Liposuction Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.17 Billion |

| Market Size (2031) | USD 5.44 Billion |

| Growth Rate (2026 - 2031) | 11.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liposuction Devices Market Analysis by Mordor Intelligence

The Liposuction Devices Market size is projected to expand from USD 2.88 billion in 2025 and USD 3.17 billion in 2026 to USD 5.44 billion by 2031, registering a CAGR of 11.39% between 2026 to 2031.

Uptake is buoyed by 349,728 U.S. procedures in 2024 and 2.09 million worldwide, even as global totals shifted toward high-definition sculpting that favors energy-assisted platforms[1]American Society of Plastic Surgeons, “2024 Plastic Surgery Statistics Report,” ASPS.ORG. North America retained procedural leadership through expanded ASC reimbursement, while Asia-Pacific accelerated on medical tourism inflows and a swelling middle class. Portable, capital-efficient systems expanded the addressable sites, particularly office-based clinics, which now pair precision fat harvest with adjunct skin-tightening. Device makers are converging suction, ultrasound, laser, and plasma into single consoles to capture per-procedure economics and defend against non-invasive alternatives.

Key Report Takeaways

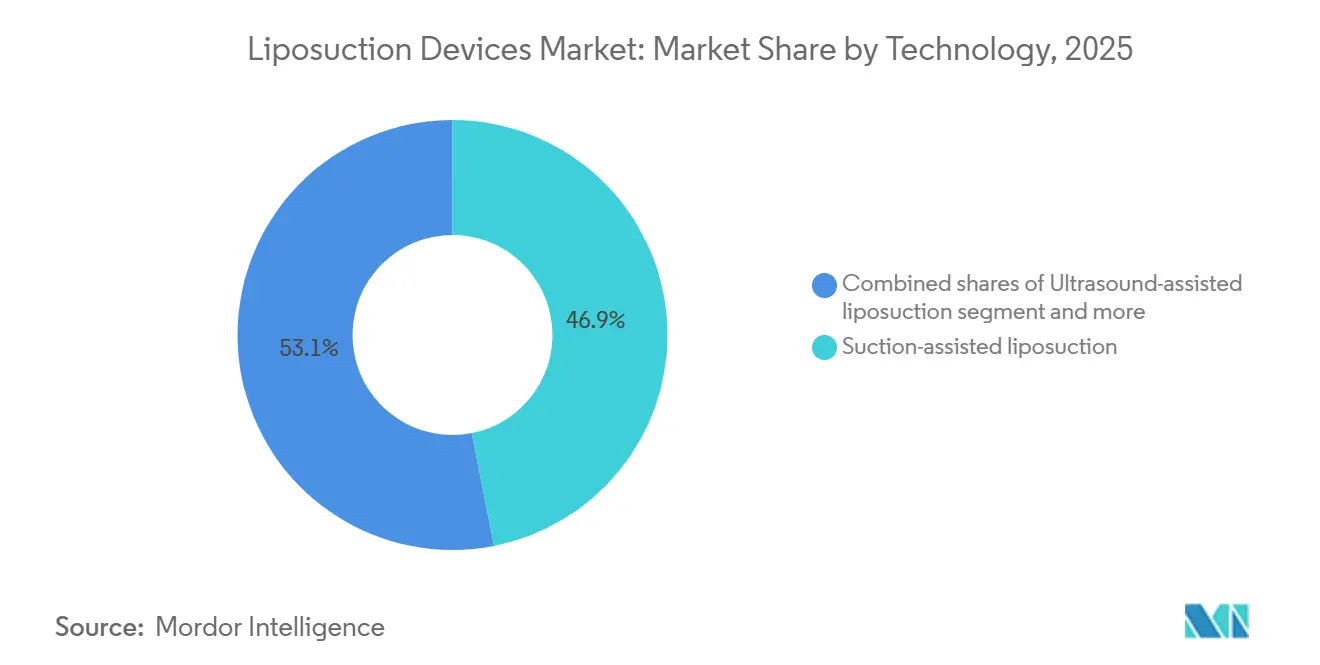

- By technology, suction-assisted systems led with 46.9% of 2025 revenue; laser-assisted platforms are projected to advance at a 12.1% CAGR to 2031.

- By product type, portable units accounted for 57.27% of 2025 sales, while the same form factor is forecast to expand at an 11.9% CAGR through 2031.

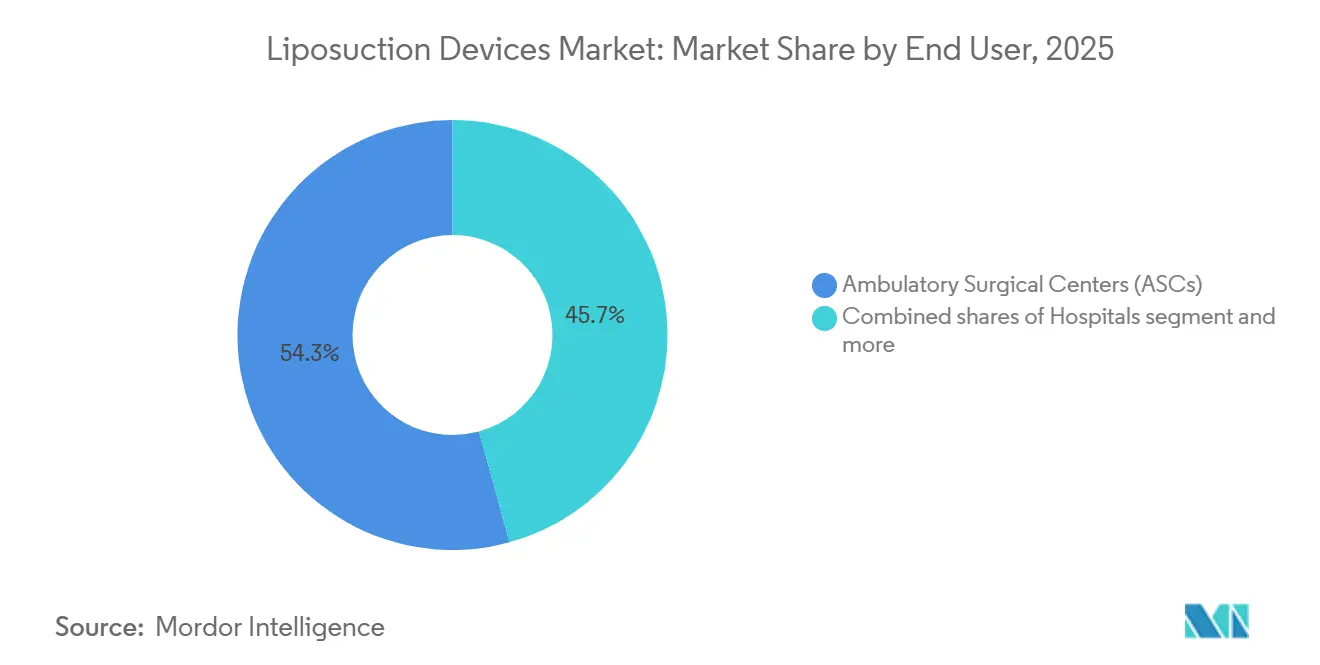

- By end user, ambulatory surgical centers held 54.27% of 2025 receipts; cosmetic surgery clinics are poised for the fastest 11.7% CAGR over the outlook period.

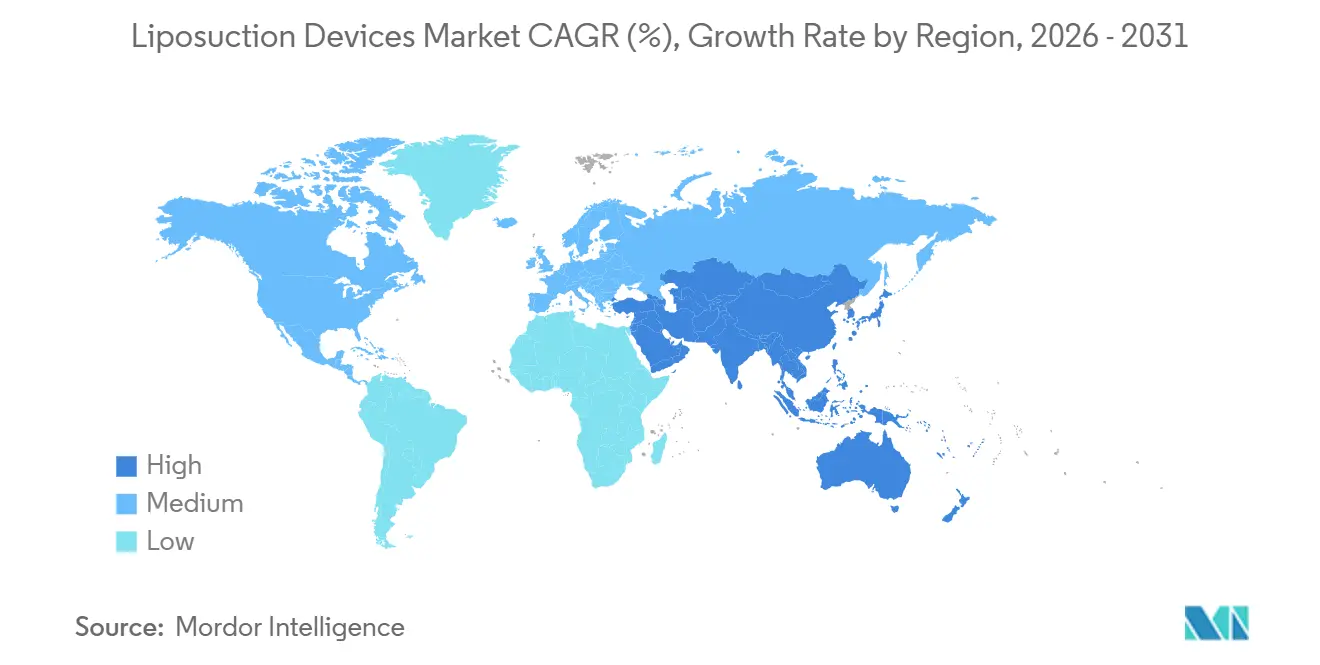

- By geography, North America accounted for 52.86% of the 2025 value, whereas Asia-Pacific is projected to grow at a 12.0% CAGR and emerge as the primary growth engine.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Liposuction Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Liposuction volumes at record highs; shift to high-definition contouring | +2.3% | Global, with North America and Asia-Pacific leading | Medium term (2–4 years) |

| Rapid adoption of energy-assisted modalities (UAL, PAL, LAL; integrated platforms) | +2.1% | North America, Europe, select APAC markets | Short term (≤2 years) |

| Migration to outpatient settings enabled by tumescent anesthesia and safety data | +1.8% | North America, Europe | Medium term (2–4 years) |

| APAC demand acceleration via medical tourism and rising middle-class incomes | +1.6% | Asia-Pacific core, spillover to Middle East | Long term (≥4 years) |

| Fat grafting use-cases drive demand for gentler harvest systems and closed-loop processing | +1.4% | Global, concentrated in North America and Latin America | Medium term (2–4 years) |

| Post-lipo skin tightening becoming standard of care (RF/helium plasma adjuncts) | +1.2% | North America, Europe, affluent APAC cities | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Liposuction Volumes at Record Highs; Shift to High-Definition Contouring

Aggregate procedures reached historic highs in developed regions, yet underlying demand now centers on athletic etching rather than bulk extraction. High-definition sculpting depends on ultrasound and laser devices that selectively emulsify fibrous zones. The “skinny BBL” exemplifies low-volume, shape-focused grafting among patients with body mass indices below 23. Precision harvest elevates the role of closed-loop cannulae and real-time imaging, motivating manufacturers toward integrated, small-footprint consoles. Global procedure divergence—expansion in the United States versus softness in some emerging economies—illustrates how currency swings and shifts in discretionary spending alter the regional mix without suppressing overall demand.

Rapid Adoption of Energy-Assisted Modalities

Ultrasound-, power-, and laser-assisted systems shorten operating time and reduce surgeon fatigue; MicroAire’s PAL platform extracted significantly more volume per minute than manual suction in company trials. Laser devices add thermal coagulation, reducing bruising and stimulating collagen renewal, enabling combined liposuction and tightening in a single session. Apyx Medical’s AYON, cleared in May 2025, channels helium plasma for controlled subsurface coagulation and is already pursuing a power-assisted indication. Bundling multiple energy sources into a single console reduces practice capital outlay and simplifies staff training, spurring rapid replacement of legacy suction-only machines in premium markets.

Migration to Outpatient Settings Enabled by Tumescent Anesthesia

Dilute lidocaine-epinephrine solutions have shifted most fat-removal cases from hospitals to ambulatory centers and private clinics. CMS placed several body-contouring codes on the ASC-payable list in 2024, dismantling a payer barrier and legitimizing same-day procedures [2]Centers for Medicare & Medicaid Services, “ASC Covered Procedures List Updates 2024,” CMS.GOV. Portable platforms that fit standard exam rooms captured 57.27% of 2025 device sales, mirroring venue migration. A systematic FDA MAUDE review reported an adverse-event rate of 0.04% for tumescent-based liposuction, further reassuring payers and patients. Privacy, convenience, and lower facility fees reinforce consumer preference for outpatient workflows.

APAC Demand Acceleration via Medical Tourism and Rising Middle-Class Incomes

Thailand hosted 1.2 million inbound medical travelers in 2024, with body contouring a marquee draw. Seoul’s Gangnam district delivered roughly 980,000 aesthetic procedures, cementing South Korea’s status as a regional hub. China’s urban middle class topped 400 million in 2024, raising elective-procedure rising among women aged 25 – 40. Device makers are localizing supply chains: Solta Medical acquired its Chinese distributor in December 2025 to tighten access to Thermage-FLX. Exchange-rate advantages and bundled tourism packages will keep Asia-Pacific the fastest-expanding liposuction devices market through 2031.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Non-invasive body contouring alternatives divert spend from surgical lipo | -1.7% | Global, concentrated in North America and Europe | Medium term (2–4 years) |

| Regulatory and safety communications temper energy-device adoption and claims | -1.1% | North America, Europe, select APAC markets | Short term (≤2 years) |

| Procedure risks and medico-legal scrutiny, especially in combined surgeries | -1.0% | Global, with heightened impact in North America and Europe | Medium term (2–4 years) |

| Ad restrictions for cosmetic interventions to under-18s curb DTC funnels | -0.9% | United Kingdom, Australia, expanding to EU and select APAC markets | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Non-Invasive Body-Contouring Alternatives Divert Spend from Surgical Lipo

Cryolipolysis, HIFU, and injectable lipolytics satisfy a risk-averse cohort that values zero downtime. AbbVie’s CoolSculpting delivers an 8.6% reduction in fat layer in 12 weeks with no anesthesia, siphoning patients who might otherwise book suction procedures. Medical-spa rollout is easier than surgical-suite investment, but it fragments discretionary dollars and tapers device utilization rates in some urban markets.

Regulatory and Safety Communications Temper Energy-Device Adoption

In October 2025 the FDA flagged burns and scarring tied to radiofrequency microneedling, reinforcing earlier warnings on helium-plasma claims [3]U.S. Food and Drug Administration, “Safety Communication on RF Microneedling Devices,” FDA.GOV. The United Kingdom and Australia tightened advertising rules, banning cosmetic-surgery pitches to minors and forbidding before-and-after imagery. Hospitals responded with stricter credentialing, slowing uptake among newer practitioners and favoring incumbents with robust training pipelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Suction-Assisted Systems Retain Core Volume

Suction-assisted devices accounted for 46.9% of 2025 revenue and are projected to post a 12.1% CAGR, anchoring the liposuction devices market size leadership. The technique’s simplicity, low capital entry, and surgeon familiarity support its share, even as ultrasound, power, and laser systems pitch precision benefits.

Energy-assisted platforms are penetrating high-definition and fibrous-tissue cases in North America and Western Europe. Laser and plasma variants bundle coagulation and tightening, thereby enhancing the procedure's value. Yet hospitals and price-sensitive clinics still default to cost-efficient suction-only consoles, slowing modal shift and keeping the liposuction devices market share of traditional systems resilient.

By Product Type: Portable Units Outpace Stand-Alone Consoles

Portable systems captured 57.27% of the 2025 value, yet are expected to grow at a CAGR of 11.86% by 2031, underscoring how outpatient migration shapes purchasing preferences in the liposuction devices market. Plug-and-play form factors slide into standard exam rooms, reducing infrastructure overhead and enabling multi-room rotation.

Stand-alone towers remain favored for extended combination surgeries that demand higher flow rates, but their footprint and cost deter office practices. Vendors now embed ultrasound guidance and closed-loop fat filtration inside carry-on chassis, narrowing performance gaps and propelling portable dominance through 2031.

By End User: ASCs Dominate, Cosmetic Clinics Surge

Ambulatory surgical centers garnered 54.27% of 2025 receipts, reflecting payer alignment and surgical safety accreditation that reassure consumers. Their purchasing scale influences vendor roadmaps toward compact, versatile devices that accelerate room turnover. Cosmetic clinics are forecast to log the fastest 11.7% CAGR as tumescent protocols and smaller-volume “skinny BBL” procedures fit office workflows. Financing plans and consumable bundles facilitate adoption among solo surgeons, thereby expanding liposuction device market share in non-hospital settings.

Geography Analysis

North America generated 52.86% of 2025 revenue, powered by 349,728 U.S. procedures and CMS reimbursement clarity that favors ASC-based operations. Canada supplies complementary demand, while Mexico attracts cross-border patients seeking cost relief. Non-invasive competition is strongest here, yet energy-assisted innovators remain headquartered in the region, sustaining premium device sales.

Europe delivered steadily, if slower, uptake, constrained by advertising curbs that dampen youthful interest and macroeconomic caution in major economies. Germany’s 80,519-procedure base anchors continental volumes, with the United Kingdom, France, and Italy rounding out the top tier. Stricter marketing codes are nudging clinics to emphasize safety credentials over glamor, influencing modal mix toward ultrasound and RF systems with published evidence.

Asia-Pacific is on track for a 12.0% CAGR, driven by surgical tourism corridors in Thailand and South Korea, and by a swelling urban middle class across China and Indonesia. China’s regulatory streamlining prompted Solta’s 2025 distributor acquisition, underscoring long-run commitment. India, fourth worldwide in 2023 cases, benefits from English-language care and cost arbitrage, placing the region at the vanguard of future growth in the liposuction devices market.

Competitive Landscape

Installed-base economics confer moderate concentration. InMode’s 30,900 global platforms generated USD 370.5 million in revenue in 2025, despite a dip amid macro headwinds. Recurring blade and handpiece sales muted console volatility and kept gross margins near 83%.

Apyx Medical gained FDA clearance for AYON in May 2025 and filed for power-assisted expansion five months later, signposting a convergence of suction and plasma energies into a single chassis. MicroAire leverages clinical data that show 49% lower surgeon fatigue to defend its PAL share in orthopedic-heavy practices, while Cynosure and Alma Lasers court dermatology networks with hybrid RF-laser offerings.

Strategic activity skews toward geography: Solta’s China buy-out accelerated Thermage penetration, and Crown Laboratories’ 2025 purchase of Revance aligned injectables with energy devices to cross-sell across 50 countries. Rising regulatory scrutiny favors firms with robust compliance resources, nudging niche water-jet start-ups toward partnerships or exits as integrated leaders grab wallet share.

Liposuction Devices Industry Leaders

InMode

Apyx Medical

MicroAire Surgical Instruments

Cynosure

Alma Lasers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: New 2026 protocols use AI-guided mapping from pre-operative 3D scans. These algorithms predict the ideal fat volume for removal to ensure symmetrical and natural results while minimizing human error.

- November 2025: Apyx Medical submitted a 510(k) seeking power-liposuction labeling for AYON .

- September 2025: Thermage FLX surpassed 5 million lifetime treatments, reinforcing RF skin-tightening adoption.

Global Liposuction Devices Market Report Scope

As per the scope of the report, liposuction devices are specialized medical equipment designed to remove subcutaneous fat via suction-assisted lipectomy. The fundamental components of a modern liposuction system include a high-powered suction pump or aspirator that generates negative pressure, flexible medical-grade tubing, and a cannula, which is a thin, hollow stainless-steel tube inserted through small skin incisions to dislodge and extract fat cells.

The liposuction devices market is segmented by technology, product type, end users, and geography. By technology, the market is segmented into suction-assisted liposuction, ultrasound-assisted liposuction, power-assisted liposuction, laser-assisted liposuction, water-jet-assisted liposuction, and RF-assisted lipocoagulation. By product type, the market is segmented into portable systems and stand-alone systems. By end users, the market is segmented into hospitals, ambulatory surgical centers, and cosmetic surgery clinics.

Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Suction-assisted liposuction |

| Ultrasound-assisted liposuction |

| Power-assisted liposuction |

| Laser-assisted liposuction |

| Water-jet assisted liposuction |

| RF-assisted lipo-coagulation |

| Portable Systems |

| Stand-alone Systems |

| Hospitals |

| Ambulatory Surgical Centers (ASCs) |

| Cosmetic Surgery Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Suction-assisted liposuction | |

| Ultrasound-assisted liposuction | ||

| Power-assisted liposuction | ||

| Laser-assisted liposuction | ||

| Water-jet assisted liposuction | ||

| RF-assisted lipo-coagulation | ||

| By Product Type | Portable Systems | |

| Stand-alone Systems | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers (ASCs) | ||

| Cosmetic Surgery Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the liposuction devices market be by 2031?

It is forecast to reach USD 5.44 billion by 2031, expanding at an 11.39% CAGR from 2026-2031.

Which technology currently holds the largest liposuction devices market share?

Suction-assisted systems led with 46.9% of 2025 revenue.

Why are portable systems growing faster than stand-alone consoles?

Outpatient migration favors compact units that fit ASC and clinic rooms, pushing portable sales to an 11.9% CAGR.

What drives Asia-Pacific’s rapid growth?

Medical-tourism hubs, rising middle-class incomes and streamlined device approvals support an expected 12.0% CAGR.

Page last updated on: