Fertility Supplement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

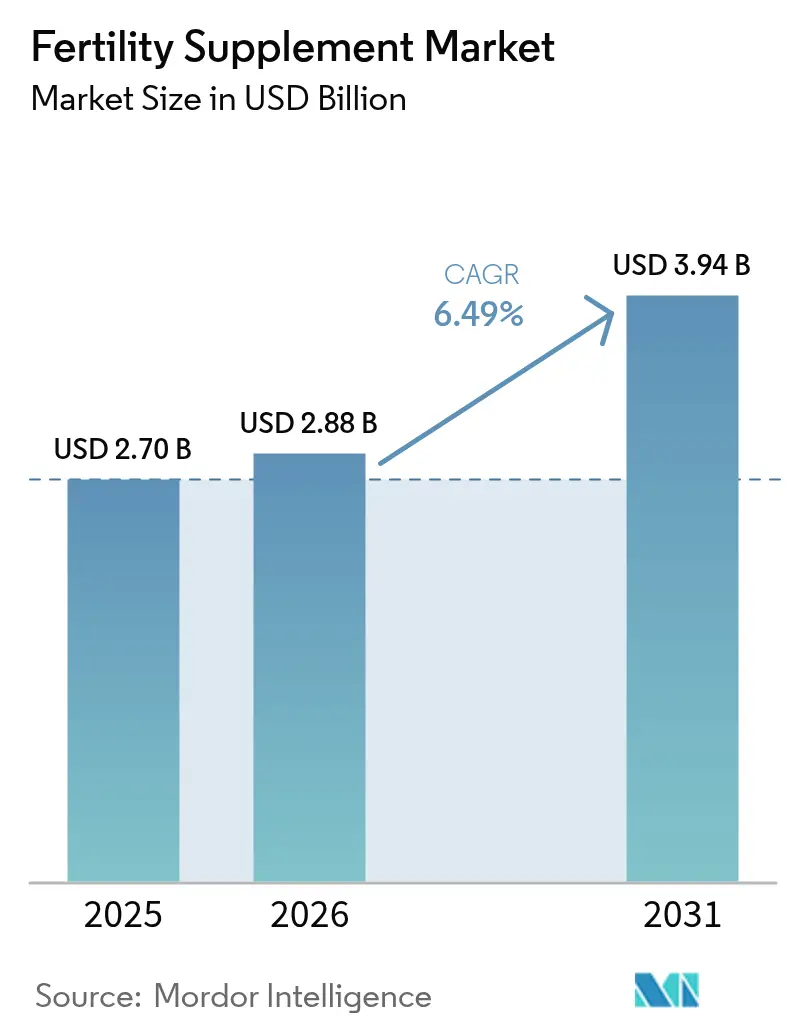

| Market Size (2026) | USD 2.88 Billion |

| Market Size (2031) | USD 3.94 Billion |

| Growth Rate (2026 - 2031) | 6.49% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fertility Supplement Market Analysis by Mordor Intelligence

The Fertility Supplement Market size was valued at USD 2.70 billion in 2025 and estimated to grow from USD 2.88 billion in 2026 to reach USD 3.94 billion by 2031, at a CAGR of 6.49% during the forecast period (2026-2031).

Momentum is sustained by rising infertility prevalence, stronger pre-conception health awareness, and broader assisted-reproductive-technology (ART) adoption in both developed and emerging economies. Clinical data confirming the reproductive benefits of nutrients such as coenzyme Q10, methylfolate and L-carnitine is helping brands justify premium pricing while building medical-community credibility[1]U.S. Food & Drug Administration, “New Dietary Ingredient Notification Final Rule,” Federal Register, federalregister.gov. Meanwhile, employers in the United States have expanded fertility coverage—from 30% in 2020 to 42% in 2024—fueling demand for adjunctive nutritional protocols that can be taken before or during ART cycles. Online sales channels, coupled with rising regulatory scrutiny over product safety and claim substantiation, continue to redefine competitive strategy and accelerate innovation across the fertility supplements market.

Key Report Takeaways

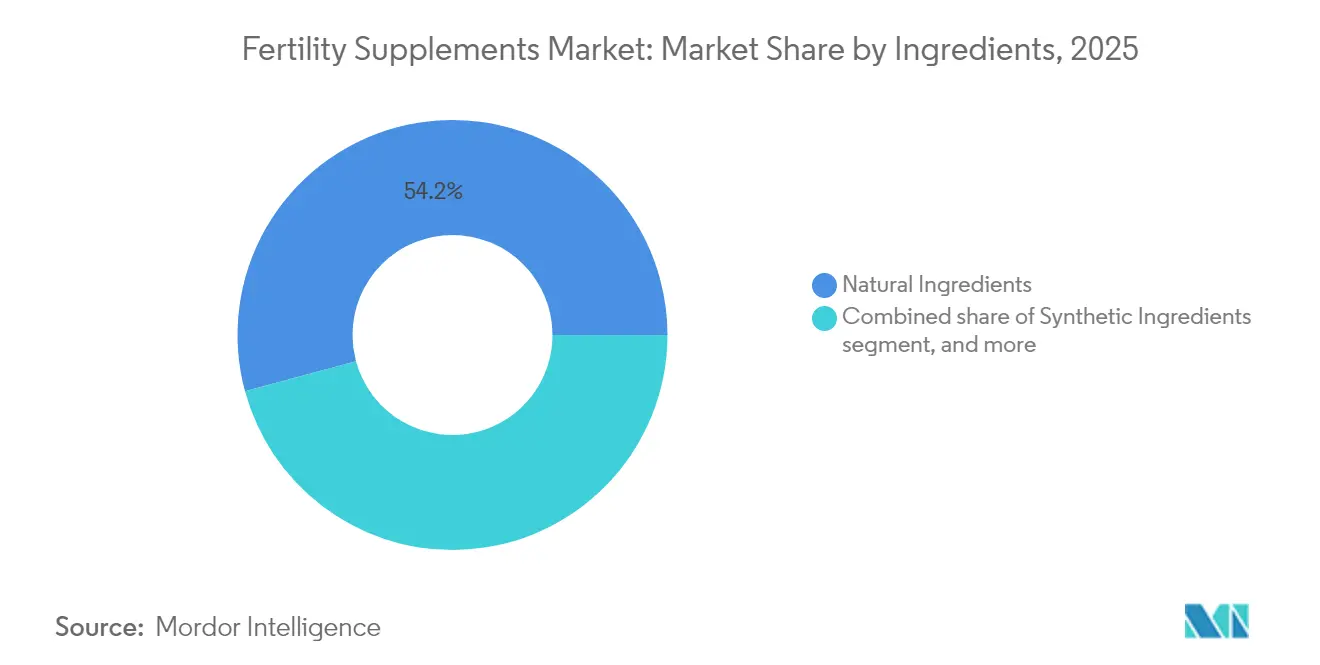

- By ingredient, natural formulations commanded 54.22% of fertility supplements market share in 2025, while blends of natural and synthetic ingredients are projected to post the fastest 8.39% CAGR through 2031.

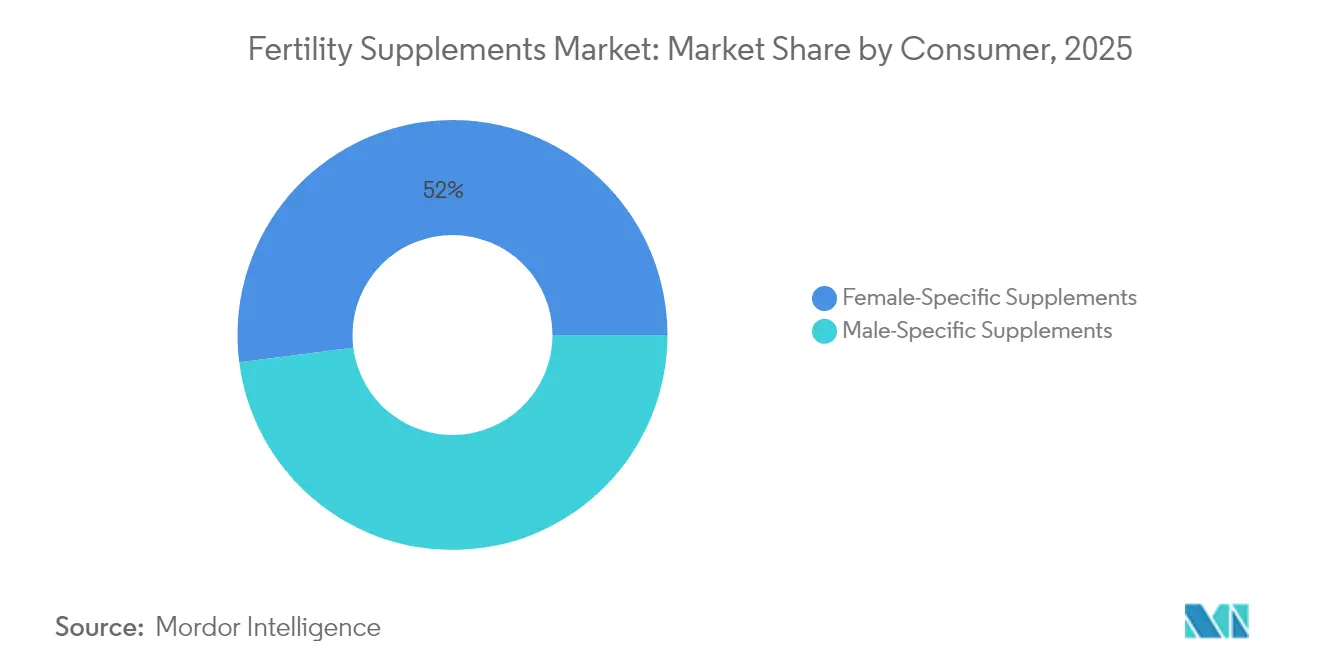

- By consumer, female-specific products held 52.02% share of the fertility supplements market size in 2025, whereas male-specific lines are expected to expand at an 8.41% CAGR to 2031.

- By form, capsules led with a 37.76% revenue contribution in 2025; gummies represent the quickest-rising format with a 9.12% CAGR to 2031.

- By distribution channel, retail pharmacy retained 43.08% share in 2025, though e-pharmacy is scaling at 9.08% CAGR on the back of convenience and privacy benefits.

- By region, North America captured 35.41% of the fertility supplements market share in 2025, while Asia-Pacific is set to grow the fastest, logging a 7.48% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Fertility Supplement Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Global Infertility Incidence | +1.8% | Global; highest in Asia-Pacific & North America | Long term (≥ 4 years) |

| Growing Awareness Of Preconception Nutrition | +1.2% | North America & Europe; expanding into Asia-Pacific | Medium term (2-4 years) |

| Expansion Of Assisted Reproductive Technologies | +1.0% | Global; concentrated in developed markets | Long term (≥ 4 years) |

| Increasing Disposable Income And Healthcare Spending | +0.9% | Asia-Pacific core; spill-over to Latin America | Medium term (2-4 years) |

| Product Innovations With Evidence-Based Ingredients | +0.7% | Global; led by North America & Europe | Short term (≤ 2 years) |

| Proliferation Of Online And Retail Distribution Channels | +0.5% | Global; fastest in Asia-Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Infertility Incidence

Roughly 8–12% of couples now struggle with male-factor infertility, and secondary infertility is climbing sharply across Asia-Pacific, with the Philippines reporting some of the highest regional rates. Contributing factors—later childbearing, sedentary lifestyles and environmental stressors—have moved fertility supplements from discretionary status to perceived healthcare essentials. Evidence for nutrients such as myo-inositol and selenium in managing polycystic ovary syndrome (PCOS) underpins long-range demand, particularly for women who postpone pregnancy into their thirties. These structural epidemiological shifts establish a durable growth platform for the fertility supplements market.

Growing Awareness of Preconception Nutrition

Survey work across five high-income countries shows the United States leading on pre-conception knowledge, yet uptake of recommended micronutrient regimens remains inconsistent. Physician guidance is the most trusted information source, elevating clinical backing as a sales catalyst. Research linking optimal copper, manganese and vitamin B12 levels during pregnancy to lower mid-life blood-pressure risk widens the conversation from immediate conception to lifelong health outcomes. By embedding these insights, brands are positioning fertility supplements as part of holistic prenatal wellness rather than short-term fixes.

Expansion of Assisted Reproductive Technologies

The global fertility-services arena is on track to double from USD 35 billion in 2023 to more than USD 70 billion by 2033, paced by a 10% CAGR in Asia. With a single IVF cycle costing USD 30,000–40,000, nutraceuticals that improve oocyte or sperm quality represent cost-effective adjuncts. Resveratrol-fortified multivitamins have delivered higher numbers of mature follicles and raised fertilization rates relative to folic-acid-only controls. Modern sperm-selection devices such as Q300™ drive cumulative pregnancy rates up to 65%, and patients often pair these technologies with antioxidant regimens to maximize outcomes. Together, these trends embed the fertility supplements market deeper into clinical fertility protocols.

Increasing Disposable Income and Healthcare Spending

The expanding middle class in China, India and Southeast Asia is channeling larger household budgets toward reproductive health. Rising insurance coverage for ART, plus government incentives in select provinces, reinforces demand for preparatory micronutrients. Latin American economies are following a similar arc, albeit at an earlier stage, offering incremental runway for the fertility supplements industry.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regulatory oversight on supplement claims | -0.8% | Global; strictest in North America & Europe | Medium term (2-4 years) |

| Limited clinical evidence supporting efficacy | -0.6% | Global; impacts premium-price tiers | Long term (≥ 4 years) |

| High price sensitivity among consumers | -0.5% | Emerging markets & price-conscious segments worldwide | Short term (≤ 2 years) |

| Competition from alternative treatment modalities | -0.4% | Global; stronger where ART coverage is expanding | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Regulatory Oversight on Supplement Claims

The U.S. FDA now mandates a 75-day pre-market notification for novel dietary ingredients, including substantial toxicology data, before commercialization[2]Center for Science in the Public Interest, “Fertility Claim Warning Letter,” cspinet.org. California’s pending SB 646 will require heavy-metal testing for prenatal vitamins, and advocacy bodies such as the Center for Science in the Public Interest have openly challenged unsubstantiated fertility claims[3] U.S. Food & Drug Administration, “New Dietary Ingredient Notification Final Rule,” Federal Register, federalregister.gov. Compliance outlays climb fastest for smaller firms, effectively raising entry barriers yet gradually building consumer confidence in the fertility supplements market.

Limited Clinical Evidence Supporting Efficacy

While antioxidants can improve sperm concentration and motility, systematic reviews reveal poor linkage to actual live-birth outcomes, owing to study bias and small sample sizes. The evidence gap deters healthcare professionals from recommending high-priced blends lacking robust randomized controlled trials. Brands investing in gold-standard studies, however, can translate validated outcomes into defensible premiums, thereby differentiating themselves within the fertility supplements industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ingredient: Natural Dominance Faces Synthetic Innovation

Natural ingredients accounted for 54.22% of the fertility supplements market in 2025, reflecting consumer trust in botanicals such as maca, ashwagandha and tribul us. Vitamins and minerals with long clinical pedigrees—folic acid, zinc and selenium—continue to anchor many formulations. Antioxidants like coenzyme Q10 and omega-3 fatty acids are increasingly positioned as gamete-protective agents against oxidative stress. Synthetic bioactives still meet hesitation, but science-driven messaging around higher absorption and genetic suitability is helping to bridge perceptions.

The blend segment is forecast to log the fastest 8.39% CAGR through 2031, marrying botanical familiarity with synthetic precision. Brands are styling these hybrids as “clinically complete” solutions, justifying premium price tags through comprehensive label claims. For example, Quatrefolic’s superior absorption profile is being paired with whole-herb inositol to meet both female-fertility and MTHFR-related needs. This positioning aligns with rising willingness in North America and Asia-Pacific to invest in condition-specific micronutrient stacks, a critical propellant for the fertility supplements market.

By Form: Capsules Lead While Gummies Surge

Capsules retained a 37.76% revenue share in 2025, appreciated for dose precision and easy inclusion of multi-ingredient matrices. Softgels dominate fat-soluble nutrients such as omega-3 DHA and ubiquinol, whereas tablets offer manufacturing economies for mass-market SKUs. Powders and ready-mix sachets fulfill niche preferences for additive-free or customizable dosing, yet palatability hurdles limit their mainstream uptake.

Gummies are projected to progress at a 9.12% CAGR to 2031—a trajectory mirrored in several adjacent supplement categories—as younger consumers equate health maintenance with snack-like convenience. Formulators address thermal sensitivity and sugar-content warnings by deploying pectin bases and lower-glycemic sweeteners. Should these technological refinements hold, gummies will carve out a larger slice of the fertility supplements market, especially in e-pharmacy baskets.

By Consumer: Female Focus Expands to Male Awareness

Women-oriented products held 52.02% of the fertility supplements market size in 2025, underpinned by folic-acid mandates and stronger OB-GYN engagement. PCOS-targeting blends that couple myo-inositol with selenium and probiotics are showing rapid shelf-rotation in Asia-Pacific pharmacies. Demand is further stoked by delayed motherhood trends and employer-backed fertility benefit coverage in the United States.

Male-specific SKUs are advancing the fastest at an 8.41% CAGR, aided by greater public exposure of male-factor infertility statistics and encouraging data on L-carnitine, omega-3s and CoQ10. A three-month, 3 g/daily L-carnitine protocol lifted sperm motility from 15% to 50% and count from 25 million/mL to 49 million/mL, validating nutrient intervention for asthenozoospermic patients. Couple-centric bundles—one box for him, one for her—are now common, simplifying buying decisions and enlarging revenue per household within the fertility supplements market.

By Distribution Channel: E-Pharmacy Disrupts Traditional Retail

Retail pharmacies preserved 43.08% market share in 2025 on the strength of in-store clinical advice. Shelf adjacency to prenatal vitamins fosters impulse purchases among women planning pregnancy. Brick-and-mortar chains are experimenting with point-of-care fertility screening kits that funnel shoppers toward bundle deals including ovulation strips and antioxidant capsules.

E-pharmacy is tracking a 9.08% CAGR, catalyzed by discreet procurement, subscription auto-ship and AI-driven product matching. Asia-Pacific markets, where smartphone penetration eclipses primary healthcare infrastructure, illustrate the channel’s capacity to democratize access to premium formulations. Direct-to-consumer startups exploit this momentum through social-media storytelling, while legacy brands counter by strengthening omnichannel presences. As such, online platforms are set to command a larger portion of the fertility supplements market over the forecast horizon.

Geography Analysis

North America controlled 35.41% of global revenues in 2025, buoyed by the highest employer penetration of fertility benefits and a mature supplement culture that accepts premium pricing for clinically backed formulations. The United States’ pre-conception knowledge advantage partially offsets patchy supplement adherence, creating room for professional-only lines that double as prescription adjuncts. Regulatory rigor is also intensifying: the FDA’s 75-day new-ingredient rule is weeding out under-substantiated SKUs but simultaneously consolidating consumer confidence. This confluence of favorable coverage, medical endorsement and consumer trust solidifies North America’s role as the anchor market for fertility supplements.

Asia-Pacific is the fastest-growing theatre, anticipated to log a 7.48% CAGR. Rising infertility—exacerbated by urban lifestyles, postponement of parenting and mounting PCOS incidence—has magnified demand in China, India and the Philippines. The fertility supplements market size for Asia-Pacific is projected to eclipse USD 1.49 billion by 2031, capturing more than one-third of incremental global dollars. Multinationals are responding through local acquisitions—Barentz’s purchase of China’s Fengli Group and Nestlé’s expanded women’s-health platform—while domestic entrants leverage herbal heritages to differentiate in an ingredient-conscious consumer base.

Europe, grounded in stringent health-claim regulation under EFSA, registers steady mid-single-digit growth as brands lead with documented benefits and transparent labelling. South America and the Middle East & Africa are still nascent, yet incremental rises in disposable income and e-commerce penetration are nurturing early adoption. Currency fluctuations and fragmented distribution keep short-term growth tempered, but escalating ART uptake and government-sponsored maternal-health programs point to medium-term potential. Consequently, the fertility supplements market maintains a genuinely global profile, albeit shaped by region-specific regulatory and cultural determinants.

Competitive Landscape

The market remains fragmented; no single supplier controls more than a mid-single-digit percentage of global revenue. Nutraceutical specialists such as Vitabiotics, Fairhaven Health and Theralogix depend on randomized controlled trial portfolios to defend price premiums. Generalist supplement houses GNC and Nature’s Bounty ride brand familiarity and broad retail presence but must update formulations to match evidence-led competitors. Pharmaceutical crossover interest is intensifying: Sanofi’s USD 1 billion purchase of Qunol injects big-pharma resources into the previously niche coenzyme Q10 segment, signalling broader convergence between therapeutics and nutrition.

Strategic playbooks cluster around three levers. First, clinical differentiation: controlled trials not only unlock physician recommendation but insulate margins against commoditization. Second, technology: sustained-release beads, liposomal carriers and taste-masked gummies are opening new demographics and dosing regimens. Third, omnichannel distribution: companies integrate direct-to-consumer subscription portals with in-clinic sampling to capture both digitally native and clinician-guided buyers. Heightened regulatory scrutiny selectively advantages incumbents with dedicated compliance functions, as smaller entrants face cost-prohibitive dossier requirements.

Partnership activity is also brisk. Brands collaborate with fertility clinics to co-develop protocol-specific packs that synchronize with ART cycles, thus embedding supplements into patient pathways. Ingredient vendors partner with finished-product formulators to generate proprietary blends offering mutual exclusivity. Investors have flagged male-fertility products, genetic-testing-led personalization and data-backed subscription models as greenfield categories. Competitive intensity will remain high, yet the growing clinical validation trend underpins rising barriers to entry, helping the fertility supplements market mature without eroding profitability.

Fertility Supplement Industry Leaders

Fairhaven Health

Coast Science

LENUS Pharma GesmbH

Exeltis USA, Inc.

Vitabiotics Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sanofi closed its USD 1 billion acquisition of CoQ10 brand Qunol, adding fertility-adjacent antioxidant assets to its consumer-health portfolio.

- June 2025: Barentz purchased China’s Fengli Group to expand its nutraceutical reach across cognition, immunity and fertility.

- June 2025: Nestlé designated women’s health—including fertility—an Asia-Pacific growth pillar, spotlighting Materna DHA and related SKUs.

- May 2025: California Senate advanced SB 646, mandating heavy-metal testing in prenatal vitamins.

- June 2025: Gnosis by Lesaffre published a study confirming HY-FOLIC’s doubled bioavailability versus standard folic acid.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global fertility supplement market as finished, non-prescription or practitioner-recommended nutraceuticals (vitamins, minerals, herbs, antioxidants, and amino acids) formulated to support male or female reproductive parameters before or during conception and sold as capsules, tablets, gummies, soft gels, powders, or liquids through pharmacies, e-pharmacies, and specialist health stores.

Scope exclusion: prescription hormonal drugs, IVF culture media, and prenatal multivitamins taken after pregnancy confirmation are not covered.

Segmentation Overview

- By Ingredient

- Natural Ingredients

- Herbal Extracts (Maca, Ashwagandha, Tribulus)

- Vitamins & Minerals (Folic Acid, Zinc, Selenium)

- Antioxidants (CoQ10, Omega-3, Lycopene)

- Synthetic Ingredients

- Blend of Natural & Synthetic

- Natural Ingredients

- By Form

- Capsules

- Tablets

- Softgels

- Gummies

- Powders

- Other Forms (Liquids, Sprays)

- By Consumer

- Female-Specific Supplements

- Male-Specific Supplements

- By Distribution Channel

- Retail Pharmacy

- E-pharmacy

- Other Distribution Channels

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed reproductive endocrinologists, contract manufacturers, retail buyers, and import agents across North America, Europe, and Asia-Pacific; their insight refined penetration ratios, distributor mark-ups, and emerging ingredient preferences that desk work alone could not quantify.

Desk Research

We, the analyst team, mapped demand with UN demographic yearbooks, WHO infertility prevalence surveys, and UN-Comtrade export codes, and then aligned those series with shipment audits from the Council for Responsible Nutrition. Quarterly 10-Ks, investor decks, and price spiders for major e-pharmacies revealed sell-through volumes and average selling prices, while paid libraries such as D&B Hoovers and Dow Jones Factiva let us match company revenues and news flows with customs records. The sources named are only illustrative, and many additional references supported data checks and clarifications.

Market-Sizing & Forecasting

Sizing begins with a top-down prevalence-to-demand model: country infertility incidence and couples actively trying to conceive are multiplied by supplement penetration ratios and blended transaction ASPs, and then sampled brand revenues and channel volumes act as bottom-up checks. Key variables feeding a multivariate regression include assisted-reproduction cycles per million population, female 30-39 cohort growth, OTC price inflation, the rising e-commerce share of supplement sales, and folic-acid fortification mandates; expert consensus bridges any residual data gaps.

Data Validation & Update Cycle

Outputs pass anomaly screens, multi-step peer review, and senior sign-off; we refresh every twelve months and issue interim updates when regulation, major recalls, or landmark clinical evidence materially shift demand.

Why Our Fertility Supplements Baseline Commands Confidence

Published estimates often diverge because firms choose different ingredient baskets, price bases, and refresh rhythms. By anchoring our 2025 value of USD 2.70 billion to prevalence data and calibrated ASPs, Mordor narrows those variables before forecasting.

Typical gap drivers are other publishers bundling prenatal vitamins, omitting male products or e-commerce sales, or rolling forward historic growth without fresh primary inputs.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.70 bn (2025) | Mordor Intelligence | |

| USD 2.20 bn (2024) | Global Consultancy A | Male products and e-commerce channels excluded |

| USD 2.50 bn (2024) | Industry Journal B | Uses list prices instead of transaction ASPs |

| USD 3.97 bn (2024) | Regional Consultancy C | Bundles prenatal and broader women's health vitamins |

The comparison shows that, once scope, price bases, and update cadence are normalized, Mordor's disciplined mix of desk evidence and front-line interviews offers the most balanced, reproducible baseline for strategic planning.

Key Questions Answered in the Report

How big is the fertility supplements market today?

The fertility supplements market is valued at USD 2.88 billion in 2026 and is projected to reach USD 3.94 billion by 2031 at a 6.49% CAGR.

Who are the key players in Fertility Supplement Market?

Natural-ingredient formulations lead, capturing 54.22% revenue share in 2025, with blended natural-synthetic products growing fastest.

Why is Asia-Pacific the fastest-growing region?

Rising infertility rates, expanding middle-class purchasing power and rapid e-commerce adoption are driving a 7.48% CAGR in Asia-Pacific.

Do male-specific fertility supplements have clinical backing?

Yes. A three-month 3,000 mg L-carnitine regimen improved sperm motility from 15% to 50% and count from 25 million/mL to 49 million/mL in asthenozoospermic patients.

What regulatory changes are shaping product development?

The FDA’s 75-day new dietary ingredient notification and California’s proposed heavy-metal testing mandate are increasing compliance costs but bolstering consumer trust.

Which sales channel is growing fastest for fertility supplements?

E-pharmacy is advancing at a 9.08% CAGR, outperforming traditional retail pharmacies by leveraging convenience, privacy and subscription models.

Page last updated on: