Subcutaneous Drug Delivery Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

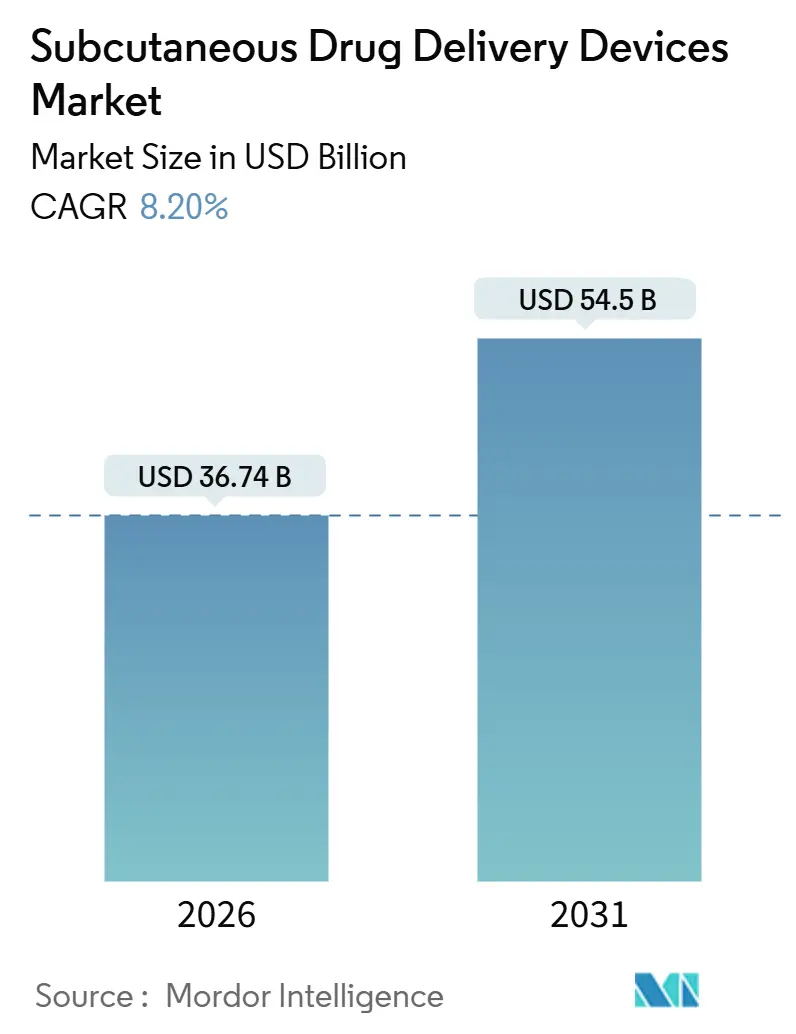

| Market Size (2026) | USD 36.74 Billion |

| Market Size (2031) | USD 54.5 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

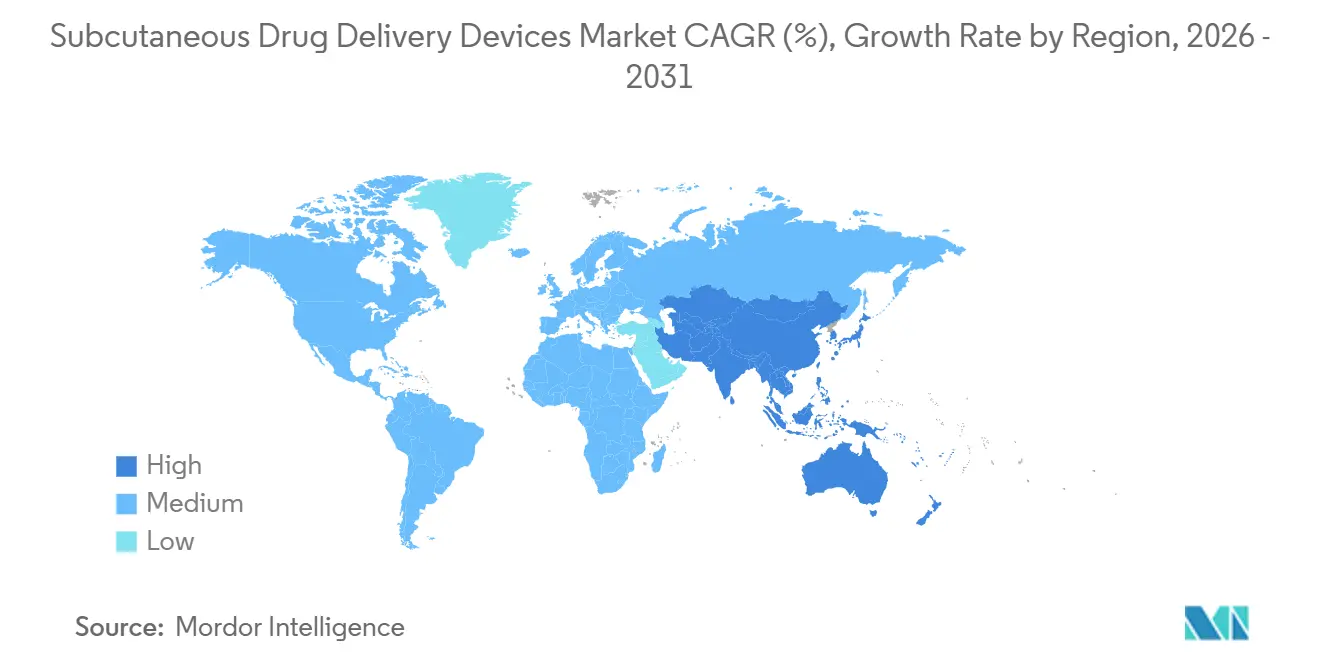

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subcutaneous Drug Delivery Devices Market Analysis by Mordor Intelligence

The Subcutaneous Drug Delivery Devices Market size is estimated at USD 36.74 billion in 2026, and is expected to reach USD 54.5 billion by 2031, at a CAGR of 8.20% during the forecast period (2026-2031).

Demand accelerates as biologics become the standard of care across chronic diseases, and regulators now accept hyaluronidase-enabled formulations that push subcutaneous volumes to 5-5.6 mL, once limited to intravenous infusion. Device makers are re-engineering platforms to handle viscosities above 20 centipoise and support 3-10-minute injection times, a shift that underpins rapid growth in wearable and connected injectors. Market expansion also reflects a worldwide pivot to home care: subcutaneous therapies administered at home cost 40%-60% less per dose than hospital infusions, after factoring in facility fees and nursing time[1]U.S. Food and Drug Administration, “FDA Approves Efgartigimod Alfa and Hyaluronidase-qvfc (VYVGART HYTRULO),” fda.gov . Heightened sustainability mandates in the European Union spur incremental adoption of reusable pens, while North American payers broaden coverage of GLP-1 receptor agonists for obesity and diabetes, reinforcing demand for high-accuracy pen injectors. Asia-Pacific offers the fastest regional upside as China, Japan, and India streamline device approvals and risk-based classifications, creating a fertile landscape for domestic low-cost platforms that can bypass cold-chain constraints.

Key Report Takeaways

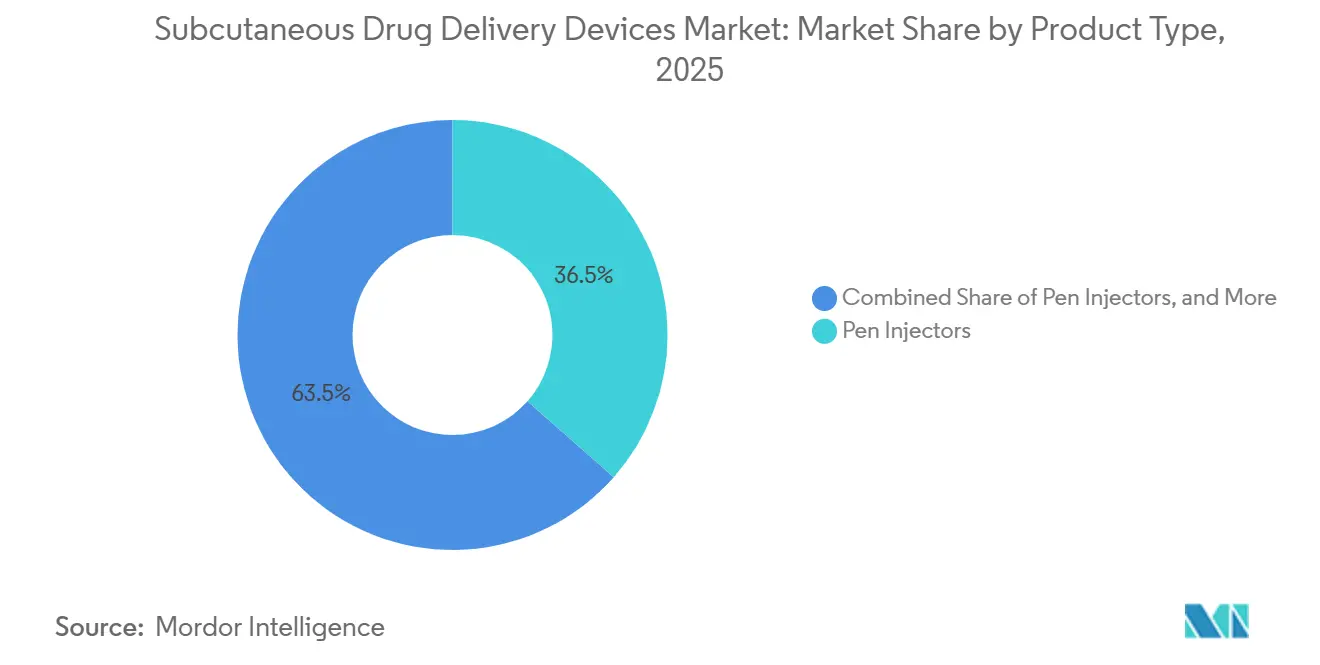

- By product type, pen injectors led with 36.55% of the subcutaneous drug delivery devices market share in 2025; wearable injectors are forecast to expand at a 14.25% CAGR through 2031.

- By usability, disposable formats accounted for 65.53% of the subcutaneous drug delivery devices market in 2025, while reusable devices are projected to grow at a 9.85% CAGR to 2031.

- By therapy area, diabetes accounted for 68.23% of revenue share in 2025, and autoimmune disorders will grow fastest at a 15.55% CAGR through 2031.

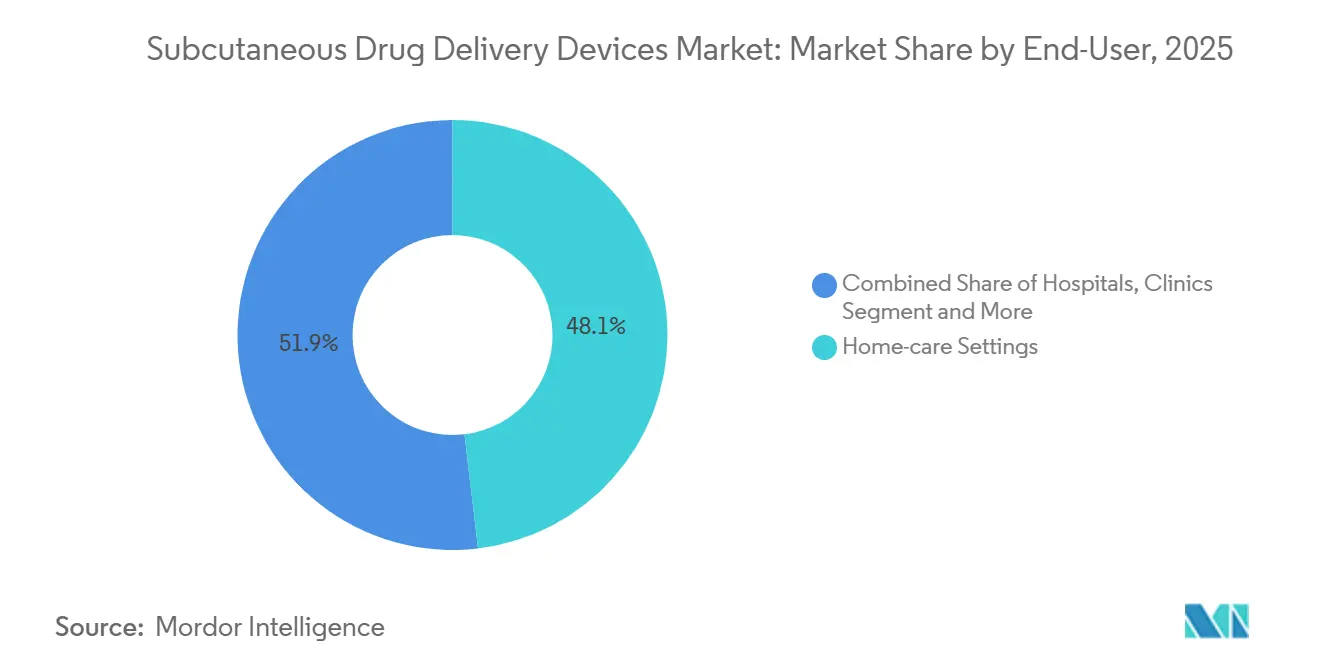

- By end user, the home-care segment held 48.13% share in 2025; clinics are advancing at a 10.81% CAGR between 2026 and 2031.

- By geography, North America captured 47.13% of the subcutaneous drug delivery devices market share in 2025, whereas Asia-Pacific is poised to grow at a 10.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Subcutaneous Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Chronic-Disease Prevalence (Diabetes, Autoimmune) | +2.1% | Global, with concentration in APAC (India, China) and MEA | Long term (≥ 4 years) |

| Shift Toward Home-Care and Self-Administration | +1.8% | North America and Europe, expanding to urban APAC | Medium term (2-4 years) |

| Rising Adoption of Biologics Suited to SC Delivery | +1.5% | North America, Europe, Japan | Medium term (2-4 years) |

| Rapid Innovation in Wearable and Connected Injectors | +1.3% | North America, Western Europe, Australia | Short term (≤ 2 years) |

| Pipeline of High-Viscosity, >3 Ml Biologics Spurring Device Redesign | +0.9% | North America, Europe | Medium term (2-4 years) |

| Sustainability Mandates Driving Reusable/Eco-Friendly Formats | +0.6% | European Union, select North American markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Chronic-Disease Prevalence

A 2024 global study recorded 828 million adults with diabetes but found 445 million remained untreated, revealing a vast care gap concentrated in India, China, Pakistan, and Indonesia. That unmet need fuels demand for pen injectors tolerant of ambient storage and intuitive enough for patients with limited health literacy. Autoimmune conditions add 18 million rheumatoid arthritis and 125 million psoriasis cases, many now shifting from intravenous infusions to weekly or biweekly subcutaneous biologics administered at home[2]World Health Organization, “Rheumatoid Arthritis Fact Sheet,” who.int. Devices must handle formulations above 50 mg/mL while maintaining injection forces below 30 Newtons to preserve comfort, prompting alignment with ISO 11608-1:2022 dose-accuracy requirements.

Shift Toward Home-Care and Self-Administration

The United Kingdom earmarked GBP 2.5 billion to roll out hybrid closed-loop insulin systems nationwide beginning in April 2024, reflecting evidence that home-based subcutaneous therapy can cut administration costs by as much as 60% per dose and raise patient satisfaction by 20-30 points. In August 2024, the FDA cleared the Omnipod 5 for Type 2 diabetes, opening automated insulin delivery to more than 30 million U.S. adults. Telehealth integration lets clinicians titrate doses remotely, halving clinic visits during the first treatment year. Yet emerging markets grapple with limited educator resources and needle phobia among up to 30% of patients, reinforcing the value of user-friendly interfaces and multilingual instructions.

Rising Adoption of Biologics Suited to SC Delivery

Between 2024 and 2025, the FDA approved seven subcutaneous biologics, including adalimumab and ustekinumab biosimilars, lebrikizumab for atopic dermatitis, and high-volume efgartigimod alfa with hyaluronidase, broadening demand beyond diabetes and rheumatology. Hyaluronidase co-formulation enables 5-5.6 mL injections delivered in under 10 minutes, reshaping device design toward larger-bore needles and controlled plunger kinetics. Biosimilar competition drives prices down 30%-50%, improving payer willingness to fund adherence-enhancing auto-injectors. The oncology field followed when atezolizumab earned subcutaneous approval for non-small cell lung cancer, cutting chair time from an hour to seven minutes

Rapid Innovation in Wearable and Connected Injectors

The Omnipod 5 pairs a tubeless pump with SmartAdjust algorithms that adapt basal insulin every five minutes, boosting time-in-range by 15-20 points relative to multiple daily injections. Enable Injections’ enFuse delivers up to 10 mL of viscous biologics over 3-10 minutes and confirms dose completion via on-body sensors. Medtronic’s Simplera CGM integrates the transmitter into a single disposable component, trimming insertion steps and manufacturing cost. Regulators now craft guidance for software-as-a-medical-device, creating new compliance hurdles yet positioning connectivity as a competitive differentiator.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Device Cost and Reimbursement Uncertainty | -0.8% | Global, acute in emerging APAC and MEA markets | Medium term (2-4 years) |

| Stringent Drug-Device Combination Regulations | -0.5% | North America, Europe, Japan | Short term (≤ 2 years) |

| Needle-Phobia and Limited Training in Emerging Markets | -0.4% | APAC (ex-Japan), MEA, Latin America | Long term (≥ 4 years) |

| Polymer-Protein Compatibility Issues with Next-Gen Biologics | -0.3% | Global, concentrated in high-viscosity formulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Device Cost and Reimbursement Uncertainty

Wearable injectors priced at USD 200-400 each remain unaffordable where out-of-pocket spending dominates, including India and Nigeria. U.S. payers impose prior authorization for biologics costing more than USD 10,000 annually, reducing first-year uptake by up to 40%. Germany’s G-BA frequently rates new drug-device combinations as having “no additional benefit,” anchoring reimbursement at reference levels. At the same time, NICE in the U.K. rejects auto-injector premiums that fail strict cost-utility thresholds. Emerging markets, lacking centralized health technology assessment, default to budget impact, skewing purchases toward low-cost syringes.

Stringent Drug-Device Combination Regulations

The FDA draft guidance released in June 2024 requires stability data under simulated-use stress, potentially extending development timelines by up to 18 months. Europe’s MDR 2017/745 elevates auto-injectors to Class III, yet notified-body capacity remains limited and approval backlogs stretch to 18 months[3]European Union, “Regulation (EU) 2017/745 on Medical Devices,” eur-lex.europa.eu . ISO 11608-1:2022 requires dose accuracy within ±5% for volumes of 0.5 mL or more, requiring validation for 95th-percentile elderly users. Compliance costs climb by USD 50,000-100,000 per variant due to expanded biocompatibility testing.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Wearables Redefine Chronic-Care Delivery

Wearable injectors will expand at 14.25% CAGR through 2031, outpacing all other product types as patch pumps remove manual steps and synchronize with continuous glucose monitors. This segment’s rise, underscored by Omnipod 5's 2024 authorization, highlights how closed-loop algorithms can drive double-digit gains in adherence. Pen injectors, while still capturing 36.55% of 2025 revenue, remain critical in emerging markets where per-dose costs fall below USD 1. The subcutaneous drug delivery devices market size for pen injectors continues to grow, fueled by biosimilar uptake in rheumatology and dermatology. Auto-injectors fill the middle ground, masking needle visibility and completing injections under ten seconds, a feature valued by needle-averse patients. Prefilled syringes retain hospital loyalty for dose flexibility but lack the convenience of self-administration.

Connected wearables integrate Bluetooth Low Energy chips that transmit dose-completion time stamps to electronic health records, enabling physicians to intervene when adherence lapses. Enable Injections’ enFuse addresses high-viscosity, high-volume biologics exceeding 50 centipoise, a limitation of legacy auto-injectors. Needle-free injectors, despite addressing trypanophobia, face formulation constraints, restricting their widespread use. Pen and pump makers are redesigning barrels and springs to manage 5-5.6 mL injections without exceeding 30 Newtons activation force, aligning with ISO 11608-6:2022 targets.

By Usability: Disposables Dominate, Reusables Gain Sustainability Traction

Disposables accounted for 65.53% of revenue in 2025 due to hospitals' preference for infection control and simplified inventory. Nevertheless, reusable platforms will register a 9.85% CAGR to 2031 as the European Union pressures manufacturers under the Single-Use Plastics Directive to justify disposability. Subcutaneous drug delivery devices market share for reusables will rise in Europe, driven by carbon-reduction targets from Becton, Dickinson & Company and national take-back schemes. The subcutaneous drug delivery devices market for reusable pens could grow as warranty programs extend device life to 730 injections, meeting durability benchmarks.

Lifecycle assessments reveal that reusable insulin pens emit half the carbon of disposable syringes across five years, yet only if cleaning compliance is high. Patient concerns about contamination drive demand for single-use needles and alcohol wipes bundled with reusable devices. Disposable wearable injectors, such as West’s SmartDose, create up to 100 grams of waste per administration, prompting pilot recycling partnerships with specialty waste handlers. Glass syringe expansion by Gerresheimer underscores recyclability advantages. However, breakage rates add hidden logistics costs.

By Therapy Area: Diabetes Leads, Autoimmune Surges

Diabetes generated 68.23% of 2025 revenue, supported by 828 million adults living with the condition and a vast, untreated cohort that now seeks affordable pens and patch pumps. The United Kingdom’s five-year hybrid closed-loop program illustrates public-payer confidence in home-based insulin delivery. Autoimmune disorders will post the fastest 15.55% CAGR, as subcutaneous tumor necrosis factor and interleukin inhibitors compress infusion times from 2 hours to under 5 minutes, improving patient convenience. The subcutaneous drug delivery devices market for autoimmune therapies is driven by biosimilar entry, which slashes prices and facilitates auto-injector adoption.

Oncology’s momentum stems from atezolizumab’s seven-minute subcutaneous dosing, freeing chair capacity for complex infusions. Cardiovascular use cases, such as twice-yearly inclisiran, underscore the breadth of chronic diseases now amenable to subcutaneous delivery once volume and viscosity barriers are overcome. Pediatric growth-hormone deficiency patients benefit from needle-free devices and microneedle patches that cut pain and improve adherence.

By End User: Home-Care Ascends, Clinics Capture Supervised Starts

Home care secured 48.13% of revenue in 2025 as telehealth matured and payers quantified 40%-60% dose-level savings compared with hospital infusions. The subcutaneous drug delivery devices market continues shifting toward domiciliary use, driven by connected injectors that automate adherence reminders and trigger refill logistics. Clinics will grow at a 10.81% CAGR by providing first-dose observation for high-risk biologics and serving patients with limited motor skills for self-injection. Hospitals reserve complex titration and adverse-event monitoring, especially in oncology and hematology.

Remote data feeds from Omnipod 5 let endocrinologists adjust basal rates without in-person visits, cutting annual patient travel costs by up to USD 1,000 in rural U.S. areas. European insurers now reimburse continuous glucose monitoring sensors, expanding pump adoption across income levels. Emerging-market training initiatives improved injection accuracy and slashed sharps-disposal errors, yet rely on community health worker funding.

Geography Analysis

North America accounted for 47.13% of 2025 revenue, as Medicare Part D added GLP-1 receptor agonists for obesity and diabetes, spurring pen-injector volume. ISO 11608-1:2022 recognition simplified FDA filings for next-gen injectors. Nonetheless, 70% of U.S. payers apply prior authorization on high-cost biologics, tempering first-year adoption. Canada’s pan-Canadian Pharmaceutical Alliance leverages pooled purchasing to secure 40%-60% discounts on biosimilars, facilitating auto-injector coverage. Mexico expanded public-sector benefits for insulin analogs, but home-care devices remain primarily accessible to privately insured urban patients.

Asia-Pacific will post the fastest CAGR of 10.52%, as China accelerates device approvals, Japan extends the Sakigake designation to connected pumps, and India enforces risk-based rules under MDR 2017. Untreated diabetes populations of 133 million in India and 78 million in China fuel demand for low-cost, battery-free pens tolerant of supply-chain heat stress. Japan’s universal coverage of closed-loop systems doubled the eligible Type 1 cohort to 120,000 by 2025, lifting patch-pump shipments. Australia’s Pharmaceutical Benefits Scheme slashed co-pays on biosimilar auto-injectors to USD 5, improving adherence by 20-25 points.

Europe’s heterogeneous reimbursement slows launches by 12-24 months post-CE mark. Germany’s G-BA often denies “additional benefit,” capping drug-device pricing. NICE enforces strict GBP 20,000-30,000 per QALY thresholds, rejecting three rheumatology auto-injector bids in 2024-2025. France’s HAS requires real-world adherence evidence, a burden smaller firms struggle to meet. The EU Medical Device Regulation raises clinical evidence demands, while notified-body bottlenecks delay Class III approvals. Elsewhere, Middle East, Africa, and Latin America contribute 15%-20% of global revenue, with private insurance and donor programs underwriting premium devices in urban centers, while rural users rely on reusable syringes.

Competitive Landscape

The subcutaneous drug delivery devices market is moderately consolidated. The top suppliers, Becton, Dickinson & Company, Novo Nordisk, Eli Lilly, and others, accounted for a significant share of 2025 revenue. Yet, specialized niches such as high-viscosity wearables remain contested by contract-manufacturing innovators. Vertical integration lets Novo Nordisk and Eli Lilly bundle insulin analogs with proprietary pens, safeguarding margins and ensuring formulation compatibility. West Pharmaceutical’s SmartDose achieved 15 pharma partnerships by 2024, proving that platform suppliers can displace in-house R&D. Enable Injections’ enFuse targets large-volume biologics beyond traditional auto-injector capacity, landing oncology collaborations.

Smaller entrants CeQur, Subcuject, and Owen Mumford address focused pain points, such as three-day basal insulin or reusable auto-injectors for biosimilars, but confront financing and regulatory resource gaps. Patent activity surged in 2024-2025 around closed-loop algorithms and micro-needle arrays; Medtronic filed 12 U.S. patents for glucose-responsive dosing, while Insulet secured eight for tubeless pump architecture. Incumbents benefit from 510(k) clearance pathways that reduce trial size to human-factors studies, trimming development time by up to 18 months.

Subcutaneous Drug Delivery Devices Industry Leaders

Amgen Inc.

Becton, Dickinson and Company

Eli Lilly and Company

Medtronic plc

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Datwyler, LTS Device Technologies, and Stevanato Group announced a three-way collaboration to advance large-volume on-body injectors for subcutaneous biologic delivery.

- July 2025: Becton, Dickinson and Company initiated the first pharma-sponsored clinical trial using its BD Libertas wearable injector for complex biologics.

Global Subcutaneous Drug Delivery Devices Market Report Scope

As per the report's scope, subcutaneous drug delivery devices are medical devices designed to administer medications into the subcutaneous tissue, the layer of fat just beneath the skin. These devices enable controlled and accurate delivery of drugs, particularly biologics and long-term therapies such as insulin, hormones, and monoclonal antibodies. Standard formats include prefilled syringes, pen injectors, auto-injectors, and wearable injectors. They are widely used for self-administration, improving patient convenience, adherence, and treatment outcomes.

The subcutaneous drug delivery devices market is segmented by product type, usability, therapy area, end user, and geography. By product type, the market is segmented into prefilled syringes, pen injectors, auto-injectors, wearable injectors, and needle-free injectors. By usability, the market is segmented into disposable devices and reusable devices. By therapy area, the market is segmented into diabetes, oncology, autoimmune disorders, cardiovascular diseases, and others. By end user, the market is segmented into hospitals, home care settings, clinics, and others. By geography, the global market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Prefilled Syringes |

| Pen Injectors |

| Auto-Injectors |

| Wearable Injectors |

| Needle-Free Injectors |

| Disposable Devices |

| Re-usable Devices |

| Diabetes |

| Oncology |

| Autoimmune Disorders |

| Cardiovascular Diseases |

| Others |

| Hospitals |

| Home-care Settings |

| Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Prefilled Syringes | |

| Pen Injectors | ||

| Auto-Injectors | ||

| Wearable Injectors | ||

| Needle-Free Injectors | ||

| By Usability | Disposable Devices | |

| Re-usable Devices | ||

| By Therapy Area | Diabetes | |

| Oncology | ||

| Autoimmune Disorders | ||

| Cardiovascular Diseases | ||

| Others | ||

| By End-User | Hospitals | |

| Home-care Settings | ||

| Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big is the subcutaneous drug delivery devices market in 2026?

The market stands at USD 36.74 billion in 2026 and is projected to expand at an 8.20% CAGR to USD 54.50 billion by 2031.

Which product type is growing fastest within subcutaneous drug delivery?

Wearable injectors are forecast to post the highest 14.25% CAGR through 2031 as patch-pump designs gain traction in diabetes and biologic therapy.

Why does Asia-Pacific show the strongest regional growth?

Streamlined regulatory pathways in China, Japan, and India, combined with large untreated diabetes populations and lower-cost reusable pen demand, drive a 10.52% CAGR for the region.

What is the main barrier to adoption of wearable injectors?

High device cost and fragmented reimbursement—wearables can cost USD 200-400 each, and many payers require prior authorization before coverage.

How are sustainability goals influencing device design?

EU single-use directives and corporate net-zero targets push manufacturers toward reusable pens and plastic-light designs, with some platforms cutting plastic waste by 70%.

Which therapy area will grow fastest after diabetes?

Autoimmune disorders will expand at a 15.55% CAGR as subcutaneous biologics for rheumatoid arthritis, psoriasis, and atopic dermatitis replace lengthy infusions.

Page last updated on: