Latin America Professional Liquid Soap Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

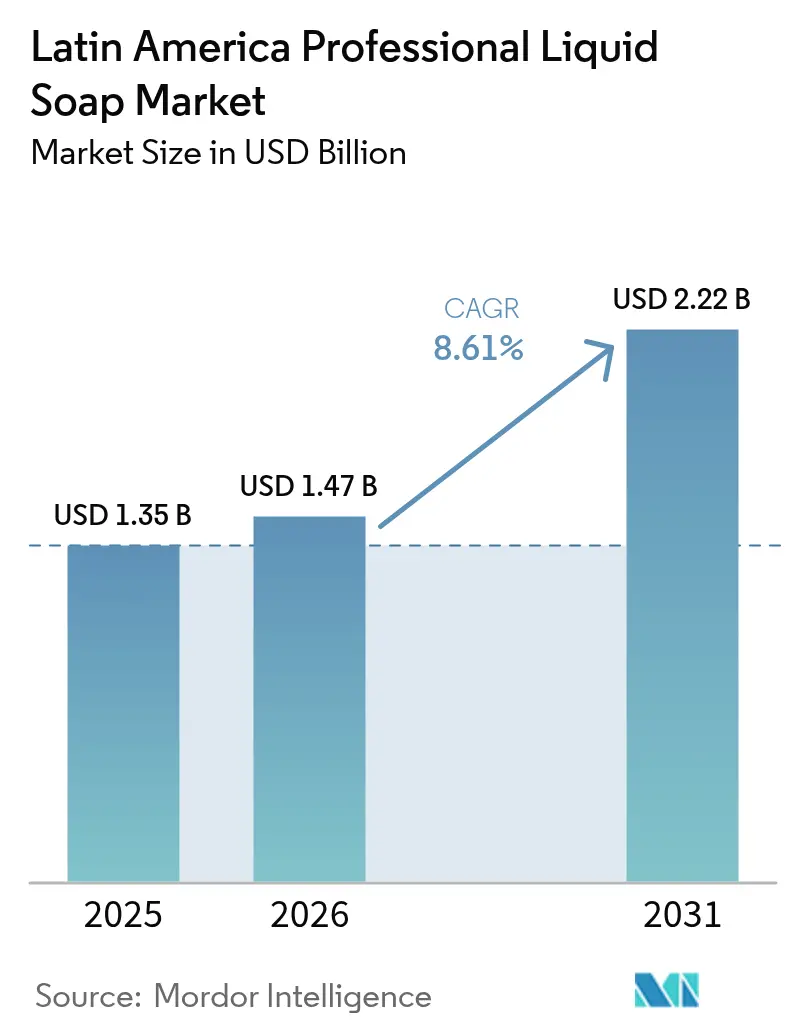

| Base Year Market Size (2025) | USD 1.35 Billion |

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 2.22 Billion |

| Growth Rate (2026 - 2031) | 8.61% CAGR |

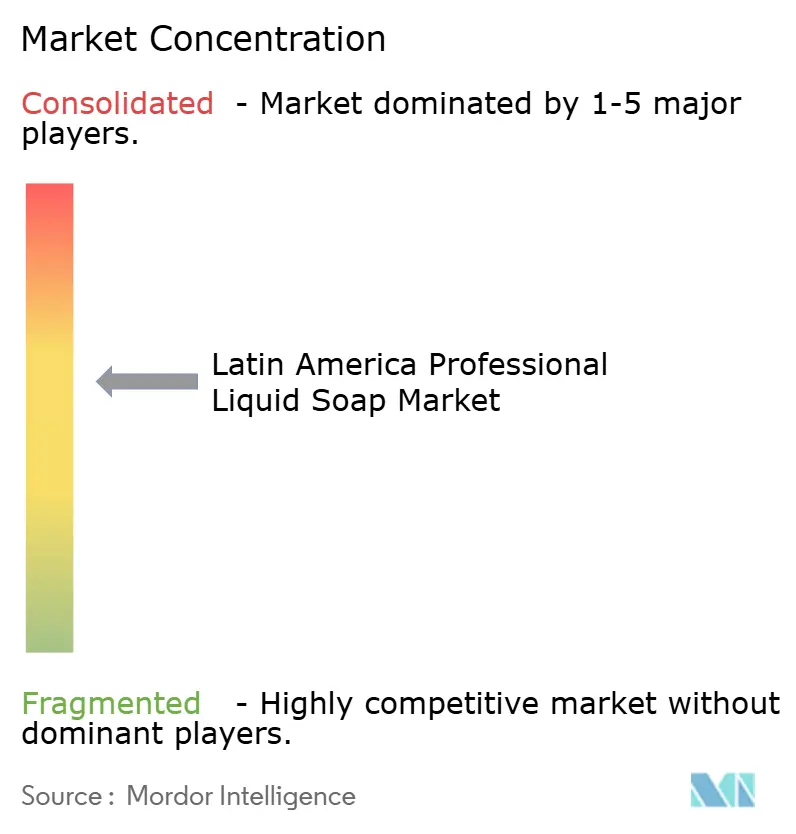

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Latin America Professional Liquid Soap Market Analysis by Mordor Intelligence

The Latin America professional liquid soap market size was valued at USD 1.35 billion in 2025 and estimated to grow from USD 1.47 billion in 2026 to reach USD 2.22 billion by 2031, at a CAGR of 8.61% during the forecast period (2026-2031). This trajectory reflects intensifying hygiene standards across institutional end-users rather than household penetration alone, with hospitals, hotels, and industrial facilities driving the bulk of incremental volume. Brazil commands 42.15% market share in 2024, anchored by ANVISA's stringent cosmetic and sanitizer regulations that compel facilities to source certified formulations, while Argentina, despite economic volatility, is set to grow at 9.22% CAGR through 2030, fueled by trade liberalization measures that slashed import tariffs on over 90 product lines and eliminated the 7.5% PAIS tax in 2024 [1]Source: OECD (Organization for Economic Co-operation and Development), "Labour taxes drive OECD tax revenues to record high in 2024", oecd.org . Hospitals, hotels, restaurants, and a widening band of industrial users are embedding liquid hand-washing protocols into safety audits, while recycled packaging rules and eco-label adoption press suppliers to redesign formats and ingredients. Foaming variants, refill pouches, natural formulations, and premium SKUs are rising fastest as buyers weigh the total cost of use, waste reduction, and brand positioning. Competitive intensity is moderate, with global majors deepening capacity and sustainability credentials, and regional specialists leveraging nimble distribution and lower minimum order quantities to serve small and mid-sized enterprises. Online B2B portals, cloud-based inventory tools, and remote dispenser monitoring are cutting transaction friction, nudging procurement away from purely offline channels.

Key Report Takeaways

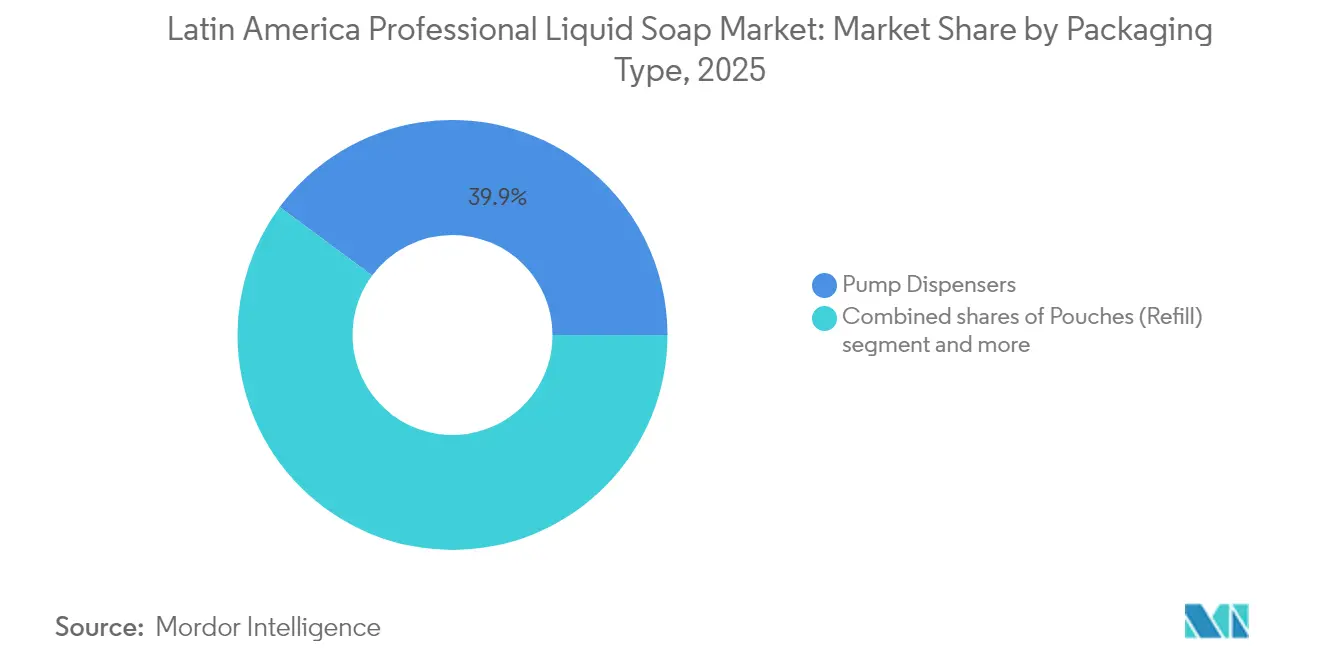

- By packaging type, pump dispensers led with 39.86% of the Latin America professional liquid soap market share in 2025, while refill pouches are advancing at an 8.79% CAGR to 2031.

- By product type, gel-based soaps accounted for 51.05% of the Latin America professional liquid soap market size in 2025; foaming soaps are on track for a 9.24% CAGR through 2031.

- By category, conventional formulas held a 69.25% share in 2025, whereas natural or organic lines are expanding at a 9.12% CAGR.

- By price tier, mass options captured 64.31% share in 2025, and premium lines are growing at a 9.74% CAGR through 2031.

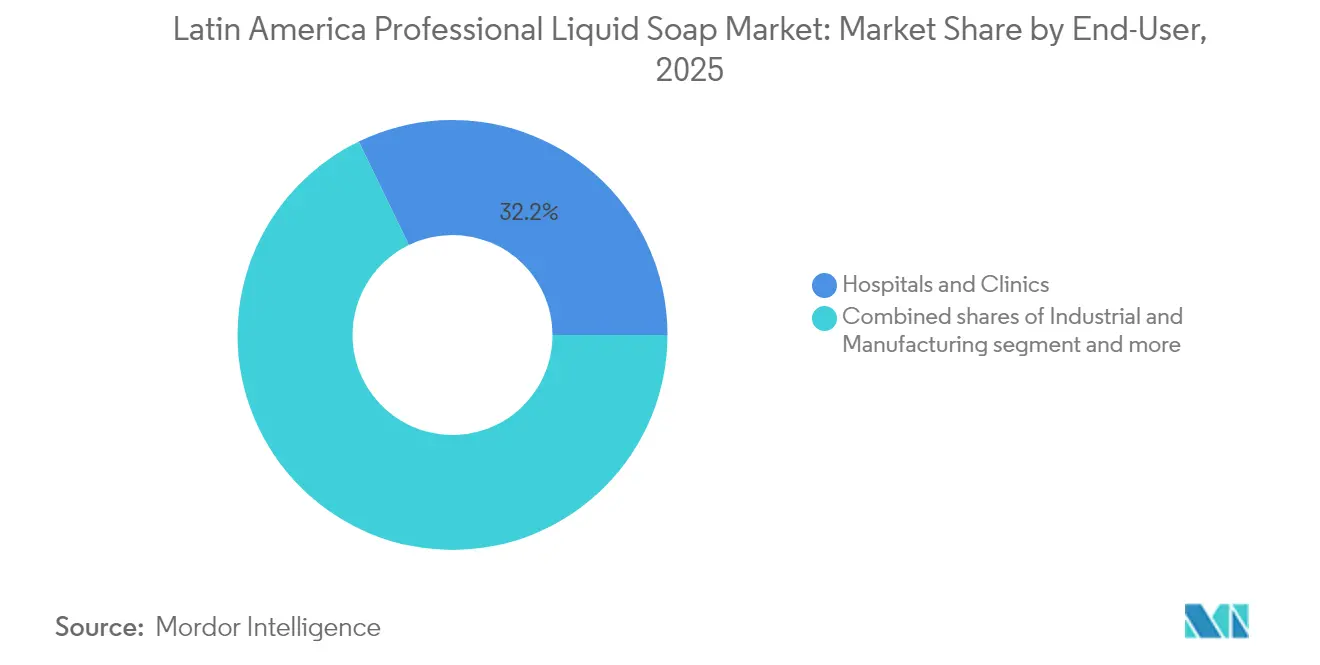

- By end user, hospitals and clinics made up 32.18% of 2025 revenues, yet industrial and manufacturing facilities registered the fastest 9.96% CAGR to 2031.

- By distribution channel, offline channels retained a 67.10% share in 2025, while online B2B procurement is climbing at a 9.31% CAGR.

- By geography, Brazil commanded 41.78% share in 2025; Argentina records the highest 9.05% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Latin America Professional Liquid Soap Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of hotels and the hospitality sector | +1.8% | Brazil, Mexico, Argentina, Colombia (Bogotá, Cartagena, Medellín) | Medium term (2-4 years) |

| Increasing adoption of touchless/automatic dispensers | +2.1% | Global, with early gains in Brazil, Mexico, Chile, healthcare and corporate sectors | Short term (≤2 years) |

| Growing demand for antibacterial and antimicrobial soaps | +1.5% | Brazil, Argentina, Peru, healthcare facilities, PAHO-aligned countries | Short term (≤2 years) |

| Demand for eco-friendly and biodegradable liquid soaps | +1.4% | Brazil (Green Seal Program), Argentina, Chile; spillover to Colombia, Peru | Medium term (2-4 years) |

| Social media and public campaigns promoting hand hygiene | +0.9% | Global, with concentrated impact in Brazil, Mexico, Argentina urban centers | Long term (≥4 years) |

| Enhanced skin-friendly and moisturizing product offerings | +0.6% | Premium hospitality and corporate segments in São Paulo, Buenos Aires, and Santiago | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of hotels and hospitality sector

Hilton reported nearly 280 hotels operating in Central and Latin America by the end of 2024, adding over 60 new properties during the year and signing agreements for approximately 6,000 rooms from 2024 deals alone; Mexico surpassed 100 hotels with roughly 40 more planned, while Brazil expanded to 25 hotels with 20 additional properties in the pipeline. This surge in branded hospitality infrastructure is elevating demand for premium liquid soap amenities, vegan, pH-balanced, PETA-certified formulations in eco-friendly sachets, that differentiate guest experiences and align with corporate sustainability pledges. Luxury and lifestyle segments are growing fastest, with properties in São Paulo, Buenos Aires, Cartagena, and Santiago specifying Cradle to Cradle Gold-certified or USDA BioPreferred formulations to appeal to environmentally conscious travelers. The shift is not merely cosmetic; hotels are bundling touchless dispensers with refillable cartridges to reduce single-use plastic waste, a move that lowers long-run procurement costs while meeting investor ESG expectations.

Increasing adoption of touchless/automatic dispensers

GOJO's January 2024 launch of the PURELL ES10 touch-free dispenser, featuring 30% less plastic and 38% lower greenhouse gas emissions versus the prior ES8 model, plus an integrated double-AA battery per refill and a complimentary Dispenser Advisor app for remote usage monitoring, exemplifies the technology race in professional hygiene. Healthcare facilities in Brazil and Mexico are prioritizing touchless systems to reduce cross-contamination; a Brazilian ICU study documented that RFID-enabled electronic hand-hygiene monitoring cut infection rates, while a Mexican pediatric hospital achieved USD 308,000 to USD 546,000 in savings over six months by deploying automated monitoring[2]Source: PAHO (Pan American Health Organization), "Bringing Health to Every Corner of the Americas", paho.org. Regulatory frameworks reinforce adoption: Brazil's NR-32 mandates hand-hygiene protocols for healthcare workers, Mexico's NOM-017-STPS-2008 requires personal protective equipment in industrial settings, and Argentina's Law 24,557 governs occupational risk prevention [3]Source: Brazilian Government, "Brazil Services and Information", gov.br. The confluence of labor shortages, exacerbated by post-pandemic attrition, and stringent hygiene audits is pushing facility managers to invest in IoT-enabled dispensers that alert staff when refills are needed, minimizing stockouts and ensuring compliance during surprise inspections.

Growing demand for antibacterial and antimicrobial soaps

Brazil's National Patient Safety Program (PNSP) and Mexico's "Lávate las Manos" school campaigns maintain public awareness, translating into sustained demand for antibacterial formulations in professional settings. Ecolab's July 2024 launch of Disinfectant 1 Wipe, the first EPA-registered, 100% plastic-free, readily degradable wipe with one-minute hospital disinfection against 40+ organisms and SARS-CoV-2 kill in 30 seconds, demonstrates how suppliers are bundling antimicrobial efficacy with sustainability credentials to win institutional contracts. The product's 94.3% relative biodegradation in 15 days under ASTM D5511 testing, versus 0.6% for standard plastic-based wipes, addresses packaging-waste concerns while meeting infection-control mandates. Colombia's INVIMA, Chile's ISP, and Peru's DIGEMID regulate hygiene products with varying stringency, but all reference WHO guidelines, creating a de facto regional standard that favors formulations with third-party ecolabel certifications (UL ECOLOGO, EPA Safer Choice, Cradle to Cradle). Industrial and manufacturing facilities, Chile's mining sector, Brazil's automotive plants, Argentina's food-processing hubs, are adopting antimicrobial soaps to comply with ILO occupational-safety frameworks, which cite 2.9 million work-related deaths and 402 million non-fatal injuries annually worldwide, with Latin America exhibiting high accident rates.

Demand for eco-friendly and biodegradable liquid soaps

Brazil's Decree 12,688, enacted in 2025, imposes mandatory reverse logistics for plastic packaging starting in 2026, with recovery targets escalating from 32% in 2026 to 50% by 2040 and recycled-content mandates rising from 22% to 40% over the same period, according to the Brazilian Government. The decree's National Circular Economy Strategy (ENEC) framework compels professional hygiene suppliers to redesign packaging and formulations for end-of-life recyclability, accelerating the shift toward refill pouches and concentrated formulations. By 2024, GOJO reported 69% of sales from certified products and a 6.7% reduction in chemicals of concern versus the 2021 baseline, with hundreds of SKUs holding Cradle to Cradle Gold certification. Unilever's February 2025 announcement of refill-solution pilots to tackle plastic waste, coupled with its global commitment to increase recycled plastic content and eliminate problematic plastics, signals that reuse and refill models will become standard in Latin America's professional hygiene channels. These certifications are increasingly specified in public-sector tenders and corporate procurement policies, creating a two-tier market where uncertified products face margin compression.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from bar soaps or alternative sanitizers | -0.8% | Rural and budget-constrained public institutions across Latin America | Medium term (2-4 years) |

| Packaging waste concerns from single-use containers | -0.6% | Brazil (Decree 12,688), Argentina, Chile; regulatory pressure spreading regionally | Short term (≤2 years) |

| High initial cost of touchless dispensing systems | -0.5% | Public hospitals, schools in Peru, Colombia, and smaller municipalities across the region | Short term (≤2 years) |

| Sensitivity of some users to chemicals and fragrances | -0.3% | Healthcare and educational institutions with vulnerable populations (pediatrics, elderly care) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Packaging waste concerns from single-use containers

Brazil's Green Seal Program, launched in June 2024 with standards expected in H1 2025, will formalize sustainability criteria for hygiene products, pressuring suppliers to demonstrate lifecycle assessments and circular-design credentials. Refill pouches, growing at 8.84% CAGR, offer a lower-plastic-mass alternative to rigid pump dispensers, with Dr. Bronner's paperboard gable-top refill carton (69% FSC-certified paper, 5% aluminum, 26% polyethylene) achieving 90% plastic reduction versus a 32-oz rPET bottle and avoiding over 27,000 pounds of plastic since launch. Evonik's REWOFERM biosurfactant platform, featuring glycolipid-based sophorolipids and rhamnolipids, enables laundry and hygiene pouches with superior biodegradability and mildness, positioning natural ingredients as performance-competitive with synthetic surfactants. The challenge lies in consumer and facility-manager education: pouches are unsuitable for wet environments and require durable reusable bottles, necessitating on-pack QR codes linking to lifecycle assessments and recycling instructions to avoid greenwashing accusations.

High initial cost of touchless dispensing systems

While touchless dispensers deliver long-term savings through reduced soap waste and lower infection rates, the upfront capital expense, ranging from USD 50 to USD 200 per unit plus installation, remains prohibitive for budget-constrained public hospitals, schools, and municipal facilities in Peru, Colombia, and smaller Argentine provinces. Ecolab's dispenser lead times of approximately three weeks and Diversey's 12-week lead times further complicate procurement cycles, particularly when facilities lack in-house technical staff to conduct site surveys and manage installations. SC Johnson's partnership with R-Zero, announced in November 2023, integrates occupancy sensors, indoor air quality monitoring, and UV-C disinfection into a unified platform, but the bundled solution's complexity and cost limit uptake to large healthcare systems and corporate campuses. Regional suppliers like Reynera in Mexico and Proeco Químicas offer lower-cost manual dispensers and training programs to distributors, capturing share in price-sensitive segments. The disparity in adoption rates between private and public sectors is widening luxury hotels and multinational corporate offices deploy IoT-enabled dispensers with real-time analytics, while public schools and rural clinics continue using manual pump dispensers or bar soaps, perpetuating hygiene gaps that regulatory audits struggle to close.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Refill Pouches Gain Momentum as Circular-Economy Mandates Tighten

Pump dispensers commanded 39.86% market share in 2025, entrenched by decades of institutional procurement inertia and compatibility with existing dispenser infrastructure in hospitals, hotels, and offices. Yet refill pouches are expanding at 8.79% CAGR through 2031, driven by Brazil's Decree 12,688 mandating escalating recycled-content and recovery targets, and corporate sustainability pledges from Unilever, Kimberly-Clark, and regional players. Bottles and containers for refill applications hold a steady share in facilities that prefer bulk purchasing and on-site refilling to minimize packaging waste, particularly in industrial and manufacturing settings where high-volume usage justifies dedicated storage.

Pouches, including sachets and mini travel packs, are proliferating in hospitality amenities, with 10 ml and 30 ml formats offering single-use convenience for guests while reducing plastic mass per dose compared to rigid bottles. Others (bulk tanks, cartridge systems) serve niche applications in food processing and pharmaceutical manufacturing, where closed-loop dispensing prevents contamination. The shift toward pouches is not uniform: Argentina's import liberalization has flooded the market with low-cost rigid bottles from Asia, temporarily slowing pouch adoption, while Chile's mining sector favors rugged pump dispensers that withstand harsh environments. Suppliers are responding with hybrid models, refillable pump dispensers accepting pouch inserts, to bridge the transition, though compatibility issues and consumer confusion around recycling instructions remain barriers.

By Product Type: Foaming Soaps Outpace Gel Variants on Water-Efficiency and User-Experience Gains

Gel-based soaps held a 51.05% share in 2025, reflecting their versatility across end-users and compatibility with legacy dispensers, but foaming soaps are surging at a 9.24% CAGR, propelled by water-efficiency mandates and superior user perception. CWS PureLine Foam's 30% water-consumption reduction and 50% soap-consumption reduction per wash resonate with facilities facing rising utility costs and sustainability audits. Foaming formulations deliver perceived luxury, richer lather, softer feel, at lower cost per dose, a combination that appeals to premium hospitality and corporate segments.

Cream-based soaps, though smaller in share, serve specialized applications in healthcare and industrial settings where emollient properties reduce dermatitis risk among workers performing frequent handwashing; Brazil's NR-32 and Mexico's NOM-017-STPS-2008 occupational-safety standards increasingly specify skin-friendly formulations to mitigate chemical-sensitivity claims. Gel-based variants retain dominance in foodservice and restaurant back-of-house applications, where viscosity aids adherence to hands during scrubbing protocols, but the gap is narrowing as foam dispensers become more affordable and reliable.

By Category: Natural/Organic Surge Reflects Certification-Driven Procurement Shifts

Regular/conventional formulations held 69.25% share in 2025, anchored by price competitiveness and established supply chains, yet natural/organic variants are expanding at 9.12% CAGR, driven by COSMOS v3 certification uptake in Colombia, Brazil's Law 10,831 organic labeling, and public-sector tenders specifying eco-certified products. QIMA's Natural Ingredients Mark and ABNT certifications are gaining traction as procurement officers seek third-party validation to avoid greenwashing accusations. Evonik's REWOFERM rhamnolipids, renewably sourced, readily biodegradable, with excellent foaming and cleaning properties, enable natural formulations that match synthetic performance, eroding the historical trade-off between sustainability and efficacy.

Premium hospitality chains in São Paulo, Buenos Aires, and Cartagena are specifying vegan, PETA-certified, fragrance-free formulations to cater to wellness-focused travelers and comply with investor ESG mandates. The challenge lies in cost: natural/organic soaps command 15-25% price premiums, limiting penetration in mass segments and public institutions. Regional players like Fuller Pinto in Colombia and Daryza in Peru are formulating hybrid products, partially bio-based surfactants blended with conventional ingredients, to offer mid-tier pricing while capturing the "natural" label, though purists question such formulations' authenticity. Regulatory harmonization across Mercosur and the Andean Community could accelerate natural/organic adoption by reducing certification complexity, but progress remains slow.

By Price: Premium Segment Expands as Hospitality and Corporate Buyers Prioritize Brand Differentiation

Mass-market offerings held a 64.31% share in 2025, serving price-sensitive public hospitals, schools, and budget hotels, but the premium segment is growing at a 9.74% CAGR, fueled by luxury hospitality expansion and corporate wellness programs. Hilton's addition of over 60 properties in 2024, with strong luxury/lifestyle segment growth, exemplifies how branded chains specify premium formulations, Cradle to Cradle Gold, USDA BioPreferred, vegan-certified, to differentiate guest experiences and justify higher room rates. Corporate offices in São Paulo, Buenos Aires, and Santiago are upgrading restroom amenities to attract and retain talent, with touchless dispensers and premium soaps signaling investment in employee well-being.

The premium segment's margin structure, 30-40% gross margins versus 15-20% for mass, incentivizes suppliers to invest in R&D, certifications, and digital service layers. Ecolab's eROI (exponential return on investment) model, which quantifies business and sustainability outcomes for customers, enables premium pricing by demonstrating total cost of ownership advantages: lower infection rates, reduced water/energy consumption, and enhanced brand reputation. The bifurcation is sharpening: premium buyers demand transparency (ingredient disclosure, lifecycle assessments, supply-chain traceability), while mass buyers prioritize upfront cost, creating distinct go-to-market strategies.

By End User: Industrial/Manufacturing Facilities Emerge as Fastest-Growing Segment Amid Occupational-Safety Enforcement

Hospitals and clinics held a 32.18% share in 2025, reflecting legacy infection-control investments and PAHO-aligned hygiene mandates, but industrial and manufacturing facilities are expanding at a 9.96% CAGR, driven by occupational-safety enforcement and rising accident rates. ILO data citing 2.9 million work-related deaths and 402 million non-fatal injuries annually, with Latin America exhibiting high rates, has prompted governments to tighten regulations: Brazil's NR-32, Mexico's NOM-017-STPS-2008 and NOM-019-STPS-2011, Argentina's Law 24,557, Colombia's Resolution 2400, Chile's Law 16,744, and Peru's Law 29,783 all mandate hand-hygiene protocols in industrial settings.

Chile's mining sector, Brazil's automotive and food-processing plants, and Argentina's agribusiness facilities are installing touchless dispensers and antimicrobial soaps to reduce dermatitis claims and comply with audits. Hotels and resorts, restaurants and foodservice, and commercial offices each contribute mid-teens share, with growth tied to post-pandemic recovery and Hilton's regional expansion. Schools and universities, though smaller in share, are upgrading hygiene infrastructure under government programs, particularly in Brazil and Mexico, where "Lávate las Manos" campaigns have raised public awareness. Others, like airports, malls, transit stations, and gyms, are deploying touchless systems to manage high-traffic volumes and minimize cross-contamination, with Ecolab's Scientific Clean line targeting these channels via retail partnerships. The industrial/manufacturing surge underscores a broader shift: hygiene is no longer viewed solely as infection control but as a productivity and risk-management tool, with facility managers calculating ROI based on reduced absenteeism, lower workers' compensation claims, and improved audit scores.

By Distribution Channel: Online B2B Procurement Accelerates as Digital Platforms Reduce Transaction Friction

Offline channels held a 67.10% share in 2025, dominated by traditional distributors, wholesalers, and direct sales forces that serve institutional accounts with consultative selling and on-site service. Yet online channels are expanding at a 9.31% CAGR, driven by digital procurement platforms that reduce transaction costs and improve inventory visibility. Vileda's B2B/B2C platform, built on SAP Commerce Cloud and spanning 30-35 countries, enables customers to order professional cleaning products with real-time pricing and delivery tracking. Caromar in Argentina, operating a 15,000-SKU catalog from its new Buenos Aires distribution center, exemplifies how wholesalers are digitizing to capture e-commerce share while maintaining offline relationships. Proeco Químicas' distributor program, offering exclusive territories, professional support, continuous training, and merchandising assistance, demonstrates that hybrid models (online ordering, offline service) are emerging as the dominant go-to-market strategy.

Ecolab's November 2025 expansion with The Home Depot into Canada, bringing the Scientific Clean line to over 180 stores and online, illustrates how professional-grade products are penetrating retail channels, blurring B2B and B2C boundaries. The online shift is uneven: large corporate accounts and hotel chains prefer direct relationships with suppliers for customized formulations and service agreements, while small and medium enterprises (SMEs), restaurants, clinics, and boutique hotels favor online platforms for price transparency and convenience. Regulatory compliance (ANVISA, ANMAT, INVIMA registration) remains a gating factor, as online marketplaces struggle to verify product certifications, creating opportunities for specialized B2B platforms that integrate compliance checks into the purchasing workflow.

Geography Analysis

Brazil's 41.78% market share in 2025 stems from ANVISA's comprehensive regulatory framework, Good Manufacturing Practices, cosmetic registration, and the Chemical Substances Inventory Law, requiring ingredient registration for volumes exceeding one tonne per year, which compels facilities to source certified formulations and creates barriers to entry for unregistered suppliers. The country's National Patient Safety Program (PNSP) and Green Seal Program (launched June 2024, standards due H1 2025) further institutionalize hygiene and sustainability as procurement criteria. Unilever's May 2025 announcement of a USD 1.5 billion investment in Mexico, including a new factory, signals that multinationals view the region as a manufacturing hub for Latin America, with Brazil and Mexico accounting for half the projected 80 million population increase to 721 million by 2030.

Argentina, despite economic volatility, is the fastest-growing geography at 9.05% CAGR, propelled by the OECD's July 2025 Economic Survey projecting GDP growth of 5.2% in 2025 and 4.3% in 2026, alongside trade liberalization that slashed tariffs on over 90 product lines, eliminated the 7.5% PAIS import tax, removed import licensing (SIRA), and lifted most capital controls under the April 2025 IMF program. Procter & Gamble's July 2024 divestiture of its Argentina operations, completing a portfolio rationalization, contrasts with the market's growth trajectory, creating white space for regional players like Prolimp del Centro and Mex-Ar Productos to expand share. Colombia, Chile, and Peru collectively contribute mid-teens share, with each exhibiting distinct drivers. Colombia's INVIMA regulates cosmetics and hygiene products, and the country's hospitality sector in Bogotá, Cartagena, and Medellín is expanding rapidly; Fuller Pinto, a Colombian manufacturer with 1,200 SKUs and presence in 21 countries, exemplifies regional champions leveraging local distribution and product breadth.

Competitive Landscape

Market concentration signals moderate fragmentation with global majors, Kimberly-Clark, GOJO, Ecolab, Henkel, Unilever, Procter & Gamble, Reckitt, Colgate-Palmolive, competing alongside regional specialists like Prolimp del Centro, Mex-Ar Productos, Fuller Pinto, and Daryza. Kimberly-Clark's May 2025 agreement to sell 51% of its International Family Care & Professional business to Suzano for USD 1.734 billion, valuing the joint venture at USD 3.4 billion, will reshape competitive dynamics; the deal covers 22 plants in 14 countries, approximately 9,000 employees, and roughly one million tonnes of capacity.

Ecolab operates a service-led, consumable-focused model supported by digital monitoring (ECOLAB3D) and eROI quantification, enabling premium pricing and sticky customer relationships. Henkel's Latin America operations generated EUR 2.1 billion in 2024, with Adhesive Technologies posting 7% organic growth and Consumer Brands 3.5%, leveraging brands like Persil, Pril, and Bref in laundry and home care. Reckitt's Latin America segment contributed significantly in 2024, with the Hygiene segment (Dettol, Lysol, Harpic, Finish) accounting for a significant share of total revenue and posting mid-single-digit growth.

Colgate-Palmolive's Latin America operations delivered significant share in net sales in 2024, the prominent among major consumer-goods companies in the region; Home Care represents a significant share of global sales, indicating strong penetration in professional hygiene channels. Strategy patterns center on bundling IoT-enabled dispensers with certified refills and digital service layers (usage analytics, predictive maintenance, compliance reporting) to lock in corporate and healthcare accounts. Opportunities exist in public-sector procurement, schools, municipal facilities, rural clinics, where budget constraints limit touchless-dispenser adoption, and in natural/organic segments where certification complexity deters smaller suppliers. Emerging disruptors include regional players like Fuller Pinto and Reynera (Mexico), which leverage localized distribution, flexible minimum order quantities, and training programs to capture SME accounts that global majors under-serve.

Latin America Professional Liquid Soap Industry Leaders

-

Kimberly‑Clark

-

Henkel AG & Co. KGaA

-

Colgate‑Palmolive Company

-

Procter & Gamble

-

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: Reckitt Pro Solutions has launched Dettol Pro Cleanse Liquid Hand Wash, its inaugural hand wash tailored exclusively for professional settings. The product is now available in two sizes: a 5-liter unit and a convenient 500ml hand pump.

- February 2024: For the third straight year, Dial®, a trusted American brand for over 75 years, clinched the prestigious 2024 Product of the Year USA Awards. The revamped Dial® Hand Soap, now boasting antibacterial liquid and foaming formulas enriched with aloe, and packaged in ergonomically designed bottles made from 100% PCR Plastic, has been crowned the top product in the Hand Soap category.

Latin America Professional Liquid Soap Market Report Scope

Professional liquid soap is a fluid cleansing agent, made from fats/oils reacted with an alkali (like potassium hydroxide), formulated for frequent, hygienic use in commercial settings. The Latin America professional liquid soap market is segmented by packaging type, product type, category, price, end-user, distribution channel, and geography. By packaging type, the market is segmented into pump dispensers and others. By product type, the market is segmented into foaming soaps and more. By category, the market is segmented into regular/conventional and natural/organic. By price, the market is segmented into mass and premium. By end-user, the market is segmented into hospitals and clinics, and more. By distribution channel, the market is segmented into online channels and offline channels. By geography, the market is segmented into Brazil and more. The market forecasts are provided in terms of value (USD).

| Pump Dispensers |

| Bottles/Containers (Refill) |

| Pouches (Refill) |

| Others |

| Foaming Soaps |

| Gel-Based Soaps |

| Cream-Based Soaps |

| Regular/Conventional |

| Natural/Organic |

| Mass |

| Premium |

| Hospitals and Clinics |

| Hotels and Resorts |

| Restaurants and Food Services |

| Commercial Offices and Corporate Buildings |

| Schools and Universities |

| Industrial and Manufacturing Facilities |

| Others |

| Online Channel |

| Offline Channel |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| Packaging Type | Pump Dispensers |

| Bottles/Containers (Refill) | |

| Pouches (Refill) | |

| Others | |

| Product Type | Foaming Soaps |

| Gel-Based Soaps | |

| Cream-Based Soaps | |

| Category | Regular/Conventional |

| Natural/Organic | |

| Price | Mass |

| Premium | |

| End User | Hospitals and Clinics |

| Hotels and Resorts | |

| Restaurants and Food Services | |

| Commercial Offices and Corporate Buildings | |

| Schools and Universities | |

| Industrial and Manufacturing Facilities | |

| Others | |

| Distribution Channel | Online Channel |

| Offline Channel | |

| Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the Latin America professional liquid soap market in 2026?

The market is valued at USD 1.47 billion in 2026 and is set to keep expanding at an 8.61% CAGR.

Which country leads regional sales?

Brazil accounts for 41.78% of regional revenue thanks to stringent ANVISA standards and high institutional penetration.

What packaging format is growing fastest?

Refill pouches show the fastest growth at an 8.79% CAGR because of Brazil’s recycled-content mandates.

Page last updated on: