Biodegradable Stents Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

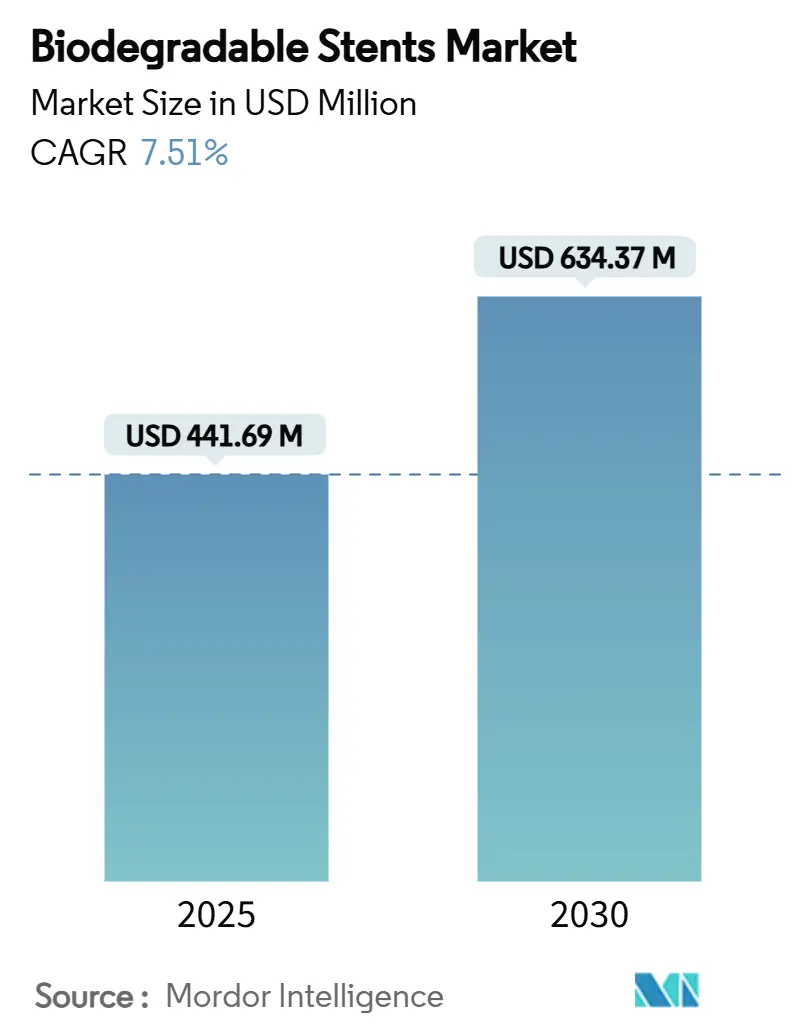

| Market Size (2025) | USD 441.69 Million |

| Market Size (2030) | USD 634.37 Million |

| Growth Rate (2025 - 2030) | 7.51% CAGR |

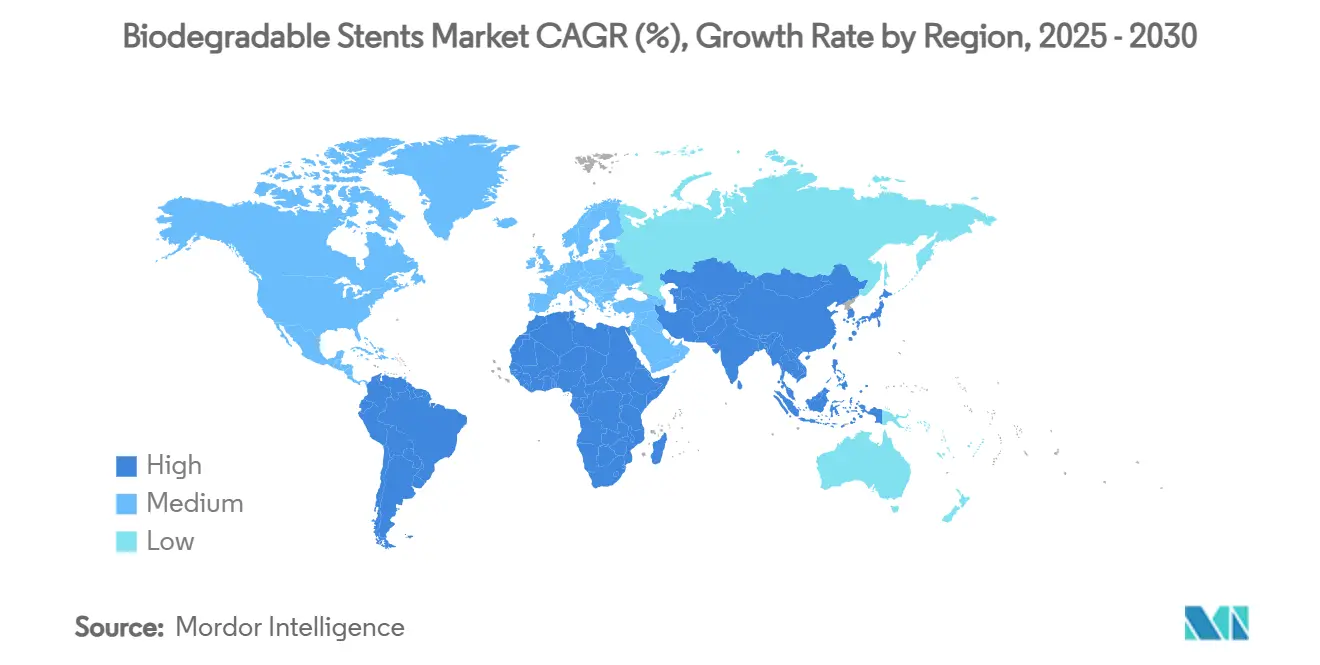

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Biodegradable Stents Market Analysis by Mordor Intelligence

The biodegradable stents market size reached USD 441.69 million in 2025 and is forecast to advance to USD 634.37 million by 2030, registering a 7.51% CAGR during the period. Regulatory encouragement, breakthroughs in polymer and magnesium alloy science, and the rising prevalence of cardiovascular disease among older adults have combined to make temporary, fully resorbable scaffolds an attractive alternative to permanent metallic implants. Hospitals and ambulatory surgical centers now view resorbable technology as a way to reduce lifetime complications, while physicians appreciate the preserved treatment flexibility for future interventions. Leading manufacturers are scaling production capacity for high-purity lactide and magnesium to avoid supply bottlenecks, and early adopters are documenting favorable real-world outcomes that further accelerate clinical confidence. Together, these factors place the biodegradable stents market on a steady upward path as platform refinements address mechanical strength, deliverability, and degradation control.

Key Report Takeaways

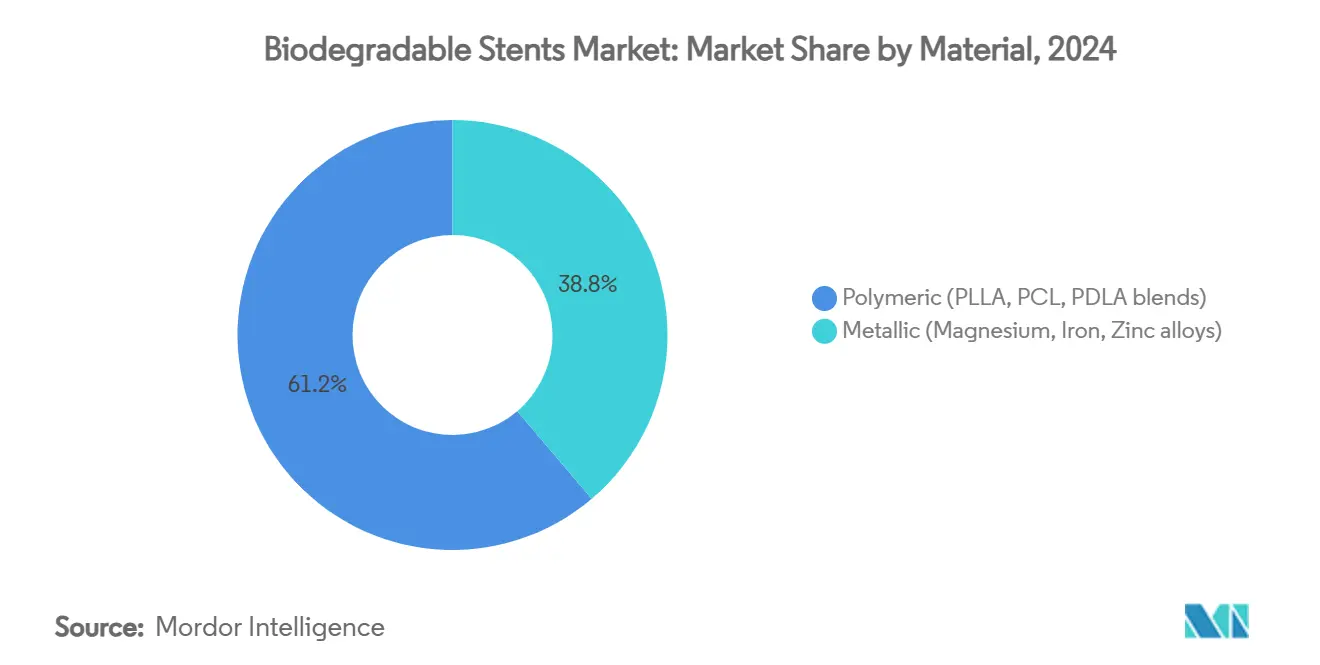

- By material, polymeric platforms held 61.22% of 2024 revenue, while metallic scaffolds are projected to grow at an 11.22% CAGR to 2030.

- By application, coronary artery disease led with 76.34% share in 2024; peripheral artery disease is expected to expand at an 11.67% CAGR through 2030.

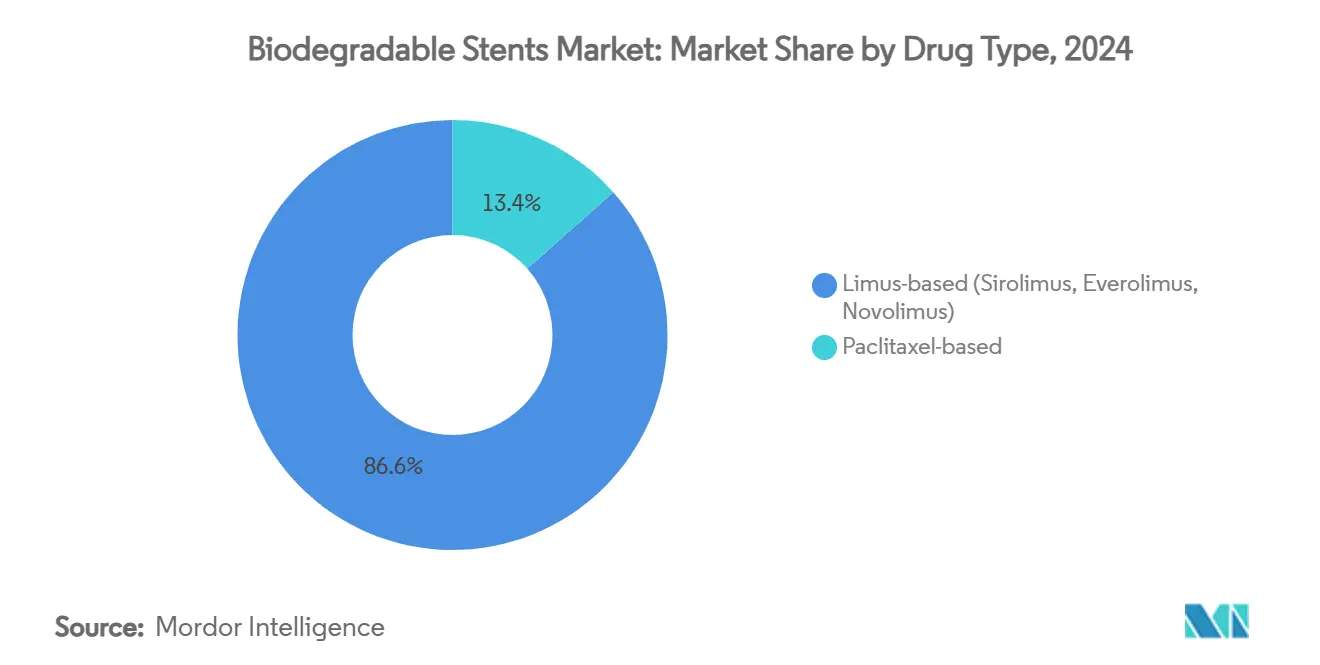

- By drug type, limus-based scaffolds commanded 86.56% of 2024 demand and are projected to grow at a 10.66% CAGR to 2030.

- By end user, hospitals accounted for 67.45% of 2024 procedures, while ambulatory surgical centers are projected to rise at a 9.78% CAGR over the forecast horizon.

- By geography, North America captured 37.33% of 2024 sales, whereas Asia-Pacific is forecast to post a 10.12% CAGR by 2030.

Global Biodegradable Stents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory tailwinds on resorbable devices | +1.8% | North America, Europe | Medium term (2-4 years) |

| Aging-population fuelled PCI volumes | +1.5% | Global developed markets | Long term (≥ 4 years) |

| Polymer science breakthroughs (PLLA co-polymers) | +1.2% | North America, Europe | Short term (≤ 2 years) |

| Post-market data validating BRS safety | +1.0% | Global | Medium term (2-4 years) |

| Magnesium alloy cost compression | +0.9% | Asia-Pacific with global spill-over | Medium term (2-4 years) |

| 3-D printed patient-specific scaffolds | +0.7% | North America, Europe, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Regulatory Tailwinds On Resorbable Devices

Health agencies now provide faster review pathways for temporary scaffolds because they resolve long-term implant complications. The FDA breakthrough designation granted to the DynamX bioadaptor in June 2024 shortens approval timelines and lowers clinical trial hurdles for innovative bioresorbable technology. Europe has introduced parallel expedited pathways, especially for devices that resorb within 24 months and show favorable remodeling. The new frameworks reduce time to market for well-documented platforms and favor firms with deep regulatory expertise. As a result, companies able to combine robust clinical data with streamlined submissions gain first-mover advantages in the biodegradable stents market. These policy supports are expected to continue through the medium term as agencies aim to reduce repeat interventions and overall healthcare costs.

Aging-Population Fuelled PCI Volumes

Global life expectancy gains mean more adults live long enough to experience coronary artery disease, and those over 65 now represent the fastest-growing cohort undergoing percutaneous coronary interventions. Elderly patients benefit from fully resorbable scaffolds because temporary support avoids late thrombosis, keeps arteries flexible, and simplifies potential future bypass or stent procedures. Long-term data from the BIOSOLVE-IV registry confirm that magnesium platforms deliver comparable event-free survival to contemporary drug-eluting stents while eliminating permanent foreign material.[1]Run-Lin Gao et al., “BiOSOLVE-IV Registry Outcomes,” EuroIntervention, eurointervention.pcronline.comHospital administrators also view the technology as a way to reduce repeat admissions. Demographic momentum will therefore underpin demand through at least the next decade.

Polymer Science Breakthroughs (PLLA Co-Polymers)

Improved poly-L-lactic acid formulations now combine refined molecular weights with co-polymer additives that boost radial strength without slowing absorption. Devices such as Evermine50 use 50-micron struts to match the crossing profile of metallic DES and still disappear within two years.[2]Meril Life Sciences Editorial Team, “Evermine50 Drug-Eluting Stent,” Meril Life, merillife.com Manufacturers exploit nano-scale drug reservoirs to synchronize drug release with scaffold resorption, reinforcing endothelial healing. The shift toward ultra-thin, high-strength polymers narrows the performance gap with metal while keeping production costs predictable. These gains make polymeric designs a reliable mainstay of the biodegradable stents market even as metallic systems mature.

Post-Market Data Validating BRS Safety

Real-world evidence is easing earlier safety doubts. Five-year follow-up from ABSORB IV shows that event curves converge with metallic DES once the scaffold is fully resorbed.[3]Gregg W. Stone et al., “Five-Year Outcomes After Bioresorbable Coronary Scaffolds Implanted With Improved Technique,” Journal of the American College of Cardiology, jacc.orgRegistries in Asia-Pacific and Europe now report negligible late scaffold thrombosis when physicians use intravascular imaging for precise sizing. This data reassures interventionists who hesitated after the first-generation Absorb setback. As confidence returns, procedure volumes rise, particularly for younger and lower-risk patients whose arteries may need future interventions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter FDA & EMA clinical-endpoint thresholds | -1.2% | North America, Europe | Medium term (2-4 years) |

| Historical Absorb BVS failures denting clinician trust | -0.9% | Global established markets | Short term (≤ 2 years) |

| Supply-chain fragility in high-purity lactide | -0.7% | Asia-Pacific concentration | Short term (≤ 2 years) |

| Interventional cardiologist training gap | -0.6% | Emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter FDA & EMA Clinical-Endpoint Thresholds

Following early scaffold setbacks, regulators now demand multi-year imaging and clinical follow-up that extends the cost and duration of trials. The FDA insists on comprehensive OCT or IVUS documentation of degradation profiles, which elevates development budgets beyond the reach of many start-ups. Similar European standards focus on long-term vessel patency rather than short-term procedural success. While these rules protect patients, they also consolidate the biodegradable stents market around companies with deep capital reserves and existing trial infrastructures.

Historical Absorb BVS Failures Denting Clinician Trust

The 2017 recall of Abbott’s first-generation device left a lasting impression on high-volume operators. Many practitioners still favor metallic DES unless presented with strong real-world evidence. Manufacturers now invest heavily in proctoring and imaging training to rebuild confidence, yet resistance remains a near-term drag on adoption in conservative centers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Metallic Platforms Drive Innovation

Polymeric scaffolds held 61.22% of the biodegradable stents market share in 2024 on the strength of mature PLLA technology and abundant clinical data. However, the biodegradable stents market size attributable to magnesium and iron alloys is expanding at an 11.22% CAGR because new metallurgy closes the radial-strength gap with metal DES while preserving full resorption within 12–18 months. In the current period, physicians still choose polymer devices for routine coronary lesions due to familiar deployment techniques and predictable degradation. Metallic scaffolds have moved quickly from early feasibility to pivotal trials, supported by imaging evidence that shows uniform degradation without inflammatory response. Iron platforms, though nascent, enable ultra-thin 60-micron designs that attract interest for small-vessel disease. Manufacturing economies of scale in Asia-Pacific compress alloy prices, narrowing cost differences with polymer devices. As a result, the biodegradable stents market will likely see a balanced material mix by the end of the forecast period.

Manufacturers differentiate metallic designs through alloy composition, drug-elution kinetics, and proprietary surface coatings that modulate endothelialization. Research programs focus on zinc enhancements to slow corrosion in peripheral arteries that require longer support. Meanwhile, polymer innovators are integrating nano-lipid reservoirs and bioactive peptides into PLLA matrices, aiming to deliver antithrombotic effects without systemic therapy. These mixed trajectories ensure that polymer and metal remain complementary rather than mutually exclusive, giving clinicians a broader toolkit for lesion-specific strategies.

By Application: Peripheral Expansion Accelerates

Coronary interventions generated 76.34% of revenue in 2024 as physicians adopted second-generation PLLA and magnesium platforms with confidence. The biodegradable stents market size linked to peripheral artery disease is forecast to climb rapidly because Abbott’s Esprit BTK approval proved the clinical value of resorbable scaffolds in mobile tibial vessels where permanent metal risks fracture. Surgeons treating critical limb ischemia appreciate the elimination of long-term foreign material that can complicate future bypass procedures. Gastrointestinal, ureteral, and airway indications are still niche, yet pilot trials of 3-D printed custom scaffolds show promising patency and patient comfort. Hospitals with thoracic units are prepping for compassionate-use programs that address pediatric airway collapse with personalized stents.

In coronary practice, resorbable technology now competes head-to-head with premium metallic DES in low-risk segments and is penetrating complex calcified lesions thanks to improved radial strength. Peripheral volumes will likely accelerate once reimbursement codes catch up and dedicated deployment tools enter the market. Non-vascular indications remain in early development, but favorable early clinical outcomes and growing surgeon interest suggest meaningful upside beyond 2030. These diverse clinical pathways reinforce the long-term relevance of the biodegradable stents market.

By Drug Type: Limus Dominance Continues

Limus-based coatings held 86.56% of 2024 revenue, the largest biodegradable stents market share, and are projected to expand at a 10.66% CAGR through 2030 thanks to sirolimus, everolimus, and novolimus profiles that align well with scaffold resorption timelines. Strong five-year data from the DESolve and DREAMS platforms confirm zero definite scaffold thrombosis in appropriately implanted limus devices, reinforcing cardiologist confidence and sustaining hospital formularies. Manufacturers continue to refine nano-reservoir designs that synchronize drug release with polymer or magnesium degradation, which further reduces late lumen loss and minimizes the need for prolonged dual antiplatelet therapy. These performance advantages keep limus products at the center of purchasing decisions across both hospital catheterization labs and outpatient centers that want predictable outcomes with minimal after-care. As a result, limus scaffolds will remain the benchmark against which new drug or drug-free concepts are evaluated.

Paclitaxel coatings occupy a small but stable niche, preferred for certain peripheral lesions where its distinct antiproliferative mechanism offers vascular compatibility. The biodegradable stents market size tied to drug-free scaffolds is still modest, yet early studies of collagen-functionalized surfaces indicate a viable path to eliminate pharmacologic payloads while promoting rapid endothelial healing. Combination strategies that pair low-dose limus with micro-RNA or peptide layers are under review, aiming to shorten antiplatelet regimens and appeal to patients at bleeding risk. Over the forecast window, limus technology will keep dominance, but incremental gains from paclitaxel refinements and bioactive surfaces will diversify clinical choices and ensure healthy innovation across the category.

Hospitals accounted for 67.45% of the biodegradable stents market share in 2024, reflecting their dominance in complex cardiovascular procedures that require intensive imaging and post-operative monitoring. Their established catheterization labs, on-site surgical teams, and reimbursement coverage keep procedure volumes high, especially for multivessel disease and high-risk patients. Teaching institutions also generate pivotal registry data that informs guideline updates and sustains hospital demand. However, administrators face cost-containment pressures and aim to shift lower-acuity cases to outpatient centers to free operating-room capacity. These financial dynamics set the stage for ambulatory surgical centers to capture a larger share of straightforward scaffold placements over the next five years.

Ambulatory surgical centers are projected to expand procedure volume at a 9.78% CAGR through 2030, adding noticeable incremental value to the biodegradable stents market size during the forecast window. Their streamlined workflows lower overhead and allow same-day discharge, which appeals to payers and patients alike. Temporary scaffold technology suits these settings because it reduces long-term surveillance and avoids late foreign-body complications. Device firms support the shift by designing simplified delivery systems and offering targeted training modules that shorten the learning curve for ASC staff. As proficiency spreads and payers adjust reimbursement schedules, outpatient centers will complement hospitals rather than displace them, broadening overall access to fully resorbable stent solutions.

Geography Analysis

North America retained 37.33% of 2024 sales thanks to early FDA approvals, broad insurance coverage, and a concentration of high-volume interventional cardiology centers. Extensive registry networks provide real-world outcomes that feed back into practice guidelines and reinforce physician confidence. The biodegradable stents market also benefits from integrated supply chains that secure high-purity polymer and magnesium inputs. Training symposia organized by professional societies ensure a steady pipeline of skilled operators who adopt new platforms quickly.

Europe follows closely, supported by coordinated research consortia and value-based procurement systems that favor devices reducing lifetime complications. Comprehensive post-approval surveillance across the region underpins physician trust and drives stable adoption. European practitioners often pioneer complex applications such as chronic total occlusions and bifurcation lesions, validating use cases later adopted elsewhere. Pricing pressures, however, require manufacturers to demonstrate clear cost offsets by reducing late re-interventions.

Asia-Pacific is the fastest-growing territory, expected to post a 10.12% CAGR to 2030 as rising cardiovascular disease prevalence intersects with rapid healthcare infrastructure expansion. Domestic manufacturers in China and India scale local production of magnesium alloys and PLLA, lowering device prices and accelerating penetration into tier-two cities. Governments invest heavily in interventional cardiology training and subsidize advanced imaging equipment, addressing historical gaps in procedural expertise. Over time, the region is likely to challenge North America for leadership in procedure volume, though reimbursement and uniform clinical guidelines remain works in progress.

Competitive Landscape

The biodegradable stents market displays moderate fragmentation with emerging consolidation. Large diversified device companies acquire scaffold specialists to broaden portfolios and secure intellectual property. Teleflex’s acquisition of Biotronik’s vascular intervention arm in February 2025 illustrates the trend, adding the Freesolve resorbable magnesium platform to Teleflex’s lineup. Such moves allow acquirers to leverage established sales channels and manufacturing scale, improving cost positions and expanding geographic reach.

Competition focuses on three vectors: material innovation, drug-delivery sophistication, and deployment tooling. Magnesium pioneers emphasize rapid endothelialization and superior radial force, while polymer leaders invest in nanoscale drug reservoirs and bioactive surface coatings. Additive manufacturing disruptors pursue patient-specific devices that can expand into pediatric, airway, and gastrointestinal fields. The need for extended clinical evidence incentivizes partnerships with academic centers that run multicenter trials and generate peer-reviewed publications to support regulatory submissions.

Barriers to entry remain high due to stringent endpoint requirements and the capital intensity of manufacturing pure polymers and high-tolerance alloys. Smaller innovator firms often license technology or accept minority investment from larger strategics seeking pipeline diversification. Over the forecast horizon, market concentration will slowly increase, yet innovation cycles remain active as start-ups exploit focused indications and novel materials to challenge incumbents.

Biodegradable Stents Industry Leaders

Abbott Laboratories

Boston Scientific

Terumo Corporation

Teleflex

Reva Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Teleflex Incorporated completed its acquisition of Biotronik’s Vascular Intervention business, adding Freesolve resorbable magnesium technology to its interventional portfolio.

- July 2024: MicroPort Scientific Corporation secured NMPA approval for Firesorb®, the first next-generation fully bioresorbable cardiac stent.

Global Biodegradable Stents Market Report Scope

| Polymeric (PLLA, PCL, PDLA blends) |

| Metallic (Magnesium, Iron, Zinc alloys) |

| Coronary Artery Disease (CAD) |

| Peripheral Artery Disease (PAD) |

| Gastrointestinal Strictures |

| Ureteral Obstruction |

| Airway Stenosis |

| Limus-based (Sirolimus, Everolimus, Novolimus) |

| Paclitaxel-based |

| Hospitals |

| Cardiac Catheterization Labs |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Polymeric (PLLA, PCL, PDLA blends) | |

| Metallic (Magnesium, Iron, Zinc alloys) | ||

| By Application | Coronary Artery Disease (CAD) | |

| Peripheral Artery Disease (PAD) | ||

| Gastrointestinal Strictures | ||

| Ureteral Obstruction | ||

| Airway Stenosis | ||

| By Drug Type | Limus-based (Sirolimus, Everolimus, Novolimus) | |

| Paclitaxel-based | ||

| By End User | Hospitals | |

| Cardiac Catheterization Labs | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the 2025 global value of biodegradable stents?

The biodegradable stents market stands at USD 441.69 million in 2025.

How fast is the market projected to grow?

It is expected to register a 7.51% CAGR and reach USD 634.37 million by 2030.

Which material category is expanding the quickest?

Metallic magnesium scaffolds are advancing at an 11.22% CAGR through 2030.

Which region is set to witness the highest growth?

Asia-Pacific is forecast to post a 10.12% CAGR during the period.

Who dominates drug formulation use in current scaffolds?

Limus-based drugs account for 86.56% of 2024 demand and keep growing.

Where are outpatient procedures gaining traction?

Ambulatory surgical centers are the fastest-growing end-user segment, rising at a 9.78% CAGR.

Page last updated on: