Body Fat Measurement Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

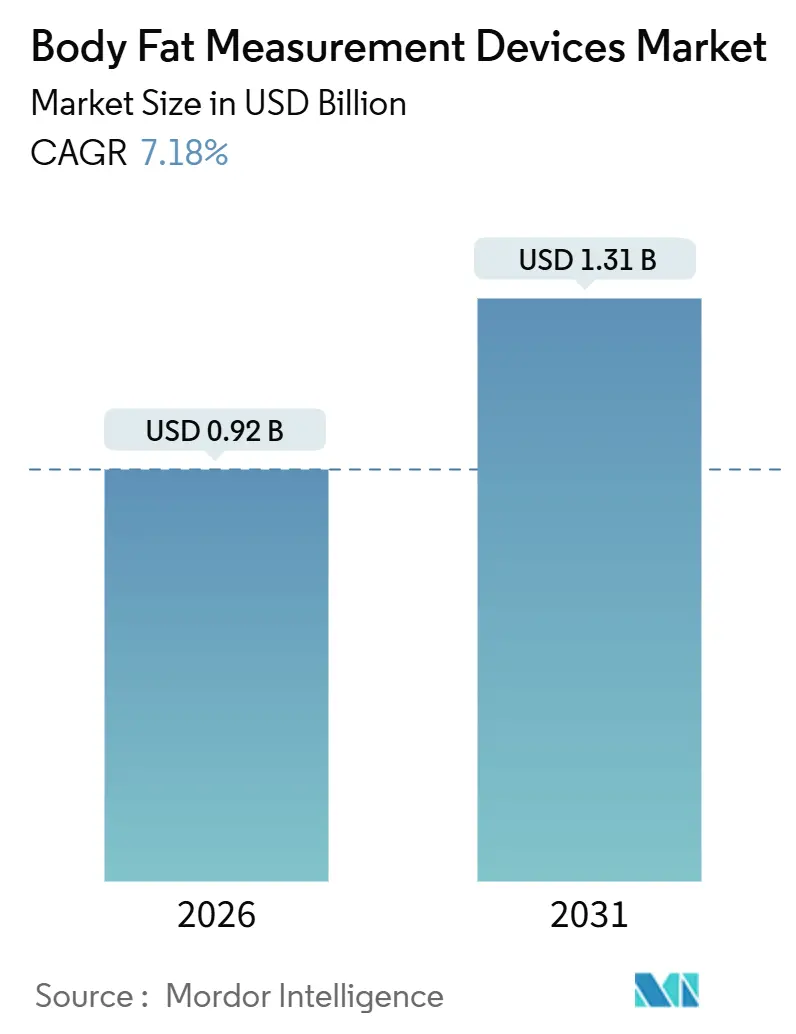

| Market Size (2026) | USD 0.92 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

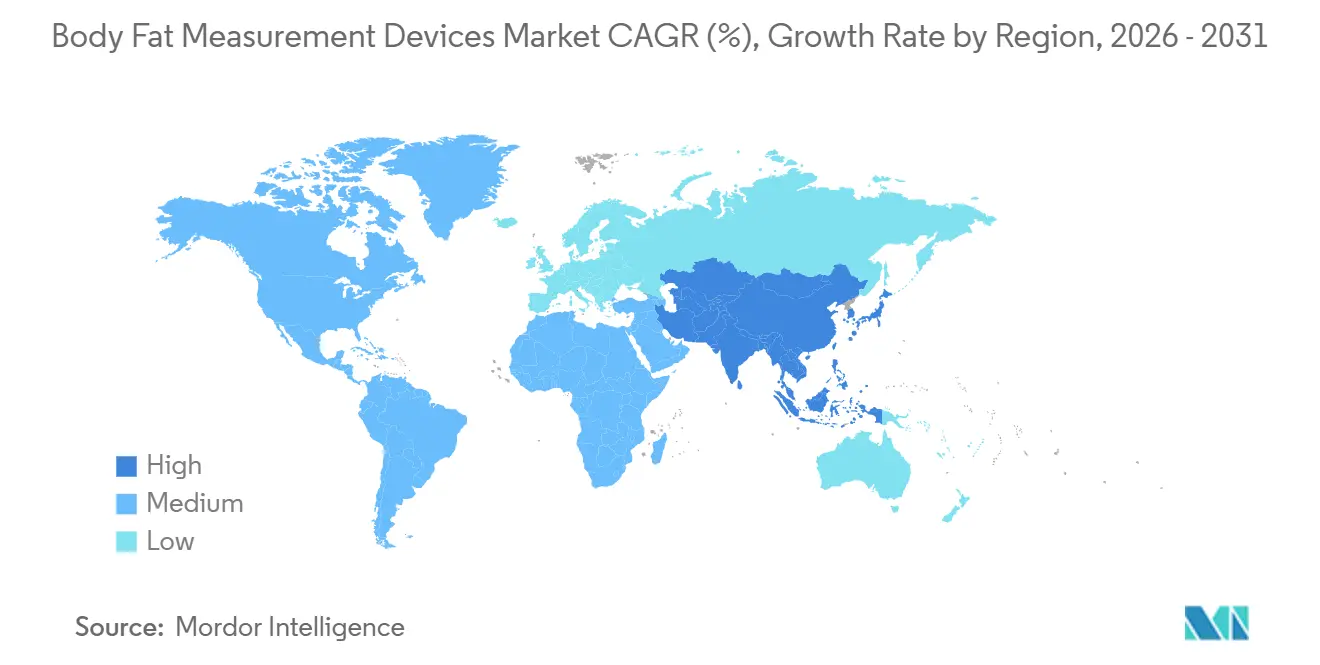

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Body Fat Measurement Devices Market Analysis by Mordor Intelligence

The Body Fat Measurement Devices Market size is estimated at USD 0.92 billion in 2026, and is expected to reach USD 1.31 billion by 2031, at a CAGR of 7.18% during the forecast period (2026-2031).

Demand is rising as healthcare systems, fitness operators, and consumers move from simple weight tracking toward precise body-composition monitoring that differentiates visceral fat from lean mass.[1]World Health Organization, “Obesity and Overweight,” WHO, who.intMulti-frequency bio-impedance analyzers (BIA) have become a clinical mainstay because they deliver sub-60-second readings without radiation exposure, while 3-D optical scanners are gaining momentum in retail gyms that gamify member progress. Insurers in North America now reimburse body-fat data transfers under remote-patient-monitoring codes, accelerating connected-device adoption. Meanwhile, Asia–Pacific governments embed body-composition checks into national health programs, creating a structural tailwind for the body fat measurement devices market.

Key Report Takeaways

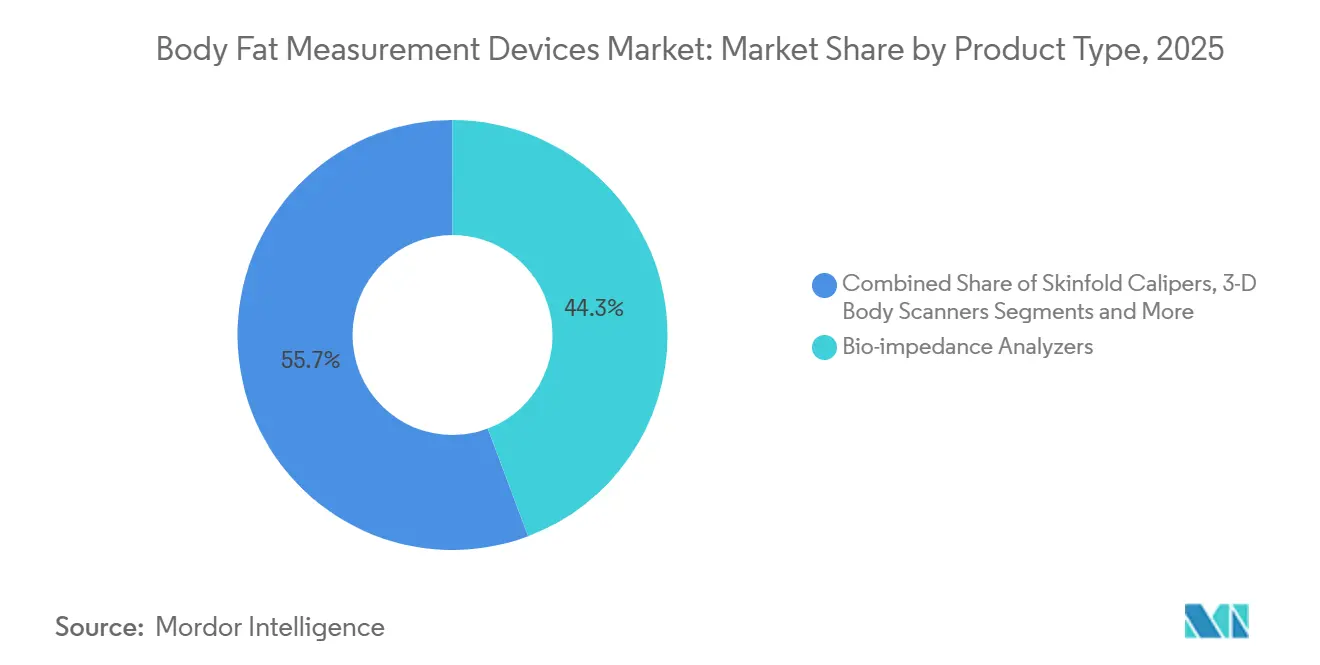

- By product type, bio-impedance analyzers led with 44.26% revenue share in 2025; 3-D body scanners are forecast to advance at an 11.96% CAGR to 2031.

- By portability, stationary systems accounted for 52.78% of the body fat measurement devices market share in 2025, whereas wearables and smart scales are expanding at an 11.96% CAGR through 2031.

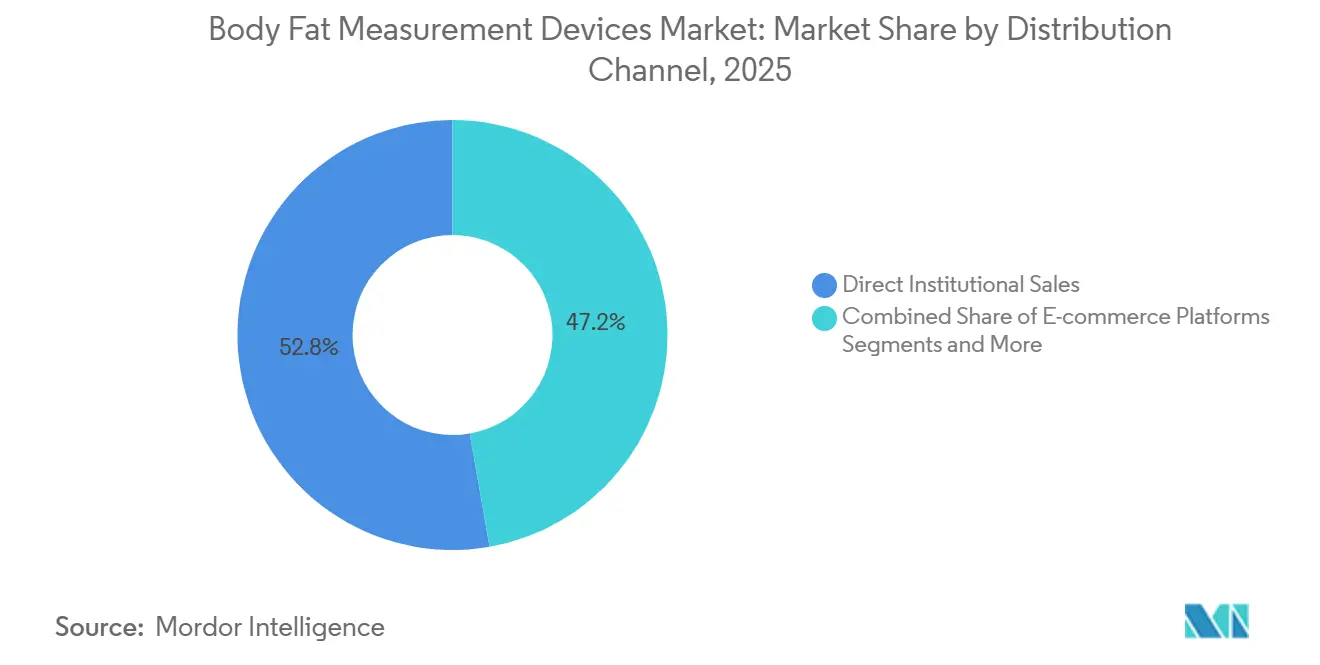

- By distribution channel, direct institutional sales represented 52.76% of 2025 revenue, while e-commerce is set to grow at a 12.06% CAGR to 2031.

- By application, sports and fitness performance captured 36.45% revenue in 2025, and bariatric assessment is projected to rise at a 10.62% CAGR through 2031.

- In 2025, North America generated 39.36% of global sales; Asia–Pacific is the fastest-growing region at a 9.67% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Body Fat Measurement Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising obesity prevalence and associated chronic diseases | +1.8% | Global—highest in North America, Middle East, Pacific Islands | Long term (≥ 4 years) |

| Expansion of fitness-club memberships and connected gym ecosystems | +1.3% | Asia–Pacific core, spill-over to Latin America and Middle East | Medium term (2-4 years) |

| Rapid technological advances in multi-frequency BIA analyzers | +1.1% | North America and Europe for clinics; Asia–Pacific for consumers | Medium term (2-4 years) |

| Integration of body-fat analyzers with tele-health platforms | +0.9% | North America and EU, pilots in India and Brazil | Short term (≤ 2 years) |

| Insurer-driven wellness incentive programs | +0.7% | North America, Western Europe, Australia | Medium term (2-4 years) |

| Corporate wellness gamification initiatives | +0.6% | North America, select Asia–Pacific hubs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Obesity Prevalence And Associated Chronic Diseases

More than 890 million adults lived with obesity in 2025, a figure expected to surpass 1 billion by 2030. BMI alone misclassifies up to 30% of people who harbor excess visceral fat despite a normal weight, a phenotype linked to two- to three-fold higher cardiovascular risk.[2]Luca A. Lotta et al., “Association of Genetic Risk Variants for Cardiometabolic Traits With Body Composition,” Nature Medicine, nature.com Diabetes diagnoses reached 537 million adults in 2024, and sarcopenic obesity now affects up to one-fifth of older adults, pushing clinics to adopt multi-compartment body-composition testing. Canada’s obesity rate climbed to 30.3% in 2023, prompting public reimbursement for body-fat assessment in primary care.[3]Statistics Canada, “Table 13-10-0096-01: Health Characteristics, Annual Estimates,” Government of Canada, statcan.gc.ca As guidelines pivot from weight to fat distribution, the body fat measurement devices market gains a durable demand base.

Expansion Of Fitness-Club Memberships And Connected Gym Ecosystems

Gym penetration remains below 1% in India yet is doubling every three years, while China mandates body-composition tracking in community health centers. Premium chains deploy InBody and Tanita analyzers during onboarding, selling USD 20–40 scans or bundling unlimited access within premium tiers. Equinox and Lifetime Fitness installed more than 500 InBody units across North America, reporting 12–15% lower membership churn when progress visuals are provided. Device utilization therefore pivots from one-time assessments to routine engagement, a shift that reinforces recurring sales for the body fat measurement devices market.

Rapid Technological Advances In Multi-Frequency BIA Analyzers

Current multi-frequency BIA platforms measure at 1 kHz to 1 MHz, allowing differentiation of intracellular and extracellular water. InBody’s direct-segmental technology correlates above 0.95 with DEXA for fat-mass estimation. ESPEN’s 2024 guidelines formally endorsed multi-frequency BIA in sarcopenia and dialysis care. Tanita’s ethnicity-specific algorithms cut error margins to ±2–3 percentage points. Artificial-intelligence models trained on thousands of paired DEXA-BIA datasets now raise accuracy in obese and elderly cohorts, underscoring why technology gains add momentum to the body fat measurement devices market.

Integration Of Body-Fat Analyzers With Tele-Health Platforms

CMS reimbursement introduced in 2024 covers remote transmission of body-composition data for chronic conditions, prompting tele-health providers to bundle BIA-enabled smart scales. Withings received FDA clearance for a scale that streams segmental fat, muscle, and vascular-age metrics to clinician dashboards. Bariatric pathways now require pre-operative and quarterly post-surgical body-fat monitoring to ensure lean-mass preservation. Moving measurements into the home boosts frequency and yields richer longitudinal datasets for care teams, further scaling the body fat measurement devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of advanced DEXA & BIA machines | −1.2% | Global, most acute in price-sensitive emerging markets | Medium term (2-4 years) |

| Radiation-exposure concerns with DEXA scans | −0.8% | North America & Europe | Long term (≥ 4 years) |

| Lack of global accuracy & calibration standards | −0.6% | Global | Long term (≥ 4 years) |

| Data-privacy compliance burden for connected devices | −0.5% | EU, North America, Asia–Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost Of Advanced DEXA & BIA Machines

Refurbished DEXA systems cost USD 30,000–45,000, with annual service fees adding USD 3,800–12,000. InBody’s flagship 970S lists at USD 32,605, while mid-tier models still command five-figure prices. Clinics in markets where healthcare spending falls below USD 500 per capita defer purchases or opt for lower-accuracy consumer scales. Leasing and refurbished channels mitigate but do not remove the barrier, extending replacement cycles and holding back the body fat measurement devices market.

Radiation-Exposure Concerns With DEXA Scans

DEXA imparts 1–15 µSv per scan—comparable to two days of natural radiation—yet 40–50% of wellness clients refuse scans labeled “X-ray”. FDA dose-optimization rules add complexity for gyms wishing to install DEXA units. Pregnant women and children are usually excluded, limiting pediatric obesity programs. As perception outstrips actual risk, buyers gravitate to radiation-free BIA and optical scanners.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Multi-Frequency BIA Dominates, 3-D Scanners Surge

Multi-frequency BIA captured 44.26% of 2025 revenue, confirming its status as the technological anchor of the body fat measurement devices market. The segment’s fast, radiation-free workflow drives acceptance in hospitals, corporate wellness clinics, and elite-sport facilities. Bio-impedance analyzers’ correlation of 0.95 with DEXA benchmarks appeals to clinicians who need repeatable metrics across large populations. In parallel, 3-D optical scanners are scaling fastest at an 11.96% CAGR because retail gyms value the visual storytelling that inch-by-inch shape reconstructions deliver to members.

Despite being the DEXA reference standard, radiation fears and higher scan costs constrain growth. Air-displacement plethysmography and hydrostatic weighing remain research staples but lack mainstream convenience. Skinfold calipers persist in field settings due to zero consumables, yet technician skill introduces variability that professional buyers increasingly reject. As AI-enhanced impedance algorithms close the accuracy gap with DEXA, diffusion of advanced BIA models deepens the body fat measurement devices market penetration in both clinic and home settings.

By Portability: Wearables Disrupt Stationary Incumbents

Stationary analyzers still hold 52.78% share because hospitals, universities, and premium gyms prioritize the precision and regulatory compliance these 30–40 kg systems deliver. However, smart scales priced under USD 100 are democratizing daily body-fat tracking for households worldwide. Withings cut the retail price of its Body Smart to USD 84.95 in 2025, making multi-frequency BIA attainable for mass consumers. That affordability lifts unit volumes and nudges the body fat measurement devices market toward a mixed landscape of clinical hardware and connected home gadgets.

Hand-held devices sit between the two extremes, serving athletic trainers and home-health nurses who need portability but accept single-frequency limitations. As ISO/IEEE 11073-10420 streamlines health-data interchange, connected wearables gain an integration edge over offline stationary systems, shifting investment toward cloud-linked product lines inside the body fat measurement devices industry.

By Distribution Channel: E-Commerce Erodes Institutional Dominance

Direct institutional sales account for 52.76% of 2025 revenue because facilities purchasing USD 10,000-plus devices need onsite demonstrations, financing, and multi-year service agreements. Yet online marketplaces are growing at 12.06% CAGR as consumers comparison-shop smart scales, read thousands of verified reviews, and leverage free-return policies. Amazon’s health-and-household category generated USD 12 billion in 2024, with body-composition scales a rising slice. Dual go-to-market strategies now split: premium manufacturers court hospitals via direct reps, while mass-market brands rely on e-commerce efficiency to scale the body fat measurement devices market.

By Application: Bariatric Assessment Accelerates Fastest

Sports and fitness performance still command the largest slice at 36.45% because athletes and gym members link lean-mass metrics to training outcomes. Yet bariatric assessment is the fastest climber, expanding at 10.62% CAGR as surgical volumes rebound post-pandemic and payers mandate body-composition profiling for risk stratification. DEXA-derived visceral-fat thresholds better predict surgical complications than BMI, triggering hospital demand for precise devices. Home monitoring for chronic-disease management also rises as smart-scale data flows directly into cardiology and endocrinology dashboards, bolstering daily cadence in the body fat measurement devices market.

Geography Analysis

North America generated 39.36% of 2025 revenue, underpinned by employer wellness mandates, CMS reimbursement of remote body-fat monitoring, and a mature gym ecosystem that embeds composition scans in premium plans. Labcorp performs millions of biometric screenings annually, reflecting insurer preference for body-fat percentage over BMI. Canada reimburses body-composition testing in primary care, while Mexico’s rising middle class fuels smart-scale adoption despite lower institutional spend.

Asia–Pacific is the fastest-growing geography at 9.67% CAGR through 2031. China’s Healthy China 2030 strategy inserts body-composition checks into community clinics, and India’s gym membership base is doubling every three years. Japan’s aging-society needs sarcopenia screening, and South Korea boasts the world’s highest per-capita penetration thanks to homegrown InBody supplying over 70% of hospitals. Australia’s private insurers mirror U.S. incentive programs, further scaling the body fat measurement devices market.

Europe maintains solid demand as ESPEN’s 2024 guidelines endorse multi-frequency BIA for clinical use. GDPR enforcement raises compliance costs, yet local champions Withings and Beurer navigate rules effectively. In the Middle East, obesity prevalence above 35% in Kuwait and Saudi Arabia propels government wellness initiatives that include BIA testing. Latin America sees momentum in Brazil and Argentina, where urban fitness culture overlaps with economic volatility that restrains high-end equipment purchases but encourages smart-scale trials.

Competitive Landscape

The body fat measurement devices market is moderately fragmented. InBody has shipped over 20 million units, cementing its multi-frequency BIA as the de facto research standard and capturing 70% of Korean hospital placements. Tanita uniquely spans USD 50 consumer scales to USD 15,000 clinical systems, leveraging Columbia University co-developed algorithms to serve both mass and professional segments. Hologic leads DEXA, yet GE HealthCare’s Lunar iDXA challenges on faster scan times and lower radiation.

Disrupters Evolt 360 and Skulpt integrate coaching advice directly into device screens, courting millennials who demand actionable insights in seconds. Withings secured FDA clearance for a clinical-grade yet consumer-priced scale that measures segmental fat plus vascular age, demonstrating that software ecosystems now rival sensor hardware as competitive moats. Interoperability under ISO/IEEE 11073-10420 favors firms with robust cloud platforms. Pediatric body-composition algorithms and senior sarcopenia solutions remain under-served niches ready for innovation within the body fat measurement devices industry.

Body Fat Measurement Devices Industry Leaders

InBody Co., Ltd

Tanita Corporation

Omron Healthcare, Inc.

GE HealthCare

Hologic, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: RunStar launched three smart scales, including the 8E SmartScan Ultra Body Fat Scale, to expand personalized health-tracking options.

- May 2025: Seca introduced the mBCA Alpha, a compact body-composition scanner tailored for primary care clinics, reinforcing its shift to technology-first solutions.

- February 2025: Prenuvo disclosed closing a USD 120 million Series B round to scale proactive whole-body MRI screening services.

Global Body Fat Measurement Devices Market Report Scope

Body fat measurement devices are tools, such as smart scales or handheld analyzers, that estimate body composition—fat, muscle, water, and bone—using Bioelectrical Impedance Analysis (BIA), offering insights for fitness, nutrition, and health monitoring.

The Body Fat Measurement Devices Market Report is segmented by Product Type, Portability, Distribution Channel, Application, and Geography. By Product Type, the market is segmented into Bio-impedance Analyzers, Skinfold Calipers, DEXA, Air-Displacement Plethysmography, Hydrostatic Weighing, and 3-D Body Scanners. By Portability, the market is segmented into Stationary, Portable, and Wearable. By Distribution Channel, the market is segmented into Direct, Retail, and E-commerce. By Application, the market is segmented into Sports, Disease Management, Wellness, and Bariatric. By Geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends across major regions globally. Market Forecasts are Provided in Terms of Value (USD).

| Bio-impedance Analyzers |

| Skinfold Calipers |

| Dual-energy X-ray Absorptiometry (DEXA) |

| Air-Displacement Plethysmography |

| Hydrostatic Weighing |

| 3-D Body Scanners |

| Stationary Systems |

| Portable Hand-held Devices |

| Wearable / Smart-Scale Systems |

| Direct Institutional Sales |

| Specialty & Mass Retail |

| E-commerce Platforms |

| Sports & Fitness Performance |

| Chronic-disease & Metabolic-syndrome Management |

| General Wellness & Lifestyle Tracking |

| Bariatric / Weight-loss Assessment |

| Hospitals & Clinics |

| Fitness & Wellness Centers / Gyms |

| Home Users |

| Universities & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Bio-impedance Analyzers | |

| Skinfold Calipers | ||

| Dual-energy X-ray Absorptiometry (DEXA) | ||

| Air-Displacement Plethysmography | ||

| Hydrostatic Weighing | ||

| 3-D Body Scanners | ||

| By Portability | Stationary Systems | |

| Portable Hand-held Devices | ||

| Wearable / Smart-Scale Systems | ||

| By Distribution Channel | Direct Institutional Sales | |

| Specialty & Mass Retail | ||

| E-commerce Platforms | ||

| By Application | Sports & Fitness Performance | |

| Chronic-disease & Metabolic-syndrome Management | ||

| General Wellness & Lifestyle Tracking | ||

| Bariatric / Weight-loss Assessment | ||

| By End User | Hospitals & Clinics | |

| Fitness & Wellness Centers / Gyms | ||

| Home Users | ||

| Universities & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected 2031 value of the body fat measurement devices market?

The body fat measurement devices market is forecast to reach USD 1.31 billion by 2031.

How fast is the market expected to grow between 2026 and 2031?

The market is set to expand at a 7.18% CAGR over the period.

Which product category currently holds the largest revenue share?

Bio-impedance analyzers lead with 44.26% of 2025 revenue.

Which region is forecast to be the fastest growing?

Asia–Pacific is expected to register a 9.67% CAGR through 2031.

Why are 3-D body scanners gaining popularity?

They offer visual body-shape reconstructions that enhance member engagement in gyms, driving an 11.96% CAGR for the segment.

What is a key restraint limiting market adoption?

High upfront costs for DEXA and advanced BIA systems, which can exceed USD 30,000 per unit, deter smaller clinics and emerging-market buyers.

Page last updated on: