Sensors And Actuators Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

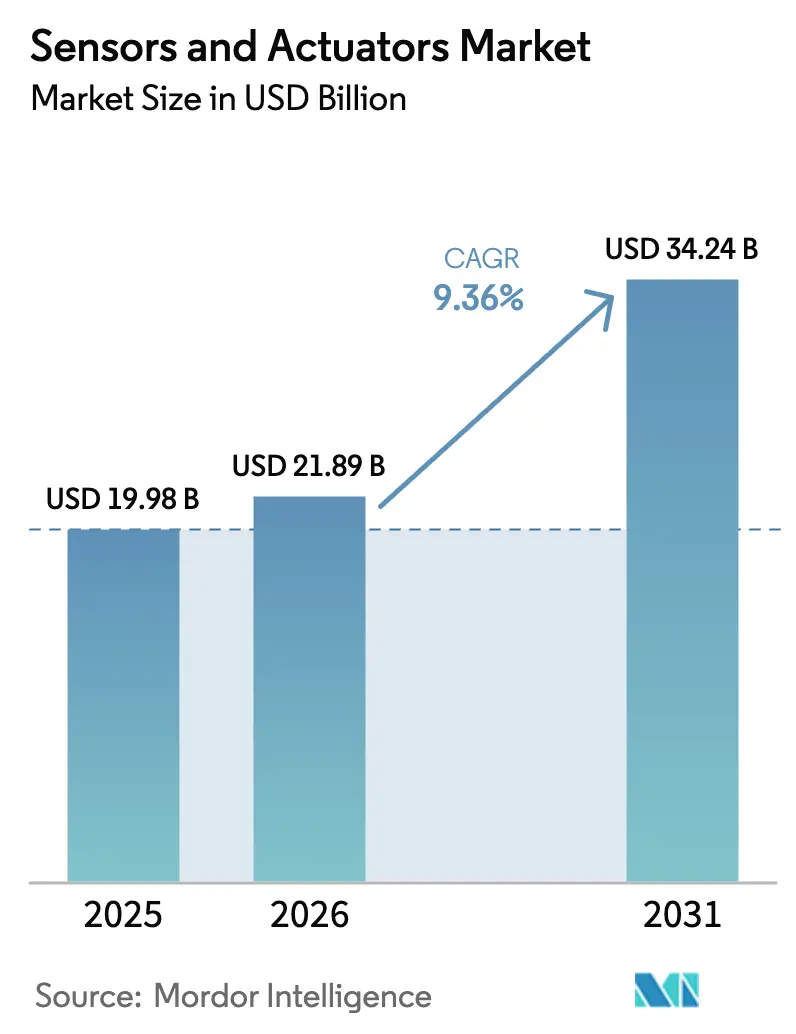

| Market Size (2026) | USD 21.89 Billion |

| Market Size (2031) | USD 34.24 Billion |

| Growth Rate (2025 - 2030) | 9.36% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sensors And Actuators Market Analysis by Mordor Intelligence

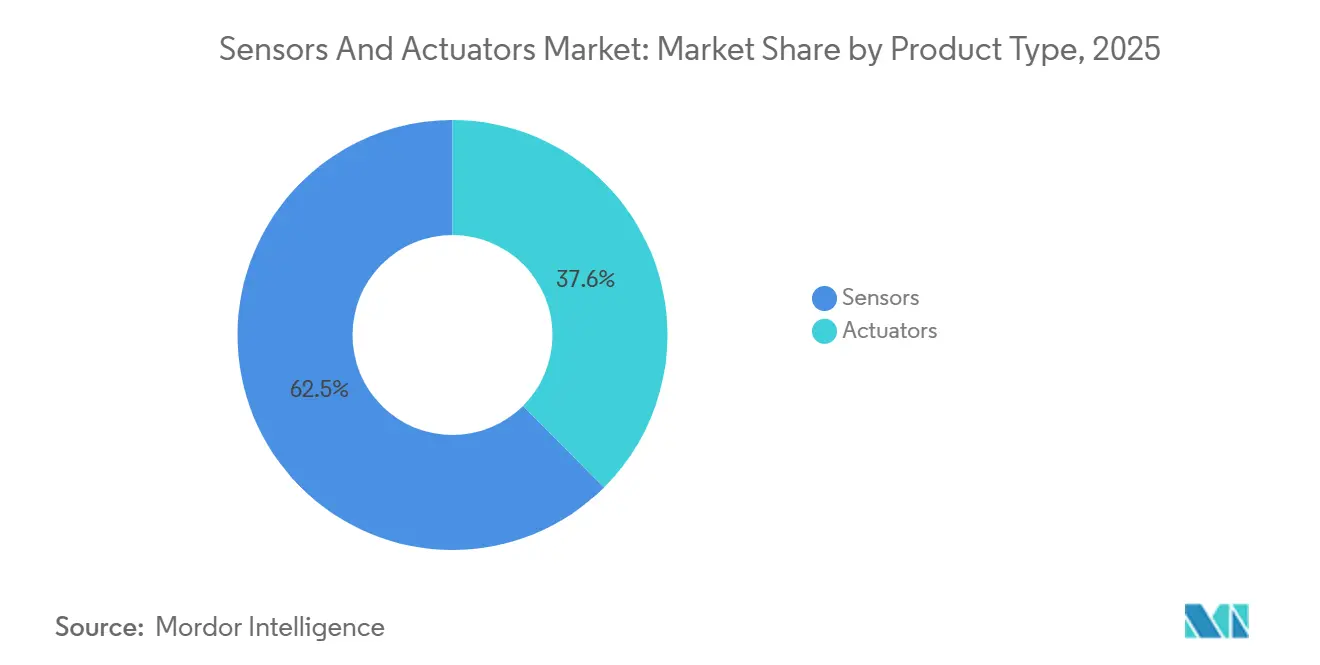

The sensors and actuators market size is projected to be USD 19.98 billion in 2025, USD 21.89 billion in 2026, and reach USD 34.24 billion by 2031, growing at a CAGR of 9.36% from 2026 to 2031. Demand is shifting toward edge-intelligent devices that both sense and perform real-time actuation at the network’s edge. Sensors held 62.45% revenue share in 2025 while chemical and bio-sensors are advancing the fastest thanks to wearable medical devices and point-of-care diagnostics. MEMS designs are eroding the cost-structure of conventional architecture, and low-power wireless links are broadening retrofit possibilities across factories, vehicles, and buildings. Healthcare providers, automotive OEMs, and discrete manufacturers are the most aggressive adopters, accelerating volume shipments of multi-axis inertial, pressure, and optical devices.

Key Report Takeaways

- By product type, sensors commanded 62.45% of the sensors and actuators market share in 2025, while chemical/bio-sensors are growing at a 10.40% CAGR in 2031.

- By end-user, Automotive and Mobility commanded 24.66% of the sensors and actuators market share in 2025, while healthcare recorded the steepest expansion at a 14.10% CAGR through 2031.

- By technology, MEMS architectures captured a 68.43% share of the sensors and actuators market size in 2025 and are growing at a 9.43% CAGR between 2026 and 2031.

- By connectivity, wireless networks captured a 54.29% share of the sensors and actuators market and advanced at an 11.10% CAGR between 2026 and 2031.

- By geography, Asia-Pacific led with 37.38% revenue share in 2025 and is growing at a 12.88% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sensors And Actuators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Low-Power MEMS Sensors Unlocking New IoT Use-Cases | 1.8% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Rapid Electrification and ADAS Integration in European Automotive Manufacturing | 1.5% | Europe, with early gains in Germany, France, Italy | Short term (≤ 2 years) |

| High Adoption of Predictive-Maintenance Platforms Amplifying Smart Actuator Demand | 1.3% | North America & EU | Medium term (2-4 years) |

| Hydrogen and CCUS Megaproject Investments Spurring Specialty Sensor Demand | 0.9% | Middle East, with early gains in Saudi Arabia, UAE | Long term (≥ 4 years) |

| Accelerated 5G and Edge-AI Roll-outs Elevating Industrial Sensor Uptake | 1.6% | APAC core (South Korea, Taiwan, China), spill-over to North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Proliferation Of Low-Power MEMS Sensors Unlocking New IoT Use-Cases

Battery-sipping MEMS accelerometers, gyroscopes, and environmental sensors now operate for up to a decade on primary cells, enabling smart-city air-quality grids, agricultural soil-moisture probes, and cold-chain asset trackers. China shipped more than 800 million sub-10-microampere sensors in 2025, driven by municipal deployments, while Indian cities installed over 200,000 wireless leak-detection nodes the same year.[1]Government of India, “Smart Cities Mission 2025 Deployment Report,” smartcities.gov.in New MEMS packages integrate vibration or thermal energy harvesters, lowering total cost of ownership by roughly one-third across a ten-year life cycle. These economics are shortening payback periods for public-sector and industrial buyers, sustaining double-digit unit growth.

Rapid Electrification And ADAS Integration In European Automotive Manufacturing

European vehicle platforms now contain 35–50 sensing nodes per car as OEMs migrate to Level 2-plus driver assistance and battery-electric powertrains. More than two-thirds of cars registered in Germany in 2025 featured adaptive cruise control and lane-keeping support, each requiring radar, ultrasonic, and optical image sensors.[2]Kraftfahrt-Bundesamt, “Vehicle Registration Data 2025,” kba.de Component suppliers have inked multi-year contracts exceeding EUR 2 billion (USD 2.2 billion) for 77 GHz radar modules and high-dynamic-range CMOS imagers. Battery packs add dozens of current, voltage, and temperature sensors for thermal-runaway prevention, extending the sensor content and reinforcing demand for automotive-grade MEMS foundry capacity.

High Adoption Of Predictive-Maintenance Platforms Amplifying Smart Actuator Demand

North American refiners, chemical producers, and discrete manufacturers connected more than 1.2 million sensor-actuator endpoints to digital plant platforms in 2025. Machine-learning models running at the device edge now flag bearing or seal degradation weeks in advance, trimming unplanned outages by up to one-fifth. Smart electric and pneumatic actuators embed microcontrollers, vibration sensors, and wireless transceivers, commanding a 20%–30% premium that users justify against downtime costs exceeding USD 50,000 per hour in continuous-process industries. As inference chips are added to actuator control boards, on-device anomaly detection is set to become standard.

Hydrogen And CCUS Megaproject Investments Spurring Specialty Sensor Demand

Gigawatt-scale hydrogen and carbon-capture plants under construction in Saudi Arabia and the UAE require sensors that survive temperatures above 400 °C, pressures to 100 bar, and corrosive gas streams. Fiber-optic distributed acoustic systems monitor several hundred kilometers of hydrogen piping in real time, while tunable-diode-laser analyzers verify CO₂ purity at ±0.5% for sequestration. Cumulative regional spend on specialty instrumentation is expected to top USD 800 million by 2030, though protracted qualification and safety-certification cycles temper near-term volume.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rare-Earth Magnet Price Volatility Inflating Precision Actuator BOM Costs | -0.7% | Global, with acute impact in North America & EU | Short term (≤ 2 years) |

| EU Data-Security Legislation Slowing Wireless Sensor-Network Adoption | -0.5% | Europe, with spill-over to UK | Medium term (2-4 years) |

| High Calibration Complexity of Multi-Axis Sensors Hindering SME Uptake | -0.4% | Global, with acute impact in APAC SME clusters | Medium term (2-4 years) |

| Semiconductor Wafer Shortages Curtailing MEMS Sensor Supply in Japan | -0.6% | Global, with acute impact in APAC automotive supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rare-Earth Magnet Price Volatility Inflating Precision Actuator BOM Costs

Neodymium-iron-boron magnet prices climbed more than one-third between mid-2024 and early 2025 after export-quota cuts and mining disruptions.[3]Financial Times, “Rare-Earth Magnet Price Surge,” ft.com Magnetic actuator suppliers faced 12%–18% bill-of-materials inflation and saw gross margins compress by roughly 250 basis points. Alternate ferrite magnets reduce torque density, while switched-reluctance designs introduce complex control algorithms, limiting substitution. Smaller vendors without scale procurement contracts feel the squeeze most acutely as they cede share to vertically integrated multinationals.

EU Data-Security Legislation Slowing Wireless Sensor-Network Adoption

Since October 2024, the European Union's NIS2 directive has mandated that certified gateways, secure boot mechanisms, and encrypted firmware updates be implemented for wireless nodes in critical infrastructure. This directive aims to enhance the security and resilience of critical systems against cyber threats. However, compliance with these requirements comes at an added cost of USD 15–25 per sensor, which can significantly impact project budgets. Additionally, rollout schedules may face delays of over a month due to the time required for certification and implementation processes. As a result, utilities and building-automation integrators are halting wireless upgrades, opting instead for wired fieldbus architectures that are perceived as more reliable and easier to certify under the new regulations. This shift is hindering the adoption and penetration of flexible, battery-powered sensors, which are otherwise valued for their versatility and ease of deployment. Furthermore, certification bottlenecks are anticipated to continue until 2027, as testing labs work to increase their capacity and vendors focus on completing necessary product redesigns to meet the directive's stringent requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Chemical And Bio-Sensors Lead Innovation Wave

Chemical and bio-sensors are forecast to grow at a 10.40% CAGR through 2031, the quickest pace among product classes. They underpin glucose, lactate, and cortisol wearables and deliver rapid infectious-disease diagnostics, driving heightened procurement from hospitals and consumer-health brands. Pressure sensors still dominate volume in automotive tire-pressure monitoring, HVAC controllers, and process instrumentation, while temperature devices serve battery-management and cold-chain use cases. Electric actuators are increasingly preferred over pneumatic units for precise motion profiles, though hydraulics remain standard in heavy construction and aerospace flight controls.

Image sensors, particularly CMOS devices, serve automotive ADAS and industrial vision, with shipments rising in line with Level 2-plus automation. Flow and torque sensors cater to specialized medical ventilators and electric-vehicle powertrains, commanding premium pricing. Together these dynamics reinforce the sensors and actuators market as a multi-speed landscape where innovation clusters around miniaturization, multi-modal integration, and lifecycle cost reduction.

By Technology: MEMS Architectures Capture Wireless Edge

MEMS devices accounted for 68.43% of the sensors and actuators market share in 2025. Batch silicon fabrication lowers unit cost to under USD 2 while enabling co-packaged ASIC logic. Total shipments from a leading European supplier surpassed 4 billion units in 2025, buoyed by smartphone, wearable, and automotive orders. Conventional macroscale sensors still serve harsh environments such as gas turbines and subsea wells where MEMS reliability tapers, yet that niche is narrowing as hermetic wafer-level packaging broadens MEMS temperature and vibration envelopes.

Wireless networks amplify the appeal of MEMS parts because coin-cell batteries can power them for years, whereas conventional sensors often require wired feeds. Foundries in Taiwan and Japan committed more than USD 500 million to expand 8-inch MEMS lines in 2025, targeting automotive safety and industrial vibration applications. As packaging innovation advances, MEMS penetration should deepen across process-automation, aerospace, and medical devices, further enlarging the sensors and actuators market size.

By Connectivity: Wireless Networks Unlock Retrofit Economics

Wireless connectivity represented 54.29% of 2025 revenue and is projected to rise at an 11.10% CAGR to 2031. Eliminating conduit and cable can cut installation cost by up to 60%, unlocking retrofits in brownfield plants and aging commercial real estate. Bluetooth LE, Zigbee, and LoRaWAN dominate smart-building and smart-city deployments, while WirelessHART and ISA100.11a offer deterministic latency for process industries.

Safety-critical domains such as brake-by-wire and flight controls still require deterministic wired links like CAN, EtherCAT, or PROFINET. Yet 5G private networks with ultra-reliable low-latency profiles now approach fieldbus response times, blurring boundaries and widening wireless avenues in discrete manufacturing. The result is an expanding installed base of battery-powered sensor nodes feeding cloud and edge platforms, reinforcing volume growth in the sensors and actuators market.

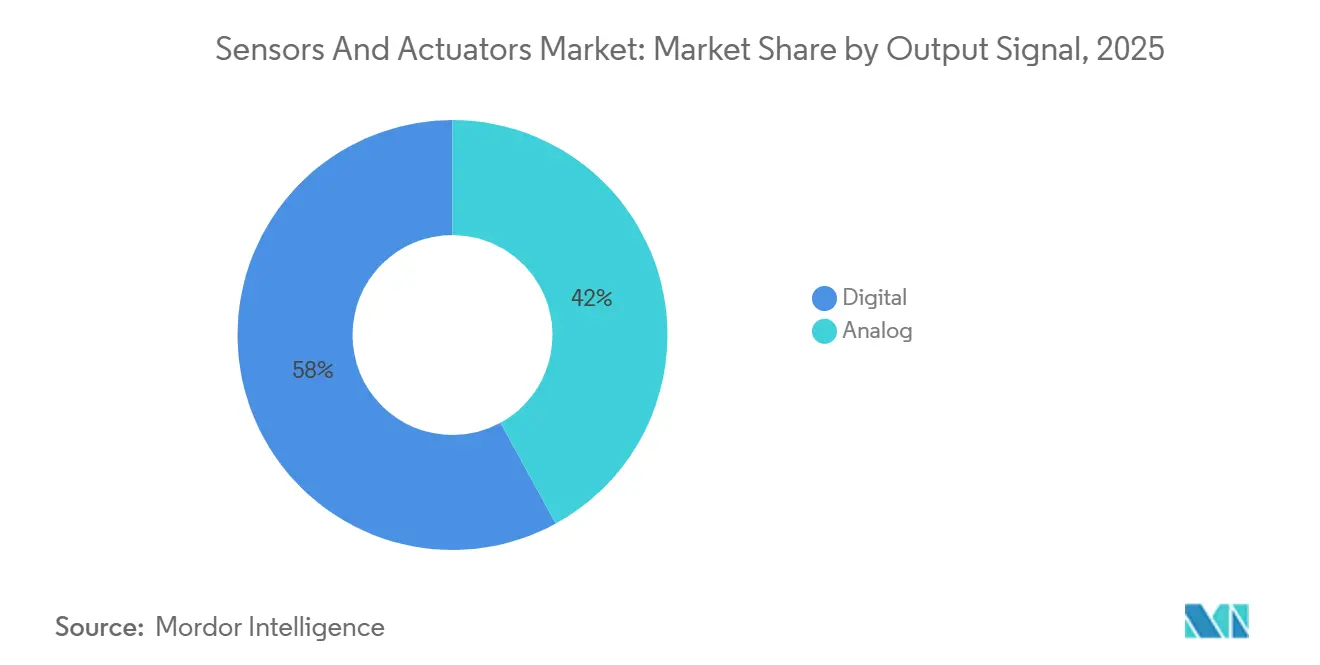

By Output Signal: Digital Interfaces Simplify System Integration

Digital-output devices captured 57.98% revenue in 2025 and are growing at 11.28% CAGR. Embedded ADCs shrink circuit-board area by up to half and enable multi-drop busses that slash wiring harness bulk in vehicles and machines. Automotive-grade digital pressure and temperature sensors with functional-safety certification are proliferating in electric-vehicle battery packs and brake systems.

Analog 4-20 mA loops endure in process plants where legacy PLCs expect current-loop inputs, but hybrid devices now offer concurrent analog and digital pins, smoothing migration without forklift upgrades. As new builds default to digital, and retrofit economics evolve, digital interfaces are expected to eclipse analog in most verticals before the end of the decade, further lifting the sensors and actuators market.

By End-User Industry: Healthcare Devices Outpace Traditional Verticals

Healthcare is forecast to post a 14.10% CAGR through 2031, spurred by continuous glucose monitors, smart inhalers, and point-of-care diagnostics. Automotive remains the largest buyer at 24.66% share in 2025 owing to ADAS and electrification. Industrial automation and robotics integrate vibration, vision, and force sensors for cobots and guided vehicles, while consumer electronics pulls billions of MEMS units into phones, watches, and earbuds each year.

Oil and gas operators demand ruggedized pressure and acoustic sensors for downhole drilling and leak detection, whereas aerospace entails radiation-tolerant designs with strict certification. Building automation uses occupancy and CO₂ sensors for energy savings, and utilities modernize grids with leak-detection arrays. Collectively, these end-users sustain diversified revenue streams that stabilize the sensors and actuators market across cycles.

Geography Analysis

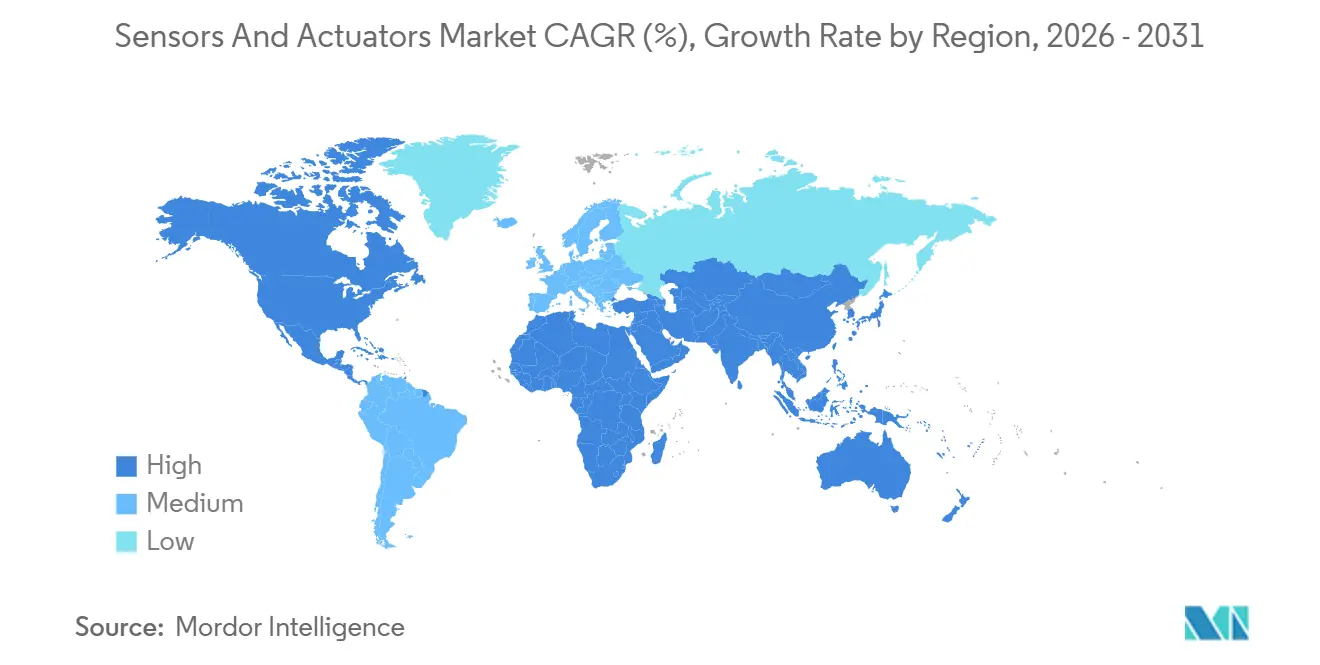

Asia-Pacific accounted for 37.38% of global revenue in 2025 and will grow at a 12.88% CAGR to 2031, fueled by China’s 290,000 new robot installations, India’s electronics mandates, and South Korea’s industrial 5G networks. Japan’s wafer-capacity additions are easing earlier MEMS shortages, while Australian miners deploy autonomous haulage systems laden with LiDAR and radar.

North America ranks second as predictive-maintenance adoption climbs in refineries and discrete manufacturing. U.S. factories integrate edge-AI gateways that crunch vibration and temperature streams, while Canadian oil-sands producers retrofit high-temp sensors into SAGD wells. Mexican automotive plants add pressure and inertial sensors as near-shoring accelerates electric-vehicle production.

Europe advances sensor content through electrified drivetrains and Level 2-plus ADAS, but wireless rollouts in critical infrastructure have slowed under NIS2 cyber-security rules. The Middle East prioritizes hydrogen pipelines and carbon-capture megaprojects that need specialty instrumentation. South American mines in Brazil and Chile automate fleets with ruggedized sensory suites, and African utilities gradually adopt water-quality and air-quality nodes as infrastructure spending ticks upward.

Competitive Landscape

The sensors and actuators market remains moderately fragmented: the top ten vendors hold 40%–45% of revenue while numerous specialists serve niches. Strategic acquisitions aim to secure MEMS IP and wafer access, exemplified by a 2025 piezoelectric-sensor takeover and a 2024 MEMS microphone purchase. Patent volumes in piezoelectric energy harvesting, neuromorphic fusion, and distributed acoustics exceed 50 filings each from multiple leaders.

Technology leadership hinges on embedding edge-AI accelerators into sensor interfaces, trimming latency and cloud fees. Analog and mixed-signal giants brought machine-learning cores into ASICs that sit next to vibration or temperature transducers, letting industrial clients shift anomaly detection from the server to the sensor. Smaller challengers differentiate via sector-specific form factors for food processing, pharma sterility, or wafer-fab cleanrooms, exploiting holes left by one-size incumbents.

Wireless and digital-first architectures are lowering barriers for software-centric entrants that monetize data analytics rather than hardware, but established manufacturers preserve scale advantages in reliability testing, global distribution, and certification. Consequently, rivalry will likely intensify around application-specific modules bundled with cloud or edge intelligence, reinforcing sustained innovation cycles in the sensors and actuators market.

Sensors And Actuators Industry Leaders

TE Connectivity Ltd

Texas Instruments Inc

Honeywell International Inc

Emerson Electric Co.

Bosch Sensortec

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Siemens AG committed EUR 350 million (USD 385 million) to expand its Amberg, Germany plant, adding 8-inch MEMS wafer lines and automated assembly for wireless industrial sensors.

- December 2025: Honeywell bought a fiber-optic sensing firm for USD 620 million to bolster pipeline integrity solutions in hydrogen and carbon-capture projects.

- November 2025: Bosch Sensortec unveiled battery-free MEMS accelerometers that harvest ambient vibration for industrial and building automation deployments.

- October 2025: TE Connectivity allocated USD 180 million for a Bangalore, India facility producing automotive pressure and temperature sensors, with output slated for Q3 2026.

Global Sensors And Actuators Market Report Scope

Sensors and actuators generally work together to automate and streamline industrial processes. A sensor is an electrical instrument that monitors and measures physical aspects of the environment and sends electrical signals to a control center when specific pre-determined conditions are detected. Sensors turn physical inputs into electrical signal output. Actuators receive electrical signals from control modules and turn them into physical outputs.

The Sensors and Actuators Market Report is Segmented by Product Type (Sensors, and Actuators), Technology (MEMS, and Non-MEMS), Connectivity (Wired, and Wireless), Output Signal (Digital, and Analog), End-User Industry (Automotive, Industrial Automation, Consumer Electronics, Healthcare, Oil and Gas, Aerospace, Building Automation, Utilities, and Mining), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Sensors | Pressure Sensors |

| Temperature Sensors | |

| Position Sensors | |

| Level Sensors | |

| Image Sensors | |

| Chemical/Bio-Sensors | |

| Torque Sensors | |

| Flow Sensors | |

| Actuators | Hydraulic Actuators |

| Pneumatic Actuators | |

| Electric Actuators | |

| Magnetic Actuators | |

| Mechanical Actuators | |

| Linear Actuators | |

| Rotary Actuators |

| MEMS |

| Non-MEMS / Conventional |

| Wired |

| Wireless |

| Digital |

| Analog |

| Automotive and Mobility |

| Industrial Automation and Robotics |

| Consumer Electronics and Wearables |

| Healthcare and Medical Devices |

| Oil, Gas and Energy |

| Aerospace and Defense |

| Building Automation and HVAC |

| Utilities, Water and Waste-Water, Power |

| Mining and Metals |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Product Type | Sensors | Pressure Sensors | |

| Temperature Sensors | |||

| Position Sensors | |||

| Level Sensors | |||

| Image Sensors | |||

| Chemical/Bio-Sensors | |||

| Torque Sensors | |||

| Flow Sensors | |||

| Actuators | Hydraulic Actuators | ||

| Pneumatic Actuators | |||

| Electric Actuators | |||

| Magnetic Actuators | |||

| Mechanical Actuators | |||

| Linear Actuators | |||

| Rotary Actuators | |||

| By Technology | MEMS | ||

| Non-MEMS / Conventional | |||

| By Connectivity | Wired | ||

| Wireless | |||

| By Output Signal | Digital | ||

| Analog | |||

| By End-User Industry | Automotive and Mobility | ||

| Industrial Automation and Robotics | |||

| Consumer Electronics and Wearables | |||

| Healthcare and Medical Devices | |||

| Oil, Gas and Energy | |||

| Aerospace and Defense | |||

| Building Automation and HVAC | |||

| Utilities, Water and Waste-Water, Power | |||

| Mining and Metals | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the sensors and actuators market by 2031?

The market is forecast to reach USD 34.24 billion by 2031, growing at a 9.36% CAGR from 2026.

Which region is expanding the fastest?

Asia-Pacific leads with a 12.88% CAGR through 2031, driven by robotics, automotive electronics, and private 5G rollouts.

Which product category is growing most rapidly?

Chemical and bio-sensors are advancing at a 10.40% CAGR thanks to demand in wearables and point-of-care diagnostics.

Why are MEMS devices gaining market share?

MEMS batch fabrication lowers cost, enables miniaturization, and supports long-life wireless deployments, giving them a 68.43% share in 2025.

Page last updated on: