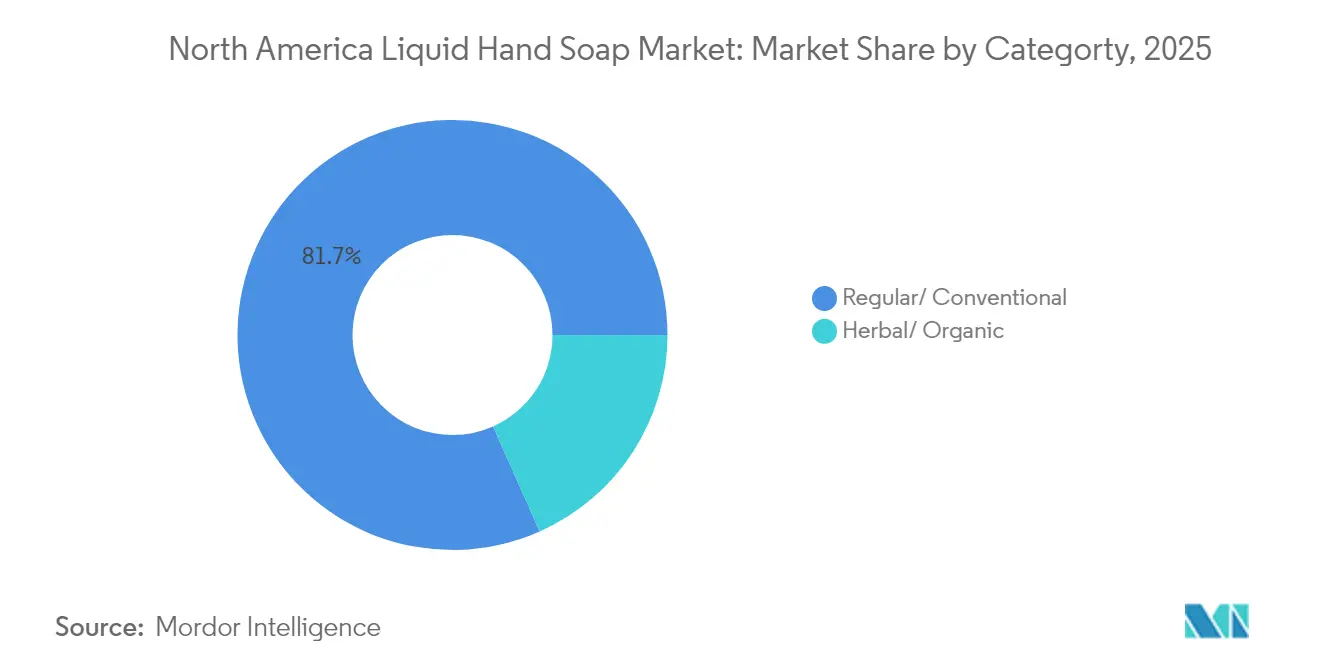

By category, regular formulations held 82.38% of the North America liquid hand soap market size in 2024, yet herbal/organic variants are projected to grow at a 6.21% CAGR over the same horizon.

By product type, gel-based offerings led with 84.42% of the North America liquid hand soap market share in 2024, whereas foaming solutions are on track for a 4.96% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Liquid Hand Soap Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-led shift to refill and recyclable packs | +1.2% | North America & Global | Medium term (2-4 years) |

| SKU premiumisation through skin-care and fragrance cross-over | +0.8% | United States & Canada | Short term (≤ 2 years) |

| Touchless dispenser adoption in commercial spaces | +1.0% | North America core, spill-over to Mexico | Short term (≤ 2 years) |

| Biosurfactant and hypoallergenic formulations uptake | +0.7% | United States & Canada | Medium term (2-4 years) |

| Federal “Buy-American” hygiene procurement clauses | +0.9% | United States | Long term (≥ 4 years) |

| Technology advancements in manufacturing | +0.6% | North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability-Led Shift to Refill and Recyclable Packs

California’s SB 54 mandates that all packaging be recyclable or compostable by 2032, driving manufacturers toward mono-material pouches and closed-loop cartridges that cut plastic tonnage and freight costs[2]Packaging School, “Exploring California’s SB 54,” packagingschool.com. Henkel’s Dial brand now employs 100% post-consumer recycled bottles, earning third-party GreenCircle certification while maintaining high production volumes at its Pennsylvania facility. Federal buyers accelerate this momentum through the GSA’s listing program for single-use plastic-free packaging, granting visibility to compliant suppliers. Together, regulatory pressure and procurement incentives add roughly 1.2% to the market CAGR as converters re-tool lines for pouch laminates and refill systems.

SKU Premiumisation Through Skin-Care and Fragrance Cross-Over

Premium positioning through skin-care and fragrance integration transforms liquid hand soap from a commodity to an experiential product category, capturing higher margins and consumer loyalty. This premiumization strategy leverages the beauty industry's expertise in sensory formulation and ingredient storytelling. Ulta Beauty's Conscious Beauty program, encompassing over 300 participating brands with criteria including clean ingredients, sustainable packaging, and cruelty-free formulations, demonstrates retailer support for premium positioning. L'Oréal's commitment to 95% biobased ingredients and 100% recyclable plastic packaging by 2030 exemplifies how beauty conglomerates apply premium innovation capabilities to adjacent categories. The crossover strategy succeeds by addressing consumers' desire for multifunctional products that deliver cleansing efficacy alongside skin conditioning benefits. GOJO's PURELL HEALTHY SOAP incorporates natural moisturizers, skin conditioners, and spa-inspired formulations while maintaining hypoallergenic properties and excluding phthalates, parabens, and triclosan[3]GOJO Industries, “PURELL HEALTHY SOAP Fresh Scent Foam,” gojo.com.

Touchless Dispenser Adoption in Commercial Spaces

Post-pandemic hygiene protocols permanently altered commercial facility management, driving sustained demand for touchless dispensing solutions that minimize cross-contamination risks. The CDC's emphasis on accessible handwashing facilities with soap and adequate drying provisions reinforces institutional adoption of automated systems. Healthcare facilities particularly benefit from touchless technology, as CDC guidelines recommend alcohol-based hand rubs for routine decontamination when hands are not visibly soiled, creating complementary demand for soap-based systems when washing is required. Diversey's IntelliCare touchless dispensers deliver up to 350 doses per cartridge with high dose efficiency, addressing both hygiene and operational cost concerns. The FDA Food Code 2022 mandates handwashing sinks with soap in foodservice operations, creating regulatory demand for reliable dispensing systems that support 20-second handwashing protocols. Commercial adoption accelerates as facility managers recognize touchless systems' dual benefits of infection control and labor efficiency, contributing 1.0% to market CAGR with immediate implementation timelines.

Biosurfactant and Hypoallergenic Formulations Uptake

The integration of biosurfactants and hypoallergenic ingredients addresses growing consumer awareness of chemical sensitivities while meeting sustainability objectives through biodegradable formulations. FDA regulation of hand soap ingredients under 21 CFR guidelines ensures safety standards while permitting innovation in surfactant chemistry. Biosurfactants derived from microbial fermentation offer superior biodegradability compared to petroleum-based alternatives, aligning with environmental regulations like the EPA's Significant New Use Rule for bisalkylated fatty alkyl amine oxide, which requires reporting for water releases above 80 ppb concentration. Diversey's SURE plant-based range achieves Cradle to Cradle GOLD certification with 100% biodegradability and approximately 16% lower carbon footprint versus petroleum-based equivalents. The formulation trend responds to institutional buyers' sustainability mandates while addressing consumer preferences for gentler ingredients that reduce skin irritation risks. This biosurfactant adoption contributes 0.7% to market CAGR with medium-term impact as manufacturers reformulate existing products and develop new offerings that meet both performance and sustainability criteria.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory and retailer pressure on single-use plastics | -0.8% | North America & Global | Short term (≤ 2 years) |

| Price war versus bar-soap & tablet concentrates | -0.6% | United States & Canada | Medium term (2-4 years) |

| Contamination risk in bulk-refill dispensers | -0.4% | North America | Short term (≤ 2 years) |

| Shrinkflation scrutiny limiting pack-size tactics | -0.3% | United States | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory and Retailer Pressure on Single-use Plastics

Escalating regulatory restrictions on single-use plastics create compliance costs and operational complexity that constrain market growth, particularly affecting traditional packaging formats. The Retail Industry Leaders Association documents heightened regulatory attention driven by ocean plastics concerns and recycling disruptions, with state regulations expanding beyond plastic bags to include containers, straws, and expanded polystyrene foodservice ware. California's SB 54 imposes civil penalties up to USD 50,000 per day per violation for non-compliance with recyclability and plastic reduction targets, creating significant financial exposure for manufacturers. The EU's Regulation 2025/40 on Packaging and Packaging Waste, effective August 2026, sets binding reduction targets of 5% by 2030, 10% by 2035, and 15% by 2040, influencing global suppliers who serve multiple markets, such as SGS. Compliance requires substantial investment in alternative packaging materials, redesigned dispensing systems, and supply chain modifications. The regulatory pressure reduces market CAGR by 0.8% as manufacturers absorb transition costs and navigate complex compliance requirements across multiple jurisdictions.

Contamination Risk in Bulk-refill Dispensers

Microbial contamination in bulk-refillable dispensers poses significant health risks that limit adoption in hygiene-sensitive environments, creating a preference for sealed refill systems despite cost considerations. A comprehensive study published in Applied and Environmental Microbiology documented that all 14 bulk refillable dispensers in an elementary school were heavily contaminated with 6.0-7.0 log10 CFU/ml of Gram-negative opportunistic species, including Citrobacter, Providencia, Pseudomonas, and Serratia. The research demonstrated that washing with contaminated bulk soap produced a 26-fold increase in Gram-negative bacteria on hands post-wash, with 97% of hands testing positive for harmful bacteria versus 52% before washing. In contrast, sealed-refill dispensers eliminated contamination entirely, with no detectable contamination 12 months post-installation and actual bacterial reduction during handwashing. The CDC's facility cleaning guidance emphasizes that cleaning with soap-containing commercial cleaners reduces germs on surfaces, but contaminated soap negates these benefits. Healthcare facilities particularly avoid bulk systems due to infection control requirements, limiting market penetration in high-value institutional segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Pouches Drive Sustainable Innovation

Pump dispensers retained 38.56% of the North America liquid hand soap market in 2025, supported by entrenched household habits and widespread fixture compatibility. Yet pouches are adding 5.17% CAGR, capturing buyers focused on reduced plastic and lower logistics costs. Brands such as Diversey supply monolayer polyethylene pouches that refill multiple trigger bottles, cutting virgin resin weight per use. This momentum positions pouches as the headline growth story within the North America liquid hand soap market.

Wall-mount cartridges and bulk gallon jugs continue serving institutional environments, but contamination concerns reinforce sealed formats. Bottles designed for in-store refill stations bridge the transition, appealing to eco-minded shoppers without demanding fixture changes. Regulatory clauses in 21 CFR 117.37 on sanitary facilities encourage operators to invest in proven dispensing integrity, indirectly benefiting high-grade packaging suppliers.

By End-user: Commercial Growth Accelerates

Residential buyers accounted for 53.12% of the North America liquid hand soap market size in 2025, reflecting daily household hygiene routines. However, commercial demand is scaling faster at 5.86% CAGR, led by hospitals, restaurants, and schools compelled to sustain stringent wash standards. CDC guidance elevates soap-and-water efficacy over sanitizers when hands are visibly soiled, reinforcing unit volume growth in large venues.

Federal agencies prioritize domestically made options under Buy American provisions, funneling volumes toward U.S. manufacturers able to demonstrate local content. Corporate campuses and travel hubs also deploy sensor-activated dispensers that favor higher-margin proprietary refill cartridges, sharpening commercial segment profitability across the North America liquid hand soap market.

By Category: Organic Variants Capture Premium Positioning

Regular formulas delivered 81.65% of 2025 revenues, underpinned by value pricing and proven antibacterial performance. Still, herbal/organic SKUs are rising at a 6.11% CAGR as clean-beauty narratives expand. Retail banners use “free-from” merchandising to justify double-digit price gaps, emboldening suppliers to invest in 95% biobased inputs consistent with L’Oréal’s 2030 roadmap.

The Consumer Product Safety Commission clarifies labeling rules that separate true soaps from OTC drug claims, enabling organic makers to tout plant oils without navigating drug monographs. As shoppers seek gentler cleansers, premium organic lines deepen channel penetration and elevate average selling prices inside the North America liquid hand soap market.

By Product Type: Gel-Based Leadership Faces Foaming Innovation

Gel variants controlled 83.74% of 2025 sales, benefiting from viscosity that dispenses cleanly through legacy pumps. Foaming systems, however, are gaining a 4.92% CAGR due to lower soap usage per wash and user perception of rich lather. GOJO’s PURELL Fresh Scent Foam saves roughly 6 gallons of water per refill and holds ECOLOGO approval, exemplifying dual sustainability and performance credentials.

As more facilities retrofit touchless foam pumps, suppliers scale surfactant blends optimized for quick-rinse performance, reducing dwell time at sinks. Specialty antimicrobial foams containing benzalkonium chloride target healthcare niches and require FDA OTC compliance filings. This interplay of convenience and regulatory rigor guides future product-type share shifts within the North America liquid hand soap market.

Geography Analysis

The United States generated 77.85% of 2025 revenue, anchored by an extensive retail grid and disciplined federal purchasing that rewards sustainable U.S. production. Walgreens Boots Alliance alone operates 8,560 stores, creating enormous shelf bandwidth for national brands. Local manufacturing, such as Henkel’s West Hazleton plant, meets Buy American thresholds, ensuring continued capture of federal facility contracts.

Mexico is forecast to outpace peers at 5.68% CAGR, propelled by a natural-personal-care segment that already equals 10% of national beauty spend. Soap manufacturing shows deep domestic roots with MX$156.7 billion output and efficient clusters in Guanajuato and Estado de México, positioning local suppliers to embrace refill pouches rapidly. International entrants often partner with upscale retailers in Mexico City and Monterrey while optimizing last-mile e-commerce logistics to reach affluent consumers. Canada remains a steady mid-single-digit contributor, underscored by active trademark filings from multinational leaders like Unilever, signaling ongoing product-cycle investment. Harmonized ingredient disclosure laws foster consumer trust, while strong pharmacy channels mirror U.S. planogram strategies, sustaining category visibility in the North America liquid hand soap market.

Competitive Landscape

Market concentration measures 6 / 10, indicating moderate consolidation. Procter & Gamble, Colgate-Palmolive, Henkel, and Unilever harness vertically integrated supply chains, broad ad budgets, and robust R&D. Henkel’s Dial exemplifies scale advantage through renewable-energy procurement and full PCR bottle conversion, shielding margins as resin prices fluctuate. Emerging challengers thrive in premium natural niches. Unilever’s 2025 purchase of Dr. Squatch accelerates its entry into male-grooming-oriented soaps, highlighting acquisition as a shortcut to credibility.. Device innovators, including GOJO and Diversey, defend institutional share through patented touchless dispensers linked to proprietary refills, creating high switching costs.

Distributor consolidation adds another layer: the BradyIFS–Envoy merger forms a USD 5 billion JanSan giant, compressing supplier lists and demanding favorable rebate structures. Simultaneously, Walgreens Boots Alliance’s take-private deal by Sycamore Partners introduces potential private-label expansion across 12,500 outlets, affecting shelf allocation for branded soaps.

North America Liquid Hand Soap Industry Leaders

Colgate-Palmolive Company

GOJO Industries

Henkel

Reckitt Benckiser

Procter & Gamble

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Unilever announced the acquisition of Dr. Squatch, a U.S. natural soap and deodorant brand, to scale the brand internationally and strengthen positioning in the fast-growing men's personal care segment.

- March 2025: Walgreens Boots Alliance entered into a definitive agreement to be acquired by Sycamore Partners for up to USD 23.7 billion, with shareholders receiving USD 11.45 per share in cash plus potential additional proceeds from VillageMD asset monetization.

North America Liquid Hand Soap Market Report Scope

Hand liquid soaps are formulated to wash and clean hands. They are mostly available in the form of gels. The North America Liquid Hand Soap Market has been segmented by packaging type, distribution channel, and geography. By packaging type, the market studied has been segmented into bottles/containers (refill), pump dispensers, and pouches (refill). By distribution channel, the market studied has been segmented into hypermarkets/supermarkets, convenience stores, online retail, and other distribution channels. By country, the market covers the major countries of North America, i.e., the United States, Canada, Mexico, and the rest of North America. For each segment, the market sizing and forecasts have been done on the basis of value (in USD million).

| Pump Dispensers |

| Bottles/Containers (Refill) |

| Pouches (Refill) |

| Wall-Mount Cartridges |

| Bulk Gallon Jugs |

| Others |

| Residential |

| Commercial |

| Regular/ Conventional |

| Natural/ Organic |

| Foaming |

| Gel-based |

| Others |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| By Packaging Type | Pump Dispensers |

| Bottles/Containers (Refill) | |

| Pouches (Refill) | |

| Wall-Mount Cartridges | |

| Bulk Gallon Jugs | |

| Others | |

| By End-user | Residential |

| Commercial | |

| By Category | Regular/ Conventional |

| Natural/ Organic | |

| By Product Type | Foaming |

| Gel-based | |

| Others | |

| Geography | United States |

| Canada | |

| Mexico | |

| Rest of North America |

Key Questions Answered in the Report

How large is the North America liquid hand soap market in 2026 and how fast will it grow?

The market is valued at USD 5.07 billion in 2026 and is projected to advance at a 5.53% CAGR to reach USD 6.63 billion by 2031.

Which packaging format is growing fastest in North America?

Refillable pouches lead with a 5.17% CAGR thanks to lower plastic weight and retailer sustainability mandates.

Why is commercial demand rising faster than residential demand?

Hospitals, foodservice sites, and schools must maintain strict hygiene protocols, boosting commercial usage at a 5.86% CAGR through 2031.

Which product category commands premium pricing?

Herbal / organic liquid hand soaps carry higher price points and are expanding at a 6.11% CAGR as consumers trade up for clean-label formulations.

Page last updated on: