Veterinary Supplements Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 10.10 Billion |

| Market Size (2030) | USD 12.80 Billion |

| Growth Rate (2025 - 2030) | 5.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Veterinary Supplements Market Analysis by Mordor Intelligence

The veterinary supplements market size stood at USD 10.1 billion in 2025 and is projected to expand to USD 12.8 billion by 2030, reflecting a 5.1% CAGR through the forecast period. Growing alignment between pet-humanization trends and advanced veterinary science, clearer ingredient-approval pathways, and rapid digital‐commerce adoption sustain demand. Formulations now emulate human nutraceutical standards, leveraging evidence-backed omega-3, probiotic, and senolytic compounds that appeal to health-conscious owners. Regulatory reforms—chiefly the U.S. Animal Food Ingredient Consultation process—offer speedier yet rigorous pathways for novel inputs, benefiting multinationals able to navigate compliance requirements. Accelerating e-commerce and subscription services, anchored by Mars Petcare’s USD 1 billion digital push, are reshaping fulfillment economics and enlarging the addressable customer base. Simultaneously, marine-omega supply volatility nudges manufacturers toward microalgae sources, ensuring product continuity and supporting ESG credentials.[1]Center for Veterinary Medicine, “Animal Food Ingredient Consultation (AFIC),” fda.gov

Key Report Takeaways

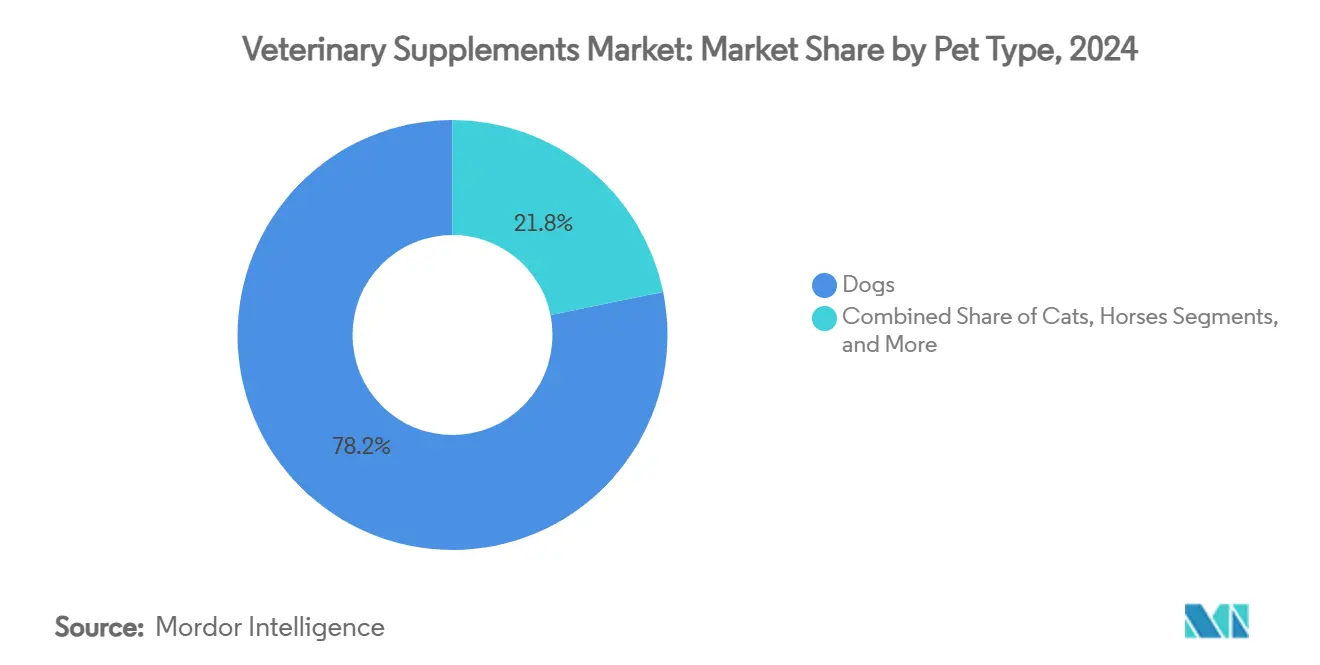

- By pet type, dogs led with 78.2% veterinary supplements market share in 2024, while cats are advancing at a 7.9% CAGR through 2030.

- By health function, hip & joint products accounted for 40.1% of the veterinary supplements market size in 2024, whereas calming & cognitive supplements are projected to grow 6.2% annually to 2030.

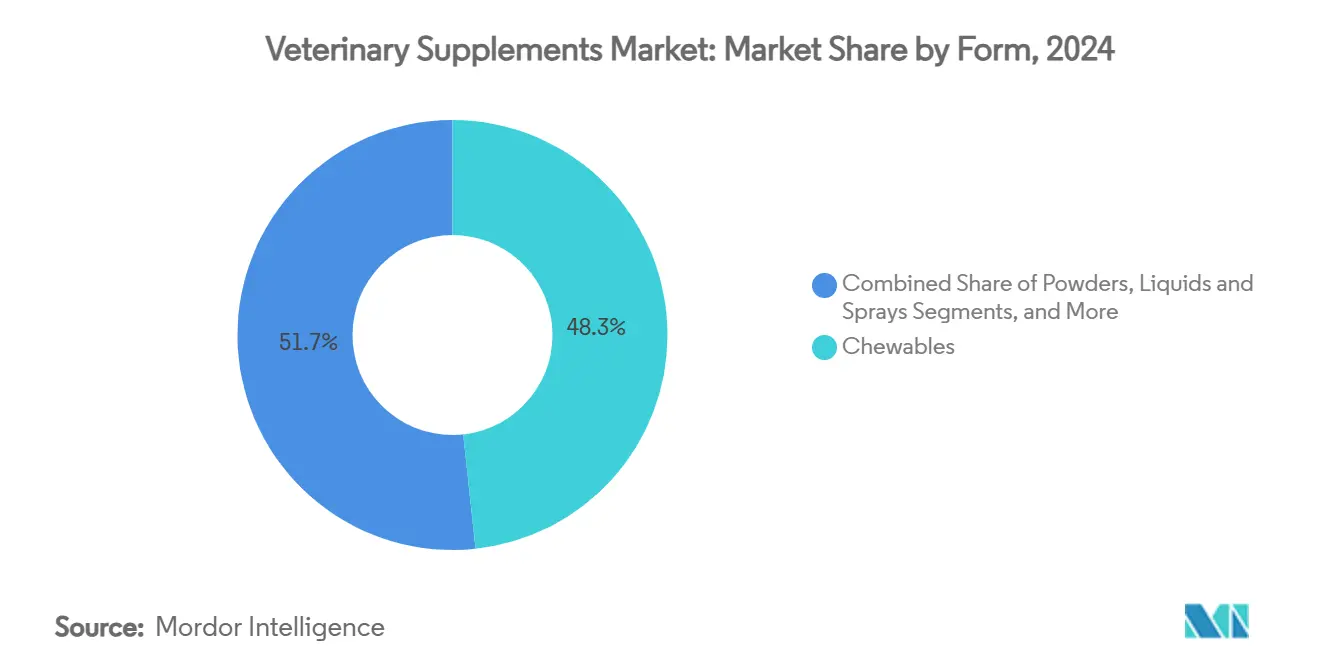

- By form, chewables captured 48.3% share of the veterinary supplements market size in 2024; liquids & sprays record the fastest 5.4% CAGR to 2030.

- By distribution channel, offline pet-specialty stores held 44.5% of the veterinary supplements market in 2024, yet online/subscription models are forecast to expand 7.6% a year.

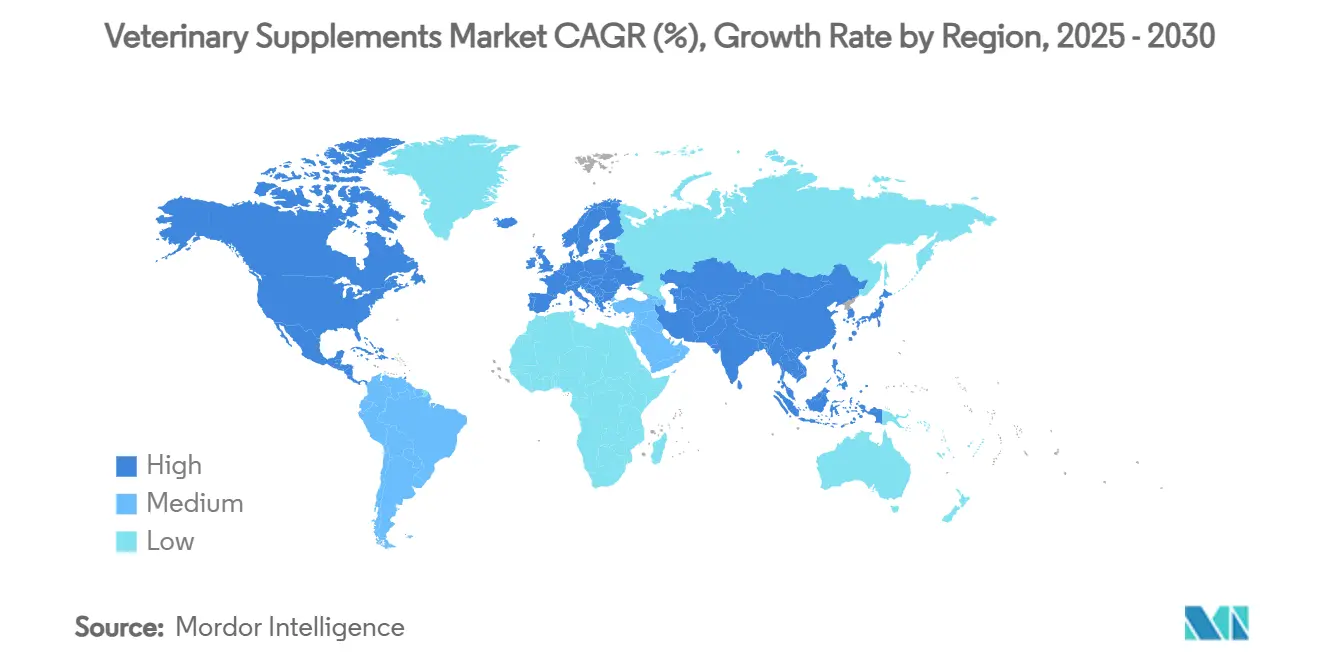

- By geography, North America represented 40.3% of the veterinary supplements market in 2024, while Asia-Pacific is poised for the highest 7.9% CAGR through 2030.

Global Veterinary Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pet Humanisation & Premium Wellness Spend | +1.80% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Ageing-Pet Population Driving Chronic-Care Supplements | +1.20% | North America & Europe core, expanding to APAC | Long term (≥ 4 years) |

| Surge In E-Commerce & Subscription Models | +0.90% | Global, led by North America digital adoption | Short term (≤ 2 years) |

| Evidence Base For Omega-3 & Probiotic Efficacy Expands | +0.70% | Global, regulatory-dependent adoption rates | Medium term (2-4 years) |

| Veterinarian Private-Label Lines Boost Clinic Margins | +0.50% | North America & Europe veterinary markets | Medium term (2-4 years) |

| AI-Driven Microbiome Tests Enabling Personalised Blends | +0.40% | North America early adoption, APAC following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pet Humanization & Premium Wellness Spend

Owners increasingly treat animals as family members, with 66% expressing willingness to pursue life-extending treatments. Spending behavior supports premium preventive care despite inflationary pressure, as 36% of owners cite cost concerns yet maintain supplement purchasing intent. In Asia-Pacific, over half of Chinese pet parents now view their pets as children, opening white-space for Western formulations. Mars Petcare’s USD 1 billion direct-to-consumer investment underscores the strategic value of personalized engagement. Millennials and Gen Z drive 84% of new supplement launch growth, ensuring longevity for this demand catalyst.

Ageing-Pet Population Driving Chronic-Care Supplements

Longer lifespans create a larger cohort of senior dogs and cats requiring joint, cognitive, and metabolic support. Brands such as Zesty Paws and Animal Biosciences are commercialising NAD+ precursors and senolytic blends that pivot care from reactive to preventive. Joint-health formulations increasingly layer collagen peptides and botanicals onto glucosamine-chondroitin cores for multi-modal efficacy. Rising veterinary visits for geriatric management elevate clinic-dispensed supplement opportunities and reinforce cross-selling with diagnostics. Developed-market concentration today indicates room for uptake as emerging economies expand companion-animal clinical services.

Surge in E-Commerce & Subscription Models

Subscription services now generate up to 45% of some retailers’ supplement revenue, reducing in-store footfall and locking in predictable cash flows. Chewy’s Goody Box exemplifies embedded loyalty; 53% of subscribers report less brick-and-mortar shopping. Industry projections place e-commerce at 45% of overall U.S. pet-product sales by 2026, with automated replenishment engines boosting customer lifetime value. Pet Valu’s partnership with Ordergroove illustrates how mid-tier retailers tap platforms rather than build proprietary tech. These dynamics elevate data-driven cross-selling and heighten barriers for brands lacking digital fluency.

Evidence Base for Omega-3 & Probiotic Efficacy Expands

Peer-reviewed studies now document measurable improvements in gut microbiota and inflammatory markers from Saccharomyces cerevisiae supplementation in aged dogs. Such findings legitimise health claims long reliant on anecdote, prompting FDA guidance that references published efficacy data. Royal Canin’s launch of biotics-powered chews formulated with clinically proven S. boulardii CNCM I-1079 signals that R&D-validated strains command premium positioning. Expanding microbiome databases underpin personalized product design, reinforcing the competitive edge of firms prepared to invest in long-term trials.[2]Animals Journal, “Effects of Dietary Saccharomyces cerevisiae Supplementation on Gut Microbiota Composition and Gut Health in Aged Labrador Retrievers,” mdpi.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Ambiguity: Feed Vs. Drug Classification | -0.80% | Global, most acute in North America & Europe | Medium term (2-4 years) |

| Limited Peer-Reviewed Efficacy Data | -0.60% | Global, regulatory-dependent markets | Long term (≥ 4 years) |

| Premium Pricing Limits Penetration In Value Segments | -0.50% | Global, pronounced in emerging markets | Short term (≤ 2 years) |

| Volatile & ESG-Scrutinised Marine-Omega Supply Chain | -0.40% | Global, supply-dependent manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Ambiguity: Feed Vs. Drug Classification

The FDA’s 2024 termination of its AAFCO cooperation agreement narrows approval paths to food-additive petitions and GRAS notifications, escalating costs and delaying launches. Functional actives such as CBD risk reclassification as drugs if therapeutic claims exceed nutritional scope, forcing expensive clinical trials and prescription-only status. Fragmented state-level oversight compounds uncertainty, exemplified by AAFCO’s objections to the federal PURR Act. Smaller brands lacking dedicated compliance teams face disproportionate burdens and may seek acquisition partners better equipped to navigate the evolving landscape.

Limited Peer-Reviewed Efficacy Data

While quality-control schemes strengthen manufacturing standards, many novel ingredients still rely on human studies or anecdotal justification. Rising veterinarian demand for strain-specific or compound-specific data places lesser-known brands at a disadvantage. The deficit is acute in cognitive and anxiety categories, where endpoints are harder to quantify. Firms funding proprietary trials, such as Hill’s Pet Nutrition’s prebiotic-fiber research, benefit from elevated clinic recommendation rates. Regulatory emphasis on evidence-backed marketing claims will further widen the divide between research-centric players and opportunistic entrants.[3]Allison P. McGrath, “Prebiotic Fiber Blend Supports Growth and Development and Favorable Digestive Health in Puppies,” Frontiers in Veterinary Science, frontiersin.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pet Type: Canine Dominance, Feline Momentum

Dogs accounted for 78.2% of the veterinary supplements market size in 2024, reflecting larger body-mass dosing needs and entrenched preventive-care habits. Sales skew toward hip-&-joint and digestive products supported by decades of efficacy validation. Cats, however, post a 7.9% CAGR to 2030 as brands engineer palatable, feline-specific formulas that address obligate-carnivore metabolic nuances. Dechra’s Lanthanum-based Catney One illustrates premium willingness among owners managing chronic kidney issues. Equine niches remain stable, while livestock and exotics deliver incremental gains as antibiotic-reduction initiatives and urban pet mini-trends emerge.

Feline growth lifts absolute revenue despite smaller share, making specialized renal, urinary, and hairball solutions attractive white-space. Canine share continues to anchor revenue forecasts, yet category leaders now segment by life stage and breed size, expanding the total addressable pool. The veterinary supplements market maintains favorable elasticity because owners perceive supplements as non-discretionary quality-of-life investments.

By Health Function: Joint Dominance, Cognitive Upside

Hip-&-joint formulations captured 40.1% veterinary supplements market share in 2024 as aging pets and obesity prevalence keep osteoarthritis management a top clinical priority. Innovation blends collagen, turmeric, and boswellia with legacy glucosamine–chondroitin stacks to offer faster onset and multi-pathway relief. Calming & cognitive products, expanding at 6.2% CAGR, benefit from elevated awareness of anxiety as a treatable condition. Probiotic-enriched chews containing L-theanine and tryptophan illustrate cross-functional design that resonates with behavioural-health trends.

Digestive health remains a core growth pillar as microbiome research fuels targeted probiotic strains and postbiotic metabolites. Skin-&-coat solutions hold steady demand but face supply-chain pressure on marine-sourced EPA/DHA, accelerating algae-derived alternatives. Immune support follows seasonal peaks yet is transitioning to year-round prophylactic positioning. Greater clinical validation will widen practitioner uptake, reinforcing premium segmentation.

By Form: Chewables Prevail, Liquids Accelerate

Chewables secured 48.3 of % veterinary supplements market share in 2024, owing to treat-like palatability, simple dosing, and packaging convenience. Soft chews cater to senior pets with dental sensitivities and rank highest on owner compliance metrics. Liquids & sprays, rising 5.4% CAGR, serve multi-pet households and weight-based precision dosing, aided by improved flavor masking and shelf stability. Pills and capsules, although cost-efficient, gradually cede share to formats that reduce “pill-fatigue”.

Powders maintain niche appeal for food-mixing, particularly in exotic or multi-species households, yet palatability challenges cap penetration. Companies experimenting with treat-infused formats blur snack-supplement lines, positioning functional indulgence as a behavioral training reward. Formulation flexibility will remain a competitive lever as owners demand both efficacy and administration ease.

By Distribution Channel: Specialist Stores Steady, Digital Surge

Pet-specialty retailers held 44.5% of the veterinary supplements market in 2024 as educated staff and in-store sampling build trust for first-time buyers. Clinic channels retain authority for therapeutic-grade offerings though shelf-space limits expansion depth. Online sales, expanding 7.6% annually, capture convenience seekers and subscription adopters; algorithms recommending refill timing elevate average order value. Mass grocery stores provide broad reach but struggle to showcase premium narratives within limited shelf real estate.

Brands winning omnichannel integration leverage data from direct-to-consumer interactions to optimize brick-and-mortar assortments. Mars Petcare’s platform investments signal category migration toward seamless online-offline ecosystems, making supply-chain agility and last-mile logistics core competencies.

Geography Analysis

North America commanded 40.3% of global revenue in 2024 as high veterinary visitation and insurance penetration underpin consistent supplement adherence. United States consumers favour premium human-grade ingredients, while Canada’s harmonized regulations facilitate efficient cross-border distribution. Mexico’s urbanisation fosters expanding pet ownership, yet price sensitivity channels demand toward value offerings. Digital natives in all three countries accelerate subscription enrollment, reinforcing Mars Petcare’s strategic USD 1 billion ecommerce allocation. Regulatory stability—even amid FDA–AAFCO realignment—sustains innovation, provided firms maintain robust compliance infrastructure.

Europe follows with steady growth, driven by strong preferences for traceable, organic inputs. Germany, the United Kingdom, and France represent core demand centers emphasizing sustainability, where algae-based omega-3 and recyclable packaging gain traction. The regional pet products sector reached €29.1 billion in 2022, signaling fertile ground for functional-supplement up-trading. Brexit complicates logistics for UK-bound shipments, prompting suppliers to establish dual warehousing. Central-Eastern markets such as Poland exhibit above-average probiotic adoption, reflecting consumer receptivity to digestive-health claims.

Asia-Pacific posts the fastest 7.9% CAGR to 2030 as millennial and Gen Z cohorts in China and India elevate companion-animal spending. China’s pet owners increasingly mirror Western attachment norms, driving import demand for trusted brands. Japan remains an innovation lighthouse, demonstrating receptivity to personalized nutrition subscriptions. Regulatory structures are maturing unevenly; Australia offers streamlined approvals, whereas India’s nascent framework still bifurcates feed and drug categorization. Nonetheless, rising disposable incomes and pet telehealth uptake point to sustained supplement-category lift.

Competitive Landscape

The veterinary supplements market is moderately fragmented; however, consolidation is accelerating as food and pharma majors purchase niche innovators to secure vertical integration. Mars Petcare’s USD 35.9 billion Kellanova and USD 120 per-share Heska acquisitions expand diagnostics and broaden pet-care touchpoints. General Mills’ USD 1.45 billion Whitebridge Pet Brands deal deepens feline treats and functional offering, illustrating cross-category synergies. Private equity, typified by Morgan Stanley Capital Partners’ FoodScience purchase, validates sector resilience and drives professionalization of operations.

Technology capabilities increasingly differentiate leaders. Mars’ digital investment and Zoetis’ AI diagnostics deliver data insights that inform product customization and accelerate R&D cycles. Niche brands such as Pet Honesty leverage ecommerce mastery to scale rapidly, then translate online success into shelf presence at Target and other major retailers. Regulatory sophistication confers competitive advantage; companies with in-house affairs teams can fast-track novel ingredients through AFIC consultations, while smaller peers often become acquisition targets.

Another battleground is personalised nutrition driven by microbiome analytics. AnimalBiome’s 12,500-sample DNA library supports targeted formulations, challenging incumbents anchored in mass-market SKUs. Strategic divestitures, like Zoetis’ sale of medicated feed additives, show a pivot toward higher-margin companion-animal therapeutics, sharpening focus on preventative supplements.

Veterinary Supplements Industry Leaders

Nestlé Purina PetCare

Mars Petcare

Nutramax Laboratories

Zoetis

Virbac

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Mars Petcare completed the acquisition of Heska for USD 120.00 per share, expanding its Science & Diagnostics division.

- May 2025: Mars Petcare closed the purchase of Champion Petfoods, adding ORIJEN and ACANA premium brands.

- May 2025: Dechra introduced Catney One, a lanthanum-based feline kidney-health supplement.

- November 2024: General Mills agreed to buy Whitebridge Pet Brands for USD 1.45 billion.

Global Veterinary Supplements Market Report Scope

| Dogs |

| Cats |

| Horses |

| Livestock (Cattle & Poultry) |

| Others (Birds & Small Mammals) |

| Hip & Joint |

| Digestive Health |

| Skin & Coat |

| Immune Support |

| Calming & Cognitive |

| Chewables & Soft Chews |

| Pills/Tablets & Capsules |

| Powders |

| Liquids & Sprays |

| Treat-Infused Supplements |

| Veterinary Clinics |

| Pet-Specialty Stores |

| Mass Retail & Grocery |

| Online / E-commerce |

| Direct-to-Consumer Subscription |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Pet Type | Dogs | |

| Cats | ||

| Horses | ||

| Livestock (Cattle & Poultry) | ||

| Others (Birds & Small Mammals) | ||

| By Health Function | Hip & Joint | |

| Digestive Health | ||

| Skin & Coat | ||

| Immune Support | ||

| Calming & Cognitive | ||

| By Form | Chewables & Soft Chews | |

| Pills/Tablets & Capsules | ||

| Powders | ||

| Liquids & Sprays | ||

| Treat-Infused Supplements | ||

| By Distribution Channel | Veterinary Clinics | |

| Pet-Specialty Stores | ||

| Mass Retail & Grocery | ||

| Online / E-commerce | ||

| Direct-to-Consumer Subscription | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the veterinary supplements market?

The veterinary supplements market size reached USD 10.1 billion in 2025 and is forecast to climb to USD 12.8 billion by 2030.

Which pet type generates the most supplement revenue?

Dogs account for 78.2% of global sales in 2024, reflecting higher dosage needs and established preventive-care routines.

Which supplement function is growing fastest?

Calming & cognitive formulations are advancing at a 6.2% CAGR through 2030, driven by greater recognition of pet anxiety.

How are online channels affecting sales?

E-commerce and subscription models are expanding 7.6% per year, steadily capturing share from brick-and-mortar outlets.

Why is Asia-Pacific considered a high-growth region?

Rising disposable incomes, urban pet adoption, and increasing humanization among younger owners push Asia-Pacific to a 7.9% CAGR through 2030.

What supply-chain challenge should manufacturers monitor?

Volatility in marine-sourced omega-3 due to Peruvian anchovy quotas is encouraging a shift toward more stable microalgae alternatives.

Page last updated on: