Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 245.67 Billion |

| Market Size (2031) | USD 348.61 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

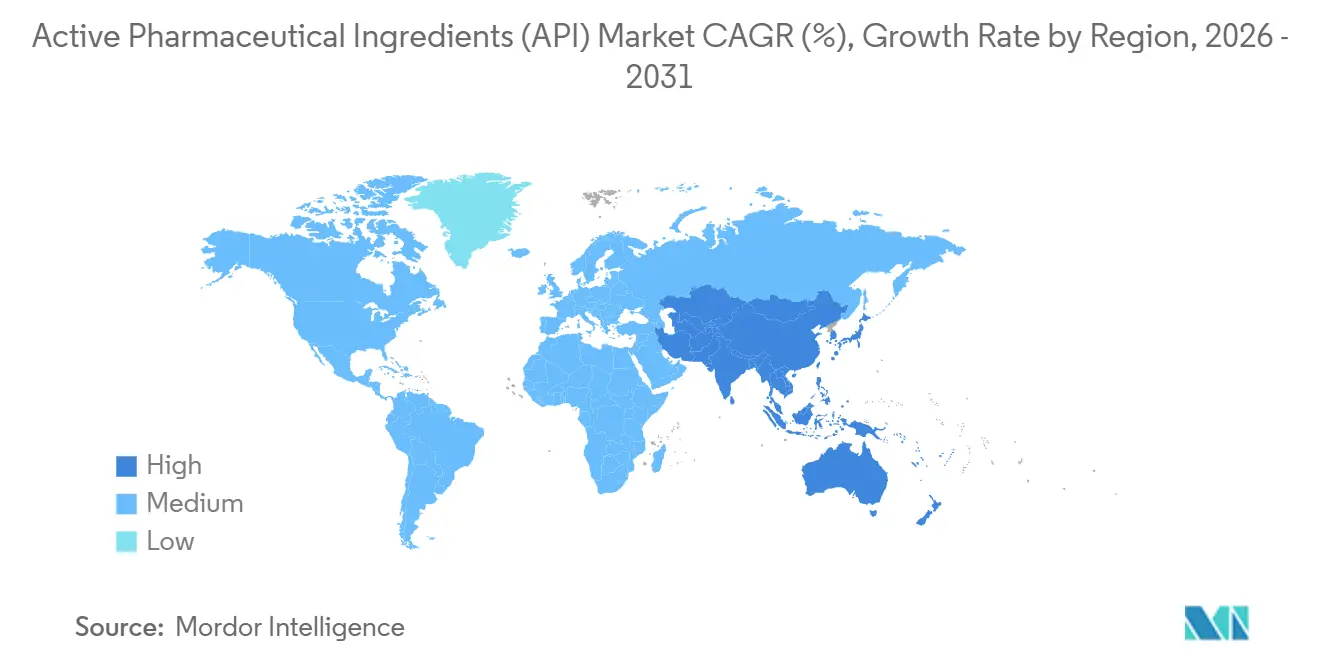

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

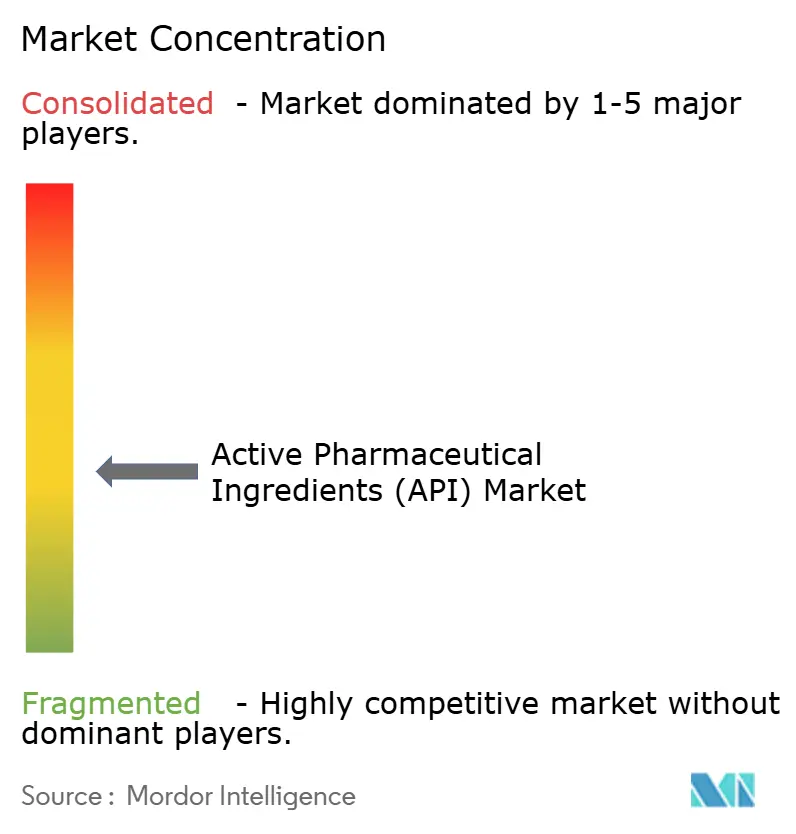

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Active Pharmaceutical Ingredients (API) Market Analysis by Mordor Intelligence

The Active Pharmaceutical Ingredients Market size is estimated at USD 245.67 billion in 2026, and is expected to reach USD 348.61 billion by 2031, at a CAGR of 7.25% during the forecast period (2026-2031).

Aging populations, the persistent rise of chronic illnesses, and surging biologics approvals keep demand strong, yet producer margins hinge on merchant manufacturing uptake, continuous-flow plant deployment, and on-shoring incentives in major economies. Governments in India, the United States, and the European Union disbursed more than USD 4 billion in combined Production Linked Incentive and tax-credit packages between 2024 and 2026, shifting new capacity toward domestic clusters. Contract development and manufacturing organizations (CDMOs) scaled faster than captives because continuous-flow and mini-plant technologies shorten cycle times and cut capital intensity for mid-volume APIs. Intensifying compliance rules, including nitrosamine testing and global GMP harmonization, temporarily raise costs but reinforce the case for larger, better-capitalized suppliers able to absorb regulatory overhead.

Key Report Takeaways

- By API type, synthetic molecules captured a 65.78% revenue share in 2025, while biological APIs are expected to expand at a 9.22% CAGR through 2031.

- By manufacturer model, the merchant segment held 48.27% of the active pharmaceutical ingredients market share in 2025 and is projected to grow at a 9.82% rate through 2031.

- By therapeutic area, oncology APIs are poised to expand at a 10.57% CAGR from 2026 to 2031, outpacing cardiovascular APIs, which held a 28.26% share of the active pharmaceutical ingredients market size in 2025.

- By geography, Asia-Pacific posted the fastest trajectory with a 10.57% forecast CAGR through 2031, whereas North America commanded 39.64% of the 2025 revenue base.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Active Pharmaceutical Ingredients (API) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating chronic-disease drug demand | +1.8% | Global, peak in North America & Europe | Medium term (2-4 years) |

| Biologics & targeted-therapy pipeline growth | +2.1% | North America, Europe, core APAC markets | Long term (≥4 years) |

| Outsourced manufacturing cost advantages | +1.5% | Global, spill-over to Middle East & Africa | Short term (≤2 years) |

| Continuous-flow & mini-plant uptake | +0.9% | North America, Europe, India | Medium term (2-4 years) |

| Government PLI/on-shoring incentives | +1.2% | India, United States, European Union | Short term (≤2 years) |

| AI-enabled retrosynthesis | +0.7% | North America, Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Escalating Chronic-Disease Drug Demand

Non-communicable diseases are forecast to increase global prescription volumes by 22% between 2025 and 2030, thereby amplifying baseline API requirements. Indian exports of statin and metformin APIs increased 14% year-over-year in 2025, as European wholesalers pre-built safety stocks. Oncology APIs for checkpoint inhibitors reached USD 12,000 per kilogram in merchant trade in 2025, nearly double the 2023 levels, highlighting the chronic-disease pull on premium molecules. Dedicated fermentation and synthesis lines are being added ahead of forecast demand, marking a departure from prior just-in-time practices.[1]Hannah Kuchler, “Pharmaceutical Manufacturing Trends,” Financial Times, ft.com Sizable but uneven spending pressures commodity suppliers, yet innovators with a specialty focus sustain stronger pricing.

Biologics & Targeted-Therapy Pipeline Expansion

Monoclonal antibodies, biosimilars, and antibody-drug conjugates made up 43% of FDA approvals in 2025, up from 31% in 2020.[2]U.S. Food and Drug Administration, “New Drug Therapy Approvals 2025,” fda.gov Samsung Biologics brought a 256,000-liter plant online in May 2025 to meet the rising demand for biologics.[3]Samsung Biologics, “Newsroom,” samsungbiologics.com Lonza invested CHF 1.2 billion in mammalian-cell capacity across Switzerland and the United States, improving scale for advanced modalities. Peptide APIs for GLP-1 agonists still face tightness despite supplier expansion, reflecting rapid uptake in diabetes and obesity therapy. Extended review timelines, often 18-24 months for multi-region filings, remain a gating factor but are gradually easing under evolving biosimilar comparability rules.

Outsourced Manufacturing Cost Advantages

CDMOs can trim total ownership costs by up to 35% through shared utilities, dossier reuse, and flexible batch scheduling. WuXi AppTec reported 19% API revenue growth for the twelve months ended June 2025, primarily driven by North American biotech clients. Piramal Pharma Solutions added OEB-5 suites in Ahmedabad in March 2025 to support high-potency oncology programs. Rising regulatory overhead, including nitrosamine testing, favors merchant partners able to amortize compliance costs across large portfolios. As venture-backed firms shun capital-intensive assets, outsourced models gain momentum.

Continuous-Flow & Mini-Plant Technologies Gain Traction

Continuous reactors compress reaction times from hours to minutes and reduce solvent use by up to 60%, aligning with FDA Quality-by-Design expectations. Pfizer CentreOne’s Michigan line cut batch-release cycles by 30% after the August 2024 retrofit. Cambrex, via its Snapdragon unit, commercialized photochemical flow systems capable of novel C–H activation routes for oncology intermediates. A 2025 EMA draft clarified validation rules for continuous processes, accelerating European adoption. Modular mini-plants, capable of producing 10–50 kg per day, are proliferating in India and China, offering rapid clinical-stage supply without the need for mega-site lead times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global GMP & nitrosamine compliance | −0.9% | Global, acute in Europe & North America | Short term (≤2 years) |

| Generic-price compression | −1.1% | North America, Europe, emerging markets | Medium term (2-4 years) |

| Supply-chain opacity | −0.6% | Global, concentrated in Asia sourcing | Medium term (2-4 years) |

| Complex biotech regulatory harmonization | −0.5% | Multi-region filings, APAC & MEA delays | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Global GMP & Nitrosamine-Control Compliance Costs

Mandatory nitrosamine testing, fully enforced from 2024, adds USD 150,000–300,000 per dossier and triggered 483 FDA observations at Indian and Chinese sites between 2024 and 2025. EMA aligned thresholds with the FDA in March 2025, removing lower-cost regulatory arbitrage. Smaller firms often lack the funds for high-resolution mass spectrometry upgrades, which accelerates consolidation. Commodity suppliers struggle to pass through new costs, whereas innovators embed compliance expense into project budgets.

Generic-Price Compression Squeezing API Margins

Average U.S. generic-drug prices fell 37% between 2020 and 2025, driven by PBM consolidation and aggressive state tenders. Indian API exporters experienced a decline in gross margins, dropping to 18-22% in 2025 compared to 26-30% in 2020. Dr. Reddy’s exited three generic lines in 2024 to focus on higher-potency niches. European hospital antibiotic bids in 2025 came in 40% below 2023 levels, forcing low-cost relocation strategies. Biologics and HPAPIs partly offset erosion due to higher complexity and fewer qualified suppliers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By API Type: Biologics Outpace Synthetics as Pipelines Evolve

Synthetic APIs held 65.78% revenue in 2025, anchored by small-molecule generics for cardiovascular and metabolic therapy, while biologics are slated to post a 9.22% CAGR to 2031, a trend that will raise the biologics share of the active pharmaceutical ingredients market size to nearly one-third. Highly potent APIs increased by 8.1% in 2025 as antibody-drug conjugate payloads advanced, prompting the development of new OEB-5 suites at Lonza and Piramal.

Developers favor biologics for their extended exclusivity and differentiated mechanisms, but large-scale capacity remains concentrated in a handful of players, which keeps average sell prices high. Synthetic producers counter by moving toward continuous-flow and green-chemistry routes that cut solvent waste and shrink batch footprints. Sustainable-sourcing certifications are increasingly influencing purchasing decisions for natural or phytochemical APIs, a small yet image-sensitive niche.

By Manufacturer Model: Merchant Gains as Innovators Shed Assets

Captive plants commanded 51.73% of 2025 revenue, but merchant producers are set to grow faster, lifting their slice of the active pharmaceutical ingredients market to more than 55% by 2031. WuXi AppTec’s 19% annual API sales gain illustrates the pivot, with biotech clients leveraging its regulatory files to avoid capital outlays.

Integrated drug makers maintain select captive lines for intellectual property control, yet fixed costs and underutilization prompt asset sales or hybrid agreements. CDMOs absorb compliance risk and offer faster scale-up, while real-time analytics and AI design tools reduce per-batch engineering, widening the cost gap versus in-house plants.

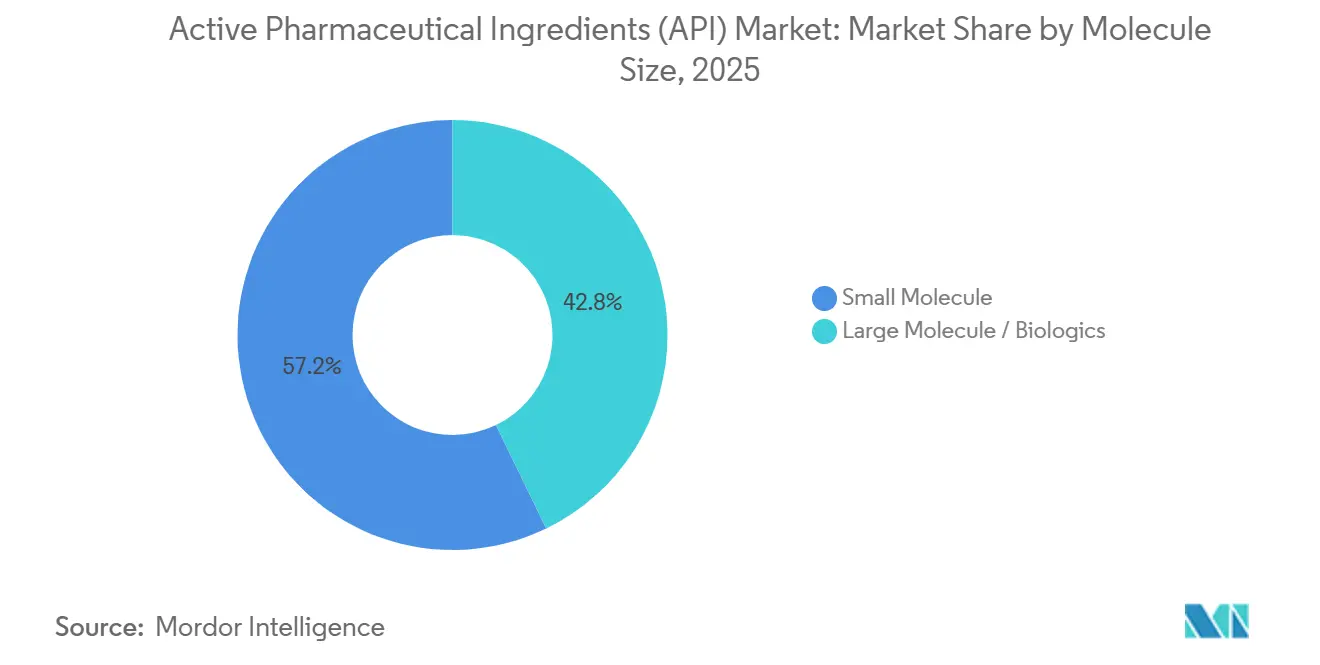

By Molecule Size: Large Molecules Gain Share

Small molecules comprised 57.18% of the volume in 2025; however, large molecules are projected to grow at 8.06% through 2031, raising their portion of the active pharmaceutical ingredients market share to near parity by the end of the period. Novo Nordisk and Eli Lilly both expanded peptide lines after GLP-1 demand strained supply, with Lilly investing USD 1.8 billion in North Carolina.

Monoclonal antibodies average USD 3,500–6,000 per gram, reflecting the upstream complexity and rigorous viral-clearance validation, whereas commodity small molecules continue to face price pressure. Process intensification and single-use systems are narrowing cost gaps for biologics, supporting sustained momentum in large-molecule output.

By Therapeutic Area: Oncology Leads Growth

Cardiovascular APIs accounted for 28.26% of 2025 revenue, but oncology is expected to expand at a 10.57% CAGR through 2031, thereby increasing its contribution to the active pharmaceutical ingredients market size by mid-forecast. Twelve antibody-drug conjugates cleared the FDA in 2024-2025, each requiring high-potency payload manufacture under strict containment, restricting the supplier field to specialized CDMOs.

Metabolic disorder APIs grew, driven by the combined uptake of diabetes and obesity therapies. Infectious-disease APIs lag due to aggressive tenders, while CNS molecules continue to track steady mid-single-digit growth, supported by mental-health initiatives.

Geography Analysis

North America captured 39.64% of the 2025 revenue in the active pharmaceutical ingredients market, driven by Pfizer CentreOne's expansions and the FDA's expedited pathways, which shave 6–9 months off oncology API timelines. The Inflation Reduction Act’s credit structure encourages the co-location of API and finished-dosage lines, as evident in AbbVie’s USD 1.5 billion biologics upgrade in Massachusetts, completed in March 2025. Canada’s regulatory alignment with the FDA speeds Drug Master File approvals, supporting modest domestic growth, while Mexico attracts European CDMOs seeking U.S. proximity through new Monterrey capacity at Recipharm.

Europe will benefit from the forthcoming Critical Medicines Act aimed at 15 essential APIs, though high labor costs temper expansion. Lonza invested CHF 1.2 billion in Swiss and UK sites through 2025, with a focus on mammalian cell and viral vector production. Post-Brexit MHRA rolling-review rules accelerate UK approvals, but dual compliance with EMA standards raises costs for cross-border suppliers. France, Italy, and Spain collectively utilize reshoring grants to revive their antibiotic and sterile-injectable lines, thereby balancing earlier offshoring to Asia.

The Asia-Pacific region is forecast to grow at 10.57% through 2031, the fastest among regions, driven by India’s PLI outlays and China’s shift from commodity to high-potency oncology intermediates. China’s NMPA issued 62 warning letters in 2024-2025, driving facility upgrades but also brief supply disruptions. Japan remains a specialty-API hub, with Fujifilm Diosynth expanding cell-culture capacity, while South Korea’s Samsung Biologics plant cements the country’s biosimilar prominence.

Competitive Landscape

The active pharmaceutical ingredients market is moderately fragmented. WuXi AppTec, Lonza, and Samsung Biologics jointly invested USD 4.8 billion between 2024 and 2026 to expand capacity and introduce new technology, thereby compressing clinical-stage lead times to 12–16 months. GSK’s 2024 divestiture of its UK cephalosporin plant to Recipharm typifies large pharma offloading lower-margin assets while safeguarding biologics lines.

White-space opportunities cluster in cell- and gene-therapy APIs such as viral vectors and lipid nanoparticles, where only a handful of firms possess commercial capacity. Green chemistry routes that reduce Scope 3 emissions also differentiate suppliers as drug makers set climate targets. Emerging disruptors such as Snapdragon Chemistry advance photochemical flow reactors, enabling previously uneconomical transformations at scale. Evonik’s bio-surfactant excipients offer petroleum-free alternatives, securing the first FDA filings in 2025.

Regulatory compliance and pre-approved Drug Master Files form durable moats, allowing certified CDMOs to command 10–15% price premiums. AI integration into process development further segments leaders from followers, with WuXi AppTec reporting 25% quicker route design after deploying retrosynthesis tools in 2025.

Active Pharmaceutical Ingredients (API) Industry Leaders

Teva Pharmaceutical Industries Ltd

Pfizer Inc.

Merck KGaA

BASF SE

Viatris, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: President Trump signed an executive order to accelerate U.S. API plant approvals and tighten inspections of overseas sites, incentivizing domestic capacity.

- April 2025: Eli Lilly unveiled a USD 5.3 billion Indiana API campus to bolster pipeline supply security.

- February 2025: Novo Nordisk expanded peptide capacity for GLP-1 receptor agonists to meet surging diabetes and obesity demand.

- January 2025: Cambrex completed a USD 30 million high-potency API expansion in North Carolina.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global active pharmaceutical ingredients (API) market as the aggregate ex-factory sales of drug substances, whether synthetic or biotech derived, supplied either captively or through merchant contracts for human therapeutic use. The valuation captures revenues from small- and large-molecule APIs, spanning traditional as well as high-potency classes, across all therapeutic areas and geographies.

Scope exclusion: excipients, finished dosage forms, veterinary APIs, diagnostics reagents, and in-process intermediates are outside this analysis.

Segmentation Overview

- By API Type

- Synthetic APIs

- Biological APIs

- Highly-Potent APIs (HPAPIs)

- Natural / Phytochemical APIs

- By Manufacturer Model

- Captive / In-house

- Merchant / Outsourced

- By Molecule Size

- Small Molecule

- Large Molecule / Biologics

- By Therapeutic Area

- Oncology

- Cardiovascular

- Infectious Diseases

- Metabolic Disorders

- CNS & Neurology

- Other Therapeutic Area

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed procurement heads at innovator pharma firms, merchant API sales managers, and regulators across North America, Europe, India, and China. These discussions validated prevailing average selling prices, captive versus outsourced mix shifts, HPAPI demand inflection points, and regional reshoring incentives that literature alone could not quantify.

Desk Research

We began by mapping universe boundaries through publicly available tier-1 sources such as US FDA DMF listings, EMA EudraGMDP certificates, UN Comtrade HS 30 export-import flows, OECD pharmaceutical output indices, and WHO ATC drug utilization datasets. Industry associations, such as the European Fine Chemicals Group and the Association for Accessible Medicines, helped us benchmark capacity and generic penetration. Company 10-Ks, investor decks, and audited CDMO financials complemented these statistics, while D&B Hoovers and Dow Jones Factiva supplied curated company-level revenue splits. The sources cited are illustrative; many additional references informed data collection, cross-checks, and scope clarity.

Market-Sizing & Forecasting

Results originate from a top-down reconstruction of global human-use medicine production value, reconciled with trade data and drug-class prevalence, and then corroborated through selective bottom-up roll-ups of sampled API volumes multiplied by blended ASPs. Key model inputs include: 1) branded drug patent expiry schedule, 2) generic Rx volume growth, 3) clinical approvals for biologics, 4) HPAPI facility count and utilization, 5) CDMO capacity additions, and 6) currency-adjusted ASP progression. Multivariate regression links these drivers to market value, and scenario analysis tests downside risks such as regulatory import bans. Where bottom-up samples diverged, gap filling relied on normalized margin bands observed in primary interviews.

Data Validation & Update Cycle

Outputs pass three-layer reviews: analyst peer checks, senior domain lead sign-off, and variance screening against external series. Models refresh annually, with interim tweaks when material events, such as plant shutdowns, major CDMO acquisitions, or policy shifts, occur, ensuring clients receive the latest vetted view.

Why Mordor's Active Pharmaceutical Ingredients Baseline Deserves Your Trust

Published estimates often differ because researchers choose dissimilar boundaries, price stacks, and refresh cadences.

Key gap drivers include: some publishers fold veterinary and excipient revenues into totals; others apply conservative ASP erosion curves or older currency bases; several snapshots rely on straight-line growth from historical consumption rather than validated capacity data that Mordor analysts obtain each quarter.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 232.13 B | Mordor Intelligence | - |

| USD 270.53 B | Global Consultancy A | Adds excipients and counts distributor mark-ups, inflating value |

| USD 144.20 B | Industry Association B | Uses production cost net of margins and omits biotech APIs |

| USD 238.68 B | Trade Journal C | Projects uniform ASP decline, ignoring HPAPI premium and reshoring uplift |

These contrasts show that Mordor's disciplined scope selection, dual-path validation, and yearly refresh deliver a balanced, transparent baseline that decision-makers can replicate and stress-test with confidence.

Key Questions Answered in the Report

What is the projected value of the active pharmaceutical ingredients market by 2031?

The market is expected to reach USD 348.61 billion by 2031, growing at a 7.25% CAGR.

Which segment will post the fastest growth through 2031?

Oncology APIs are forecast to grow at a 10.57% CAGR, the highest among therapeutic areas.

How quickly are biologics APIs expanding compared to synthetic APIs?

Biologics APIs are projected to rise at 9.22% CAGR, versus mid-single-digit growth for synthetics, reflecting pipeline shifts toward complex modalities.

Which region will lead growth in the next five years?

Asia-Pacific is set to post a 10.57% CAGR through 2031, outpacing all other regions due to capacity additions and cost advantages.

Why are CDMOs gaining share in API production?

Outsourcing offers up to 35% cost savings, faster regulatory timelines through pre-approved dossiers, and flexibility that suits asset-light innovator strategies.

Page last updated on: