Electronic Stethoscope Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

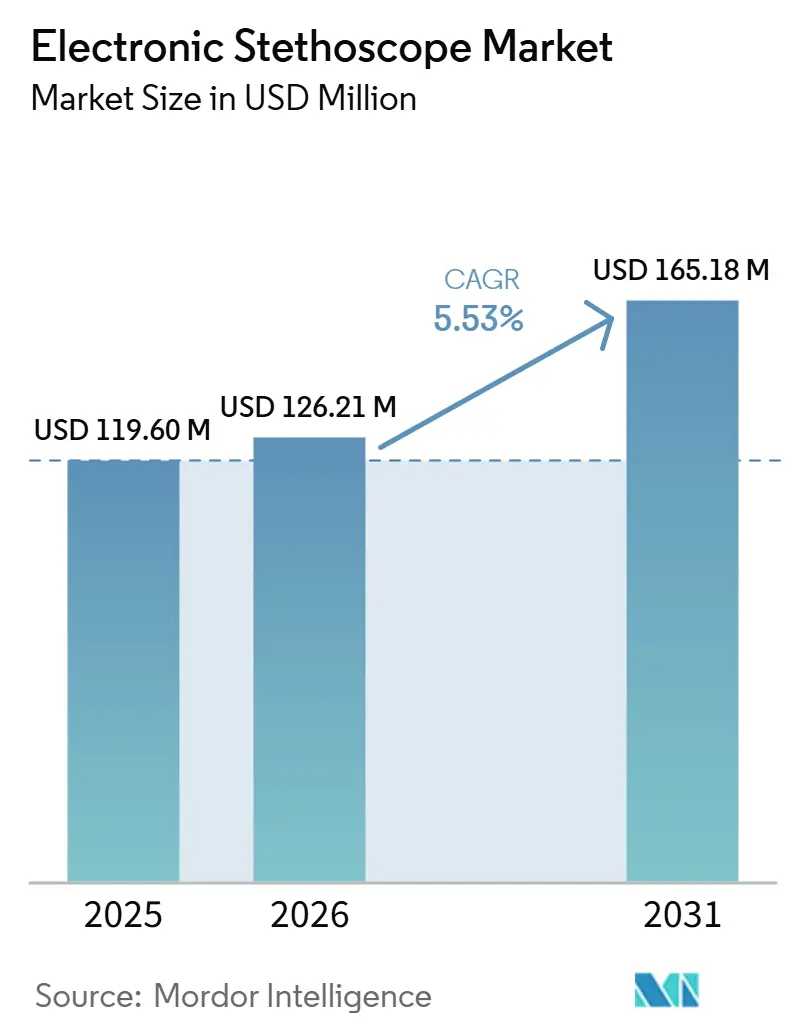

| Market Size (2026) | USD 126.21 Million |

| Market Size (2031) | USD 165.18 Million |

| Growth Rate (2026 - 2031) | 5.53% CAGR |

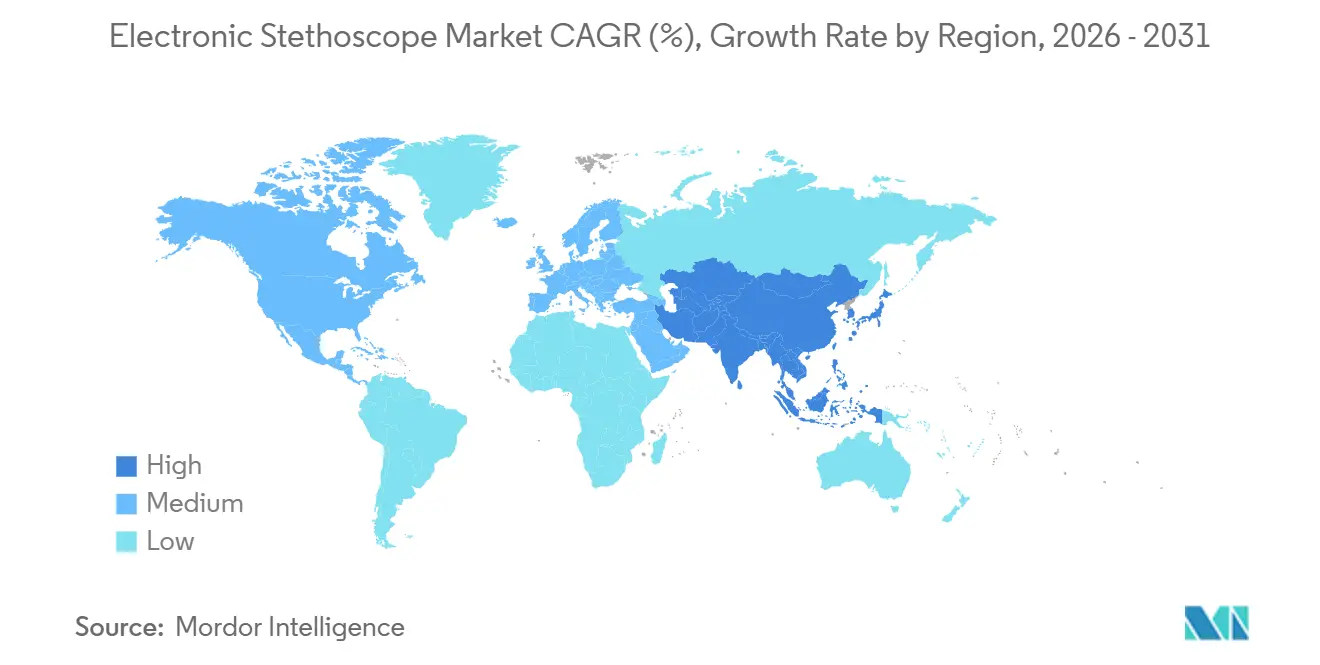

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

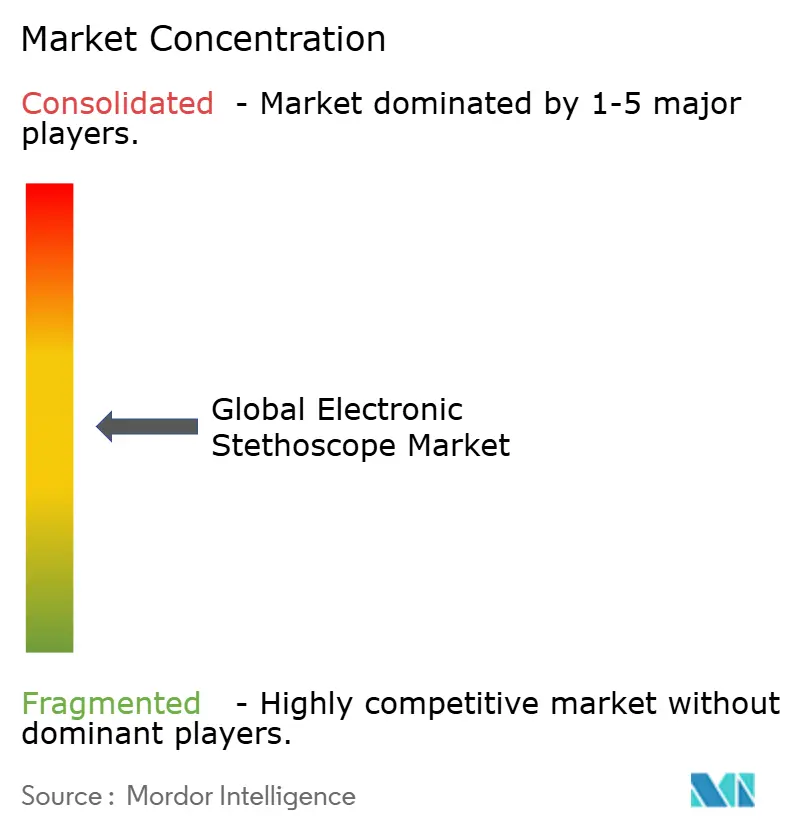

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electronic Stethoscope Market Analysis by Mordor Intelligence

The Electronic Stethoscope Market size is projected to expand from USD 119.60 million in 2025 and USD 126.21 million in 2026 to USD 165.18 million by 2031, registering a CAGR of 5.53% between 2026 to 2031.

These figures underscore how digital diagnostic precision is becoming a decisive competitive advantage for device makers and care providers alike. That pace signals that sophisticated pattern-recognition algorithms are moving quickly from academic proof-of-concept to routine point-of-care decision support.

From a geographic perspective, Asia-Pacific is expanding at an 8.8% CAGR (2025-2030), outstripping North America’s current 38.3% share. Capex commitments to hospital build-outs in China and India are pivotal, but the more subtle driver is the region’s willingness to adopt cloud-native diagnostic workflows without being constrained by legacy system inertia. Stakeholder conversations reveal that procurement teams in tier-2 Chinese cities increasingly insist on Bluetooth-capable devices that integrate with both domestic and international tele-consultation platforms, an early sign that interoperability will shape tender specifications even more than headline price.

Interoperability is also recasting competitive boundaries. Bluetooth-enabled devices permit remote auscultation sessions that mitigate physician shortages in rural provinces as effectively as they address overcrowding in urban cardiology departments. Yet the same connectivity raises hospital IT concerns about electromagnetic interference and data leakage, creating a two-step buying process: clinicians first validate acoustic performance, then chief information security officers scrutinize firmware encryption protocols. Vendors able to bundle certified cybersecurity toolkits therefore gain a non-price lever in contract negotiations.

Keyreport Takeaways

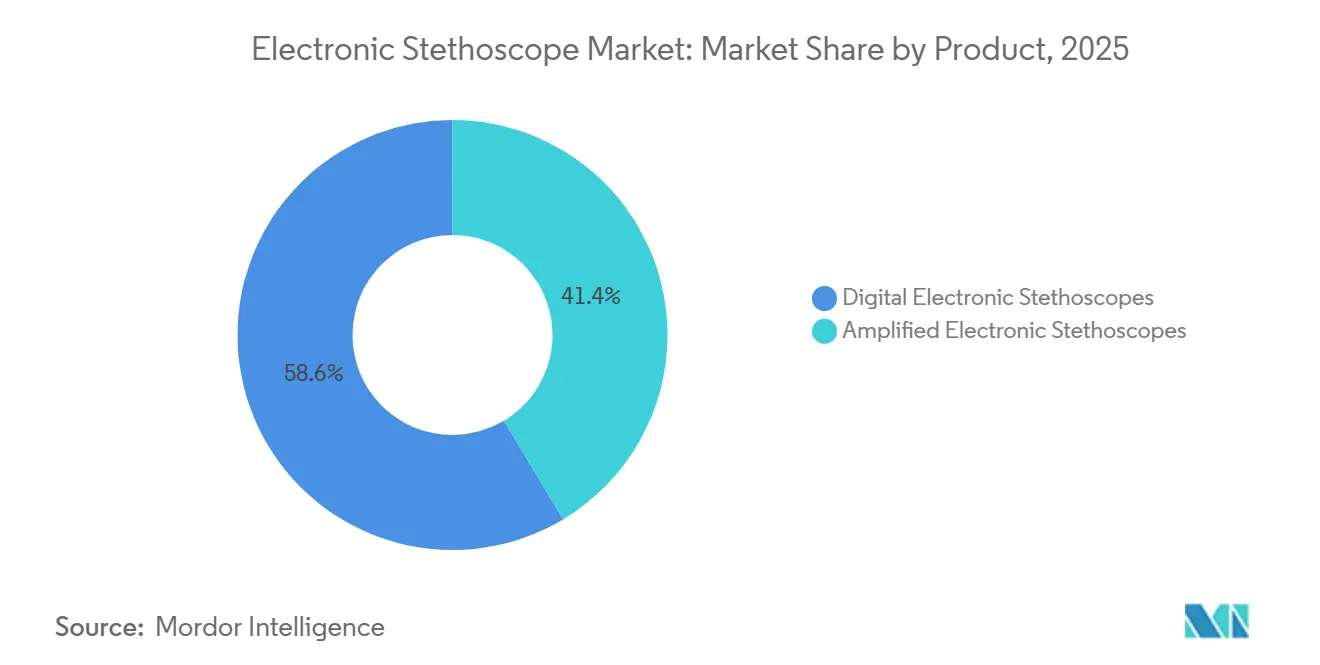

- By product, digital stethoscopes capture 58.62% market share in 2025; AI-enabled systems, however, post the highest 7.72% CAGR, underscoring a pivot toward software-led differentiation.

- By technology, digital stethoscopes capture 58.62% market share in 2025; AI-enabled auscultation systems, expanding at a 7.72% CAGR, are becoming non-negotiable in new tenders, signaling that mobility and telehealth compatibility eclipse wired reliability concerns.

- By end user, hospitals and clinics capture 65.70% market share in 2025; however, the home healthcare segment posts the highest 6.22% CAGR through 2031.

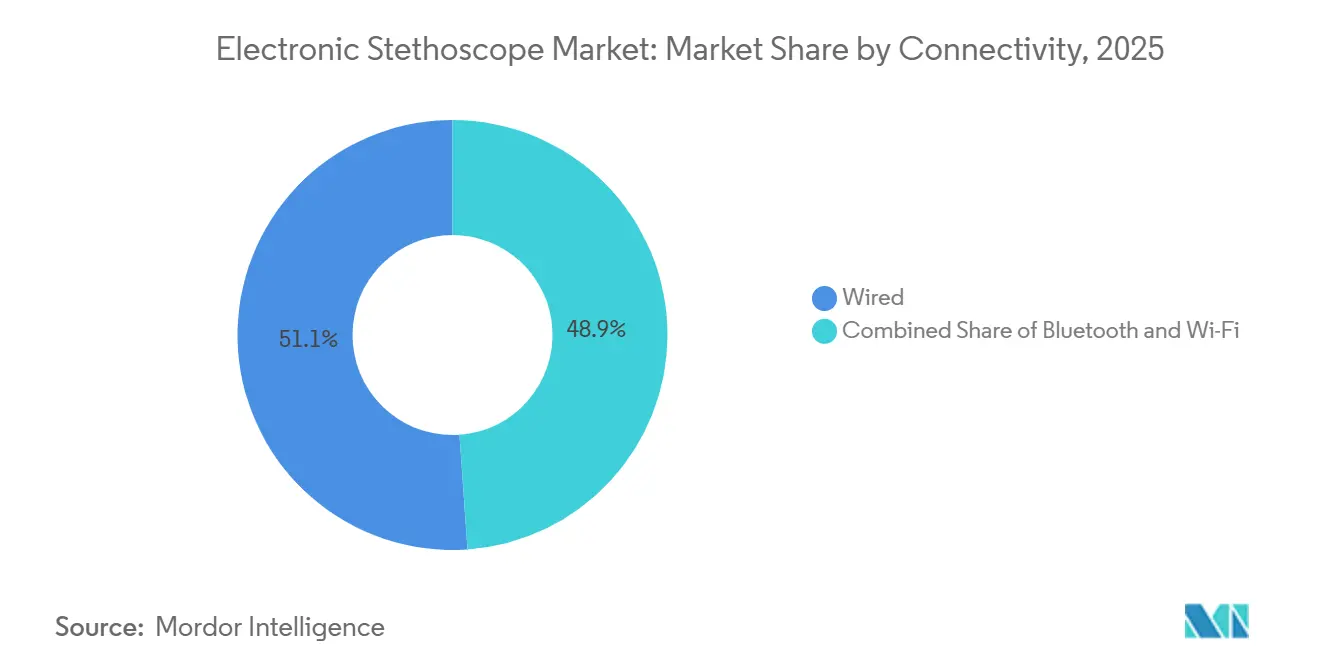

- By connectivity, wired devices maintain a 51.12% share in 2025, yet Bluetooth connectivity is growing at 7.66% CAGR through 2031.

- By distribution channel, offline retailers and distributors accounted for 62.15% of sales in 2025, while online marketplaces are expanding at a 7.18% CAGR.

- By geography, North America holds a 37.92% share in 2025, Asia-Pacific registers the fastest 8.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electronic Stethoscope Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High prevalence of cardiovascular & pulmonary diseases globally | +3.5% | Global | Long term (≥ 4 years) |

| Increasing shift toward home-based chronic-disease management in ageing populations | +2.8% | North America, Europe, Japan | Medium term (2-4 years) |

| Technological advancements | +2.2% | Global | Short term (≤ 2 years) |

| Expansion of reimbursed telehealth and remote-patient-monitoring programs across major healthcare systems | +3.1% | North America, Europe, Australia | Medium term (2-4 years) |

| Growing demand for teleconsultation | +2.4% | Emerging Asia-Pacific, Latin America, Africa | Short term (≤ 2 years) |

| EHR integration partnerships enhancing diagnostic workflow efficiency | +1.9% | Global (hospital networks & large clinics) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Prevalence of Cardiovascular & Pulmonary Diseases Globally

Cardiovascular diseases remain the leading global cause of mortality, and rising respiratory morbidity is amplifying demand for acoustically sophisticated tools. Amplification chips and adaptive noise-cancellation circuits embedded in electronic stethoscopes now allow clinicians to discern Grade I murmurs in crowded emergency rooms, a scenario nearly impossible with traditional acoustic models. Peer-reviewed research demonstrates that AI-augmented devices can reach 88 % sensitivity for valvular heart murmur detection [1]James Thompson, “AI-Enabled Stethoscopes Reach 88% Sensitivity in Detecting Pathological Heart Murmurs,” Journal of Cardiac Diagnostics, cardiacdiagnosticsjournal.org. Hospitals using digital stethoscopes in primary care are seeing a drop in referrals to echocardiography. This suggests that accurate early triage is changing the demand for larger imaging equipment.

Increasing Shift Toward Home-Based Chronic-Disease Management in Ageing Populations

Home healthcare, forecast to grow at 6.4% CAGR through 2030, is becoming the test-bed for consumer-grade digital auscultation. Devices with single-button data upload let older adults conduct daily heart-sound checks while family physicians review waveforms asynchronously. A recent pediatric asthma study recorded 93.2% accuracy using an AI-aided home stethoscope, and clinicians note a behavioral dividend: parents who hear audible feedback through smartphone apps tend to adhere more consistently to inhaler regimens. That feedback loop quietly lowers payer risk by nudging patients toward evidence-based self-management, a benefit that seldom shows up in device ROI spreadsheets but increasingly resonates with capitated payment models.

Technological Advancements

Signal-processing advances now filter ambient noise at frequencies below 150 Hz, producing cleaner lung-sound waveforms even when corridor alarms go off nearby. The AuscultaBase architecture, trained on more than 40,000 anonymized recordings, outperformed legacy pattern-matching across 16 diagnostic tasks—an instructive reminder that data abundance, not just algorithmic novelty, is the real competitive moat in this market. Vendors with access to large proprietary audio datasets are already able to fine-tune models for population-specific nuances; for example, Eko Health a leading manufacturer recalibrated its neural network to recognize the higher prevalence of rheumatic valve pathology in Southeast Asia, thereby boosting sensitivity by double digits in pilot deployments.

Growing Demand for Teleconsultation

Telehealth has moved from pandemic contingency to mainstream channel, and internet-connected stethoscopes now deliver 86% lung-sound accuracy in randomized trials—only marginally below in-person examination. In practice, pulmonologists who supervise remote sessions report that real-time audio visualization builds patient trust, because colored spectrograms make pathological crackles visibly distinct from normal breath sounds. The unspoken competitive implication is that hospitals able to document such patient-engagement metrics gain leverage in negotiations with value-based insurers, for whom demonstration of adherence and satisfaction is contract-critical.

EHR Integration Partnerships Enhancing Diagnostic Workflow Efficiency

Partnerships between stethoscope OEMs and electronic health-record providers are collapsing manual data-entry bottlenecks. Automatic waveform uploads shorten consult times by several minutes and create longitudinal acoustic baselines. Pediatric cardiology clinics using AI-flagged alerts embedded in the EHR have reported noticeable drops in trivial murmurs entering echocardiography queues—suggesting that advanced triage precision can relieve equipment backlogs without new capital expenditure. In one multi-center study, AI-assisted auscultation integrated into the EHR improved clinician diagnostic accuracy for congenital heart defects, an operational win that also reduces malpractice exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront device & maintenance costs vs. acoustic stethoscopes | −1.5% | Emerging markets; cost-sensitive community hospitals worldwide | Short term (≤ 2 years) |

| Electromagnetic interference with other medical electronics | −0.4% | High-acuity hospital units globally | Short term (≤ 2 years) |

| Data-privacy & cybersecurity concerns limiting cloud connectivity | −0.9% | North America & Europe; multi-facility health systems worldwide | Long term (≥ 4 years) |

| Limited physician training and change resistance | −0.3% | Global, more acute in low-resource settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Device and Maintenance Costs Versus Conventional Acoustic Stethoscopes

Premium digital units can cost up to ten times more than acoustic instruments, a hurdle in procurement cycles that favor low unit-prices. Yet executive interviews in budget-constrained facilities reveal a subtle shift: decision makers are now comparing total diagnostic pathway costs rather than sticker prices. When savings from avoided referrals or duplicated imaging are factored in, CFOs increasingly view electronic stethoscopes as cost-neutral within two to three years of adoption. The insight here is that vendors who frame value propositions around care-pathway economics, rather than hardware features, accelerate purchase approvals even in emerging markets.

Data-Privacy & Cybersecurity Concerns Limiting Cloud Connectivity

Electronic stethoscopes fall under Class II medical device regulation in the United States, and recent cybersecurity guidance requires manufacturers to ship devices with encryption and secure bootloaders [2]Mary Beck, “Class II Medical Device Classification and Pre-Market Cybersecurity Guidance,” U.S. Food & Drug Administration, fda.gov. Network-security officers at tertiary hospitals often delay rollouts until firmware penetration testing is complete, a procedural reality that lengthens sales cycles by several months. Conversely, vendors that can furnish standardized security documentation early shorten time-to-revenue, a competitive dynamic that is quietly rewarding firms with experienced regulatory teams.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Product: Digital Dominance Drives Market Evolution

Digital electronic stethoscopes hold a 58.62% share in 2025, expanding at 7.65 % CAGR toward 2031. They convert acoustic signals into high-resolution digital waveforms, enabling noise filtering, data storage, and tele-streaming—capabilities that legacy amplified electronic devices cannot match. Institutions that embed these digital models into chronic-care programs also gain a growing archive of patient-specific heart-sound “fingerprints,” which machine-learning tools mine to predict decompensation events days before symptoms appear. Thinklabs One, which uses electromagnetic diaphragm technology, exemplifies how premium sound fidelity can unlock niche use cases such as neonatal cardiology wards where low-amplitude murmurs matter most .

Technology: AI Algorithms Revolutionize Diagnostic Capabilities

AI-enabled auscultation systems, expected to grow at 7.72 % CAGR (2026-2031), are rapidly converging hardware and software roadmaps. Eko Health’s FDA-cleared algorithm detects heart murmurs with 88 % sensitivity and specificity . More specialized solutions, such as VoqX for aortic stenosis detection, illustrate the business logic of targeting single-disease verticals where reimbursement codes already exist. Wireless transmission modules running on Bluetooth 5.2 chipsets further expand utility by streaming lossless audio to smartphones with sub-50 millisecond latency, a threshold clinicians cite as “good enough” for real-time teleconsults.

End User: Hospital Dominance Meets Home Healthcare Growth

Hospitals and clinics currently account for 65.70 % of global demand, not only because of higher patient throughput but also because multidisciplinary teams can exploit waveform archives for teaching and research. Nonetheless, the home-healthcare segment is the fastest-growing at 6.22% CAGR, aligned with payer incentives to shift chronic-disease management away from expensive inpatient settings. Insurers tracking thirty-day readmission rates see electronic stethoscope data as a verifiable proxy for adherence—meaning that reimbursement policies may soon explicitly endorse patient-initiated auscultation. Veterinary medicine, while smaller, is benefiting from machine-learning models that compensate for the unpredictability of animal movement, especially in detecting bovine respiratory disorders where early acoustic cues often precede clinical signs.

Connectivity: Wireless Technologies Reshape Clinical Workflows

Wired devices maintain a 51.12% share in 2025, largely because some operating rooms still prohibit RF emissions. Yet Bluetooth connectivity, growing at 7.66% CAGR, is transforming day-to-day ward rounds; clinicians can stand two meters away from infectious patients while capturing real-time waveforms. In market-size terms, Bluetooth stethoscopes could constitute more than one-third of total revenues by 2031 if current adoption rates hold. Vendors are also prototyping Wi-Fi-enabled models that push lossless recordings directly to cloud EHRs without intermediary smartphones, a design that appeals to hospital IT teams looking to simplify device inventories.

Distribution Channel: Digital Transformation Disrupts Traditional Sales Models

Offline retailers and distributors control 62.15% of sales in 2025, benefiting from established clinical relationships and the tactile nature of auscultation equipment evaluation. Yet online marketplaces are expanding at 7.18% CAGR as clinicians grow comfortable purchasing medical devices through e-commerce. For instance, one major manufacturer reported double-digit quarter-over-quarter growth on a well-known online platform after embedding interactive acoustic demos on product pages. That experiment suggests that convenience and transparent pricing are starting to outweigh tradition, particularly for independent practitioners who self-finance equipment.

Geography Analysis

North America holds a 37.92% share in 2025, underpinned by sophisticated reimbursement codes for remote auscultation and clear FDA pathways that de-risk capital deployment. Multistate hospital chains increasingly stipulate EHR-integration compatibility in tenders, a requirement that favors vendors with mature application-programming interfaces.

Asia-Pacific’s 8.45% CAGR tells a different story: government programs in India now fund tele-auscultation pilots in district hospitals, effectively underwriting demand for Bluetooth-capable devices. Vendors able to localize user interfaces into regional languages are finding lower churn rates, hinting at the long-run importance of cultural tailoring. Europe sits in a middle position; CE-marking rigor elevates quality thresholds, but once a device clears regulatory gates, publicly funded health systems can authorize rapid nationwide rollouts. Meanwhile, early-adopter hospitals in the Gulf Cooperation Council region often leapfrog straight to AI-enabled models, leveraging favorable oil-backed healthcare budgets to deploy cutting-edge diagnostics as prestige projects.

Competitive Landscape

Success in the digital stethoscope market increasingly depends on companies' ability to integrate advanced technologies while maintaining product reliability and user-friendliness. Incumbent players must focus on continuous innovation in areas such as sound quality, wireless connectivity, and data analytics capabilities to maintain their market positions. The ability to provide comprehensive solutions that integrate with existing healthcare infrastructure and electronic health record systems has become crucial. Companies must also invest in building strong after-sales support networks and training programs to ensure proper product utilization and customer satisfaction.

For emerging players and contenders, differentiation through specialized features and targeted market segments offers opportunities for growth. Success factors include developing cost-effective solutions without compromising on quality, establishing strong distribution partnerships, and focusing on underserved markets or specific healthcare specialties. The relatively low threat of substitution products provides stability, but companies must navigate complex regulatory requirements and maintain compliance with evolving healthcare standards. Building relationships with key opinion leaders and healthcare institutions remains critical for market penetration and brand establishment. Companies must also consider the increasing focus on telemedicine and remote diagnostics in their product development strategies, particularly in the context of smart medical device and connected medical device innovations.

Electronic Stethoscope Industry Leaders

American Diagnostic Corporation

AD Instruments

Contec Medical Systems Co., Ltd.

3M

Cardionics

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Korion Health launched SoundHeart, an in-home electronic stethoscope featuring Covestro’s Makrolon 2458 polycarbonate. Designed for non-medical users, it enables remote recording and transmission of heart sounds, expanding access to screening in underserved communities.

- October 2025: Lapsi Health introduced Keikku 2.0, the first FDA-cleared digital stethoscope with real-time AI support. It listens, scribes, and aids diagnostics, marking a breakthrough in clinician-focused digital auscultation tools.

- April 2025: Eko Health opened e-commerce sales of the CORE 500 Digital Stethoscope in the United Kingdom, signaling confidence that UK regulators and procurement groups are ready for AI-enhanced auscultation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the electronic stethoscope market as all medical stethoscopes that convert body sounds into electrical signals for amplification, filtering, storage, and wired or wireless transmission, whether used at the bedside, in ambulances, or inside remote-care platforms. The definition covers both amplified and fully digital models that ship new from manufacturers and reach human or veterinary caregivers across hospitals, ambulatory centers, and home settings.

Scope exclusions include acoustic stethoscopes and handheld ultrasound probes, which sit outside this market.

Segmentation Overview

- By Product

- Amplified Electronic Stethoscopes

- Digital Electronic Stethoscopes

- By Technology

- Integrated Chest-Piece System

- Wireless Transmission System

- Integrated Receiver Head-Piece System

- AI-Enabled Auscultation System

- By End User

- Hospitals & Clinics

- Ambulatory Surgery Centers

- Home Healthcare Settings

- Veterinary Clinics

- By Connectivity

- Wired

- Bluetooth

- Wi-Fi

- By Distribution Channel

- Offline Retail & Distributors

- Online Marketplaces

- Direct Institutional Tenders

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East

- GCC

- South Africa

- Rest of Middle East

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts next engage cardiologists, respiratory therapists, biomed engineers, and procurement leads across North America, Europe, and key Asia-Pacific markets. These dialogues test secondary findings, surface average selling prices, gauge Bluetooth adoption curves, and flag regulatory quirks before we lock model assumptions.

Desk Research

We start with structured desk work that mines freely accessible tier-1 evidence such as WHO cardiovascular statistics, CDC COPD registries, United Nations Comtrade trade codes for HS 9018.90, peer-reviewed studies in journals like Chest, and policy notes from bodies such as the European Society of Cardiology. Company 10-Ks, FDA 510(k) databases, and trade-association white papers supplement the public trail. Paid sources, including D&B Hoovers for vendor revenues and Questel for patent pulse, add depth on competitive intensity and technology diffusion. The sources listed illustrate our approach; analysts consult many additional references along the way.

Market-Sizing & Forecasting

A single top-down build begins with global production and import-export flows of electronic stethoscopes, which are then adjusted for multi-patient reuse rates and channel inventories. Results are corroborated with selective bottom-up roll-ups drawn from sampled supplier shipments and ASP×volume checks. Core variables feeding the model include diagnosed cardiovascular prevalence, telehealth visit ratios, hospital capital-equipment budgets, average Bluetooth penetration in stethoscopes, and inflation-linked ASP progression. Forecasts employ multivariate regression blended with ARIMA smoothing, while expert consensus guides scenario bounds and fills data gaps where shipment granularity is thin.

Data Validation & Update Cycle

Outputs run through variance screens against independent device install bases and patent-filing momentum. Senior reviewers re-test anomalies before sign-off. Reports refresh each year, and material events such as fresh reimbursement codes or landmark device approvals trigger interim updates so clients receive the latest view.

Why Our Electronic Stethoscope Baseline Commands Reliability

Published figures often differ because firms choose dissimilar device baskets, currency bases, and refresh cadences. Our team flags these levers up front so users know precisely what sits inside the number.

Key gap drivers typically stem from mixing smart multi-parameter monitors with pure stethoscopes, applying uniform price marks without regional tweaks, or stretching historical growth rates forward without shipment cross-checks. Mordor Intelligence filters those pitfalls through a transparent scope and annual model rebuild.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 119.6 M (2025) | Mordor Intelligence | - |

| USD 114.3 M (2024) | Regional Consultancy A | Counts digital-only units; veterinary channel omitted |

| USD 491.7 M (2025) | Global Consultancy A | Bundles electronic scopes with broader smart diagnostic hardware |

| USD 282.4 M (2025) | Trade Journal B | Extrapolates CAGR from limited base year; no shipment validation |

The comparison shows that estimates swing wide when scope or validation rigor shifts. By anchoring on clearly defined devices, verified shipment trails, and yearly primary-source updates, Mordor's baseline offers decision-makers a balanced, reproducible starting point they can trust.

Key Questions Answered in the Report

What is the current electronic stethoscope market size?

The electronic stethoscope market is projected to register a CAGR of 5.53% during the forecast period (2026-2031)

Who are the key players in electronic stethoscope market?

American Diagnostic Corporation, AD Instruments, Contec Medical Systems Co., Ltd., 3M and Cardionics are the major companies operating in the Global Electronic Stethoscope Market.

Which is the fastest growing region in electronic stethoscope market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in electronic stethoscope market?

In 2025, the North America accounts for the largest market share in electronic stethoscope market.

Why are Bluetooth-enabled stethoscopes gaining popularity?

Bluetooth connectivity supports remote auscultation and seamless data transfer to telehealth and EHR platforms, helping clinicians maintain distance from infectious patients while preserving audio fidelity.

Page last updated on: