Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 44.25 Billion |

| Market Size (2031) | USD 56.63 Billion |

| Growth Rate (2026 - 2031) | 5.05% CAGR |

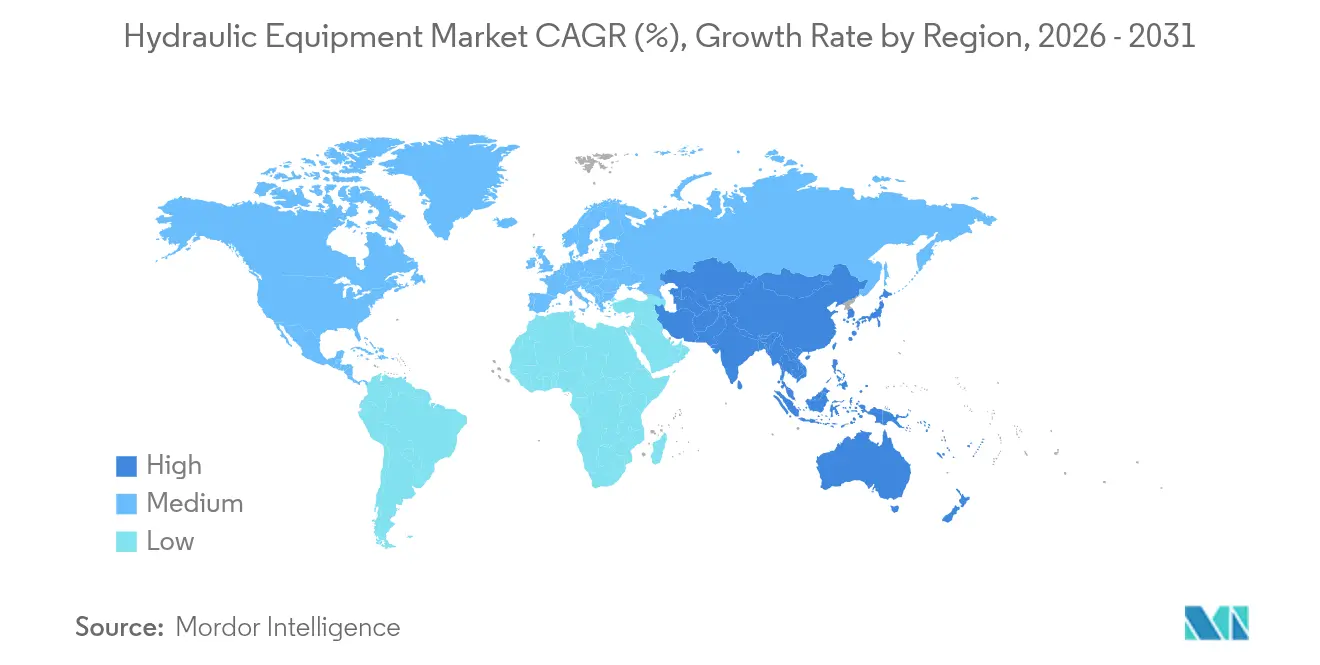

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Hydraulic Equipment Market Analysis by Mordor Intelligence

The hydraulic equipment market size was valued at USD 42.11 billion in 2025 and estimated to grow from USD 44.25 billion in 2026 to reach USD 56.63 billion by 2031, at a CAGR of 5.05% during the forecast period (2026-2031). This steady momentum underscores the sector’s resilience in the face of cyclical slowdowns, raw material volatility, and intensifying pressures from electrification. Robust public infrastructure spending in the United States and China, rising warehouse automation in global e-commerce, and expanding precision agriculture underpin demand, even as equipment makers accelerate the shift toward energy-efficient electro-hydraulic hybrids. Heightened consolidation, exemplified by Applied Industrial Technologies' acquisition of Hydradyne, signals how suppliers are responding to margin compression and the need for digital, power-dense solutions. North America remains the largest regional base, supported by unprecedented water infrastructure appropriations, while the Asia-Pacific records the fastest gains as China and India commit multi-trillion-dollar stimulus to transport and urban services.

Key Report Takeaways

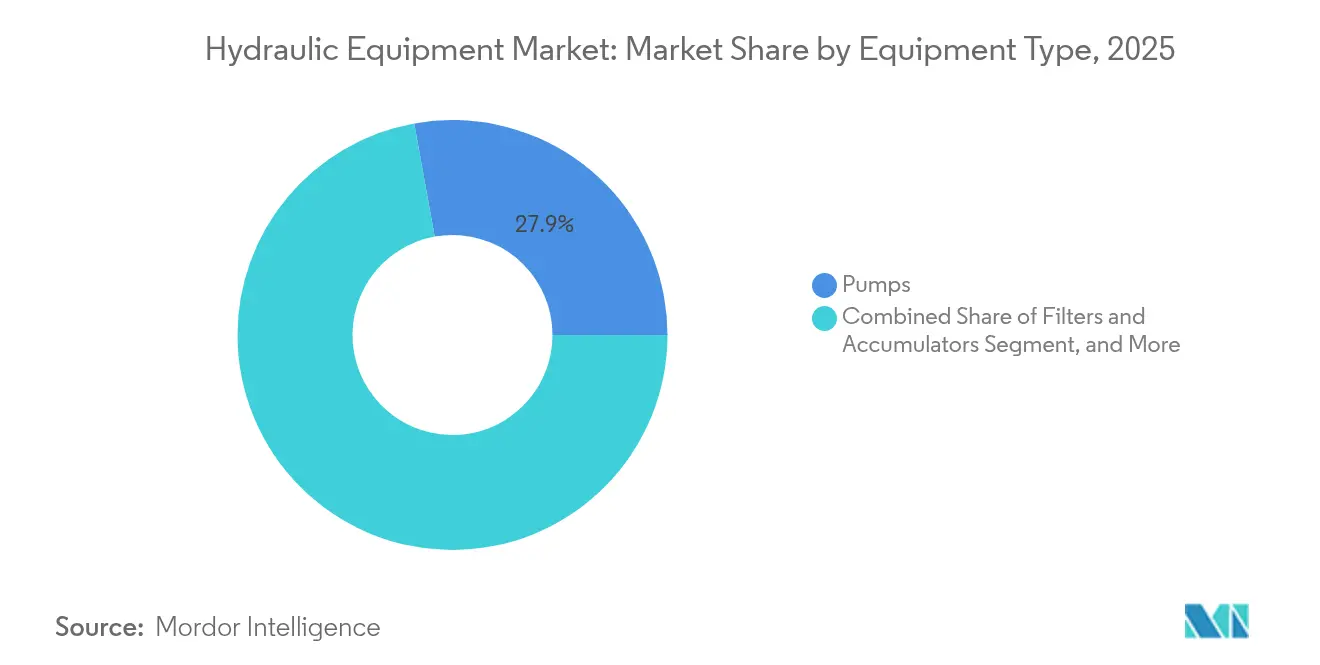

- By equipment type, pumps led with 27.85% of hydraulic equipment market share in 2025; filters and accumulators are projected to grow at a 6.18% CAGR through 2031.

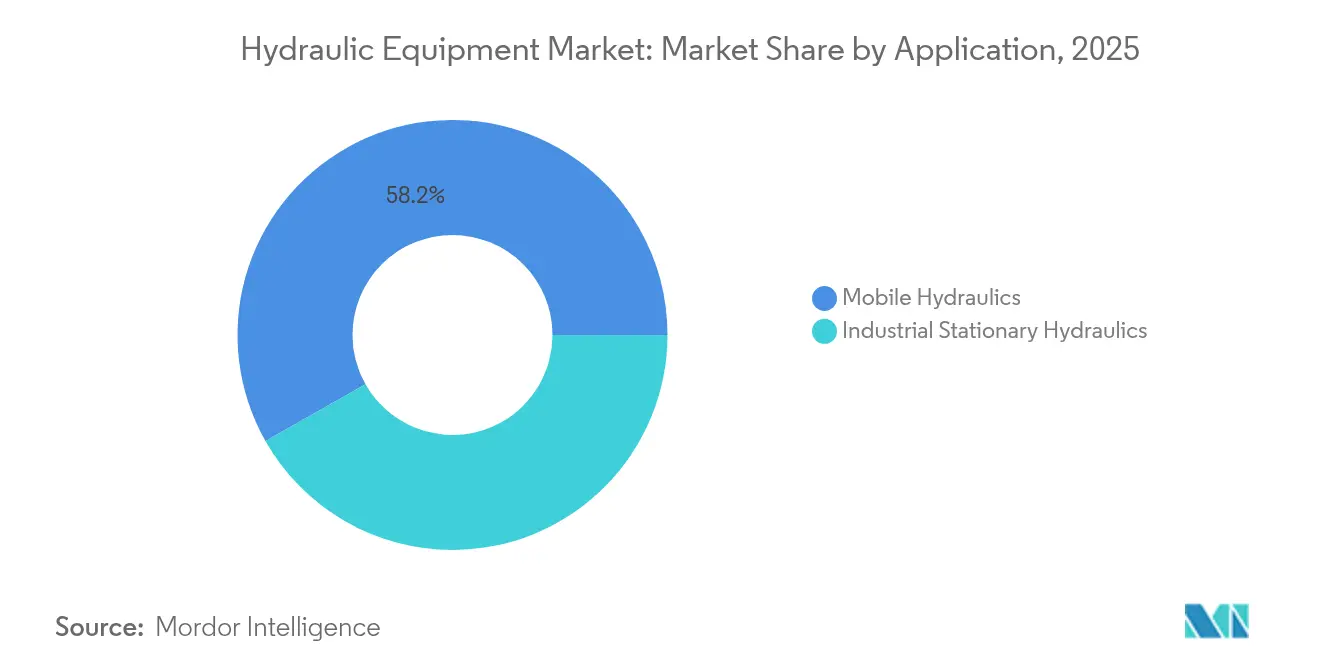

- By application, mobile hydraulics captured 58.20% revenue in 2025 and is advancing at an 7.72% CAGR to 2031.

- By end-user, construction dominated with 31.05% contribution in 2025; aerospace and defense is forecast to expand at a 6.35% CAGR to 2031.

- By operating-pressure range, medium-pressure systems held 42.35% of the hydraulic equipment market size in 2025, while high-pressure systems are projected to post a 7.29% CAGR through 2031.

- By geography, North America retained 37.65% share in 2025; Asia-Pacific is set to register an 8.07% CAGR and deliver the fastest regional growth to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hydraulic Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated warehouse automation in e-commerce fulfillment | +1.20% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Government-funded mega infrastructure programmes | +1.80% | North America, Asia-Pacific core, spill-over to Europe | Long term (≥ 4 years) |

| Shift to energy-efficient electro-hydraulic hybrids | +0.90% | Global, early adoption in Europe and North America | Long term (≥ 4 years) |

| Increasing off-highway electrification driving compact power-dense hydraulics | +0.70% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growing adoption of precision agriculture machinery | +0.60% | Global, with early gains in North America, Brazil, India | Medium term (2-4 years) |

| Ageing industrial machinery replacement cycle in OECD | +0.50% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated Warehouse Automation in E-commerce Fulfillment

Explosive e-commerce order volumes compel distribution centers to deploy autonomous forklifts, shuttle systems, and goods-to-person robots that rely on compact servo-hydraulic cylinders for milli-meter accuracy. Amazon’s network of mobile robots illustrates how 24/7 operation requires leak-free, sensor-equipped hydraulics offering predictive failure alerts to minimize downtime.[1]Logistics Management Editors, “Autonomous Forklift Market to Reach USD 12.45 Billion by 2034,” LOGISTICSMGMT.COM Warehouse operators typically report 40% productivity gains, enabling component suppliers to charge premium prices for ultra-reliable, contamination-controlled assemblies.

Government-Funded Mega-Infrastructure Programmes

Multi-year public works—from the USD 1.2 trillion U.S. Infrastructure Investment and Jobs Act to China’s USD 1.4 trillion local-government debt plan—create demand visibility for excavators, concrete pumps, and large-bore cylinders.[2]Reuters Staff, “China Approves USD 1.4 Trillion Debt Package for Local Governments,” REUTERS.COM Extended project pipelines allow OEMs to lock-in long-term contracts, expand regional service hubs, and co-develop application-specific hydraulics for bridge, port, and renewable-energy construction.

Shift to Energy-Efficient Electro-Hydraulic Hybrids

Electro-hydrostatic actuators from Bosch Rexroth demonstrate up to 30% energy savings while retaining the power density vital for mobile machinery.[3]Bosch Rexroth AG, “Electro-Hydraulic Actuators Deliver 30% Energy Savings,” BOSCHREXROTH.COM Hybrid circuits recuperate braking energy and slash idle losses, helping equipment makers meet Stage V and Tier 4f emissions limits without sacrificing rapid response or lifting capacity.

Increasing Off-Highway Electrification

OEMs electrifying compact loaders and aerial work platforms increasingly specify high-pressure micro-hydraulic pumps that deliver identical force from smaller battery packs. Component miniaturization eases packaging constraints in zero-emission drivetrains, while silent operation and instant torque improve operator comfort, raising adoption in Europe’s low-emission job sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Total cost of ownership higher than electric drives in light-duty ranges | -1.10% | Global, most pronounced in Europe and North America | Medium term (2-4 years) |

| Intensifying raw-material price volatility for steel and rare earths | -0.80% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Rising ESG scrutiny over hydraulic-fluid leakage | -0.60% | Europe and North America, expanding globally | Long term (≥ 4 years) |

| Skilled-labour shortage for maintenance and retrofits | -0.40% | OECD countries, emerging in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Raw-Material Price Volatility for Steel and Rare Earths

Steel prices swung 40% in 2024, while China’s dominance of rare-earth processing exposes magnet-motor supply chains to geopolitical risk.[4]U.S. Geological Survey, “Critical Minerals List 2024,” USGS.GOV Tariffs of 44–54% on Chinese hydraulic components further compress margins, forcing suppliers to hedge commodities, redesign to reduce material intensity, or pursue scale through mergers.

Skilled-Labor Shortage for Maintenance and Retrofits

NFPA surveys indicate that 35% of fluid-power technicians will retire within the next decade, while training pipelines struggle to meet demand.[5]National Fluid Power Association, “Workforce Development Survey 2024,” NFPA.COM Shortfalls prolong downtime on high-pressure systems, inflate service contracts, and drive some fleet operators to delay upgrades, throttling replacement sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Equipment Type: Pumps Retain Primacy, Filters Accelerate

Pumps anchored 27.85% of the hydraulic equipment market in 2025 as the indispensable power-source across construction, agriculture, and industrial machinery. Variable-displacement and load-sensing models cut fuel draw, satisfying OEM efficiency targets and boosting aftermarket retrofit sales. The hydraulic equipment market size for pumps is positioned to advance with infrastructure investment cycles through 2031. Filters and accumulators log the quickest gains at a 6.18% CAGR as stricter ISO 4406 cleanliness codes make contamination control decisive during warranty negotiations. Demand for high-flow, low-delta-pressure filter media elevates margins, while nitrogen-charged bladders store regenerative energy in hybrid circuits, extending the hydraulic equipment market share of this sub-segment across mobile applications.

Valve suppliers capitalize on precision flow control required by tele-operation and autonomous tasks. Cylinders benefit from e-commerce warehouse robotics that necessitate repeatable, high-cycle linear motion. Motors and transmissions cater to specialty mobile equipment where torque density and overload capacity remain critical. Ancillary components—reservoirs, manifolds, coolers—gain from integrated power-packs that simplify OEM assembly lines and shorten time-to-market.

By End-User Industry: Construction Dominates, Aerospace Accelerates

Construction contributed 31.05% of hydraulic equipment market revenue in 2025, buoyed by global public-works pipelines and commercial real-estate starts. Fleet operators adopt electro-hydraulic hybrids to meet stricter job-site emissions caps, sustaining high utilization and parts consumption. The hydraulic equipment market size for construction is poised for stable mid-single-digit growth as bridge, port, and rail projects consume long-stroke actuators and heavy-duty pumps over multi-year timelines. Aerospace and defense, however, posts the sharpest trajectory at 6.35% CAGR as commercial narrow-body production ramps and defense agencies modernize airframes. High-pressure, weight-optimized actuation for flight-control and landing-gear commands premium pricing, increasing the hydraulic equipment market share captured by aerospace suppliers.

Agriculture maintains steady gains as precision farming embeds GPS-guided hydraulics for centimeter-level seed placement. Material-handling thrives on omnichannel retail logistics, while oil and gas demand stabilizes around offshore construction and pipeline maintenance. Machine-tool, plastics, and automotive segments experience mixed trends tied to global manufacturing cycles yet remain indispensable volume anchors for seal, valve, and small-bore cylinder demand.

By Application: Mobile Hydraulics Expands Rapidly

Mobile hydraulics held 58.20% revenue in 2025 and is expected to achieve the segment’s highest 7.72% CAGR to 2031. Equipment replacements in North America and capacity additions in Asia amplify shipments of swing drives, travel motors, and load-sensing pumps. The push toward electro-hydraulic hybrids positions suppliers with advanced energy-recovery valves to gain disproportionate share. The hydraulic equipment market size for the mobile segment widens as regulatory credits reward CO₂-saving systems. Stationary industrial hydraulics remains a mature but essential base, with servo-valves and proportional pumps supporting precision metal-forming and injection-molding processes.

By Operating-Pressure Range: High-Pressure Systems Gain Momentum

Medium-pressure architectures (150–350 bar) comprised 42.35% of 2025 revenue, prized for balanced cost-performance in mainstream excavators and presses. High-pressure (>350 bar) solutions, however, exhibit a 7.29% CAGR as aerospace, tunneling, and exo-skeleton robotics require compact, power-dense packages. Material advances in chrome-plated rods and high-temperature seals prove critical for endurance. Low-pressure (<150 bar) markets remain price-sensitive and face substitution risk from all-electric actuators in lightweight tasks.

Geography Analysis

North America generated 37.65% of global revenue in 2025, supported by USD 68.8 billion in obligated water-infrastructure funds and USD 850 million dedicated to reclamation projects. Robust warehouse-automation investments and aging fleet replacements underpin sales of cylinders, proportional valves, and filtration kits. Nevertheless, the softness of transport equipment presents a headwind, prompting suppliers to emphasize aftermarket service contracts and digitalized maintenance offers.

The Asia-Pacific region registers the fastest growth, with an 8.07% CAGR through 2031, as China’s USD 1.4 trillion credit package and India’s urban-rail and water-supply programs sustain demand peaks beyond domestic cycles. Local OEMs partner with component specialists to meet Tier 4f standards, while tariff disputes prompt multinational suppliers to diversify assembly footprints into Southeast Asia. High-pressure micro-pumps and contamination-resistant valves are seeing a rising take-up in Korean and Japanese precision-manufacturing clusters.

Europe presents a mixed outlook: German fluid-power orders fell 8% in 2024, yet projects such as France’s Grand Paris Express and Italy’s wind-farm builds drive niche high-pressure requirements. PFAS restrictions are accelerating the shift to bio-based seals, prompting significant R&D investment across the hydraulic equipment market. The REPowerEU plan’s EUR 300 billion (USD 339 billion) allocation for renewable energy infrastructure multiplies demand for telescopic cylinders in offshore wind installation vessels, cushioning macroeconomic softness.

Competitive Landscape

The hydraulic equipment market remains moderately fragmented, yet consolidation is accelerating as suppliers pursue scale and technological depth. Applied Industrial Technologies’ acquisition of Hydradyne (USD 260 million sales) enlarges its service footprint in mobile hydraulics and enhances engineered-systems capabilities. Atlas Copco’s planned USD 218 million acquisition of National Tank & Equipment strengthens its niche in high-pressure filtration and dewatering systems, broadening cross-selling potential in the mining and construction sectors.

Strategic moves pivot on electrification, digital condition monitoring, and ESG compliance. Bosch Rexroth’s integration of HydraForce deepens its mobile-valve stack, enabling differentiated load-sensing architectures for hybrid excavators. Parker Hannifin secures record margins by streamlining its aerospace and filtration portfolios, demonstrating how disciplined inventory and pricing can offset sectoral weakness. Mid-tier players are pursuing IoT-enabled predictive maintenance modules to ease the skilled labor bottleneck and lock in recurring software-as-a-service revenue.

White-space opportunities multiply in autonomous construction, renewable-energy erection, and precision farming. Suppliers able to merge high-pressure capability with energy-harvesting and sensorized analytics stand to capture a premium share as OEMs re-platform equipment around zero-emission mandates. The hydraulic equipment market, therefore, rewards those investing in material science, digital twins, and plug-and-play sub-systems that lower OEM engineering costs and accelerate time-to-compliance.

Hydraulic Equipment Industry Leaders

-

Bosch Rexroth AG

-

Parker Hannifin Corporation

-

Danfoss A/S

-

KYB Corporation

-

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: Parker Hannifin Corporation's Pump & Motor Division Europe has launched its new T7G Series of truck hydraulic pumps. These single and double hydraulic vane pumps, equipped with durable new housings and Parker's state-of-the-art variable speed drive technology, are designed to meet the ISO 7653 mounting standard. The T7G series, an evolution of the T6G Series, caters to diesel trucks and hybrid, electric, and hydrogen vehicles.

- September 2024: Atlas Copco agreed to acquire National Tank and Equipment, expanding into specialty high-pressure pumping for mining. The move diversifies revenue away from compressors and leverages Atlas’ global distribution to scale niche hydraulic rental assets.

- October 2024: Applied Industrial Technologies purchased Hydradyne, adding USD 260 million in sales and deepening aftermarket service density across the Gulf Coast. The strategy centers on bundling engineered systems with filtration and IoT retrofits to increase the customer's share of the wallet.

- November 2024: Texas Hydraulics and TH Holdings were acquired by Fortress Investment Group. The private-equity entry supplies capital for factory automation and new hybrid-cylinder lines, positioning the business to serve infrastructure backlogs in North America.

Global Hydraulic Equipment Market Report Scope

Hydraulic equipment employs pressurized fluid to perform a wide range of machining operations. A pump, driven by an engine or motor, pressurizes the hydraulic fluid within the machinery. This pressurized fluid travels through hydraulic tubes to the machine's actuators, which harness the fluid's pressure to execute their tasks. The market is defined by the revenue generated from the global hydraulic equipment sales by diverse market players.

The hydraulic equipment market is segmented by type (pumps, valves, cylinders, motors, filters and accumulators, transmission, and other product types), end-user industry (construction, agriculture, material handling, aerospace and defense, machine tools, oil and gas, hydraulic press, plastics, automotive, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Rest of the World ). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Equipment Type

| Pumps |

| Valves |

| Cylinders |

| Motors |

| Filters and Accumulators |

| Transmissions |

| Others |

By End-user Industry

| Construction |

| Agriculture |

| Material Handling |

| Aerospace and Defence |

| Machine Tools |

| Oil and Gas |

| Hydraulic Press |

| Plastics |

| Automotive |

| Other End-users |

By Application

| Mobile Hydraulics |

| Industrial Stationary Hydraulics |

By Operating-Pressure Range

| Low (Less than 150 bar) |

| Medium (150-350 bar) |

| High (Greater than 350 bar) |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Equipment Type | Pumps | ||

| Valves | |||

| Cylinders | |||

| Motors | |||

| Filters and Accumulators | |||

| Transmissions | |||

| Others | |||

| By End-user Industry | Construction | ||

| Agriculture | |||

| Material Handling | |||

| Aerospace and Defence | |||

| Machine Tools | |||

| Oil and Gas | |||

| Hydraulic Press | |||

| Plastics | |||

| Automotive | |||

| Other End-users | |||

| By Application | Mobile Hydraulics | ||

| Industrial Stationary Hydraulics | |||

| By Operating-Pressure Range | Low (Less than 150 bar) | ||

| Medium (150-350 bar) | |||

| High (Greater than 350 bar) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast is the hydraulic equipment market expected to grow through 2031?

It is forecast to expand from USD 44.25 billion in 2026 to USD 56.63 billion by 2031, marking a 5.05% CAGR driven by infrastructure outlays and mobile-equipment electrification.

What sub-segment leads hydraulic equipment demand?

Pumps dominate with 27.85% revenue share thanks to their indispensable role as the power source in virtually every hydraulic circuit.

Which region offers the highest growth opportunity?

Asia-Pacific posts an 8.07% CAGR through 2031 as China and India unleash multi-trillion-dollar infrastructure and urbanization programs.

Why are electro-hydraulic hybrids gaining traction?

They deliver up to 30% energy savings and help OEMs meet stringent emissions rules while maintaining hydraulic power density.

What is the main restraint facing suppliers today?

Extreme volatility in steel and rare-earth prices compresses margins and complicates long-term pricing agreements.

How are companies addressing the skilled-labor gap in maintenance?

Leading firms embed sensors and develop predictive-maintenance software that reduces service time and broadens the technician talent pool.

Page last updated on: