Pneumatic Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 37.41 Billion |

| Market Size (2031) | USD 52.29 Billion |

| Growth Rate (2026 - 2031) | 6.93% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

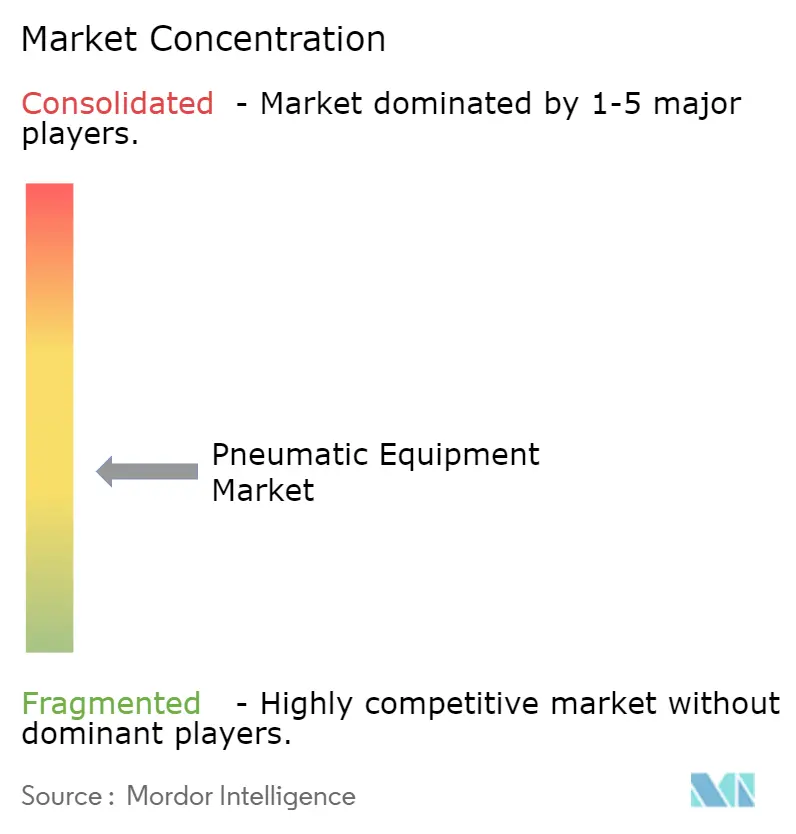

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pneumatic Equipment Market Analysis by Mordor Intelligence

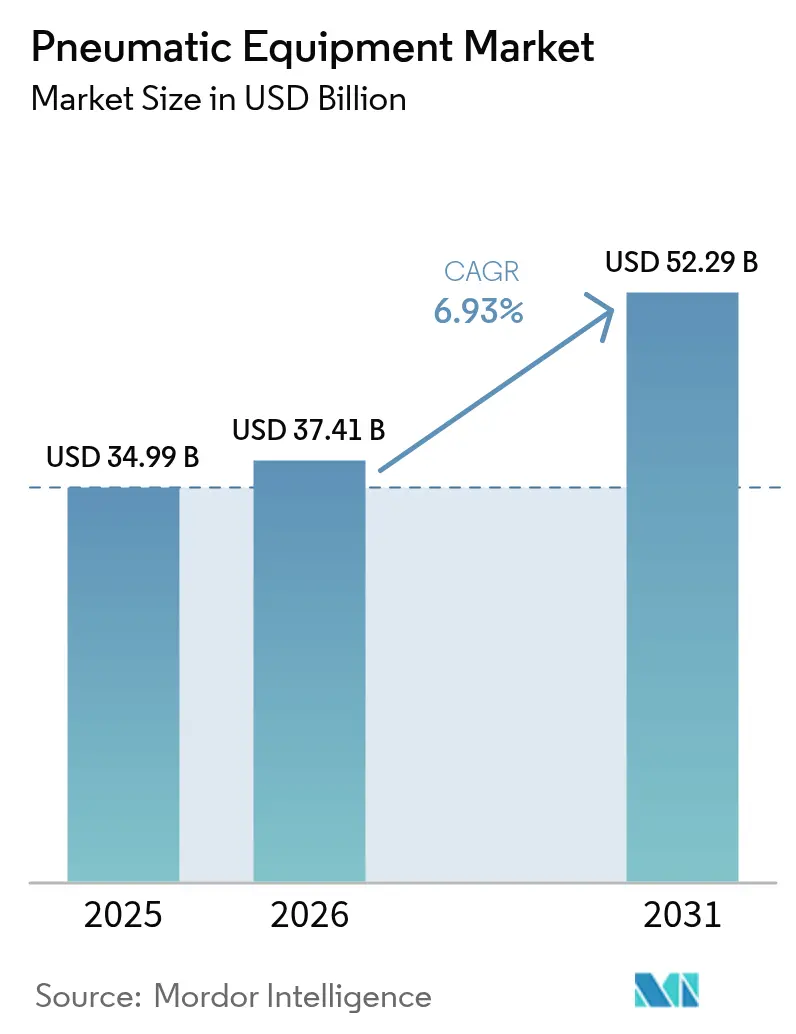

The pneumatic equipment market size in 2026 is estimated at USD 37.41 billion, growing from 2025 value of USD 34.99 billion with 2031 projections showing USD 52.29 billion, growing at 6.93% CAGR over 2026-2031. Industrial automation upgrades, energy-efficient compressed-air retrofits, and the fusion of pneumatic hardware with IIoT diagnostics are the primary growth catalysts. Demand spikes from semiconductor clean rooms, electric-vehicle battery lines, and hygienic food plants underscore the sector’s expanding application scope. Competitive intensity is rising as market leaders pair traditional pneumatics with digital monitoring to cut downtime and energy loss. At the same time, tightening efficiency rules in major economies are accelerating the shift toward hybrid electro-pneumatic solutions, giving suppliers a new avenue for differentiation.

Key Report Takeaways

- By component, valves led with 33.02% of pneumatic equipment market share in 2025, while actuators are projected to post the fastest 7.46% CAGR through 2031.

- By function, motion control dominated with 40.02% share of the pneumatic equipment market size in 2025; material handling is set to expand at an 7.95% CAGR to 2031.

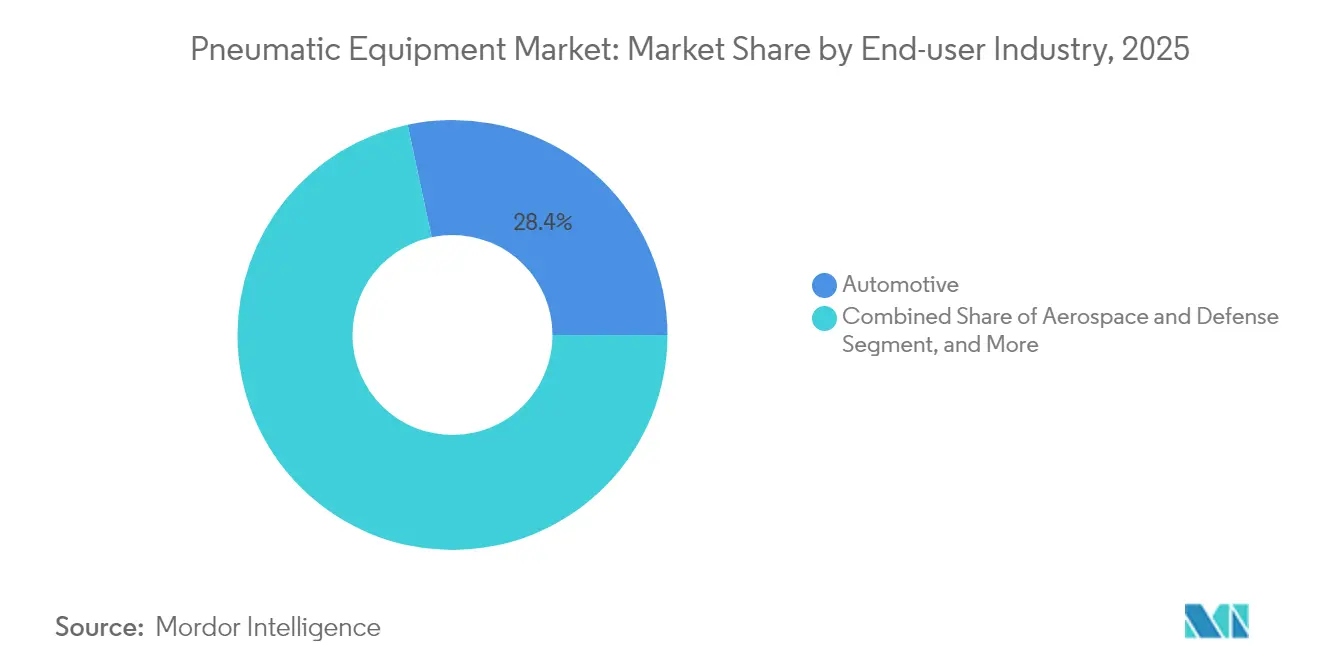

- By end-user industry, automotive held 28.35% of 2025 revenue, whereas life sciences record the highest 7.20% growth trajectory to 2031.

- By pressure range, low-pressure systems captured 45.12% of the 2025 base, yet high-pressure equipment is poised for the quickest 8.06% CAGR through 2031.

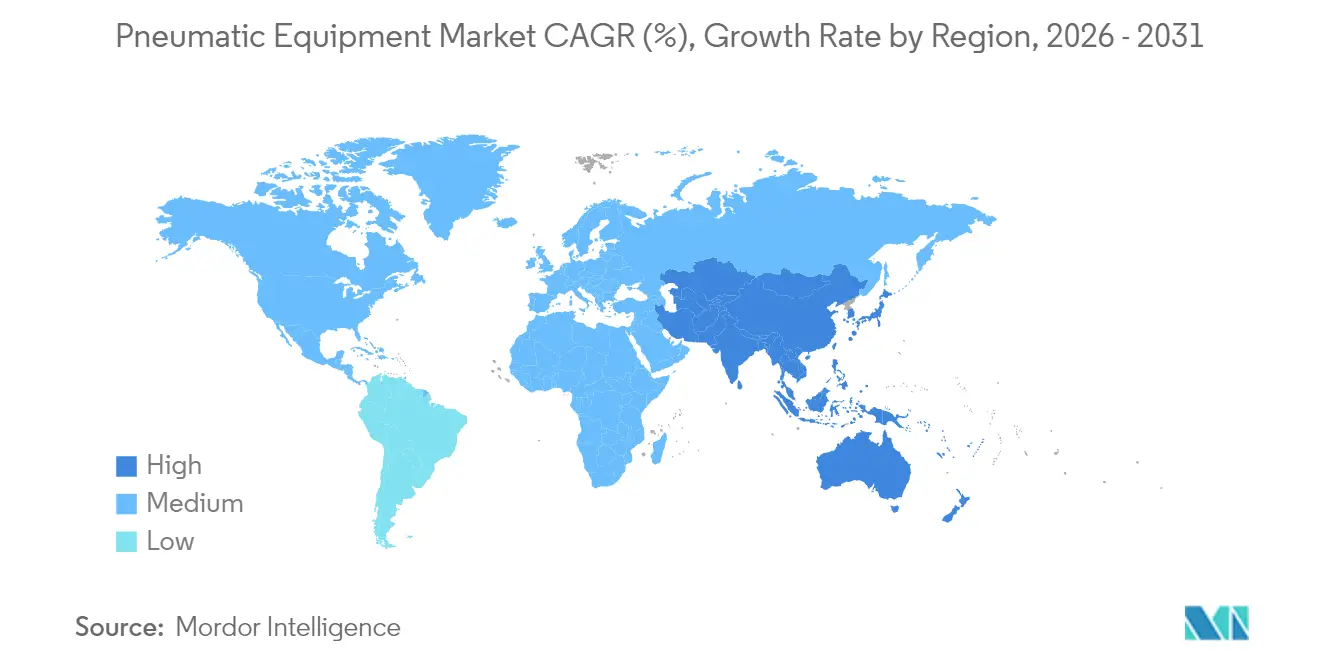

- By geography, North America accounted for 34.21% revenue in 2025, while Asia Pacific is advancing at a 7.66% CAGR and is on track to narrow the gap by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pneumatic Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing automation across industries | +1.8% | Global, with concentration in APAC and North America | Medium term (2-4 years) |

| Demand for energy-efficient compressed-air systems | +1.2% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Rapid growth of hygienic F&B processing lines | +0.9% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Expansion of EV manufacturing facilities | +1.1% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| Micro-fluidic assembly demand for micro-actuators | +0.6% | APAC and North America semiconductor hubs | Long term (≥ 4 years) |

| IIoT-enabled predictive maintenance retrofits | +0.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Automation Across Industries

Mass-scale factory digitalization is reshaping pneumatic design, prompting suppliers to embed sensors and wireless modules that allow predictive analytics. SMC’s EXW1 wireless node trims valve-manifold size by 86% and supports leading industrial Ethernet protocols, demonstrating how miniaturization and connectivity now converge in a single package.[1]SMC Corporation, “The EXW1 Wireless System,” smcusa.com For plant managers, real-time health data on cylinders and valves translates into fewer unplanned stops and faster root-cause analysis. Adoption momentum is especially strong in electronics, automotive, and packaged-goods plants building greenfield “lights-out” lines. Compliance audits under ISO 11011 give added weight to solutions that quantify compressed-air baselines, making digitally enabled pneumatics a compelling investment. Suppliers able to prove measurable OEE gains are winning head-to-head bids against legacy offerings.

Demand for Energy-Efficient Compressed-Air Systems

Compressed air accounts for roughly 10% of industrial electricity load, and new U.S. DOE efficiency rules effective January 2025 are forcing upgrades across the installed base. Atlas Copco’s hybrid compressor portfolio, which toggles between fixed-speed and VSD modes, can trim annual CO₂ output by 9 tons per unit while keeping pressure stability within ±0.1 bar.[2]Atlas Copco Group, “Hybrid Compressors for Sustainable Efficiency,” atlascopcogroup.com In Europe, ASHRAE 90.1-2022 inclusion of compressed air raises the bar for building designers as well. From a financial angle, leak rates often exceed 30% and cost individual factories tens of thousands of dollars in wasted power each year, incentivizing rapid payback retrofits. Enterprise sustainability officers now view leak-detection programs as low-hanging decarbonization wins, further accelerating demand for high-efficiency pneumatics.

Expansion of EV Manufacturing Facilities

Gigafactories assembling lithium-ion packs require class-0 compressed-air and nitrogen infrastructure to prevent particle contamination during electrode coating and cell sealing. Festo’s degassing cell integrates pneumatic cylinders with electric axes to pierce and vent pouch cells in one synchronized motion, illustrating the hybrid architectures emerging in battery lines [FESTO.COM]. With Asian battery supply chains clustering in Korea and China, local tier-one automakers are sourcing regionally to cut logistics risk, thereby boosting Asia Pacific demand. North American expansion from legacy carmakers broadens the opportunity set for vendors that can meet strict validation protocols and support multi-site rollouts.

IIoT-Enabled Predictive Maintenance Retrofits

Brownfield factories often run 10-year-old manifolds lacking diagnostics, so retrofittable sensor blocks and edge gateways offer an attractive upgrade path. Emerson’s Aventics platform channels pressure and flow data to cloud dashboards, enabling alerts before seal wear triggers downtime. Field case studies show that predictive algorithms can reduce unscheduled stoppages by 25% and cut mean-time-to-repair by 30%. The strongest uptake is in packaging and life-science plants where batch integrity and traceability are paramount. As subscription-based software revenues grow, leading vendors are evolving from hardware sellers into lifecycle solution partners.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High lifetime maintenance and energy costs | -1.4% | Global, particularly in energy-intensive regions | Long term (≥ 4 years) |

| Substitution by electric actuators in precision tasks | -1.1% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| ESG-driven penalties on compressed-air leakage | -0.8% | Europe and North America, with regulatory expansion to APAC | Medium term (2-4 years) |

| Shortage of ultra-clean compressed air for semicon fabs | -0.6% | APAC core semiconductor hubs, spill-over to North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Lifetime Maintenance and Energy Costs

Total cost-of-ownership audits reveal that energy can make up 77% of compressor lifecycle expense, dwarfing capital outlay. Leak-fix programs cut consumption, yet they demand instrumentation and staff hours that smaller plants often lack. Government studies in Australia report average leakage at 30%, confirming a global inefficiency pattern.[3]NSW Government, “Industrial Compressed-Air Guide,” energy.nsw.gov.au While IIoT sensors promise automated leak tracking, initial hardware and analytics subscriptions deter price-sensitive operators. The persistence of double-digit electricity inflation in parts of Europe amplifies scrutiny on pneumatic bills and nudges buyers toward alternative actuation modes when duty cycles permit.

Substitution by Electric Actuators in Precision Tasks

Electric rod actuators deliver 75–80% energy efficiency versus 10–20% for equivalent pneumatic cylinders, and cycle life now exceeds 100 million strokes. Falling motor-drive prices are narrowing the upfront cost gap, particularly in semiconductor tooling and medical-device assembly where micron-level repeatability matters. Suppliers such as SMAC are streamlining production to lower list prices, signaling an intensifying replacement threat. However, pneumatics still excel in high-force, harsh-environment, and fail-safe spring-return scenarios, giving the technology a defensible role in many heavy-duty lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Valves Preserve Leadership Amid Smart-Actuator

Upswing Valves captured 33.02% of the pneumatic equipment market share in 2025, underscoring their central role in pressure and flow governance inside automated lines. Their dominance persists because every circuit, from pick-and-place robots to bulk conveyors, relies on directional and proportional valves to orchestrate motion sequences. Growth leans toward compact, protocol-agnostic manifolds that shorten installation time and align with smart-factory architectures.

Actuators are accelerating with a 7.46% CAGR, reflecting manufacturers’ need for higher payload accuracy and faster cycle rates. Emerson’s XV Series pushes 350 NL/min in a slim footprint, allowing designers to shrink cabinets without sacrificing throughput. Air preparation units and precision fittings round out the component mix as clean-air mandates intensify, while sensor accessories flourish thanks to predictive-maintenance adoption. As a result, the pneumatic equipment market continues to migrate from stand-alone parts to fully integrated, data-rich assemblies.

By Function: Motion Control Dominant; Material Handling Gains Steam

Motion control held 40.02% of 2025 demand across the pneumatic equipment market, reflecting its ubiquity in linear slides, rotary tables, and pressing stations. The segment benefits from pneumatics’ favorable power-to-weight ratio and millisecond response, assets prized on high-speed assembly lines. Emphasis is now on feedback-ready cylinders that feed stroke data to MES platforms for traceability.

Material handling posts the swiftest 7.95% CAGR as e-commerce logistics fuels automated sortation centers. SMC’s RMH grippers, certified for cobot collaboration, illustrate how soft-touch gripping opens new SKU handling capabilities. Fluid control retains a niche in process industries, while vacuum generation expands in semiconductor wafer transport. Convergence is evident: advanced manifolds are combining positioning, gripping, and vacuum logic in one node, fortifying supplier stickiness in the pneumatic equipment market.

By End-user Industry: Automotive Still on Top, Life Sciences in Catch-Up Mode

Automotive lines commanded 28.35% of 2025 sales, keeping the segment at the forefront of the pneumatic equipment market size. Traditional uses include spot-weld gun actuation and body-in-white clamping; newer EV pack stations demand class-0 compressed air and finer pressure control. Rockwell Automation promotes modular cells that let line builders switch from ICE to battery variants with minimal downtime, a capability underpinned by smart pneumatics.

Life sciences register the fastest 7.20% CAGR as vaccine fill-finish suites and single-use bioreactors multiply. FDA cGMP rules push for stainless-steel valve blocks, redundant filters, and documentation-ready sensor kits, all of which deepen integration needs between OEMs and pneumatic suppliers. Packaging, electronics, and aerospace remain sizable niches, each with specialized cleanliness, force, or redundancy specifications that sustain healthy diversity within the pneumatic equipment industry.

By Pressure Range: Low-Pressure Prevalence Faces High-Pressure Niches

Low-pressure (less than 7 bar) systems delivered 45.12% revenue in 2025, supported by energy-optimization campaigns such as SMC’s 4-bar factory initiative, which promises CO₂ and cost cuts without throughput loss. Lower operating levels pair well with modern high-efficiency tooling, extending compressor life and shrinking leaks.

High-pressure (above 15 bar) units, though smaller in base, exhibit an 8.06% CAGR driven by aerospace fatigue testing, injection molding, and hydrogen refueling skids. Vendors are investing in composite-wound receiver tanks and advanced sealing to handle the added stress. Mid-pressure solutions bridge both worlds, enabling balanced force and economy for general industry. This dynamic keeps suppliers targeting tailored offerings rather than one-pressure-fits-all approaches, sustaining expansion across the pneumatic equipment market.

Geography Analysis

North America generated 34.21% of global 2025 revenue owing to mature aerospace, pharmaceutical, and automotive sectors that demand high-specification solutions. Siemens’ USD 10 billion commitment to new Texas and California plants illustrates the region’s ongoing reshoring trend, which lifts component orders for motion, valve, and compressor packages. Imminent DOE compressor rules are sparking retrofit waves that stabilize equipment replacement cycles.

Asia Pacific posts the steepest 7.66% CAGR and is set to narrow the gap by 2031 as China, India, and ASEAN states erect new fabs and battery plants. Atlas Copco’s USD 46.5 million purchase of Korea-based Kyungwon Machinery signals strategic moves to localize supply and meet skyrocketing regional demand. Government incentives for semiconductor self-reliance in India and Vietnam add fresh pull for ultra-clean pneumatics.

Europe maintains a solid share, buoyed by stringent energy and sustainability directives. Bosch Rexroth’s EUR 160 million plant in Mexico underscores European OEMs’ split-market strategy: retain R&D at home while building cost-effective capacity near the U.S. customer base. Smaller but rising opportunities in South America and the Middle East hinge on petrochemical diversification projects that require rugged high-pressure pneumatic arrays, adding incremental volume to the pneumatic equipment market.

Competitive Landscape

The pneumatic equipment market shows moderate consolidation as top players blend hardware proficiency with software analytics. Festo, SMC, Parker-Hannifin, and Emerson collectively channel double-digit R&D budgets into sensor-rich valves and cloud dashboards that convert air data into actionable OEE insights. Patent filings on MEMS-based proportional valves highlight a migration toward finer pressure modulation suited for micro-assembly lines.

Strategic M&A is a key lever. Emerson’s Aventics buyout deepens fluid-automation intellect, while Ingersoll Rand’s bolt-ons in nitrogen generation widen its downstream reach. Applied Industrial Technologies’ USD 260 million Hydradyne deal adds fluid-power distribution heft and accelerates aftermarket parts access. Such moves aim to lock in regional presence and round out product gaps, maintaining a robust defense against niche challengers.

Emergent disruptors target wireless, battery-powered sensor nodes that clip onto legacy actuators, promising leak alerts within minutes. Simultaneously, ESG-focused innovators such as Kathairos pioneer zero-emission nitrogen-powered devices for oil-field pads, carving out green-premium niches. Established brands counter by pledging carbon-neutral operations, evidenced by Festo’s German sites achieving neutrality in 2023, an initiative that resonates with OEMs chasing Scope 3 reductions.

Pneumatic Equipment Industry Leaders

Emerson Electric Co.

SMC Corporation

Siemens AG

Festo SE and Co. KG

Janatics India Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Applied Industrial Technologies finalized its USD 260 million Hydradyne acquisition to deepen fluid-power distribution.

- March 2025: Milton Industries, backed by Levine Leichtman Capital, purchased Arrow Pneumatics, expanding air-preparation portfolios.

- March 2025: Siemens pledged USD 10 billion to boost U.S. capacity, including two new plants projected to create 900 jobs.

- March 2025: Atlas Copco agreed to acquire Korea’s Kyungwon Machinery for USD 46.5 million, adding 126 staff and bolstering regional compressor coverage.

Global Pneumatic Equipment Market Report Scope

Pneumatic equipment refers to systems and components that utilize compressed air or pressurized gas to perform various types of work. These systems are commonly found in industrial manufacturing, transportation, medical equipment, and other applications. Pneumatic equipment includes various components such as air brakes, air compressors, pneumatic tools, pneumatic actuators, and pneumatic pumps.

The pneumatic equipment market is segmented by type of equipment (actuators, valves, and fittings, other type of equipment), end-user industry (automotive, food and beverage processing and packaging, aerospace and defense, life sciences, chemicals and petroleum, industrial, other end-user industries), and geography (North America [United States, Canada], Europe [United Kingdom, Germany, France, and the Rest of Europe], Asia-Pacific [China, Japan, India, and the Rest of Asia-Pacific], Latin America, and the Middle East & Africa). The report offers the market size in value terms in USD for all the abovementioned segments.

| Actuators |

| Valves |

| Air Preparation Units (FRLs) |

| Fittings and Tubing |

| Air Compressors |

| Vacuum Generators |

| Accessories |

| Motion Control |

| Fluid Control |

| Material Handling |

| Vacuum Creation |

| Power Generation / Air Supply |

| Automotive |

| Food and Beverage Processing and Packaging |

| Aerospace and Defense |

| Life Sciences (Pharma and Medical Devices) |

| Electronics and Semiconductor |

| Chemical and Petrochemical |

| Packaging Machinery |

| Other End-user Industries |

| Low Pressure (less than 7 bar) |

| Medium Pressure (7 - 15 bar) |

| High Pressure (above 15 bar) |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN-5 | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Actuators | ||

| Valves | |||

| Air Preparation Units (FRLs) | |||

| Fittings and Tubing | |||

| Air Compressors | |||

| Vacuum Generators | |||

| Accessories | |||

| By Function | Motion Control | ||

| Fluid Control | |||

| Material Handling | |||

| Vacuum Creation | |||

| Power Generation / Air Supply | |||

| By End-user Industry | Automotive | ||

| Food and Beverage Processing and Packaging | |||

| Aerospace and Defense | |||

| Life Sciences (Pharma and Medical Devices) | |||

| Electronics and Semiconductor | |||

| Chemical and Petrochemical | |||

| Packaging Machinery | |||

| Other End-user Industries | |||

| By Pressure Range | Low Pressure (less than 7 bar) | ||

| Medium Pressure (7 - 15 bar) | |||

| High Pressure (above 15 bar) | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN-5 | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How big is the pneumatic equipment market in 2026?

The pneumatic equipment market size is USD 37.41 billion in 2026 and is projected to reach USD 52.29 billion by 2031.

What is the forecast CAGR for pneumatic equipment through 2031?

The sector is expected to post a 6.93% CAGR between 2026 and 2031.

Which component segment grows the fastest?

Actuators lead growth with a 7.46% CAGR, driven by demand for higher-precision motion in automated lines.

Which region is expanding most rapidly?

Asia Pacific records the quickest pace at 7.66% CAGR through 2031, propelled by battery and semiconductor investments.

What regulation is influencing compressor upgrades in the United States?

New DOE energy-efficiency standards for rotary air compressors, effective January 2025, are triggering nationwide retrofits.

Page last updated on: