Lifescience Membrane Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

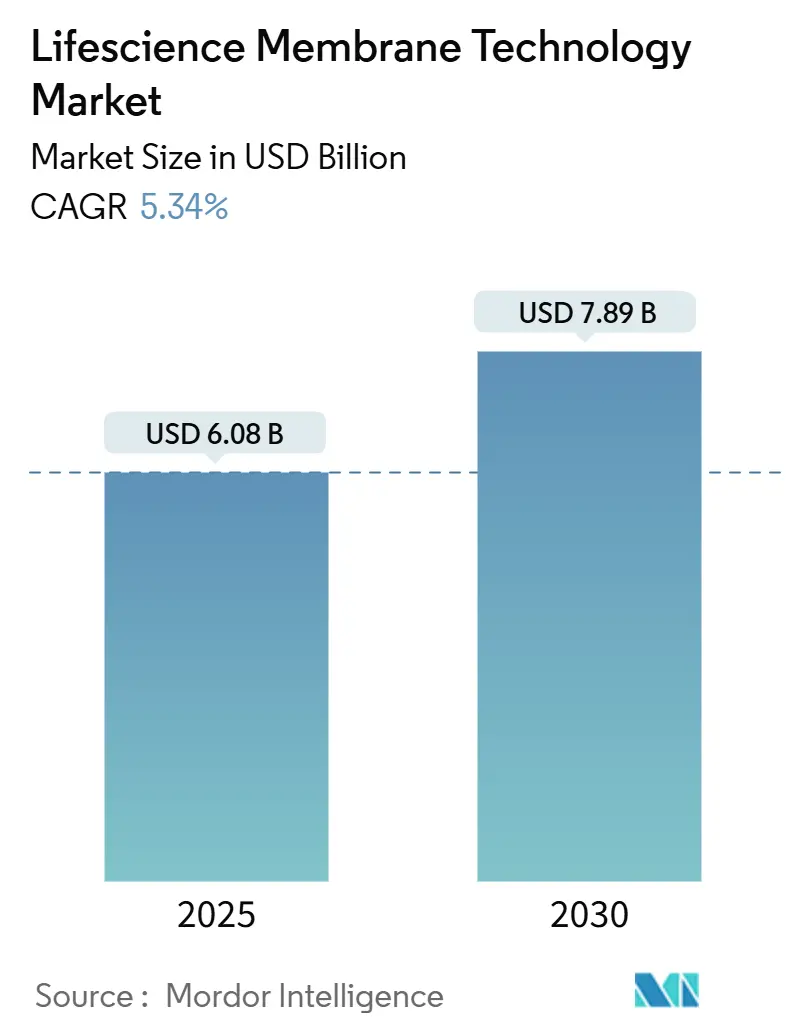

| Market Size (2025) | USD 6.08 Billion |

| Market Size (2030) | USD 7.89 Billion |

| Growth Rate (2025 - 2030) | 5.34% CAGR |

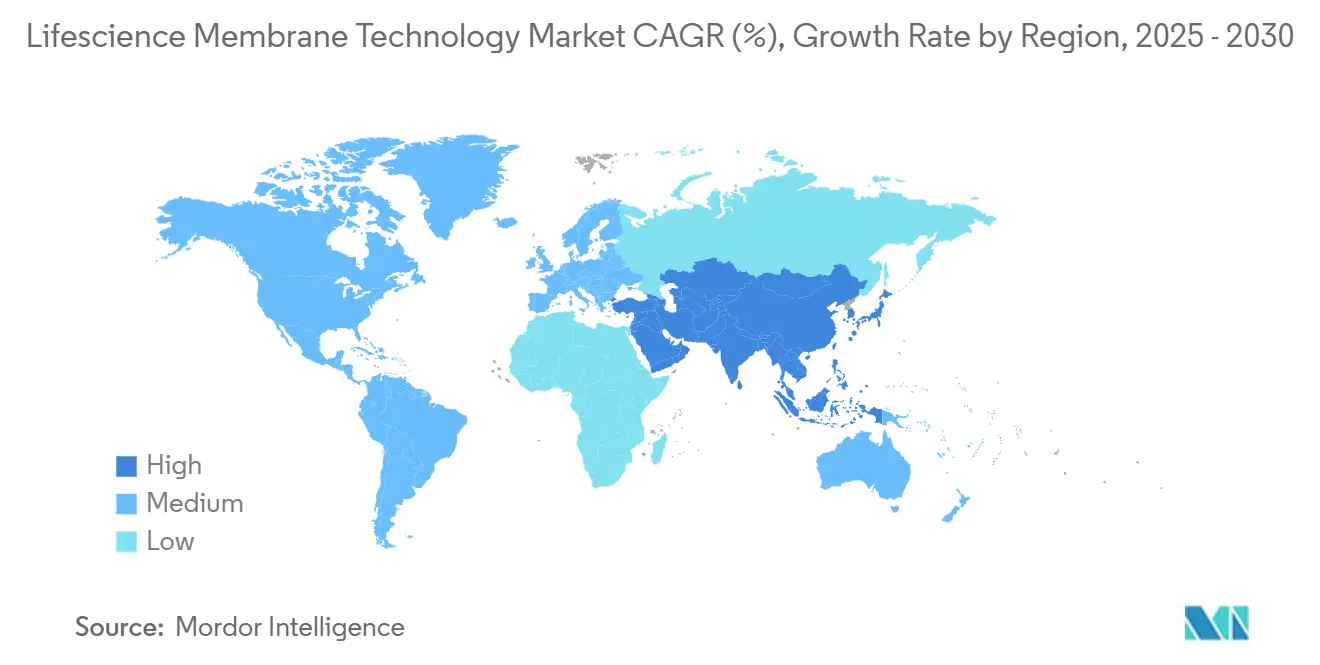

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Lifescience Membrane Technology Market Analysis by Mordor Intelligence

The lifescience membrane technology market size stood at USD 6.08 billion in 2025 and is on track to reach USD 7.89 billion by 2030, advancing at a 5.34% CAGR. The lifescience membrane technology market continues to benefit from rising biologics volumes, the move toward continuous processing, and stricter global purity standards that favor high-selectivity filtration. Consolidation among filtration specialists and bioprocess suppliers is accelerating, with large players absorbing niche innovators to secure end-to-end offerings. Rapid uptake of single-use assemblies shortens batch changeovers, while AI-driven membrane design unlocks higher flux without sacrificing integrity. Supply-chain constraints for PVDF and the impending PFAS phase-outs are nudging users toward ceramic or hybrid solutions, which promise longer service life and smaller environmental footprints.

Key Report Takeaways

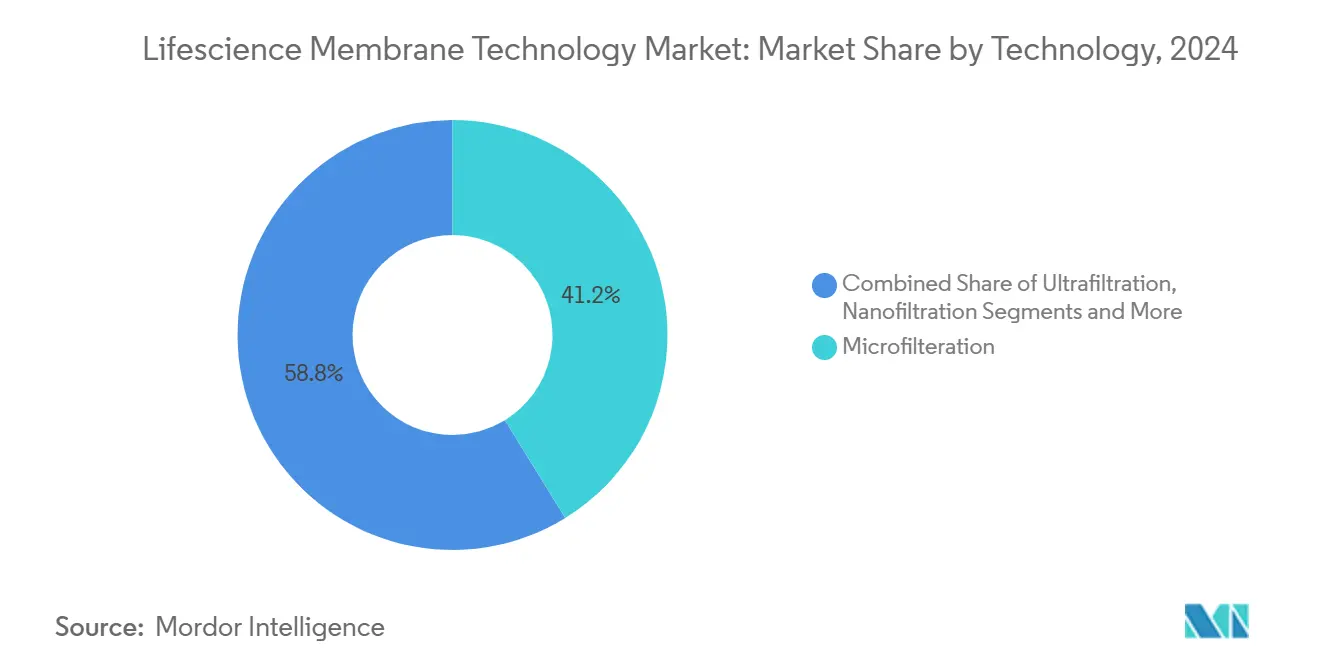

- By technology, microfiltration led with 41.22% of the lifescience membrane technology market share in 2024; nanofiltration is projected to grow at a 9.36% CAGR through 2030.

- By material, polymeric membranes accounted for 81.44% share of the lifescience membrane technology market size in 2024, whereas ceramic membranes are expected to expand at 8.47% CAGR.

- By application, pharmaceutical manufacturing captured 37.42% share of the lifescience membrane technology market size in 2024, and cell & gene therapy is forecast to post a 9.66% CAGR by 2030.

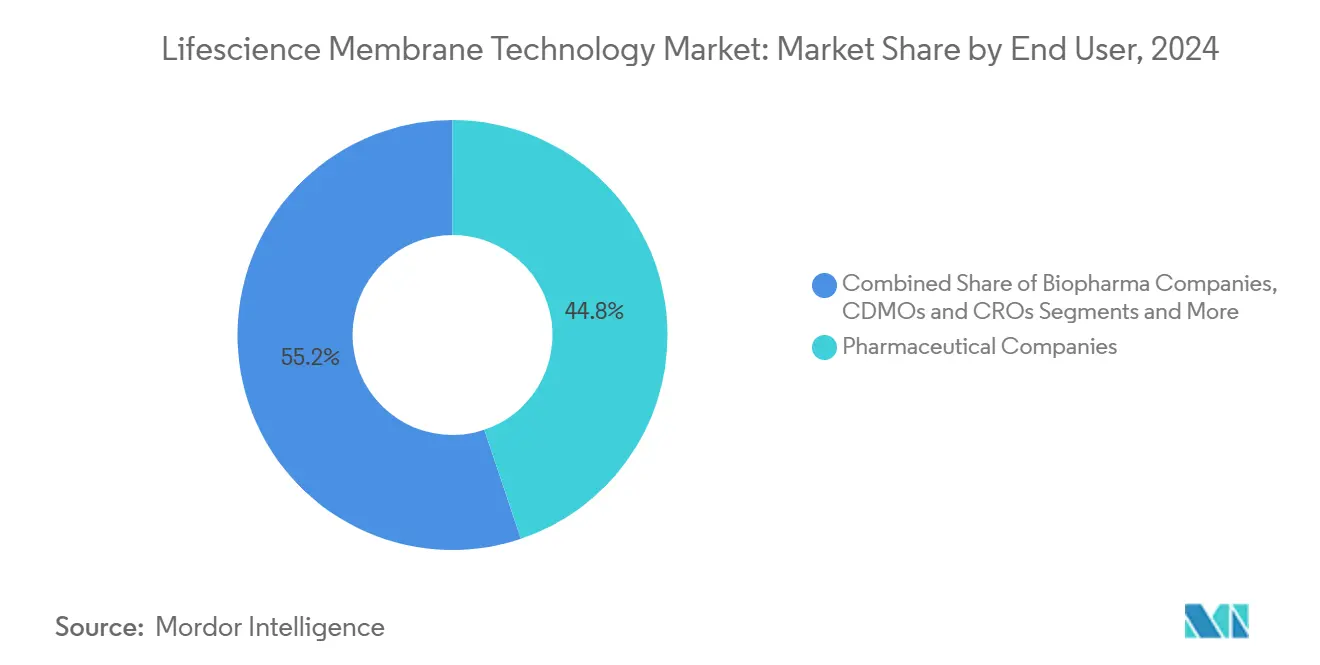

- By end user, pharmaceutical companies held 44.84% share of the lifescience membrane technology market size in 2024, while CDMOs & CROs are set to advance at 9.03% CAGR.

- By product type, membrane filters controlled 51.49% of the lifescience membrane technology market share in 2024; single-use TFF systems exhibit the fastest pace at 8.25% CAGR.

- By geography, North America commanded 33.58% of lifescience membrane technology market share in 2024, while Asia-Pacific records the strongest 7.67% CAGR outlook.

Global Lifescience Membrane Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing biopharma production volumes | +1.2% | Global, concentrated in North America & Europe | Medium term (2-4 years) |

| Stringent purity regulations in drug manufacturing | +0.8% | Global, led by FDA and EMA jurisdictions | Short term (≤ 2 years) |

| Surge in single-use bioprocessing platforms | +0.9% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Rising R&D in cell & gene therapy | +1.1% | North America core, spill-over to EU and APAC | Long term (≥ 4 years) |

| AI-optimized custom membrane design | +0.6% | North America & EU, early adoption in China | Long term (≥ 4 years) |

| Localized “factory-in-a-box” drug production | +0.4% | Global, with emphasis on emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Biopharma Production Volumes

Large-scale biologics plants are multiplying, pushing the lifescience membrane technology market toward higher-capacity modules that can withstand dense cell cultures while preserving product quality. Fujifilm’s USD 1.2 billion expansion in North Carolina, adding 160,000 L of bioreactor space, captures the scale of new capacity coming online.[1]Fujifilm Corporation, “Fujifilm to Invest Additional $1.2 Billion to Expand its Large-Scale Cell Culture CDMO Business in North Carolina,” fujifilm.com The swing from batch to perfusion culture intensifies requirements for membranes that combine durability with constant flux. Suppliers that document robust performance under high cell-density conditions secure preferred-vendor status, especially when they bundle integrity-testing software for cGMP audits. As a result, microfiltration and ultrafiltration lines designed for continuous harvest are overtaking legacy cartridge filters in new installations.

Stringent Purity Regulations in Drug Manufacturing

FDA, EMA, and other agencies are tightening viral-clearance and endotoxin limits, pushing manufacturers to adopt multi-layer stacks with documented log-reduction values exceeding historical norms. Parallel U.S. EPA rules add disposal obligations for hazardous waste pharmaceuticals, forcing plants to rethink cleaning validation strategies.[2]Association for the Health Care Environment, “EPA Addresses Challenges in Managing Hazardous Waste Pharmaceuticals,” ahe.orgVendors that embed automated integrity testing and generate compliant electronic batch records gain an edge, because they cut audit prep time and limit manual interventions. Heightened scrutiny also drives interest in disposable virus filters such as Asahi Kasei’s Planova FG1, whose seven-fold flux boost shortens batch times without raising breakthrough risk.[3]Asahi Kasei Medical, “Asahi Kasei Medical Launches Planova™ FG1 Next-Generation Virus Removal Filter,” asahi-kasei.com

Surge in Single-Use Bioprocessing Platforms

CDMOs favor single-use trains for fast tech transfers and minimal cross-contamination, making high-surface-area capsules and pre-sterilized TFF cassettes standard in new suites. Danaher’s USD 1.5 billion capacity build for Cytiva and Pall underlines how single-use demand guides capital allocation. For the lifescience membrane technology market, this shift rewards suppliers that can ship gamma-irradiated assemblies complete with fully validated flow paths. Integrated sensor arrays and auto-tune valves further reduce operator exposure and accelerate batch release.

Rising R&D in Cell & Gene Therapy

Gene-modifying modalities exact tight specifications on shear stress and temperature, steering buyers toward gentle hollow-fiber modules that preserve viral vector integrity. High-throughput screenings show that optimized filtration steps raise AAV recovery yields, pushing their economic break-even earlier in clinical pipelines. Suppliers with configurable surface chemistries that minimize non-specific binding can charge premium pricing. Accelerated approvals for ex vivo gene therapies keep the order book full through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Membrane fouling & short service life | -0.7% | Global, notably high-density processes | Short term (≤ 2 years) |

| High capital cost of advanced systems | -0.5% | Global, stronger in emerging markets | Medium term (2-4 years) |

| Shortage of high-grade polymer precursors | -0.4% | Global supply chains, centered in Asia-Pacific | Short term (≤ 2 years) |

| Unclear rules on membrane waste disposal | -0.3% | EU and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Membrane Fouling & Short Service Life

Protein build-up and cell debris quickly raise trans-membrane pressure, shortening run times and inflating replacement budgets. A 2024 study on alternating tangential flow showed pressure spikes despite maintaining 88% protein transmission, proving the economic drag of fouling. Coatings that resist hydrophobic adsorption plus back-flush-friendly module geometries are under rapid development, yet no universal fix exists. Facilities hedge by ordering surplus filter sets, elevating inventory spend.

High Capital Cost of Advanced Systems

A fully automated, analytics-ready filtration skid can top USD 1 million, a hurdle for start-ups and emerging-market manufacturers. Leasing models and performance-based contracts partially ease adoption but have yet to dominate purchasing habits. Vendors that modularize designs into upgradable nodes reduce perceived obsolescence risk, shrinking payback periods.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Microfiltration Dominance Faces Nanofiltration Disruption

Microfiltration secured 41.22% lifescience membrane technology market share in 2024, owing to its entrenched role in cell harvest and clarification. Demand stays resilient as perfusion culture scales, yet nanofiltration, with a 9.36% CAGR outlook, positions itself as the go-to for high-resolution viral clearance and solvent exchange. The lifescience membrane technology market size for nanofiltration will likely triple by 2030 as plants retrofit downstream lines to meet Annex 1 viral safety clauses. Ultrafiltration remains the workhorse for protein concentration, whereas reverse osmosis serves a niche for water-for-injection (WFI) and solvent recycling. Asahi Kasei’s WFI membrane system showcases energy savings over thermal distillation, signaling room for innovation even in mature categories.

Providers now ship hybrid skids that stack micro-, ultra-, and nanofiltration in sequence, shrinking footprint and cutting cleanroom HVAC loads. Chromatography or affinity membranes augment such stacks, capturing specific impurities inline. Early adopters report 15% shorter campaign cycles, stirring broader interest. The advance of electrodialysis and ion-exchange membranes stays subdued because of their power draws, though they retain value in solvent-intensive API plants.

By Material: Polymeric Leadership Challenged by Ceramic Innovation

Polymeric substrates captured 81.44% of lifescience membrane technology market size in 2024 due to low cost and proven scalability. Yet ceramic variants post an 8.47% CAGR, riding PFAS backlash and offering chemical resilience for aggressive cleaning regimens. Mixed-matrix designs blending inorganic fillers into polymer backbones attempt to deliver the best of both, but complex fabrication hampers mass rollout. Sustainability drivers now influence purchasing, with buyers rewarding solvent-free casting and recyclable frames. The lifescience membrane technology market is witnessing pilot lots of bio-based membranes; performance parity remains a hurdle but regulatory incentives could tilt the field after 2028.

Longer service life offsets ceramics’ premium, especially in continuous-manufacturing suites that avoid scheduled shutdowns. Vendors tout total-cost-of-ownership calculators to demonstrate savings. Users balancing CapEx limits with new PFAS liability hesitate, leaving scope for dual-sourcing strategies that keep polymeric lines for low-risk buffers and ceramics for harsh CIP zones.

By Application: Pharmaceutical Manufacturing Leads While Cell & Gene Therapy Surges

Pharmaceutical manufacturing retained 37.42% of lifescience membrane technology market size in 2024 as membranes permeate nearly every unit operation from media prep to final fill. Meanwhile, cell & gene therapy displays a 9.66% CAGR, requiring bespoke hollow-fiber configurations to safeguard viral particle integrity. Diagnostics and life-science research segments grow steadily as labs proliferate in emerging economies, but command lower unit prices. Dialysis membranes remain steady through demographic aging, yet price competition caps revenue upside.

Continuous-processing units merge reaction and purification, placing membranes center-stage. Factory-in-a-box concepts rely on compact, multi-task modules to maintain sterility across local climates. Such architectures enlarge addressable demand in markets previously constrained by infrastructure deficits, lifting overall lifescience membrane technology market growth.

By End User: Pharmaceutical Companies Dominate as CDMOs Accelerate

Pharmaceutical companies controlled 44.84% market share in 2024, sustained by vertically integrated biologics pipelines. CDMOs & CROs clock the highest 9.03% CAGR as outsourcing becomes mainstream for specialized modalities. Academic and research institutes catalyze early innovation, often partnering with CDMOs to scale proof-of-concept batches. Hospitals and clinical labs represent a budding niche, leveraging point-of-care compounding units fitted with disposable micro-filters.

Collaborative models proliferate: Sartorius and LFB BIOMANUFACTURING aligned to speed cell-line development using high-throughput membrane analytics, exemplifying cross-entity synergies that compress development timelines. Such arrangements distribute technology risk while widening market access for membrane vendors.

By Product Type: Membrane Filters Lead While Single-Use TFF Systems Gain Momentum

Membrane filters represented 51.49% lifescience membrane technology market share in 2024, led by flat-sheet and disc forms integral to lab-scale tasks. Single-use TFF modules grow at 8.25% CAGR, driven by gene therapy expansions and the desire to skip steam-in-place cycles. Capsule and cartridge formats thrive in pilot plants, whereas hollow-fiber modules dominate commercial biologics lines for their surface-area efficiency. Repligen’s automated TFF skid shows how embedded analytics cut manual oversight and enhance consistency.

Transfer and blotting membranes serve diagnostic kits and Western blots; revenue growth remains flat but stable. Smart modules that pair filtration with inline spectrophotometry hint at future value-add paths, elevating barriers for commodity entrants and sustaining premium pricing in the lifescience membrane technology industry.

Geography Analysis

North America held 33.58% of lifescience membrane technology market share in 2024, underpinned by dense biotech clusters, generous federal grants, and fast regulatory turnaround. Investors favor domestic manufacturing to de-risk supply, as illustrated by Johnson & Johnson’s USD 2 billion biologics facility in North Carolina slated to create 420 jobs. Continuous-manufacturing pilots gain traction thanks to accessible automation suppliers and established cold-chain networks.

Asia-Pacific logs the fastest 7.67% CAGR, propelled by national policies that promote vaccine sovereignty and biopharma clusters. China funnels subsidies toward single-use lines, while South Korea lures multinationals with tax breaks, evidenced by MilliporeSigma’s USD 300 million plant in Daejeon. Local production of base polymers and ceramics helps temper cost volatility, further lifting the lifescience membrane technology market penetration.

Europe maintains steady demand through 2030, championed by a robust regulatory framework and strong sustainability mandates that favor low-carbon ceramics. Government incentives for PFAS replacement accelerate the swap-out cycle, padding revenue for vendors able to validate new materials swiftly. Smaller regions—Middle East & Africa and South America—show emerging interest; uptake is tempered by limited GMP infrastructure and currency fluctuations, but turnkey pod solutions promise to bridge gaps, especially for domestic vaccine fill-finish.

Competitive Landscape

The lifescience membrane technology market is moderately consolidated. Strategic acquisitions mark the period, notably Thermo Fisher’s USD 4.1 billion purchase of Solventum’s filtration arm to widen its biologics toolkit. Merck KGaA, Danaher, and Sartorius leverage vertical integration to offer membranes, housings, sensors, and data-analytics suites under single contracts.

Digital twins, predictive maintenance, and AI-driven membrane tailoring emerge as differentiation levers. Smaller innovators specializing in ceramic or hybrid matrices attract partnerships for accelerated market entry. Meanwhile, supply-side risk around PVDF pushes large buyers to dual-source between polymeric and ceramic offerings, broadening the supplier mix yet rewarding those with global manufacturing footprints and robust quality records.

Patent filings in gradient pore structures and solvent-free casting processes rose 18% during 2024, signaling continued R&D investment. Start-ups focusing on recyclable or bio-based membranes chase sustainable-procurement budgets, though they must qualify performance under real-world multiproduct regimes to gain share. Overall, pricing power rests with suppliers who couple superior flux with exhaustive regulatory support.

Lifescience Membrane Technology Industry Leaders

Merck KGaA

Danaher

Sartorius AG

Thermo Fisher Scientific

Asahi Kasei Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Asahi Kasei Life Science Corp. began operating independently, scaling Planova virus-filter capacity in the U.S. and Japan while broadening contract R&D capabilities.

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s Purification & Filtration business for USD 4.1 billion, aiming to close by year-end.

- October 2024: Asahi Kasei Medical released Planova FG1, offering seven-times higher flux than the BioEX predecessor for faster biotherapeutic filtration.

Global Lifescience Membrane Technology Market Report Scope

| Microfiltration |

| Ultrafiltration |

| Nanofiltration |

| Reverse Osmosis |

| Chromatography & Affinity Membranes |

| Electrodialysis & Ion Exchange |

| Polymeric |

| Ceramic |

| Mixed-matrix / Hybrid |

| Pharmaceutical Manufacturing |

| Bioprocessing & Biologics |

| Medical Devices & Dialysis |

| Diagnostics & Life-science Research |

| Laboratory Water Purification |

| Biopharma Companies |

| Pharmaceutical Companies |

| CDMOs & CROs |

| Academic & Research Institutes |

| Hospitals & Clinical Labs |

| Membrane Filters (flat-sheet, disc) |

| Capsule / Cartridge Filters |

| Hollow-Fiber Modules |

| Single-use TFF Systems |

| Transfer / Blotting Membranes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Microfiltration | |

| Ultrafiltration | ||

| Nanofiltration | ||

| Reverse Osmosis | ||

| Chromatography & Affinity Membranes | ||

| Electrodialysis & Ion Exchange | ||

| By Material | Polymeric | |

| Ceramic | ||

| Mixed-matrix / Hybrid | ||

| By Application | Pharmaceutical Manufacturing | |

| Bioprocessing & Biologics | ||

| Medical Devices & Dialysis | ||

| Diagnostics & Life-science Research | ||

| Laboratory Water Purification | ||

| By End-user | Biopharma Companies | |

| Pharmaceutical Companies | ||

| CDMOs & CROs | ||

| Academic & Research Institutes | ||

| Hospitals & Clinical Labs | ||

| By Product Type | Membrane Filters (flat-sheet, disc) | |

| Capsule / Cartridge Filters | ||

| Hollow-Fiber Modules | ||

| Single-use TFF Systems | ||

| Transfer / Blotting Membranes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the lifescience membrane technology market?

The market was valued at USD 6.08 billion in 2025 and is forecast to reach USD 7.89 billion by 2030.

Which technology segment leads revenue?

Microfiltration remains the largest, contributing 41.22% of 2024 revenue.

Which region is growing the fastest?

Asia-Pacific is projected to post a 7.67% CAGR through 2030.

Why are single-use TFF systems gaining popularity?

They eliminate cleaning validation, reduce cross-contamination risk, and align with flexible manufacturing needs.

How will PFAS regulations influence membrane materials?

Restrictions on PVDF drive interest in ceramic and hybrid membranes that avoid fluorinated polymers.

Which end-user segment shows the highest growth?

CDMOs & CROs exhibit a 9.03% CAGR as outsourcing of biologics production expands.

Page last updated on: