Vascular Stents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 14.37 Billion |

| Market Size (2031) | USD 19.71 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

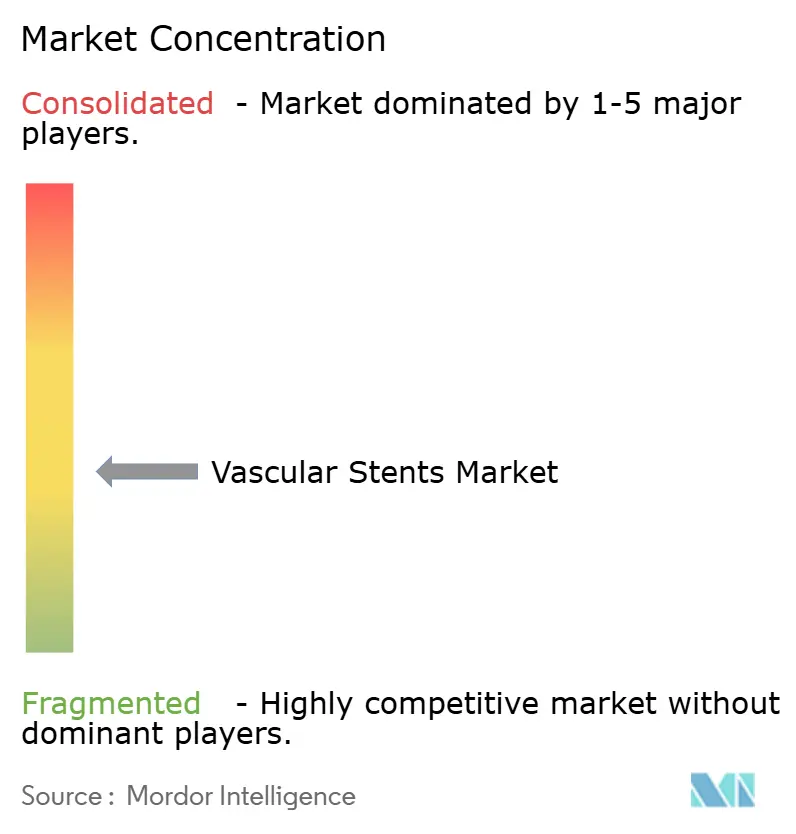

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vascular Stents Market Analysis by Mordor Intelligence

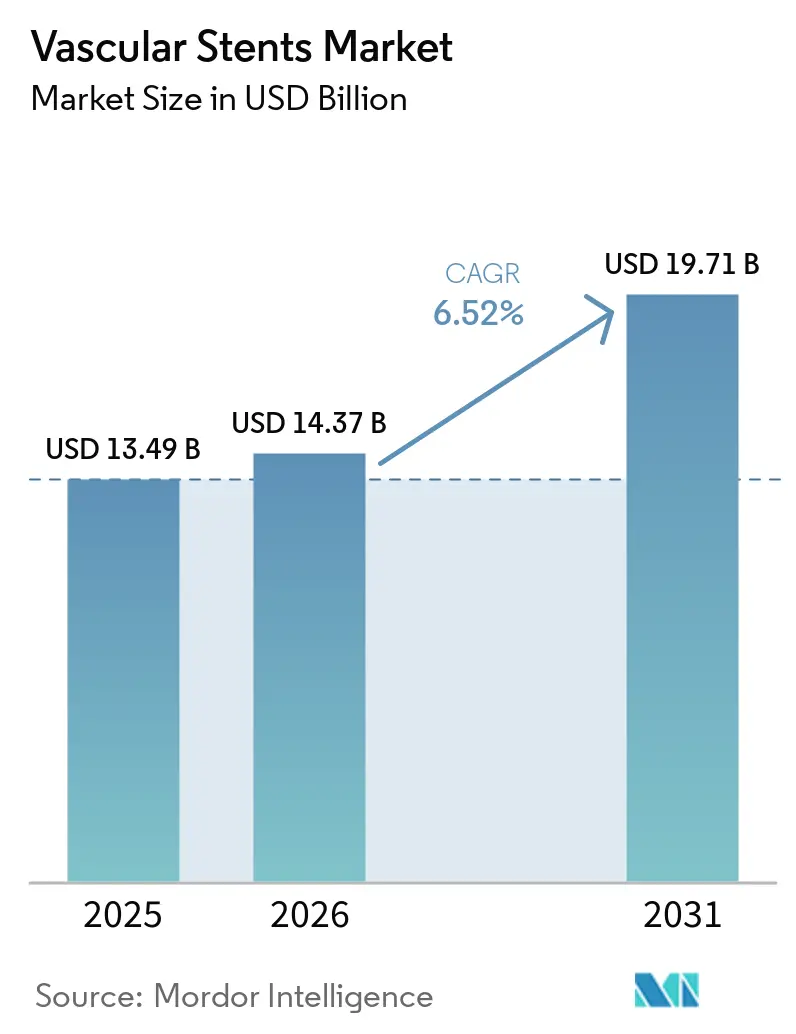

The Vascular Stents Market size is projected to expand from USD 13.49 billion in 2025 and USD 14.37 billion in 2026 to USD 19.71 billion by 2031, registering a CAGR of 6.52% between 2026 to 2031.

Coronary artery disease remains the clearest demand anchor for the vascular stents market, with 254 million prevalent cases worldwide in 2021 and a projected 525 million by 2046, which keeps intervention demand tied to a long disease curve instead of a short replacement cycle. Cardiovascular disease caused nearly 20 million deaths annually, which keeps stent procedures within essential care budgets across hospitals, cardiac centers, and public health systems. The vascular stents market is also being supported by aging populations and repeat interventions, as older patients remain in care pathways for longer periods and often return for staged or secondary procedures. Procedure migration into outpatient settings is widening installation opportunities for catheterization capacity and is changing how device makers position premium platforms, especially when physician preference shapes procurement more directly than hospital formularies. Growth in the vascular stents market remains broad rather than uniform, because complex aortic repair, bioabsorbable scaffolds, self-expanding platforms, and imaging-guided implantation are advancing at the same time that thrombosis, restenosis, and alternative therapies still limit unrestricted adoption.

Key Report Takeaways

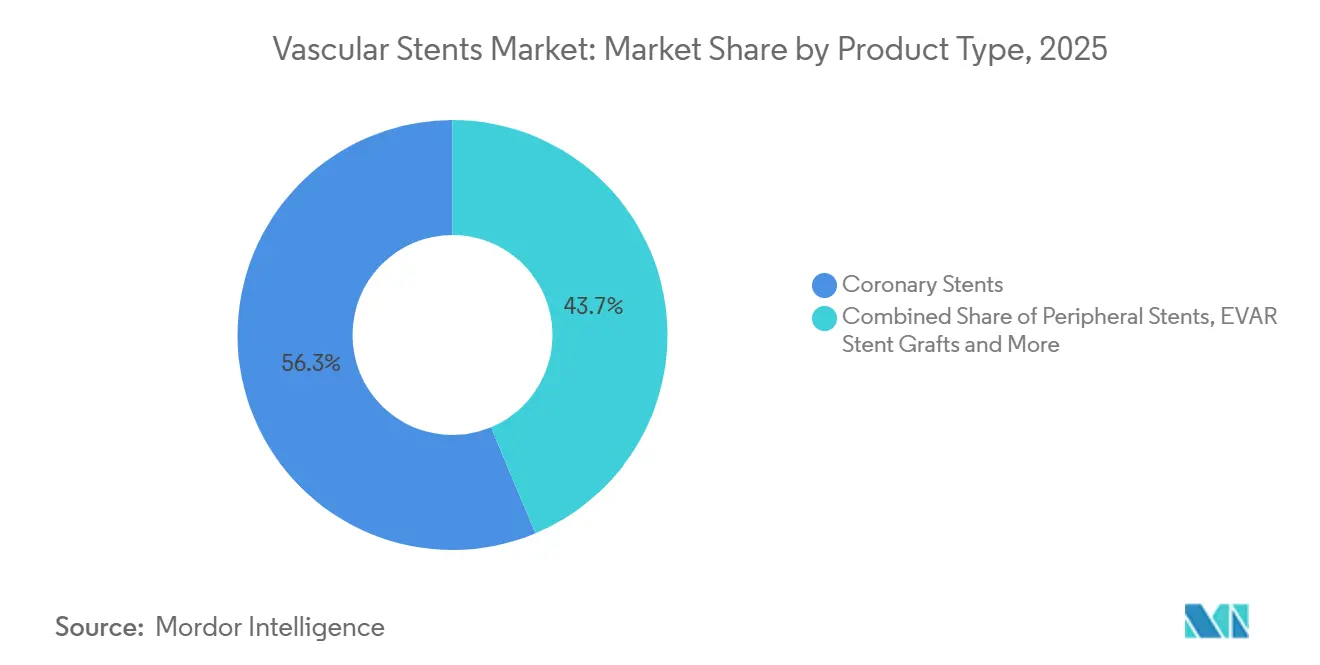

- By product type, coronary stents held 56.31% of the market in 2025, while EVAR stent grafts are projected to expand at a 9.38% CAGR through 2031.

- By technology, covered stents accounted for 38.24% of the market in 2025, while bioabsorbable stents are forecast to grow at an 8.52% CAGR through 2031.

- By material, metallic materials represented 54.52% of the market in 2025, while polymeric materials are projected to rise at a 9.25% CAGR through 2031.

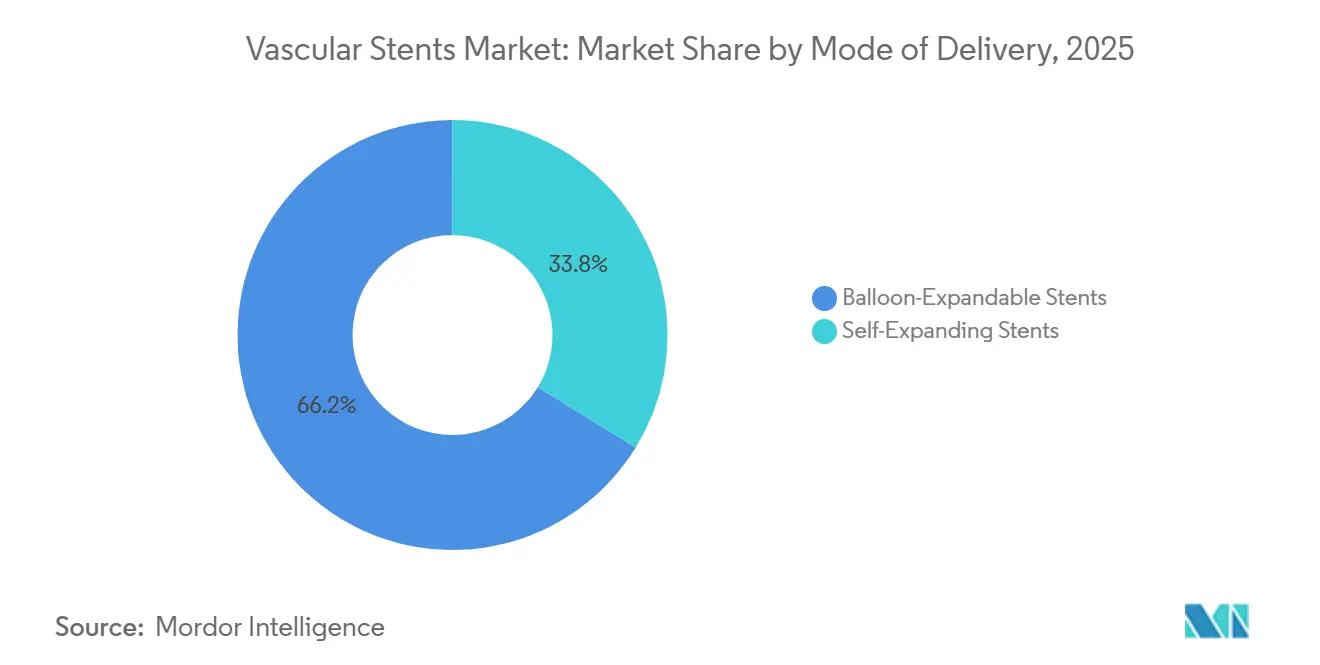

- By mode of delivery, balloon-expandable stents held 66.24% of the market in 2025, while self-expanding stents are expected to grow at a 9.52% CAGR through 2031.

- By end user, hospitals accounted for 65.52% of the market in 2025, while ambulatory surgical centers are anticipated to record the highest CAGR at 9.55% through 2031.

- By geography, North America held 41.22% of the market in 2025, while Asia-Pacific is forecast to advance at an 8.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vascular Stents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Coronary and Peripheral Artery Disease Burden | +1.5% | Global, highest in APAC and low-to-middle SDI regions | Short term (≤ 2 years) |

| Expanding Minimally Invasive Intervention Volumes | +1.2% | Global, APAC and North America lead procedural volume growth | Medium term (2-4 years) |

| Faster Adoption of Drug-Eluting and Covered Stent Platforms | +1.0% | North America and Europe, with spillover to emerging markets through tenders | Medium term (2-4 years) |

| Aging Population and Higher Reintervention Demand | +0.8% | APAC, Europe, and North America | Long term (≥ 4 years) |

| Imaging-Guided Precision Implantation and Complex Lesion Planning | +0.6% | North America, Europe, and Japan, with wider APAC uptake | Medium term (2-4 years) |

| Cost Pressure Shifting Purchasers Toward High-Value Stent Platforms | +0.4% | APAC centralized procurement markets, with spillover to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Coronary and Peripheral Artery Disease Burden

The vascular stents market continues to draw strength from the global rise in ischemic heart disease, which reached 31.9 million new cases in 2021 and is projected to climb to 56.4 million annual cases by 2046. This pattern keeps the vascular stents market tied to long-term disease progression, because treatment demand remains linked to aging populations and widening metabolic risk exposure instead of short-term procedure cycles. The burden is also widening across lower and middle Socio-Demographic Index regions, where high fasting plasma glucose is becoming a stronger contributor to atherosclerotic disease and is changing which devices are purchased first. In those settings, the vascular stents market is not moving through the same premium platform curve seen in higher income economies, because cost-sensitive acute care still favors simpler device choices in many cases. Peripheral artery disease is adding a separate patient pool for the vascular stents market, which means demand is not dependent only on coronary referrals or established PCI pathways.

Expanding Minimally Invasive Intervention Volumes

The vascular stents market is also benefiting from a steady shift toward minimally invasive treatment settings, as outpatient and ambulatory models are receiving broader procedural support. A Medicare analysis presented at SCAI 2025 projected a 21% increase in PCI volume in ambulatory surgical centers over the next decade, which supports longer-term placement demand for devices designed around faster workflows and predictable outcomes[1]TCTMD, “Medicare Analysis Reassures on PCI in Ambulatory Surgery Centers,” TCTMD, tctmd.com. This site-of-care shift matters for the vascular stents market because physician-led procurement often moves faster when platform performance is clear and formulary layers are lighter. The same trend also raises the value of systems that shorten procedure time and reduce repeat intervention risk, which keeps premium device adoption linked to operational efficiency as much as to clinical differentiation.

Faster Adoption of Drug-Eluting and Covered Stent Platforms

The vascular stents market is moving further toward drug-eluting and covered platforms, as newer generations address the long-standing concerns that limited early designs. Abbott’s ESPRIT BTK resorbable scaffold, which received FDA clearance in 2024 and Health Canada authorization in September 2025, showed 48% fewer repeat procedures than balloon angioplasty over 2 years in the LIFE-BTK trial. Biotronik began the BIOMAG-LL trial in February 2025 to study its Freesolve resorbable magnesium scaffold in longer coronary lesions, which shows that development is moving beyond narrow lesion profiles. Covered platforms are also gaining support in complex aortic and peripheral repair, where guideline backing and device design upgrades are expanding clinical use across anatomies that were once handled more selectively[2]European Society for Vascular Surgery, “Clinical Practice Guidelines on the Management of Descending Thoracic and Thoraco-Abdominal Aortic Diseases,” European Journal of Vascular and Endovascular Surgery, ejves.com. For the vascular stents market, this means premium adoption is being driven not only by incremental efficacy, but also by the removal of long-term concerns around permanent implants in younger and more active patient groups.

Imaging-Guided Precision Implantation and Complex Lesion Planning

The vascular stents market is gaining support from imaging-guided implantation, as the 2025 ACC, AHA, and SCAI guideline elevated IVUS or OCT guidance to a Class I, Level A recommendation for complex and left main lesions. A 2025 meta-analysis in the International Journal of Cardiology reported that IVUS-guided PCI produced a higher post-PCI minimum stent area than angiography-only guidance, which strengthens the case for more exact placement standards. This matters for the vascular stents market because stronger imaging support makes complex lesions more treatable by catheter-based intervention and reduces the boundary between routine and high-difficulty cases. Medtronic’s April 2026 acquisition of CathWorks for USD 585 million shows how major suppliers are linking physiology assessment and implant selection into one commercial pathway. As a result, the vascular stents market is moving toward integrated procedure planning, where diagnosis, lesion assessment, and final implant choice are increasingly sold as part of one workflow.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Device Thrombosis, Restenosis, and Reintervention Risk | -0.8% | Global, most acute where dual antiplatelet therapy adherence monitoring is limited | Medium term (2-4 years) |

| Stringent Regulatory Evidence and Post-Market Surveillance Burden | -0.6% | North America and Europe, with high pressure on smaller manufacturers | Medium term (2-4 years) |

| Reimbursement Constraints in Price-Sensitive Care Settings | -0.5% | APAC centralized procurement markets and MEA public hospital systems | Medium term (2-4 years) |

| Procedural Preference for Alternative Revascularization Approaches in Select Cases | -0.3% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Device Thrombosis, Restenosis, and Reintervention Risk

The vascular stents market still faces a clear device-level limitation, because late scaffold thrombosis and restenosis remain unresolved in several use cases and still influence physician confidence. Pooled 5-year ABSORB data published in 2025 showed higher adverse event rates for bioresorbable vascular scaffolds than for metallic drug-eluting stents during years 1 through 3, which explains why broad uptake was delayed after early enthusiasm. This issue matters beyond product reputation, because the vascular stents market depends on durable outcome data when new scaffolds seek broader reimbursement and guideline support. The problem is not limited to coronary use, since peripheral lesions also carry high reintervention exposure and keep repeat care costs elevated over the patient pathway. That creates a difficult balance for the vascular stents market, where repeat interventions can support short-term device revenue but can also weaken long-term outcome credibility and invite tighter scrutiny from regulators and payers.

Reimbursement Constraints in Price-Sensitive Care Settings

The vascular stents market is also constrained by reimbursement pressure in price-sensitive systems, where centralized procurement can compress pricing much faster than clinical differentiation can widen it. China’s first centralized coronary stent procurement round reduced prices by more than 90%, which changed the commercial model from margin protection to scale capture and forced suppliers to defend volume first. The second round concluded in May 2026 and demanded 2.73 million units across 4,468 institutions, which shows that higher procedural throughput can coexist with stricter pricing discipline when reimbursement systems mature. The vascular stents market could face similar pressure if centralized tender models spread more broadly across India, Brazil, and Southeast Asia, because those are also the regions where long-term volume growth remains attractive. At the same time, reimbursement innovation can still preserve premium pricing for selected products, as shown by Abbott’s U.S. payment pathway support for Esprit BTK[3]Abbott reimbursement coverage report, “Abbott Earns CMS Reimbursement Win for Esprit Drug-Eluting Scaffold,” TMG Pulse, tmgpulse.com.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: EVAR Graft Expansion Rebalances a Coronary-Dominated Portfolio

Coronary stents held 56.31% of vascular stents market share in 2025, which kept them as the core revenue segment across the vascular stents market. Drug-eluting coronary platforms remained the procedural base in developed systems because they combine long clinical experience with payer familiarity and broad physician acceptance. The product mix also reflects how the vascular stents market still depends heavily on PCI as the dominant global revascularization route, especially in systems that already have mature catheterization capacity. Coronary use has therefore stayed commercially central even while newer device classes have gained attention in more specialized settings. The same base gives large manufacturers a stable platform for launching incremental upgrades, because coronary accounts usually support training, inventory depth, and evidence generation at scale.

Peripheral stents, carotid systems, and neurovascular devices broaden the vascular stents market beyond coronary disease, but their commercial profiles remain more fragmented and more dependent on indication-specific data. The vascular stents industry also shows wider variability across these categories, since vessel anatomy, stroke protection needs, and reimbursement rules differ more than they do in coronary care. Neurovascular stents keep a technically differentiated role because pipeline embolization and intracranial applications command specialist use and often benefit from dedicated reimbursement pathways. EVAR stent grafts are the fastest-growing product category, and vascular stents market size for this segment is projected to expand at a 9.38% CAGR through 2031 as abdominal and thoracoabdominal aortic repair volumes rise. The 2026 ESVS guideline shift toward fenestrated and branched repair as the preferred treatment for thoracoabdominal aneurysms expands the addressable pool for the vascular stents market beyond standard infrarenal anatomy and brings more complex cases into endovascular pathways.

By Technology: Bioabsorbable Stents Gain Ground Without Displacing Proven Platforms

Covered stents accounted for 38.24% of the market in 2025, which made them the largest technology segment within the vascular stents market. Their role is broader than aneurysm exclusion alone, because they also support peripheral and aortic repair in lesions where vessel sealing and structural durability matter as much as lumen patency. Drug-eluting stents remained the core value driver in coronary care, where second-generation thin-strut platforms and biodegradable polymer coatings improved the balance between radial support and vessel healing. Bare-metal platforms retained a narrower role in emergency use and in settings where dual antiplatelet adherence remains uncertain, which shows that technology replacement across the vascular stents market is still incomplete. This uneven transition keeps older and newer technologies commercially relevant at the same time, especially across mixed reimbursement environments.

Bioabsorbable stents are forecast to grow at 8.52% CAGR from 2026 to 2031, and vascular stents market size in this technology band is moving faster than any other technology segment. Abbott’s Esprit BTK, Biotronik’s Freesolve program, and MicroPort’s Firesorb all show how the vascular stents market is building a new scaffold pipeline around improved degradation profiles, longer lesion usability, and lower repeat procedure expectations. The vascular stents industry is not seeing immediate displacement of metallic DES, because long-term evidence and commercialization timelines still favor established platforms in the largest coronary accounts. A 2025 systematic review in Biomedicines reported clinically equivalent 12-month outcomes between biodegradable polymer DES and polymer-free DES, which is already narrowing the premium attached to durable-polymer systems and pressuring pricing within this subsegment. The technology path in the vascular stents market therefore points to coexistence, with evidence-backed incumbent platforms retaining scale while scaffold-based systems expand first in targeted lesions and patient groups.

By Material: Polymeric Growth Signals Platform Transition, Not Substitution

Metallic materials represented 54.52% of the market in 2025, which kept them as the largest material base in the vascular stents market. Cobalt-chromium remained important in coronary drug-eluting devices because it supports thin struts with strong radiopacity, while nitinol stayed central in peripheral devices that must tolerate vessel movement and deformation. Stainless steel continued to hold relevance in price-sensitive markets where premium alloy reimbursement is weaker and procurement systems still reward lower acquisition cost. This material mix shows that the vascular stents market still values established mechanical reliability and manufacturing familiarity, especially in high-volume categories that face tighter pricing pressure. It also explains why metal has not lost structural importance even as biodegradable platforms attract more development attention.

Polymeric materials are projected to grow at a 9.25% CAGR through 2031, and vascular stents market size for this material category is increasing faster than any other material group. Polymeric growth does not mean direct replacement of metal across the vascular stents market, because polymers are mainly advancing through drug-elution architecture and degradable matrix design rather than through full structural substitution. The next stage is being shaped by biodegradable systems such as PLGA and by magnesium scaffold programs that address the strut thickness and late thrombosis concerns that limited earlier polymer-only designs. Research published in Hypertension Research in March 2026 also linked nitinol-PTFE EVAR combinations with higher 2-year all-cause mortality than stainless steel Dacron combinations in the studied cohort, which could alter material selection in certain aortic cases inside the vascular stents market. The material transition in the vascular stents market therefore looks selective and application-specific, with polymers adding value through platform architecture while metals still anchor core structural performance.

By Mode of Delivery: Self-Expanding Stents Outpacing the Dominant Balloon-Expandable Segment

Balloon-expandable stents held 66.24% of the market in 2025, which gave them the largest delivery-mode position in the vascular stents market. Their lead reflects the importance of precision deployment in coronary interventions, especially in left main and bifurcation lesions where exact expansion and placement control remain critical. Balloon-expandable systems also play a central role in fenestrated and branched EVAR, where bridging applications require stable positioning and dependable radial strength. Gore’s VIABAHN VBX received a broader CE Mark indication in 2025 for bridging use in fenestrated and branched repair, which reinforces the importance of balloon-expandable systems in complex aortic workflows. The 2025 guideline support for imaging-guided complex stenting also strengthens this segment by making deployment precision more visible and more measurable in daily practice.

Self-expanding stents are growing at a 9.52% CAGR from 2026 to 2031, and vascular stents market size in this mode is rising quickly as peripheral lesions become more central to the growth mix. Self-expanding platforms fit the vascular stents market well in femoropopliteal and similar anatomies because vessel motion, lesion length, and calcification often favor nitinol-based radial recovery over balloon-fixed expansion. A 2025 real-world registry in the European Journal of Medical Research reported 92.5% sustained clinical improvement at 18 months in complex femoropopliteal lesions treated with the S.M.A.R.T. Flex self-expanding system, which supports use in demanding peripheral anatomy. The commercial effect is that the vascular stents market is widening around anatomies where flexibility and fatigue resistance matter more than pure deployment precision. This keeps the vascular stents market on a two-track delivery path, with balloon-expandable systems staying dominant in coronary and complex bridging use while self-expanding devices capture more of the growth in peripheral care.

By End User: ASC Migration Reshapes Purchasing Dynamics

Hospitals retained 65.52% of the market in 2025, which kept them as the main end-user base in the vascular stents market. Their position reflects the concentration of complex coronary, aortic, and neurovascular procedures in settings that can support hybrid operating rooms, critical care backup, and multidisciplinary intervention teams. Large hospitals also remain the main sites for advanced imaging-guided implantation, which gives them an advantage in handling difficult lesions and in adopting broader endovascular protocols. In Europe, Germany continued to provide a stable procedural base, with 4.7 million coronary artery disease patients and 538,675 hospital admissions for coronary artery disease in 2023, which supports sustained institutional demand for advanced cardiovascular devices. Hospital purchasing still exerts downward pressure on unit pricing across the vascular stents market, because volume contracts and formulary controls remain stronger there than in most outpatient settings.

Ambulatory surgical centers are expected to grow at a 9.55% CAGR through 2031, which makes them the fastest-growing end-user category in the vascular stents market. The move is being supported by CMS procedure approvals and by continued investment in outpatient cardiology capacity, which is shifting selected interventions into settings with lighter infrastructure and faster procurement cycles. This matters for the vascular stents market because physician-directed purchasing tends to reward strong clinical data and ease of use more quickly than hospital committee processes do. It also creates a more favorable opening for newer platforms when they can show clear reductions in repeat procedures or workflow burden. The result is a vascular stents market where hospitals still hold the largest share, but ambulatory sites are reshaping commercial priorities and are gaining influence over which products move from early adoption into routine use.

Geography Analysis

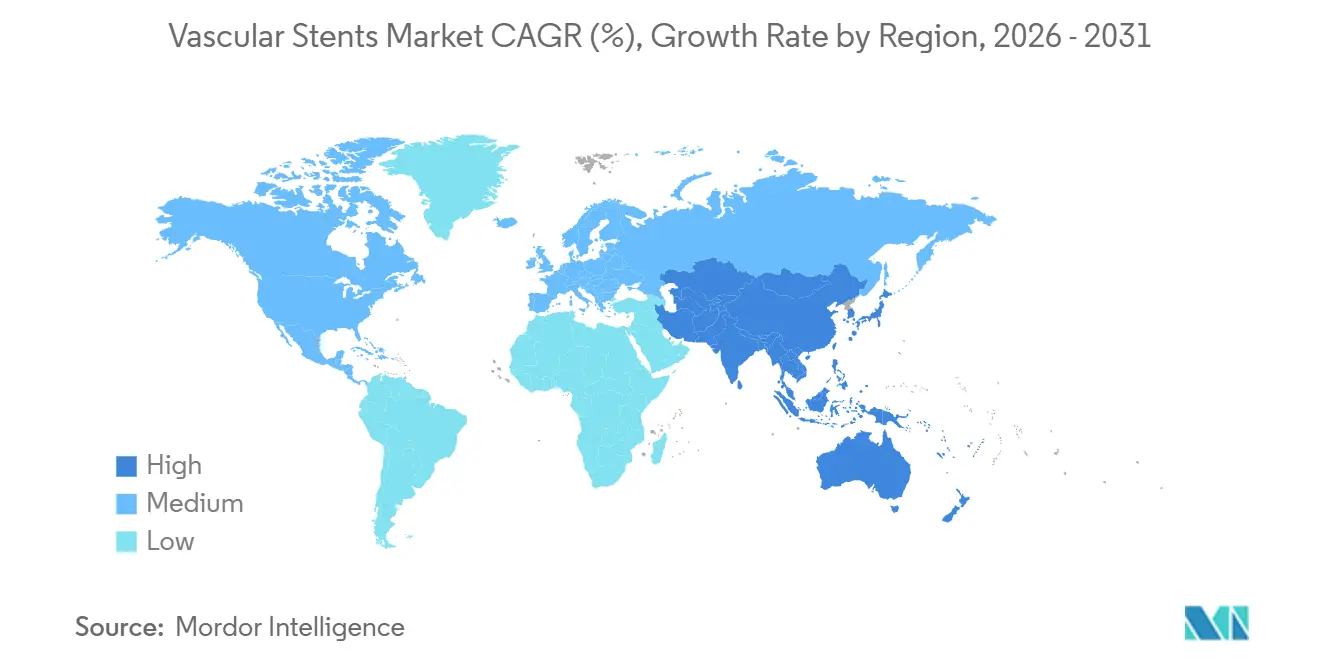

North America held 41.22% of vascular stents market share in 2025, which kept it as the largest regional contributor to the vascular stents market. Its position rests on mature reimbursement systems, high interventional volumes, and broad physician access to advanced imaging and device options. The 2025 ACC, AHA, and SCAI guideline update is supporting more imaging-guided complex stenting, which can lift device value per case even when regional procedure growth is moderate. The United States therefore remains the main premium platform market, especially for advanced coronary and below-the-knee technologies that need both evidence and payment support. Canada also supports the vascular stents market through adoption pathways for newer dissolvable scaffolds, as seen in the September 2025 authorization for Abbott’s Esprit BTK.

Europe remains an important stabilizing region for the vascular stents market because of its large procedure base and strong specialty center infrastructure. Germany is a key example, with a large coronary disease burden and a high volume of hospital admissions that keep cardiovascular intervention demand structurally relevant. The ESVS 2026 guideline is also expanding support for fenestrated and branched endovascular repair, which benefits device makers active in complex aortic treatment. At the same time, MDR compliance is narrowing European portfolios toward suppliers with established regulatory depth, which favors larger companies with already certified platforms. This keeps the vascular stents market in Europe more selective, with fewer commercialization shortcuts and a stronger premium on clinical follow-up data.

Asia-Pacific is the fastest-growing region, and vascular stents market size in the region is forecast to advance at an 8.85% CAGR through 2031. China remains central to that growth because its centralized procurement system now operates at very large scale, with the second 2026 coronary stent round covering 2.73 million units across 4,468 institutions. This means the vascular stents market in Asia-Pacific combines strong demand expansion with intense price discipline, which creates a different growth model than the one seen in North America. India adds another layer through a mix of price-sensitive public accounts and a growing private hospital base, which keeps room open for both multinational and local DES suppliers. The Middle East and Africa and South America remain smaller in absolute value, but they continue to gain relevance as training capacity, catheterization infrastructure, and cost-competitive imports expand access to intervention across more health systems.

Competitive Landscape

The vascular stents market is moderately consolidated at the top, with Abbott, Medtronic, Boston Scientific, B. Braun SE, and W. L. Gore and Associates, Inc. holding strong positions in premium coronary and aortic categories. At the same time, the vascular stents market remains fragmented across peripheral care and emerging economies, where MicroPort Scientific, Sahajanand Medical Technologies, Meril Life Sciences, and other regional firms compete actively on price and local access. This split structure means leadership is clearer in the highest-value segments than it is across the full vascular stents market. Large multinationals still benefit from evidence depth, physician familiarity, and regulatory scale, while regional firms remain effective in tender-driven accounts where price and domestic supply matter more. The result is a vascular stents market where top-end concentration and broad-base fragmentation exist at the same time.

Competitive strategy in the vascular stents market is increasingly centered on procedure integration instead of simple product line extension. Medtronic’s April 2026 completion of the CathWorks acquisition brought wire-free coronary physiology assessment into its cardiovascular portfolio, which supports the broader move toward diagnosis-to-implant alignment. Abbott’s continued expansion around Esprit BTK and XIENCE also shows how suppliers are trying to hold both established DES leadership and next-generation scaffold positioning at the same time. Gore is pushing the vascular stents market into more complex aortic repair through Excluder TAMBE in Europe and through the ARISE III ascending aortic stent graft study, which extends endovascular ambition into anatomies that were previously dominated by surgery.

White space in the vascular stents market is still most visible in complex anatomies and in below-the-knee peripheral disease, where evidence is expanding but commercial penetration is still early. That leaves room for companies that can combine regulatory execution, clinical data, and design precision in niche use cases that larger portfolios do not fully cover yet. The vascular stents market is also seeing stronger pressure from national procurement systems, which gives efficient domestic suppliers a better opening in standard segments while global firms protect premium tiers with evidence-backed differentiation. Compliance demands under device standards and post-market surveillance frameworks continue to raise entry barriers, which makes scale and follow-up capability more important than before. This keeps the vascular stents market competitive, but not open in the same way across every segment or geography.

Vascular Stents Industry Leaders

Medtronic plc

Boston Scientific Corporation

B. Braun SE

Abbott Laboratories

W. L. Gore and Associates, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Abbott launched XIENCE Skypoint in India. This is the latest and most advanced stent in Abbott's XIENCE family, designed to deliver everolimus (drug)-eluting benefits for coronary care.

- March 2026: BD (Becton, Dickinson and Company) received CE Marking for its Revello Vascular Covered Stent, a cutting-edge solution aimed at treating atherosclerotic lesions in the common and external iliac arteries.

Global Vascular Stents Market Report Scope

As per the scope of the report, vascular stents are small, expandable mesh tubes made of metal or polymer that are inserted into blood vessels to keep them open. They are commonly used to treat conditions like arterial blockages or narrowing (stenosis), ensuring proper blood flow.

The segmentation of the vascular stents market is categorized by product type, technology, material, mode of delivery, end user, and geography. By product type, the market includes coronary stents (drug-eluting coronary stents, bare-metal coronary stents, covered coronary stents, and bioabsorbable coronary stents), peripheral stents (carotid artery stents, femoral artery stents, iliac artery stents, renal artery stents, and other peripheral stents), EVAR stent grafts (abdominal aortic aneurysm stent grafts and thoracic aortic aneurysm stent grafts), and neurovascular stents (flow-diverter stents and intracranial atherosclerotic stents). By technology, the market is segmented into drug-eluting stents, covered stents, bare-metal stents, and bioabsorbable stents. By material, the segmentation includes metallic materials (cobalt chromium, platinum chromium, nickel titanium, and stainless steel) and polymeric materials (biodegradable polymers and non-biodegradable polymers). By mode of delivery, the market is divided into balloon-expandable stents and self-expanding stents. By end user, the market is segmented into hospitals, cardiac centers, ambulatory surgical centers, and cath labs. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Coronary Stents | Drug-Eluting Coronary Stents |

| Bare-Metal Coronary Stents | |

| Covered Coronary Stents | |

| Bioabsorbable Coronary Stents | |

| Peripheral Stents | Carotid Artery Stents |

| Femoral Artery Stents | |

| Iliac Artery Stents | |

| Renal Artery Stents | |

| Other Peripheral Stents | |

| EVAR Stent Grafts | Abdominal Aortic Aneurysm Stent Grafts |

| Thoracic Aortic Aneurysm Stent Grafts | |

| Neurovascular Stents | Flow-Diverter Stents |

| Intracranial Atherosclerotic Stents |

| Drug-Eluting Stents |

| Covered Stents |

| Bare-Metal Stents |

| Bioabsorbable Stents |

| Metallic Materials | Cobalt Chromium |

| Platinum Chromium | |

| Nickel Titanium | |

| Stainless Steel | |

| Polymeric Materials | Biodegradable Polymers |

| Non-Biodegradable Polymers |

| Balloon-Expandable Stents |

| Self-Expanding Stents |

| Hospitals |

| Cardiac Centers |

| Ambulatory Surgical Centers |

| Cath Labs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Coronary Stents | Drug-Eluting Coronary Stents |

| Bare-Metal Coronary Stents | ||

| Covered Coronary Stents | ||

| Bioabsorbable Coronary Stents | ||

| Peripheral Stents | Carotid Artery Stents | |

| Femoral Artery Stents | ||

| Iliac Artery Stents | ||

| Renal Artery Stents | ||

| Other Peripheral Stents | ||

| EVAR Stent Grafts | Abdominal Aortic Aneurysm Stent Grafts | |

| Thoracic Aortic Aneurysm Stent Grafts | ||

| Neurovascular Stents | Flow-Diverter Stents | |

| Intracranial Atherosclerotic Stents | ||

| By Technology | Drug-Eluting Stents | |

| Covered Stents | ||

| Bare-Metal Stents | ||

| Bioabsorbable Stents | ||

| By Material | Metallic Materials | Cobalt Chromium |

| Platinum Chromium | ||

| Nickel Titanium | ||

| Stainless Steel | ||

| Polymeric Materials | Biodegradable Polymers | |

| Non-Biodegradable Polymers | ||

| By Mode of Delivery | Balloon-Expandable Stents | |

| Self-Expanding Stents | ||

| By End User | Hospitals | |

| Cardiac Centers | ||

| Ambulatory Surgical Centers | ||

| Cath Labs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in vascular stents through 2031?

Growth is being supported by a rise in coronary and peripheral artery disease, more imaging-guided interventions, greater outpatient procedure capacity, and stronger uptake of EVAR, bioabsorbable, and self-expanding platforms.

How large is the vascular stents space expected to become by 2031?

The vascular stents market is projected to reach USD 19.71 billion by 2031 from USD 14.37 billion in 2026, with a CAGR of 6.52% over 2026 to 2031.

Which product category leads current revenue?

Coronary stents remained the largest product segment in 2025 with a 56.31% share, reflecting the continued scale of PCI-based revascularization.

Which category is growing fastest by product type?

EVAR stent grafts are the fastest-growing product type, with a projected CAGR of 9.38% through 2031 as complex aortic repair shifts further toward endovascular treatment.

Which region leads today and which one grows fastest?

North America led with 41.22% share in 2025, while Asia-Pacific is expected to post the highest regional CAGR at 8.85% through 2031.

Why are ambulatory surgical centers becoming more important?

Ambulatory surgical centers are projected to grow at a 9.55% CAGR through 2031 because procedure migration, physician-led purchasing, and approval support for outpatient intervention are making them a more influential end-user setting.

Page last updated on: