Advanced Surface Movement Guidance And Control Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

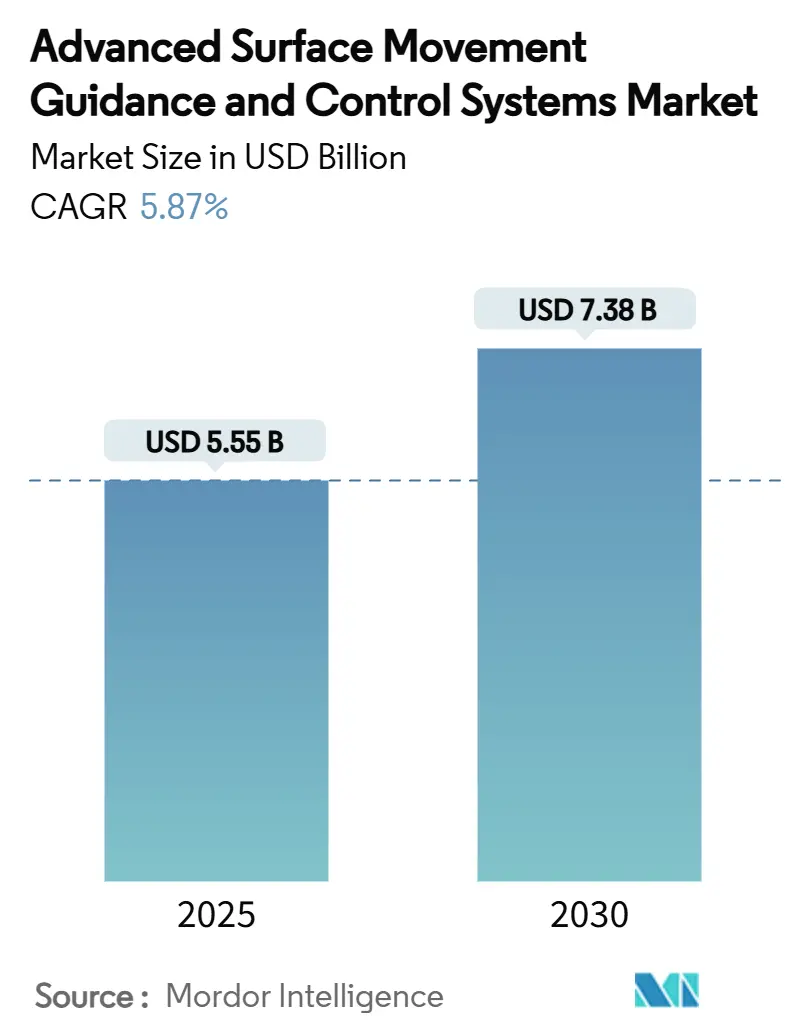

| Market Size (2025) | USD 5.55 Billion |

| Market Size (2030) | USD 7.38 Billion |

| Growth Rate (2025 - 2030) | 5.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

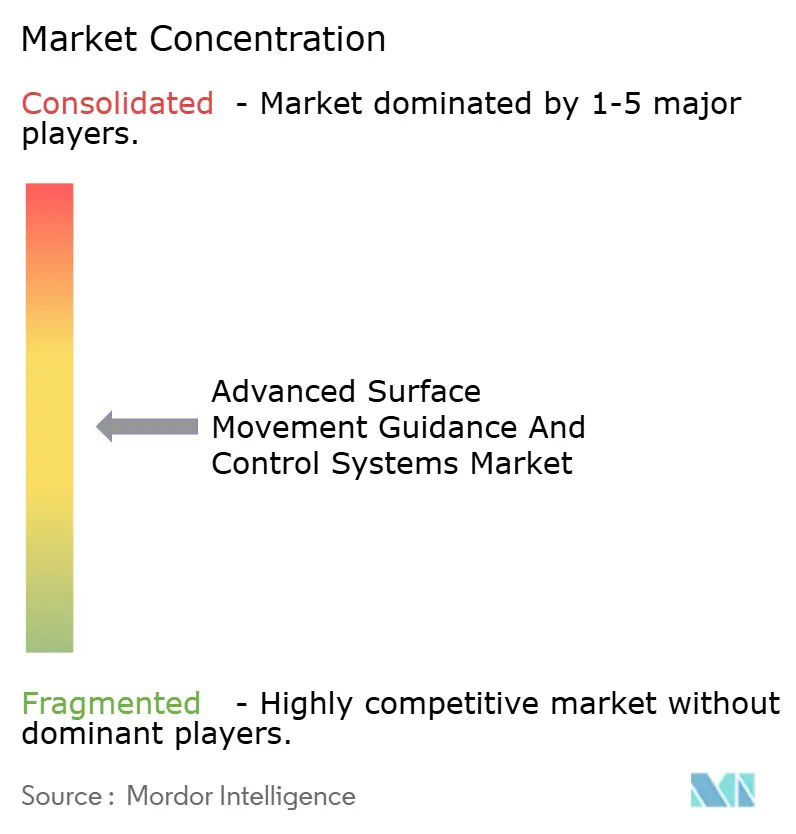

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Advanced Surface Movement Guidance And Control Systems Market Analysis by Mordor Intelligence

The airport surface movement guidance and control systems market size is pegged at USD 5.55 billion in 2025. It is projected to advance to USD 7.38 billion by 2030, translating into a 5.87% CAGR for the review period. The figure underlines how the accelerating return of passenger volumes, rising runway-capacity projects, and stricter low-visibility rules converge to establish surface-movement automation as a core safety layer in daily airport operations. While legacy visual control methods remain adequate at a handful of low-traffic aerodromes, most hubs now treat multilateration arrays, high-definition surface radars, and intelligent lighting systems as non-negotiable infrastructure because the complexity of modern ground environments pushes human reaction times to their operational limits. Airports that deployed Level 2 or higher solutions during the pandemic downturn now report faster taxi-out times, fewer runway incursions, and measurable fuel savings, proof that the financial logic of advanced surveillance is as compelling as its safety rationale. As a result, procurement pipelines continue to lengthen, with European and North American projects driven mainly by regulatory mandates and Asia-Pacific programmes powered by airport capacity additions and brand-new greenfield sites. Large hardware orders, however, only tell part of the story. The bigger strategic narrative is that decision makers increasingly view A-SMGCS as the digital entry point to wider smart-airport architectures that link stand allocation, turn-around management, passenger analytics, and vertiport integration under a single data platform. Against that backdrop, the airport surface movement guidance and control systems market offers suppliers an opportunity set that extends well beyond conventional ground surveillance gear into cloud services, artificial-intelligence software, and cybersecurity upgrades, all of which are becoming integral to long-term concession contracts.[1]Source: EUROCONTROL, “Advanced Surface Movement Guidance and Control System (A-SMGCS),” eurocontrol.int

Key Report Takeaways

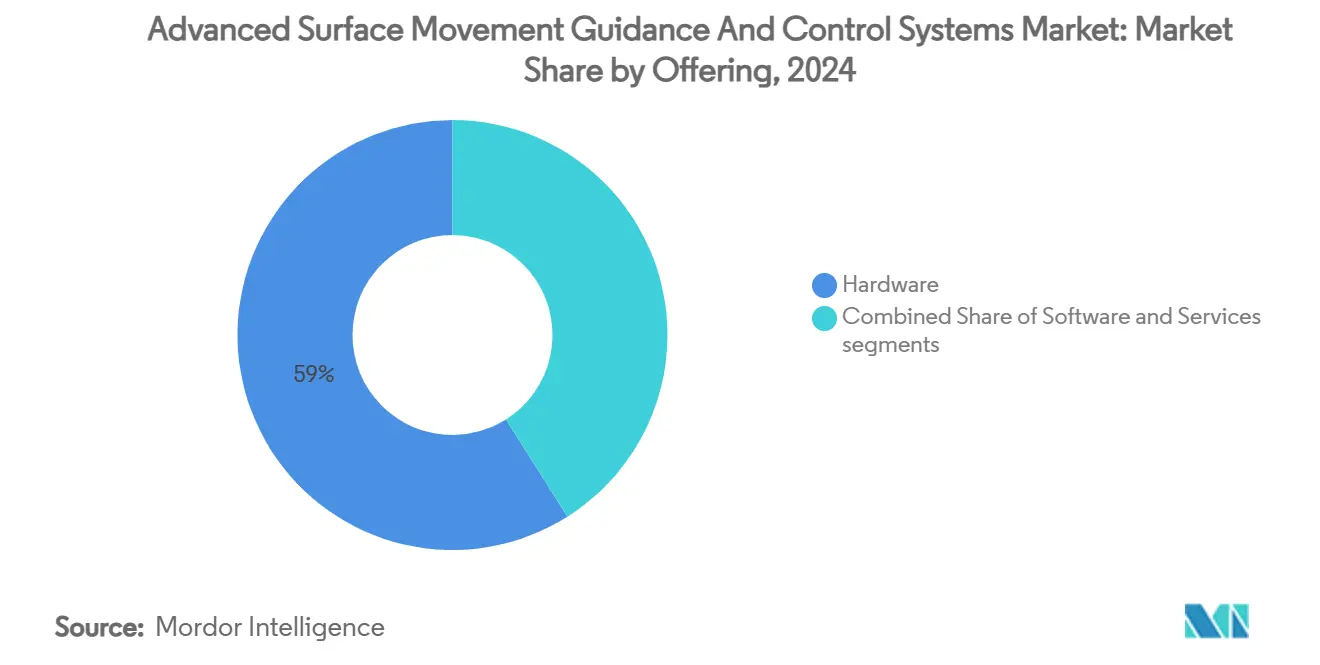

- By offering, the hardware segment led with 58.98% of airport surface movement guidance and control systems market share in 2024, whereas the services segment is forecasted to expand at a 7.34% CAGR through 2030.

- By implementation level, Level 2 solutions commanded a 45.70% share of the airport surface movement guidance and control systems market in 2024, and Level 4 deployments are projected to post the fastest 9.72% CAGR to 2030.

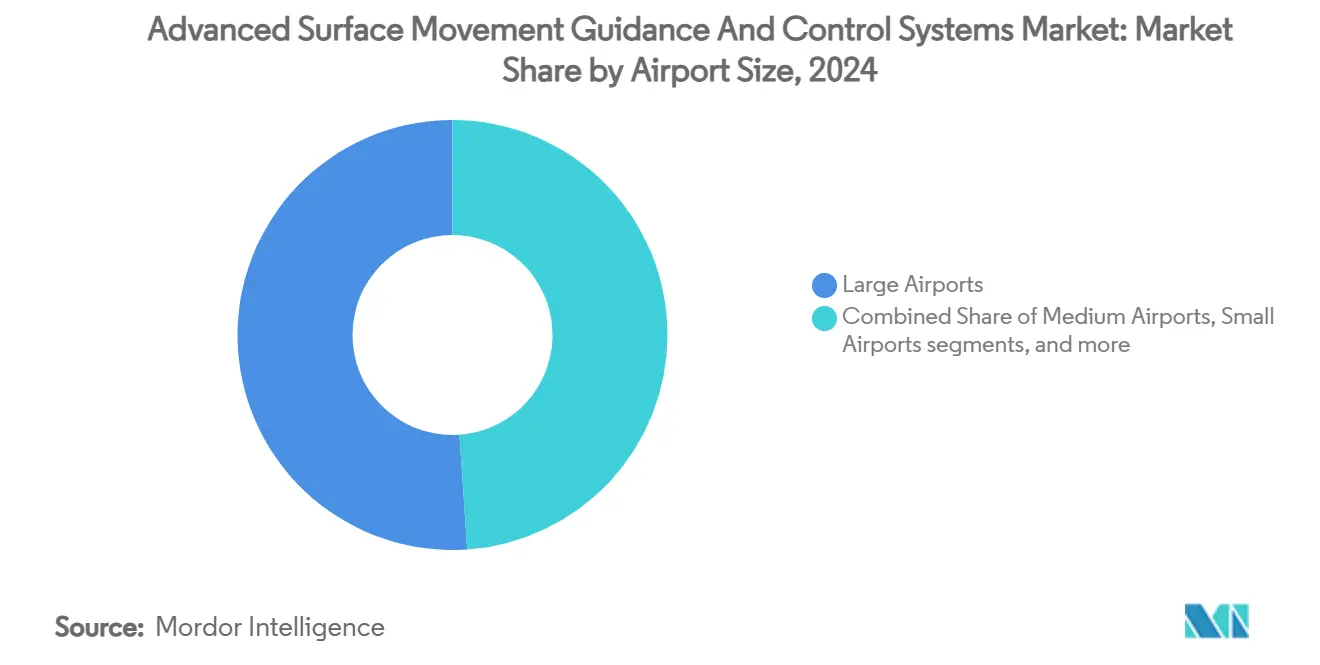

- By airport size, large hubs secured 51.10% revenue share in 2024, while small airports are set to register the highest 6.98% CAGR during the outlook window.

- By application, surveillance represented a 36.85% share of the airport surface movement guidance and control systems market size in 2024, but guidance functions are predicted to grow at a 7.65% CAGR through 2030.

- By geography, Europe dominated with a 31.74% stake in 2024; Asia-Pacific is positioned to deliver the fastest 7.14% CAGR over the same horizon.

Global Advanced Surface Movement Guidance And Control Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High-density runway expansion at Tier-1 hubs | +1.2% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Adoption of A-SMGCS Level 4 for “follow-the-greens” guidance | +0.9% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Integration with digital-tower programs | +0.8% | Global, led by Europe and North America | Medium term (2-4 years) |

| Mandatory low-visibility (RVR less than 1 200 ft) rules in the US and EU | +1.1% | North America and Europe | Short term (≤ 2 years) |

| AI-driven predictive conflict-alert algorithms | +0.7% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Vertiport certification standards requiring surface-movement automation | +0.5% | Global, initial focus in urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High-density runway expansion at Tier-1 hubs

Major international airports are undertaking parallel-runway additions and rapid-exit-taxiway programmes to handle post-COVID growth. However, each new slab of concrete multiplies the number of intersection points controllers must monitor. The United States alone earmarks USD 67.5 billion in eligible airport-development spending through 2029, with an appreciable share channeled to surface-movement projects.[2]Source: Federal Aviation Administration, “National Plan of Integrated Airport Systems (NPIAS) 2025-2029,” faa.gov Investments stretch beyond concrete to sensor fusion suites capable of tracking every aircraft, tug, and catering truck in three-second cycles, as illustrated by JFK’s Terminal One project, where a virtual ramp-control module manages 23 gates around the clock. Large airports facing taxi-out delays above 20 minutes during peak departure banks now view advanced A-SMGCS as the only scalable answer to capacity pressure because building additional runways without digital coordination risks shifting bottlenecks from the sky to the apron.

Adoption of A-SMGCS Level 4 for “follow-the-greens” guidance

Full automation introduces dynamic taxi-route lighting that changes in real time as aircraft progress from stand to runway, a concept verified in SESAR trials at Munich, where controller workload dropped measurably and holding times fell across every studied flight bank. The technology couples precision LED lighting arrays with 4D trajectory engines that amend clearances without additional radio calls, turning what used to be a paper-strip procedure into a digital handshake between tower and cockpit. Implementation costs, however, remain high because airports must install kilometres of individually addressable lights and certify them against fail-safe requirements. For now, therefore, only top-tier hubs in Europe, Singapore, and the Gulf are moving beyond Level 3, but regulatory agencies increasingly frame Level 4 as the long-run benchmark for net-zero taxiing emissions and capacity optimisation, building a clear future business case despite today’s capital hurdles.

Integration with digital-tower programs

Remote-tower centres in Sweden, Norway, Germany, and the United States pool high-resolution visual feeds, surface-movement radar, and multilateration tracks into panoramic displays that rival, and sometimes surpass, the field of view from conventional glass towers. Saab’s r-TWR at NATO Air Base Geilenkirchen, certified in early 2025, highlights how the fusion of military-grade encryption, cyber-hardened sensors, and commercial off-the-shelf optics can support simultaneous operations of multiple fast-jet types under adverse weather. Digital-tower adoption catalyses A-SMGCS upgrades because the data backbone that drives panoramic displays also feeds conflict-detection and routing engines, lowering incremental cost for airports to add higher-level functions. Smaller aerodromes also benefit since one remote-tower-plus-A-SMGCS suite can supervise several low-traffic fields, a model already trialed in Spain and Australia.

Mandatory low-visibility (RVR less than 1 200 ft) rules in the US and EU

Regulators now demand automated surveillance whenever visual reference drops below 1,200 ft, converting what was previously viewed as an operational upgrade into a compliance necessity. The FAA’s AC 120-57C codifies performance specifications for surface-movement aids that cover range, latency, alert logic, and redundancy. European authorities mirror the approach through EUROCONTROL guidance, ensuring interoperability across 30+ states. The rules affect Category III runways, taxiways, and aprons, pushing airports to integrate surveillance layers far beyond the traditional manoeuvring area. Airlines gain measurable benefits because fewer missed approaches and divert decisions translate directly into fuel savings and schedule resilience, reinforcing management’s appetite to fund compliant A-SMGCS deployments ahead of the deadlines.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Budget freezes at secondary airports post-COVID | -1.3% | Global, particularly acute in developing markets | Short term (≤ 2 years) |

| Cyber-hardening gaps in legacy surveillance sensors | -0.8% | Global, concentrated in airports with older infrastructure | Medium term (2-4 years) |

| Spectrum-allocation delays for multilateration beacons | -0.6% | Global, regulatory coordination challenges | Medium term (2-4 years) |

| Limited ROIs for Level 4 deployments at less than 2 million pax airports | -0.9% | Global, affecting small to medium airports | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Budget freezes at secondary airports post-COVID

Regional gateways that rely heavily on leisure traffic or a single anchor carrier saw aeronautical revenues fall sharply in 2020-2022 and have yet to regain pre-crisis capital budgets. Many must now replace aged ground vehicles and passenger-facilitation equipment before contemplating multilateration upgrades. Multilateral-development-bank grants cover some safety items, but the typical loan envelope is insufficient for complete A-SMGCS suites, forcing management to phase implementation across multiple fiscal cycles. The result is a widening technology gap between megahubs equipped with AI-backed safety nets and secondary fields still operating single-channel surface radars, raising systemic safety concerns as traffic rebounds.

Cyber-hardening gaps in legacy surveillance sensors

Early-generation surface radars often lack encryption and rely on outdated operating systems that push patches only annually. EUROCONTROL highlights over 1,000 reported cyber events that touched air-traffic-management assets between 2020 and 2023. Airports, therefore, face a dual-cost dilemma: purchase new radars or pour scarce funds into security layers that may generate no additional operational benefit. US lawmakers note that 90% of critical ATC assets reached obsolescence status as early as 2021. Until finance teams carve out dedicated cybersecurity lines, upgrade orders risk slipping year after year, dampening near-term demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Hardware Dominance Drives Infrastructure Investment

Hardware captured 58.98% share of the airport surface movement guidance and control systems market size in 2024 because multilateration beacon arrays, surface-movement radars, antenna masts, and individually controlled airfield lights are the physical prerequisites for any automation layer. Procurement managers typically bundle these assets into multi-year capital plans aligned with runway-rehabilitation windows, ensuring economies of scale and minimal disruption to operations. Once sensors are in place, they serve as high-value data generators that feed software modules for up to 15 years, thereby locking in hardware’s primacy within the spending hierarchy. For suppliers, the implication is clear: the long lead-time visibility of hardware orders provides a stable revenue base even as software and services margins climb.

Services, however, are poised for a 7.34% CAGR, the fastest of all offering categories, because airports now look for turnkey partners that shoulder system-integration risk, train staff, and deliver performance-based service-level agreements. Outsourcing this complexity converts capital bills into predictable operating expenses and aligns with the concession-contract mindset of many privatized hubs. Meanwhile, software continues to carve out incremental share by embedding artificial-intelligence modules, predictive maintenance dashboards, and cloud-native APIs that extend A-SMGCS data to airline and ramp-handling stakeholders, creating ancillary revenue streams for vendors and airport IT departments.

By Implementation Level: Level 2 Maturity Balances Capability and Cost

Level 2 solutions owned 45.70% of the airport surface movement guidance and control systems market share in 2024, a testament to their sweet-spot positioning between operational benefit and financial feasibility. Unlike Level 1, which merely aggregates sensor tracks, Level 2 adds safety nets such as runway-incursion alerts and conflicting-clearance warnings that immediately raise situational awareness. Controllers adapt quickly because the interface builds on traditional radar screens, requiring minimal retraining and avoiding wholesale procedure rewrites.

Yet the growth spotlight falls on Level 4, slated for a 9.72% CAGR, as mega-hubs pursue net-zero taxiing and move toward digital share-tower paradigms. While the investment threshold is high—often topping USD 150 million for greenfield installations—the upside includes taxi-time cuts of 3-5 minutes per movement and fuel savings that airlines quantify at USD 10,000 per long-haul leg. Early European and Gulf adopters already fold Level 4 metrics into sustainability disclosures, forecasting that emissions savings alone cover about a third of the capital cost within a decade.

By Airport Size: Large Airports Lead While Small Facilities Accelerate

Large hubs secured 51.10% of 2024 revenue because they must handle hundreds of simultaneous ground actors, scheduled jets, cargo feeders, ground support equipment, and autonomous air-side buses under conditions under which surveillance failures carry catastrophic safety risk and massive commercial fallout. Consequently, boards approve capital plans that bundle runway repairs, pier extensions, and A-SMGCS upgrades into single mega-projects, ensuring synchronisation across civil works and digital systems.

Small airports, many of which serve as feeders to national networks, are on course for a 6.98% CAGR due to modular cloud-native offerings that slash up-front camera, server, and license fees. Vendors now pre-configure sensor kits based on traffic bands fewer than 20,000, 50,000, or 100,000 annual movements, simplifying procurement for operators with limited engineering capacity. The democratisation effect is evident in India and South-East Asia, where state governments want regional airports to meet the same safety baseline as international gateways to secure airline interest.

By Application: Surveillance Foundation Enables Advanced Capabilities

Surveillance accounted for a 36.85% share of the airport surface movement guidance and control systems market in 2024 because reliable positional data is the root input for every higher-order function in the stack. Airlines, air navigation service providers, and ground handlers all ingest the same track data, which transforms the surveillance layer into a single source of truth that streamlines coordination across departments.

Guidance applications, however, are projected to grow at 7.65% CAGR, mirroring the industry’s pivot from reactive to proactive surface-movement management. Dynamic taxi-lighting, automated crossing clearances, and congestion-aware routing engines shrink block times and cut fuel burn, delivering ESG dividends that bolster airports’ access to green bond financing. Software vendors increasingly license guidance modules on a per-movement fee rather than a fixed licence, aligning vendor incentives with customer efficiency goals and smoothing cash-flow profiles for smaller gateways.

Geography Analysis

Europe controlled 31.74% of the airport surface movement guidance and control systems market in 2024 because a single policy umbrella—Single European Sky—accelerates equipment standardisation and enables consortia such as COOPANS to pool procurement, training, and cyber-defence resources. Multi-country ANSP collaborations mean suppliers benefit from larger contract scopes that cover numerous locations, allowing more robust maintenance footprints and sparking R&D around AI-native decision-support modules. The European Union’s cohesive climate-policy framework further stimulates uptake by making emissions-saving ground-handling tech eligible for green-infrastructure funds, effectively lowering the cost of capital for airports.

North America ranks second by value, underpinned by the FAA’s Surface Awareness Initiative that places multilateration receivers on over 450 fields and enforces low-visibility guidance rules. Airlines operating under the hub-and-spoke system champion these capabilities because even minor taxi-out delays at large connecting airports cascade across their networks. Parallel bills such as the 2025 National Aviation Preparedness Act earmark cybersecurity grants that specifically name air-side surveillance as a recipient, signalling continued federal financial support.

Asia-Pacific is the out-and-out growth leader, forecast at 7.14% CAGR through 2030. China’s five-year transport plan greenlights more than a dozen new civil airports, each wired from day one for Level 3 or higher functions because national airspace reforms emphasise data-driven operations. India’s privatisation of regional airports pairs PPP capital with Directorate General of Civil Aviation safety targets, leading operators like GMR and Adani to fast-track sensor procurement to secure traffic growth credits. Elsewhere, Indonesia, Vietnam, and the Philippines combine sovereign-wealth-fund money and JICA loans to modernise primary gateways, opening procurement doors for mid-tier A-SMGCS vendors looking to diversify beyond mature Western markets. The Middle East and Africa trail in absolute spend, yet the Dubai-Doha-Riyadh triad and fast-rising Ethiopian Aviation Group maintain world-class master-planning ambitions, sustaining a long-tail project pipeline that suppliers cannot ignore.

Competitive Landscape

Thales, Saab, and Honeywell anchor the upper tier of a market with moderate concentration because high regulatory hurdles and multi-year safety records act as natural entry barriers. Thales’ TopSky upgrades under the COOPANS alliance bring uniform functionality across six ANSPs. This proves that a single-code-base model reduces lifecycle costs while keeping pace with evolving SESAR-driven requirements. Saab’s ASDE-X pedigree at 35 US airports extends to Terminal Flight Data Management technology in nearly 90 towers, cementing a reputation for reliability that resonates with risk-averse procurement boards.[3]Source: Saab, “FAA Surface Safety Solutions,” saab.com

Mid-tier contenders such as Indra and Frequentis carve niches through modular digital-tower and virtual-ramp solutions that integrate neatly with legacy radar backbones. Indra’s July 2024 framework agreement with the FAA puts AeroBOSS on the Qualified Product List for more than 450 airports, unlocking a Pathfinder-style route to the US market. Frequentis, meanwhile, increases its share by offering camera-based remote-tower kits that smaller European and Canadian aerodromes can deploy within 18 months.

A third group of digital-native firms focuses exclusively on AI optimisation. Assaia’s turnaround platform layers computer-vision analytics on top of surveillance tracks to free one gate turn per day across pilot sites, an outcome that airlines monetise instantly. These specialists often partner with primes, providing the algorithmic secret sauce while leaving certification, hardware, and maintenance to incumbents. As a result, the competitive frontier increasingly centres on service-delivery models and data-exchange ecosystems rather than hardware specs alone.

Advanced Surface Movement Guidance And Control Systems Industry Leaders

Thales Group

Saab AB

Honeywell International Inc.

Indra Sistemas, S.A.

ADB SAFEGATE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: CISCEA, part of DECEA, awarded Thales a contract to modernize nine Primary and Secondary Surveillance Radars in Brazil. Installing a co-mounted Primary TRAC NG and Secondary RSM NG radar at Presidente Prudente airport marks Thales' 133rd ATC radar deployment, securing over 80% of Brazil's airspace.

- February 2024: Terma, a Danish radar solutions leader, secured a significant order for its SCANTER 5502 Surface Movement Radars (SMR) from Indra Sistemas. These radars will be installed at Bengaluru, Mumbai, Navi Mumbai, and Hyderabad airports, enhancing operational capabilities and safety. Terma continues to support India's growing aviation sector with cutting-edge technology.

Global Advanced Surface Movement Guidance And Control Systems Market Report Scope

| Hardware |

| Software |

| Services |

| Level 1 |

| Level 2 |

| Level 3 |

| Level 4 |

| Large Airports |

| Medium Airports |

| Small Airports |

| Military Airbases |

| Surveillance |

| Monitoring and Alerting |

| Guidance |

| Planning and Routing |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Offering | Hardware | ||

| Software | |||

| Services | |||

| By Implementation Level | Level 1 | ||

| Level 2 | |||

| Level 3 | |||

| Level 4 | |||

| By Airport Size | Large Airports | ||

| Medium Airports | |||

| Small Airports | |||

| Military Airbases | |||

| By Application | Surveillance | ||

| Monitoring and Alerting | |||

| Guidance | |||

| Planning and Routing | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the Airport Surface Movement Guidance and Control Systems market in 2025?

The market stands at USD 5.55 billion in 2025 and is forecasted to reach USD 7.38 billion by 2030, reflecting a 5.87% CAGR.

Which offering segment grows the fastest?

Services expand at 7.34% CAGR because airports increasingly favor turnkey integration and performance-based contracts.

What implementation level dominates current deployments?

Level 2 solutions hold 45.70% share as they balance enhanced surveillance with manageable cost and operational change.

Which airport size shows the highest growth rate?

Small airports record a 6.98% CAGR through 2030 as modular cloud-native solutions lower entry barriers.

Why is Asia-Pacific the fastest-growing region?

The region’s 7.14% CAGR stems from extensive greenfield airport construction in China, India and Southeast Asia coupled with government funding support.

Who are the leading A-SMGCS suppliers?

Thales, Saab and Honeywell top the list, with Indra and ADB SAFEGATE strengthening mid-tier positions through digital-tower and AI partnerships.

Page last updated on: