Vascular Closure Device Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 6.56% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

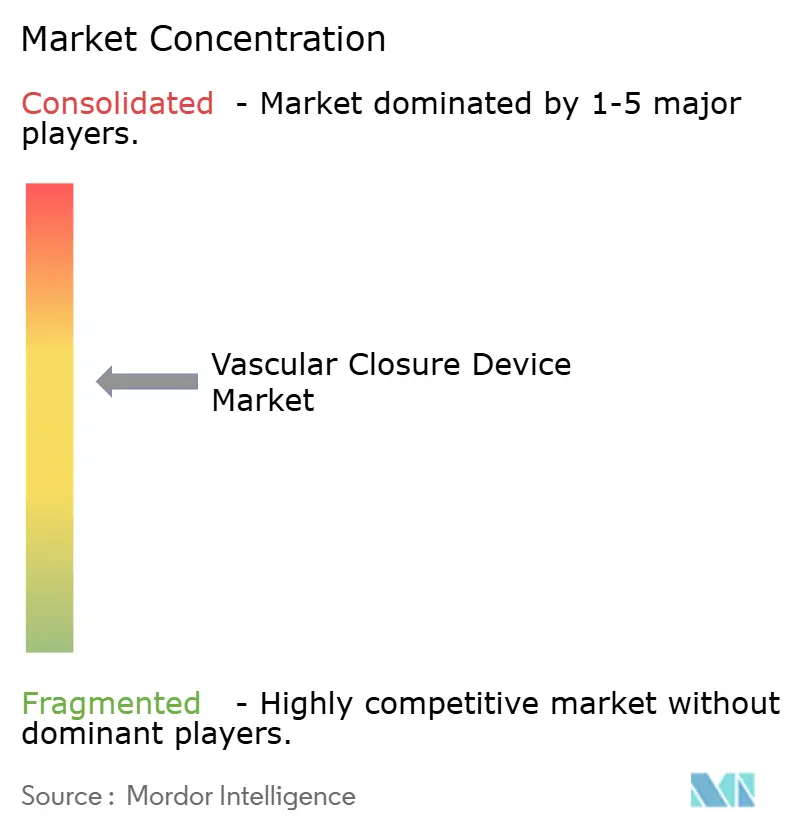

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vascular Closure Device Market Analysis by Mordor Intelligence

The vascular closure devices market size was valued at USD 1.77 billion in 2025 and estimated to grow from USD 1.89 billion in 2026 to reach USD 2.59 billion by 2031, at a CAGR of 6.56% during the forecast period (2026-2031). Heightened procedural complexity in transcatheter aortic valve replacement (TAVR), endovascular aneurysm repair (EVAR), neuro‐interventions, and complex peripheral cases positions vascular closure as an indispensable step in contemporary endovascular therapy. Purchaser preference is tilting away from manual compression because large‐bore access sites up to 25 Fr demand predictable hemostasis, and same-day discharge mandates rapid ambulation. Growing outpatient volumes, adoption of minimally invasive therapies for high-risk elderly patients, and expanding reimbursement for ambulatory care are reinforcing the business case for device-based closure. Innovation momentum is strongest in bio-absorbable materials and large-bore implant designs that shorten deployment time and remove operator variability. Concurrently, radial-specific compression bands address the procedural migration from femoral to radial routes, ensuring that the vascular closure devices market continues to evolve rather than stagnate.

Key Report Takeaways

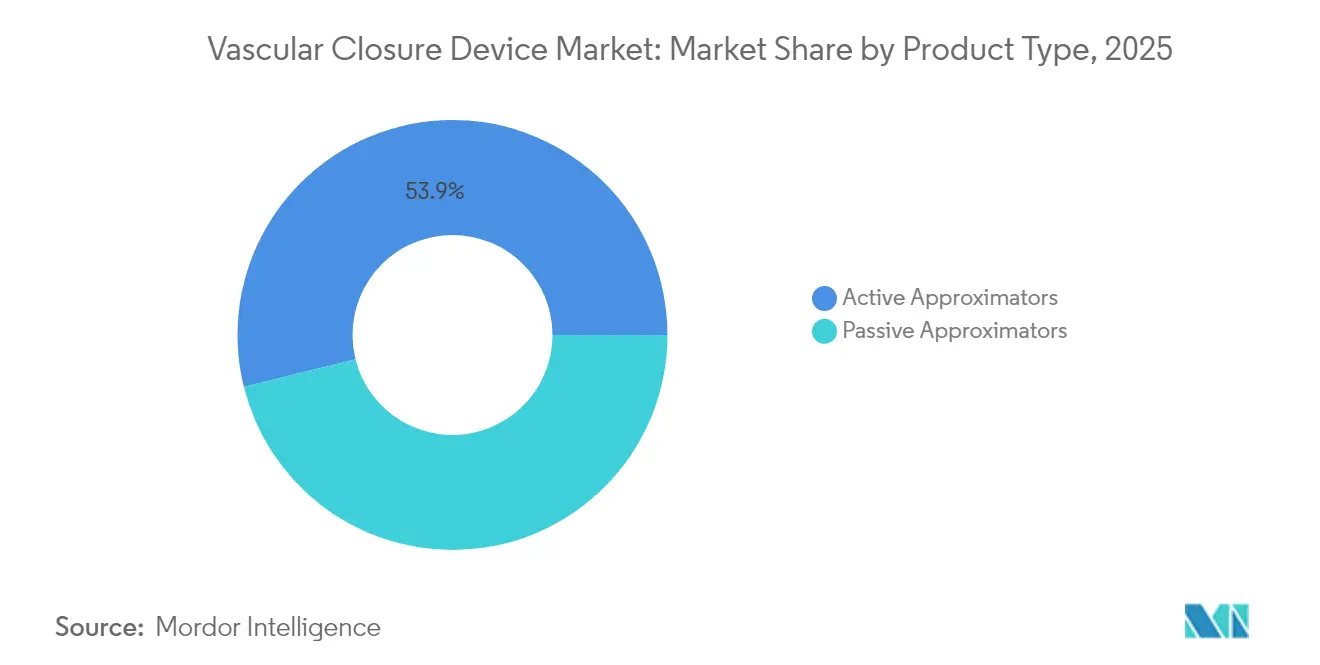

- By product type, active approximators led with 53.89% revenue share in 2025; passive approximators are projected to expand at an 8.12% CAGR through 2031.

- By material composition, collagen-based systems held 50.78% of the vascular closure devices market share in 2025, while suture and filament solutions are advancing at an 8.6% CAGR to 2031.

- By mode of access, femoral sites ≤8 Fr accounted for 60.72% of the vascular closure devices market size in 2025; large-bore femoral sites ≥12 Fr represent the fastest segment, growing at 7.84% CAGR through 2031.

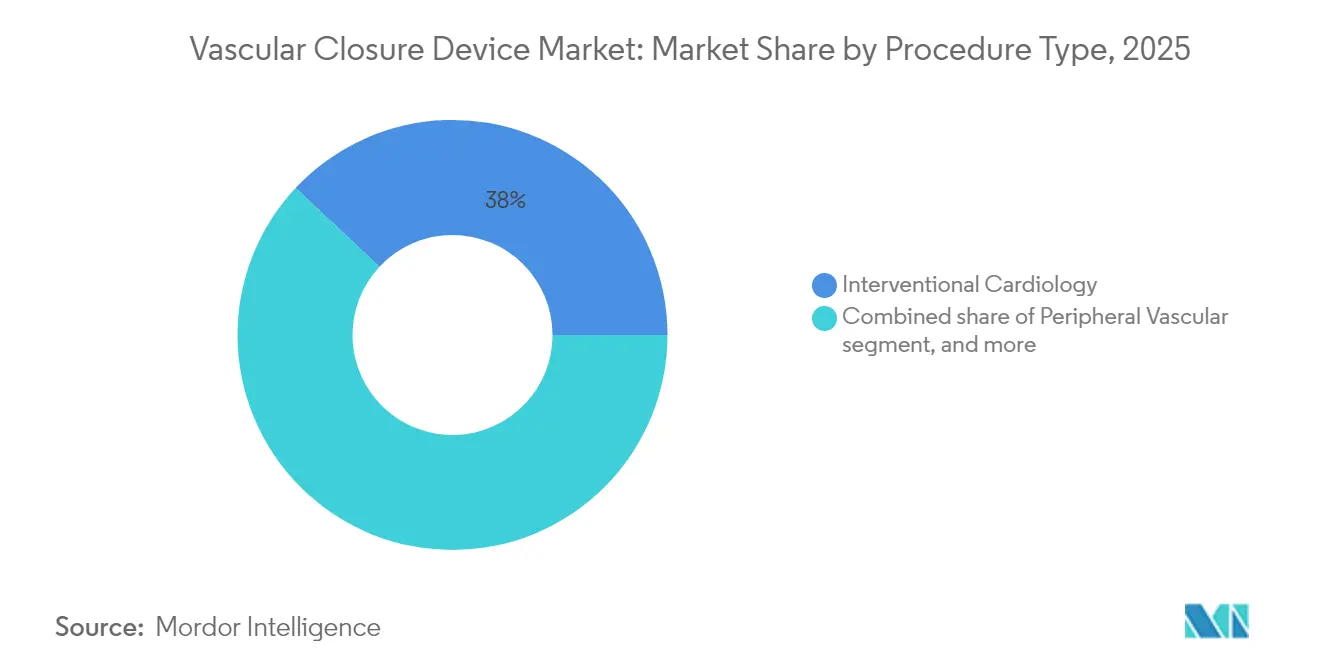

- By procedure, interventional cardiology commanded 38.02% share of the vascular closure devices market size in 2025, whereas neurovascular procedures record the highest projected CAGR at 9.12% to 2031.

- By end user, hospitals captured 55.12% of vascular closure devices market share in 2025; catheterization laboratories and outpatient vascular centers are set to expand at a 9.18% CAGR through 2031.

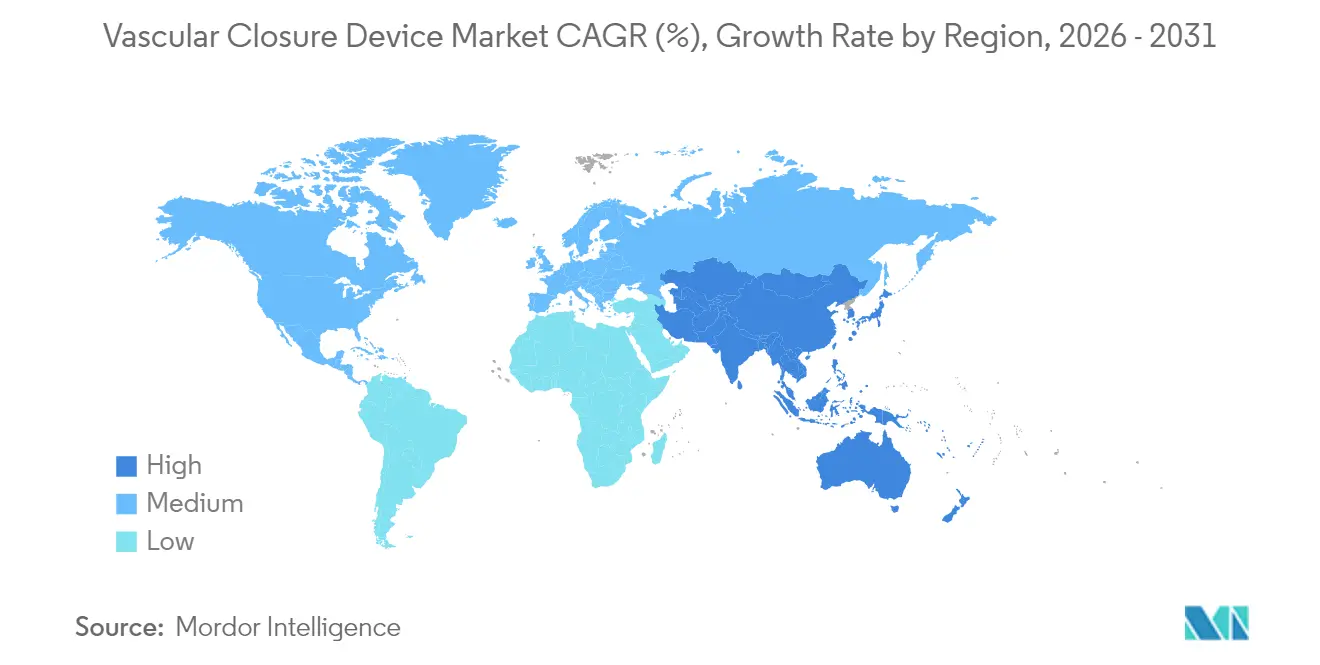

- By geography, North America held 42.30% revenue share in 2025; Asia-Pacific is forecast to post the fastest 7.6% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Vascular Closure Device Market*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increase in catheterization‐related procedures | +1.8% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Growing preference for minimally invasive interventions | +1.2% | Global, led by developed markets | Long term (≥ 4 years) |

| Shift toward radial access in PCI & electrophysiology | +0.9% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Aging population expanding CVD treatment volumes | +1.5% | Global, most pronounced in Asia-Pacific & North America | Long term (≥ 4 years) |

| Expansion of large-bore TAVR/EVAR driving next-gen VCD demand | +1.1% | North America & Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Out-patient & same-day discharge reimbursement incentives | +0.7% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increase in Catheterization-Related Procedures

Procedure counts have escalated as indications for percutaneous coronary interventions, structural heart repair, and complex peripheral revascularization broaden. Abbott confirmed that vessel closure products were a key contributor to its 12.5% medical devices revenue growth in Q1 2025, reflecting direct linkage between access‐site volumes and device demand. Mechanical thrombectomy and high-sheath electrophysiology cases produce multiple puncture sites per patient, pushing operators toward closure systems that manage varied vessel sizes with consistent outcomes. Trials such as AMBULATE demonstrated a 54% reduction in time to ambulation when the VASCADE MVP system replaced manual compression, underscoring workflow gains[1]H. Patel et al., “AMBULATE Trial,” Journal of the American College of Cardiology, jacc.org. Together, these dynamics position procedural volume growth as a persistent catalyst for the vascular closure devices market.

Growing Preference for Minimally Invasive Interventions

Hospitals and ambulatory centers favor minimally invasive care to trim length of stay, reduce infection risk, and improve patient satisfaction. The Heart Rhythm Society and the American College of Cardiology endorse same-day discharge after intracardiac ablation when secure venous hemostasis is achieved, directly tying closure performance to throughput. Terumo’s 15.6% revenue jump in its Cardiac & Vascular Company aligns with this macro-shift and illustrates how robust closure tools accelerate adoption of catheter-based therapies. Imaging navigation improvements further widen the scope of lesions treatable through small punctures, amplifying reliance on vascular closure devices market solutions that seal access quickly and predictably.

Aging Population Expanding Cardiovascular Treatment Volumes

By 2040, individuals ≥65 years will represent 22% of the population, raising the prevalence of structural heart disease and peripheral arterial disease. Elderly cohorts often require multi-site interventions and present coagulation challenges that favor device-based closure over prolonged manual pressure. Japan’s rapid uptake of percutaneous left atrial appendage occlusion after WATCHMAN approval illustrates how age-driven morbidity expands demand for vascular closure devices market products tailored to fragile vessels. Demographic pressure is long lasting and geographically universal, giving suppliers a durable growth runway.

Expansion of Large-Bore TAVR/EVAR Driving Next-Gen Device Demand

Large-bore arteriotomies from 10 Fr to 25 Fr are now commonplace in TAVR and EVAR. Teleflex’s MANTA device and the InSeal VCD both achieved favorable clinical results in closing up to 25 Fr punctures, addressing gaps left by legacy plug technologies. With the global TAVR procedure volume rising toward 300,000 annually, hospitals seek closure platforms that obviate surgical cut-down, shorten turnaround, and reduce bleeding events. Manufacturers with proven large-bore offerings therefore occupy a premium niche within the broader vascular closure devices market.

Restraints Impact Analysis of Vascular Closure Device Market*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of advanced VCDs vs. manual compression | −1.3% | Global; most pronounced in price-sensitive markets | Medium term (2-4 years) |

| Device-related complications & product recalls | −0.8% | Global; with stronger regulatory focus in developed markets | Short term (≤ 2 years) |

| Lengthy approval cycles for bio-absorbable polymers | −0.6% | Europe & United States | Medium term (2-4 years) |

| Cannibalisation from low-cost radial compression bands | −0.4% | Global; especially high radial-adoption centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Cost Of Advanced VCDs Versus Manual Compression

A single closure unit often prices between USD 200 and USD 250, contrasted with negligible material cost for manual compression. While high-income systems justify expenditure through staff time savings, many emerging markets still rely on manual pressure to contain budgets. Value-based purchasing is gradually shifting toward total episode economics, but capital scarcity keeps price sensitivity high, especially where catheter volumes are just now scaling. Manufacturers are responding with tiered product lines and targeted reimbursement dossiers that highlight reduced nursing hours and shorter admissions.

Device-Related Complications And Product Recalls

Safety events undermine physician confidence and trigger regulatory scrutiny. The FDA’s Class I recall of Medtronic’s Pipeline Vantage embolization platform in March 2025 involved 7,820 devices and reignited debate on deployment complexity[2]U.S. Food and Drug Administration, “Medical Device Recall: Pipeline Vantage,” fda.gov. Philips also withdrew its Tack Endovascular System because of incomplete wall apposition concerns, reinforcing vigilance across neurovascular closure applications. Though serious adverse events are statistically rare, publicity around any Class I action can slow adoption curves. Continuous operator education, design refinements, and post-market surveillance are central to sustaining growth in the vascular closure devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Vascular Closure Device Market Segment Analysis

By Product Type:

Active Approximators Remain the WorkhorseActive approximators controlled 53.89% of the vascular closure devices market in 2025. This leadership derives from their suture-mediated or clip-based mechanisms that lock arteriotomies immediately, enabling anticoagulated or large-bore patients to ambulate within hours. Abbott’s Perclose ProGlide illustrates category strength by offering 100% procedural success in multiple high-sheath trials. Hospitals prize the deterministic closure these devices provide, particularly when intra-procedural anticoagulation is mandatory.

Passive approximators occupy a smaller base but are pacing growth at 8.12% CAGR through 2031. Plug, patch, and sealant systems such as Haemonetics’ VASCADE MVP shorten deployment to a single push, reducing fluoroscopy and operator fatigue. The AMBULATE study confirmed a 54% decline in time-to-ambulation, showcasing workflow dividends that resonate with outpatient programs. Simplified technique lowers training barriers, raising adoption in mid-volume centers. As regulatory pressures favor same-day discharge, passive approximators are positioned to expand their contribution to the vascular closure devices market.

By Material Composition:

Bio-Absorbable Polymers Challenge Collagen DominanceCollagen plugs retained 50.78% share in 2025, reflecting three decades of clinical familiarity. Terumo’s Angio-Seal VIP employs a collagen sponge, a polymer anchor, and a suture that collectively resorb within 90 days, offering predictable vessel healing. Physicians value collagen’s thrombin-rich matrix, which accelerates clot formation especially in anticoagulated patients.

Suture and filament devices built from polyglycolic acid, polyethylene glycol, or proprietary polymers are advancing at 8.6% CAGR. Vivasure’s PerQseal Elite is entirely bio-absorbable and designed for 14-22 Fr TAVR sheaths, eliminating retained foreign material and imaging artifacts. Polymer innovations provide tailored degradation kinetics, enabling large-bore security without permanent implants. Clip-based metal systems remain a niche for cases where radiopaque markers aid follow-up imaging. Material diversification reinforces competitive differentiation inside the vascular closure devices market.

By Mode of Access:

Large-Bore Innovation Steals the SpotlightFemoral access ≤8 Fr continues to dominate with 60.72% of vascular closure devices market size in 2025. Established devices like Abbott’s StarClose and Cordis’ ExoSeal deliver reproducible hemostasis for PCI and diagnostic angiography, sustaining demand despite radial penetration. However, radial adoption has already carved share from low-sheath femoral cases and generated a parallel radial compression market.

Large-bore femoral access ≥12 Fr is expanding at 7.84% CAGR on the back of TAVR, EVAR, and mechanical circulatory support. Teleflex’s MANTA and the InSeal patch close 10-25 Fr arteriotomies in a single step, eradicating surgical cut-downs while meeting stringent bleed-through criteria in anticoagulated elders. Radial access maintains utility for diagnostic studies but yields limited incremental revenue to the vascular closure devices market because inexpensive compression bands suffice.

By Procedure Type:

Neurovascular Momentum Overtakes CardiologyInterventional cardiology held 38.02% share of the vascular closure devices market size in 2025. Chronic total occlusion PCI, left main stenting, and alcohol septal ablation supply sustained volume, though radial access curtails femoral device usage. Growth within cardiology hinges on structural heart therapies such as left atrial appendage occlusion, which continue to require femoral access and favor large-bore solutions.

Neurovascular intervention is the fastest-growing slice at 9.12% CAGR. Mechanical thrombectomy volumes are surging because earlier stroke detection meets guideline support for endovascular clot retrieval. The Tubridge flow diverter delivered 100% deployment success in Chinese multicenter assessment, validating procedure efficacy and elevating closure demand. Vascular access for neuro work typically involves 6-9 Fr femoral sheaths, a sweet spot for both active and passive approximators. Electrophysiology ablation adds another vector, where venous closure devices cut bed rest from six hours to two, enhancing patient satisfaction.

By End User:

Outpatient Centers Capture Runway for ExpansionHospitals continued as the principal customer group with 55.12% of vascular closure devices market share in 2025. They benefit from 24/7 imaging, surgical backup, and volume agreements that incentivize bundled procurement. Tertiary centers increasingly push routine elective cases to satellites or ambulatory hubs to preserve ICU resources for complex care.

Catheterization laboratories and outpatient vascular centers will grow 9.18% per year as payers reimburse same-day discharge and patients value rapid turnover. CMS has introduced additional C-codes recognizing complexity adjustments, directly rewarding facilities that achieve prompt hemostasis and early mobilization [3]“NMPA Annual Report on Innovative Devices 2023,” Hankun Law, hankunlaw.com. Telemetry‐ready recovery bays, fixed-cost service lines, and lean nursing ratios make ASCs ideal arenas for devices that guarantee predictable closure, uplifting the vascular closure devices market.

Geography Analysis

North America Vascular Closure Device Market

North America, with 42.30% share, remains the largest regional constituent of the vascular closure devices market. High per-capita procedure rates, early technology adoption, and robust reimbursement frameworks underpin leadership. The FDA granted 510(k) clearance for Cordis’ MYNX CONTROL venous VCD in 2024, emphasizing the region’s role as a primary gateway for next-generation systems. Notwithstanding recalls, North America maintains physician confidence through structured training and rapid post-market surveillance.

APAC Vascular Closure Device Market

Asia-Pacific records the fastest 7.6% CAGR through 2031, spurred by health infrastructure build-out, government investment in cardiovascular care, and an aging population predisposed to stenotic and valvular disease. China’s National Medical Products Administration accepted 61 innovative device dossiers in 2023, signaling accelerating regulatory throughput for local and foreign suppliers. Terumo’s double-digit cardiovascular revenue growth and MicroPort CardioFlow’s VitaFlow Liberty TAVI approval in early 2025 confirm vibrant regional demand. Although device cost sensitivity persists, expanding private insurance and public funding improve affordability.

Europe Vascular Closure Device Market

Europe maintains steady, albeit slower, expansion amid transition to the Medical Device Regulation framework. CE marks awarded to Terumo’s Angio-Seal VIP and Vivasure’s PerQseal Elite under MDR attest to adaptability of manufacturers. Radial penetration in continental centers is higher than in North America, moderating femoral closure volumes, yet growth in large-bore structural heart programs counterbalances attrition. Economic pressures in Southern Europe constrain premium device uptake, but Northern European networks compensate with procedure innovation, sustaining the vascular closure devices market.

Competitive Landscape

Incumbent leaders Abbott, Terumo, and Medtronic anchor the vascular closure devices market with broad portfolios, multiyear safety datasets, and global sales footprints. Abbott leverages combined vessel closure, coronary, and structural heart platforms to cross-sell into hybrid suites, while Terumo aligns Angio-Seal sales with its interventional guidewire franchise. Medtronic pursues neurovascular synergy, though its March 2025 Pipeline Vantage recall underscores execution risk.

Specialists Haemonetics and Vivasure carve niches through technology differentiation. Haemonetics extends VASCADE MVP capabilities into larger venous sheaths for complex ablation, reflecting tailored innovation. Vivasure’s bio-absorbable PerQseal responds directly to unmet large-bore closure needs in TAVR, creating a unique value proposition for structural heart programs. Cordis competes in radial with the ZEPHYR band and complements femoral solutions with ExoSeal, displaying versatility.

Strategic consolidation reshapes boundaries. Stryker’s USD 4.9 billion takeover of Inari adds venous thrombectomy and sets a platform for future closure synergies, while Teleflex sealed a EUR 760 million deal for Biotronik’s vascular assets to expand its large-bore presence. New entrants focus on polymer science and smart deployment mechanics rather than scale, betting on hospital desire for evidence-backed performance gains. Competition now hinges less on price and more on ease of use, post-procedure mobility, and regulatory compliance, sustaining healthy rivalry across the vascular closure devices market.

Vascular Closure Device Industry Leaders

Abbott Laboratories

Cardiva Medical Inc.

Terumo Corporation

Biotronik SE & Co. KG

Cardinal Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Vascular Closure Device Market Companies Covered in this Report

- Abbott Laboratories

- Terumo

- Medtronic

- Haemonetics Corp.

- Teleflex

- Cardinal Health / Cordis

- Beckton Dickinson

- B. Braun

- BIOTRONIK

- Merit Medical Systems

- Vivasure Medical

- Cardiva Medical

- Advanced Vascular Dynamics

- Essential Medical

- InSeal Medical

- Manta (Abbott-Manta)

- Forge Medical

- Rex Medical

- Morrison Medical

- Medeon Biodesign

Recent Industry Developments in Vascular Closure Device Market

- June 2025: Vivasure Medical received CE mark for PerQseal Elite, the first fully bio-absorbable large-bore arterial closure platform.

- February 2025: Stryker completed its acquisition of Inari Medical for USD 4.9 billion, entering high-growth peripheral markets.

- February 2025: Teleflex acquired Biotronik’s vascular intervention business for EUR 760 million to broaden its interventional cardiology lineup.

- January 2025: MicroPort CardioFlow secured NMPA approval for the VitaFlow Liberty Flex TAVI system featuring motorized delivery.

- April 2024: Haemonetics launched VASCADE MVP XL in the United States, offering greater collagen volume for 10-12 Fr venous sheaths.

Vascular Closure Device Market Report Scope and Research Methodology

Market Definition and Coverage

Our study treats the vascular closure device (VCD) market as all sterile, single-use devices purposely designed to seal arterial or venous punctures created during percutaneous diagnostic or interventional procedures. Products covered include active approximators (suture, clip, staple), passive plug or sealant systems, and large-bore solutions used after TAVR and EVAR. The analysis tracks value generated from original device sales to hospitals, cath-labs, and ambulatory surgical centers across 20 major countries.

Scope exclusion: hemostatic pads, compression bands, and manual compression accessories are not counted because they do not create an intraluminal seal.

Segments Covered in This Report

- By Product Type

- Active Approximators

- Clip-based Devices

- Suture-based Devices

- Plug-based Devices

- Passive Approximators

- Hemostatic Pads & Patches

- Compression Devices

- Active Approximators

- By Material Composition

- Collagen-based

- PEG / Polymer-based

- Suture / Filament-based

- Metal Clip-based

- By Mode of Access

- Femoral Access

- Large-bore Femoral

- Radial Access

- Other Mode of Access

- By Procedure Type

- Interventional Cardiology

- Peripheral Vascular

- Neurovascular

- Structural Heart / TAVR

- Electrophysiology

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Cath-labs & Out-patient Vascular Centres

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Interviews with cardiologists, interventional radiologists, and procurement managers in North America, Europe, and Asia-Pacific were conducted. Our team used these calls to validate plug preference in same-day discharge protocols, gauge pricing pressure from group-purchasing organizations, and fine-tune penetration curves for large-bore devices entering TAVR workflows. Insights were blended with a short online survey of cath-lab nurses on time-to-ambulation thresholds.

Desk Research

We began by mapping procedure volumes and access-site splits from open datasets such as the American College of Cardiology's NCDR, EuroPCR abstracts, Japan Circulation Society audits, and national catheterization registries. Device unit shipments were approximated using import-export codes (HS 901890) available through UN Comtrade and Volza, then crosschecked against annual reports and 10-Ks. Clinical outcome meta-analyses published in journals like JACC and EuroIntervention refined assumptions on adoption rates of radial versus femoral closure. To size hospital spending, we referenced average selling prices reported in Medicare Part B claim files and tender notices collated by Tenders Info. D&B Hoovers and Dow Jones Factiva supplied supplemental company-level revenue splits. These sources illustrate, not exhaust, the desk material consulted; additional public and subscription data further informed the work.

Market-Sizing & Forecasting

Mordor analysts applied a top-down rebuild that starts with coronary, peripheral, and neurovascular procedure counts, followed by access-site shares and device-per-procedure ratios. Outputs were then stress-tested with selected bottom-up roll-ups of supplier revenues and channel checks. Key variables modeled include PCI growth, shift to radial access, TAVR volume expansion, average selling price erosion, and hospital adoption of same-day discharge. Multivariate regression against macro indicators (aging population, hypertension prevalence, cath-lab capacity) underpins the 2025-2030 forecast, while scenario analysis captures reimbursement or recall shocks. Data gaps in bottom-up estimates were smoothed using weighted moving averages anchored to verified shipment trends.

Data Validation & Update Cycle

Each draft model passes a three-layer review: analyst, senior domain lead, and quality team, before sign-off. Variances exceeding ±5% versus historical patterns trigger re-contact with primary sources. We refresh the dataset annually and issue interim revisions if material events (e.g., mass recall, pivotal trial success) distort the baseline.

How Mordor Intelligence's Vascular Closure Device Market Size Compares to Other Published Estimates

Published estimates often diverge because firms select different product mixes, assume varying price erosion, or refresh on uneven cadences.

Key gap drivers here include: some publishers fold external hemostasis pads into market value, others extrapolate revenues from small hospital samples, and a few project aggressive plug price drops without validating with purchasing managers. Mordor's scoped definition, dual-route modeling, and yearly refresh temper such swings.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.77 B (2025) | Mordor Intelligence | - |

| USD 1.74 B (2024) | Global Consultancy A | Excludes large-bore devices and applies uniform ASP across regions |

| USD 1.56 B (2024) | Trade Journal B | Uses limited hospital survey, no adjustment for radial adoption |

| USD 1.96 B (2024) | Regional Consultancy C | Bundles manual compression aids, inflates base by mixed device categories |

Taken together, the comparison shows that our disciplined scope selection and transparent variable mapping deliver a balanced, repeatable baseline that decision-makers can trust.

Key Questions Answered in the Report

How fast is the vascular closure devices market expected to grow between 2026 and 2031?

The market is projected to expand at a 6.56% CAGR, moving from USD 1.89 billion in 2026 to USD 2.59 billion by 2031.

Which region shows the highest growth potential?

Asia-Pacific leads in expansion with a 7.6% forecast CAGR, propelled by healthcare modernization, regulatory acceleration, and aging demographics.

What product category currently dominates the sector?

Active approximators hold 53.89% revenue share due to their immediate hemostasis and suitability for complex, large-bore procedures.

Why are large-bore closure systems gaining traction?

The rise of TAVR and EVAR produces punctures up to 25 Fr that traditional plugs cannot seal, driving demand for devices like Teleflex’s MANTA that secure large arteriotomies safely.

How do outpatient reimbursement trends influence device selection?

New CMS codes reward same-day discharge, so centers prioritize closure tools that achieve rapid hemostasis and early ambulation, shifting purchases toward high-efficacy systems.

What safety concerns exist around vascular closure devices?

While complication rates are low, recalls such as the FDA Class I action on Medtronic’s Pipeline Vantage highlight the need for continuous design refinement and operator training.

Page last updated on: