Valves And Actuators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

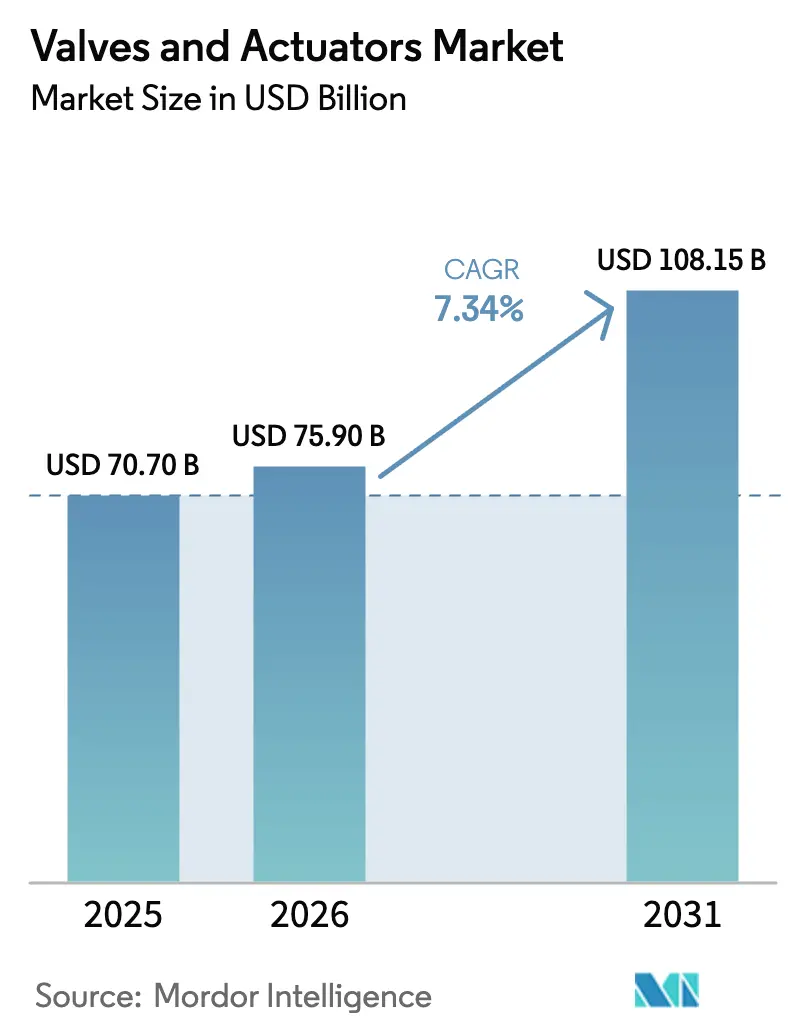

| Market Size (2026) | USD 75.90 Billion |

| Market Size (2031) | USD 108.15 Billion |

| Growth Rate (2026 - 2031) | 7.34% CAGR |

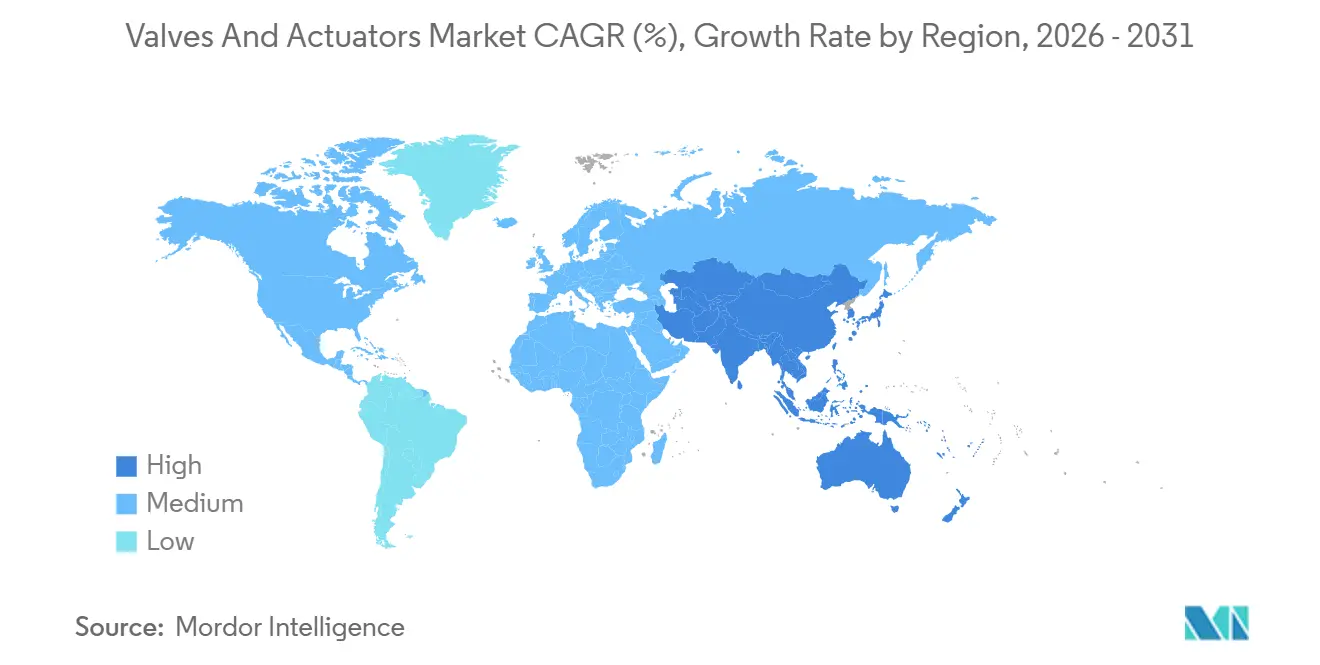

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

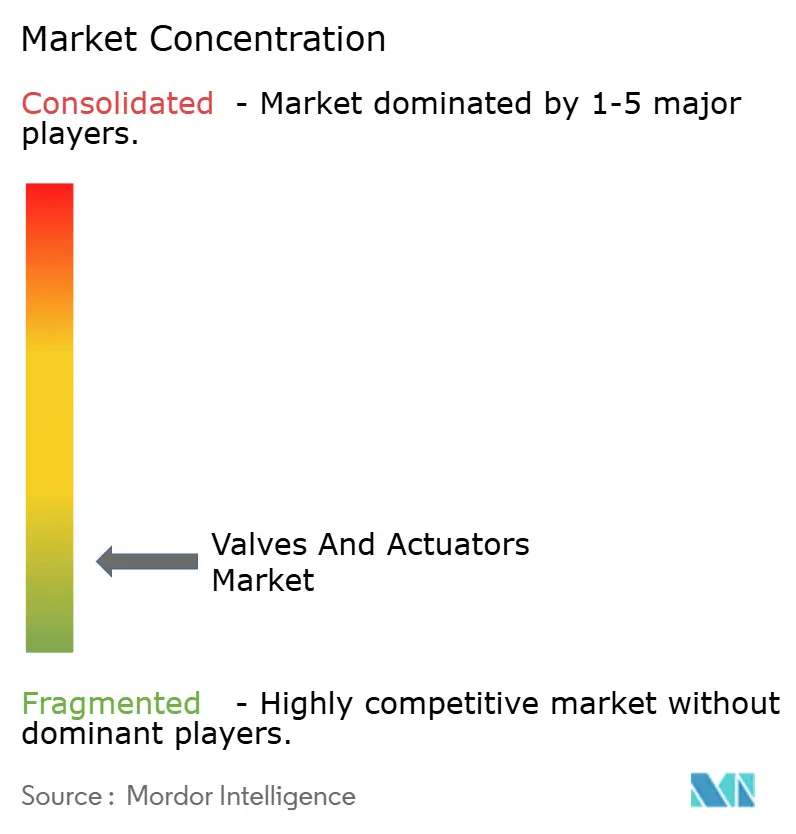

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Valves And Actuators Market Analysis by Mordor Intelligence

The Valves and actuators market size stood at USD 75.9 billion in 2026 and is projected to reach USD 108.15 billion by 2031 at a 7.34% CAGR. Digitalization mandates, fugitive-emission retrofits, hydrogen-ready designs and LNG infrastructure additions are synchronizing to sustain demand even as legacy refinery spending moderates. Ball valves remain the workhorse for shale wellheads, desalination feed lines and LNG loading arms, while predictive-maintenance software embedded in smart actuators is trimming unplanned downtime across chemical, water and power assets. Material selection is shifting toward stainless steel and super duplex alloys able to manage chloride-rich and hydrogen-embrittling media. At the same time, municipalities are deploying automated valve grids to stem non-revenue water, and OEMs are recasting their portfolios around cyber-secure, edge-analytical devices that comply with IEC 62443 standards.

Key Report Takeaways

- By product type, ball valves captured 28.73% of the Valves and actuators market share in 2025, while pressure relief and safety valves are advancing at an 8.21% CAGR through 2031.

- By actuator type, pneumatic actuators led with 37.63% revenue share in 2025 of the Valves and actuators market, whereas smart and intelligent variants are poised to rise at an 8.44% CAGR to 2031.

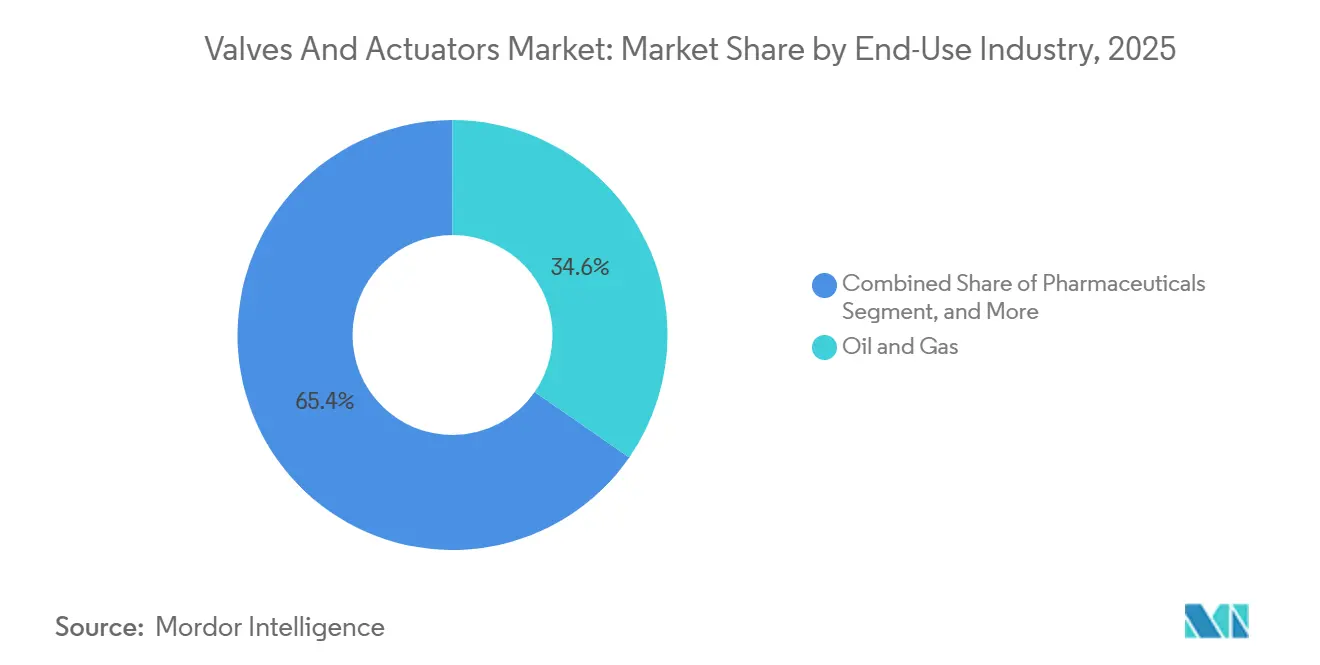

- By end-use, oil and gas accounted for 34.64% of demand in 2025 of the Valves and actuators market, but water and wastewater treatment is expanding at an 8.56% CAGR to 2031.

- By material, stainless steel commanded 42.62% share in 2025 of the Valves and actuators market, with plastic and composite alternatives growing at an 8.99% CAGR.

- By geography, North America held 38.73% of 2025 sales of the Valves and actuators market, whereas Asia Pacific is projected to climb at an 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Valves And Actuators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid adoption of Industry 4.0-enabled smart valves and actuators | +1.4% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Expansion of global desalination capacity, especially in MENA | +1.2% | Middle East and North Africa core, spillover to Asia Pacific | Long term (≥ 4 years) |

| LNG infrastructure build-out in North America and APAC | +1.3% | North America and Asia Pacific | Medium term (2-4 years) |

| Retrofit demand driven by fugitive-emission regulations | +1.1% | North America and Europe | Short term (≤ 2 years) |

| Shift to all-electric subsea production systems | +0.8% | Global offshore regions, concentrated in North Sea and Gulf of Mexico | Long term (≥ 4 years) |

| Hydrogen-ready valve designs for green-H₂ projects | +0.9% | Europe and Middle East, emerging in Asia Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Industry 4.0-Enabled Smart Valves and Actuators

Operators are embedding edge processors and wireless sensors in valve assemblies to detect torque deviations and seal wear, converting reactive maintenance into condition-based programs that cut refinery downtime worth USD 500,000 per day.[1]Fisher FIELDVUE DVC7K Digital Valve Controller, Emerson Automation Solutions, emerson.com Emerson’s Fisher FIELDVUE DVC7K digital controller captures vibration signatures, while similar positioners from Siemens and ABB communicate over HART and PROFIBUS to legacy DCS platforms. Energy-harvesting modules now power diagnostics without the need for batteries, thereby lowering ownership costs in remote pipeline corridors. Compliance with ISO 50001 is accelerating the adoption of smart pneumatics, as they can reduce air consumption by 15%-20%. The resulting productivity gains reinforce the positive 1.4% impact on the Valves and actuators market CAGR.

Expansion of Global Desalination Capacity

Middle Eastern utilities are contracting reverse-osmosis megaprojects to ease water scarcity, adding a combined 12 million m³-per-day capacity by 2028.[2]World Energy Investment 2025, International Energy Agency, iea.org Dubai’s Hassyan plant, for example, specified motorized butterfly valves with IP68 protection against salt-spray corrosion. Similar projects in Egypt and Algeria mirror these specifications, reinforcing a steady pipeline for duplex-steel ball valves and nickel-aluminum-bronze alloys that support the Valves and actuators market.

LNG Infrastructure Build-Out

North America is adding 50 million tpa of liquefaction capacity, each train outfitted with cryogenic ball valves and triple-offset butterfly valves rated to -162 °C. Rotork won contracts for stainless-steel pneumatic actuators able to withstand low-temperature brittleness, while Asia Pacific follows with floating storage and regasification units in Zhejiang and Dahej. High safety standards under API 6FA raise entry barriers, fortifying revenue for vendors with proven cryogenic portfolios.

Retrofit Demand From Fugitive-Emission Rules

The United States EPA methane rule obliges quarterly leak audits, compelling replacement of 1.2 million valves by 2027.[3]Final Rule on Methane Emissions, U.S. Environmental Protection Agency, epa.gov Low-emission graphite packing can cut leaks by 95%, and ISO 15848-1 certification has become a purchasing prerequisite. Penalties of USD 10,000 per non-compliant valve in the Permian Basin create an immediate retrofit wave, magnifying the short-term uplift in the Valves and actuators market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prolonged CAPEX slowdown in conventional oil and gas refining | -0.9% | Global, concentrated in Europe and North America | Medium term (2-4 years) |

| Supply-chain bottlenecks for castings and forgings | -0.7% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Skills gap in digital valve commissioning and maintenance | -0.5% | Global, most pronounced in emerging markets | Long term (≥ 4 years) |

| Cyber-hardening costs for connected flow-control assets | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prolonged CAPEX Slowdown in Conventional Oil and Gas Refining

Integrated majors are diverting capital toward renewable fuels and carbon capture, reducing refinery projects by 12% year-on-year in 2025. Deferred fluid catalytic cracking upgrades eliminate near-term orders for high-temperature gate and globe valves, squeezing margins for suppliers tied to the hydrocarbon cycle. Vendors are pivoting to aftermarket services and digital retrofits, yet the chill subtracts 0.9% from the Valves and actuators market CAGR.

Supply-Chain Bottlenecks for Castings and Forgings

Foundries in North America and Europe are running at 85%-90% utilization, stretching lead times for large-diameter bodies to 18 weeks. Chinese overflow capacity contracted after energy-rationing mandates, pushing nickel-surcharge premiums up 10%. Dual sourcing in India and South Korea eases bottlenecks but adds four to six weeks for ASME certifications. The resulting price escalation weighs on cost-sensitive municipal water projects, trimming 0.7% from overall growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Valve Product Type: Ball Valves Anchor Upstream Reliability

Ball valves accounted for 28.73% of the Valves and actuators market in 2025, highlighting their quarter-turn simplicity and bubble-tight shutoff, which is essential for wellhead isolation. Pressure relief and safety valves are forecast to grow at a rate of 8.21% through 2031, as petrochemical complexes upgrade to API 520 designs following high-profile overpressure incidents.

The product spectrum is splintering into niche certifications such as API 607 fire-safe and BS 6364 cryogenic approvals, consolidating supplier bases around firms that can finance multiple test rigs. Control and butterfly valves are gaining ground in desalination and HVAC networks, while plug-valve adoption in slurry services spreads from Chilean tailings dams to Indonesian bauxite mines. These shifts preserve the momentum of the Valves and actuators market.

By Actuator Type: Pneumatics Persist but Smart Systems Surge

Pneumatic actuators led with 37.63% revenue share in 2025, favored for intrinsic safety in explosive zones and compatibility with existing air loops. Smart electric models, however, are accelerating at an 8.44% CAGR as asset-performance software tracks stroke counts and torque profiles in real time.

Electric units are displacing pneumatics in water utilities where energy audits spotlight compressed-air costs, while hydraulic designs remain entrenched in subsea trees until all-electric systems scale. ABB’s MotorSense actuator, which harvests vibration energy to power onboard sensors, exemplifies cost-saving innovation. This bifurcation sustains healthy competition within the Valves and actuators market.

By End-Use Industry: Water Treatment Outpaces Oil and Gas

Oil and gas applications still represented 34.64% of 2025 demand, yet water and wastewater utilities are expanding at 8.56% through 2031 on the back of USD 55 billion in U.S. infrastructure funding. Automated valve grids reduce non-revenue water by 18% in pilot studies.

Chemical processors are embracing digital control to cut batch variability, while mining projects in Chile and Australia specify abrasion-resistant valves for mineral slurries. Pharmaceutical and food plants prioritize sanitary, single-use assemblies, underscoring a structural tilt that diversifies the Valves and actuators market.

By Material: Stainless Steel Dominates but Composites Gain

Stainless steel captured 42.62% share in 2025 thanks to its corrosion resistance in chloride and hydrogen environments. Plastic and composite valves are growing at 8.99%, riding demand for PVDF-lined units that eliminate ion leaching in drug manufacturing.

Alloy prices surged when Indonesian nickel exports tightened, spurring exploration of cobalt-free alternatives for hydrogen duties. Composite options offer 30%-40% weight savings on offshore platforms, lowering crane rentals and installation risks. Such material innovation supports continuous evolution within the Valves and actuators market size discussion.

Geography Analysis

North America retained leadership in 2025 with 38.73% of global revenue as shale play monetization and Gulf Coast LNG projects collectively required up to 500,000 valves. Installed-base services generate nearly half of regional turnover, cushioning suppliers from project lulls. Asia Pacific is forecast to register an 8.55% CAGR through 2031, propelled by China’s coal-to-chemicals complexes and India’s smart-city water grids, trends that will steadily lift the Valves and actuators market size in the region.

Europe’s valve demand is driven more by replacement than expansion as the Industrial Emissions Directive compels chemical plants to retrofit low-emission stems every six months. Refineries, however, are shuttering or converting to biofuels, trimming orders for large-bore isolation valves. South America shows episodic spikes tied to Brazil’s pre-salt fields and Argentina’s Vaca Muerta pipelines, yet municipal water spending remains constrained by fiscal headwinds.

The Middle East and Africa rely heavily on desalination and petrochemical megaprojects. High-salinity feedwater cuts butterfly-valve life cycles to five-seven years, guaranteeing a steady aftermarket. Nigeria’s Dangote refinery and Egypt’s Zohr gas field have set precedents for large-scale procurement, though regional distributor networks are still maturing. These geographic dynamics collectively reinforce long-term growth prospects for the Valves and actuators market.

Regulatory Landscape

Compliance requirements are tightening across pressure integrity, functional safety, and actuator interoperability, increasing the documentation and testing burden for valve and actuator OEMs serving regulated industries. In the European Union, the Pressure Equipment Directive (Directive 2014/68/EU) continues to anchor conformity assessment for industrial valves, and the European Commission updated the list of harmonized standards via Commission Implementing Decision (EU) 2026/79 (January 2026). The update includes EN 16668:2025 for industrial valves, reinforcing the need for aligned technical files and traceability for EU end users.

Standards activity in 2024-2026 also reflects deeper scrutiny of automated valve assemblies and actuator interfaces. CEN published EN 17955:2024 on functional safety of safety-related automated valves (August 2024), while ISO issued ISO 5640:2024 (mounting kits) and later ISO 22109:2026 (gearboxes for valves, February 2026), supporting more standardized actuator attachment and gearbox requirements. In the United States, PHMSA updated pipeline safety regulations in July 2025 to incorporate the 25th edition of API Spec 6D for pipeline valves, and UL updated UL 125 (Flow Control Valves for Anhydrous Ammonia and LP-Gas) in January 2026, both of which shape procurement specifications for oil and gas midstream and hazardous-gas handling applications.

Value Chain Analysis

The value chain spans raw materials (carbon and stainless steels, duplex and nickel alloys, elastomers, electronics), component manufacturing (castings/forgings, stems, seats, seals, gearboxes, positioners), and valve and actuator assembly through certification and testing, then delivery via EPCs, OEM packages, distributors, and direct-to-end-user service networks. Certification and documentation checkpoints, such as EN 10204 3.1 material certificates and project-specific traceability, extend cycle times for critical-duty valves. At the same time, the move toward smart actuators adds embedded sensing, firmware, and cybersecurity hardening tasks that sit alongside traditional mechanical QA.

Constraints and bottlenecks remain concentrated in large cast and forged bodies and specialty materials, with lead times stretched by high foundry utilization and qualification requirements for engineered projects. Semiconductor and ultra-high-purity tool ecosystems also add validation steps, with qualification timelines commonly running 12 to 24 months. Specifications tied to standards such as SEMI F57 tend to favor suppliers that can support long validation cycles and contamination-controlled manufacturing, while distribution and aftermarket service remain central to margin capture through installed-base maintenance, spare parts, and retrofit programs (packing upgrades, actuator swaps, and digital positioner retrofits).

Competitive Landscape

The supplier landscape remains highly fragmented, with the top 10 suppliers accounting for a limited share of global sales, consistent with a low market concentration profile. Scale players such as Emerson, Flowserve, and Rotork monetize installed-base service contracts that deliver nearly half of automation revenue. Their digital-twin platforms differentiate them from regional specialists that compete on customization speed for hydrogen, cryogenic, and sanitary niches.

Technology innovation shapes current competition. ABB has patented a self-diagnosing actuator that predicts seal failure 90 days in advance, while Bürkert’s modular valve islands reduce panel footprints by 40%, offering tangible savings to pharmaceutical plants. Commodity pneumatic segments face intense pricing from Chinese imports that undercut Western catalogs by up to 30%, forcing incumbents to focus on smart, engineered-to-order product lines.

Mergers and acquisitions continue but at smaller scales, for instance, Crane’s 2024 purchase of a cryogenic-valve specialist deepened its LNG portfolio, whereas Emerson’s 2025 acquisition of a European smart-actuator firm added 120 wireless-sensor engineers. Compliance with IEC 62443 creates a cybersecurity moat, making certification capacity a decisive factor in upcoming bids and sustaining competition intensity within the Valves and actuators market.

Valves And Actuators Industry Leaders

Emerson Electric Co.

Schlumberger Limited

Alfa Laval Corporate AB

Flowserve Corporation

Crane Company

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digital retrofit and service-led opportunities are expanding as end users add connected diagnostics to installed valves and actuators to reduce downtime and standardize maintenance across multi-site operations. This aligns with the market shift toward IEC 62443-aligned, cyber-secure edge devices and positioners described in the report context, and it creates whitespace for suppliers combining actuator hardware with predictive maintenance software and field services that turn large installed bases into recurring revenue.

Large project pipelines in LNG and downstream upgrades continue to drive demand for engineered packages (including cryogenic valves, triple-offset butterfly valves, and automation scopes), alongside capacity additions by manufacturers. In Texas, ABB received additional orders from Bechtel in March 2026 for integrated automation and electrical scope on Rio Grande LNG Trains 4 and 5, while AMPO POYAM VALVES cited supply of approximately 15,000 valves for the first five trains, with Train 4 deliveries referenced by mid-July 2026, pointing to sizeable, multi-train valve demand tied to named infrastructure. On the supply side, Neway broke ground in April 2026 for Phase II of a high-end industrial valve project with intelligent manufacturing and IoT integration, targeting annual output above 56,000 units. That indicates continued investment aimed at shortening lead times and improving quality consistency for higher-specification valves and automated assemblies.

Recent Industry Developments

- June 2026: Flowserve completed the acquisition of the Trillium Flow Technologies Valves Division for USD 490 million plus working capital. The deal expands Flowserve's valve portfolio and installed base in nuclear and other power end markets, strengthening its position in engineered, compliance-intensive applications where lifecycle service capability is a differentiator.

- June 2025: Emerson announced the Fisher GX bolted bonnet globe valve and actuator system for the European market, emphasizing maintainability features such as a locknut design that supports actuator work without exposing process media. The launch targets regulated plants and retrofit work where uptime, worker safety, and leakage control influence valve replacement decisions.

- April 2024: Emerson introduced the ASCO Series 148/149 safety valve and motorized actuator for industrial fuel oil burner recirculation and safety shutoff duties. This expands offerings in safety-critical combustion and burner management applications, where packaged valve-actuator solutions simplify compliance and commissioning for end users.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the valves and actuators market is defined as the revenue generated from valves and actuator systems used to control, stop, and regulate the flow of liquids and gases across industrial and infrastructure applications, counted at the point of sale in USD.

Scope exclusions: We exclude labor-only installation services, plant-wide automation software, and unrelated piping items like flanges, gaskets, and generic fittings.

Segmentation Overview

- By Valve Product Type

- Ball

- Butterfly

- Gate/Globe/Check

- Plug

- Control

- Pressure Relief / Safety

- Other Valve Product Types

- By Actuator Type

- Hydraulic

- Pneumatic

- Electric

- Electro-hydraulic

- Mechanical

- Smart / Intelligent

- Other Actuator Types

- By End-Use Industry

- Oil and Gas

- Power Generation

- Chemical and Petrochemical

- Water and Wastewater

- Mining and Metals

- Pharmaceuticals

- Food and Beverage

- Pulp and Paper

- HVAC and Building Services

- Marine and Shipbuilding

- Other End-Use Industries

- By Material

- Stainless Steel

- Carbon Steel

- Alloy-based (Duplex, Inconel, etc.)

- Cast Iron

- Plastic and Composite

- Cryogenic-service Materials

- Other Materials

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- ASEAN

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We first built the market context from public, non-paywalled sources that can be checked and refreshed each year. Typical inputs include industrial production and manufacturing indicators from agencies such as the US Federal Reserve, energy and refinery capacity statistics from sources such as the US EIA, and water and wastewater datasets from sources such as US EPA and similar national regulators.

We also reviewed trade and supply signals, including shipment and customs trends from sources such as UN Comtrade, plus technical and adoption cues from patent databases, engineering standards bodies, and peer-reviewed journals that cover valve materials, sealing, and actuation. Company annual reports, investor presentations, and reputable industry press were used to understand demand drivers, pricing direction, and aftermarket dynamics. This desk list is illustrative, and other sources were included for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary discussions were used to pressure-test assumptions that are not consistently visible in public datasets, such as actuator attach rates by valve type, the split between OEM and replacement demand, and how pricing moves when material costs change. Interviews included manufacturers, distributors, EPC-linked stakeholders, and end-user procurement and maintenance teams across major regions, so desk research gaps could be closed and final totals cross-checked from more than one angle.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 31% | CXOs: 12% | APAC: 41% |

| Mid tier: 47% | Functional/Unit leaders: 38% | EMEA: 32% |

| Smaller Players: 22% | Managers: 50% | Americas: 27% |

Market-Sizing & Forecasting

Market sizing was built using a top-down approach where industrial activity and asset base indicators are translated into a valves and actuators demand pool, and then value is reconstructed through usage intensity and pricing. In practice, we tied the model to end-use signals such as refinery and petrochemical capacity additions, power generation investment cycles, municipal water and wastewater capex, and oil and gas project spend (onshore and offshore).

To keep the numbers realistic, totals were corroborated with selective bottom-up approximations, including sampled ASP ranges by valve type and actuation method, channel feedback on order books, and supplier-side sanity checks on regional shipment direction. Where bottom-up coverage was thin in a country or niche application, we used comparable industry intensity ratios, then validated again using interview feedback.

For forecasting, scenario analysis was used around a central case, since demand can shift with project timing and maintenance cycles. Key forward variables were industrial production outlook, energy capacity buildout, infrastructure spending pipelines, and expected changes in automation adoption and emission compliance retrofits, which were tuned using expert views on lead times and pricing progression.

Data Validation & Update Cycle

Before sign-off, outputs are triangulated against independent signals such as trade flow direction, major project awards, and regional industrial production trends, so the model stays tied to real-world activity. Outliers are flagged, assumptions are rechecked, and a second analyst review is completed to confirm that growth rates and year-to-year jumps are explainable.

Reports are refreshed annually, and interim updates are triggered when material events occur, such as a large regulatory change, a sharp commodity price move affecting materials, or a major shift in energy and infrastructure spending. Right before delivery, we do a final pass to confirm the latest available public indicators, and ensure interview takeaways are reflected in the numbers.

Mordor Intelligence's Valves and Actuators Market Size Versus Other Published Estimates

Published market numbers for valves and actuators can look far apart because category boundaries are drawn differently, and because pricing, currency timing, and what counts as industrial demand are not treated the same way. Differences also show up when one estimate leans more on optimistic project starts, while another emphasizes replacement demand and realized shipment patterns.

In this market, the biggest gap drivers usually come from whether the scope includes only industrial-use valves and actuators or also pulls in adjacent non-industrial demand, plus how actuator packages and smart add-ons are valued. Some estimates anchor on an earlier base year and apply a single growth rate across regions without rechecking end-use indicators, which can overstate the near-term market when large projects slip.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 75.90 B (2026) | |

| Global Consultancy A | USD 151.11 B (2024) | The figure is positioned as industrial valves and actuators and may use a wider inclusion set for industrial equipment revenue, which can pull in broader product bundles and earlier-stage project value rather than realized equipment demand. |

| Industry Publisher B | USD 89.57 B (2024) | The base year is earlier and the model appears to apply broad end-user segmentation with less visible adjustment for actuator attach rates, aftermarket intensity, and region-specific pricing, which can shift totals materially. |

The table shows that scope and timing choices can create large spreads even before forecasting starts. When the market is counted from equipment revenue tied to defined valve and actuation needs, then rechecked against end-use activity and pricing signals, the result is easier to trace and repeat, which is the sizing logic applied by Mordor Intelligence.

Key Questions Answered in the Report

How fast is the Valves and actuators market expected to grow through 2031?

The market is projected to expand from USD 75.9 billion in 2026 to USD 108.15 billion by 2031 at a 7.34% CAGR.

Which product type currently dominates global demand?

Ball valves led sales in 2025, accounting for 28.73% of global revenue thanks to their quarter-turn reliability in oil, gas and water applications.

What segment is growing the quickest?

Pressure relief and safety valves are forecast to register the fastest growth, rising at an 8.21% CAGR through 2031 as safety standards tighten.

Why are smart actuators gaining traction?

Intelligent electric actuators with embedded diagnostics enable predictive maintenance that cuts plant downtime and compressed-air costs, driving an 8.44% CAGR for the category.

Which region offers the strongest growth outlook?

Asia Pacific is set to record an 8.55% CAGR to 2031, propelled by industrial expansion in China and urban water investments in India.

Page last updated on: