Cake Mixes Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.9 Billion |

| Market Size (2031) | USD 2.25 Billion |

| Growth Rate (2026 - 2031) | 3.44% CAGR |

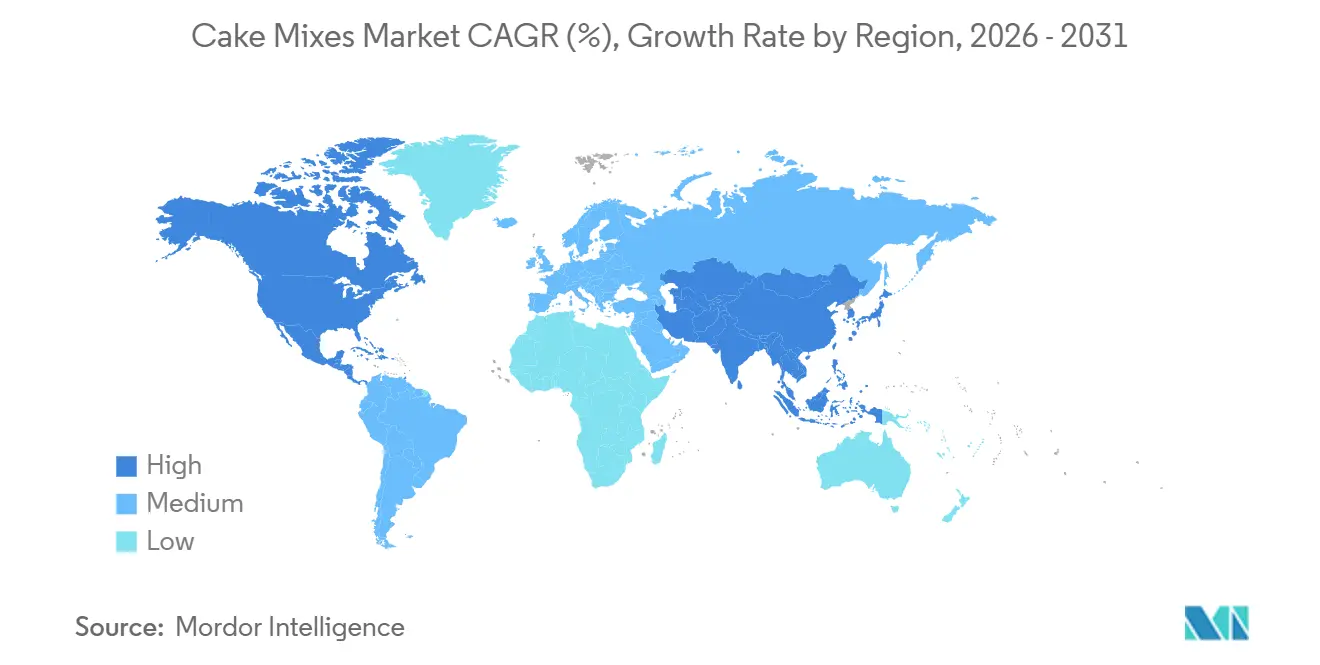

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

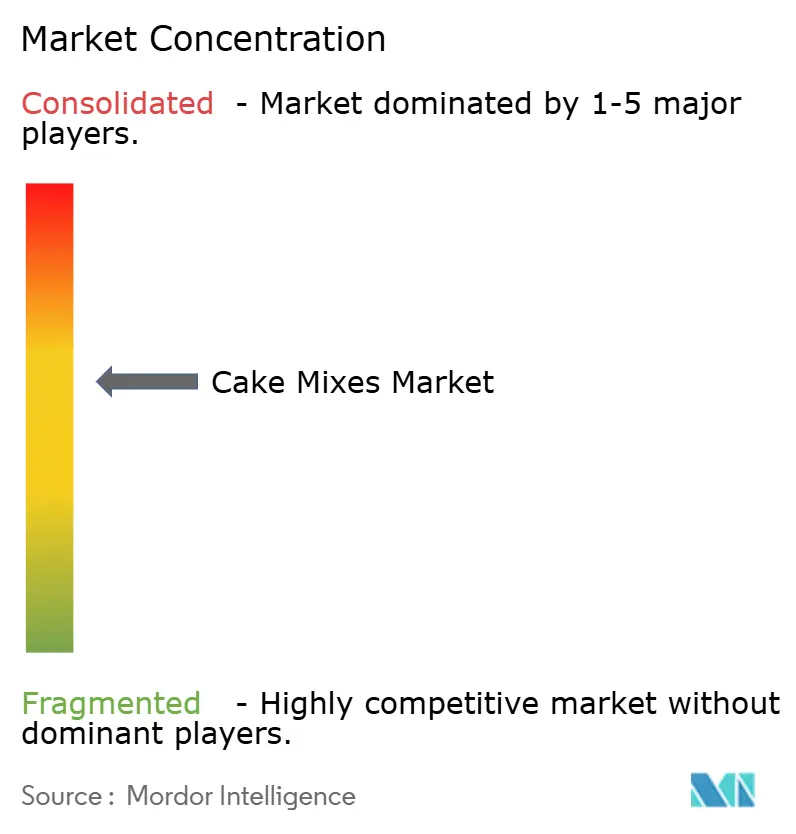

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cake Mixes Market Analysis by Mordor Intelligence

The cake mixes market size is expected to be USD 1.79 billion in 2025, USD 1.90 billion in 2026, and reach USD 2.25 billion by 2031, growing at a CAGR of 3.44% from 2026 to 2031. As dietary awareness intensifies, consumers are now prioritizing not just convenience, but also clean labels, allergen transparency, and the nutritional value of their purchases. Companies are pivoting from traditional wheat-centric recipes to embrace alternative flours, with gluten-free cake mix formulations witnessing the most rapid expansion. The rise of e-commerce, coupled with the trend of portion-controlled packs and a push towards premiumization, is broadening the avenues for consumer engagement. However, the industry grapples with challenges like commodity price fluctuations and escalating compliance costs, which are squeezing operating margins. In this moderately fragmented landscape, both multinational food giants and regional specialists are fine-tuning their portfolio strategies, enhancing direct-to-consumer approaches, and charting out sustainability initiatives to safeguard their market share.

Key Report Takeaways

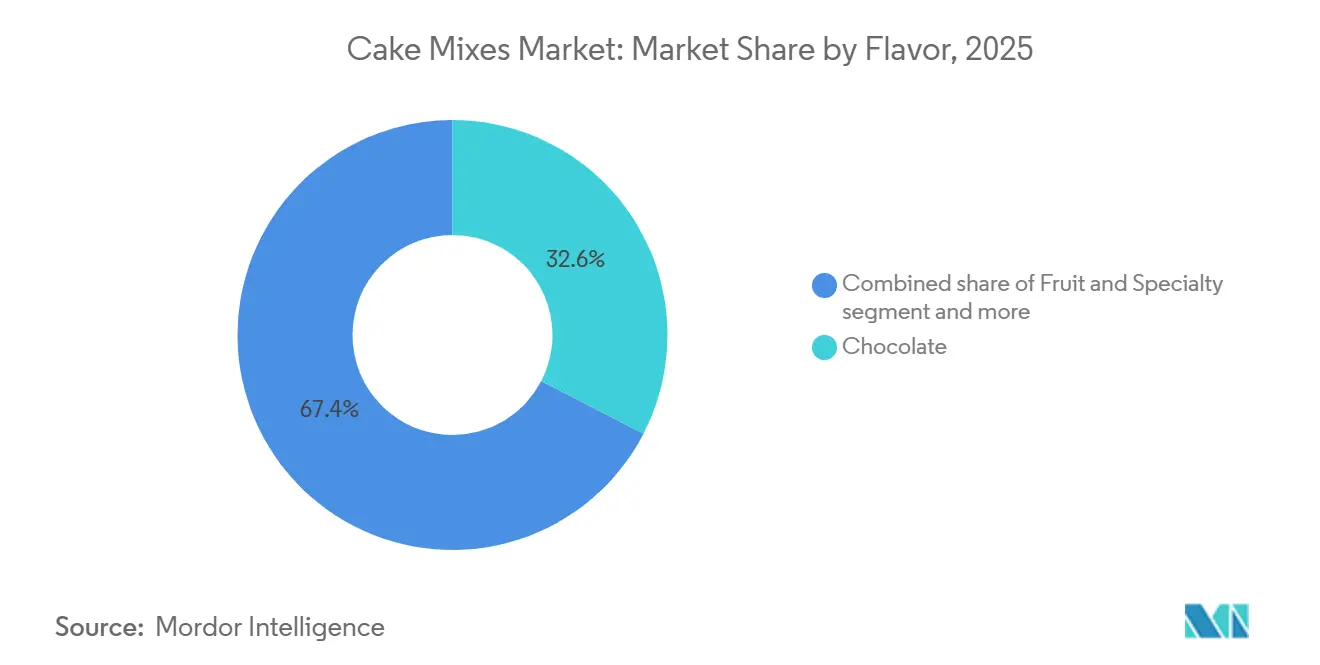

- By flavor, chocolate led with 32.59% of cake mixes market share in 2025, whereas fruit and specialty variants are forecast to register a 4.08% CAGR through 2031.

- By category, conventional mixes accounted for 75.69% of the cake mixes market size in 2025, while organic formulations are advancing at a 4.97% CAGR to 2031.

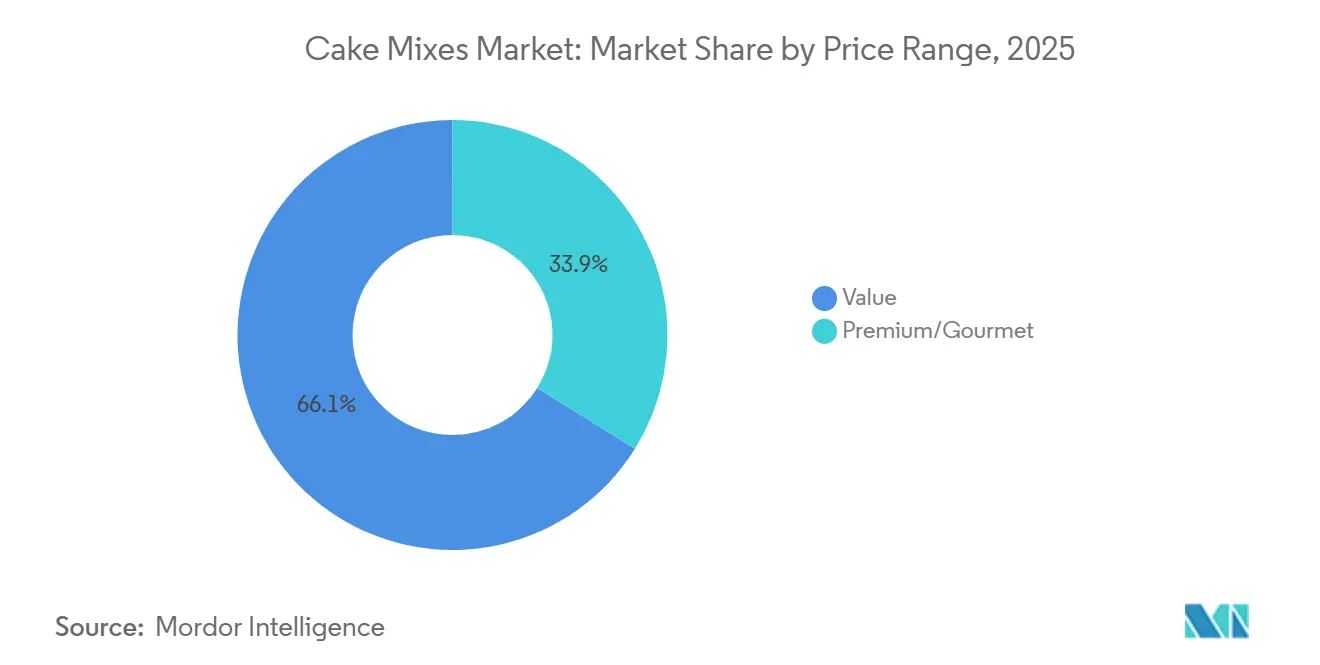

- By price range, the value tier dominated with 66.12% revenue share in 2025, but premium and gourmet offerings are projected to rise at a 5.01% CAGR over the same horizon.

- By distribution channel, foodservice held 35.72% revenue share in 2025, yet retail is primed for the quickest climb with a 4.81% CAGR through 2031.

- By region, North America captured 35.40% of the cake mixes market value in 2025, while Asia-Pacific is expected to lead growth at a 4.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cake Mixes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Convenience and time-saving appeal | +0.8% | Global, with the highest intensity in North America and urban Asia-Pacific | Short term (≤ 2 years) |

| Rising home baking and DIY trends | +0.6% | North America and Europe, moderate uptake in Asia-Pacific metros | Medium term (2-4 years) |

| Expansion of online grocery and D2C channels | +0.7% | Global, led by North America and China, is spreading to Southeast Asia | Medium term (2-4 years) |

| Functional protein-/collagen-enriched cake mixes | +0.5% | North America and Europe, early adoption in Australia and Japan | Long term (≥ 4 years) |

| Intelligent portion-controlled packaging reduces waste | +0.4% | North America and Europe, emerging in the Asia-Pacific urban centers | Medium term (2-4 years) |

| Upcycled-ingredient (fruit-pomace) formulations | +0.3% | Europe and North America, pilot programs in select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Convenience and Time-Saving Appeal

Convenience remains the foundational driver, yet its expression has evolved beyond simple preparation speed. Consumers under 34 years old use ready-to-bake cake premixes at higher frequencies than older cohorts, reflecting generational shifts in cooking skills and time allocation. The appeal now extends to multi-step occasions: breakfast cakes, mid-afternoon snacks, and celebration desserts that require minimal cleanup. Portion-controlled formats align with this trend, as a majority of Americans reported snacking 3 or more times daily in recent consumer surveys, creating demand for single-serve or small-batch mixes that avoid leftovers. Manufacturers are responding by segmenting pack sizes into 1-ounce cake bites, 3-ounce muffins, and 6-serving tins that cater to solitary consumption and reduce food waste. This granular approach to convenience is less about shaving minutes off prep time and more about matching product architecture to fragmented eating patterns that dominate urban lifestyles.

Rising Home Baking and DIY Trends

Data from the Agriculture and Horticulture Development Board reveals that home baking in the UK faced a 7% year-over-year decline in 2025[1]Source: Agriculture and Horticulture Development Board, “UK Home Baking Trends 2025,” ahdb.org.uk . As the novelty of home baking faded and consumers returned to pre-2020 habits, categories like sweet baking, particularly cakes, experienced sharper downturns. Yet, this overall dip conceals a split in the baking community: while enthusiast bakers are diving into scratch recipes and artisanal methods, occasional bakers are leaning on customizable mixes. These mixes allow for add-ins, frosting combinations, and decorative toppings, all without the need for foundational baking skills. The allure of cake mixes lies in their hybrid design: they serve as a base for personalization, granting users a sense of creative ownership while minimizing technical challenges. Brands are seizing this opportunity, rolling out co-creation content, video tutorials, flavor innovations, and seasonal tweaks. This strategy positions mixes as versatile platforms, not just end products, ensuring continued interest from consumers who might be tempted to switch to scratch baking.

Expansion of Online Grocery and D2C Channels

By 2025, e-commerce was reshaping the distribution economics of baking mixes. Brands, leveraging direct-to-consumer models, sidestep retailer slotting fees and gain insights into purchase frequency, flavor preferences, and basket composition. Subscription services, offering cake mixes and curated assortments, are resonating with millennials and Gen Z, who prefer discovery without the hassle of in-store browsing. Online platforms also cater to niche markets: gluten-free, keto-friendly, and vegan variants, often sidelined in physical stores, are finding their audience through targeted digital ads and influencer collaborations. This trend is especially evident in the Asia-Pacific region, where mobile commerce and digital payments are outpacing the growth of brick-and-mortar groceries in tier-2 and tier-3 cities. This evolution in channels is shortening product life cycles, enabling brands to swiftly test limited-edition flavors and phase out underperformers, thus speeding up innovation and diversifying the competitive landscape.

Functional Protein-/Collagen-Enriched Cake Mixes

Functional fortification marks a shift from mere indulgence to a more health-conscious approach. Cake mixes infused with collagen, offering 5 to 10 grams of hydrolyzed collagen peptides per serving, cater to consumers desiring beauty benefits, improved skin elasticity, and joint health, all while enjoying their desserts. Additions of plant-based proteins, often from pea or rice isolates, appeal to fitness enthusiasts and parents seeking nutritious snacks for their kids. These premium-priced formulations, costing 30% to 50% more than standard mixes, have found traction primarily in North America and select European markets, where wellness trends are well-established. A key challenge is preserving sensory quality: both protein and collagen can introduce off-flavors or change textures. This necessitates advanced masking agents and hydrocolloid systems, complicating the formulation process. While niche brands have successfully demonstrated the concept, broader market acceptance hinges on reducing costs of functional ingredients and educating consumers about bioavailability and efficacy. This educational journey is expected to progress over the next 4 to 6 years, coinciding with the accumulation of clinical evidence and the stabilization of regulatory frameworks for structure-function claims.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile wheat and sugar prices | -0.6% | Global, most acute in import-dependent regions like the Middle East and North Africa | Short term (≤ 2 years) |

| Consumer shift to scratch/artisanal baking | -0.4% | Europe and North America, limited impact in Asia-Pacific | Medium term (2-4 years) |

| Stricter sustainable-packaging mandates | -0.3% | Europe and North America, emerging in select Asia-Pacific markets | Long term (≥ 4 years) |

| Allergen-traceability compliance burden | -0.2% | Global, with the highest regulatory intensity in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Wheat and Sugar Prices

Commodity input costs continue to exert pressure on margins, even as forecasts hint at a potential stabilization. The USDA anticipates global wheat production to hit a record 1.097 billion tonnes in the 2025/26 crop year, a figure poised to mitigate the price surges seen in 2022 and 2023[2]Source: U.S. Food and Drug Administration, “Food Safety Modernization Act Final Rule for Preventive Controls,” fda.gov . Yet, challenges persist: climate fluctuations in vital growing areas, export bans driven by domestic food security worries, and the ripple effects of energy prices on fertilizer costs create a landscape where risks are unevenly distributed. While there's limited protection against downturns, sudden upswings can swiftly diminish profits. The sugar market mirrors these challenges, with Brazil and India's cane production swayed by monsoon patterns and shifting biofuel policies. Cake mix producers grapple with these input fluctuations, facing squeezed gross margins during inflationary periods. They find it challenging to adjust pricing strategies, especially when retail partners resist frequent price changes. Consumers, too, have their limits; push them too far, and they might pivot to private labels or abandon the category altogether. This challenge hits hardest for value-tier products with already slim margins. In response, brands are either reformulating with alternative sweeteners or downsizing pack sizes, a move that risks alienating buyers who prioritize volume.

Stricter Sustainable-Packaging Mandates

Regulatory pressure on packaging is intensifying, especially in the European Union. The Packaging and Packaging Waste Directive mandates minimum recycled content and recyclability standards[3]Source: European Commission, “Packaging and Packaging Waste Directive Revision,” europa.eu. Many flexible film structures currently fall short of these standards. Transitioning from multi-layer laminates, which are crucial for moisture barriers in shelf-stable mixes, to mono-material films or paper-based alternatives demands significant capital investment. Manufacturers need new sealing equipment and must reformulate to address the reduced barrier properties. Smaller manufacturers, lacking the scale to absorb these tooling changes, disproportionately bear the brunt of compliance costs. This financial strain accelerates consolidation, with many regional players either exiting the market or selling to larger entities. North American markets, particularly in states like California, Maine, and Oregon, are witnessing similar trends. Extended producer responsibility laws impose fees on non-recyclable packaging, pushing brands towards design changes. While these mandates promise environmental benefits, they present immediate challenges. Brands grapple with transition periods, manage inventories of legacy packaging, and work to educate consumers on new disposal methods. The regulatory impact is set to peak between 2027 and 2029, aligning with major regulatory deadlines. Post this period, the hope is that standardized solutions will help mitigate these costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Flavor: Chocolate Dominance Meets Fruit Innovation

In 2025, chocolate flavor commanded a dominant 32.59% share of the market value, underscoring its widespread appeal across diverse age groups and occasions. However, fruit and specialty variants are projected to outpace with a 4.08% CAGR through 2031, as consumers gravitate towards novel, lighter profiles that resonate with health-conscious trends. Vanilla, consistently holding the second spot, acts as a versatile canvas for enhancements, be it chocolate chips, nuts, or dried fruits. Yet, it lacks the standalone allure that drives premium-tier trials. Once riding a wave of rapid growth, Red Velvet has now settled into a stable niche, boasting dedicated fans in North America and select global markets. However, its distinct cocoa-buttermilk flavor profile poses challenges for expansion in regions unfamiliar with its traditional roots. Meanwhile, fruit and specialty variants ranging from lemon and strawberry to seasonal favorites like pumpkin spice, are riding the clean-label wave. These offerings are increasingly viewed as lighter indulgences compared to their chocolate or vanilla counterparts. Highlighting the trend, King Arthur Baking debuted a confetti cake mix in April 2026, showcasing colorful sprinkles in the batter, a move designed to capture the attention of younger, Instagram-savvy bakers.

Geographically, flavor preferences diverge: while chocolate reigns supreme in North America and Europe, the Asia-Pacific region leans towards matcha, red bean, and tropical fruits, echoing local tastes. This regional disparity poses challenges for global SKU strategies. Multinational brands find themselves at a crossroads, needing to balance a diverse portfolio against the intricacies of supply chains and the potential pitfalls of slow-moving inventory in markets where localized flavors may not resonate. The burgeoning fruit and specialty segment, now a magnet for innovation, sees brands delving into exotic fruits like passionfruit, yuzu, and hibiscus. These not only command premium pricing but also carve out distinct niches in an oversaturated market.

By Category: Organic Gains Ground Amid Conventional Stability

In 2025, conventional cake mixes commanded a dominant 75.69% share of the category's revenue, bolstered by their price accessibility and widespread availability in mass-market retailers. However, organic cake mixes are carving out a niche, expanding at a robust 4.97% CAGR through 2031. This growth is driven by health-conscious consumers who prioritize ingredient transparency and seek pesticide-free options. The organic segment's ascent outpaces the overall market, hinting at a swift shift in market share. This momentum is expected to quicken as the costs of organic ingredients drop due to economies of scale. Additionally, private-label programs from retailers are rolling out mid-priced organic options, further bridging the price gap with conventional mixes. In the U.S., organic certification is overseen by the USDA's National Organic Program standards, with similar frameworks in Europe and the Asia-Pacific. These standards, emphasizing traceability and documentation, tend to benefit larger manufacturers boasting dedicated supply chains and robust quality assurance infrastructures.

While conventional mixes enjoy advantages in shelf stability, cost efficiency, and flavor intensity, organic formulations grapple with restrictions on additives and flavor enhancers. Yet, organic options are witnessing a decline in popularity among millennial and Gen Z households, where organic purchases have transitioned from occasional to habitual. The market segmentation reveals that organic mixes predominantly occupy premium price tiers and specialty distribution channels. This positioning creates a "halo effect," where organic certification not only signifies pesticide-free attributes but also suggests a broader quality assurance. Responding to the convergence of dietary restrictions and wellness trends, organic formulations are increasingly offering gluten-free and eggless chocolate cake mix variants. This trend underscores a shift in research and development priorities, with brands now focusing on multi-attribute products. Instead of diversifying into niche offerings that complicate manufacturing and inventory, brands are channeling investments into single SKUs that meet criteria like organic, gluten-free, and high-protein.

By Price Range: Premiumization Outpaces Value Growth

In 2025, the value price tier captured 66.12% of the market share, catering to price-sensitive households and bulk buyers. These consumers prioritize cost per serving over factors like ingredient provenance or functional claims. However, the premium and gourmet segments are projected to expand at a 5.01% CAGR through 2031. This growth is driven by affluent consumers seeking artisanal positioning, exotic flavors, and functional fortification. Mid-range offerings, which strike a balance between quality and accessible pricing, find themselves in a fiercely contested middle ground. Here, competition from private labels is intense, and brand loyalty is notably weak. The premium tier's success underscores a broader trend: consumers are either opting for value for everyday staples or splurging on premium for special occasions and gifts. This shift has left the mid-tier struggling, as it's the hardest to differentiate.

Premium and gourmet mixes command higher price points through various strategies. These include organic certifications, single-origin ingredients, functional additives like collagen or probiotics, and an artisanal branding approach. This branding often suggests small-batch production, even if the products are manufactured at scale. While these premium products might retail at prices akin to the value tier, their per-serving costs remain competitive. This competitiveness is especially evident when considering yield and the fact that premium mixes can substitute for cakes bought at bakeries. The gourmet segment further capitalizes on occasions like gifting, holiday baking kits, and subscription boxes. Such positioning elevates these mixes from mere commodities to experiential products. Although the value tier's growth is modest in percentage terms, it's substantial in absolute volume due to its large base. Brands in this segment are actively defending their market share. They're doing this through strategies like optimizing pack sizes, intensifying promotions, and reformulating products to enhance sensory quality without raising prices.

By Distribution Channel: Retail Gains on Foodservice

In 2025, foodservice channels captured 35.72% of the market value, catering to bakeries, cafés, and institutional kitchens. These establishments utilized commercial-grade mixes, available in bulk formats of 5-kilogram and 20-kilogram bags, to standardize their output and cut down on labor costs. Meanwhile, the retail sector is set to expand at a 4.81% CAGR through 2031, driven by the growth of e-commerce, the reach of specialty stores, and a rise in home baking occasions. Within the retail landscape, supermarkets and hypermarkets dominate, providing a wide assortment and promotional visibility. However, online retail stores are steadily gaining ground, leveraging subscription models and targeted advertising to cater to niche dietary segments like gluten-free, keto, and vegan, which often find limited representation on physical shelves. While convenience and specialty stores are smaller players, urbanization and a trend towards on-the-go consumption are fueling their growth, especially for single-serve and impulse formats.

While foodservice growth faces challenges from labor shortages and a revival of scratch baking, especially in premium bakeries emphasizing artisanal techniques, quick-service and fast-casual restaurants are increasingly turning to mixes for their dessert offerings. Here, the emphasis on consistency and speed often overshadows the allure of scratch-made claims. Geographically, the channel dynamics differ: Asia-Pacific markets see foodservice taking the lead, buoyed by the rapid expansion of bakery chains, whereas North America and Europe tilt towards retail, bolstered by a robust home baking infrastructure, including stand mixers, ovens, and bakeware. In India, General Mills has rolled out egg-free vanilla and chocolate cake mixes in 5-kilogram and 20-kilogram packs, specifically targeting the foodservice segment. This move aligns with the market's strong vegetarian preferences, where egg-free formulations are essential for widespread acceptance.

Geography Analysis

North America maintains market leadership with 35.40% share in 2025, supported by established baking traditions, widespread retail penetration, and high consumer familiarity with cake mix products. The region benefits from mature supply chains, extensive product variety, and strong brand recognition that creates customer loyalty and repeat purchase behavior. Major manufacturers like General Mills and Conagra have deep regional roots and distribution networks that provide competitive advantages in market access and consumer engagement.

Asia-Pacific emerges as the fastest-growing region at 4.92% CAGR through 2031, driven by rapid urbanization, rising disposable incomes, and increasing adoption of Western baking practices among expanding middle-class populations. The region's growth potential is amplified by relatively low current penetration rates, creating significant opportunities for market expansion through retail development and consumer education initiatives. Cultural adaptation of flavors and packaging to local preferences enhances acceptance, while modern retail expansion provides the distribution infrastructure necessary for market development.

In Europe, the growth is driven by a strong tradition of baking, increasing consumer interest in premium, artisanal, organic, and gourmet cake mixes, and high consumer awareness of product quality. Innovations in flavors and packaging are also boosting demand, alongside well-established retail channels across countries like the United Kingdom, France, Germany, and Italy. The demand in Latin America is fueled by a growing middle class looking for convenient baking solutions, ceremonial occasions, and premium food products. Market growth is aided by increasing retail penetration and online availability.The Middle East and Africa region is characterized by emerging demand for convenient and quick baking solutions as consumer lifestyles change amidst urban growth. The Middle East and Africa market is progressively adopting global food trends, fostering acceptance of cake mixes for home baking and commercial use.

Competitive Landscape

The competitive landscape of the cake mixes market is moderately concentrated, shaped by a dynamic interplay of legacy brands, health-focused innovators, and premium disruptors. Historically, competition centered on price and widespread availability, but evolving consumer preferences have forced brands to differentiate through clean label formulations, functional ingredients, and a broader range of dietary options, including gluten-free, vegan, and sugar-free mixes. Established companies such as General Mills Inc., Conagra Brands, and Rich Products Corporation continue to command significant market share, leveraging economies of scale, extensive distribution networks, and long-standing brand loyalty.

Strategic patterns reveal a shift toward portfolio premiumization and direct consumer engagement, with companies investing heavily in brand building and digital marketing capabilities. General Mills' Accelerate strategy emphasizes brand investment and innovation. At the same time, newer entrants and artisanal brands carve out niches by emphasizing transparency, organic sourcing, and small-batch authenticity, capitalizing on premiumization trends and the growing wellness movement.

External market shocks such as tariffs and supply chain disruptions are also influencing the competitive environment. Large multinational brands have responded by optimizing procurement strategies, negotiating long-term contracts, and, where possible, localizing sourcing and production to control costs and ensure supply chain resilience. Furthermore, as part of its marketing strategies, companies are also offering gift sets along with cake mix to lure customers. Overall, the competitive landscape of the cake mixes market is defined by continuous innovation, strategic brand differentiation, and adaptability to changing consumer preferences, ensuring that companies are able to balance quality, convenience, and evolving trends and remain at the forefront of industry growth.

Cake Mixes Industry Leaders

General Mills Inc.

Conagra Brands, Inc.

Rich Products Corporation

Puratos Group

Bob's Red Mill Natural Foods Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: King Arthur Baking Company launched 5 new baking mixes, including a gluten-free roll and bun mix, gluten-free double chocolate chip cookie mix, and a confetti cake mix, expanding its portfolio to address dietary restrictions and celebration occasions. The launches reflect the company's strategy to capture incremental share in specialty segments where premium pricing and brand loyalty offset higher ingredient costs.

- March 2026: Dawn Foods announced a partnership with a European ingredients supplier to co-develop plant-based cake mix formulations targeting vegan and flexitarian consumers. The collaboration aims to improve texture and moisture retention in egg-free formulations, addressing a key sensory gap that has limited mainstream adoption of plant-based baking mixes.

- January 2026: Puratos Group opened a new innovation center in Singapore focused on Asia-Pacific flavor development and functional ingredient research. The facility will support localized product development for markets where taste preferences diverge from Western norms, including matcha, red bean, and tropical fruit profiles.

Global Cake Mixes Market Report Scope

A cake mix is a pre-packaged, commercial preparation of dry ingredients designed to simplify the baking process. The global cake mixes market is segmented by flavor, category, price range, distribution channel, and geography. By flavor, the market is segmented into chocolate, vanilla, red velvet, and fruit and specialty. By category, the market is segmented into conventional and organic. By price range, the market is segmented into value, mid-range, and premium/gourmet. By distribution channel, the market is segmented into foodservice and retail. The retail segment is further sub-segmented into supermarkets/hypermarkets, convenience stores, specialty stores, online retail stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa. The Market Forecasts are Provided in Terms of Value (USD).

| Chocolate |

| Vanilla |

| Red Velvet |

| Fruit and Specialty |

| Conventional |

| Organic |

| Value |

| Mid-Range |

| Premium/Gourmet |

| Foodservice | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Specialty Stores | |

| Online Retail Stores | |

| Other Distribution channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Sweden | |

| Belgium | |

| Poland | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Thailand | |

| Singapore | |

| Indonesia | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Peru | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Saudi Arabia | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| Flavor | Chocolate | |

| Vanilla | ||

| Red Velvet | ||

| Fruit and Specialty | ||

| Category | Conventional | |

| Organic | ||

| Price Range | Value | |

| Mid-Range | ||

| Premium/Gourmet | ||

| Distribution Channel | Foodservice | |

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution channels | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Sweden | ||

| Belgium | ||

| Poland | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Peru | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the cake mixes market in 2026?

The cake mixes market size is USD 1.90 billion in 2026, on track to reach USD 2.25 billion by 2031.

Which flavor holds the biggest slice of sales?

Chocolate leads with 32.59% of the cake mixes market share in 2025.

What is the fastest-growing regional market?

Asia-Pacific is projected to post a 4.92% CAGR through 2031, outpacing all other regions.

How quickly are organic cake mixes expanding?

Organic formulations are growing at a 4.97% CAGR between 2026 and 2031.

Page last updated on: