Lip Augmentation Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 7.81 Billion |

| Market Size (2030) | USD 11.48 Billion |

| Growth Rate (2025 - 2030) | 8.01% CAGR |

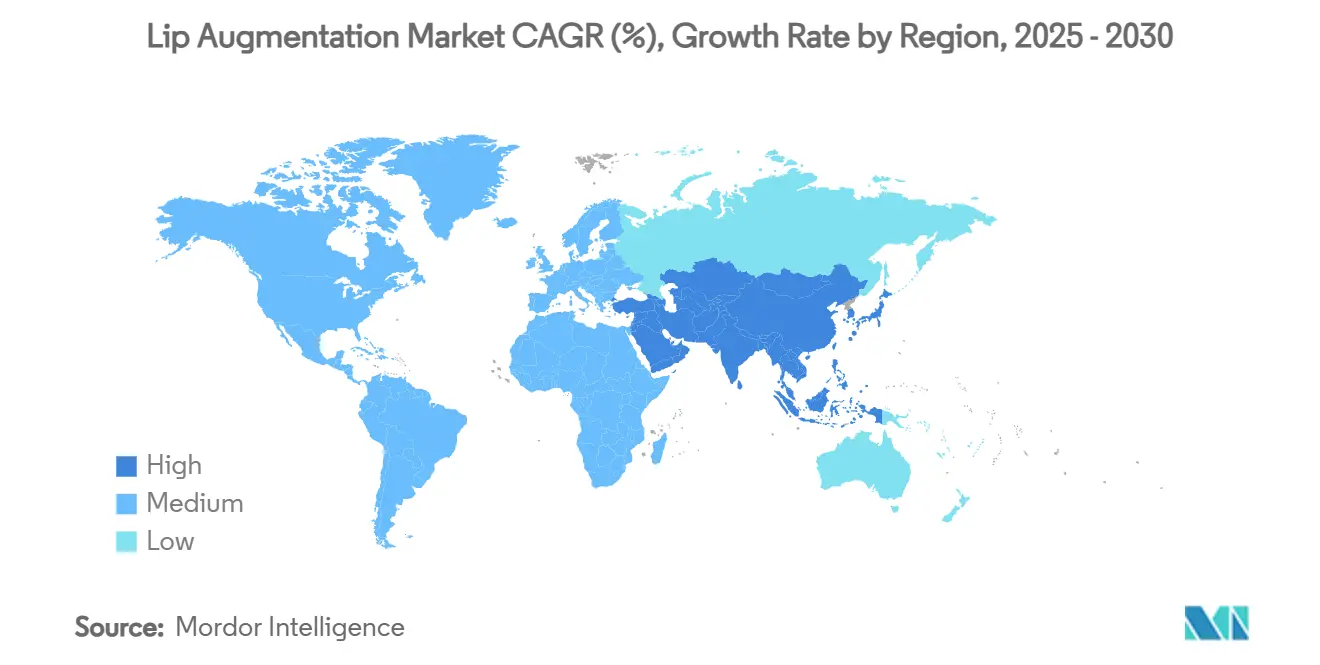

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

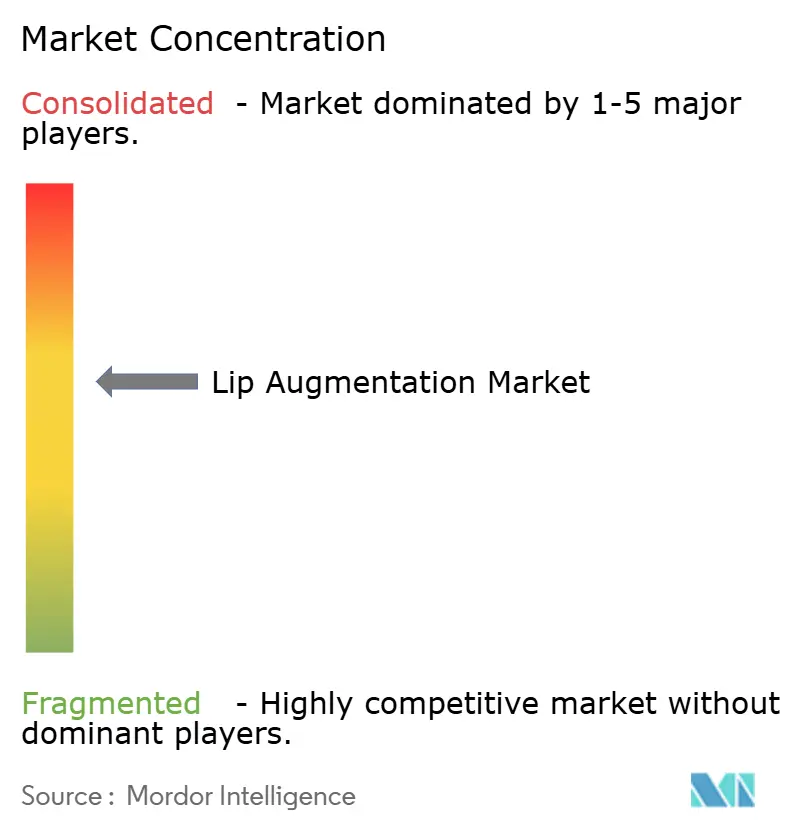

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lip Augmentation Market Analysis by Mordor Intelligence

The lip augmentation market size stands at USD 7.81 billion in 2025 and is expected to reach USD 11.48 billion by 2030, advancing at an 8.01% CAGR. Strong social-media influence, next-generation hyaluronic-acid (HA) technologies and widening male participation are keeping demand resilient despite tightening regulations. Immediate aesthetic results with minimal downtime position the procedure as an accessible “lunchtime” treatment that fits modern professional schedules. Regenerative approaches such as platelet hybridized adipose therapy are shifting consumer expectations toward natural-looking, longer-lasting outcomes. At the same time, advisory reviews scheduled by the U.S. Food and Drug Administration signal higher safety hurdles that established players are well equipped to navigate.

Key Report Takeaways

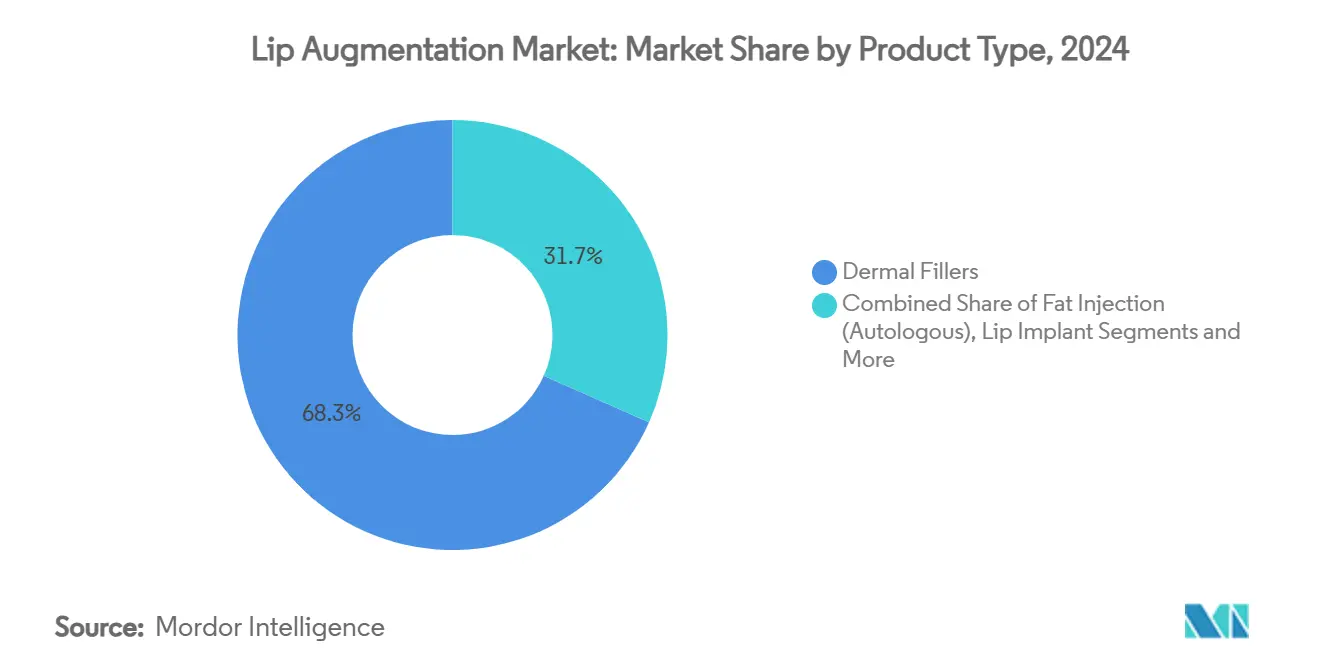

- By product type, dermal fillers led with 68.34% revenue share in 2024; fat injection is projected to grow at an 11.89% CAGR to 2030.

- By material, hyaluronic acid captured 77.24% of the lip augmentation market share in 2024, while autologous fat is set to expand at a 12.07% CAGR through 2030.

- By procedure type, non-invasive methods accounted for 81.22% of the lip augmentation market size in 2024 and are advancing at a 12.89% CAGR to 2030.

- By gender, women represented 89.34% of procedures in 2024; the male segment is growing fastest at a 10.34% CAGR.

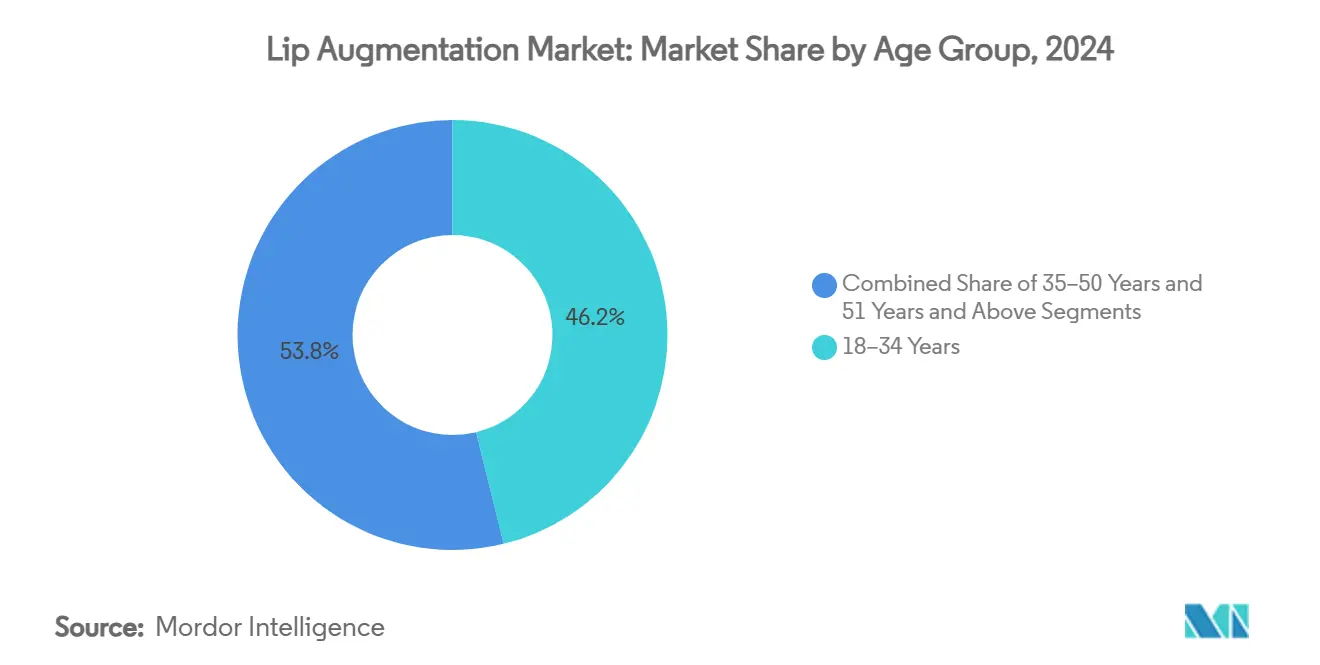

- By age group, the 18-34 cohort held 46.19% of procedures in 2024, whereas the 35-50 segment shows the highest 10.67% CAGR through 2030.

- By end-user, dermatology clinics commanded 44.33% share in 2024; medical spas are expanding at an 11.47% CAGR.

- By geography, North America dominated at 36.48% share in 2024; Asia-Pacific is forecast to grow at a 10.83% CAGR.

Global Lip Augmentation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Minimally-invasive procedure preference | +2.1% | Global, strongest in North America & Europe | Medium term (2-4 years) |

| Social-media and selfie culture | +1.8% | Asia-Pacific and North America | Short term (≤2 years) |

| Next-generation HA innovations | +1.5% | North America & Europe, spreading to Asia-Pacific | Medium term (2-4 years) |

| Expanding male aesthetics segment | +1.2% | North America & Europe, emerging in Asia-Pacific | Long term (≥4 years) |

| Regenerative fat-grafting techniques | +0.9% | North America & Europe | Long term (≥4 years) |

| AI-enabled 3-D visualization consults | +0.6% | North America & Europe, global rollout | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Minimally-Invasive Aesthetic Procedures

Post-pandemic wellness priorities have recast lip treatments as confidence boosters rather than vanity projects, with two-thirds of patients citing psychological benefit as their main motive.[1]E. Ashley et al., “Exploring the Psychological and Social Motivations for Aesthetic Treatments in the Post-COVID Era,” Journal of Cosmetic Medicine, doi.org Faster injection protocols now complete in under 30 minutes and deliver 12–18 month durability, satisfying busy professionals. Social media normalization reduces stigma, bringing first-time clients into clinics. The procedure’s reversibility through hyaluronidase adds a safety cushion valued by both providers and consumers. Together, these factors underpin enduring demand across mature and emerging economies.

Rising Social-Media–Driven Beauty Ideals and “Selfie Culture”

Filtered images encourage consumers to seek lips that replicate influencer aesthetics, and reference photos now accompany many consultations.[2]K. Frank, “Revealing the Perfect Smile: How Philtrum Length Shapes Lip Beauty,” Aesthetic Plastic Surgery, springer.comWhile “Instagram lips” once favored dramatic volume, a shift toward subtle, face-balanced enhancement is emerging. Continuous self-documentation heightens awareness of minor imperfections, driving repeat visits. Practitioners respond by tailoring injection plans that respect ethnic and anatomical diversity. This trend keeps volumes high even as style preferences evolve.

Rapid Product Innovations in Next-Generation Hyaluronic-Acid Fillers

Hybrid fillers that blend HA with calcium hydroxyapatite deliver both immediate plumpness and collagen stimulation.[3] B. Bravo et al., “Blending Hyaluronic Acid and Calcium Hydroxylapatite for Injectable Facial Dermal Fillers,” Cosmetics, mdpi.com Advanced cross-linking like NAHYCO enables integration into adipose tissue, reducing migration risk and touch-up frequency. Manufacturer control over molecular weight through microbial fermentation lets providers match viscosity to patient anatomy. Ready-to-use liquid formulations streamline chair time, allowing general dermatologists to enter the lip augmentation market. The result is wider access and sustained premium pricing.

Expanding Male Aesthetics Segment (Under-Penetrated Demographic)

Redefined masculinity and visual-centric careers have lifted male procedure volumes at a double-digit pace. Men favor discreet contouring rather than pronounced projection, prompting injector training on gender-specific anatomy. Targeted marketing highlights professional advantages and confidence gains rather than beauty. Higher willingness to pay for privacy and natural results boosts margins. As acceptance rises in Asia-Pacific, global share of male clients is expected to keep climbing over the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High procedure cost & limited reimbursement | -1.8% | Global, most acute in emerging markets | Medium term (2-4 years) |

| Adverse events and litigation risk | -1.2% | North America & Europe | Short term (≤2 years) |

| Intensifying regulatory scrutiny & product recalls | -0.9% | North America & Europe, moving into Asia-Pacific | Medium term (2-4 years) |

| HA supply-chain tightness and price volatility | -0.7% | Global, production centered in Asia-Pacific | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost and Limited Insurance Reimbursement

With price points between USD 600 and USD 1,500 per session, annual maintenance strains middle-income budgets. Absent insurance cover, demand tracks economic cycles, pushing some consumers toward lower-cost medical tourism hubs. Manufacturers counter by extending product longevity, yet affordability remains a ceiling on penetration, especially in Latin America and parts of Asia.

Adverse Events and Safety Concerns Leading to Litigations

One-third of recent filler complications reported to the FDA involved delayed issues such as nodules, fuelling malpractice claims. Rising insurance premiums increase provider costs, and media coverage of rare vascular accidents temporarily suppresses bookings. Counterfeit products and unqualified injectors exacerbate public fear, prompting calls for tighter licensing standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dermal Fillers Remain the Default Choice

Dermal fillers commanded 68.34% of the lip augmentation market share in 2024, highlighting practitioner confidence in their safety profile and the comfort patients derive from hyaluronidase reversibility. Fat injection, though still a smaller contributor, is set to expand at an 11.89% CAGR through 2030 as consumers seek autologous, regenerative benefits that combine body-contouring harvest with facial enhancement. Lip implants hold a niche for patients prioritizing permanence, yet concerns around revision complexity continue to temper adoption. Lip-plumping devices and topical serums draw cost-sensitive first-timers, but their fleeting results limit repeat uptake.

Combination protocols are now common; clinicians may inject HA for border definition and layer micro-fat for central volume, delivering immediate shape with longer-term tissue quality gains. Treatment selection increasingly considers downtime tolerance, budget and desired longevity rather than a simple injectable-versus-surgical divide. Product-specific training by manufacturers strengthens brand loyalty, particularly among high-volume clinics. As a result, dermal filler innovation—cross-linking chemistry, rheology optimization and lidocaine buffering—remains the primary competitive battlefield that keeps the lip augmentation market dynamic.

By Material: Hyaluronic Acid Dominance Meets Regenerative Aspirations

Hyaluronic-acid formulations accounted for 77.24% of the lip augmentation market size in 2024 thanks to proven biocompatibility, reversibility and modular viscosity ranges tailored to individual anatomy. Autologous fat, projected to climb at a 12.07% CAGR, appeals to patients seeking permanent fullness and collagen support rather than episodic top-ups. Collagen and bovine-derived fillers have largely ceded share following allergy scrutiny, while poly-L-lactic acid attracts users comfortable with gradual improvement over several months.

Late-entry permanent materials such as silicone and PMMA observe strict regulatory oversight, limiting them to specialist practices. Material choice is moving toward personalized matching: younger clients favor soft, moldable HA for subtle plumping, whereas mature clients often combine medium-G’ HA with nanofat to address perioral fine lines. Ongoing advances in microbial fermentation allow suppliers to fine-tune HA molecular weight, reinforcing their leadership even as regenerative options gain momentum.

By Procedure Type: Non-Invasive Techniques Drive Volume and Velocity

Non-invasive injections generated 81.22% of 2024 revenue and are forecast to expand at a 12.89% CAGR, underscoring patient preference for “walk-in, walk-out” solutions that suit busy work schedules. Procedure times now average under 30 minutes, with topical or local anesthesia minimizing discomfort. Follow-up visits every 12–18 months create a predictable annuity stream for clinics, while loyalty apps and reminder systems further improve retention.

Surgical augmentation retains relevance for anatomical challenges—cleft lip correction, significant asymmetry or prior implant revision—but a growing arsenal of minimally invasive tools is shrinking the candidate pool for invasive routes. Advancements in cannula design and ultrasound-guided injections continue to reduce bruising and arterial risk, reinforcing the dominance of needle-free or micro-needle approaches. Overall, the lip augmentation market pivots around convenience and safety, relegating surgery to a high-skill specialty corner.

By Gender: Male Participation Adds New Nuance

Women remained the core clientele at 89.34% in 2024, yet the male segment is advancing at a 10.34% CAGR as modern masculinity embraces subtle aesthetic upkeep. Men typically request linear vermillion definition and minimal projection, requiring injectors to adapt technique and product choice. Digital-first marketing that reframes treatments as professional grooming rather than cosmetic enhancement resonates strongly.

Clinics are redesigning waiting areas and consultation materials to feel gender-neutral, lowering psychological barriers that once deterred male bookings. The rise of non-binary identities is also encouraging practitioners to master a continuum of lip aesthetics that blend traditionally masculine and feminine ideals. Providers skilled in nuanced, low-visibility outcomes now enjoy a competitive edge and higher margins within the lip augmentation market.

By Age Group: Millennials Lead, Gen X Accelerates

Consumers aged 18–34 delivered 46.19% of global procedures in 2024, reflecting their comfort with social-media-driven beauty routines and willingness to experiment early. The 35–50 cohort, however, shows the fastest 10.67% CAGR as career visibility, divorce-driven reinvention and preventative aging strategies converge. For these clients, treatment protocols often shift from pure volumization to structural support that counters perioral collapse.

Baby boomers enter selectively, encouraged by safer products and regenerative options that promise discreet freshness rather than dramatic change. Across all ages, repeat visitation patterns are stabilizing around personalized maintenance schedules; clinics bundle lip fillers with skin boosters or neuromodulators, reinforcing a holistic approach. Age-specific marketing—youthful exuberance for millennials, professional vitality for Gen X—maximizes conversion in the lip augmentation market.

By End-User: Medical Spas Narrow the Gap with Clinics

Dermatology and cosmetic clinics captured 44.33% of procedures in 2024, leveraging board-certified expertise and robust complication management protocols. Yet medical spas are growing at an 11.47% CAGR, blending clinical oversight with luxury service touches that elevate the customer experience. Concierge booking apps, aromatherapy rooms and post-treatment gloss bars help spas convert first-timers into loyalists.

Hospitals and surgical centers remain critical for complex reconstructions and high-risk patients but account for a shrinking share of routine lip work. Mobile injectables teams and hybrid spa-clinic concepts further fragment the channel landscape, giving consumers unprecedented choice. Ultimately, providers that pair outcome reliability with elevated ambiance are capturing disproportionate wallet share within the lip augmentation market.

Geography Analysis

North America generated 36.48% of global revenue in 2024, backed by high disposable income and an entrenched aesthetic culture. The United States alone hosts dense networks of board-certified injectors, robust training pathways and strong brand loyalty among practitioners. Yet market maturity compresses margins and places a premium on product innovation and bundled service offerings. FDA oversight remains a double-edged sword; it safeguards safety but raises compliance costs that smaller players struggle to bear.

Asia-Pacific is forecast to record a 10.83% CAGR, the fastest worldwide. Rising middle-class populations, K-beauty influence and increased social-media exposure fuel uptake across China, South Korea and Southeast Asia. Medical tourism draws regional travelers to reputable hubs where procedure costs are lower than in Western markets. However, regulatory disparities require brand-by-brand clearance strategies, and cultural diversity means one-size-fits-all marketing falls flat.

Europe delivers steady but moderate growth as established injector skill sets and harmonized regulations ensure safety and access. Germany, France and the United Kingdom anchor innovation, championing natural-look philosophies that echo across the globe. Economic uncertainty and stringent advertising rules slow expansion in some Southern and Eastern markets, but continued demand for subtle enhancement keeps clinics busy. Cross-border professional education and product distribution support a pan-European ecosystem that sustains premium pricing.

Competitive Landscape

The lip augmentation market is moderately fragmented. Galderma, AbbVie’s Allergan Aesthetics and Merz Pharma headline the space, combining broad portfolios, global distribution and heavy R&D spend. Galderma posted USD 3.259 billion in net sales during the first nine months of 2024, with injectables up 10.6% year on year. AbbVie’s JUVÉDERM line and Merz’s BELOTERO range secure long-term clinician loyalty through continuous data generation and injector education.

Hybrid fillers like Allergan’s HArmonyCa, which merges HA and calcium hydroxyapatite, exemplify the shift to multi-benefit products that justify premium pricing. Mid-tier competitors pursue narrow niches such as vegan-based gels or AI-guided delivery systems. Some start-ups license novel cross-linking science but face capital constraints when navigating protracted regulatory approval.

Strategic moves include Evolus securing FDA approval for its Evolysse filler collection in February 2025, expanding a neuromodulator-centric portfolio into fillers. Galderma continues clinical programs for regenerative HA lines, while Merz invests in digital injector-support platforms. Heightened regulatory complexities drive selective M&A as smaller innovators seek the compliance infrastructure of larger groups.

Lip Augmentation Industry Leaders

Galderma SA

Merz Pharma

Teoxane Laboratories

Sinclair Pharma

Abbvie

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Biotech beauty brand Ourself released a redesigned Replenishing Lip Filler with patented TRV vesicle technology.

- February 2025: Evolus won FDA clearance for Evolysse Form and Evolysse Smooth injectable HA gels.

- March 2024: Allergan Aesthetics received FDA approval for JUVÉDERM VOLUMA XC to treat moderate to severe temple hollowing in adults.

Global Lip Augmentation Market Report Scope

| Dermal Fillers |

| Fat Injection (Autologous) |

| Lip Implants |

| Lip-Plumping Devices & Topicals |

| Hyaluronic Acid |

| Collagen & Bovine-Derived |

| Poly-L-Lactic Acid (PLLA) |

| Silicone |

| PMMA Microspheres |

| Autologous Fat |

| Non-Invasive / Minimally Invasive |

| Surgical / Invasive |

| Female |

| Male |

| Non-Binary |

| 18–34 Years |

| 35–50 Years |

| 51 Years & Above |

| Hospitals & Surgical Centers |

| Dermatology & Cosmetic Clinics |

| Medical Spas (MedSpas) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Dermal Fillers | |

| Fat Injection (Autologous) | ||

| Lip Implants | ||

| Lip-Plumping Devices & Topicals | ||

| By Material | Hyaluronic Acid | |

| Collagen & Bovine-Derived | ||

| Poly-L-Lactic Acid (PLLA) | ||

| Silicone | ||

| PMMA Microspheres | ||

| Autologous Fat | ||

| By Procedure Type | Non-Invasive / Minimally Invasive | |

| Surgical / Invasive | ||

| By Gender | Female | |

| Male | ||

| Non-Binary | ||

| By Age Group | 18–34 Years | |

| 35–50 Years | ||

| 51 Years & Above | ||

| By End-User | Hospitals & Surgical Centers | |

| Dermatology & Cosmetic Clinics | ||

| Medical Spas (MedSpas) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

1. What is the current value of the lip augmentation market?

The lip augmentation market size stands at USD 7.81 billion in 2025 and is projected to reach USD 11.48 billion by 2030.

2. Which product type leads the market?

Dermal fillers dominate with 68.34% share in 2024, favored for predictable outcomes and reversibility.

3. Which region is growing fastest?

Asia-Pacific shows the highest growth, set to advance at a 10.83% CAGR through 2030.

4. Why are male procedures increasing?

Changing masculinity norms and image-driven careers are pushing male participation, which is rising at a 10.34% CAGR.

5. How is technology improving patient consultations?

AI-powered 3-D visualization platforms simulate outcomes, helping patients set realistic expectations and reducing revision rates.

Page last updated on: