Pneumatic Tools Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

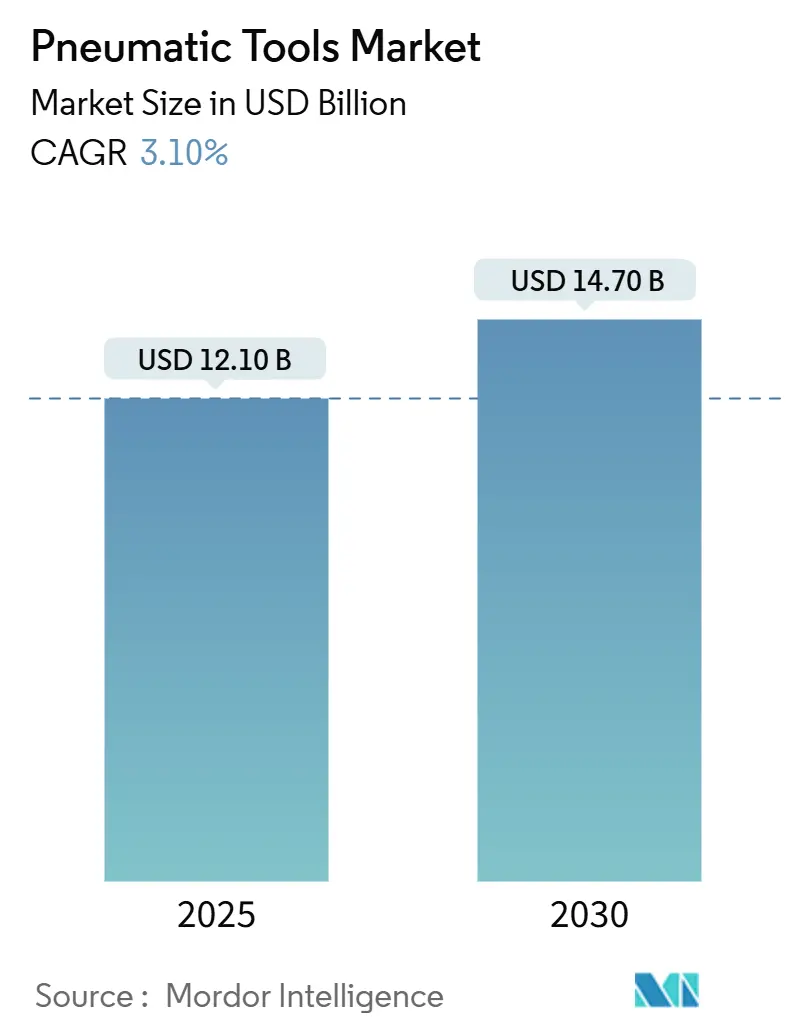

| Market Size (2025) | USD 12.10 Billion |

| Market Size (2030) | USD 14.70 Billion |

| Growth Rate (2025 - 2030) | 3.10% CAGR |

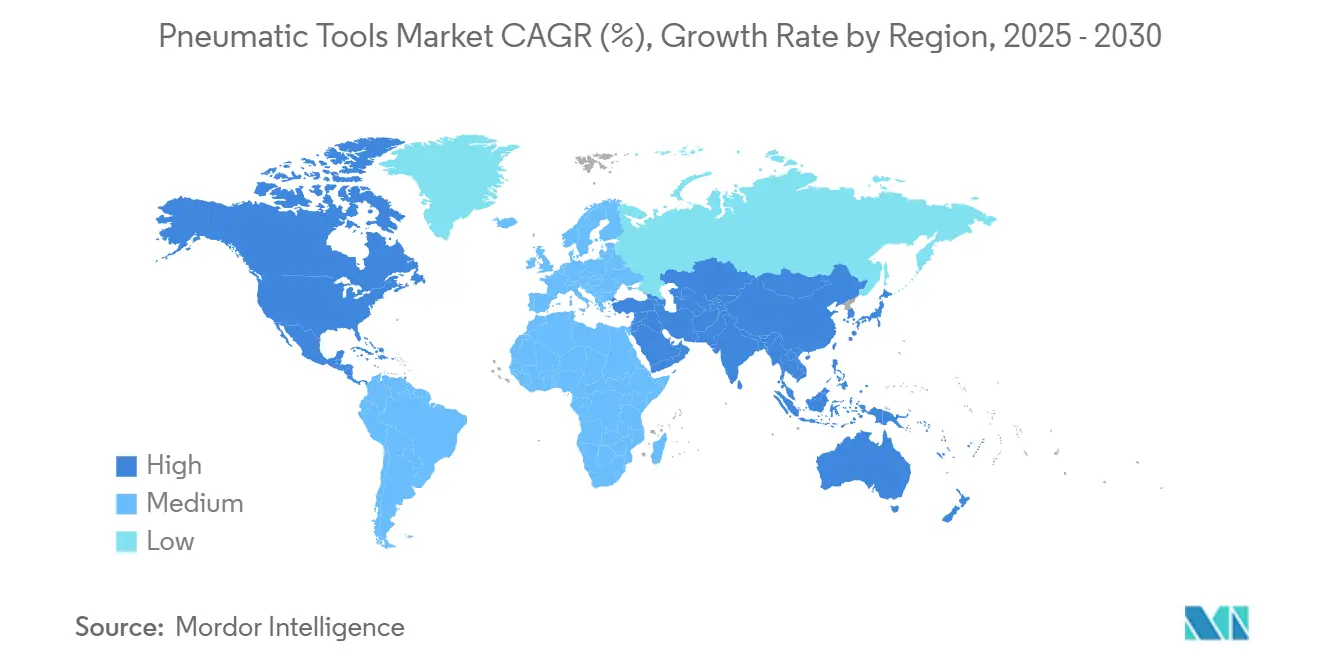

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pneumatic Tools Market Analysis by Mordor Intelligence

The pneumatic tools market size stands at USD 12.1 billion in 2025 and is forecast to reach USD 14.7 billion by 2030, advancing at a 3.1% CAGR. Steady growth reflects the sector’s maturity as well as its continued indispensability in environments that require high torque, spark-free operation, and round-the-clock duty cycles. Demand is reinforced by factory digitalization, where precision air-powered fastening shortens quality-control loops; by public-sector infrastructure spending that lifts tool orders for concrete breaking, steel fixing, and pipe work; and by brisk automotive repair activity that favors impact wrenches and ratchets. Energy-efficiency regulation and vibration-exposure limits nudge manufacturers toward quieter, lighter, and low-loss designs, creating differentiation for suppliers that can marry performance with compliance. Competitive intensity remains moderate because scale advantages in compressor technology and global service networks still deter new entrants, yet mid-tier local brands thrive in specialized niches through price agility and application know-how.

Key Report Takeaways

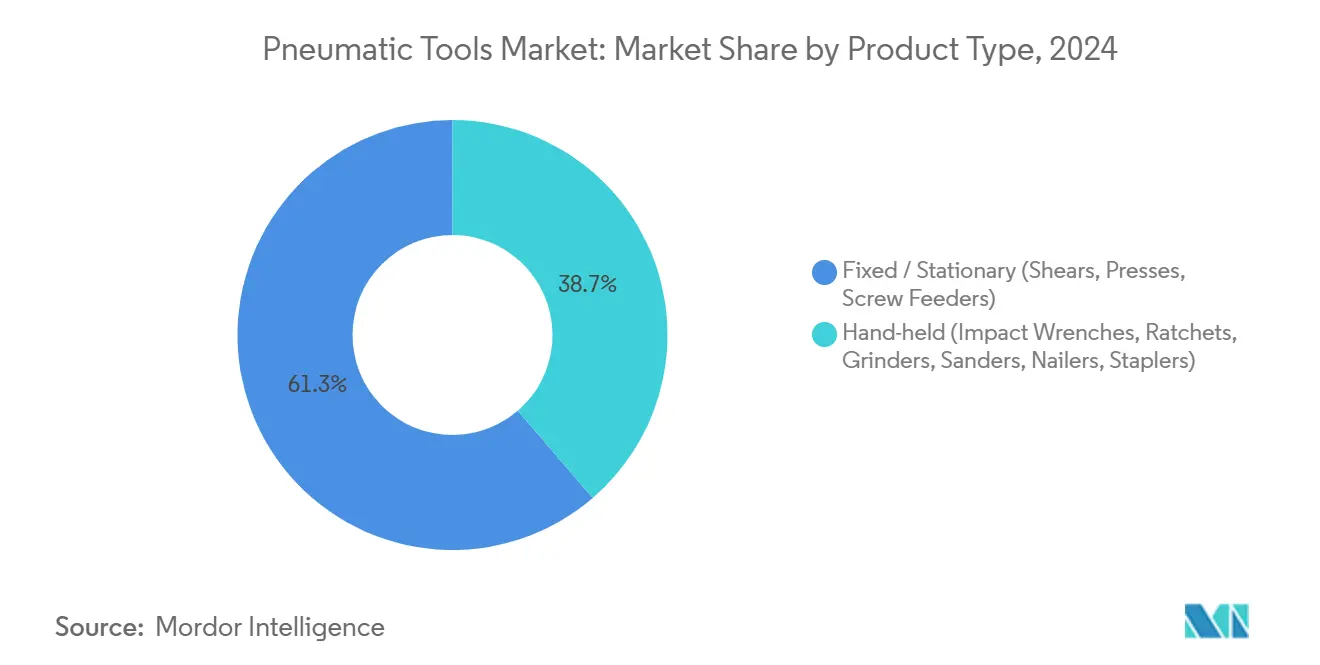

- By product type, hand-held impact wrenches led with 38.7% of pneumatic tools market share in 2024, while fixed and stationary tools are projected to post the fastest 5.0% CAGR through 2030.

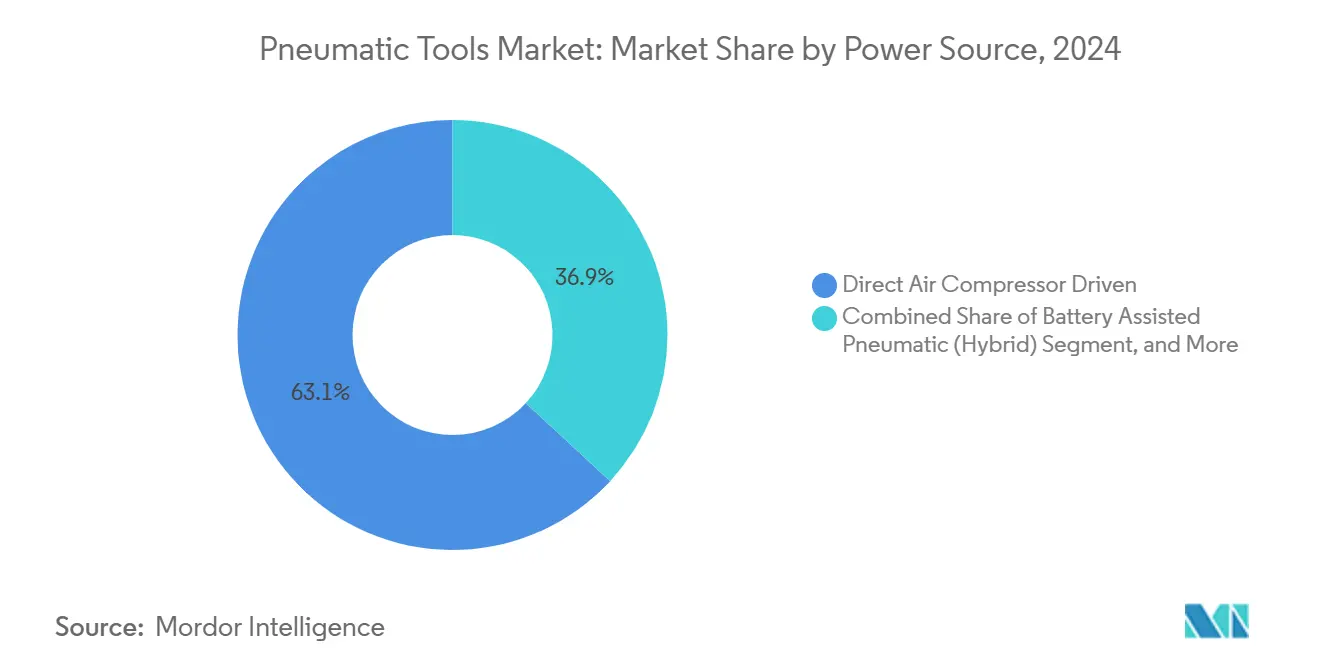

- By power source, direct air-compressor systems accounted for 63.1% of the pneumatic tools market size in 2024, whereas battery-assisted hybrids are on track for a 4.76% CAGR to 2030.

- By end-user industry, automotive and transportation held 28.9% revenue share in 2024, and aerospace and defense are forecast to expand at a 3.9% CAGR through 2030.

- By geography, Asia-Pacific commanded 33.7% revenue share in 2024, and North America is expected to grow at the fastest 4.8% CAGR through 2030.

Global Pneumatic Tools Market Trends and Insights

Driver Imapct Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in industrial automation and tightening quality-control cycles | +0.8% | Global; strongest in Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in global construction and infrastructure CAPEX | +0.7% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Expanding automotive after-sales and repair volumes | +0.5% | Global; mature vehicle parks | Medium term (2-4 years) |

| Occupational-health-driven shift to low-vibration ergonomic tools | +0.4% | Europe, North America, developed Asia-Pacific | Long term (≥ 4 years) |

| Hybrid battery-assisted pneumatic systems unlock cordless mobility | +0.3% | North America, Europe early adopters | Long term (≥ 4 years) |

| Compressed-air decarbonisation mandates (oil-free, energy-efficient compressors) | +0.2% | Europe, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Industrial Automation and Tighter Quality-Control Cycles

Production lines integrate vision systems, torque traceability, and IoT-ready valves to cut defect rates in real time, and air motors remain a preferred power medium because they do not overheat and can be stalled without damage[1]Source: Beth Stackpole, “Why Pneumatics Remain an Automation Mainstay,” Automation World, automationworld.com. Automotive assembly plants have trimmed joint-integrity audit windows from days to hours by pairing sensor-equipped pneumatic nutrunners with MES software.[2]Source: Sara Jensen, “A Positive Outlook for Pneumatics Market in 2025,” Power & Motion, powermotiontech.comPackaging factories deploy compact air cylinders and air-logic grippers that index hundreds of packs per minute without thermal drift. These automation gains underpin recurrent consumables demand—regulators, filters, seals—and lock in tool platform loyalty. As a result, the pneumatic tools market continues to benefit even as robotics spreads because robot end-effectors often incorporate air-powered screwdrivers and drills.

Growth in Global Construction and Infrastructure CAPEX

United States construction starts are slated to hit USD 1.277 trillion in 2025, buoyed by allocations from the USD 1.2 trillion Infrastructure Investment and Jobs Act. Large-diameter pipelines, bridge retrofits, and airport runways all rely on chipping hammers, pavement breakers, and nut-runners that deliver continuous torque without battery swaps. Midwest urban growth of 4% in 2020-25 raises demand for rebar cutting and concrete fastening tools on multistory housing sites.[3]Source: Iowa-Nebraska Equipment Dealers Association, “2025 Construction Equipment Sales Outlook in the Midwest,” issuu.com Contractors grappling with skilled-labor shortages substitute heavier-duty air nailers and framing tools that boost per-worker output. Consequently, the pneumatic tools market finds fresh volumes even where civil engineering mechanization had been stagnant.

Expanding Automotive After-Sales and Repair Volumes

Auto Care Association projects the global aftermarket to reach USD 617.3 billion by 2027, up from 2024 levels.[4]Source: Auto Care Association, “Industry Expected to Reach USD 617.3 Billion in 2027,” autocare.org Elevated vehicle age lifts service intake, and tire, brake, and suspension work favors air impact wrenches that can cycle thousands of times per shift without overheating. Fleet operators keep in-house service bays equipped with high-flow composite-body tools to minimize downtime for last-mile vans. Electric-vehicle adoption only partially dilutes tool demand because wheel, chassis, and structural repairs still need fast, high-torque removal. As parts complexity rises, repairers gravitate to torque-controlled pulse tools that cut rework rates, supporting premium pricing within the pneumatic tools market.

Occupational-Health Push for Low-Vibration Ergonomic Tools

EU Directive 2002/44/EC caps daily hand-arm vibration exposure at 5 m/s², prompting a redesign wave in hammers, grinders, and riveters. U.S. OSHA 29 CFR 1910.242 likewise compels employers to maintain tools in safe operating condition. Vendors respond with twin-hosed vibration-dampening handles, air-cushion clutches, and composite housings that trim vibration up to 8-fold. Health-based purchasing criteria diversify away from lowest-price bids, boosting value-added sales in the pneumatic tools industry. Insurers are starting to factor HAVS claims into premiums, further accelerating ergonomic upgrades.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising adoption of brushless-electric and cordless power tools | -0.6% | North America and Europe | Medium term (2-4 years) |

| Compressed-air energy losses driving OPEX scrutiny | -0.4% | Europe, North America | Long term (≥ 4 years) |

| Stringent worker-exposure limits on noise and vibration | -0.3% | Europe, North America, and developed APAC markets | Medium term (2-4 years) |

| Global helium scarcity is raising the cost of leak-testing in tool manufacture | -0.2% | Global, concentrated in manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Brushless Electric and Cordless Power Tools

Lithium-ion packs now drive hammer drills and rotary hammers that rival 1,200 ft-lb pneumatic impacts, undercutting hose-driven models in portability. DEWALT’s POWERSHIFT lineup claims 60% lower carbon emissions than gas or air equivalents while matching runtime for structural concrete vibration jobs. Milwaukee Tool posted 11.6% 2024 sales growth on cordless demand, reflecting contractor preference for plug-free worksites. Nevertheless, continuous-duty settings such as engine assembly lines still value shop-air reliability, limiting the substitution risk to intermittent applications. The net effect trims top-line acceleration but does not derail the pneumatic tools market trajectory.

Compressed-Air Energy Losses Heighten OPEX Scrutiny

Industrial audits reveal 20-30% leak loss across aging distribution headers. With compressed air consuming up to 40% of plant electricity in assembly operations, efficiency projects compete head-to-head with tool upgrades for capital budgets. Owners weigh the dual cost of compressor compliance and tool replacement, occasionally favoring electric drives in renovation cycles. Vendors that can demonstrate 15 scfm-class tools delivering equivalent torque at 12 scfm will mitigate this restraint, preserving share in the pneumatic tools market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fixed Systems Benefit from Automation

Manufacturers’ move toward lights-out production elevated fixed and stationary installations, resulting in a 5.0% CAGR outlook through 2030. Hand-held impact wrenches still command 38.7% of the pneumatic tools market share as of 2024 on the strength of their versatility in service bays and structural steel erection. Automated screw feeders and presses integrate with line PLCs, enabling part-traceability down to individual fasteners, which in turn solidifies the fixed-tool growth story. Across both classes, vibration-dampened housings, quick-change anvils, and smart torque sensors form the next competitive frontier. Makers that package remote diagnostics and predictive-maintenance dashboards are likely to widen margins in the pneumatic tools market.

Fixed-system expansion dovetails with demand for synchronized multi-spindle units in appliance, HVAC, and battery-pack assembly lines. Meanwhile, aerospace parts factories adopt slim-body pneumatic drills that accommodate composite lay-ups without delamination. The pneumatic tools market size attributed to fixed stations will therefore outpace portable categories even as cordless penetration rises elsewhere. In contrast, sanders, nailers, and staplers fight stiffer competition from brushless electrics in lighter-duty trades, prompting pneumatic suppliers to emphasize lower lifetime operating costs and rugged duty cycling.

By Power Source: Hybrids Carve a Niche

Direct compressors supply underpinned 63.1% of 2024 revenue and remain the backbone of large-volume plants thanks to 24/7 uptime. The pneumatic tools market size attributable to hybrid battery-assisted units, however, is projected to expand at a 4.76% CAGR through 2030 on the back of hose-free productivity in confined or elevated work zones. Hybrid designs use compact air tanks re-pressurized by onboard micro-compressors, smoothing peak-torque delivery while shrinking hose reliance. Nitrogen and CO₂ cartridges address contamination-sensitive food and pharma sectors, albeit at lower volumes.

Field service organizations appreciate that hybrids circumvent the noise of large mobile compressors while still outputting 700-900 Nm torque. Municipal utility crews and wind-turbine technicians form early adopter clusters. These features help defend the pneumatic tools market against fully electric encroachment while stimulating premium ASPs.

By End-User Industry: Aerospace Accelerates

Automotive and transportation accounted for 28.9% of 2024 revenue, propelled by a high repair cadence and ongoing vehicle production. Yet aerospace and defense will register the fastest 3.9% CAGR, aligned with global military budgets of USD 2.44 trillion and commercial fleet restoration schedules. Tight-tolerance airframe assembly requires torque-traceable pulse tools and angle-sensing riveting systems, giving pneumatic technology an edge over electrics on weight-to-power ratio. General manufacturing sustains mid-single-digit growth by embedding pneumatic nutrunners in robotic cells.

Oil and gas sites increasingly digitize maintenance, capturing 80% cost savings by deploying sensorized air tools tied to AI scheduling modules. Construction remains cyclical but stable, its order book underwritten by public infrastructure grants. Niche adopters in life sciences reward stainless-steel, oil-free designs that satisfy GMP auditing, adding resilience to the pneumatic tools industry.

Geography Analysis

Asia-Pacific retained a 33.7% share in 2024, fueled by China’s machinery exports, India’s auto-parts hub scale-up, and Southeast Asia’s electronics clustering. Provincial subsidies for smart-factory upgrades incentivize compressed-air optimization projects that bundle tool renewals. Atlas Copco sources 40% of its global revenue from the region and continues building local service depots to lock in installed-base loyalty.[5]Source: Atlas Copco Group, “A Global Footprint,” atlascopcogroup.com Domestic challengers in China offer entry-level ranges at 15-20% lower prices, but multinationals defend turf with warranty, precision, and safety credentials, sustaining the premium tier of the pneumatic tools market.

North America is projected to grow at a 4.8% CAGR through 2030 as public-works outlays crest and advanced manufacturing reshoring gathers momentum. U.S. pipe-valve-fitting demand estimated at USD 42.5 billion in 2025 will translate into elevated consumption of flange spreaders, torque multipliers, and cutting tools. OSHA vibration and DOE compressor rules raise switching costs for non-compliant imports, indirectly shielding established brands.

Europe’s mature installed base still drives captive replacement, but stringent vibration and energy directives foster replacement cycles toward ergonomic, low-leak models. France’s EUR 57.4 billion aerospace output of 2024, 82% exported, keeps regional demand for high-precision pneumatic drills elevated. Meanwhile, the Middle East and Africa, as well as South America, represent frontier territories where political risk tempers growth, but state-owned oil and mining projects provide periodic spikes in heavy-duty tool orders.

Competitive Landscape

Industry concentration is moderate. Atlas Copco reinforced its leadership by purchasing Korea-based Kyungwon Machinery for USD 465 million in March 2025, enriching its screw-compressor line and adding Asian capacity. Ingersoll Rand rolled up APSCO, Blutek, UT Pumps, and Friulair for a combined USD 281 million across 2024-25, layering filtration, nitrogen-generation, and hydraulic solutions onto its air-tools mix. Techtronic Industries, parent of Milwaukee Tool, posted USD 14.6 billion revenue in 2024, fueled by cordless innovation that cross-pressures pneumatic incumbents.

Product differentiation now hinges on embedded diagnostics, vibration mitigation, and air-use efficiency rather than brute torque alone. IoT gateways on premium nutrunners stream cycle-count and leak-rate data to ERP dashboards, allowing predictive replacement. Mid-tier Asian entrants focus on price, but procurement managers in regulated sectors still favor brands offering certified vibration values and CE/UL compliance. White-space opportunities lie in hybrid power modules, oil-free silent compressors, and service subscriptions that bundle leak audits with tool refurbishment. Market participants able to span compressor, distribution, and tool know-how will continue to shape the pneumatic tools market trajectory.

Pneumatic Tools Industry Leaders

Atlas Copco AB

Ingersoll Rand Inc.

Stanley Black & Decker Inc.

Snap-on Incorporated

Makita Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Atlas Copco bought Kyungwon Machinery Industry for USD 465 million, boosting its oil-injected and oil-free screw-compressor portfolio.

- February 2025: Ingersoll Rand reported USD 7.106 billion in 2024 orders and a 30.3% EBITDA margin in its Industrial Technologies and Services segment, underscoring pricing discipline in air systems.

- January 2025: New DOE efficiency rules for oil-flooded rotary compressors took effect, setting minimum isentropic targets for 35-1,250 cfm models.

- November 2024: DEWALT launched its POWERSHIFT cordless equipment system, claiming a 60% CO₂ cut versus gas or air counterparts.

- October 2024: Ingersoll Rand completed three bolt-on deals worth USD 135 million, adding specialty truck hydraulics and compressed-air generators.

Global Pneumatic Tools Market Report Scope

| Hand-held (Impact Wrenches, Ratchets, Grinders, Sanders, Nailers, Staplers) |

| Fixed / Stationary (Shears, Presses, Screw Feeders) |

| Direct Air-Compressor Driven |

| Battery-Assisted Pneumatic (Hybrid) |

| Other Gas-Driven (e.g., Nitrogen, CO₂) |

| Automotive and Transportation |

| General Manufacturing |

| Construction and Infrastructure |

| Oil and Gas / Petrochemicals |

| Aerospace and Defence |

| Other End-user Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Hand-held (Impact Wrenches, Ratchets, Grinders, Sanders, Nailers, Staplers) | ||

| Fixed / Stationary (Shears, Presses, Screw Feeders) | |||

| By Power Source | Direct Air-Compressor Driven | ||

| Battery-Assisted Pneumatic (Hybrid) | |||

| Other Gas-Driven (e.g., Nitrogen, CO₂) | |||

| By End-user Industry | Automotive and Transportation | ||

| General Manufacturing | |||

| Construction and Infrastructure | |||

| Oil and Gas / Petrochemicals | |||

| Aerospace and Defence | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the pneumatic tools market today?

The pneumatic tools market size is USD 12.1 billion in 2025 and is projected to reach USD 14.7 billion by 2030.

Which segment is growing fastest within pneumatic tools?

Fixed and stationary systems are expected to post the highest 5.0% CAGR through 2030 on the back of factory automation investments.

What region offers the highest growth outlook?

North America shows the strongest 4.8% CAGR forecast to 2030, supported by infrastructure spending and the reshoring of advanced manufacturing.

Why are pneumatic tools still preferred over cordless alternatives?

Air tools deliver continuous high torque, operate safely in spark-sensitive zones, and avoid battery downtime, keeping them vital in heavy-duty and hazardous settings.

Page last updated on: