Liposome Drug Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

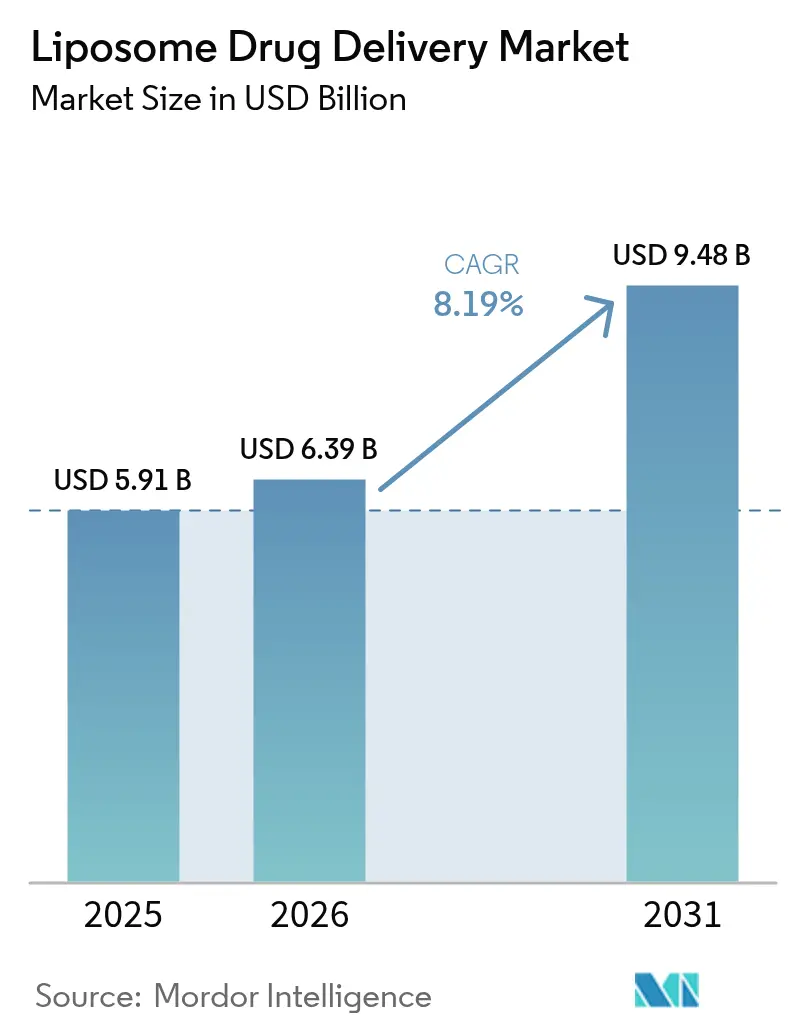

| Market Size (2026) | USD 6.39 Billion |

| Market Size (2031) | USD 9.48 Billion |

| Growth Rate (2026 - 2031) | 8.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Liposome Drug Delivery Market Analysis by Mordor Intelligence

liposome drug delivery market size in 2026 is estimated at USD 6.39 billion, growing from 2025 value of USD 5.91 billion with 2031 projections showing USD 9.48 billion, growing at 8.19% CAGR over 2026-2031. This growth path shows how the liposome drug delivery market has evolved beyond niche oncology use into broader applications, including viral vaccines, pain control, and respiratory therapy. Regulatory agencies show greater willingness to license complex nanomedicines, which shortens approval timelines and lowers perceived risk. Demand also gains from the proven safety bias of liposomal formulations relative to free‐drug alternatives, an advantage actively promoted by clinicians as they look to reduce organ toxicity. Manufacturing scale-up remains costly, yet newer continuous processes are trimming production time, which supports competitive pricing and wider access in cost-sensitive regions.

Key Report Takeaways

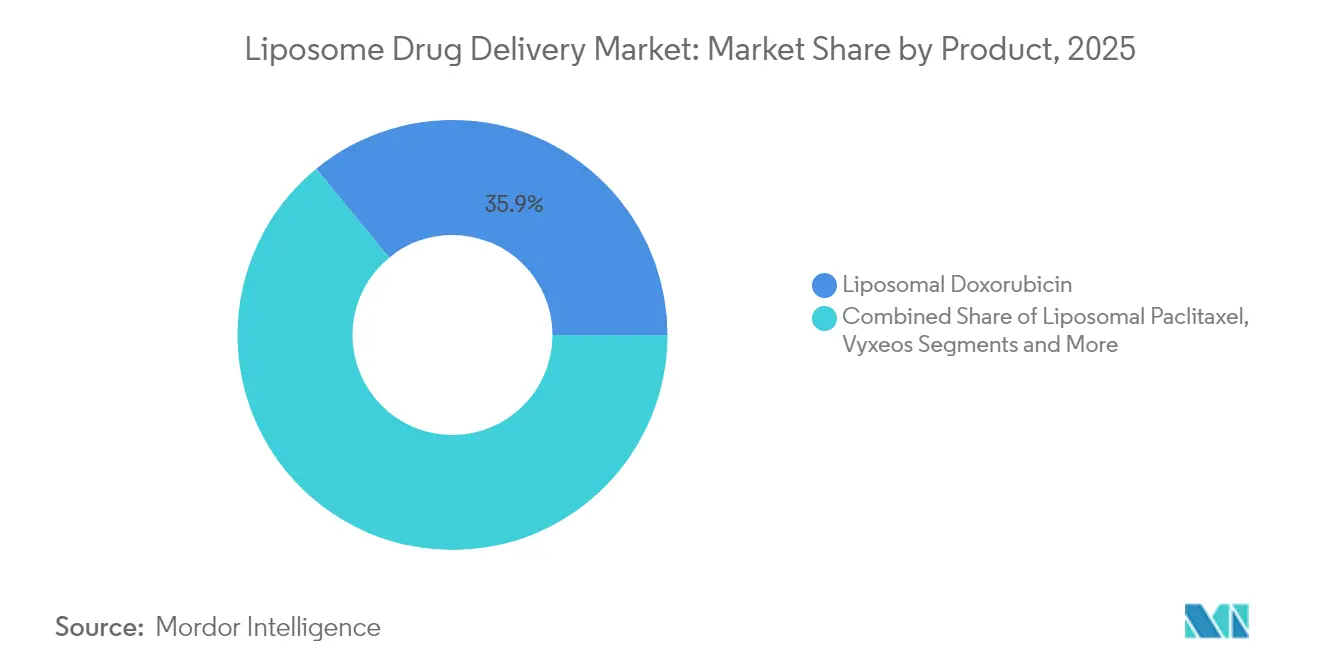

- By product type, liposomal doxorubicin led with 35.92% of the liposome drug delivery market share in 2025, while liposomal paclitaxel posted the fastest 11.09% CAGR to 2031.

- By technology, PEGylated stealth systems held 60.65% share of the liposome drug delivery market in 2025; cubosome-based lipid nanoparticles are advancing at a 10.42% CAGR through 2031.

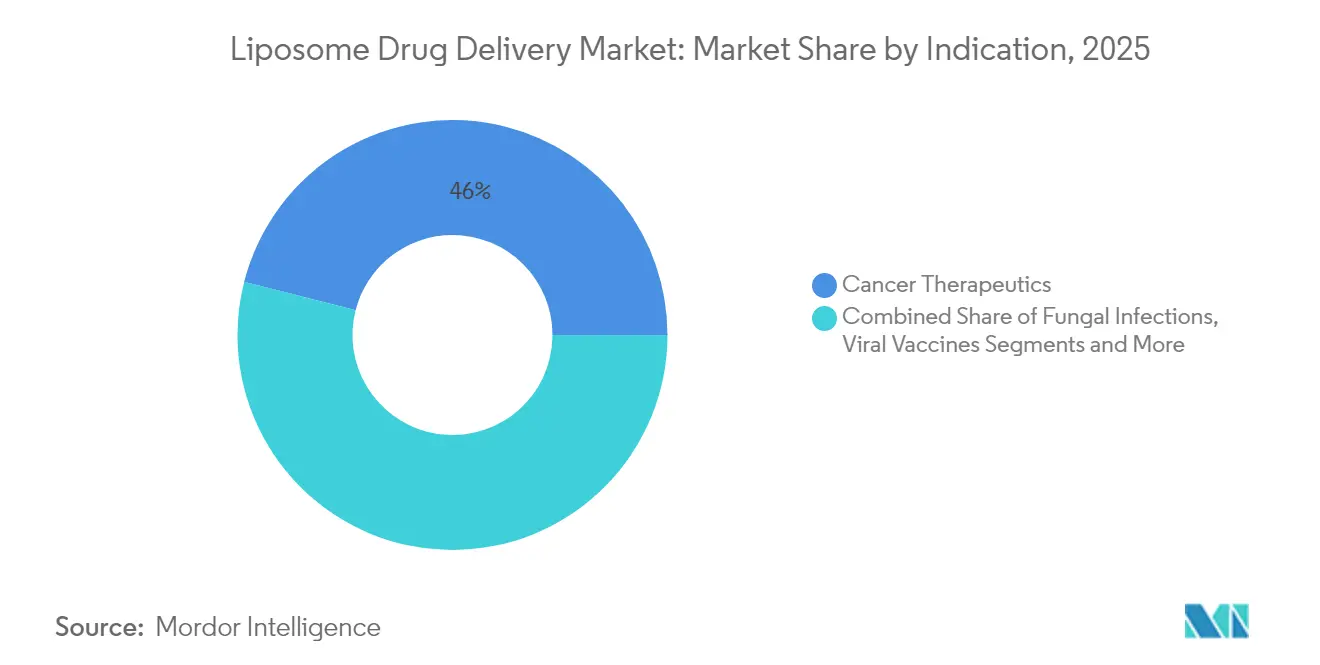

- By indication, cancer therapeutics captured 46.02% of the liposome drug delivery market size in 2025, whereas viral vaccines record the highest 10.95% CAGR toward 2031.

- By route of administration, intravenous delivery accounted for 74.60% of the liposome drug delivery market in 2025, and pulmonary delivery is growing at 10.21% CAGR.

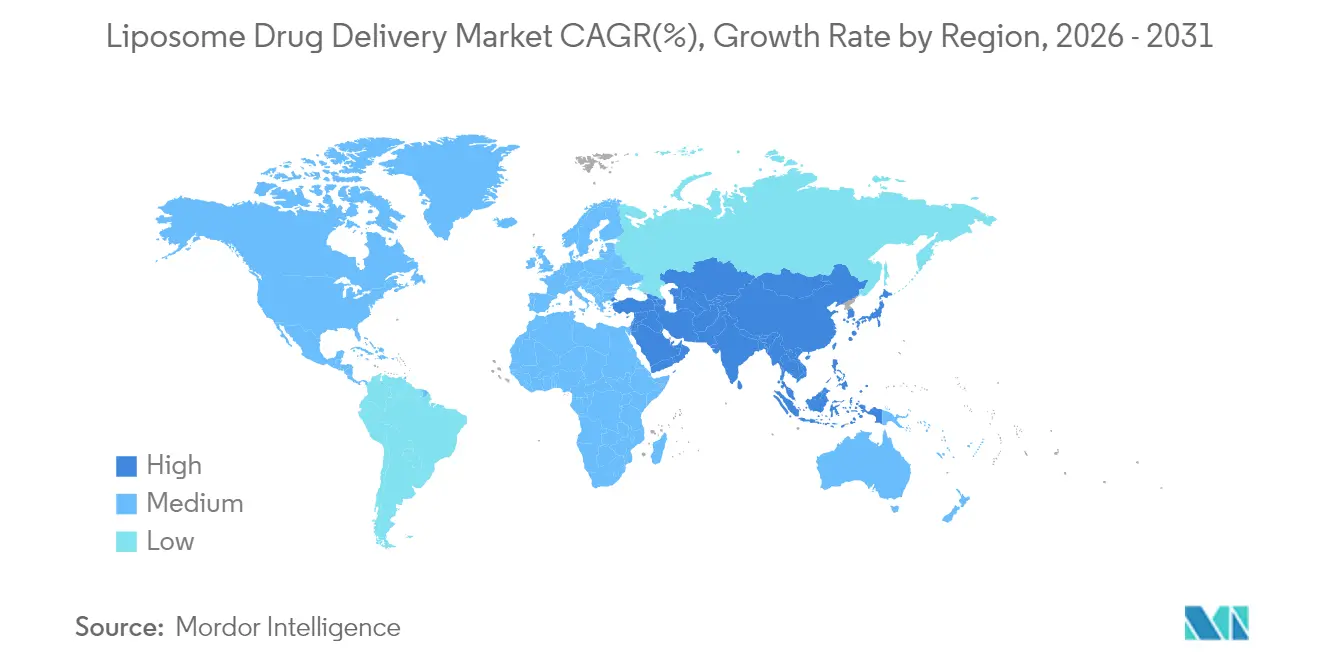

- By geography, North America commanded 40.78% share of the liposome drug delivery market in 2025, while Asia-Pacific is projected to expand at an 10.57% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Liposome Drug Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of cancer & fungal infections | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Proven safety bias vs. conventional formulations | +1.8% | Global regulated markets | Medium term (2-4 years) |

| Rapid adoption of PEGylation & stealth technologies | +1.4% | North America, EU expanding to APAC | Medium term (2-4 years) |

| Expiring patents pushing liposomal reformulations | +1.2% | North America first, global later | Short term (≤ 2 years) |

| Cubosome & other non-spherical LNPs boosting uptake | +0.9% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| AI/ML-guided lipid composition optimisation | +0.7% | North America, EU, emerging APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Cancer & Fungal Infections

Cancer incidence keeps the liposome drug delivery market growing, as targeted liposomes concentrate chemotherapies at tumor sites and reduce systemic toxicity. Pegylated liposomal doxorubicin retains circulation for 55 hours, versus under 10 minutes for free doxorubicin.[1]Alberto Gabizon, “Thirty Years From FDA Approval of Pegylated Liposomal Doxorubicin,” BMJ Oncology, bmjoncology.bmj.com Fungal infections in immunocompromised populations also favor liposomal amphotericin B, which lowers nephrotoxicity yet maintains antifungal strength.[2]Marina Santiago Franco, “Triggered Drug Release From Liposomes: Exploiting the Tumor Environment,” ncbi.nlm.nih.govThese two high-burden disease groups anchor long-term volume growth and underwrite pipeline investment.

Proven Safety Bias vs. Conventional Formulations

Regulators approve liposomal versions more readily as data accumulate showing longer overall survival and lower severe toxicities. The FDA’s 2024 irinotecan liposome decision illustrates the accepted benefit-risk profile, with median survival of 11.1 months versus 9.2 months for standard therapy.[3]Center for Drug Evaluation and Research, “FDA Approves Irinotecan Liposome for First-Line Treatment of Metastatic Pancreatic Adenocarcinoma,” fda.gov Physicians now prescribe many liposomal drugs first line, boosting demand and reinforcing a virtuous safety-perception cycle.

Rapid Adoption of PEGylation & Stealth Technologies

PEGylation confers stealth that minimizes macrophage clearance, sustaining product efficacy and shaping the liposome drug delivery market. Yet anti-PEG antibodies appear in up to 10% of patients, prompting companies to trial ganglioside-modified or other coatings to hold efficacy and curb immunogenicity. R&D spend flows into new polymer and lipid chemistries rather than abandoning the stealth principle.

Expiring Patents Pushing Liposomal Reformulations

Patent cliffs open space for reformulated liposomal versions that secure fresh intellectual property. Bioequivalence guidance for liposomes is strict, effectively raising entry barriers for simple generics and favoring branded lifecycle-management tactics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent CMC & sterility regulations | -1.5% | North America, EU | Medium term (2-4 years) |

| High manufacturing CAPEX & scale-up complexity | -1.2% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Short shelf-life & cold-chain dependence | -0.8% | Tropical regions worldwide | Medium term (2-4 years) |

| Anti-PEG antibody–driven hypersensitivity events | -0.6% | Developed markets with high PEG exposure | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent CMC & Sterility Regulations

The FDA demands full particle-size, encapsulation, and release-profile datasets, which stretch timelines and budgets. Aseptic processing adds cost because liposomes cannot tolerate terminal sterilization. Smaller firms often lack the analytic platforms and GMP suites needed for compliance, leaving the liposome drug delivery market weighted toward large incumbents.

Anti-PEG Antibody–Driven Hypersensitivity Events

Pre-existing and therapy-induced anti-PEG antibodies accelerate blood clearance and can trigger complement activation, lowering efficacy and risking acute reactions. Screening and desensitisation protocols raise clinical overheads, and some chronic indications move toward non-PEG stealth systems to avoid repeat-dose complications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Doxorubicin Leadership Faces Paclitaxel Challenge

The liposome drug delivery market size for liposomal doxorubicin reached USD 2.12 billion in 2025, equal to 35.92% of total revenue. Its long record of reduced cardiotoxicity keeps the brand entrenched, especially in ovarian cancer and multiple myeloma. Recent hyperthermia-triggered variants raise local drug release without altering systemic profiles, sustaining clinical relevance. Liposomal paclitaxel posted the quickest 11.09% CAGR as solid tumor treatment centers adopt the nanoformulation to avoid Cremophor-related hypersensitivity. Amphotericin B liposomes hold stable infectious-disease demand, and newly approved irinotecan liposome presents a fresh first-line option for metastatic pancreatic cancer. Pipeline candidates bundle cytotoxics inside temperature-sensitive vesicles, aiming to combine high loading (89.5% encapsulation) with on-demand release.

Ongoing reformulation programs extend patent life for mature chemotherapies and avert pricing erosion. The liposome drug delivery market therefore remains dominated by cancer care, yet formulators are experimenting with antimicrobial dual-payload liposomes to slow resistance growth. Growth rates suggest paclitaxel liposomes may nudge doxorubicin from the top spot beyond 2030 if current uptake persists.

By Technology: PEGylation Dominance Under Immunogenicity Pressure

The liposome drug delivery market saw PEGylated stealth coatings account for 60.65% revenue in 2025, capitalizing on three decades of safety data and well-characterised GMP methods. Yet clinicians grow cautious after hypersensitivity case series, so manufacturers are pivoting to ganglioside or zwitterionic alternatives that evade complement activation. Cubosome-based LNPs, advancing at 10.42% CAGR, promise superior endosomal escape and gene-editing payload delivery.

DepoFoam multivesicular structures deliver bupivacaine for up to 96 hours, proving controlled-release value in post-surgical pain. Continuous-flow manufacture emerges as a cost lever, and AI selects lipid ratios that cut batch variability. Over the forecast, tech mix will likely rebalance in favor of cubosomes and other advanced particles, though PEGylation remains the commercial workhorse for large-volume oncology brands.

By Indication: Cancer Dominance Challenged by Viral Vaccine Acceleration

Cancer care contributed 46.02% of the liposome drug delivery market size in 2025, as liposomes exploit tumor microvascular leakiness to raise local drug concentration. Multidrug liposome Vyxeos reshapes acute myeloid leukemia therapy by synchronously delivering daunorubicin and cytarabine, and similar combination designs populate the late-stage pipeline. Viral vaccines, led by mRNA–lipid nanoparticle technology, show the fastest 10.95% CAGR because the COVID-19 experience validated rapid, scalable production.

Pain management indications gain share via DepoFoam bupivacaine that holds analgesia through 96 hours, reducing opioid need. Fungal infections remain a niche yet stable segment. CNS applications lag because blood–brain barrier penetration is difficult, but early data using glutathione-coated liposomes are encouraging for Parkinson’s and glioblastoma trials.

By Route of Administration: IV Dominance Faces Pulmonary Innovation

Intravenous delivery made up 74.60% of liposome drug delivery market revenue in 2025, supported by precise dosing control and oncology’s reliance on infusion centers. However, pulmonic administration posts a 10.21% CAGR as deep-lung deposition tools mature and asthma therapy gains 18-hour drug residence with nanoliposomal salbutamol. Ocular and topical routes benefit dermatology and ophthalmology pipelines that demand longer residence and skin penetration.

Reformulated inhalable liposomal antibiotics may soon enter cystic-fibrosis care, and dry-powder devices extend shelf life in tropical markets, easing cold-chain burdens. Intrathecal and intraventricular dosing hold small but vital roles in CNS oncology.

Geography Analysis

North America represented 40.78% of the liposome drug delivery market in 2025 on the strength of reimbursement parity for nanomedicines and deep clinical trial networks. The approval pathway remains predictable, letting innovators price at a premium when they can prove toxicity savings or extended survival. Manufacturers invest heavily in U.S. continuous-manufacturing suites to secure on-shore supply and satisfy rising political pressure for domestic production.

Europe maintains robust adoption as EMA procedures allow centralized marketing authorizations that cover 27 states. Germany, France, and the United Kingdom champion specialist oncology centers piloting combination liposome regimens. EU policy also funds Horizon Europe grants aimed at cold-chain-free lipid nanoparticle vaccines, smoothing path to scale once technical milestones clear.

Asia-Pacific achieves the fastest 10.57% CAGR to 2031. China’s contract development organizations align with multinational sponsors to produce GMP batches at lower cost, while Singapore and South Korea subsidize advanced therapy manufacturing parks. Local incidence of stomach, liver, and lung cancers fuels demand, and healthcare access expands via public-private insurance plans. India and Indonesia focus on generic liposomal anticancer drugs after expiries, anchoring regional volume growth.

Latin America and the Middle East & Africa show slower uptake because of shorter reimbursement lists and weaker cold-chain logistics. Nonetheless, Gulf Cooperation Council states pilot targeted oncology centers adopting irinotecan liposome. Brazil explores public–private partnerships to lease continuous-flow lines and slash import costs, and South Africa tests inhalable liposomal TB therapy at academic centers.

Competitive Landscape

The liposome drug delivery market is moderately concentrated. Gilead Sciences holds entrenched share through AmBisome and developing long-acting HIV lenacapavir liposomes. Pacira BioSciences leverages its multivesicular DepoFoam platform and hit USD 675 million sales in 2023, reinvesting into osteoarthritis programs. Ipsen pushes Onivyde into front-line metastatic pancreatic cancer, and Spectrum Pharmaceuticals commercialises poziotinib inside stealth vesicles for EGFR exon 20 insertions.

Strategic moves focus on platform reuse: single lipid chemistries can support multiple payloads, raising R&D efficiency. Continuous-flow microfluidics in pilot plants cut batch time from hours to minutes, and leaders file patents to protect device-process combinations. Partnerships between big pharma and AI start-ups accelerate pre-formulation screening, shortening candidate nomination by several months.

Challengers differentiate via cubosomes that promise eight-fold higher uptake and broaden IP space. Most license from academic institutes in Australia and China, aiming at mRNA cancer vaccines. Smaller U.S. firms pursue galactose-targeted liposomes for hepatocellular carcinoma. Overall, barriers stay high because GMP lipid sourcing, aseptic-filling, and sterility validation require capital and know-how, keeping the playing field tilted toward incumbents.

Liposome Drug Delivery Industry Leaders

Gilead Sciences, Inc.

Pacira BioSciences, Inc.

Luye Pharma Group

Johnson and Johnson

Ispen

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: China Medical University Hospital and Shine-On Biomedical unveiled SOB100, the first HLA-G–targeted exosome platform, with FDA Phase I clearance.

- February 2025: Innocan Pharma received an Indian patent covering LPT-CBD prolonged-release liposomal cannabinoids, validated by a positive US FDA pre-IND meeting.

- August 2024: Lupin launched doxorubicin liposome single-dose vials in the U.S. after ForDoz secured ANDA approval.

- February 2024: FDA cleared irinotecan liposome with oxaliplatin, fluorouracil, and leucovorin for first-line metastatic pancreatic adenocarcinoma therapy.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the liposome drug delivery market as revenue from prescription-grade, lipid-bilayer vesicle formulations that encapsulate active pharmaceutical ingredients and are sold for human therapy across oncology, anti-infective, pain, vaccine, and central-nervous-system indications. It covers finished dosage forms such as liposomal doxorubicin, paclitaxel, amphotericin B, irinotecan, and daunorubicin plus cytarabine delivered through hospital and retail channels.

Scope Exclusions: Over-the-counter cosmetic liposome creams, gene-therapy lipid nanoparticles, research-only reagents, and contract manufacturing service fees are outside our lens.

Segmentation Overview

- By Product

- Liposomal Paclitaxel

- Liposomal Doxorubicin

- Liposomal Amphotericin B

- Vyxeos (Daunorubicin + Cytarabine)

- Liposomal Irinotecan

- Others

- By Technology

- PEGylated (Stealth)

- Non-PEGylated Conventional

- DepoFoam

- Cubosome-based LNPs

- By Indication

- Cancer Therapeutics

- Fungal Infections

- Pain Management

- Viral Vaccines

- CNS Disorders

- By Route of Administration

- Intravenous

- Intrathecal / Intraventricular

- Topical / Dermal

- Ocular

- Pulmonary / Inhalation

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

During this step, Mordor analysts interviewed hospital pharmacists, oncology clinicians, contract manufacturers, and formulation scientists across North America, Europe, and Asia-Pacific. These conversations validated treated-patient ratios, typical vial pricing, and pipeline transition probabilities that desk work alone could not resolve.

Desk Research

We began with open regulators like the US FDA Drugs@FDA, EMA EPAR, and India's CDSCO to map approved liposomal products. We then mined UN Comtrade trade codes to size cross-border volumes. Epidemiology series from WHO cancer observatories, CDC fungal trackers, and OECD health-spend dashboards anchored demand. Company 10-Ks, earnings calls, and investor decks supplied pricing clues, while peer-reviewed outlets such as the Journal of Controlled Release traced technology uptake. Internal paid repositories, including D and B Hoovers for financials and Dow Jones Factiva for deal flow, rounded out the evidence. This list is illustrative; many other sources informed the data checks.

Market-Sizing & Forecasting

We applied a top-down patient-flow model built on treated volumes by indication. We then corroborated totals with sampled manufacturer revenue roll-ups to adjust gaps. Key inputs included cancer and invasive-fungal incidence, average vials per cycle, median ex-factory prices, approval cadence, and regional reimbursement coverage. Multivariate regression combined with scenario analysis projected each driver to 2030, letting us stress-test growth under pricing pressure or faster biologic substitution. Where bottom-up sums under-reported niches, we normalized using validated hospital-utilization ratios.

Data Validation & Update Cycle

Outputs pass a two-stage peer review in which another analyst replicates calculations and a senior reviewer probes anomalies above five percent. Models refresh every year, with interim updates triggered by major label expansions or safety withdrawals. A final pre-release sweep ensures clients receive the latest view.

Why Mordor's Liposome Drug Delivery Baseline Earns Dependable Market Trust

Published values often vary because publishers mix product baskets, price bases, or refresh rhythms. By restricting scope to regulator-approved therapeutics and standardizing to ex-factory values, we cut noise for decision makers.

Key gap drivers include some firms bundling lipid nanoparticles for genetic payloads, others pricing at wholesale acquisition cost, or extrapolating from single-country samples. Mordor's annual rebuild and patient-flow logic curb these skews.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.91 B (2025) | Mordor Intelligence | - |

| USD 5.59 B (2024) | Global Consultancy A | Broader lipid carriers included and uses wholesale prices |

| USD 5.98 B (2025) | Industry Journal B | Omits pipeline attrition and relies on press releases for volume |

Together, the comparison shows that our disciplined scope choice and transparent patient-volume math deliver a balanced, traceable baseline that stakeholders can readily audit and replicate.

Key Questions Answered in the Report

What is the current value of the liposome drug delivery market?

The liposome drug delivery market is valued at USD 6.39 billion in 2026 and is projected to grow to USD 9.48 billion by 2031 at an 8.19% CAGR.

Which product holds the largest share in the liposome segment?

Liposomal doxorubicin leads with 35.92% share, supported by decades of clinical use and proven cardiotoxicity reduction benefits.

Why is Asia-Pacific the fastest-growing region?

Cost-efficient manufacturing, expanding healthcare coverage, and rising cancer incidence give Asia-Pacific an 10.57% CAGR through 2031.

How do cubosomes differ from traditional liposomes?

Cubosomes feature a cubic lipid phase that provides up to eight-fold higher cellular uptake and improved endosomal escape, which benefits gene-therapy and vaccine delivery.

What is the main regulatory hurdle for new liposomal drugs?

Stringent chemistry, manufacturing, and controls standards require detailed characterization of particle size, encapsulation efficiency, and release kinetics, inflating development costs and timelines.

Are PEGylated liposomes still viable despite antibody concerns?

Yes, PEGylated systems still hold 60.65% market share; however, firms are investing in alternative stealth coatings to reduce hypersensitivity risk while preserving extended circulation.

Page last updated on: