Linear Motion System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

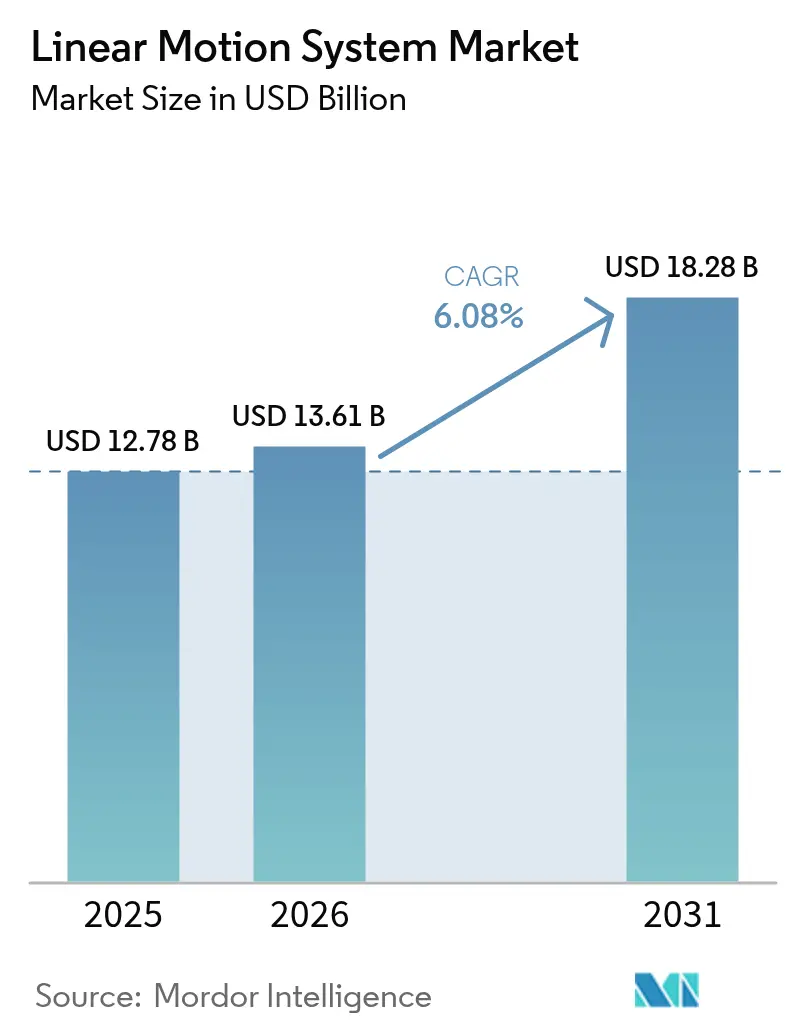

| Market Size (2026) | USD 13.61 Billion |

| Market Size (2031) | USD 18.28 Billion |

| Growth Rate (2026 - 2031) | 6.08% CAGR |

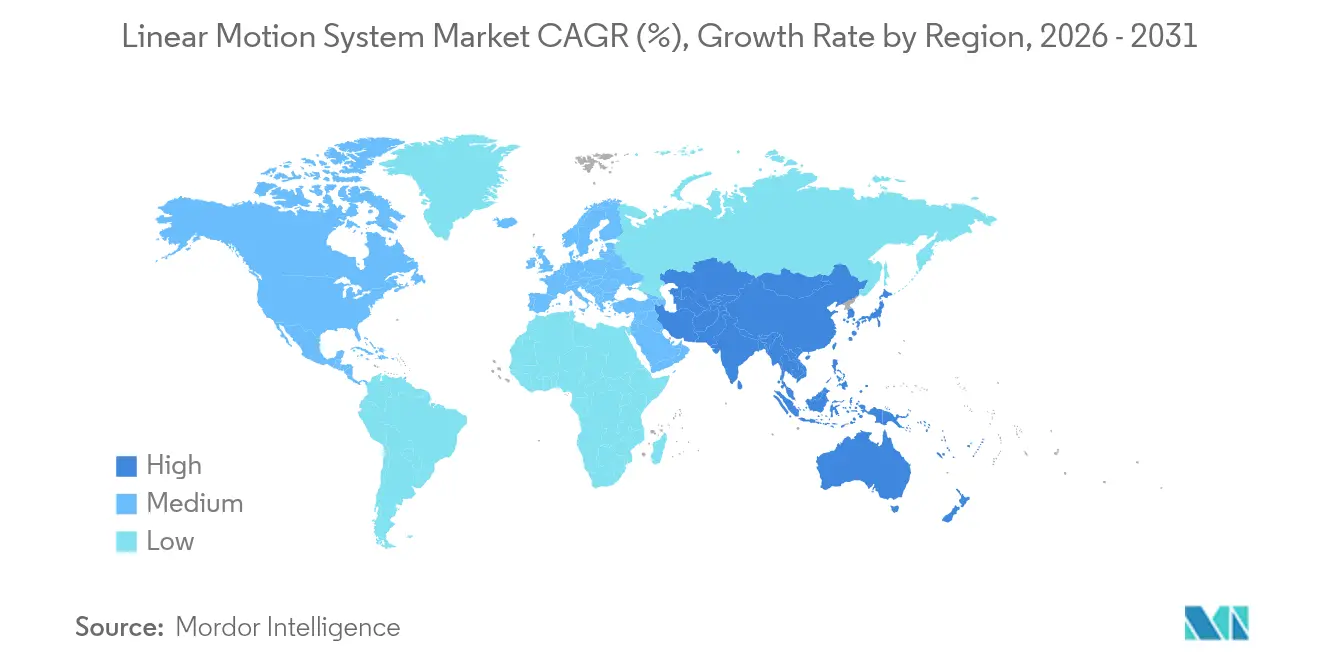

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Linear Motion System Market Analysis by Mordor Intelligence

The linear motion system market size is projected to be USD 13.61 billion in 2026 and reach USD 18.28 billion by 2031, growing at a CAGR of 6.08% between 2026 and 2031. The shift from pneumatic and hydraulic platforms toward electromechanical and direct-drive architectures is accelerating as plant managers seek tighter positional repeatability, lower lifetime cost, and seamless Industry 4.0 connectivity. Multi-axis platforms dominate in revenue terms because complex machine-tool and semiconductor stages demand synchronized X-Y-Z motion, yet direct-drive topologies are winning share due to their maintenance-free operation and energy savings. Component innovation is moving toward edge-intelligent controllers that embed real-time diagnostics and trajectory optimization, while advances in linear guides and miniature actuators support cleanroom deployment across semiconductor and medical-device facilities. Manufacturers are also compressing commissioning cycles through modular, software-defined motion stacks that can be reconfigured digitally when product lifecycles shorten.

Key Report Takeaways

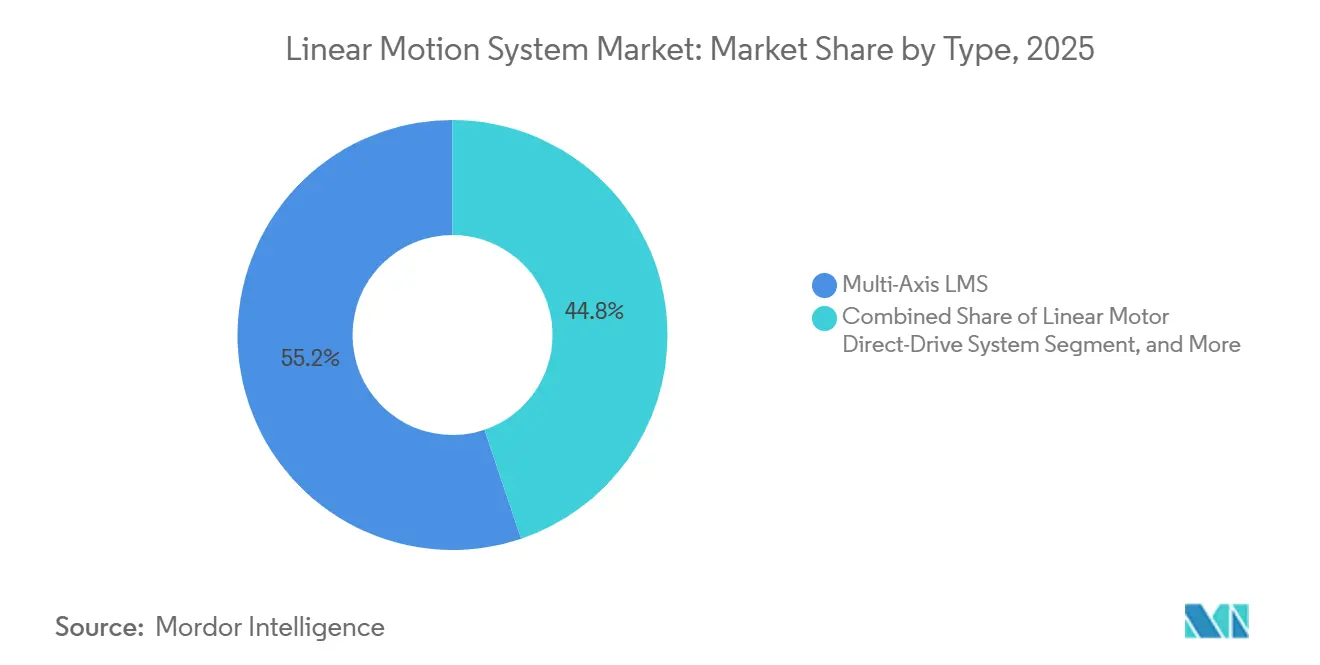

- By type, multi-axis platforms held 55.18% of the linear motion system market share in 2025, while linear motor direct-drive systems are forecast to expand at a 6.78% CAGR through 2031.

- By component, linear guides commanded 49.59% of 2025 revenue, yet controllers are projected to grow at a 6.96% CAGR to 2031.

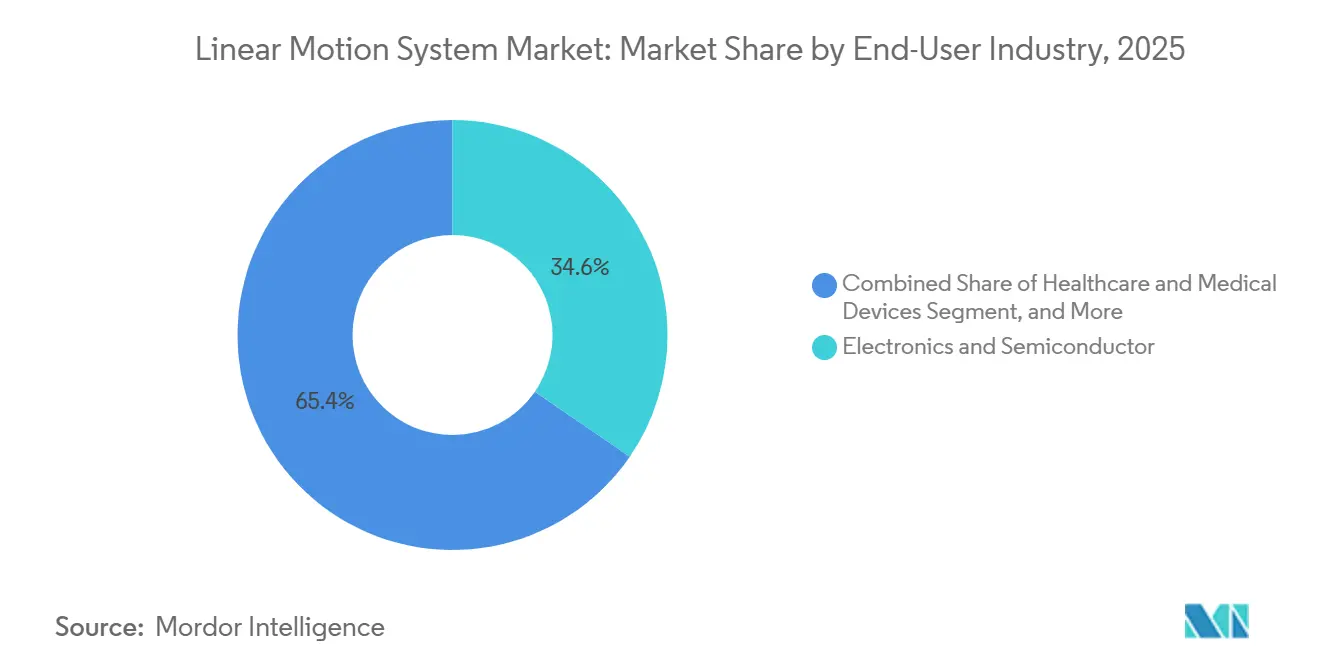

- By end-user industry, electronics and semiconductor fabrication accounted for 34.59% of 2025 demand and healthcare is expected to post a 6.55% CAGR, the fastest among all verticals, through 2031.

- By application, material handling captured 32.33% of 2025 installations, whereas robotics and cobots are poised to lead with a 7.01% CAGR to 2031.

- By geography, Asia-Pacific held 46.84% of global shipments in 2025, and South America is projected to advance at a 6.84% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Linear Motion System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Adoption of Industry 4.0 Automation | +1.80% | Global, with concentration in Germany, Japan, United States, South Korea | Medium term (2-4 years) |

| Expanding E-Commerce Boosting Automated Warehousing | +1.20% | North America and Europe core, APAC spill-over | Short term (≤ 2 years) |

| Rising Semiconductor and Electronics Precision Needs | +1.40% | APAC core (Taiwan, South Korea, Japan), spill-over to United States, Europe | Long term (≥ 4 years) |

| Demand Surge for Miniature Maintenance-Free LMS in Diagnostic Devices | +0.90% | North America and Europe, emerging in India, China | Medium term (2-4 years) |

| Sustainable Flexible-Package Formats Requiring High-Precision Motion | +0.60% | Global, early gains in Europe and North America | Medium term (2-4 years) |

| Reshoring Incentives for Medical-Device Clean-Room Lines | +0.70% | United States, Germany, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Adoption of Industry 4.0 Automation

Industrial executives see measurable gains from digitalized production. Plant upgrades that replace pneumatic cylinders with electromechanical actuators provide sub-micrometer feedback, enable over-the-air updates, and cut commissioning time by up to 40%. Edge-ready motion controllers now host Linux-based app ecosystems that push firmware and digital-twin data directly to the shop floor. These capabilities shorten changeover intervals when product batches fragment and allow predictive maintenance schedules to be generated automatically from live sensor data. As a result, the linear motion system market is increasingly tied to Industry 4.0 investment cycles rather than traditional capital-equipment budgets.

Expanding E-Commerce Boosting Automated Warehousing

Fulfilment operators are deploying vertical lift modules, shuttle systems, and mobile robots to meet next-day delivery promises. Each subsystem relies on high-cycle linear stages that position totes within milliseconds. Space utilization benefits are compelling because a single automated storage tower can replace 10,000 ft² of static racks, while energy-efficient direct-drive motors reduce total ownership cost by up to 20% over a decade. As third-party logistics providers extend networks into secondary cities, small-footprint, maintenance-free actuators become a core specification for new cross-dock hubs.

Rising Semiconductor and Electronics Precision Needs

Sub-3 nm lithography nodes demand wafer stages capable of maintaining overlay errors below a single nanometer while accelerating at multiple g-forces. Linear motors with active thermal management sustain peak forces above 10,000 N without derating, removing throughput bottlenecks in extreme-ultraviolet scanners. Asia-Pacific fabs under construction for advanced chips are ordering hundreds of such stages per site, locking in long-term demand for ultra-precision linear motion.

Demand Surge for Miniature Maintenance-Free LMS in Diagnostic Devices

Automated blood analysers and surgical robots require actuators no wider than 50 mm that operate particle-free in ISO 14644 cleanrooms. Plug-and-play modules that integrate motor, drive, and safety switches simplify FDA design-control documentation and accelerate time-to-market for new instruments. Pharmaceutical companies investing in continuous-manufacturing lines also prefer sealed, lubrication-free linear motors that eliminate contamination risk and support electronic batch records.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Cost and ROI Cycle of Customised Systems | -0.90% | Global, pronounced in cost-sensitive segments | Short term (≤ 2 years) |

| Scarcity of Skilled LMS Technicians | -0.60% | North America and Europe acute, emerging in APAC | Medium term (2-4 years) |

| Rare-Earth Magnet Price Volatility | -1.10% | Global, supply concentrated in China | Long term (≥ 4 years) |

| IEC-62443 Cybersecurity Compliance Cost for Smart LMS | -0.40% | North America and Europe, spreading to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rare-Earth Magnet Price Volatility

Permanent-magnet linear motors depend on neodymium-iron-boron alloys, yet China supplies more than 90% of refined material. Prices for neodymium-praseodymium oxide climbed 243% between 2020 and 2025, and new non-Chinese projects face higher capital intensity and stricter environmental permits. Motor makers evaluating ferrite or reluctance alternatives must accept a 30% loss of force density, limiting those options to low-torque applications and constraining near-term diversification efforts.

High Upfront Cost and ROI Cycle of Customized Systems

Roughly a quarter of new installations require bespoke stroke lengths, seals, or mounting flanges, pushing unit prices 40%-60% above catalogue norms. Direct-drive stages can repay themselves in as little as three years for high-duty cycles, yet small and medium factories with tight capex budgets often defer upgrades, preferring incremental pneumatic fixes. Leasing and as-a-service models are emerging, but adoption outside logistics remains limited.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Direct-Drive Topologies Gain Traction

Linear motor direct-drive platforms are expected to post a 6.78% CAGR, the highest among type categories, because they slash preventive-maintenance downtime and reduce energy use by up to 30%. Multi-axis assemblies still anchor more than half of 2025 revenue, driven by machine-tool gantries and semiconductor handlers that need coordinated motion. Single-axis systems satisfy simple pick-and-place duties where cost and speed outweigh sub-micron accuracy.[1]PBC Linear, “Flexible Manufacturing System Case Study,” pbclinear.com

Belt-driven stages remain the preferred solution for strokes exceeding 10 m at moderate loads, while ball-screw actuators balance thrust and pricing for general industrial automation. The linear motion system market maintains diverse topology demand because users match architecture to cycle rate, accuracy, and environmental constraints. Manufacturers increasingly evaluate safety certification, total cost, and digital-twin readiness alongside mechanical performance when selecting a topology.

By Component: Controllers Embed Edge Intelligence

Controllers are projected to outpace other components at a 6.96% CAGR because edge modules now handle vibration suppression, adaptive feed-rate control, and condition monitoring that once required separate hardware. The linear motion system market size for linear guides was nearly half of 2025 revenue thanks to their ubiquity in machine tools and packaging cells.

Linear bearings, actuators, and motors are transitioning toward brushless permanent-magnet designs that prolong life and improve thermal stability. Ball screws and lead screws still offer 5:1 to 50:1 mechanical advantage but cede precision niches to direct-drive motors. Cable chains, limit sensors, and lubrication cartridges round out system bills of material, and quick-connect interfaces shorten installation time.

By End-User Industry: Healthcare Leads Growth Trajectory

Healthcare devices are forecast to expand at a 6.55% CAGR through 2031 as hospitals automate diagnostics, surgical suites, and pharmacies. Cleanroom-rated miniature actuators underpin these gains by eliminating particulate shedding and easing regulatory validation.

Electronics and semiconductor fabs remain the largest demand pool at 34.59% of 2025 consumption, followed by automotive lines that pivot to battery and module assembly. Metals, machinery, aerospace, and food processing each apply linear motion for specialized tasks from metal forming to washdown packaging.

By Application: Robotics and Cobots Surge Ahead

Robotics and cobots are projected to lead application growth at 7.01% CAGR because collaborative workcells require force-limited linear stages that coexist safely with operators. Material handling already commands 32.33% of 2025 installations, reflecting widespread use in warehouses and palletizers.

Machine-tool spindles, labelling heads, pick-and-place gantries, and precision inspection rigs each rely on customized linear axes. The linear motion system market size for inspection platforms is expanding as zero-defect mandates push manufacturers to integrate automated metrology at every production stage.

Geography Analysis

Asia-Pacific represented 46.84% of global shipments in 2025, anchored by China’s rare-earth supply chain and Japan’s component expertise. Subsidies under India’s production-linked incentive scheme and South Korea’s USD 230 billion semiconductor roadmap will bolster regional orders for ultra-precision stages. North America contributed roughly 22% of 2025 revenue, benefitting from electric-vehicle assembly lines and medical-device reshoring supported by recent U.S. policy incentives. Mexico’s nearshoring inflows are translating directly into actuator demand for automotive and electronics plants serving United States customers.[2]United States Department of Energy, “Critical Materials Assessment,” energy.gov

Europe accounted for about 20% of 2025 installations, with Germany’s Industry 4.0 program sustaining machine-tool exports despite energy-price pressures. France’s re-industrialization initiative is upgrading packaging and pharmaceutical plants with next-generation linear motors and edge controllers. The Middle East, led by Saudi Arabia and the United Arab Emirates, is emerging as a boutique automation hub as government grants offset initial capex for greenfield factories.

South America is projected to grow fastest at 6.84% CAGR through 2031 as Brazilian automotive and Argentine food processors automate to curb labour inflation. Africa remains nascent, though South African auto assembly and Egyptian food-processing lines signal early motion-control adoption. Across regions, the linear motion system market encounters varying tariff, skills, and power-cost barriers that shape technology uptake.

Competitive Landscape

The five largest suppliers Bosch Rexroth, THK, Hiwin, NSK, and Parker Hannifin collectively held about 40% of 2025 revenue, yielding a moderately concentrated field. Each company operates vertically integrated plants that machine guides, screws, actuators, and controllers in-house to guarantee interchangeability.[3]THK Co. Ltd, “LM Guide Actuator IoT Upgrade,” thk.com

Regional specialists such as Akribis Systems and Aerotech focus on semiconductor metrology and aerospace inspection, where micron-level tolerances justify premium pricing. Strategic differentiation now centers on digital-twin bundles, IoT-enabled health monitoring, and modular kits that slice up to 40% from commissioning time. Patent activity in thrust-ripple suppression and magnetic-flux shaping has intensified since 2024, signalling a race to improve dynamic rather than static metrics.

White-space growth areas include collaborative-robot actuators with integrated torque sensing and sealed, lubrication-free units for FDA-regulated cleanrooms. Software-defined motion startups are unbundling hardware and control logic, allowing end users to mix vendor components while maintaining synchronized trajectories, thereby challenging traditional closed ecosystems.

Linear Motion System Industry Leaders

Bosch Rexroth AG (Robert Bosch GmbH)

Schneeberger Group

Ewellix AB (Schaeffler Group)

Hiwin Corporation

Thomson Industries Inc. (Regal Rexnord Corporation)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Rockwell Automation rolled out FactoryTalk Studio updates that auto-tune linear profiles for collaborative robots, cutting programming time by 30%.

- January 2025: Schneider Electric expanded its Lexium cobot series with ISO/TS 15066 safety functions aimed at electronics assembly cells.

- November 2024: Parker Hannifin Corporation acquired Precision Motion Industries for USD 280 million, boosting its medical mini-actuator line.

- October 2024: NSK Ltd formed a joint venture with Siemens AG for integrated Industry 4.0 motion solutions targeting Europe.

Global Linear Motion System Market Report Scope

The Linear Motion System Market Report is Segmented by Type (Single-Axis, Multi-Axis, Belt-Driven, Ball Screw, Linear Motor Direct-Drive), Component (Actuators and Motors, Linear Guides, Linear Bearings, Controllers, Ball Screws and Lead Screws, Other Components), End-User Industry (Automotive, Electronics and Semiconductor, Manufacturing Metals and Machinery, Aerospace and Defense, Healthcare and Medical Devices, Food and Beverage, Logistics and Warehousing, Other End-User Industries), Application (Material Handling, Machine Tools, Robotics and Cobots, Packaging and Labelling, Pick-and-Place, Inspection and Metrology, Other Applications), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Single-Axis Linear Motion System |

| Multi-Axis Linear Motion System |

| Belt-Driven Linear Motion System |

| Ball Screw Linear Motion System |

| Linear Motor Direct-Drive System |

| Actuators and Motors |

| Linear Guides |

| Linear Bearings |

| Controllers |

| Ball Screws and Lead Screws |

| Other Components |

| Automotive |

| Electronics and Semiconductor |

| Manufacturing, Metals and Machinery |

| Aerospace and Defense |

| Healthcare and Medical Devices |

| Food and Beverage |

| Logistics and Warehousing |

| Other End-User Industries |

| Material Handling |

| Machine Tools |

| Robotics and Cobots |

| Packaging and Labelling |

| Pick-and-Place |

| Inspection and Metrology |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Type | Single-Axis Linear Motion System | |

| Multi-Axis Linear Motion System | ||

| Belt-Driven Linear Motion System | ||

| Ball Screw Linear Motion System | ||

| Linear Motor Direct-Drive System | ||

| By Component | Actuators and Motors | |

| Linear Guides | ||

| Linear Bearings | ||

| Controllers | ||

| Ball Screws and Lead Screws | ||

| Other Components | ||

| By End-User Industry | Automotive | |

| Electronics and Semiconductor | ||

| Manufacturing, Metals and Machinery | ||

| Aerospace and Defense | ||

| Healthcare and Medical Devices | ||

| Food and Beverage | ||

| Logistics and Warehousing | ||

| Other End-User Industries | ||

| By Application | Material Handling | |

| Machine Tools | ||

| Robotics and Cobots | ||

| Packaging and Labelling | ||

| Pick-and-Place | ||

| Inspection and Metrology | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the global linear motion system size be by 2031?

It is forecast to reach USD 18.28 billion by 2031.

What compound annual growth rate is expected for linear motion systems between 2026 and 2031?

A 6.08% CAGR is projected for the 2026-2031 period.

Which platform type is expanding at the quickest pace?

Direct-drive linear motor systems are set to grow the fastest, advancing at a 6.78% CAGR.

Why are healthcare applications adopting linear motion technology so rapidly?

Hospitals and laboratories need miniature, maintenance-free actuators for diagnostics and surgical robotics, fueling a 6.55% CAGR in healthcare demand.

Which geographic region is projected to post the highest growth through 2031?

South America is expected to advance at a 6.84% CAGR, led by Brazilian and Argentine automation investments.

How concentrated is supplier competition in linear motion systems?

The top five vendors control about 40% of global revenue, indicating moderate concentration with room for regional specialists.

Page last updated on: