Piezoelectric Actuators And Motors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

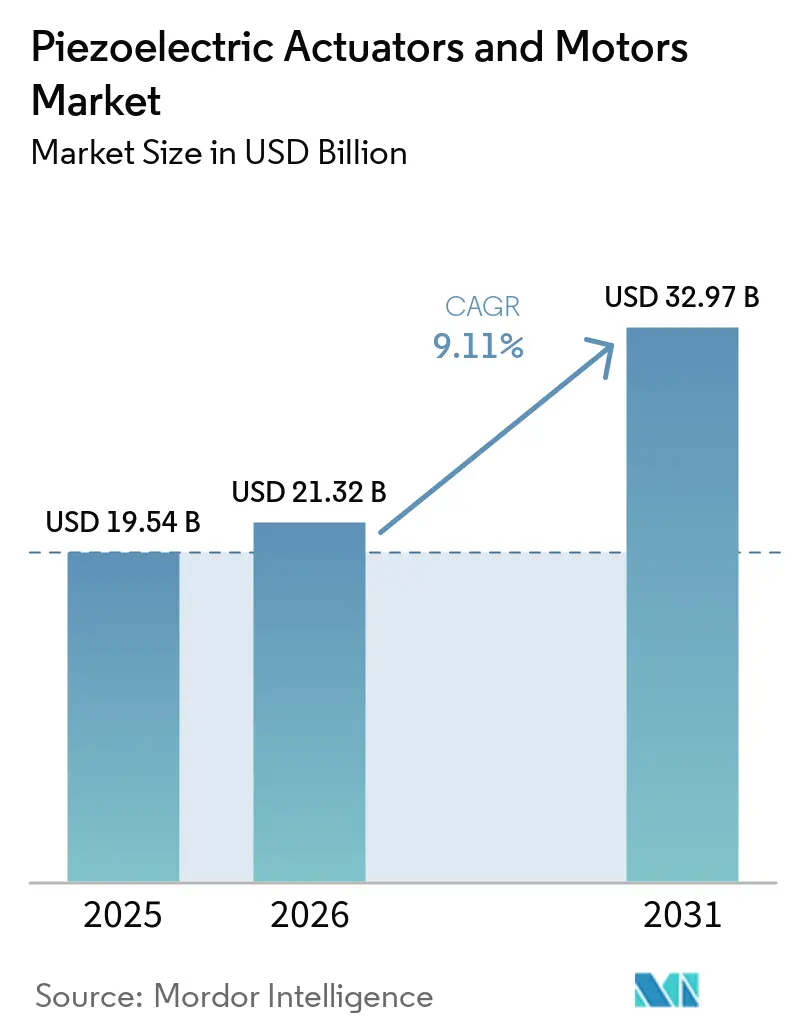

| Market Size (2026) | USD 21.32 Billion |

| Market Size (2031) | USD 32.97 Billion |

| Growth Rate (2026 - 2031) | 9.11% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Piezoelectric Actuators And Motors Market Analysis by Mordor Intelligence

The piezoelectric actuators and motors market size is expected to increase from USD 19.54 billion in 2025 and USD 21.32 billion in 2026 and reach USD 32.97 billion by 2031, growing at a CAGR of 9.11% over 2026-2031. The piezoelectric actuators and motors market is advancing because semiconductor lithography, medical robotics, and photonic integration all require motion control at precision levels that electromagnetic alternatives cannot match within similar space constraints. The supply base for electroceramics remains concentrated in Japan, Germany, and South Korea, which continues to shape pricing discipline and delivery timelines for system integrators across regions. Export controls on advanced semiconductor equipment and the reshoring of precision manufacturing are supporting near-term demand in North America and Europe, while Asia-Pacific remains anchored by large electronics and semiconductor production clusters. Procurement teams are also paying closer attention to lead-containing PZT exposure under the RoHS exemption, and this is bringing lead-free material qualification into sourcing decisions across the piezoelectric actuators and motors market. At the same time, closed-loop smart motion platforms with AI-based drift compensation are moving into production settings, reducing practical adoption barriers tied to drift and system costs.

Key Report Takeaways

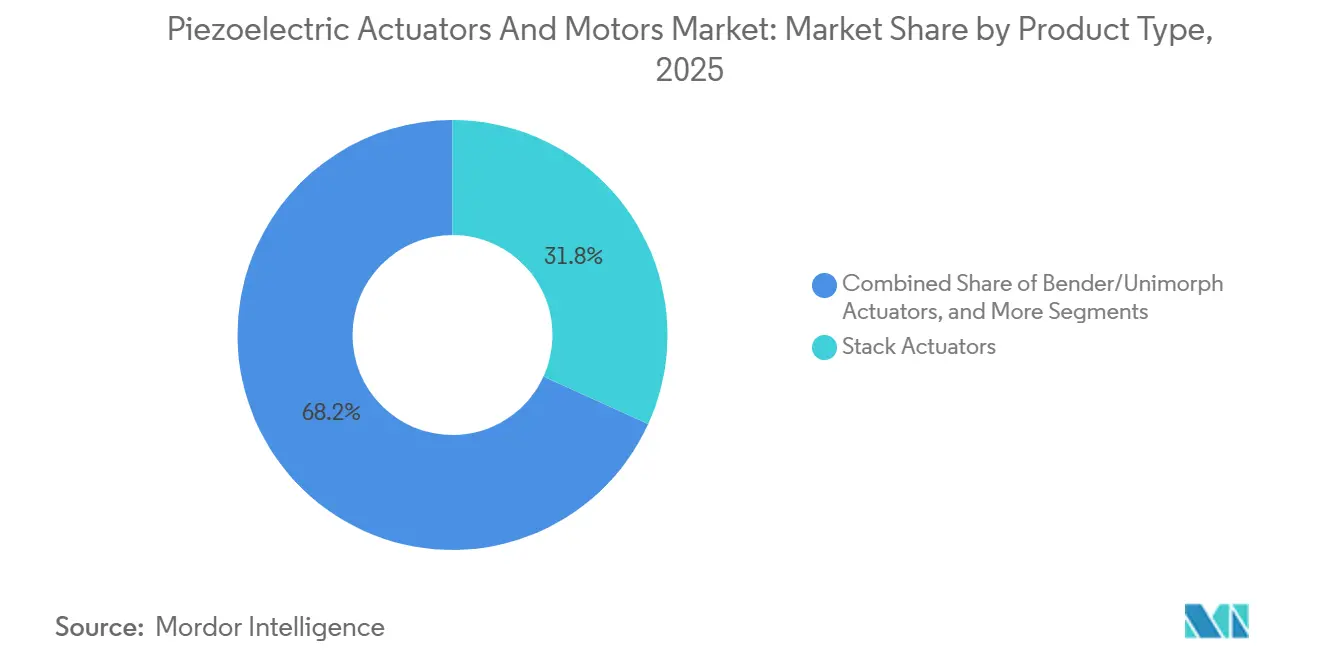

- By product type, stack actuators led with 31.80% share of piezoelectric actuators and motors market in 2025, while ultrasonic motors, linear variants specifically, are projected to expand at 9.28% CAGR through 2031.

- By operation principle, resonant and ultrasonic systems held 46.47% share of piezoelectric actuators and motors market in 2025, while hybrid-mode systems are projected to grow at 9.35% CAGR through 2031.

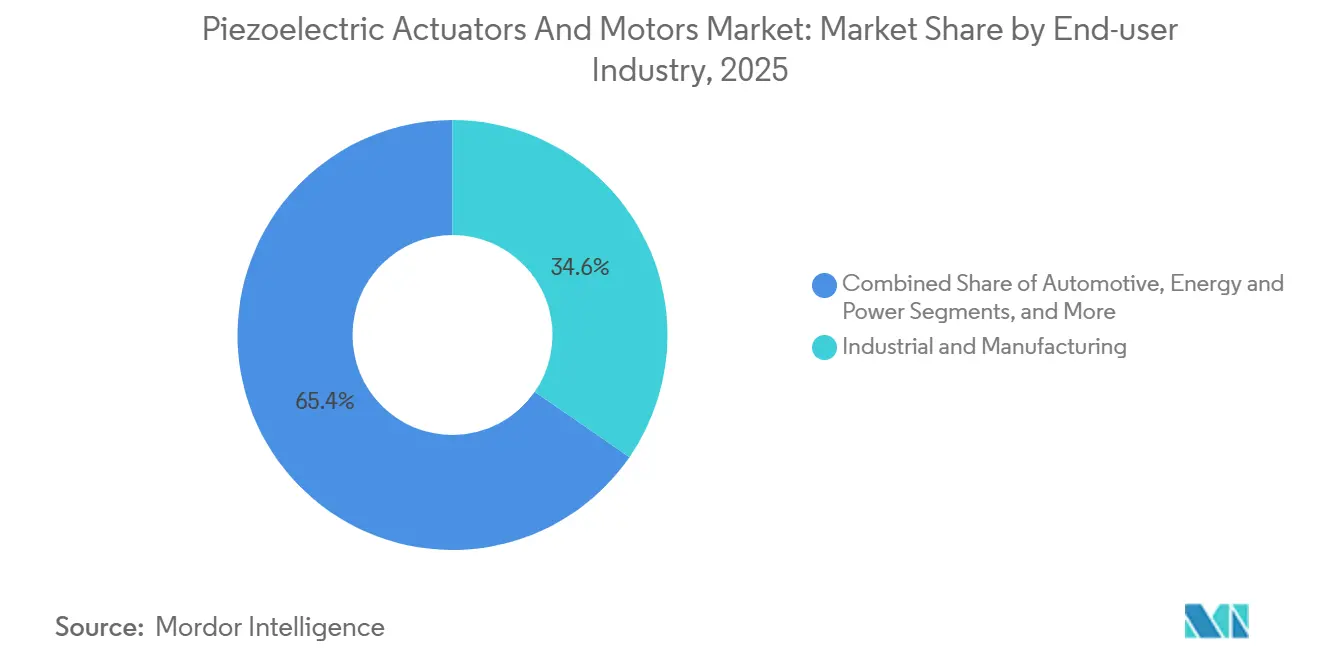

- By end-user industry, industrial and manufacturing accounted for 34.62% share of piezoelectric actuators and motors market in 2025, while medical and life sciences is forecast to advance at 10.02% CAGR through 2031.

- By application, precision and nanopositioning held 32.91% share of piezoelectric actuators and motors market in 2025, while robotics and micromanipulation is expected to grow at 9.97% CAGR through 2031.

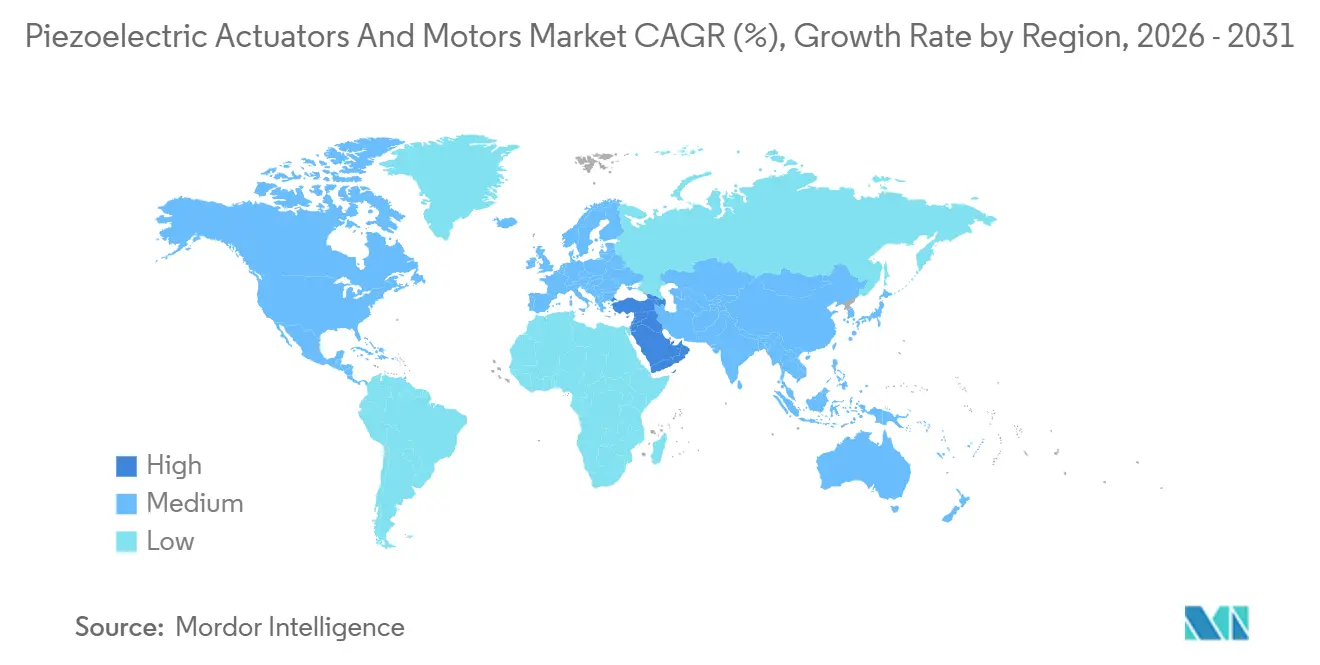

- By geography, Asia-Pacific held 40.75% share of piezoelectric actuators and motors market in 2025, while the Middle East is projected to expand at 9.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Piezoelectric Actuators And Motors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Semiconductor Lithography and Advanced Packaging Precision Demand | +2.1% | Global, core intensity in Asia-Pacific, North America | Short term (≤ 2 years) |

| Medical and Surgical Robotics Need for Non-Magnetic Silent Motion | +1.8% | North America and Europe, with growing spillover to Asia-Pacific | Medium term (2-4 years) |

| Optical Alignment and Photonics Proliferation in Datacom and Imaging | +1.5% | Global, strongest in North America, Europe, and East Asia | Medium term (2-4 years) |

| Miniaturized Consumer Camera and Sensing Modules | +1.2% | Asia-Pacific, spreading through global OEM supply chains | Short term (≤ 2 years) |

| RoHS-Driven Shift to Lead-Free Piezo Platforms | +0.9% | Europe, North America, with compliance spillover to Asia-Pacific | Long term (≥ 4 years) |

| Closed-Loop Smart Motion Architectures With AI Compensation | +0.8% | Global, early adoption concentrated in Germany, the United States, and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Semiconductor Lithography And Advanced Packaging Precision Demand

The move toward sub-3 nm device architectures has made piezoelectric positioning increasingly central to the piezoelectric actuators and motors market, especially inside EUV and high-NA EUV lithography tools. Researchers at SPIE Advanced Lithography and Patterning 2026 presented a 3-DOF thin-film PZT actuator integrated into pillar-supported substrates for EUV overlay correction, with displacement above 30 nm and sub-nanometer repeatability. SPIE Advanced Packaging is reinforcing this demand pattern because wafer-level fan-out and chiplet bonding require high-force, low-voltage multilayer stack actuators that also operate in cleanroom-compatible environments down to 10⁻⁹ hPa. PI Ceramic GmbH reduced PICMA Stack lead times from 12 weeks to 4 weeks in March 2025, showing how suppliers are reshaping inventory and production models to support faster equipment ramp-ups.[1]PI Ceramic GmbH, “High-Performance Piezo Actuators for Extreme Applications With Fast Availability,” Physik Instrumente, physikinstrumente.com In the piezoelectric actuators and motors market, tighter supplier response times are pushing component makers deeper into OEM qualification cycles and creating longer commercial lock-in once a platform is approved.

Medical And Surgical Robotics Need For Non-Magnetic Silent Motion

MRI-guided robotics remains one of the clearest areas where the piezoelectric actuators and motors market benefits from non-magnetic, quiet, and compact motion systems. Tekceleo reported in July 2025 that a University College London cardiac catheterization robot powered by Wavelling series ultrasonic motors achieved a 100% procedural success rate in phantom testing and reduced trajectory deviation by 33.9% compared with the manual technique. That result matters because it ties silent piezo motion directly to clinical usability inside the MRI bore, where fluoroscopy alternatives raise radiation exposure. The same requirement is extending into robotic-assisted laparoscopy and high-content imaging, where electromagnetic drives introduce heat and electromagnetic interference that nearby sensors cannot tolerate. Across the piezoelectric actuators and motors market, FDA 510(k) and CE qualification steps also narrow the field of acceptable suppliers, which supports premium pricing for platforms with verified performance in medical settings.

Optical Alignment And Photonics Proliferation In Datacom And Imaging

Silicon photonics packaging is driving the piezoelectric actuators and motors market toward tighter alignment performance, as single-mode fiber coupling tolerances fall below the range of conventional pick-and-place accuracy. Physik Instrumente introduced the 6D NanoCube in January 2026 as a 6-DOF parallel-kinematic piezo alignment system that can find optical coupling peaks in under 1 second, with a minimum incremental motion of 50 nm and bidirectional repeatability of 40 nm. The launch matters beyond one product because it shows that motion control and process intelligence are being combined inside controller firmware rather than sold as separate layers. This reduces alignment cycle times in production and increases the value of suppliers that can deliver hardware, control software, and workflow tuning as a single package. In the piezoelectric actuators and motors market, photonics demand is shifting competition toward full-solution platforms rather than standalone motion components.

Miniaturized Consumer Camera And Sensing Modules

Consumer imaging remains a large-volume market for piezoelectric actuators and motors, as autofocus and optical image stabilization continue to favor compact ultrasonic and linear ultrasonic motion. Labs raised USD 21 million in October 2025 to scale production of its piezoMEMS platform for AI-enabled wearables, smartphones, and edge AI devices, and the company stated that it held more than 250 granted patents. XMEMS Demand is also broadening beyond smartphones as multi-camera arrays and time-of-flight sensing expand in automotive ADAS modules that need compact focus and alignment control. Xeryon’s XLA series sets the performance benchmark for compact systems, with rated speeds above 1,000 mm/s and maintenance-free travel exceeding 1,000 km. That volume pressure is forcing suppliers in the piezoelectric actuators and motors market to compete on controller integration, software, and packaging efficiency rather than only on core actuator specifications.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost Versus Electromagnetic and Voice-Coil Alternatives | -1.9% | Global, most acute in cost-sensitive industrial and consumer automation markets | Medium term (2-4 years) |

| Control Electronics and Integration Complexity | -1.0% | Global, higher impact in markets with lower systems integration capability | Medium term (2-4 years) |

| Lead-Free Material Performance Gap and Requalification Burden | -0.8% | Europe, with secondary impact in North America | Long term (≥ 4 years) |

| Wear, Drift, and Lifetime Validation in High-Duty Ultrasonic and Stick-Slip Systems | -0.5% | Global, concentrated in industrial automation and continuous-motion robotics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High System Cost Versus Electromagnetic And Voice-Coil Alternatives

System pricing remains the largest commercial barrier in the piezoelectric actuators and motors market because the total package includes the actuator, high-voltage amplifier, sensor, and controller. In many industrial use cases, the full system cost still runs 3 to 10 times above comparable electromagnetic servo options for similar force and displacement requirements. The gap is tied to specialized ceramic production, dedicated high-voltage electronics, and far lower manufacturing volumes than brushless DC motor platforms. In September 2025, PI introduced its Nanopositioning and Micropositioning Essentials range to offer shorter delivery times and volume savings for OEM buyers, which shows that suppliers are already trying to soften the price barrier through scale-oriented packaging. Even with those efforts, the piezoelectric actuators and motors market continues to see slower penetration in applications where millimeter-level accuracy is sufficient and lower-cost voice-coil or servo systems remain acceptable.

Control Electronics And Integration Complexity

Control complexity remains a practical limit on the piezoelectric actuators and motors market, as stack actuators often require drive voltages of 100 V to 1,000 V. That forces designers to use specialized amplifier circuits, larger thermal management allowances, and more demanding electromagnetic compatibility planning than standard motor driver ecosystems require. The issue becomes sharper in closed-loop systems, where settling performance and feedback accuracy push firmware and sensing requirements well beyond simple PID implementations. SmarAct’s MCS2 modular controller reflects the current industry response, with EtherCAT, USB, and Ethernet interfaces plus software libraries for Python, C/C++, and LabVIEW to reduce customer-side engineering effort.[2]SmarAct GmbH, “Catalog 2026,” SmarAct, smaract.com Still, until low-cost standardized high-voltage amplifier ICs become more common, integration effort will remain a meaningful drag on wider adoption across the piezoelectric actuators and motors market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Stack Actuators Anchor Revenue, Linear Motors Drive Next Growth

Stack actuators held 31.80% of the piezoelectric actuators and motors market share in 2025, and they kept that lead because force density and positioning resolution remain difficult to match in compact assemblies. Within the piezoelectric actuators and motors market, these devices are at the center of wafer-stage positioning, precision valve control in microfluidics, and fast-steering mirror actuation in beam-handling systems. Their role remains durable because the applications they support require force, speed, and accuracy simultaneously, not just one of those characteristics. Bender and unimorph actuators remain important in lower-cost ultrasonic cleaning and imaging transducer uses, while amplified and flexure types serve motion ranges that exceed the basic strain limit of bulk ceramics.

Shear and torsional devices continue to occupy smaller but high-value niches in scanning probe microscopy and atomic force microscopy, where unit pricing is supported by technical fit rather than shipment volume. Ultrasonic motors, specifically linear variants, are projected to grow at a 9.28% CAGR from 2026 to 2031, keeping product innovation active across the piezoelectric actuators and motors market. Xeryon’s planned 2026 integrated-controller release for the XLA-10, offering 10 N force in an 11.5 mm width, shows how smaller formats are widening use in portable diagnostics and compact imaging systems.[3]Xeryon, “Linear Piezo Actuators,” Xeryon, xeryon.com Inertia motors and piezo-walk systems still matter where long travel and very high resolution have to coexist, especially in electron microscopy stages and beamline optics. SmarAct’s SLC-1720, described as a closed-loop piezo stage at 22 × 17 × 8.5 mm with sub-nanometer resolution and 12 mm stroke, shows how space-limited OEM platforms are expanding the addressable range of these architectures.

By Operation Principle: Resonant Systems Hold Scale, Hybrid Designs Gain Relevance

Resonant and ultrasonic systems accounted for 46.47% share of the piezoelectric actuators and motors market size in 2025, reflecting their broad use in autofocus drives, surgical handpieces, and optical steering assemblies. Their lead comes from compact motor formats, silent operation, and power-off holding behavior that are well-suited to portable and medical devices. Quasi-static operation remains important where high force and very short travel are acceptable, especially in nanopositioning stages and precision valve actuation. In the piezoelectric actuators and motors market, the split between quasi-static and resonant modes is less about replacing one another and more about matching different motion envelopes.

Hybrid-mode systems are projected to grow at a 9.35% CAGR through 2031, and that pace reflects customers' desire for both longer travel and nanometer-level settling on the same platform. The piezoelectric actuators and motors industry is responding to that need by blending resonant and quasi-static behavior under software control, rather than forcing OEMs to choose one operating mode early in system design. Physik Instrumente’s 6D NanoCube, launched in January 2026, illustrates this direction with closed-loop piezo flexure drives and machine-learning-enhanced alignment routines that complete coupling tasks in under 1 second. SmarAct’s ISO 9001:2015-certified production setup, along with its dedicated motion, metrology, and automation units, demonstrates how suppliers are packaging modular platforms to simplify qualification for integrators. As a result, the piezoelectric actuators and motors market is moving toward software-defined motion behavior rather than strictly hardware-defined product categories.

By End-User Industry: Industrial Demand Holds Scale, Medical Demand Lifts Growth

Industrial and manufacturing accounted for 34.62% share of the piezoelectric actuators and motors market size in 2025, supported by sustained spending on precision automation, semiconductor tools, and micro-dispensing equipment. The largest installed base still comes from production settings where high repeatability improves yield or reduces waste at very small motion ranges. Advanced packaging has widened this role by integrating stack actuators into bonding-head force control and solder-paste micro-dispensing, not just wafer-stage positioning. Automotive demand also contributed in 2025 through the use of park assist sensing and fuel injection, while research laboratories continued to require vacuum-compatible stages down to 10⁻¹¹ mbar for quantum and synchrotron work.

The medical and life sciences segment is projected to grow at a 10.02% CAGR from 2026 to 2031, making it the fastest-growing end-user segment in the piezoelectric actuators and motors market. The piezoelectric actuators and motors industry is gaining from robotic-assisted surgery, high-content imaging, and microfluidic pumping, where non-magnetic motion and low heat output improve system compatibility. Tekceleo’s July 2025 report on the UCL cardiac catheterization robot, with 100% procedural success in phantom studies and a 33.9% reduction in trajectory deviation compared with the manual technique, provided hospital buyers with a concrete clinical reference point. Aerospace and defense buyers also continue to pay for vacuum-compatible, radiation-tolerant motion in fine-pointing and optical bench applications. The energy and power segment remains smaller, but hydrogen fuel cell balance-of-plant valve control is opening a practical growth path during the forecast period.

By Application: Nanopositioning Leads Revenue, Robotics Broadens Future Demand

Precision and nanopositioning held a 32.91% share of the piezoelectric actuators and motors market in 2025, and that leadership reflects the many core uses that still depend on ultra-fine motion accuracy. A visible shift inside this segment is the move from single-axis assemblies to parallel-kinematic platforms that reduce cumulative error during photonic alignment and similar tasks. Physik Instrumente’s P-616.65S NanoCube launch in December 2025 illustrated that trend with a 6-axis alignment system designed for photonic chip packaging and micro-optics assembly. Vibration and motion control, fluid handling, and imaging modules remain adjacent demand pockets because piezo bandwidth, seal-free pumping, and compact focus actuation each solve specific design constraints.

Robotics and micromanipulation are forecast to expand at a 9.97% CAGR from 2026 to 2031, providing the piezoelectric actuators and motors market with a broader path beyond traditional nanopositioning tools. The piezoelectric actuators and motors industry is seeing this shift in wafer handling, pharmaceutical pick-and-place, and surgical robotics, where compact grippers and stages must work without magnetic interference or bulky drive trains. SmarAct’s SG-series micro-grippers, with closed-loop gripping resolution down to 1 nm and gripping force up to 3.5 N in a 17 mm form factor, show the practical hardware now available for these tasks. Energy harvesting remains at an early stage, but work at CEA-Leti and Fraunhofer IKTS on lead-free MEMS harvesters and improved lead-free piezoceramics points to a broader application base over time. This makes applications one of the clearest areas where the piezoelectric actuators and motors market is widening its addressable base without losing its precision core.

Geography Analysis

Asia-Pacific held 40.75% of the piezoelectric actuators and motors market share in 2025, and that lead came from the region’s concentration of semiconductor fabs, consumer electronics OEMs, and precision manufacturing supply chains. China, Japan, South Korea, and Taiwan host much of the world’s advanced logic and memory capacity, creating a steady demand for stack actuators, ultrasonic motors, and nanopositioning systems used in lithography and inspection. That installed industrial base provides the piezoelectric actuators and motors market with a strong demand anchor in Asia-Pacific, even when conditions soften in individual downstream sectors. Japan’s supply chain remains especially deep because companies such as Murata, Kyocera, and TDK operate across materials, components, and finished systems. Kyocera’s February 2025 investment of EUR 5 million (USD 5.4 million), in TactoTek showed how regional suppliers are also extending piezo use into automotive haptics and connected-device interfaces.[4]Kyocera Corporation, “Kyocera Participates in TactoTek Funding With EUR 5 Million Investment and Strategic Partnership,” Kyocera Denmark, denmark.kyocera.com

North America and Europe formed the second-largest revenue bloc in 2025, supported by the concentration of precision instrument OEMs, defense contractors, and life science equipment makers. Germany remains a core design center for the piezoelectric actuators and motors market because it hosts Physik Instrumente, PI Ceramic, SmarAct, Piezosystem Jena, and Attocube within a tight engineering cluster. PI’s planned expansion into a new 140,000 sq ft production facility in Shrewsbury, Massachusetts, with a Fall 2025 target, reflected the broader reshoring push closer to semiconductor and photonics customers in North America. PI-USA France’s CEA-Leti and Germany’s Fraunhofer IKTS strengthen Europe’s position in lead-free piezo development by advancing KNN-based and related material work compatible with commercial VLSI processes.

The piezoelectric actuators and motors market in the Middle East is projected to expand at a 9.44% CAGR between 2026 and 2031. That pace is linked to public investment in precision manufacturing, defense modernization, and healthcare infrastructure under long-horizon national development programs. Israel stands out in this region because Nanomotion delivered a prototype positioning stage with 0.25 nm resolution and sub-1 nm stability for semiconductor metrology in 2025. Africa and South America remain early-stage markets, but wider localization of assembly and after-sales support should still support the gradual uptake of piezoelectric actuators and motors over the forecast period.

Competitive Landscape

A limited group of vertically integrated specialists, led by Physik Instrumente, Kyocera, and TDK, combines ceramics, actuator assembly, and system integration to improve qualification speed and value capture. The December 2025 HOERBIGER agreement to acquire Physik Instrumente was the clearest consolidation signal in the piezoelectric actuators and motors market during the review period. That transaction pairs PI’s precision motion depth with HOERBIGER’s distribution reach and financial capacity, raising the benchmark for suppliers that lack comparable global scale. It also suggests that larger industrial groups see precision piezo motion as a strategic platform rather than a narrow component category.

Mid-tier specialists such as SmarAct, Cedrat Technologies, New Scale Technologies, and Xeryon compete by offering deeper application fit and faster customization for OEM programs in the piezoelectric actuators and motors market. SmarAct’s controller and software ecosystem, which includes EtherCAT, USB, Ethernet, and SDK support for Python, C/C++, and LabVIEW, shows how ease of integration is becoming a competitive lever rather than only a technical feature. Xeryon’s compact linear ultrasonic actuator portfolio points to the same direction, where deployment speed and packaging efficiency carry more weight in customer decisions. These firms tend to win when customers need a precise fit for medical, analytical, or photonic systems and do not want to build motion control from the component level upward.

MEMS-based entrants are creating another competitive layer in the piezoelectric actuators and motors market by changing the cost structure and form-factor expectations for thin-film actuation. xMEMS raised USD 21 million in October 2025 to accelerate production of its piezoMEMS platform for AI-enabled consumer devices, signaling that investor support for alternative manufacturing models remains strong. Lead-free materials are another open field because CEA-Leti and Fraunhofer IKTS are advancing alternatives that narrow the performance gap with PZT in dynamic control use cases.[5]CEA-Leti, “Lead-Free Piezoelectric Materials,” CEA-Leti, cea.fr Taken together, these patterns describe a piezoelectric actuators and motors market where scale, software, materials, and application depth now shape competition as much as the actuator itself.

Piezoelectric Actuators And Motors Industry Leaders

Piezosystem Jena GmbH

Attocube Systems GmbH

Nanomotion Ltd.

Johnson Electric Holding Ltd.

Cedrat Technologies SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: HOERBIGER acquired Physik Instrumente, creating a new Positioning Division within HOERBIGER. The transaction preserves PI as a standalone operating unit while providing capital and distribution infrastructure for global scaling, pending regulatory approval.

- October 2025: xMEMS Labs closed a USD 21 million Series D funding round to scale production of its piezoMEMS platform, thin-film piezoelectric speakers, and micro-cooling chips for AI-enabled wearables, smartphones, and edge AI devices, backed by more than 250 granted patents.

- March 2025: Nanomotion delivered a prototype 0.25 nm-resolution positioning stage for semiconductor metrology, achieving sub-nanometer position stability below 1 nm for next-generation semiconductor inspection equipment.

- February 2025: Kyocera invested EUR 5 million (USD 5.45 million) in TactoTek's funding round and established a strategic partnership to advance HAPTIVITY i, in-mold structural electronics integrating piezoceramic actuators for haptic HMIs in automotive and connected-device applications.

Global Piezoelectric Actuators And Motors Market Report Scope

The Piezoelectric Actuators and Motors Market is Segmented by Product Type (Stack Actuators, Bender/Unimorph Actuators, Amplified/Flexure Actuators, Shear/Torsional Actuators, Ultrasonic Motors – Rotary, Ultrasonic Motors – Linear, Inertia (Stick-Slip) Motors, and Piezo-Walk / Step Motors), Operation Principle (Quasi-Static, Resonant/Ultrasonic, and Hybrid-Mode), End-User Industry (Industrial and Manufacturing, Automotive, Medical and Life Sciences, Aerospace and Defense, Consumer Electronics, Energy and Power, and Research and Academia), Application (Precision and Nanopositioning, Vibration and Motion Control, Fluid Handling and Valves, Imaging and Optics Focus, Robotics and Micromanipulation, and Energy-Harvesting Systems), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East, Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Stack Actuators |

| Bender/Unimorph Actuators |

| Amplified/Flexure Actuators |

| Shear/Torsional Actuators |

| Ultrasonic Motors - Rotary |

| Ultrasonic Motors - Linear |

| Inertia (Stick-Slip) Motors |

| Piezo-Walk / Step Motors |

| Quasi-Static (Direct) |

| Resonant / Ultrasonic |

| Hybrid-Mode |

| Industrial and Manufacturing |

| Automotive |

| Medical and Life Sciences |

| Aerospace and Defense |

| Consumer Electronics |

| Energy and Power |

| Research and Academia |

| Precision and Nanopositioning |

| Vibration and Motion Control |

| Fluid Handling and Valves |

| Imaging and Optics Focus |

| Robotics and Micromanipulation |

| Energy-Harvesting Systems |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Israel | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Product Type | Stack Actuators | |

| Bender/Unimorph Actuators | ||

| Amplified/Flexure Actuators | ||

| Shear/Torsional Actuators | ||

| Ultrasonic Motors - Rotary | ||

| Ultrasonic Motors - Linear | ||

| Inertia (Stick-Slip) Motors | ||

| Piezo-Walk / Step Motors | ||

| By Operation Principle | Quasi-Static (Direct) | |

| Resonant / Ultrasonic | ||

| Hybrid-Mode | ||

| By End-user Industry | Industrial and Manufacturing | |

| Automotive | ||

| Medical and Life Sciences | ||

| Aerospace and Defense | ||

| Consumer Electronics | ||

| Energy and Power | ||

| Research and Academia | ||

| By Application | Precision and Nanopositioning | |

| Vibration and Motion Control | ||

| Fluid Handling and Valves | ||

| Imaging and Optics Focus | ||

| Robotics and Micromanipulation | ||

| Energy-Harvesting Systems | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Israel | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the piezoelectric actuators and motors market?

The piezoelectric actuators and motors market stands at USD 21.32 billion in 2026 and is forecast to reach USD 32.97 billion by 2031 at a 9.11% CAGR.

Which product category leads revenue generation?

Stack actuators led product revenue with a 31.80% share in 2025 because they combine high force density with sub-nanometer motion control.

Which end-user group is growing the fastest?

Medical and life sciences is the fastest-growing end-user segment, with projected growth of 10.02% CAGR through 2031, supported by MRI-compatible robotics and imaging systems.

Why does Asia-Pacific lead global demand?

Asia-Pacific held 40.75% share in 2025 due to its concentration of semiconductor fabs, consumer electronics OEMs, and vertically integrated piezo supply chains.

What is the main adoption barrier for buyers?

The main barrier is total system cost, since a full piezo setup often includes the actuator, amplifier, position sensor, and controller, which can keep pricing above alternatives.

What recent competitive move matters most?

The December 2025 HOERBIGER agreement to acquire Physik Instrumente is the clearest strategic move because it combines precision motion expertise with wider distribution and capital support.

Page last updated on: