Hand Wash Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

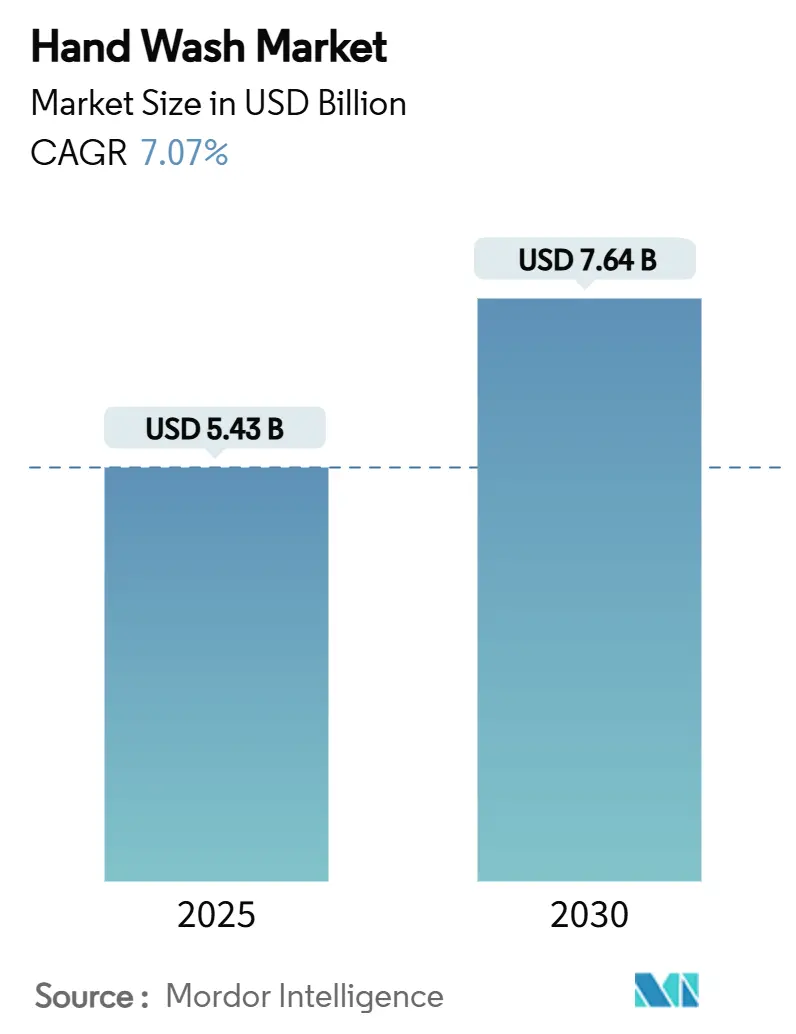

| Market Size (2025) | USD 5.43 Billion |

| Market Size (2030) | USD 7.64 Billion |

| Growth Rate (2025 - 2030) | 7.07% CAGR |

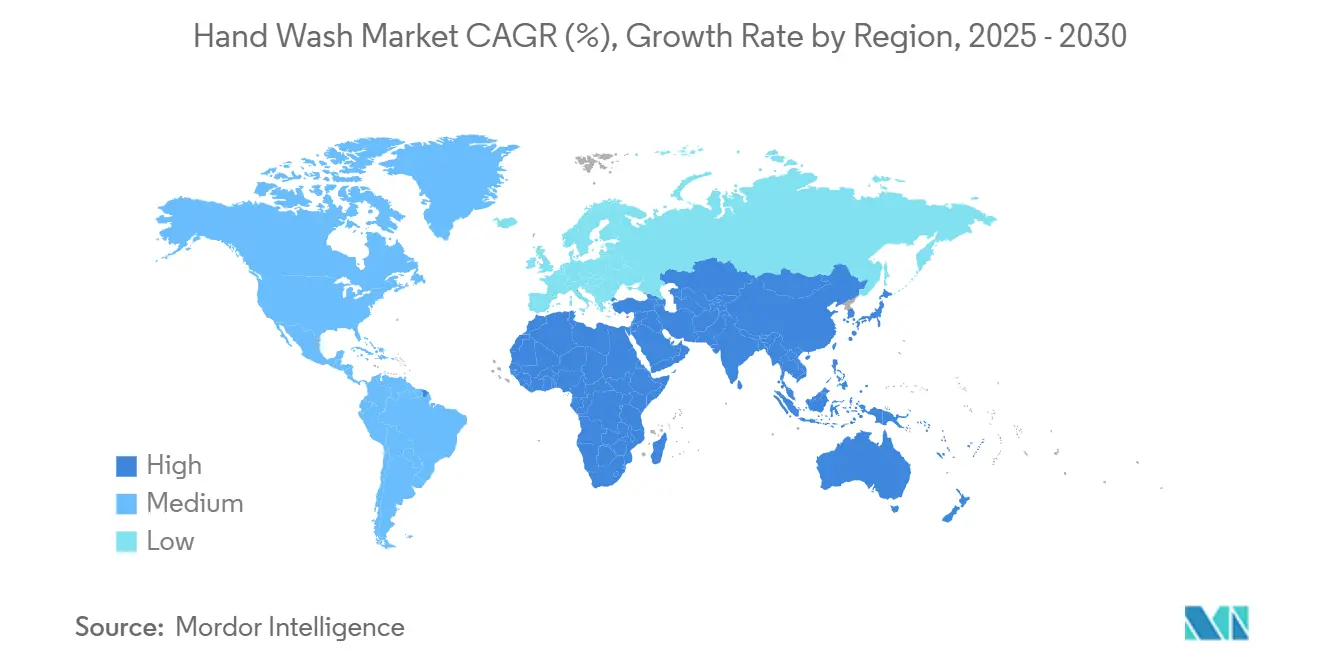

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

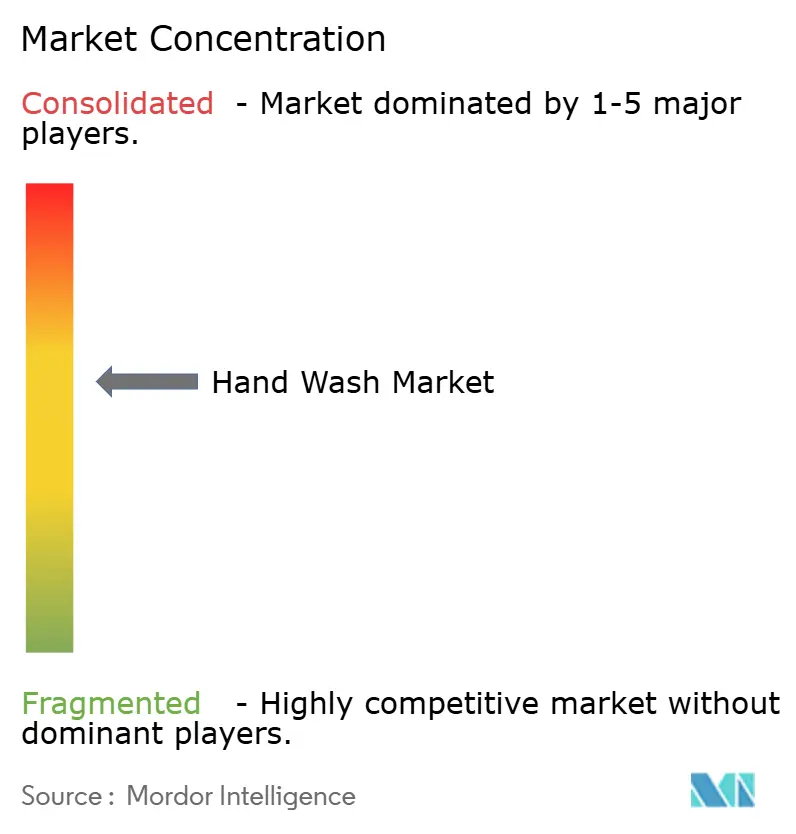

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hand Wash Market Analysis by Mordor Intelligence

The global hand wash market, valued at USD 5.43 billion in 2025, is projected to grow to USD 7.64 billion by 2030, with a CAGR of 7.07%. This growth reflects a shift from temporary, pandemic-driven demand to a sustained focus on personal hygiene, establishing hand washing as a routine necessity for consumers. Key factors driving this expansion include stricter government regulations, the introduction of high-quality and premium products, and increased accessibility through diverse distribution channels. While liquid hand wash remains the most widely used format, alternative options such as natural, foam, and cartridge-based products are gaining popularity due to growing consumer and institutional emphasis on sustainability. Additionally, evolving regulatory standards, such as the FDA’s Modernization of Cosmetics Regulation Act and the EU Chemicals Strategy for Sustainability, are raising compliance costs. This trend is creating a competitive advantage for established players who are better equipped to meet these requirements.

Key Report Takeaways

- By category, conventional formulations held 84.53% of the hand wash market share in 2024; natural/organic options are advancing at a 7.52% CAGR through 2030.

- By product form, liquids accounted for 61.23% of the hand wash market size in 2024, while foam variants posted the fastest 8.61% CAGR to 2030.

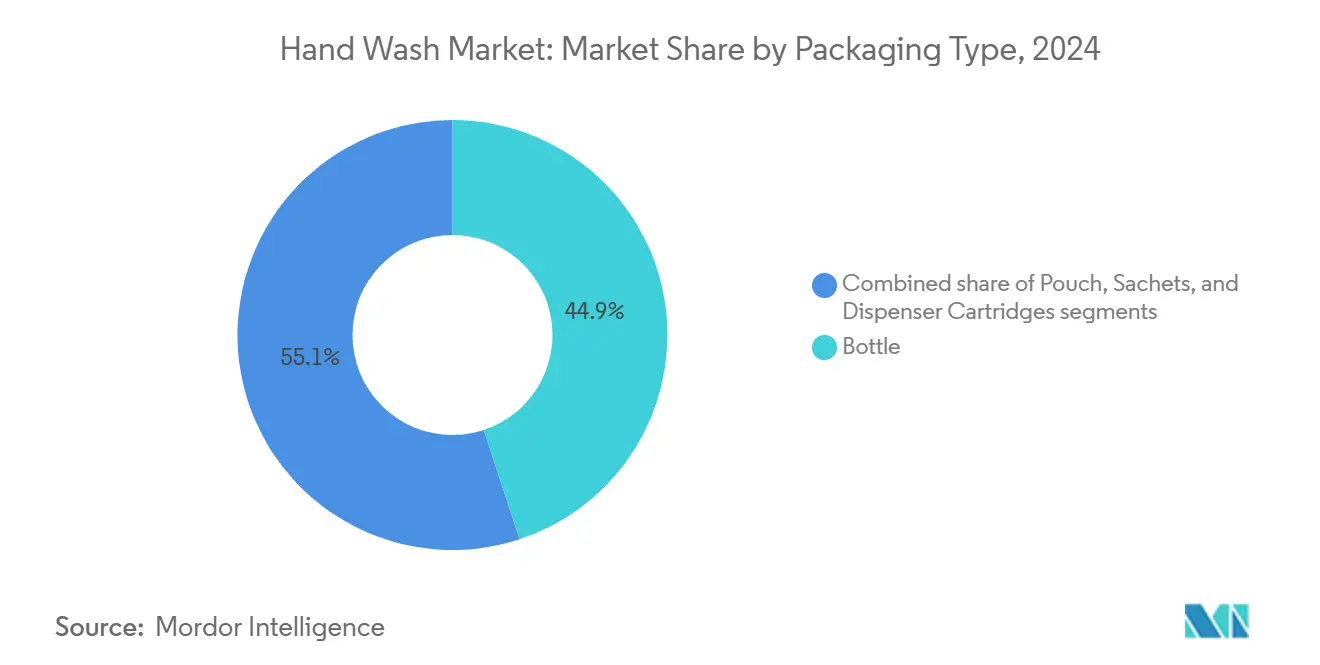

- By packaging, traditional bottles captured 44.93% of the hand wash market size in 2024, whereas dispenser cartridges expand at a 9.43% CAGR through 2030.

- By distribution channel, offline retail retained 75.62% revenue share in 2024; online sales represent the quickest route forward at a 9.01% CAGR through 2030.

- By geography, North America led with 31.86% hand wash market share in 2024, while Asia-Pacific advances at an 8.36% CAGR between 2025 and 2030.

Global Hand Wash Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing preference for natural and eco-friendly solutions | +1.2% | Global, with premium concentration in North America and Europe | Medium term (2-4 years) |

| Frequent public health campaigns | +0.8% | Global, with healthcare system emphasis in developed markets | Short term (≤ 2 years) |

| Rising e-commerce penetration for personal care | +1.1% | Asia-Pacific core, spill-over to Middle East and Africa and Latin America | Medium term (2-4 years) |

| Social influence and lifestyle shifts | +0.9% | Urban centers globally, youth demographics in Asia-Pacific | Long term (≥ 4 years) |

| Technological and formulation innovation | +1.3% | North America and Europe innovation hubs, manufacturing in Asia-Pacific | Long term (≥ 4 years) |

| Impact of epidemics and pandemics | +0.7% | Global, with institutional focus in healthcare systems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing preference for natural and eco-friendly solutions

Consumer demand for natural and organic personal care ingredients is rising, with companies like Seventh Generation benefiting significantly by offering products such as hand wash formulations with 97% USDA Certified Biobased Product content. This trend reflects growing consumer distrust, especially among millennials and Gen Z, towards synthetic preservatives and chemical additives. In 2024, Millennials made up 21.81% of the U.S. population, while Gen Z accounted for 20.81%, according to the US Census Bureau[1]US Census Bureau, "Population distribution in the United States in 2024, by generation", census.gov. These groups increasingly value ingredient transparency and environmental sustainability. However, manufacturers face challenges in ensuring ethical sourcing. Research highlights that closer connections between producers and consumers can reduce the risk of unethical practices. On the regulatory side, frameworks like the European Green Deal's Chemicals Strategy for Sustainability are driving changes in ingredient sourcing. The shift from specific risk assessments to a broader Generic Risk Approach is pushing brands to rethink their formulations. Meanwhile, companies adopting plant-based surfactants and biodegradable packaging are not only meeting regulatory requirements but also appealing to consumers willing to pay more for sustainable products. This dual focus on compliance and consumer preference positions these companies to thrive in the evolving market.

Frequent public health campaigns

Institutional hand hygiene campaigns continue to drive demand for hand wash products beyond the pandemic-related surge. The CDC's Clean Hands Count campaign provides targeted educational and promotional materials for healthcare providers and patients. Similarly, the WHO's 2025 World Hand Hygiene Day initiative prioritizes compliance monitoring, with 68% of countries currently reporting such practices, ensuring consistent demand in healthcare facilities. These campaigns establish procurement protocols and compliance standards, embedding hand wash usage in healthcare, education, and hospitality sectors[4]World Health Organization, "World Hand Hygiene Day - 5 May 2025 #handhygiene", www.who.int. The Pan American Health Organization integrates hand hygiene into national infection prevention strategies, creating policy-driven demand that remains resilient during economic downturns. Social media further amplifies these efforts, with hashtags like #CleanHandsCount boosting awareness, influencing consumer behavior, and shaping institutional policies.

Rising e-commerce penetration for personal care

The hand wash market is experiencing significant growth, particularly in Asia-Pacific, where mobile-first consumers are adopting omnichannel shopping. This growth is driven by the increasing popularity of subscription models and the convenience of bulk purchasing. The expansion of e-commerce allows brands to implement direct-to-consumer strategies, bypassing traditional retail margins. These cost savings are being reinvested in developing innovative formulations and sustainable packaging solutions. Additionally, companies are leveraging consumer purchasing data to improve product development and manage inventory more effectively. Predictive analytics is playing a crucial role in enhancing demand forecasting, giving companies a competitive edge. Online platforms are also enabling premium and niche brands, which often lack access to traditional retail distribution, to enter the market. This has intensified competition and encouraged innovation across different price segments. To meet consumer expectations for fast delivery, companies are focusing on optimizing their supply chains. This creates opportunities for regional manufacturers and private label producers, who can offer competitive pricing and faster delivery due to shorter logistics chains.

Social influence and lifestyle shifts

Advanced formulation technologies are transforming market dynamics by improving product efficacy and enhancing user experiences. For instance, Procter & Gamble has introduced micellar deep cleansing technology, which uses micelle structures to effectively attract and remove dirt and bacteria. In the field of antimicrobial solutions, innovations now go beyond traditional antibacterial agents. They include zinc-aminoclay compounds and natural extracts like Opuntia humifusa, which not only maintain antimicrobial effectiveness but also provide moisturizing benefits. Foam technology has also seen significant advancements, with the development of formulations containing 90% biobased content. These formulations exceed USDA standards, offer controlled dispensing, and improve users' perception of cleansing performance. Additionally, packaging innovations are combining sustainability with functionality. A notable example is energy-on-the-refill technology, which reduces battery waste by 68% compared to conventional dispenser systems. These technological advancements offer companies opportunities to differentiate themselves by investing in Research and Development, while also setting high-performance standards that smaller players may find challenging to meet without substantial capital investment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer perception of safety and efficacy | -0.6% | Global, with regulatory scrutiny in developed markets | Medium term (2-4 years) |

| Ingredient sourcing and supply chain vulnerabilities | -0.9% | Global, with concentration risk in APAC manufacturing | Short term (≤ 2 years) |

| Regulatory and compliance complexities | -0.7% | North America and EU regulatory frameworks, spill-over to APAC | Medium term (2-4 years) |

| Allergenicity and fragrance sensitivities | -0.4% | Global, with higher impact in developed markets with sensitive demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Consumer perception of safety and efficacy

Consumer skepticism toward antibacterial formulations is growing as scientific studies question their added health benefits compared to plain soap. Research from the CDC indicates no significant advantage for consumers using antibacterial soaps, which has shifted consumer perception. This change is pressuring manufacturers to reformulate their products and revise marketing strategies, leading to higher development costs and potential market share losses, particularly for brands heavily reliant on antibacterial positioning. Regulatory agencies are also increasing scrutiny of antimicrobial claims, requiring evidence that many companies cannot provide. This has resulted in additional reformulation expenses and heightened legal risks. At the same time, the demand for "free-from" formulations is rising, as consumers prefer products without harsh preservatives, synthetic dyes, or artificial fragrances. This trend limits formulation choices and raises ingredient costs for manufacturers. Companies must now navigate the challenge of delivering effective products while meeting consumer preferences for gentle and natural formulations. These demands create significant R&D challenges, requiring substantial investment with no assurance of market acceptance.

Ingredient sourcing and supply chain vulnerabilities

Global supply chain disruptions are creating significant challenges for the beauty industry, including rising costs, geopolitical instability, and complex sourcing issues. These factors are pushing companies to expand their supplier networks and implement cost-control strategies to remain competitive. Sourcing natural ingredients is particularly difficult, as the growing demand exceeds the capacity for sustainable supply. This imbalance leads to price volatility and inconsistent quality, which disrupt product development schedules and reduce profit margins. Additionally, regulatory compliance adds another layer of complexity. Different regions enforce varying standards for ingredient safety and environmental impact, requiring companies to manage multiple product formulations and maintain detailed documentation systems. The Independent Beauty Association highlights the importance of multi-year contracts to stabilize costs, but smaller companies often lack the bargaining power to secure favorable terms, putting them at a competitive disadvantage. To reduce tariff risks, some companies are exploring alternative sourcing options outside China. However, this shift results in higher costs and longer approval times for new suppliers, which temporarily limits growth opportunities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Category: Conventional Dominance Faces Natural Disruption

In 2024, conventional hand wash formulations dominate the market with an 84.53% share, driven by their affordability, reliability, and consumer familiarity. These products use proven surfactant systems and antimicrobial agents, ensuring consistent performance. Economies of scale enable cost-efficient production and global standardization, supported by strong distribution networks and marketing by major FMCG companies like Procter & Gamble. For instance, Safeguard offers antibacterial formulas with skin conditioners to prevent dryness. Regulatory clarity and established supply chains further strengthen this segment. However, concerns over synthetic preservatives and environmental impact are rising. CDC research shows no added health benefits of antibacterial soaps over plain soap, but market leaders retain their position through strong branding and competitive pricing that appeals to value-conscious consumers.

The natural and organic hand wash segment is growing at a 7.52% CAGR through 2030, driven by demand for sustainable and transparent products. Brands like Seventh Generation lead with plant-based formulations, achieving 97% USDA Certified Biobased Product content, free from dyes and synthetic fragrances, while ensuring effective bacterial removal. Certifications like ECOLOGO and EPA Safer Choice enhance credibility, and investments in sustainable sourcing provide a competitive edge. However, challenges like ethical sourcing and price volatility of natural ingredients limit faster growth. The trend toward "free-from" products shows consumers are willing to pay more for gentle, effective, and environmentally friendly options, creating opportunities for brands that balance efficacy with natural positioning.

By Product Form: Liquid Leadership Challenged by Foam Innovation

In 2024, liquid formulations command a dominant 61.23% market share, underscoring their consumer-favored versatility and seamless integration with existing dispensers and packaging. This leadership is bolstered by manufacturing efficiencies, cost-effective production, and a robust supply chain, all catering to a consumer preference for traditional liquid cleansing. Liquid formulations boast the flexibility to incorporate a range of ingredients, from standard surfactants to premium natural extracts, allowing brands to target diverse market segments from a single production line. Colgate-Palmolive capitalizes on this liquid dominance, with brands like Palmolive, Protex, and Softsoap, solidifying their presence in the global liquid hand soap market. The enduring appeal of the liquid segment is evident in its retail compatibility, facilitating broad distribution and promotional efforts.

Foam formulations are set to be the fastest-growing product, projected to expand at an 8.61% CAGR through 2030. This surge is largely attributed to institutions, especially in healthcare and hospitality, favoring foam for its controlled dispensing, which curbs waste and bolsters hygiene. Leveraging advanced foam technology, some formulations boast 90% biobased content, surpassing USDA standards. Brands like WAXIE Select are leading the charge, offering hypoallergenic foams devoid of harsh preservatives, ensuring a superior lather and efficacy. The appeal of foam extends to its water-saving benefits, with systems conserving an estimated 6 gallons per refill compared to standard soap, resonating with eco-conscious consumers. Innovations like energy-on-the-refill technology slash battery waste by 68%, and automated dispensers not only elevate user experience but also ensure compliance in institutional settings. In manufacturing, advancements enable precise dosage and contamination prevention, crucial for healthcare settings where hand hygiene is paramount to patient safety.

By Packaging Type: Sustainability Drives Dispenser Innovation

In 2024, traditional bottles hold a 44.93% market share due to their widespread consumer acceptance and compatibility with retail distribution channels. Their dominance is supported by cost-effective production enabled by established manufacturing systems and consumer preference for portable, resealable containers suitable for home and travel use. Sustainability concerns are driving innovation in this segment. For example, Waitrose introduced recyclable pumps for its handwash range, preventing over a ton of packaging waste annually while maintaining convenience. Companies are focusing on recycled materials and refillable designs to address environmental issues. Dial’s concentrated refills, which use 95% less plastic, and partnerships with organizations like Plastic Bank and TerraCycle highlight efforts to promote a circular economy. The segment remains resilient due to its versatility, accommodating various formulations and usage occasions while benefiting from economies of scale to keep prices competitive.

Dispenser cartridges are the fastest-growing packaging format, with a 9.43% CAGR projected through 2030. This growth is driven by institutional demand for hygienic, refillable systems that reduce contamination risks and operational costs, particularly in healthcare and commercial settings. Sealed cartridge systems prevent soap contamination, require less maintenance time (6 seconds versus 30 seconds for bulk dispensers), and promote healthier hand-washing practices, reducing illness and absenteeism. Sustainability initiatives further boost this format, with innovations like energy-on-the-refill technology cutting battery waste by 68% compared to traditional systems. Advanced systems, such as PURELL's ES platform, offer SANITARY SEALED refills and AT-A-GLANCE monitoring, reducing contamination and providing over 30% more washes with 36% less product than lotion soap. Institutional buyers prefer these systems for their compliance monitoring capabilities and reduced labor costs associated with maintenance and refilling.

By Distribution Channel: Digital Acceleration Transforms Retail

In 2024, offline retail channels hold a significant 75.62% market share, driven by consumers' preference for immediate product availability and the ability to physically evaluate items, especially in personal care. These channels excel in providing brand visibility and encouraging impulse purchases, particularly in mass market segments where price and promotions heavily influence decisions. Strong manufacturer-retailer relationships ensure effective product placement, merchandising, and promotional activities across regions. Institutional buyers in sectors like healthcare, hospitality, and education rely on specialized distributors for bulk procurement and technical support. Companies such as Ecolab, with their Nexa dispensers offering high evacuation rates and antimicrobial features, cater to these needs. Offline retail remains resilient due to consumer comfort with in-store shopping and retailers' focus on hygiene product merchandising, which boosts brand visibility and sales conversions.

Online retail stores are growing rapidly, with a 9.01% CAGR projected through 2030. This growth is fueled by the convenience of subscription-based hygiene purchases and bulk ordering for institutions, supported by automated replenishment systems. E-commerce enables brands to bypass traditional retail margins, redirecting savings into product innovation and sustainable packaging while maintaining competitive pricing. Digital platforms also provide market access for premium and niche brands without traditional distribution networks, increasing competition and offering consumers specialized products like Bower Collective's eco-friendly refillable systems. Subscription models drive predictable revenue and customer loyalty while simplifying inventory management. Companies leverage data analytics to refine product development and improve demand forecasting. This growth reflects a shift in consumer behavior toward digital commerce and institutional buyers' preference for efficient procurement processes.

Geography Analysis

In 2024, North America holds a 31.86% market share, showcasing its mature market dynamics. Here, institutional demand from sectors like healthcare, education, and hospitality consistently drives purchasing volumes. The region's regulatory landscape, notably influenced by the FDA's Modernization of Cosmetics Regulation Act 2022, sets compliance benchmarks. This environment tends to favor established players with regulatory know-how, while posing challenges for smaller entrants[2]Food and Drug Administration, "Guidance for Industry: Registration and Listing of Cosmetic Product Facilities and Products", fda.gov. As consumers increasingly gravitate towards premium products boasting natural ingredients and eco-friendly packaging, brands are seizing the chance to stand out through innovation, sidestepping the pitfalls of price wars. While market growth shows signs of moderation due to saturation, trends like premiumization and heightened institutional hygiene standards continue to bolster value expansion. Furthermore, North America's sophisticated e-commerce framework bolsters direct-to-consumer initiatives and subscription models, amplifying customer loyalty and ensuring steady revenue streams.

Asia-Pacific is on a robust trajectory, boasting an 8.36% CAGR through 2030. This growth is fueled by urbanization, rising disposable incomes, and a harmonized regulatory landscape across ASEAN nations, simplifying product registration and market entry. Data from China's National Bureau of Statistics highlights this trend: in 2024, the average annual per capita disposable income for Chinese households hit approximately 41,300 CNY, a notable rise from 39,218 CNY in 2023[3]National Bureau of Statistics of China, "Average annual per capita disposable income of households in China from 1990 to 2024", stats.gov.cn.. Such figures underscore the surging demand in the region. China's vast market allure is drawing substantial investments. Notably, Reckitt has set up new R&D centers in the country, buoyed by optimistic double-digit growth forecasts, a testament to the swift consumer shift towards premium hygiene products. Meanwhile, Japan's evolving regulations on PFAS compounds and chemical controls present a maze of compliance challenges. These complexities seem to favor multinational giants with robust regulatory expertise, potentially sidelining local players. In Indonesia, the BPOM's 2024 legislative blueprint aligns with ASEAN standards, introducing new mandates on cosmetic notifications, labeling, and contamination limits. This alignment not only standardizes frameworks but also paves the way for smoother regional expansion.

European markets are grappling with a significant regulatory overhaul, courtesy of the European Green Deal's Chemicals Strategy for Sustainability. This strategy pivots chemical management from specific risk assessments to a more generalized risk approach, influencing ingredient sourcing and formulation tactics. With the region's pronounced focus on sustainability, companies delving into biodegradable formulations and circular packaging systems stand to gain. However, the costs of regulatory compliance seem to tilt the scales in favor of established entities boasting advanced R&D capabilities. In Latin America, while growth prospects are evident, they're tempered by economic fluctuations and currency volatility, both of which can sway consumer purchasing power and impact import costs for global brands. The Middle East and Africa, with their urbanization and infrastructure strides, present enticing expansion avenues. Yet, the landscape is dotted with challenges: distribution hurdles and a fragmented regulatory environment necessitate tailored strategies and collaborative partnerships for successful market entry.

Competitive Landscape

The hand wash market is moderately consolidated, with both global and regional players contributing to its competitive dynamics. Leading multinational brands hold a significant share of the market due to their extensive distribution networks, strong brand presence, and consistent product innovation. Prominent companies in this space include Unilever Plc, The Procter and Gamble Company, Reckitt Benckiser Group Plc, The Colgate-Palmolive Company, and Johnson & Johnsonc. On the other hand, regional players are gaining traction by offering affordable alternatives and catering to specific consumer needs. The market is witnessing frequent product launches that emphasize natural ingredients and eco-friendly packaging, which has intensified competition. Despite the dominance of established players, there are opportunities for new entrants focusing on health, hygiene, and sustainable solutions.

In the institutional segment, companies can explore untapped opportunities by adopting automated dispensing systems and compliance monitoring technologies. These innovations can help businesses differentiate themselves, provided they invest in integrating technology and enhancing service capabilities. Additionally, the FDA's cosmetic facility registration requirements under MoCRA create regulatory challenges. While these regulations favor established players with compliance expertise, they can act as barriers for smaller companies that lack the necessary resources to meet these standards.

Emerging disruptors are reshaping the market by prioritizing sustainability and adopting direct-to-consumer strategies. They are leveraging e-commerce platforms and subscription-based models to bypass traditional retail channels, building brand loyalty through transparent ingredient sourcing and environmentally conscious practices. The adoption of advanced technologies is also accelerating, with companies using AI-driven marketing and predictive analytics to forecast demand. Businesses that successfully combine these digital tools with traditional manufacturing and distribution strengths are likely to gain a competitive advantage in the market.

Hand Wash Industry Leaders

-

Unilever Plc

-

The Procter and Gamble Company

-

Reckitt Benckiser Group Plc

-

The Colgate-Palmolive Company

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Colgate-Palmolive plans to expand in India by launching more global brands, aiming to capture growth in the Asian market. This includes strengthening its hand wash segment to meet rising hygiene demand, enhancing its presence in personal care and household products.

- June 2025: Diversey has globally launched the LESSEAU solid hand wash system, featuring a new manual dispenser co-developed with Slimstones for institutional settings such as healthcare, hospitality, and education. The system uses plant-based, plastic-free solid hand wash bars that dissolve instantly, drastically cutting plastic waste and reducing carbon emissions by 90% compared to conventional liquid soaps.

- June 2025: Native has launched its most requested product to date: Liquid Hand Soap. According to the brand, the new liquid hand soap (hand wash) features naturally derived, vegan, and cruelty-free ingredients, free from sulfates, parabens, and dyes, and offers gentle cleansing with customer-favorite scents.

- May 2025: SUPA, a UK-based sustainability innovator, has launched bio-based hand wash packs utilizing a paper exterior and a waterproof lining derived from pine tree sap. According to the brand, the new packaging is fully plastic-free and incorporates a reusable matte black metal pump, encouraging consumers to reuse components and reduce waste.

Global Hand Wash Market Report Scope

| Conventional |

| Natural/Organic |

| Liquid |

| Gel |

| Foam |

| Others (Powder, Wipes, and Others) |

| Bottle |

| Pouch |

| Sachets |

| Dispenser Cartridges |

| Online Retail Stores |

| Offline Retail Stores |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Category | Conventional | |

| Natural/Organic | ||

| By Product Form | Liquid | |

| Gel | ||

| Foam | ||

| Others (Powder, Wipes, and Others) | ||

| By Packaging Type | Bottle | |

| Pouch | ||

| Sachets | ||

| Dispenser Cartridges | ||

| By Distribution Channel | Online Retail Stores | |

| Offline Retail Stores | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the global hand wash category by 2030?

Forecasts indicate the category will reach USD 7.64 billion by 2030, expanding at a 7.07% CAGR.

Which region is expected to post the fastest growth in hand wash demand up to 2030?

Asia-Pacific is forecast to register an 8.36% CAGR driven by urbanization, rising incomes, and streamlined regulatory frameworks.

Which product form is gaining share most quickly within hand hygiene?

Foam formulations are expanding at an 8.61% CAGR due to controlled dosing, lower water use, and growing institutional adoption.

What packaging innovation is resonating with institutional buyers?

Dispenser cartridges, growing at a 9.43% CAGR, minimize contamination, reduce maintenance labor, and cut packaging waste.

Page last updated on: