Linear Actuators Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

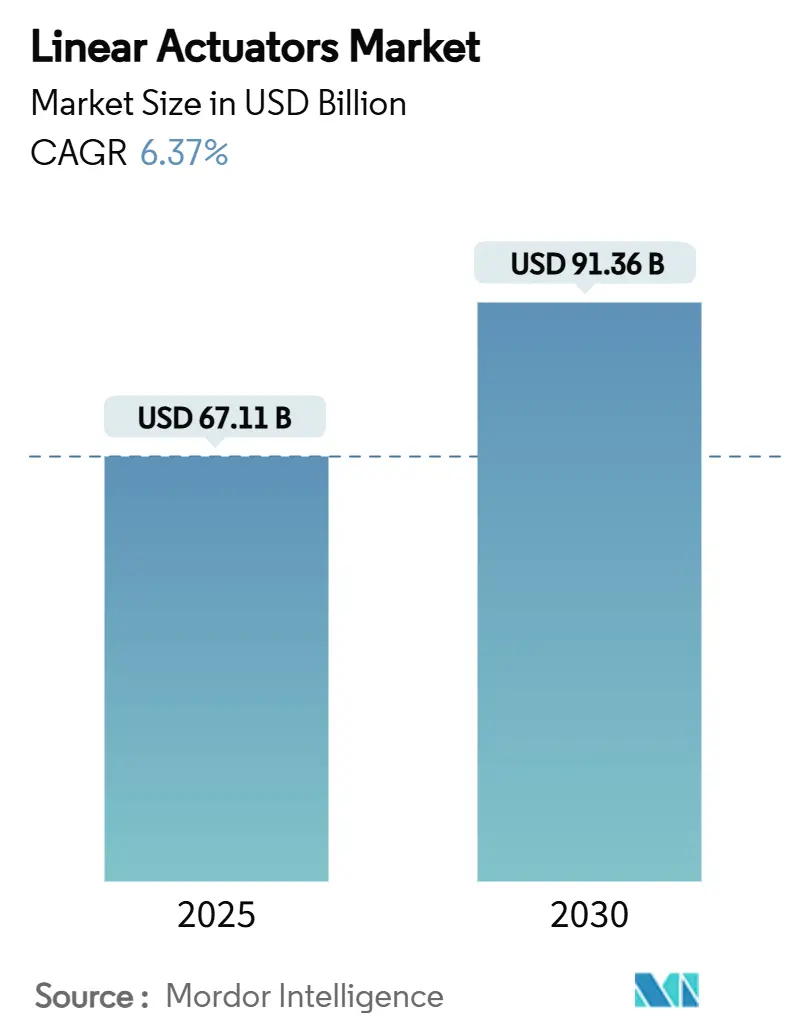

| Market Size (2025) | USD 67.11 Billion |

| Market Size (2030) | USD 91.36 Billion |

| Growth Rate (2025 - 2030) | 6.37% CAGR |

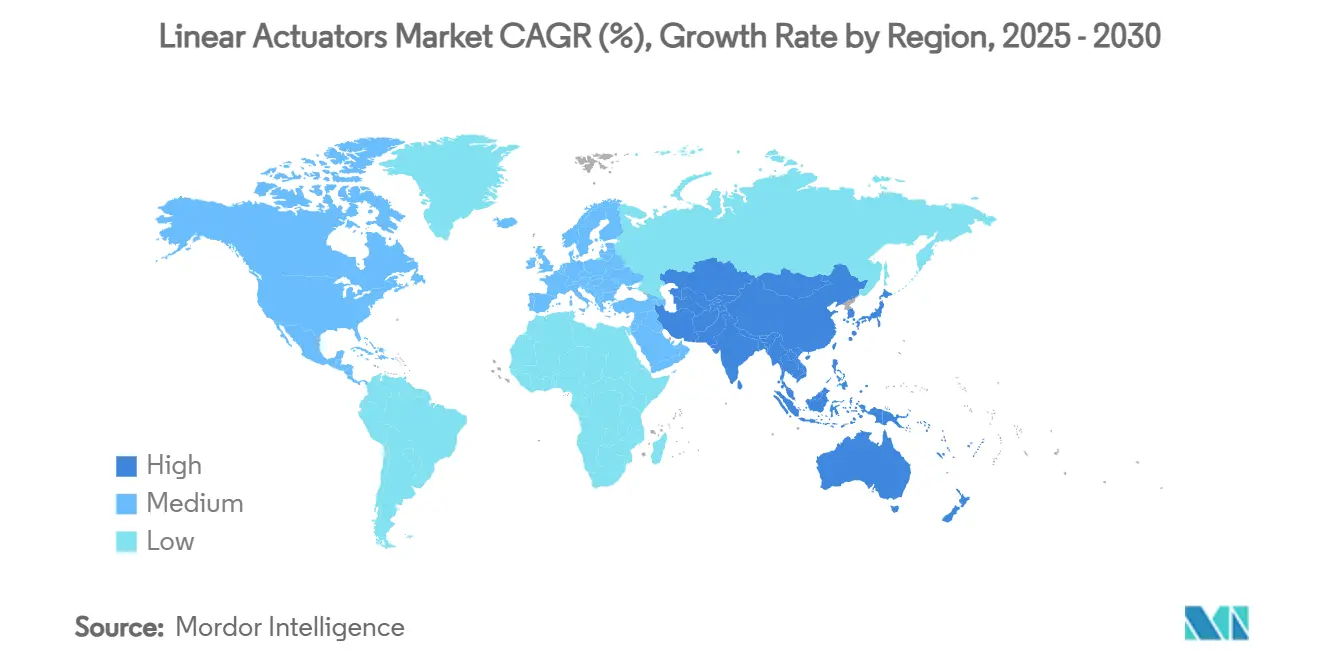

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

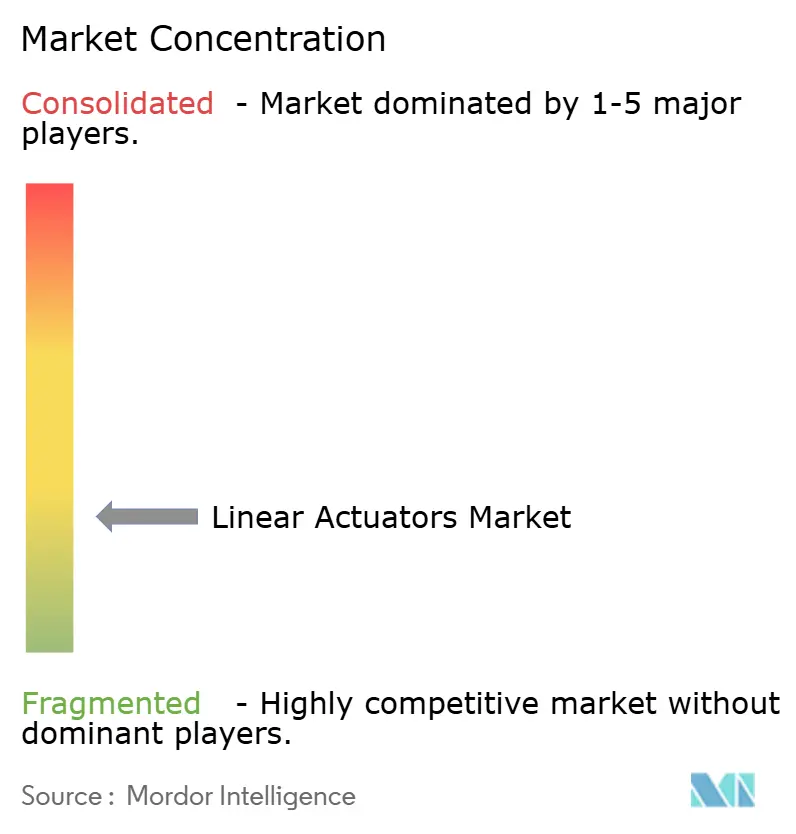

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Linear Actuators Market Analysis by Mordor Intelligence

The linear actuators market size touched USD 67.11 billion in 2025 and is expected to advance to USD 91.36 billion by 2030, translating into a 6.37% CAGR. This growth reflects the widening preference for intelligent, energy-frugal motion systems that meet global decarbonization objectives. A decisive move away from hydraulic and pneumatic devices toward digitally controlled electric alternatives is underway as manufacturers seek cleaner operations, tighter process control, and easier integration with Industry 4.0 platforms. Investments in factory automation, electrified aerospace subsystems, and precision medical equipment are sustaining demand even during raw-material price swings. Meanwhile, advances in ball-screw design, direct-drive linear motors, and high-voltage servo architectures continue to lift performance ceilings and broaden application scopes across the linear actuators market.

Key Report Takeaways

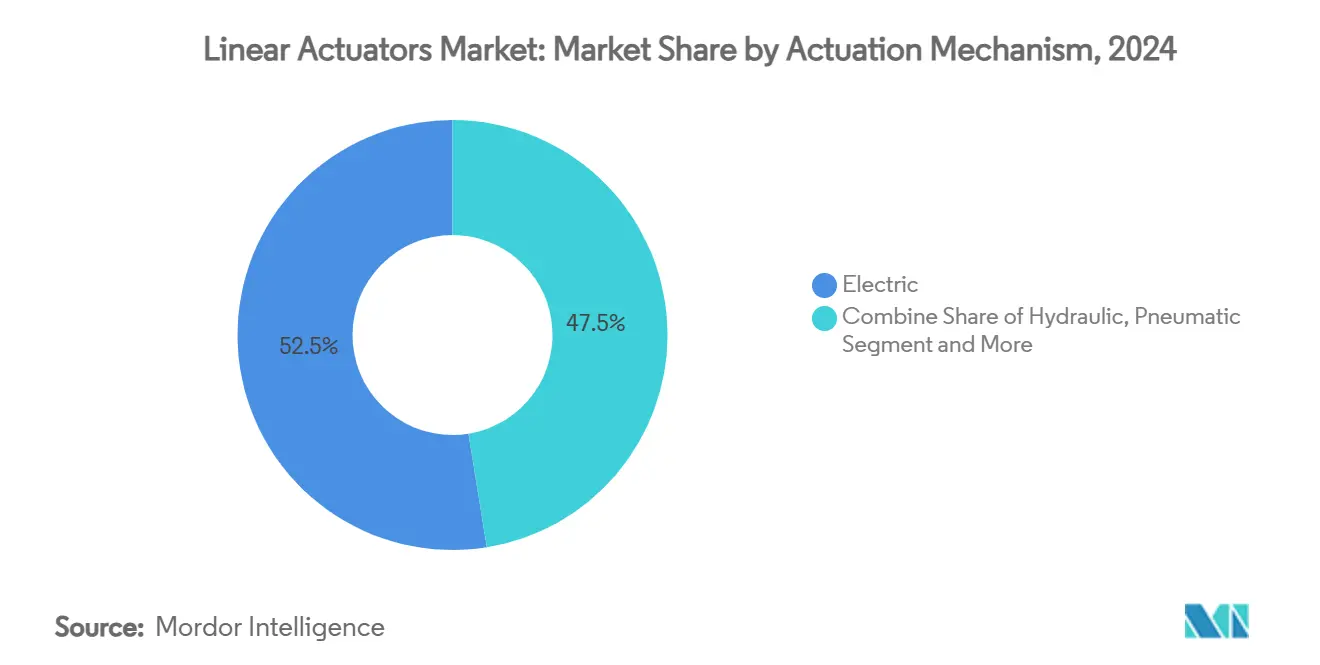

- By actuation mechanism, electric actuators captured 52.54% of the linear actuators market share in 2024 and are forecast to compound at an 8.56% CAGR through 2030.

- By motion control technology, ball-screw drives led with 42.54% revenue share in 2024, while direct-drive linear motors are projected to expand at a 7.45% CAGR.

- By end-use industry, industrial automation accounted for 28.53% of the linear actuators market size in 2024; healthcare and medical devices are advancing at a 9.01% CAGR to 2030.

- By load capacity, the 2-10 kN range held 33.57% share of the linear actuators market size in 2024, whereas sub-2 kN units are growing at a 7.89% CAGR.

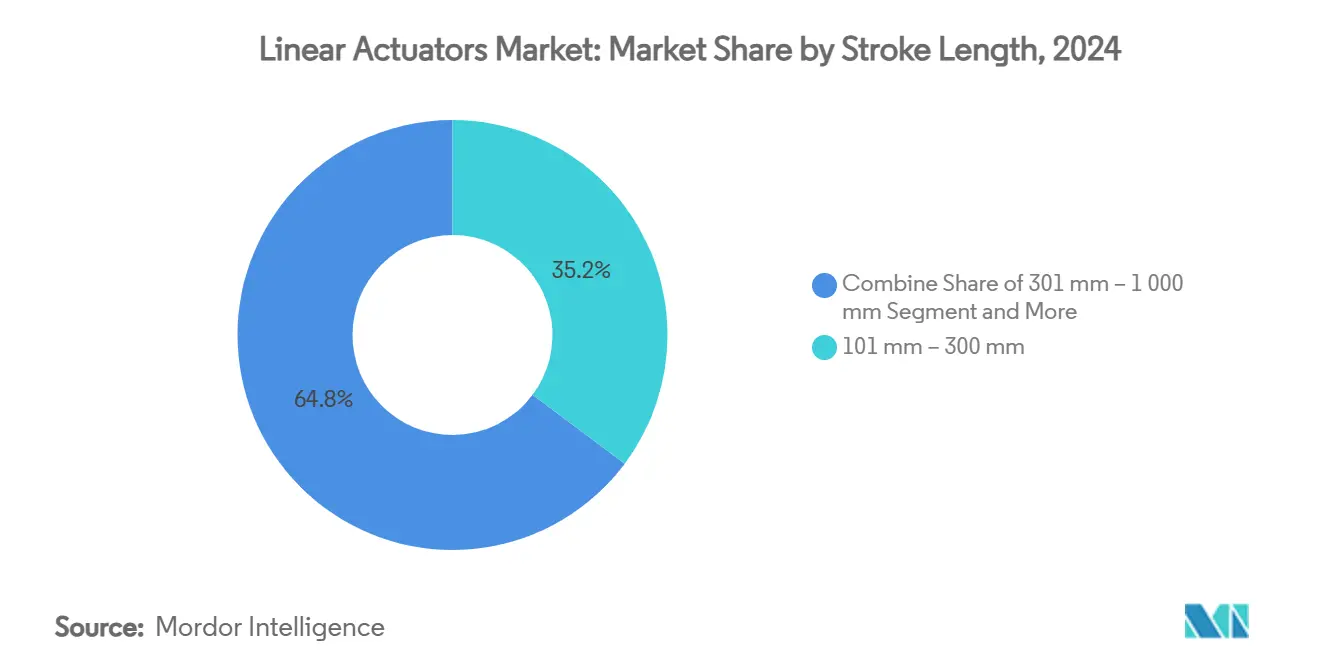

- By stroke length, 101-300 mm variants controlled 35.21% share in 2024; strokes below 100 mm exhibit the fastest 8.95% CAGR.

- By geography, North America commanded 38.46% of the linear actuators market share in 2024, and Asia-Pacific registers the highest 9.64% CAGR through 2030.

Global Linear Actuators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sustainability-led shift toward electric actuation | +1.8% | Global; strongest in EU and North America | Medium term (2–4 years) |

| Industry 4.0 automation surge in discrete and process plants | +1.5% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Aerospace push for More-Electric Aircraft subsystems | +0.9% | North America & EU | Long term (≥ 4 years) |

| Rapid robotics adoption in agriculture and warehousing | +0.7% | Global; early gains in North America, China | Medium term (2–4 years) |

| OEM preference for compact, modular smart actuators | +0.6% | Global | Short term (≤ 2 years) |

| Miniaturization demand in micro-surgical devices | +0.4% | North America, EU, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Sustainability-led shift toward electric actuation

Electric actuators deliver around 57% system efficiency, sharply above the 30% typical for hydraulic equivalents, giving plant owners immediate energy savings while eliminating leakage-related contamination risks in regulated industries. Parker Hannifin lowered Scope 1 and 2 greenhouse-gas intensity by 52% between 2021 and 2024 by replacing fluid power with electric drives across its factories. The European Union’s Net-Zero Industry Act, which targets 40% local production of net-zero technologies by 2030, is steering capital toward electric motion solutions in renewable-energy and industrial-automation lines. Construction OEMs such as Bobcat demonstrated viability by launching a fully electric compact loader that uses smart linear actuators to replace every hydraulic circuit, cutting noise and maintenance while meeting job-site emissions limits.

Industry 4.0 automation surge in discrete and process plants

Smart electric cylinders furnish native position feedback and on-board diagnostics, feeding real-time data to predictive maintenance algorithms that reduce unplanned downtime by up to 30%. Emerson’s AVENTICS SPRA line offers interchangeable lead-screw, ball-screw, and roller-screw options so OEMs can right-size precision and load profiles for digital-ready projects. [1]Emerson, “Electric Linear Actuators,” emerson.comThe company’s Ovation 4.0 platform launched in 2024 pairs actuator telemetry with generative-AI analytics to optimize power-plant operations. Bosch Rexroth’s ctrlX AUTOMATION architecture pushes simulation twins to the edge, enabling millisecond-level adjustments in packaging lines. Decentralized control reduces cabinet wiring, speeds commissioning, and simplifies modular expansion—critical factors for high-mix, low-volume factories adopting the linear actuators market’s newest smart-drive designs.

Aerospace push for More-Electric Aircraft subsystems

Electromechanical actuators replace heavy hydraulic lines, lowering aircraft weight by 15-20% and eradicating fluid-leak failure modes. Curtiss-Wright’s dual-motor configurations deliver redundancy for primary flight-control surfaces in next-generation platforms. Permanent-magnet synchronous linear motors applied to landing-gear dampers cut sprung-mass displacement by 70%, improving ride quality and cutting energy draw in taxi phases.[2]Wang & Yao, “Vehicle Height Lifting Strategy...,” mdpi.com Saab integrates brushless motors with high power-to-weight ratios inside electromechanical flap actuators that help carriers hit fleet-wide decarbonization targets. These innovations collectively enlarge the aerospace demand base for the linear actuators market well beyond today’s secondary mechanisms.

Rapid robotics adoption in agriculture and warehousing

Field robots guiding seeders to centimeter-level accuracy lift yields by 10-15% while curbing chemical use. In warehouses, belt-driven electric actuators achieve 5 m/s vertical lifts, enabling next-hour order fulfilment without compressed-air infrastructure. Tolomatic’s servo linear press series provides programmable force curves that electricify former hydraulic stations and trim energy costs in assembly lines. Such capabilities anchor the linear actuators market as robotics proliferates in non-traditional sectors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in raw-material costs (steel, rare-earth magnets) | -1.2% | Global; China-centric supply chain | Short term (≤ 2 years) |

| High switching cost from legacy hydraulic systems | -0.8% | North America & EU industrial base | Medium term (2–4 years) |

| Limited force density of electric actuators in heavy-duty uses | -0.6% | Global; construction & mining | Long term (≥ 4 years) |

| Cyber-security risks in networked smart actuators | -0.4% | Global; critical infrastructure | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Volatility in raw-material costs (steel, rare-earth magnets)

Rare-earth magnets see annual price swings of 30–40%, and their supply remains highly concentrated in China, straining actuator makers who operate on tight OEM contracts. [3]National Defense Magazine, “Sourcing Rare Earth Magnets Posing Challenges,” nationaldefensemagazine.org Rising alloy surcharges for corrosion-resistant steel further cloud cost forecasts, pushing vendors to seek reclaimed magnet materials from end-of-life motors. Although recycling technologies progress, commercial-scale capacity will lag demand until late-decade, tempering short-term margins in the linear actuators market.

High switching cost from legacy hydraulic systems

Converting a single production line from hydraulics to electric actuation can run USD 50,000–200,000, dampening uptake in heavy-industry assets with long depreciation cycles. Electric cylinders above 25 kN often require oversize frames that consume floor space and complicate retrofits. Skills gaps add friction because maintenance crews versed in valves and pumps must master servo tuning and embedded diagnostics. Nevertheless, lifecycle analyses show 18–36-month paybacks once energy savings and lower fluid-management costs accrue, nudging cautious operators toward phased hybrid solutions that keep the linear actuators market expansion on track.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Actuation Mechanism: Electric Dominance Accelerates

Electric actuators seized 52.54% of the linear actuators market share in 2024 and are projected to grow at an 8.56% CAGR, propelled by regulatory pressure for oil-free production lines and the ease of syncing drive profiles with Industry 4.0 controllers. Hydraulic devices cling to heavy-duty niches such as steel-mill manipulators where >25 kN forces remain commonplace, yet even here high-voltage direct-drive tech is eroding the stronghold. Pneumatic cylinders persist in wash-down food plants thanks to simple layouts and low upfront cost, but their compressed-air losses weigh on sustainability audits, nudging operators toward hybrid electro-pneumatic options.

Demand momentum centers on software-defined motion. Integrated servo drives with IO-Link and Ethernet/IP simplify commissioning and give OEMs cloud-ready diagnostics. Kollmorgen’s 2025 iron-core DDL series delivers 8,211 N continuous at 400/480 VAC, removing transformers and shrinking control cabinets. These gains underpin the linear actuators market size leadership that electric drives enjoy and promise further share grabs as energy-efficiency mandates tighten worldwide.

By End-Use Industry: Healthcare Drives Precision Revolution

Industrial automation retained 28.53% of the linear actuators market size in 2024, thanks to pervasive use in pick-and-place, press-fit, and material-handling stations. Yet medical devices represent the fastest-rising vertical at a 9.01% CAGR through 2030. Robotic surgeries demand sub-micron positioning and sterilisable, oil-free mechanics. The FDA’s 2024 clearance of the HYDROS robotic platform underscores confidence in electromechanically actuated tools for minimally invasive procedures. Battery-electric vehicle makers also raise adoption by embedding linear drives in thermal-management flaps and active suspensions.

Healthcare’s surge rests on demographic pressures and reimbursement models that reward shorter hospital stays. Compact electric cylinders with magnetic encoders enable surgeons to manipulate tissue accurately while sensors capture force feedback for haptic consoles. As these precision requirements amplify, suppliers that tailor ultra-small, sterilisation-ready mechanisms will outpace general-purpose vendors across the linear actuators market.

By Load Capacity: Mid-Range Dominance Shifts Toward Miniaturization

The 2–10 kN bracket controlled 33.57% of revenue in 2024 because its force profile matches assembly, packaging, and cobot palletising needs. Yet sub-2 kN devices are forecast to climb at a 7.89% CAGR as smartphone, wearables, and endoscope producers push for lighter, quieter drives. THK answered this trend by adding Ø80 mm and Ø100 mm shafts to its Medium-Torque Ball Spline range so medical-imaging OEMs can boost torque within tight housings.

Rapid advances in magnetic-field-actuated micro-grippers capable of 340 mN forces and 20 ms response times further validate miniaturisation’s pull on the linear actuators market. On the opposite end, applications above 25 kN stay hydraulic for now, although multi-lead roller-screw designs are closing the gap by multiplying contact points and boosting life cycles under heavy loads.

By Stroke Length: Compact Applications Lead Growth

Strokes of 101–300 mm delivered 35.21% revenue in 2024, suiting automotive weld guns and carton-erector slides. Lengths below 100 mm are on course for an 8.95% CAGR as electronics assembly and minimally invasive surgical tools proliferate. LINAK’s LA33 serves this compact zone with up to 5,000 N thrust while fitting into confined medical carts.

For conveyors and palletisers, 301–1,000 mm strokes maintain strong demand, whereas extra-long travels often shift to rack-and-pinion rails. The linear actuators market adjusts by offering modular profiles that let OEMs stack identical carriages and tailor stroke without redesign, trimming engineering lead-times and inventory SKUs.

By Motion Control Technology: Ball-Screw Maintains Leadership

Ball-screws secured 42.54% market share in 2024 by balancing precision, load, and cost. Yet direct-drive linear motors are increasing at 7.45% CAGR because they abolish mechanical backlash, an asset in semiconductor steppers and DNA sequencers. Thomson Industries refreshed its metric ball-screw line in 2024 with higher dynamic loads while retaining standard footprints, guarding incumbency in the linear actuators market.

Belt-driven actuators fill the speed niche, now hitting 10 m/s in lightweight carton sorters. PBC Linear’s MTB 105, launched in 2024, encloses the belt to resist debris and corrosion in harsh factories. Engineers thus have a widening toolkit, selecting the optimal topology rather than compromising with a one-size-fits-all mechanism.

Geography Analysis

North America controlled 38.46% of the linear actuators market share in 2024, underpinned by entrenched aerospace and electric-vehicle ecosystems that require high-precision motion for flight-control surfaces and battery thermal flaps. Washington’s USD 6 billion clean-manufacturing grant pool stimulates domestic servo-drive investments, buffering suppliers against overseas material shocks. Demand also stems from retrofitting brownfield plants as industrial users chase federal energy-efficiency tax credits.

Asia-Pacific exhibits the fastest 9.64% CAGR through 2030, propelled by relentless electronics output and an expanding robotics footprint in China, Japan, and South Korea. Harmonic Drive Systems tripled Asia sales between 2022 and 2024, illustrating how local OEM clusters favour home-region suppliers that master precision gear and actuator integration. However, the region’s dominance in rare-earth supply both lowers component costs and exposes producers to export-control risks, making supply-chain redundancy a strategic priority.

Europe blends mature factory automation capacity with aggressive climate legislation. The Net-Zero Industry Act encourages on-shore production of renewable-energy hardware, creating new plants that embed electric cylinders in solar trackers and wind-turbine pitch systems. Festo’s centenary in 2025 showcased continued breakthroughs in digital-ready electromechanical drives, reinforcing the region’s technical leadership.

Competitive Landscape

The linear actuators market remains fragmented; the top five vendors collectively control close to 35%, leaving space for specialists that focus on medical, aerospace, or harsh-environment applications. Market leaders differentiate by embedding IoT firmware, edge analytics, and cybersecurity protocols that transform a commodity cylinder into a data-rich asset. Parker Hannifin’s Win Strategy targets 4–6% organic sales growth by extending electromechanical portfolios and applying operational excellence templates across acquired brands.

Consolidation persists. Emerson closed the Afag takeover to blend pick-and-place electric motion systems with its pneumatic family, creating a broader one-stop shop for OEMs seeking mixed-technology lines. Bosch Rexroth likewise partners with Kassow Robots, launching mobile cobot stations that use ctrlX CORE drives for untethered four-hour shifts—an illustration of how control software and power electronics increasingly shape purchase decisions.

White-space opportunities cluster around miniaturised medical devices and renewable-energy structures operating in salt spray or desert heat. Vendors able to certify biocompatibility, IP69K sealing, or high-voltage vacuum encapsulation can command margins exceeding industrial averages. Digital twin support, end-to-end lifecycle services, and zero-emission valve actuation partnerships—such as Emerson’s work with Laramie Energy—create additional moats. Competitive intensity is thus shifting from pure mechanics toward software, materials science, and ecosystem alliances.

Linear Actuators Industry Leaders

Emerson Electric Co.

ABB Ltd.

Parker-Hannifin Corp.

Bosch Rexroth AG

Thomson Industries Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Kollmorgen introduced high-voltage IC Ironcore DDL direct-drive linear motors supporting 400/480 VAC and continuous forces up to 8,211 N, trimming control-cabinet footprints.

- March 2025: Tolomatic showcased next-gen servo linear actuators at Automate 2025, highlighting precision-force profiles for factory-automation presses.

- February 2025: Bosch Rexroth unveiled a battery-powered mobile cobot station featuring KR810 seven-axis robots and ctrlX CORE controls, enabling four hours of autonomous operation.

- January 2025: Emerson partnered with Laramie Energy to deploy ASCO zero-emission electric dump valves that actuate faster than pneumatic predecessors while eliminating vented methane.

Global Linear Actuators Market Report Scope

| Electric |

| Hydraulic |

| Pneumatic |

| Mechanical and Others |

| Industrial Automation |

| Automotive |

| Aerospace and Defense |

| Healthcare and Medical Devices |

| Agriculture |

| Energy and Utilities |

| Up to 2 kN |

| 2 kN - 10 kN |

| 10 kN - 25 kN |

| Above 25 kN |

| Less than equal to 100 mm |

| 101 mm - 300 mm |

| 301 mm - 1 000 mm |

| More than 1 000 mm |

| Ball-screw Drive |

| Belt-drive |

| Direct-drive Linear Motor |

| Rack-and-Pinion and Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Actuation Mechanism | Electric | ||

| Hydraulic | |||

| Pneumatic | |||

| Mechanical and Others | |||

| By End-use Industry | Industrial Automation | ||

| Automotive | |||

| Aerospace and Defense | |||

| Healthcare and Medical Devices | |||

| Agriculture | |||

| Energy and Utilities | |||

| By Load Capacity | Up to 2 kN | ||

| 2 kN - 10 kN | |||

| 10 kN - 25 kN | |||

| Above 25 kN | |||

| By Stroke Length | Less than equal to 100 mm | ||

| 101 mm - 300 mm | |||

| 301 mm - 1 000 mm | |||

| More than 1 000 mm | |||

| By Motion Control Technology | Ball-screw Drive | ||

| Belt-drive | |||

| Direct-drive Linear Motor | |||

| Rack-and-Pinion and Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current linear actuators market size?

The linear actuators market size stood at USD 67.11 billion in 2025 and is forecast to climb to USD 91.36 billion by 2030.

Which actuation mechanism leads the market?

Electric actuators dominate, holding 52.54% of linear actuators market share in 2024 and expanding at an 8.56% CAGR.

Which end-use industry is growing the fastest?

Healthcare and medical devices register the highest 9.01% CAGR because surgical robotics and diagnostic equipment require high-precision, oil-free motion.

Why are direct-drive linear motors gaining traction?

They remove mechanical transmission components, delivering sub-micron accuracy and lower maintenance, which supports the 7.45% CAGR forecast for this technology.

Which region is the most lucrative for future growth?

Asia-Pacific shows the strongest outlook with a 9.64% CAGR, driven by large-scale electronics manufacturing, robotics adoption, and supportive industrial policies.

What is the biggest restraint for electric actuator adoption?

High switching costs from legacy hydraulic systems—often USD 50,000–200,000 per line—slow conversion in heavy-duty sectors despite favorable long-term operating economics.

Page last updated on: