Phytoestrogen Supplements Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

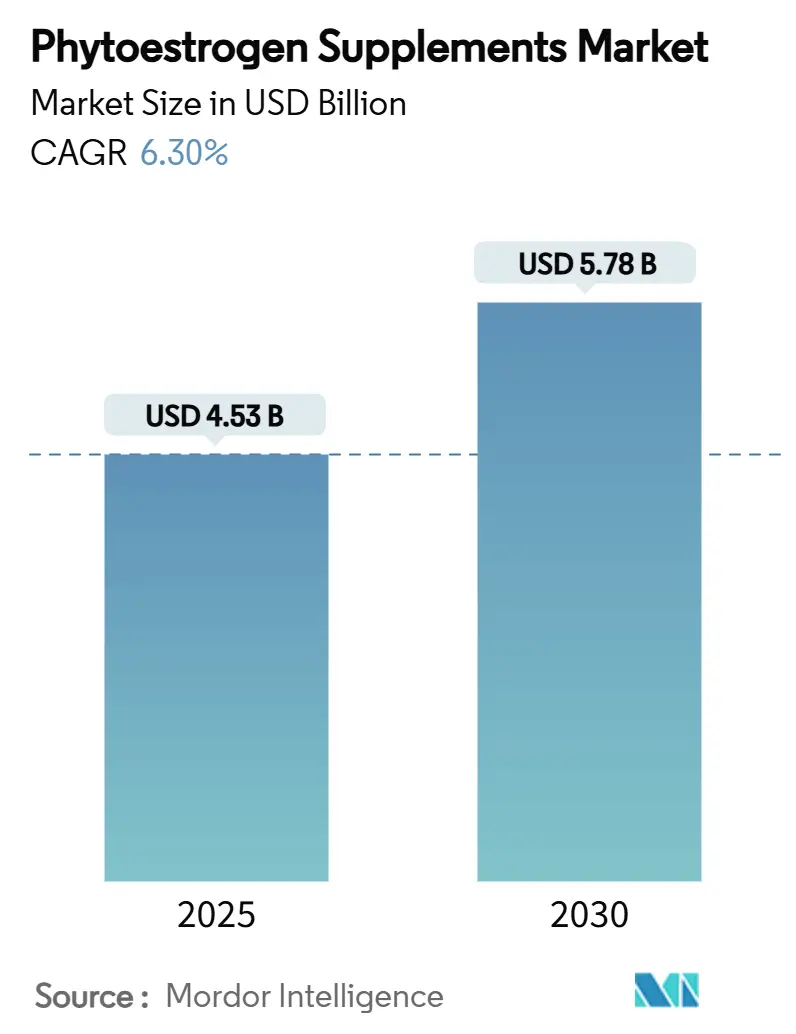

| Market Size (2025) | USD 4.53 Billion |

| Market Size (2030) | USD 5.78 Billion |

| Growth Rate (2025 - 2030) | 6.30% CAGR |

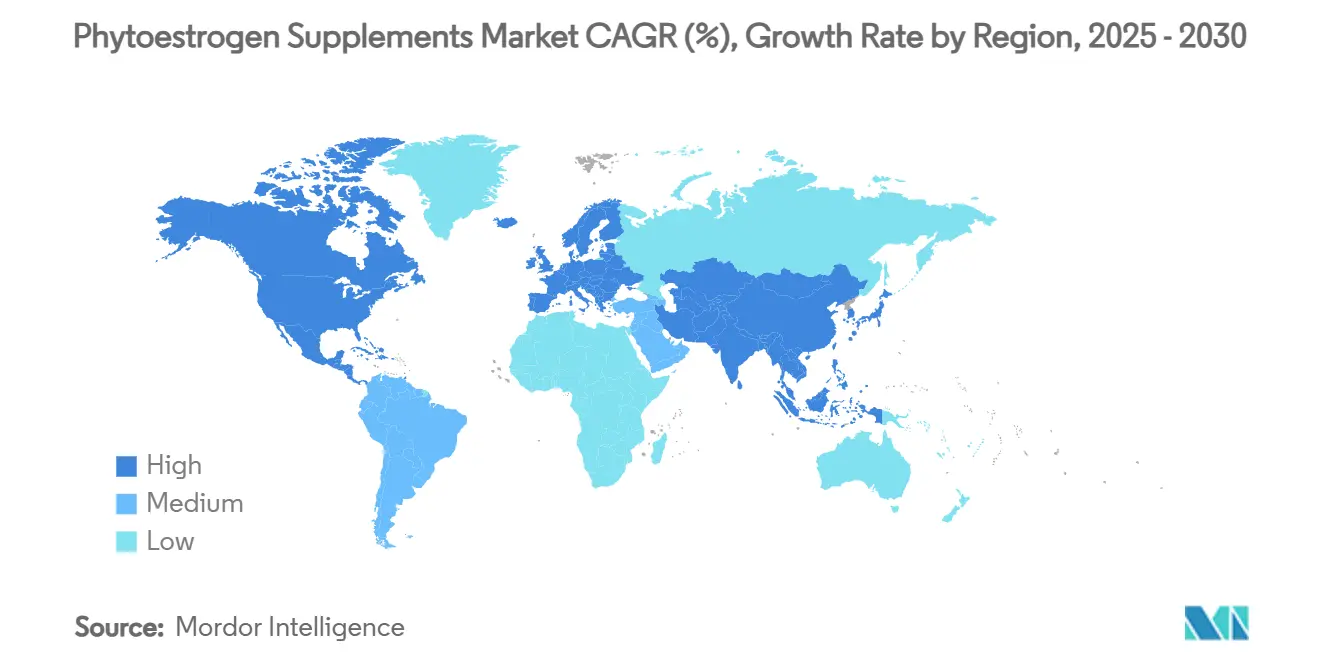

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Phytoestrogen Supplements Market Analysis by Mordor Intelligence

The phytoestrogen supplements market size stood at USD 4.53 billion in 2025 and is forecast to reach USD 5.78 billion by 2030, advancing at a 6.30% CAGR during 2025-2030. Generational shifts, growing clinical confidence in plant-based alternatives to hormone therapy, and favorable risk assessments from the European Food Safety Authority are aligning to keep the phytoestrogen supplements market on an upward trajectory. Heightened awareness among peri- and post-menopausal women, coupled with an expanding online retail footprint, is widening access to evidence-based formulations. The convergence of an aging female population, e-commerce penetration, and intensifying healthcare professional support is steering demand toward clinically validated soy and red-clover extracts, while emerging bone-density data is opening secondary indications beyond vasomotor symptom relief. Competitive intensity is moderate, partly because robust clinical files and regulatory compliance requirements deter quick follower entry, yet significant white-space remains for brands with sustainable supply chains and differentiated delivery systems.

Key Report Takeaways

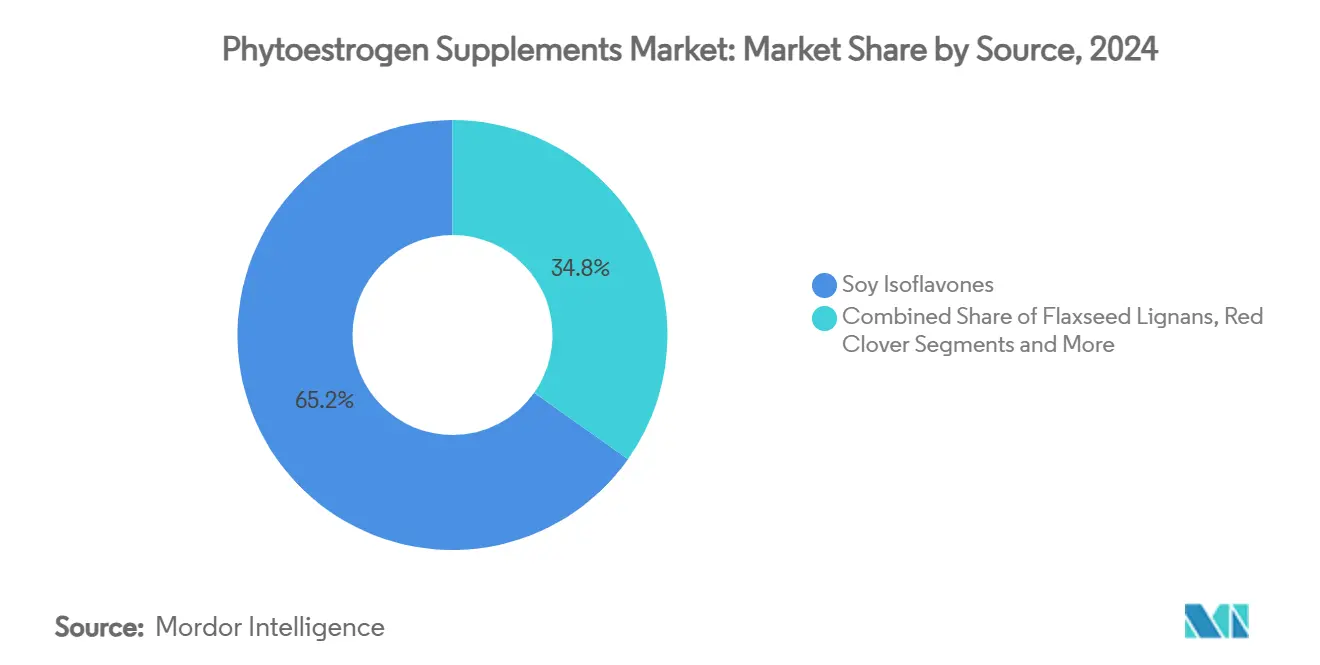

- By source, soy isoflavones led with 65.2% of the phytoestrogen supplements market share in 2024. Red clover isoflavones are projected to post the fastest 9.9% CAGR through 2030.

- By form, capsules accounted for a 45.8% share of the phytoestrogen supplements market size in 2024. Gummies and chewables are forecast to expand at an 11.7% CAGR to 2030.

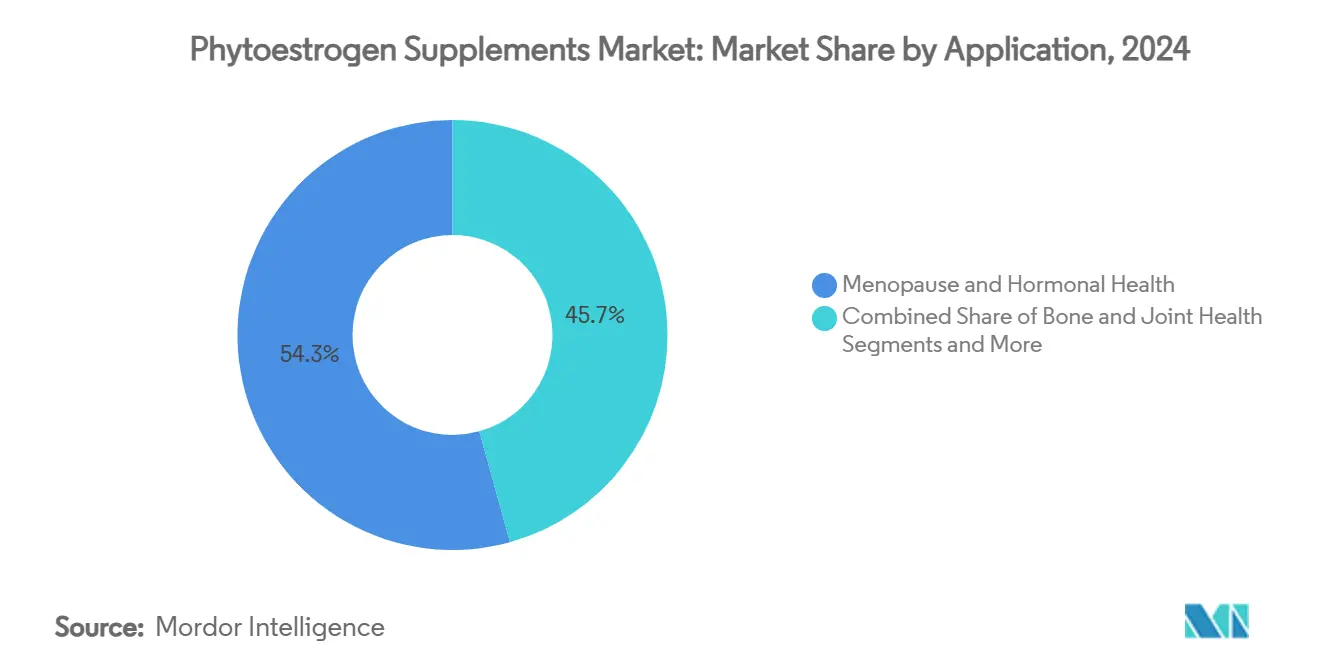

- By application, menopause and hormonal health commanded 54.3% revenue share in 2024. Bone and joint health is advancing at a 10.1% CAGR through 2030.

- By geography, North America captured 34.7% of the phytoestrogen supplements market in 2024. Asia Pacific is recording the highest projected 7.80% CAGR during 2025-2030.

Global Phytoestrogen Supplements Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of menopausal symptoms & HRT avoidance | +1.80% | North America & Europe | Medium term (2-4 years) |

| Consumer shift toward plant-based/natural supplements | +1.20% | Global, led by developed markets | Long term (≥ 4 years) |

| Expanding e-commerce & direct-to-consumer channels | +0.90% | Global, strongest in APAC | Short term (≤ 2 years) |

| Emerging clinical evidence on bone-density benefits | +0.70% | North America & Europe | Long term (≥ 4 years) |

| Demand from sports nutrition for natural hormone modulators | +0.60% | North America & Europe expanding to APAC | Medium term (2-4 years) |

| Fertility clinics recommending isoflavone adjunct therapy | +0.40% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Menopausal Symptoms & HRT Avoidance

An unprecedented cohort of baby-boomer and Gen X women is entering menopause, elevating demand for options that do not rely on synthetic hormone replacement. Contemporary clinical consensus positions soy isoflavones as a first-line modality for vasomotor symptom relief, underpinned by evidence showing daily doses up to 150 mg remain safe for at least three years. Large-scale studies reveal that genistein-, daidzein-, and S-equol-rich formulations reduce hot-flash frequency while preserving cognitive performance. Healthcare providers increasingly recommend phytoestrogen supplementation as part of routine menopausal care, a practice likely to persist through 2030 as societal taboos around menopause lessen and women actively seek science-backed self-care solutions.

Consumer Shift Toward Plant-Based/Natural Supplements

Rising skepticism toward chemically synthesized ingredients is accelerating the adoption of botanical products. U.S. herbal supplement sales reached USD 8.84 billion in 2024, registering the sharpest growth in two decades. The phytoestrogen supplements market benefits directly from this natural-first mindset because isoflavones carry a decades-long safety dossier derived from dietary exposure, satisfying consumer demand for transparent and validated ingredients. Sustainability certifications and non-GMO labeling are now baseline expectations, nudging brands to invest in traceable supply chains and organic verification.

Expanding E-Commerce & Direct-To-Consumer Channels

The digital retail wave continues to expand the phytoestrogen supplements market, with online channels advancing at a 14.5% CAGR against slower brick-and-mortar growth.[1]Ronan Lordan, “Dietary Supplements and Nutraceuticals Market Growth During the Coronavirus Pandemic,” ncbi.nlm.nih.gov Direct-to-consumer platforms create low-friction purchasing paths for peri-menopausal shoppers seeking personalized guidance. Subscription models encourage adherence, enhancing lifetime value in a category where symptom relief is dependent on consistent daily dosing. Targeted social-media campaigns educate consumers about dose levels, contraindications, and realistic benefit timelines, cementing brand loyalty in a market that places high trust on accessible science communication.

Emerging Clinical Evidence on Bone-Density Benefits

The 10.1% CAGR logged by bone and joint health applications reflects deeper scientific inquiry into genistein’s anabolic effects on bone. FOSTEUM received FDA recognition as a medical food for osteopenia management and is influencing physician perceptions of phytoestrogens as dual-action agents for menopausal symptom relief and skeletal support.[2]Primus Pharmaceuticals, “FOSTEUM Capsules Genistein Aglycone 27 MG Citrated Zinc Bisglycinate 20 MG Cholecalciferol 200 IU,” DailyMed, dailymed.nlm.nih.gov Network meta-analyses now explore sequential therapy paradigms that incorporate natural compounds alongside anti-resorptive drugs. As bone-health guidelines emphasize early intervention in post-menopausal women, isoflavone-fuelling formulations are poised to serve a broadened patient pool that includes athletes and active-aging populations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scientific controversy & inconsistent clinical outcomes | -1.10% | Global, strongest in regulated markets | Medium term (2-4 years) |

| Hormone-sensitive cancer risk concerns | -0.80% | North America & Europe | Long term (≥ 4 years) |

| Supply-chain volatility for non-GMO soy & red-clover crops | -0.50% | Global sourcing regions | Short term (≤ 2 years) |

| Stricter EFSA/FDA health-claims regulation | -0.30% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Scientific Controversy & Inconsistent Clinical Outcomes

Heterogeneous trial designs and varied bioactive content across commercial supplements have produced conflicting efficacy data.[3]Anja Jacobs, “Efficacy of isoflavones in relieving vasomotor menopausal symptoms,” Wiley Online Library, wiley.com Such inconsistencies inhibit blanket endorsements by medical associations and deter risk-averse consumers. Variability originates from differences in extraction technology, raw-material provenance, and standardization practices, underscoring the need for rigorous quality systems. Brands investing in Good Manufacturing Practices and double-blind trials are positioned to turn this restraint into a competitive moat.

Hormone-Sensitive Cancer Risk Concerns

Residual anxiety about estrogen receptor-positive cancers continues to cloud high-dose isoflavone supplementation, even though epidemiological studies suggest a neutral or protective effect at dietary levels. The Norwegian Scientific Committee for Food Safety cites modest hormonal shifts in pre-menopausal women, prompting conservative dosage recommendations. Clear labeling, post-market surveillance, and physician-led education will be essential to assuage apprehension among oncologists and breast-cancer survivors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Soy Dominance Faces Botanical Diversification

Soy isolates retained a commanding 65.2% share of the phytoestrogen supplements market in 2024, owing to robust agronomic supply chains and an unparalleled clinical evidence base. Red clover, however, is accelerating at 9.9% CAGR because consumers view botanical diversity as a hedge against allergenicity and GMO exposure. Flaxseed lignans and hop-derived prenylflavonoids are carving niches in cardiovascular and sleep wellness, respectively. Supply-chain sustainability considerations are catalyzing investments in regenerative cultivation, climate-resilient seed stock, and fair-trade certification, ensuring long-term availability of multiple botanical inputs.

Soy’s entrenched position is reflected in decades of epidemiological data linking high-isoflavone diets to lower incidences of vasomotor complaints among Asian women. Yet red-clover extracts enriched with biochanin A and formononetin demonstrate superior LDL-cholesterol reduction in male subjects, signaling potential gender-specific positioning. Brands are, therefore, balancing portfolio depth with raw-material flexibility to weather climate-induced crop fluctuations and evolving consumer tastes.

By Form: Capsules Lead While Gummies Drive Innovation

Capsules claimed 45.8% of the phytoestrogen supplements market share in 2024, buoyed by physician preference for standardized dosing. Gummies, expanding at 11.7% CAGR, are transforming category aesthetics by addressing pill fatigue and enhancing compliance. Tablets retain relevance due to cost-efficiency, whereas powders cater to sports-nutrition users keen on stackable formulations.

Capsule leadership rests on bioavailability controls such as sustained-release beadlets and phytosome complexes. Gummy manufacturers, meanwhile, invest in pectin-based matrices to align with vegan norms and use natural sweeteners to keep sugar loads low. Liquid tinctures have small yet loyal followings among holistic practitioners who value sublingual delivery for rapid absorption. Technology advances that shorten dissolution times or mask isoflavone bitterness will remain critical for format differentiation.

By Application: Menopause Focus Expands Into Bone Health

Menopause care occupied 54.3% of 2024 revenues, substantiated by clinical guidelines that endorse soy isoflavones for hot-flash management. Bone health, on a 10.1% CAGR arc, is gaining traction after FDA recognition of genistein-rich medical foods for osteopenia, signaling regulatory acceptance of phytoestrogens as skeletal support agents. Cardiovascular benefits associated with red-clover-based products are broadening the addressable population, especially among men seeking natural lipid management. Skin-health and fertility-adjunct sub-segments are in nascent stages but expected to firm up as dose-response relationships become clearer.

Cross-functional formulations are emerging, embedding phytoestrogens with vitamin D3, K2-MK7, or omega-3s to satisfy consumer interest in multi-benefit products. Such combinations reduce pill burden, but scientific validation must confirm that ingredient synergies deliver additive rather than redundant effects.

By Distribution Channel: Pharmacy Strength Meets Digital Disruption

Pharmacies and drugstores held 37.9% of 2024 sales, but online platforms clocked the fastest growth at 14.5% CAGR. Pharmacist endorsement preserves brick-and-mortar relevance, especially in markets where menopause discussions still carry stigma and professional guidance is valued. Supermarkets serve price-sensitive shoppers, while specialty health-food outlets differentiate via curated assortments of certified-organic botanicals.

Digital channels leverage AI-powered symptom quizzes and remote nutritionists to raise conversion rates. The COVID-19 pandemic normalized subscription replenishment, shifting customer expectations toward auto-ship convenience. Brands must, therefore, orchestrate omnichannel inventories to prevent stock-outs that could trigger brand switching.

Geography Analysis

North America led with a 34.7% share in 2024, thanks to clear dietary supplement regulations and Medicare Advantage pathways that sometimes cover medical foods targeting vasomotor relief. The United States dominates consumption, but Canada’s science-driven Natural Health Products Directorate fosters cross-border formulation harmonization. Mexico is a rising contributor, bolstered by expanding middle-class health spending.

Europe’s trajectory remains firmly growth-oriented, underpinned by stronger preventive-health cultures in Germany, Italy, and Spain. EFSA’s evolving claims framework demands extensive dossiers but rewards compliant firms with EU-wide market access. The United Kingdom, while diverging post-Brexit, is nurturing innovation hubs focused on mental-wellbeing adjacencies, providing a foothold for adaptogenic-phytoestrogen hybrids.

Asia Pacific will post the quickest 7.80% CAGR as its nutraceutical sector heads toward massive growth as China is spearheading demand by promoting functional foods for healthy aging, while Japan’s FOSHU regime, valued near USD 500 billion, remains the gold standard for functional-claim rigor. India adds momentum through Ayurvedic endorsements of plant compounds, merging traditional wisdom with modern dosage forms. Regulatory heterogeneity, however, necessitates market-entry flexibility, from country-specific labeling to joint ventures that accommodate local distribution norms.

Competitive Landscape

The phytoestrogen supplements industry shows moderate concentration. Multinationals such as Solgar (Nestlé Health Science) and GNC Holdings deploy internal extraction units and global clinical networks to accelerate the dossier generation. Vertical integration—from non-GMO seed contracts to proprietary CO₂ extraction—helps secure consistent isoflavone profiles and reduces exposure to commodity price swings. Merger-and-acquisition activity is accelerating, illustrated by Barentz’s 2025 purchase of China’s Fengli Group to cement APAC sourcing depth.

Strategic themes include multi-ingredient product launches that combine isoflavones with calcium or magnesium to win shelf space in bone-health aisles. Personalized-nutrition startups are using genotyping to determine equol-producer status, tailoring dose levels accordingly.

Meanwhile, established players are boosting digital marketing budgets to defend their share against nimble direct-to-consumer challengers. Intellectual-property filings concentrate on microencapsulation and liposomal-delivery patents designed to enhance bioavailability.

Phytoestrogen Supplements Industry Leaders

NOW Foods

Nature’s Way

Solgar

Swanson Health

Blackmores

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Barentz completed the acquisition of China's Fengli Group to enhance its presence in the Chinese nutraceuticals market. Leveraging local supplier networks and technical capabilities, Barentz will expand APAC operations in the regional market.

- July 2025: The National Institutes of Health launched the ACE Trial, which investigated the effects of equol supplementation on arterial stiffness and cognitive decline. Four hundred participants aged 65-85 received daily 10 mg doses over 24 months to clarify the phytoestrogen metabolite's therapeutic potential.

- March 2024: The FDA approved qualified health claims for cocoa flavanols, indicating cardiovascular disease risk reduction with at least 200 mg per serving. This establishes precedent for flavonoid-based health claims that may benefit phytoestrogen regulatory pathways.

Global Phytoestrogen Supplements Market Report Scope

| Soy Isoflavones |

| Flaxseed Lignans |

| Red Clover Isoflavones |

| Hops & Kudzu Extracts |

| Other Botanical Sources |

| Tablets |

| Capsules |

| Powder |

| Liquid & Tinctures |

| Gummies & Chewables |

| Menopause & Hormonal Health |

| Bone & Joint Health |

| Cardiovascular Health |

| Skin & Hair Health |

| Others |

| Pharmacies & Drug Stores |

| Supermarkets & Hypermarkets |

| Online Retail |

| Specialty Stores |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Source | Soy Isoflavones | |

| Flaxseed Lignans | ||

| Red Clover Isoflavones | ||

| Hops & Kudzu Extracts | ||

| Other Botanical Sources | ||

| By Form | Tablets | |

| Capsules | ||

| Powder | ||

| Liquid & Tinctures | ||

| Gummies & Chewables | ||

| By Application | Menopause & Hormonal Health | |

| Bone & Joint Health | ||

| Cardiovascular Health | ||

| Skin & Hair Health | ||

| Others | ||

| By Distribution Channel | Pharmacies & Drug Stores | |

| Supermarkets & Hypermarkets | ||

| Online Retail | ||

| Specialty Stores | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the phytoestrogen supplements market in 2025?

It is valued at USD 4.53 billion and projected to climb to USD 5.78 billion by 2030, reflecting a 6.30% CAGR.

Which region currently leads sales of phytoestrogen supplements?

North America holds the top position with 34.7% revenue share, supported by clear regulations and high healthcare access.

Which botanical source dominates commercial formulations?

Soy-derived isoflavones account for 65.2% of 2024 revenues, thanks to established supply chains and the broadest clinical record.

What is the fastest-growing application area?

Bone and joint health is forecast to rise at a 10.1% CAGR as evidence mounts for genisteins positive impact on bone mineral density.

How are online channels influencing market growth?

E-commerce is expanding at a 14.5% CAGR, enabling direct-to-consumer brands to offer personalized regimens and subscription models.

What are the main safety concerns?

Some clinicians remain cautious about hormone-sensitive cancers, but current EFSA reviews indicate no elevated breast-cancer risk at recommended doses.

Page last updated on: