Non-Invasive Fat Reduction Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

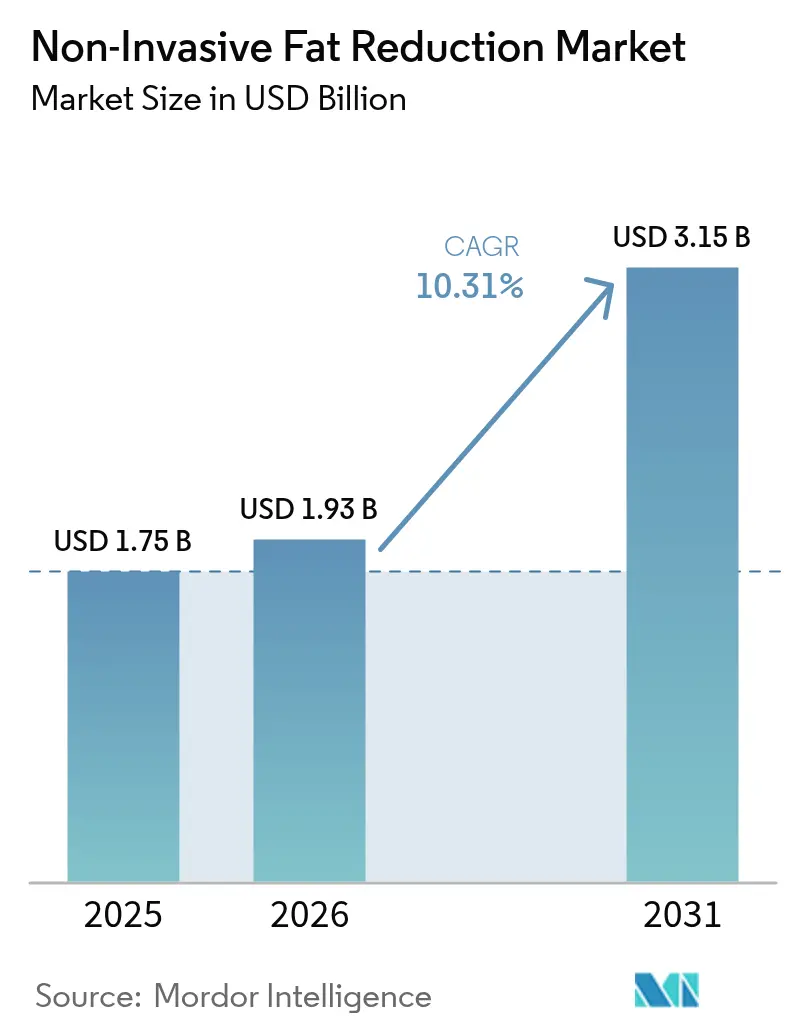

| Market Size (2026) | USD 1.93 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 10.31% CAGR |

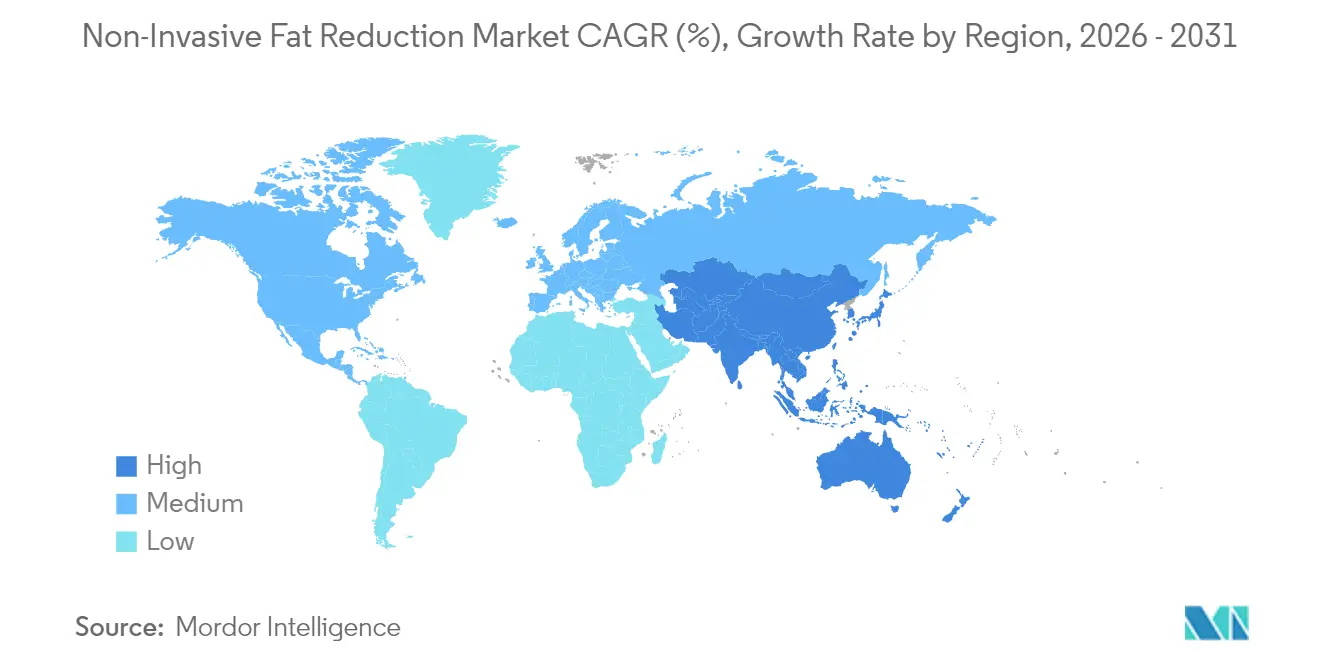

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

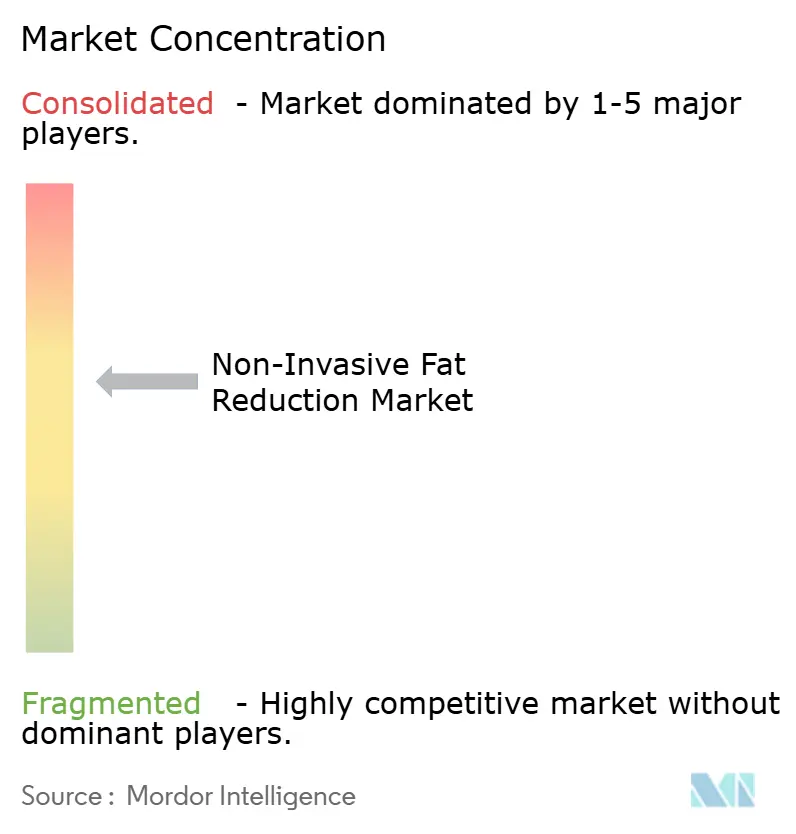

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Invasive Fat Reduction Market Analysis by Mordor Intelligence

non-invasive fat reduction market size in 2026 is estimated at USD 1.93 billion, growing from 2025 value of USD 1.75 billion with 2031 projections showing USD 3.15 billion, growing at 10.31% CAGR over 2026-2031. Demand accelerates as GLP-1 weight-loss drugs expose skin laxity that patients want corrected by device-based sculpting solutions. Cryolipolysis holds entrenched adoption, yet high-intensity focused electromagnetic (HIFEM) systems capture share by pairing fat apoptosis with visible muscle toning. Provider expansion into tier-2 cities, particularly through medspa chains, improves access and price transparency. AI-guided body scanning tightens treatment planning precision, while a growing male customer base broadens the overall non-invasive fat reduction market universe.

Key Report Takeaways

- By technology, cryolipolysis led with 41.78% revenue share of the non-invasive fat reduction market in 2025; HIFEM is projected to grow at 17.61% CAGR to 2031.

- By end user, dermatology and cosmetic clinics held 53.83% of the non-invasive fat reduction market share in 2025, while medspas carry the highest projected CAGR at 17.23% through 2031.

- By application, abdominal procedures accounted for a 38.25% share of the non-invasive fat reduction market size in 2025, whereas submental treatments are expected to expand at 11.92% CAGR between 2026-2031.

- By gender, female patients dominated with 71.98% share in 2025; male participation is advancing at 12.88% CAGR to 2031.

- By age group, adults aged 35-50 owned the largest 41.95% revenue slice in 2025; the 18-34 cohort is the fastest-growing segment at 12.19% CAGR.

- By geography, North America led with 38.12% revenue share in 2025 and Asia-Pacific is forecast to expand at a 11.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Non-Invasive Fat Reduction Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge In GLP-1 Weight-Loss Drug Users Seeking Skin-Tightening Add-Ons | +2.1% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Growing Medspa Chain Roll-Outs In Tier-2 Cities | +1.8% | Global, with concentration in North America and Asia-Pacific | Long term (≥ 4 years) |

| Rising Obesity Prevalence | +1.4% | Global | Long term (≥ 4 years) |

| Preference For Minimally-Invasive Aesthetics | +1.3% | Global | Medium term (2-4 years) |

| AI-Driven Body-Scanning Enabling Personalised Treatment Planning | +0.9% | North America & Europe, early adoption in APAC | Medium term (2-4 years) |

| Insurance Pilots Covering Cryolipolysis For Metabolic Syndrome | +0.6% | North America, limited EU coverage | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in GLP-1 Weight-Loss Drug Users Seeking Skin-Tightening Add-Ons

Widespread GLP-1 prescription growth lifts ancillary demand as rapid fat loss reveals residual laxity requiring contour correction. Randomized trials confirm these agonists reduce fat mass more than muscle, creating specific sculpting needs that device platforms address. Providers market combination programs that synchronize medication, nutrition, and cryolipolysis or HIFEM sessions, effectively converting pharmacotherapy patients into aesthetic clients. The approach sustains recurring revenue because body contouring is performed in staged cycles. However, insurer reluctance to cover GLP-1 drugs may temper downstream device uptake, highlighting the importance of flexible financing models for bundled care.

Growing Medspa Chain Roll-Outs in Tier-2 Cities

Scaling chains bring branded, standardized treatment menus to previously under-served secondary metros and suburban corridors. Lower real-estate overhead and agile staffing structures underpin unit economics that support competitive pricing without quality compromise. Franchised platforms cross-sell skincare, laser, and wellness memberships, embedding the non-invasive fat reduction market into a broader lifestyle offering. Consolidators employ centralized training and shared-service procurement to protect margins while accelerating geographic penetration. The model hedges recession risk by diversifying revenue streams across a wider demographic and price spectrum.

Preference for Minimally-Invasive Aesthetics

Patient risk tolerance favors techniques with little downtime, minimal bruising, and no surgical scars. Controlled cooling studies cite 14.67%-28.5% adipose reduction after a single cryolipolysis cycle with 73% satisfaction at three-month follow-up[1]Nestor Demosthenous, “Cryolipolysis: A Review of Published Clinical Data,” PMFA Journal, thepmfajournal.com. Radiofrequency-plus-HIFEM combinations further add 25% muscle mass and 30% fat loss, delivering a visibly athletic physique without anesthesia. Younger buyers view such upkeep as part of holistic wellness rather than vanity, reinforcing sustained, preventive demand across life stages.

AI-Driven Body-Scanning Enabling Personalized Treatment Planning

Three-dimensional imaging platforms collect thousands of anthropometric data points, allowing software to recommend applicator placement and session duration. Clinical pilots recorded 6% hip and 8% waist circumference drops when algorithms guided device settings versus conventional protocols. Real-time feedback also reduces the likelihood of thermal injury or overtreatment, supporting better patient safety dossiers that accelerate regulatory clearance cycles. Providers leverage photo-realistic simulations to set realistic expectations, tightening conversion rates and justifying premium fees.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure Cost & Limited Reimbursement | -1.9% | Global, particularly impactful in price-sensitive markets | Medium term (2-4 years) |

| Adverse-Event Publicity On Paradoxical Adipose Hyperplasia | -1.2% | Global, with heightened awareness in North America | Short term (≤ 2 years) |

| Competitive Cannibalisation From Weight-Loss Drugs | -0.8% | North America & Europe, expanding globally | Medium term (2-4 years) |

| Regulatory Gray Zones For Spa-Based Operators | -0.7% | Global, with varying intensity by jurisdiction | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Procedure Cost & Limited Reimbursement

Average pricing ranges from USD 750 to USD 4,000 per body zone, with full courses often exceeding USD 10,000 when multiple cycles and areas are treated. Major insurers classify device-based fat reduction as elective, leaving patients to self-finance. Disposable income volatility therefore influences booking intent; provider data show appointment cancellations rise sharply during macro-economic uncertainty. Clinics now partner with fintech firms to offer 0% installment plans, yet credit approvals remain a barrier for younger consumers, delaying penetration into the broader middle class of the non-invasive fat reduction market.

Adverse-Event Publicity on Paradoxical Adipose Hyperplasia

Though incidence rates run between 0.0051% and 0.39%, media coverage of paradoxical adipose hyperplasia (PAH) amplifies perceived risk[2]Demitri Franzoni, “Paradoxical Adipose Hyperplasia,” PubMed, pubmed.ncbi.nlm.nih.gov. The American Society of Plastic Surgeons advises immediate ultrasound diagnosis followed by liposuction or abdominoplasty in refractory cases. News cycles featuring celebrity PAH cases stimulate momentary procedure slow-downs and higher malpractice premiums. Device manufacturers respond by updating applicator designs with real-time temperature mapping, while physicians emphasize meticulous patient selection and consent documentation to mitigate litigation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: HIFEM Broadens Body Goals Beyond Fat Loss

Cryolipolysis retains 41.78% of 2025 device revenues as its decade-long safety dossier and straightforward workflow appeal to both new and veteran providers. Nonetheless, HIFEM systems post an 17.61% CAGR because they tackle two biologic targets simultaneously: apoptotic adipocytes and hypertrophic muscle fibers. Post-procedure ultrasound imaging shows 16% muscle growth and 19% local fat depletion after four sessions. This holistic outcome aligns with patient expectations shaped by social media fitness influencers. The non-invasive fat reduction market size for electromagnetic platforms is projected to widen further once rehabilitative pain indications gain insurance codes. High-intensity focused ultrasound (HIFU) competes in skin tightening niches, while low-level laser light appeals to clients seeking gentler metabolic modulation with virtually no downtime. Each modality thus occupies a distinct performance-versus-comfort position, encouraging clinics to stock multiple systems for tailored plans.

Bi-modal combinations register growing traction. Providers layer radiofrequency heat to increase adipocyte susceptibility before cryolipolysis cooling or coordinate sequential HIFEM plus RF-micro-needling to tighten skin post-lipolysis. Early adopters report 30% higher average revenue per client when two devices are packaged into curated “transformation journeys.” Meanwhile, injectable ice slurry, still in in-human feasibility trials, could disrupt capital-intensive platforms by lowering per-procedure consumable costs. Manufacturers therefore accelerate pipeline R&D to hedge against future commoditization. Taken together, technology diversification cements the non-invasive fat reduction market as a dynamic playground where iterative upgrades spur repeat capital expenditure cycles.

By End User: Medspas Convert Footfall Into Lifetime Value

Dermatology and cosmetic clinics delivered 53.83% of 2025 revenue owing to physician trust and clinical oversight. Yet medspas outpace them with a 17.23% CAGR by integrating hospitality design, wellness retail, and membership billing. Since most devices do not legally require supervision by board-certified surgeons, entrepreneurs can scale multi-unit footprints staffed by physician assistants and nurses operating under tele-supervision agreements. Lower wage differentials in tier-2 cities combined with centralized digital marketing reduce customer acquisition cost, elevating EBITDA margins above 20%.

Hospitals tend to specialize in complex lipedema or post-bariatric contour cases requiring anesthesia and multidisciplinary aftercare. Fitness centers, in contrast, trial adjunct cryolipolysis pods near strength-training zones, capturing impulse purchasers seeking immediate visual feedback. The non-invasive fat reduction industry also witnesses hybrid “surgical spa” build-outs where plastic surgeons co-locate operating rooms and device suites, cross-pollinating patient pipelines. Capital inflows from private equity exceeded USD 3.1 billion across 400 medspa transactions between 2020-2024, underscoring institutional conviction in scalable aesthetics. This liquidity funds CRM platforms that track lifetime value, automate appointment reminders, and upsell adjunct skincare lines, cementing sticky client relationships across decades.

By Application Area: Facial Zoom Culture Elevates Submental Focus

Abdominal sculpting remains the flagship, commanding 38.25% of 2025 procedure fees; yet submental programs clock a 11.92% CAGR as remote video conferencing magnifies chin contours on high-definition cameras. The non-invasive fat reduction market size for injectable deoxycholic acid leapt after the FDA cleared Kybella, paving a regulatory pathway for future enzyme cocktails targeting small adipose pockets. Experimental lipase-collagenase blends achieved a 22.8% patient-reported improvement at 90-day follow-up, confirming appetite for less bulky applicators over the neck zone.

Love-handle reshaping and inner-thigh contouring cater to fashion-driven consumers who wear slim silhouettes. Arm and bra-line treatments gain momentum during spring-summer seasons when sleeveless apparel dominates retail racks. Providers that stagger promotions around seasonal wardrobe shifts smooth clinic occupancy year-round. Muscle-enhancing modalities further blur traditional boundaries: a HIFEM session on the gluteal region both trims adjacent adipose and lifts tissue, tapping cultural fascination with athletic posterior profiles. Such cross-functional outcomes fortify device ROI and justify higher price points versus single-endpoint systems.

By Gender: Inclusive Marketing Adds New Growth Lanes

Female clients continue to generate 71.98% of receipts, reflecting ingrained social acceptance and broader knowledge of aesthetic options. However, male bookings grow 12.88% annually as messaging pivots from beauty to performance and confidence. Campaigns highlight core-strength improvement and posture benefits to resonate with gym-going audiences. HIFEM treatments are particularly popular because they deliver visible “six-pack” definition without extended cardio regimens.

Clinic floorplans adjust by adding gender-neutral lounges and flexible scheduling outside typical office hours to accommodate male professionals. Protocols now include privacy-first draping and anatomical mapping that accounts for thicker dermal layers and distinct fat deposition patterns. Social stigma dissipates as sports celebrities openly endorse body-sculpt services, normalizing consumption. The widening demographic mix minimizes reliance on a single cohort, insulating the non-invasive fat reduction market from gender-specific economic shocks such as maternity-related spending pauses.

By Age Group: Prevention Culture Drives Early Adoption

Consumers aged 35-50 hold 41.95% of 2025 value, leveraging peak earnings to address postpartum or career-related physique concerns. Yet the 18-34 segment accelerates at 12.19% CAGR, propelled by social networks that portray aesthetic care as routine self-maintenance. Clinics curate starter packages—such as small-volume cryolipolysis for “muffin top” smoothing—that introduce young adults to device categories before age-related collagen loss becomes pronounced. Flexible payment plans and loyalty apps lock in multi-year engagement, lowering churn.

Peer-reviewed data reveal millennials prioritize body positivity yet remain highly responsive to subtle contour enhancements that elevate confidence in photos and videos. Providers thus emphasize natural “refinement” rather than dramatic transformations, aligning with emerging ethical marketing codes. The 51+ group continues to present steady demand for skin laxity improvement, especially when weight loss or menopause redistributes fat. Together, staggered age-segment growth underpins a diversified revenue runway that supports robust device amortization schedules.

Geography Analysis

North America captured 38.12% of 2025 demand thanks to established medspa density, high discretionary income, and a transparent FDA pathway that accelerates first-to-market launches. The United States makes up more than 80% of regional revenue, amplified by medical tourism from Canada and Latin America for proprietary cryolipolysis applicators unavailable elsewhere. Reimbursement pilots covering cryolipolysis in metabolic syndrome cases further legitimize procedure value and could unlock broader payer traction if outcomes demonstrate cardiovascular benefit. Digital health start-ups integrate post-procedure monitoring wearables, providing clinicians with longitudinal data that refine follow-up scheduling.

Europe accounts for the second-largest slice, characterized by highly regulated device approval under the Medical Device Regulation framework. Germany, France, and the United Kingdom are core spenders, although southern European nations show above-average growth as tourism-centric economies market “vacation plus treatment” packages. Strict advertising rules limit hyperbolic claims, compelling brands to publish peer-reviewed substantiation that inadvertently boosts consumer trust. Eco-responsibility themes resonate strongly; clinics favor energy-efficient generators and recyclable gel pads, creating a market differentiator for suppliers who verify lower life-cycle emissions.

Asia-Pacific is the fastest-growing territory at a 11.95% CAGR through 2031, driven by expanding middle-class populations and heightened appearance consciousness in urban centers. China leads volume, where 91% of surveyed aesthetic consumers plan to maintain or increase spend despite macro-economic volatility. Japan advances innovation, exemplified by robotics-assisted applicator arms that cut session set-up time by 40%. South Korea exports K-beauty protocols, popularizing combination therapy blueprints adopted across Southeast Asia. India’s young demographic, coupled with rapid private-hospital build-outs, presents significant upside once device import duties ease. Australia rounds out regional uptake, leveraging tele-health consults to bridge geographic distance and optimize patient funnel management.

South America and the Middle East & Africa represent emerging hot spots, with Brazil and the United Arab Emirates championing procedure affordability relative to local cosmetic surgery alternatives. Currency fluctuations and customs tariffs pose adoption hurdles, yet medical tourism bundles that combine lodging with treatment mitigate sticker shock. Across all regions, localized regulatory clarity and clinician training remain decisive determinants of non-invasive fat reduction market expansion.

Regulatory Landscape

In the United States, non-invasive body contouring technologies, including fat-reducing lasers and ultrasound-based systems, generally fall under FDA Class II oversight and commonly use the 510(k) premarket notification pathway to demonstrate substantial equivalence (for example, devices regulated under 21 CFR 878.5400). Recent 510(k) clearances in 2026 for low-level laser fat reduction systems point to continued product flow through this pathway, and review timelines can vary depending on submission complexity.

In Europe, the Medical Device Regulation (MDR 2017/745) and the implementing requirements for certain non-medical aesthetic devices (Annex XVI) increased the conformity assessment burden for equipment intended for adipose tissue reduction, often raising scrutiny such as Class IIb with Notified Body involvement. MDR transitional provisions for legacy products marketed before June 23, 2023 allow continued EU market presence into 2028 or 2029 depending on whether a clinical investigation is required, which in turn shapes portfolio prioritization, documentation upgrades, and post-market evidence planning.

Competitive Landscape

The competitive arena displays moderate fragmentation: the top five manufacturers contribute significant global device sales. Hahn & Company’s merger of Cynosure and Lutronic in 2024 illustrates active consolidation designed to combine complementary laser, RF, and cryolipolysis IP. The integrated portfolio empowers cross-selling into physician networks while eliminating duplicative R&D and supply-chain costs. Nevertheless, region-specific challengers flourish by offering lower-cost systems backed by localized service hubs, appealing to budget-conscious clinics outside Tier-1 cities.

Clinical evidence is a paramount differentiator. Firms such as Allergan Aesthetics publish multi-center trials demonstrating sustained fat-volume decrease and histologic safety, securing trust that underpins premium list prices. Competitors unable to match data depth often pivot to specialized applicators—like small cup sizes for underarm bulges—to carve niche loyalty. AI-enabled platforms represent a next-wave moat: proprietary machine-learning algorithms trained on thousands of pre- and post-images improve parameter prediction accuracy, creating lock-in as clinics hesitate to retrain staff on unfamiliar dashboards.

Financial health shapes strategic flexibility. Cutera’s 2025 restructuring underscores susceptibility to cyclical cash-flow swings tied to capital equipment cycles. Vendors diversify by launching consumable-heavy add-ons, such as single-use adhesive arrays, that generate predictable recurring revenue. Service-level agreements bundled with remote diagnostics further shore up margins while enhancing device uptime. Geographic white spaces—Africa, Central Asia, and parts of Eastern Europe—remain ripe for partnership models where distributors assume regulatory filing and after-sales obligations, enabling lean entrance strategies for midsize brands.

Non-Invasive Fat Reduction Industry Leaders

Cutera Inc

Candela Corporation

Alma Lasers

Bausch Health (Solta Medical)

Cynosure LLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Combination protocols that address both volume reduction and post-weight-loss tissue quality create whitespace for platforms that pair modalities, especially for providers building programs around GLP-1 patient pathways where skin laxity and contour refinement are common add-on needs. The near-term opportunity is strongest in workflow and planning layers, including AI-guided body scanning and standardized treatment mapping that reduce operator variability across multi-site medspa chains expanding into tier-2 cities. With typical self-pay price points spanning roughly USD 750 to USD 4,000 per body zone and limited reimbursement, vendors and providers are also leaning on consumer financing and bundled memberships to improve conversion and repeat visits, which favors systems with clear ROI narratives and strong consumable or service attach rates.

Market access and differentiation continue to hinge on regulatory alignment and evidence generation, so vendors with predicate-aligned iterations and peer-reviewed clinical substantiation tend to gain traction. A peer-reviewed study published in Nature Scientific Reports in June 2025 reported non-invasive abdominal fat layer reduction using Alma's Accent Prime platform, supporting provider marketing within permissible claims and strengthening defenses of premium positioning. In the EU, the higher MDR compliance bar for adipose-reduction equipment increases the value of quality systems, clinical data packages, and Notified Body readiness, while in the United States the 510(k) pathway continues to favor substantial-equivalence strategies that shorten time-to-market for updated applicators and ergonomics across diverse body regions.

Recent Industry Developments

- February 2026: Bausch Health's aesthetics business, Solta Medical, launched the Clear + Brilliant Touch laser in Canada following prior Health Canada approval. The rollout widens Solta Medical's addressable clinic footprint in a market where dermatology and aesthetic practices often cross-sell energy-based procedures, supporting platform standardization across sites.

- June 2025: Alma reported a peer-reviewed study in Nature Scientific Reports supporting non-invasive abdominal fat layer reduction using the Accent Prime platform. The published evidence strengthens provider confidence and helps vendors compete on outcomes documentation as adverse-event scrutiny and informed consent expectations rise in body contouring.

- April 2025: Bausch Health (Solta Medical) received Health Canada medical device license clearance for the Thermage FLX system for non-invasive skin tightening and contouring. The clearance supports commercial expansion in Canada and reinforces the role of radiofrequency-based tightening as a complementary purchase alongside fat-reduction offerings, particularly for post-weight-loss laxity management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenues generated from non-invasive procedures and devices that reduce localized subcutaneous fat without surgery, mainly using energy-based modalities delivered in aesthetic care settings.

Scope exclusions: We exclude surgical liposuction and other operating room based fat removal procedures, along with weight-loss drugs, bariatric surgery, and general fitness services.

Segmentation Overview

- By Technology

- Cryolipolysis

- High-Intensity Focused Ultrasound (HIFU)

- Low-Level Laser Therapy (LLLT)

- Radiofrequency Lipolysis

- Cavitation / Ultrasound Cavitation

- Electromagnetic Muscle Stimulation (HIFEM)

- Emerging: Injectable Ice-Slurry

- By End User

- Hospitals

- Dermatology & Cosmetic Clinics

- MedSpas

- Fitness & Wellness Centers

- By Application Area

- Abdomen

- Flanks (Love-handles)

- Thighs

- Sub-mental

- Arms

- Buttocks & Back

- By Gender

- Female

- Male

- By Age Group

- 18-34 Years

- 35-50 Years

- 51+ Years

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set a clear market boundary and build the first cut of adoption and pricing logic by country and care setting. We used non-paywalled sources such as the American Society of Plastic Surgeons, the International Society of Aesthetic Plastic Surgery, the World Bank, OECD health statistics, and peer-reviewed clinical journals that discuss body contouring outcomes and typical treatment cadence.

We also reviewed public company filings and investor presentations to understand how suppliers describe exposure to body contouring, along with reputed press and association websites for product launches and regulatory milestones. When required, paid subscriptions were used for company financials, news validation, and patent databases so innovation cycles and investment patterns could be checked with fewer gaps. The sources listed here are illustrative rather than exhaustive, since we also used other public references for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys were used to validate what clinics actually purchase and use, and how procedure volumes shift with consumer budgets, promotions, and physician preference. Inputs such as pricing bands, utilization ranges, and technology mix were pressure-tested with providers, distributors, and industry specialists across APAC, EMEA, and the Americas, then compared back to the assumptions from desk research.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 50% |

| Mid tier: 58% | Functional/Unit leaders: 42% | EMEA: 30% |

| Smaller Players: 17% | Managers: 44% | Americas: 20% |

Market-Sizing & Forecasting

Sizing starts with a top-down demand pool build where procedure opportunity is reconstructed from aesthetic procedure counts, the share of non-invasive body contouring within total aesthetics, and the typical number of sessions per patient. Once the demand pool is formed, country totals are converted into revenue using observed price ranges for a treatment course and the split by technology (such as cryolipolysis, ultrasound, and low-level laser), then rolled up by region.

To keep totals realistic, we use selective bottom-up approximations as a cross-check, mainly by sanity-checking clinic throughput, installed base signals, and distributor feedback on replacement cycles, then adjusting outliers. Inputs that move the model in a meaningful way include treatment price ranges by setting, utilization rates (sessions per week per device), the number of sessions per treatment plan, consumer willingness to pay by income cohort, and mix shifts between modalities as promotions and comfort levels change.

For forecasting, scenario analysis is applied with a base case anchored on expert consensus for utilization normalization and price drift, then lighter and stronger uptake paths are built around consumer spending and clinic capital budgets. Where local data is thin, gaps are handled by using comparable-country ratios for procedure incidence and re-checking those outputs through provider feedback before inclusion in the final roll-up.

Data Validation & Update Cycle

Validation is done by comparing model outputs with independent signals such as procedure-count directionality, clinic expansion trends, and modality mix commentary from providers, which helps catch unrealistic jumps. When a variance looks unusual, assumptions are traced back to the driver level (price, sessions, penetration, or mix) and then re-tested through follow-up outreach before sign-off.

A multi-step analyst review is followed so calculations, currency conversions, and year alignment are checked consistently across regions. Reports refresh annually, with interim updates triggered by material events such as regulatory changes, sharp pricing moves, or sudden shifts in clinic purchasing. Before delivery, we perform a final pass so clients receive the most current view supported by the latest available public signals.

Mordor Intelligence's Non Invasive Fat Reduction Market Size Measured Against Other Published Estimates

Published market sizes for non-invasive fat reduction often diverge because studies do not always count the same revenues, and they may rely on different base years, price assumptions, and refresh timing. Differences also show up when one estimate leans more on device-related revenue signals, while another leans more on procedure activity inside aesthetic clinics.

The main gap comes from whether adjacent body contouring categories are included along with non-invasive fat reduction, where Mordor Intelligence keeps the scope centered on cryolipolysis, ultrasound, and low-level laser and cross-checks pricing using care-setting level inputs instead of applying one global average price. Spreads can also be explained by how quickly prices are assumed to change, how currency timing is handled, and whether technology mix is updated when newer systems shift demand between modalities.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.93 B (2026) | |

| Global Consultancy A | USD 1.69 B (2023) | Uses an earlier base year and a different growth window, and the published scope snapshot appears to be anchored more tightly around a smaller set of technology revenues, which can understate later-year adoption and price effects in clinics. |

| Industry Research Group B | USD 1.56 B (2023) | Starts from 2023 and applies a higher forward growth path, and it can also widen end-use tagging without fully reconciling care-setting utilization and treatment-course pricing differences by country. |

The spread in the table is largely explained by timing and what is counted, since the cited figures are anchored to different base years and do not always reconcile utilization and treatment-course pricing in the same way. When the core drivers are kept visible and reviewed with provider feedback, the market value stays traceable and repeatable during updates.

Key Questions Answered in the Report

What is the current size of the non-invasive fat reduction market?

The non-invasive fat reduction market is valued at USD 1.93 billion in 2026 and is projected to reach USD 3.15 billion by 2031.

Which technology segment is growing fastest?

High-intensity focused electromagnetic (HIFEM) systems are expanding at 17.61% CAGR because they simultaneously reduce fat and build muscle.

Why are GLP-1 drugs influencing demand for body-contouring devices?

GLP-1 prescriptions trigger rapid fat loss that often leaves residual skin laxity, prompting patients to seek non-surgical tightening and sculpting procedures.

How significant is male participation in the market?

Male clients currently account for roughly 28.02% of procedures, and their bookings are rising at 12.88% CAGR through 2031.

Which region is expected to grow quickest?

Asia-Pacific leads growth with a forecast 11.95% CAGR, buoyed by rising disposable incomes and increasing acceptance of aesthetic medicine.

Page last updated on: